Exhibit (c)(1)

PRELIMINARY BACKGROUND MATERIALS Project Panda Presentation to the Special Committee of the Board of Directors June 18, 2022

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 13E-3

RULE 13E-3 TRANSACTION STATEMENT UNDER SECTION 13(E)

OF THE SECURITIES ACT OF 1934

PZENA INVESTMENT MANAGEMENT, INC.

(Name of the Issuer)

Pzena Investment Management, Inc.

Pzena Investment Management, LLC

Panda Merger Sub, LLC

(Names of Persons Filing Statement)

Class A Common Stock, par value $0.01 per share

(Title of Class of Securities)

74731Q103

(CUSIP Number of Class of Securities)

| Joan Berger | Richard S. Pzena | |

| Pzena Investment Management, Inc. | Pzena Investment Management, LLC | |

| 320 Park Avenue, 8th Floor | 320 Park Avenue, 8th Floor | |

| New York, NY 10022 | New York, NY 10022 | |

| (212) 355-1600 | (212) 355-1600 |

(Name, Address, and Telephone Numbers of Person Authorized to Receive Notices and Communications on Behalf of the Persons Filing Statement)

With copies to

| Andrew J. Nussbaum Nicholas G. Demmo |

Scott Golenbock Milbank LLP | |

| Wachtell, Lipton, Rosen & Katz | 55 Hudson Yards | |

| 51 West 52nd Street | New York, NY 10011-2163 | |

| New York, NY 10019 | (212) 553-5000 | |

| (212) 403-1000 |

This statement is filed in connection with (check the appropriate box):

| a. | ☒ | The filing of solicitation materials or an information statement subject to Regulation 14A, Regulation 14C or Rule 13e-3(c) under the Securities Exchange Act of 1934. | ||

| b. | ☐ | The filing of a registration statement under the Securities Act of 1933. | ||

| c. | ☐ | A tender offer. | ||

| d. | ☐ | None of the above. | ||

Check the following box if the soliciting materials or information statement referred to in checking box (a) are preliminary copies: ☒

Introduction

This Transaction Statement on Schedule 13E-3 (which we refer to as this “Transaction Statement”) is being filed with the U.S. Securities and Exchange Commission (which we refer to as the “SEC”) pursuant to Section 13(e) of the Securities Exchange Act of 1934, as amended (which we refer to, together with the rules and regulations promulgated thereunder, as the “Exchange Act”), by (1) Pzena Investment Management, Inc., a Delaware corporation (which we refer to as “PZN” or the “Company”); (2) Pzena Investment Management, LLC, a Delaware limited liability company (which we refer to as “PIM, LLC”); and (3) Panda Merger Sub, LLC , a Delaware limited liability company and a wholly owned subsidiary of PIM, LLC (which we refer to as “Merger Sub”). The persons filing this Transaction Statement are collectively referred to as the “Filing Persons”.

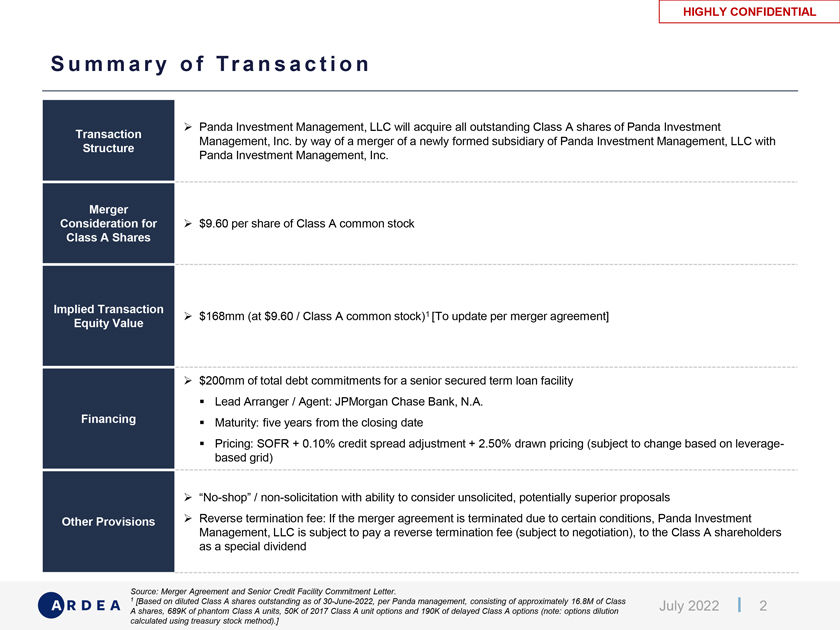

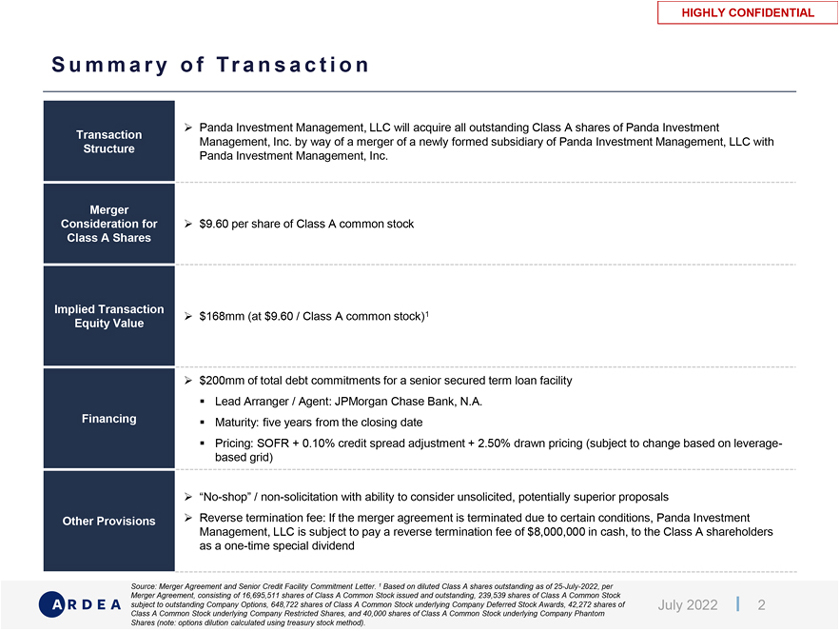

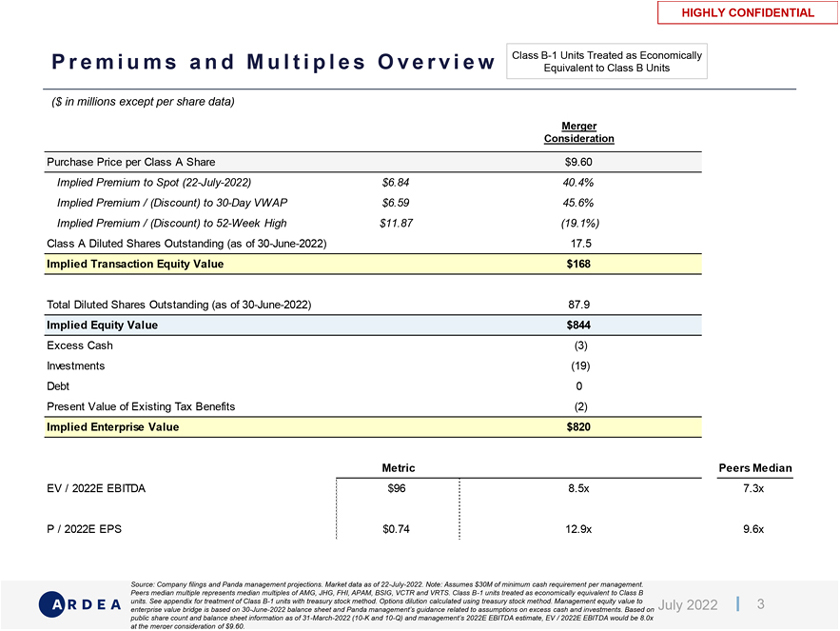

This Transaction Statement relates to the Agreement and Plan of Merger, dated as of July 26, 2022 (which we refer to, as it may be amended from time to time, as the “merger agreement”), by and among the Company, PIM, LLC and Merger Sub. If the merger agreement is adopted by the Company’s stockholders and the other conditions under the merger agreement are either satisfied or waived, the Company will be merged with and into Merger Sub (which we refer to as the “merger”), with Merger Sub surviving the merger as a wholly owned subsidiary of PIM, LLC. At the effective time of the merger, (1) each outstanding share of Class A common stock, par value $0.01 per share, of the Company (which we refer to as “PZN Class A common stock”) (other than (x) shares PZN Class A common stock that are to be cancelled in accordance with the merger agreement and (y) shares of PZN Class A common stock that are owned by stockholders of the Company who did not vote in favor of the adoption of the merger agreement and who have perfected and have not withdrawn a demand for appraisal rights pursuant to Section 262 of the DGCL) will be converted into the right to receive $9.60 in cash per share, without interest (which we refer to as the “merger consideration”) and (2) each outstanding share of Class B common stock, par value $0.000001 per share, of the Company (which we refer to as “PZN Class B common stock”) will be automatically cancelled and the holders thereof will not receive the merger consideration. Following the completion of the merger, the PZN Class A common stock will be delisted from the New York Stock Exchange, will be deregistered under the Exchange Act and will cease to be publicly traded.

The board of directors of the Company (which we refer to as the “Board”) formed a special committee (which we refer to as the “Special Committee”) consisting solely of independent and disinterested directors to, among other things, evaluate the merger. After reviewing the terms of the merger agreement with its independent legal and financial advisors, the Special Committee unanimously determined that the transactions contemplated by the merger agreement, including the merger, are fair to and in the best interests of the Company and the holders of PZN Class A common stock, and unanimously recommended that the Board approve the merger agreement and that the Company’s stockholders vote for the adoption of the merger agreement.

Based on the Special Committee’s recommendation, the Board (other than five directors who recused themselves due to their affiliation with PIM, LLC and/or their interests in the transaction) has determined that the transactions contemplated by the merger agreement, including the merger, are fair to and in the best interests of the Company and the holders of PZN Class A common stock; has approved and declared advisable the merger agreement and transactions contemplated thereby; and has recommended that the Company’s stockholders vote for the adoption of the merger agreement and for the other proposals described in the Proxy Statement (as defined below).

The merger cannot be completed unless both (1) the holders of a majority of the total number of votes of Company common stock outstanding and (2) the holders of a majority of the outstanding shares of PZN Class A common stock not owned, directly or indirectly, by PIM, LLC, Merger Sub or any holder of PZN Class B common stock vote in favor of the adoption of the merger agreement.

Concurrently with the filing of this Transaction Statement, the Company is filing a proxy statement (which we refer to as the “Proxy Statement”) under Regulation 14A of the Exchange Act with the SEC, pursuant to which the Company is soliciting proxies from stockholders of the Company in connection with the merger. The Proxy Statement is attached hereto as Exhibit (a)(1). A copy of the merger agreement is attached to the Proxy Statement as Annex A and is incorporated herein by reference. As of the date hereof, the Proxy Statement is in preliminary form, and is subject to completion or amendment. Terms used but not defined in this Transaction Statement have the meanings assigned to them in the Proxy Statement.

Pursuant to General Instruction F to Schedule 13E-3, the information in the Proxy Statement, including all annexes thereto, is expressly incorporated by reference herein in its entirety, and responses to each item herein are qualified in their entirety by the information contained in the Proxy Statement. The cross-references below are being supplied pursuant to General Instruction G to Schedule 13E-3 and show the location in the Proxy Statement of the information required to be included in response to the items of Schedule 13E-3.

While each of the Filing Persons acknowledges that the merger is a going private transaction for purposes of Rule 13e-3 under the Exchange Act, the filing of this Transaction Statement shall not be construed as an admission by any Filing Person, or by any affiliate of a Filing Person, that the Company is “controlled” by any of the Filing Persons and/or their respective affiliates.

All information contained in, or incorporated by reference into, this Transaction Statement concerning each Filing Person has been supplied by such Filing Person.

Item 1. Summary Term Sheet (Regulation M-A Item 1001)

The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

Item 2. Subject Company Information (Regulation M-A Item 1002)

(a) Name and address. The Company’s name, and the address and telephone number of its principal executive offices are:

Pzena Investment Management, Inc.

320 Park Avenue, 8th Floor

New York, New York 10022

(212) 355-1600

(b) Securities. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Questions and Answers About the Special Meeting and the Merger—How many votes do I have?”

“The Special Meeting—Record Date and Quorum”

(c) Trading market and price. The information set forth in the Proxy Statement under the following caption is incorporated herein by reference:

“Other Important Information Regarding the Company—Market Price of Class A Common Stock and Dividends”

(d) Dividends. The information set forth in the Proxy Statement under the following caption is incorporated herein by reference:

“Other Important Information Regarding the Company—Market Price of Class A Common Stock and Dividends”

(e) Prior public offerings. Not applicable.

2

(f) Prior stock purchases. The information set forth in the Proxy Statement under the following caption is incorporated herein by reference:

“Other Important Information Regarding the Company—Certain Transactions in the Shares of Common Stock”

Item 3. Identity and Background of Filing Person (Regulation M-A Item 1003)

(a) – (b) Name and Address of Each Filing Person; Business and Background of Entities. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet—Parties to the Merger”

“Parties to the Merger”

“Other Important Information Regarding the Company—Directors and Executive Officers of the Company”

“Other Important Information Regarding PIM, LLC”

“Where You Can Find More Information”

(c) Business and Background of Natural Persons. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Other Important Information Regarding the Company—Directors and Executive Officers of the Company”

“Other Important Information Regarding PIM, LLC”

“Where You Can Find More Information”

Item 4. Terms of the Transaction (Regulation M-A Item 1004)

(a) Material terms.

(1) Tender offer. Not applicable

(2) Merger or Similar Transactions.

(i) The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Effective Time of the Merger”

“Special Factors—Payment of Merger Consideration”

“The Merger Agreement—Closing and Effective Time of the Merger”

“The Merger Agreement—Treatment of Common Stock and Company Equity Awards”

“The Merger Agreement—Conditions to the Merger”

(ii) The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

3

“Special Factors—Certain Effects of the Merger”

“Special Factors—Payment of Merger Consideration”

“The Merger Agreement—Treatment of Common Stock and Company Equity Awards”

(iii) The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Special Factors—Reasons for the Merger; Recommendation of the Special Committee and the Board; Fairness of the Merger”

“Special Factors—Position of PIM, LLC as to the Fairness of the Merger”

“Special Factors—Purpose and Reasons of PIM, LLC for the Merger”

“Special Factors—Plans for the Company After the Merger”

“Special Factors—Opinion of Ardea Partners LP”

“Special Factors—Opinion of CastleOak Securities, L.P.”

“Special Factors—Unaudited Prospective Financial Information of the Company”

(iv) The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Questions and Answers About the Special Meeting and the Merger”

“The Merger Agreement—Stockholders Meeting”

“The Special Meeting—Vote Required”

“The Special Meeting—Management Stockholders’ Obligation to Vote in Favor of the Merger”

(v) The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Interests of Executive Officers and Directors of the Company in the Merger”

(vi) The information set forth in the Proxy Statement under the following caption is incorporated herein by reference:

“Special Factors—Accounting Treatment”

(vii) The information set forth in the Proxy Statement under the following caption is incorporated herein by reference:

“Special Factors—Material U.S. Federal Income Tax Consequences of the Merger”

(c) Different terms. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Interests of Executive Officers and Directors of the Company in the Merger”

“The Merger Agreement—Treatment of Common Stock and Company Equity Awards”

“The Voting Agreement”

4

(d) Appraisal rights. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Appraisal Rights”

(e) Provisions for unaffiliated security holders. The information set forth in the Proxy Statement under the following caption is incorporated herein by reference:

“Special Factors—Provisions for Unaffiliated Stockholders”

(f) Eligibility for listing or trading. Not applicable.

Item 5. Past Contacts, Transactions, Negotiations and Agreements (Regulation M-A Item 1005)

(a)(1) – (2) Transactions. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Special Factors—Background of the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Interests of Executive Officers and Directors of the Company in the Merger”

“The Merger Agreement—Treatment of Common Stock and Company Equity Awards”

“Other Important Information Regarding the Company—Certain Transactions in the Shares of Common Stock”

“The Voting Agreement”

(b) – (c) Significant corporate events; Negotiations or contacts. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Special Factors—Background of the Merger”

“Special Factors—Reasons for the Merger; Recommendation of the Special Committee and the Board; Fairness of the Merger”

“Special Factors—Position of PIM, LLC as to the Fairness of the Merger”

“Special Factors—Purpose and Reasons of PIM, LLC for the Merger”

“Special Factors—Interests of Executive Officers and Directors of the Company in the Merger”

“Special Factors—Financing of the Merger”

“The Merger Agreement”

“The Voting Agreement”

Annex A—Agreement and Plan of Merger

Annex E—Voting Agreement

(e) Agreements involving the subject company’s securities. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

5

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Plans for the Company After the Merger”

“Special Factors—Financing of the Merger”

“The Merger Agreement”

“The Voting Agreement”

“The Special Meeting—Vote Required”

“The Special Meeting—Management Stockholders’ Obligation to Vote in Favor of the Merger”

“Other Important Information Regarding the Company—Certain Transactions in the Shares of Common Stock”

Annex A—Agreement and Plan of Merger

Annex E—Voting Agreement

Item 6. Purposes of the Transaction, and Plans or Proposals (Regulation M-A Item 1006)

(b) Use of securities acquired. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Plans for the Company After the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Certain Effects of the Merger for PIM, LLC”

“Special Factors—Certain Effects on the Company if the Merger Is Not Completed”

“Special Factors—Payment of Merger Consideration”

“The Merger Agreement—Treatment of Common Stock and Company Equity Awards”

“Delisting and Deregistration of Common Stock”

(c)(1) – (8) Plans. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Reasons for the Merger; Recommendation of the Special Committee and the Board; Fairness of the Merger”

“Special Factors—Position of PIM, LLC as to the Fairness of the Merger”

“Special Factors—Purpose and Reasons of PIM, LLC for the Merger”

“Special Factors—Plans for the Company After the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Certain Effects of the Merger for PIM, LLC”

“Special Factors—Certain Effects on the Company if the Merger Is Not Completed”

6

“Special Factors—Interests of Executive Officers and Directors of the Company in the Merger”

“Special Factors—Financing of the Merger”

“The Voting Agreement”

“The Merger Agreement—Effects of the Merger; Directors and Officers; Articles of Incorporation; Bylaws”

“The Merger Agreement—Closing and Effective Time of the Merger”

“The Merger Agreement—Treatment of Common Stock and Company Equity Awards”

“The Merger Agreement—Conduct of PIM, LLC Pending the Merger”

“Other Important Information Regarding the Company—Market Price of Class A Common Stock and Dividends”

“Other Important Information Regarding the Company—Directors and Executive Officers of the Company”

“Delisting and Deregistration of Common Stock”

Annex A—Agreement and Plan of Merger

Item 7. Purposes, Alternatives, Reasons and Effects (Regulation M-A Item 1013)

(a) Purposes. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Reasons for the Merger; Recommendation of the Special Committee and the Board; Fairness of the Merger”

“Special Factors—Position of PIM, LLC as to the Fairness of the Merger”

“Special Factors—Purpose and Reasons of PIM, LLC for the Merger”

“Special Factors—Plans for the Company After the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Certain Effects of the Merger for PIM, LLC”

(b) Alternatives. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Special Factors—Background of the Merger”

“Special Factors—Reasons for the Merger; Recommendation of the Special Committee and the Board; Fairness of the Merger”

“Special Factors—Position of PIM, LLC as to the Fairness of the Merger”

“Special Factors—Purpose and Reasons of PIM, LLC for the Merger”

(c) Reasons. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Special Factors—Background of the Merger”

“Special Factors—Reasons for the Merger; Recommendation of the Special Committee and the Board; Fairness of the Merger”

7

“Special Factors—Position of PIM, LLC as to the Fairness of the Merger”

“Special Factors—Purpose and Reasons of PIM, LLC for the Merger”

“Special Factors—Opinion of Ardea Partners LP”

“Special Factors—Opinion of CastleOak Securities, L.P.”

“Special Factors—Unaudited Prospective Financial Information of the Company”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Certain Effects of the Merger for PIM, LLC”

Annex B – Opinion of Ardea Partners LP

Annex C – Opinion of CastleOak Securities, L.P.

(d) Effects. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Reasons for the Merger; Recommendation of the Special Committee and the Board; Fairness of the Merger”

“Special Factors—Position of PIM, LLC as to the Fairness of the Merger”

“Special Factors—Purpose and Reasons of PIM, LLC for the Merger”

“Special Factors—Plans for the Company After the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Certain Effects of the Merger for PIM, LLC”

“Special Factors—Certain Effects on the Company if the Merger Is Not Completed”

“Special Factors—Interests of Executive Officers and Directors of the Company in the Merger”

“Special Factors—Material U.S. Federal Income Tax Consequences of the Merger”

“Special Factors—Accounting Treatment”

“Special Factors—Financing of the Merger”

“Special Factors—Fees and Expenses”

“Special Factors—Payment of Merger Consideration”

“The Merger Agreement—Effects of the Merger; Directors and Officers; Articles of Incorporation; Bylaws”

“The Merger Agreement—Treatment of Common Stock and Company Equity Awards”

“The Merger Agreement—Conduct of PIM, LLC Pending the Merger”

“Other Important Information Regarding the Company—Market Price of Class A Common Stock and Dividends”

“Delisting and Deregistration of Common Stock”

Annex A—Agreement and Plan of Merger

8

Item 8. Fairness of the Transaction (Regulation M-A Item 1014)

(a) – (b) Fairness; Factors considered in determining fairness. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Reasons for the Merger; Recommendation of the Special Committee and the Board; Fairness of the Merger”

“Special Factors—Position of PIM, LLC as to the Fairness of the Merger”

“Special Factors—Opinion of Ardea Partners LP”

“Special Factors—Opinion of CastleOak Securities, L.P.”

“Special Factors—Purpose and Reasons of PIM, LLC for the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Interests of Executive Officers and Directors of the Company in the Merger”

Annex B – Opinion of Ardea Partners LP

Annex C – Opinion of CastleOak Securities, L.P.

Presentation of Ardea Partners LP to the Special Committee of the Board of Directors, dated as of June 18, 2022, is attached hereto as Exhibit (c)(1) and is incorporated herein by reference.

Presentation of Ardea Partners LP to the Special Committee of the Board of Directors, dated as of July 6, 2022, is attached hereto as Exhibit (c)(2) and is incorporated herein by reference.

Presentation of Ardea Partners LP to the Special Committee of the Board of Directors, dated as of July 26, 2022 (and presented on July 25, 2022), is attached hereto as Exhibit (c)(3) and is incorporated herein by reference.

Presentation of Ardea Partners LP to the Special Committee of the Board of Directors, dated as of July 26, 2022, is attached hereto as Exhibit (c)(4) and is incorporated herein by reference.

Presentation of CastleOak Securities, L.P. to the Special Committee of the Board of Directors, dated as of July 6, 2022, is attached hereto as Exhibit (c)(5) and is incorporated herein by reference.

Presentation of CastleOak Securities, L.P. to the Special Committee of the Board of Directors, dated as of July 25, 2022, is attached hereto as Exhibit (c)(6) and is incorporated herein by reference.

(c) Approval of security holders. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Reasons for the Merger; Recommendation of the Special Committee and the Board; Fairness of the Merger”

“Special Factors—Position of PIM, LLC as to the Fairness of the Merger”

“The Merger Agreement—Conditions to the Merger”

“The Special Meeting—Vote Required”

Annex A—Agreement and Plan of Merger

9

(d) Unaffiliated representative. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Special Factors—Background of the Merger”

“Special Factors—Reasons for the Merger; Recommendation of the Special Committee and the Board; Fairness of the Merger”

“Special Factors—Position of PIM, LLC as to the Fairness of the Merger”

“Special Factors—Opinion of Ardea Partners LP”

“Special Factors—Opinion of CastleOak Securities, L.P.”

(e) Approval of directors. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Reasons for the Merger; Recommendation of the Special Committee and the Board; Fairness of the Merger”

“Special Factors—Position of PIM, LLC as to the Fairness of the Merger”

“Special Factors—Opinion of Ardea Partners LP”

“Special Factors—Opinion of CastleOak Securities, L.P.”

“Special Factors—Interests of Executive Officers and Directors of the Company in the Merger”

“The Merger (The Merger Agreement Proposal—Proposal 1)”

(f) Other offers. Not applicable.

Item 9. Reports, Opinions, Appraisals and Negotiations (Regulation M-A Item 1015)

(a) – (c) Report, opinion or appraisal; Preparer and summary of the report, opinion or appraisal; Availability of documents. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Reasons for the Merger; Recommendation of the Special Committee and the Board; Fairness of the Merger”

“Special Factors—Position of PIM, LLC as to the Fairness of the Merger”

“Special Factors—Opinion of Ardea Partners LP”

“Special Factors—Opinion of CastleOak Securities, L.P.”

“Where You Can Find More Information”

Annex B – Opinion of Ardea Partners LP

Annex C – Opinion of CastleOak Securities, L.P.

Presentation of Ardea Partners LP to the Special Committee of the Board of Directors, dated as of June 18, 2022, is attached hereto as Exhibit (c)(1) and is incorporated herein by reference.

10

Presentation of Ardea Partners LP to the Special Committee of the Board of Directors, dated as of July 6, 2022, is attached hereto as Exhibit (c)(2) and is incorporated herein by reference.

Presentation of Ardea Partners LP to the Special Committee of the Board of Directors, dated as of July 26, 2022 (and presented on July 25, 2022), is attached hereto as Exhibit (c)(3) and is incorporated herein by reference.

Presentation of Ardea Partners LP to the Special Committee of the Board of Directors, dated as of July 26, 2022, is attached hereto as Exhibit (c)(4) and is incorporated herein by reference.

Presentation of CastleOak Securities, L.P. to the Special Committee of the Board of Directors, dated as of July 6, 2022, is attached hereto as Exhibit (c)(5) and is incorporated herein by reference.

Presentation of CastleOak Securities, L.P. to the Special Committee of the Board of Directors, dated as of July 25, 2022, is attached hereto as Exhibit (c)(6) and is incorporated herein by reference.

The reports, opinions or appraisals referenced in this Item 9 will be made available for inspection and copying at the principal executive offices of the Company during its regular business hours by any interested equity security holder of the Company or representative who has been so designated in writing.

Item 10. Source and Amounts of Funds or Other Consideration (Regulation M-A Item 1007)

(a) – (b) Source of funds; Conditions. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Special Factors—Financing of the Merger”

“The Merger Agreement—Financing”

Senior Credit Facility Commitment Letter, dated as of July 26, 2022, by and between, JPMorgan Chase Bank, N.A. and Pzena Investment Management, LLC. (filed as Exhibit 10.2 to Pzena Investment Management, Inc.’s Current Report on Form 8-K, filed July 28, 2022 and incorporated herein by reference), is attached hereto as Exhibit (b)(1) and is incorporated herein by reference.

(c) Expenses. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Fees and Expenses”

“The Merger Agreement—Termination”

“The Merger Agreement—PIM, LLC Termination Fee”

“The Merger Agreement—Expenses”

“The Special Meeting—Solicitation of Proxies; Payment of Solicitation Expenses”

(d) Borrowed funds. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Special Factors—Financing of the Merger”

“The Merger Agreement—Financing”

Senior Credit Facility Commitment Letter, dated as of July 26, 2022, by and between, JPMorgan Chase Bank, N.A. and Pzena Investment Management, LLC. (filed as Exhibit 10.2 to Pzena Investment Management, Inc.’s Current Report on Form 8-K, filed July 28, 2022 and incorporated herein by reference), is attached hereto as Exhibit (b)(1) and is incorporated herein by reference.

11

Item 11. Interest in Securities of the Subject Company (Regulation M-A Item 1008)

(a) Securities ownership. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Special Factors—Interests of Executive Officers and Directors of the Company in the Merger”

“Other Important Information Regarding the Company—Security Ownership of Certain Beneficial Owners and Management”

(b) Securities transactions. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Other Important Information Regarding the Company—Certain Transactions in the Shares of Common Stock”

Item 12. The Solicitation or Recommendation (Regulation M-A Item 1012)

(d) Intent to tender or vote in a going-private transaction. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Reasons for the Merger; Recommendation of the Special Committee and the Board; Fairness of the Merger”

“Special Factors—Position of PIM, LLC as to the Fairness of the Merger”

“Special Factors—Purpose and Reasons of PIM, LLC for the Merger”

“Special Factors—Management Stockholders’ Obligation to Vote in Favor of the Merger”

“The Special Meeting—Vote Required”

“The Voting Agreement”

Annex E—Voting Agreement

(e) Recommendation of others. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Reasons for the Merger; Recommendation of the Special Committee and the Board; Fairness of the Merger”

“Special Factors—Position of PIM, LLC as to the Fairness of the Merger”

“Special Factors—Purpose and Reasons of PIM, LLC for the Merger”

“The Merger (The Merger Agreement Proposal—Proposal 1)”

Item 13. Financial Information (Regulation M-A Item 1010)

(a) Financial statements. The audited consolidated financial statements set forth in Item 8 of the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2021 and the financial statements set forth in Item 1 of the Company’s Quarterly Report on Form 10-Q for the quarterly period ended June 30, 2022 are incorporated herein by reference.

12

The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Special Factors—Certain Effects of the Merger”

“Special Factors—Unaudited Prospective Financial Information of the Company”

“Other Important Information Regarding the Company—Book Value per Share”

“Where You Can Find More Information”

(b) Pro forma information. Not applicable.

Item 14. Persons/Assets, Retained, Employed, Compensated or Used (Regulation M-A Item 1009)

(a) – (b) Solicitations or recommendations; Employees and corporate assets. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers About the Special Meeting and the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Fees and Expenses”

“The Special Meeting—Solicitation of Proxies; Payment of Solicitation Expenses”

Item 15. Additional Information (Regulation M-A Item 1011)

(b) Golden Parachute Compensation. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Special Factors—Interests of Executive Officers and Directors of the Company in the Merger—Golden Parachute Compensation”

“Merger-Related Executive Compensation Arrangement (The Merger-Related Compensation Proposal—Proposal 3)”

(c) Other material information. The information set forth in the Proxy Statement, including all annexes thereto, is incorporated herein by reference.

Item 16. Exhibits (Regulation M-A Item 1016)

(a)(1) Preliminary Proxy Statement of Pzena Investment Management, Inc. (the “Proxy Statement”) (incorporated herein by reference to the Schedule 14A filed concurrently with the SEC).

(a)(2) Form of Proxy Card.*

(a)(3) Letter to Stockholders (incorporated herein by reference to the Proxy Statement).

(a)(4) Notice of Special Meeting of Stockholders (incorporated herein by reference to the Proxy Statement).

(a)(5) Press Release, dated July 26, 2022 (incorporated herein by reference to Exhibit 99.1 to the Company’s Current Report on Form 8-K, filed July 26, 2022).

(b)(1) Senior Credit Facility Commitment Letter, dated as of July 26, 2022, by and between, JPMorgan Chase Bank, N.A. and Pzena Investment Management, LLC. (incorporated herein by reference to Exhibit 10.2 to the Company’s Current Report on Form 8-K, filed July 28, 2022).

13

(c)(1) Presentation of Ardea Partners LP to the Special Committee of the Board of Directors, dated as of June 18, 2022.

(c)(2) Presentation of Ardea Partners LP to the Special Committee of the Board of Directors, dated as of July 6, 2022.

(c)(3) Presentation of Ardea Partners LP to the Special Committee of the Board of Directors, dated as of July 26, 2022 (and presented on July 25, 2022).

(c)(4) Presentation of Ardea Partners LP to the Special Committee of the Board of Directors, dated as of July 26, 2022.

(c)(5) Presentation of CastleOak Securities, L.P. to the Special Committee of the Board of Directors, dated as of July 6, 2022.

(c)(6) Presentation of CastleOak Securities, L.P. to the Special Committee of the Board of Directors, dated as of July 25, 2022.

(c)(7) Opinion of Ardea Partners LP, dated July 26, 2022 (incorporated herein by reference to Annex B of the Proxy Statement).

(c)(8) Opinion of CastleOak Securities, L.P. dated July 26, 2022 (incorporated herein by reference to Annex C of the Proxy Statement).

(d)(1) Agreement and Plan of Merger, dated as of July 26, 2022, by and among Pzena Investment Management, LLC, Panda Merger Sub, LLC, and Pzena Investment Management, Inc. (incorporated herein by reference to Annex A of the Proxy Statement).

(d)(2) Voting Agreement, dated as of July 26, 2022, by and among Pzena Investment Management, Inc., Richard S. Pzena, John P. Goetz, William L. Lipsey, Chenyu Caroline Cai, and Allison Fisch (incorporated herein by reference to Annex E of the Proxy Statement).

(d)(3) Class B Stockholders’ Agreement, dated as of October 30, 2007, by and among Pzena Investment Management, Inc. and the Class B Stockholders named therein (incorporated herein by reference to Exhibit 4.5 to the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2021, filed on March 9, 2022.

(f) Section 262 of the General Corporation Law of the State of Delaware (incorporated herein by reference to Annex D of the Proxy Statement).

(g) None.

107 Filing Fee Table.

| * | To be filed by amendment |

14

SIGNATURE

After due inquiry and to the best of each of the undersigned’s knowledge and belief, each of the undersigned certifies that the information set forth in this statement is true, complete and correct.

Dated as of August 22, 2022

| PZENA INVESTMENT MANAGEMENT, INC. | ||||

| By: | /s/ Richard S. Pzena | |||

| Name: | Richard S. Pzena | |||

| Title: | Chief Executive Officer | |||

| PZENA INVESTMENT MANAGEMENT, LLC

By: Pzena Investment Management, Inc., its Managing Member | ||||

| By: | /s/ Richard S. Pzena | |||

| Name: | Richard S. Pzena | |||

| Title: | Chief Executive Officer | |||

| PANDA MERGER SUB, LLC | ||||

| By: Pzena Investment Management, LLC, its Managing Member

By: Pzena Investment Management, Inc., its Managing Member | ||||

| By: | /s/ Richard S. Pzena | |||

| Name: | Richard S. Pzena | |||

| Title: | Chief Executive Officer | |||

[Signature Page to SC 13e-3]

Exhibit (c)(1)

PRELIMINARY BACKGROUND MATERIALS Project Panda Presentation to the Special Committee of the Board of Directors June 18, 2022

PRELIMINARY BACKGROUND MATERIALS Agenda Items 1 Summary of Proposals 2 Trading Overview 3 Premiums and Multiples Overview 4 Selected Valuation Benchmarks A Appendix June 2022 2

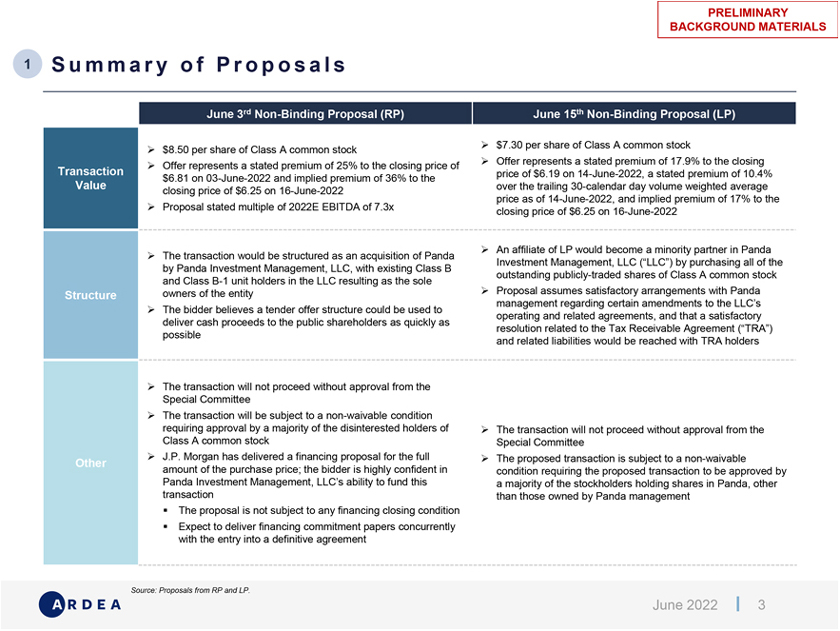

PRELIMINARY BACKGROUND MATERIALS 1 Summary of Proposals $8.50 per share of Class A common stock $7.30 per share of Class A common stock Offer represents a stated premium of 25% to the closing price of Offer represents a stated premium of 17.9% to the closing $6.81 on 03-June-2022 and implied premium of 36% to the price of $6.19 on 14-June-2022, a stated premium of 10.4% over the trailing 30-calendar day volume weighted average closing price of $6.25 on 16-June-2022 price as of 14-June-2022, and implied premium of 17% to the Proposal stated multiple of 2022E EBITDA of 7.3x closing price of $6.25 on 16-June-2022 An affiliate of LP would become a minority partner in Panda The transaction would be structured as an acquisition of Panda Investment Management, LLC (“LLC”) by purchasing all of the by Panda Investment Management, LLC, with existing Class B outstanding publicly-traded shares of Class A common stock and Class B-1 unit holders in the LLC resulting as the sole owners of the entity Proposal assumes satisfactory arrangements with Panda management regarding certain amendments to the LLC’s The bidder believes a tender offer structure could be used to operating and related agreements, and that a satisfactory deliver cash proceeds to the public shareholders as quickly as resolution related to the Tax Receivable Agreement (“TRA”) possible and related liabilities would be reached with TRA holders The transaction will not proceed without approval from the Special Committee The transaction will be subject to a non-waivable condition requiring approval by a majority of the disinterested holders of The transaction will not proceed without approval from the Class A common stock Special Committee J.P. Morgan has delivered a financing proposal for the full The proposed transaction is subject to a non-waivable amount of the purchase price; the bidder is highly confident in condition requiring the proposed transaction to be approved by Panda Investment Management, LLC’s ability to fund this a majority of the stockholders holding shares in Panda, other transaction than those owned by Panda management The proposal is not subject to any financing closing condition Expect to deliver financing commitment papers concurrently with the entry into a definitive agreement Source: Proposals from RP and LP. June 2022 3

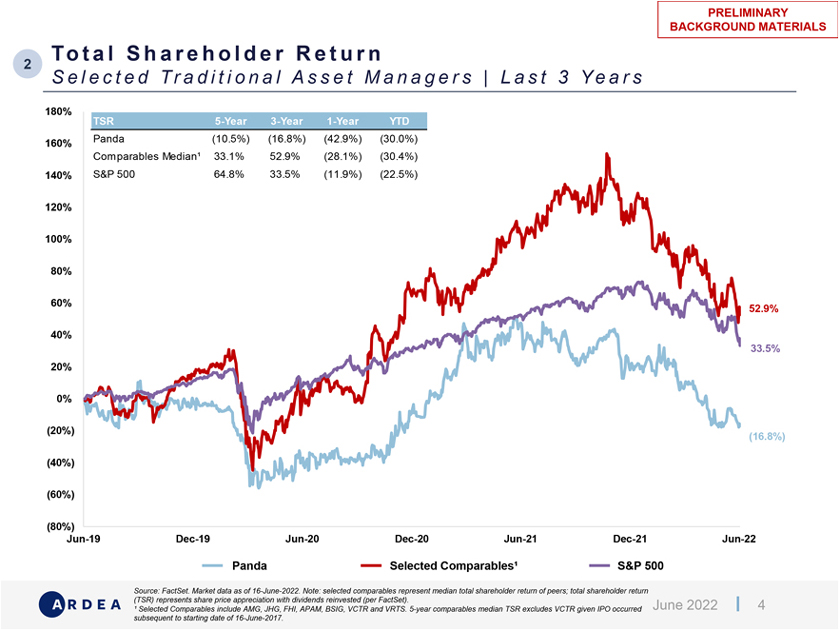

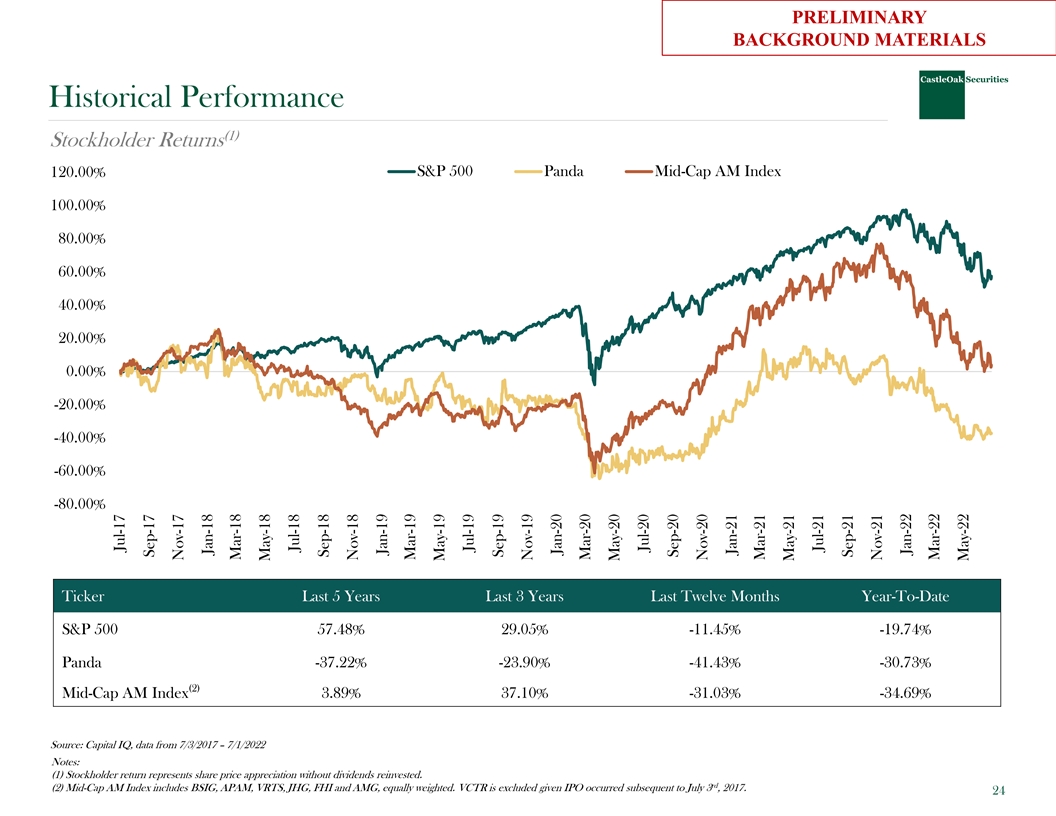

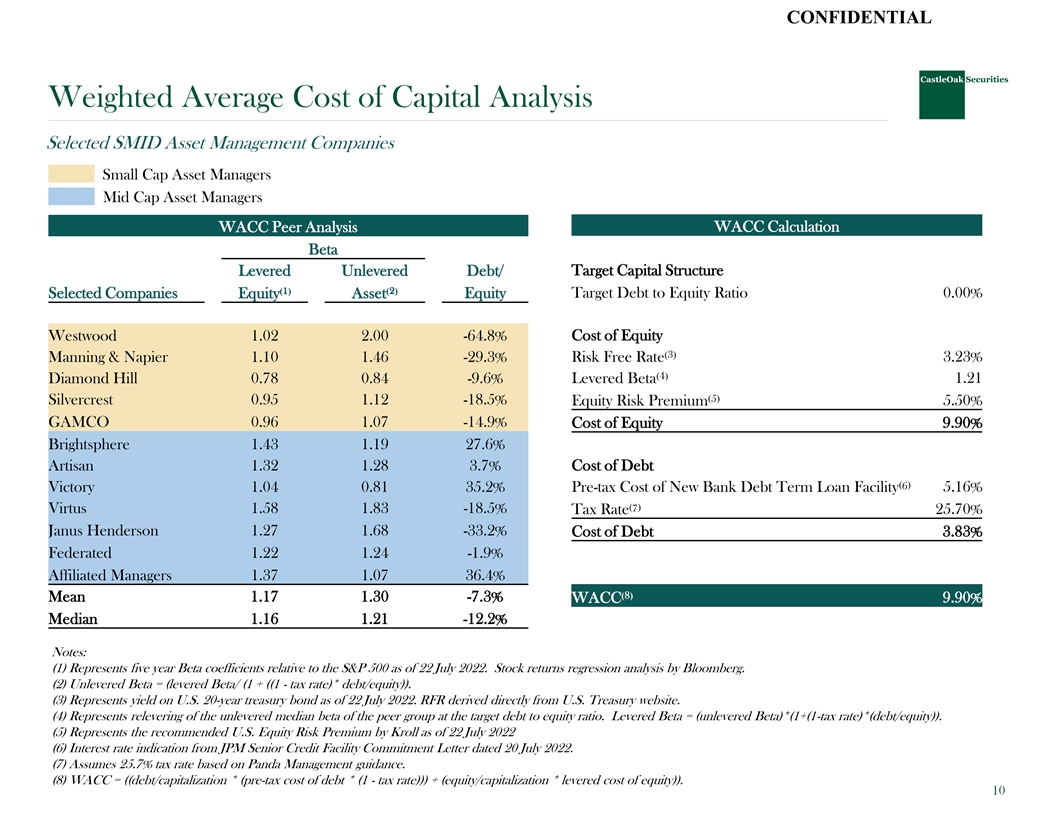

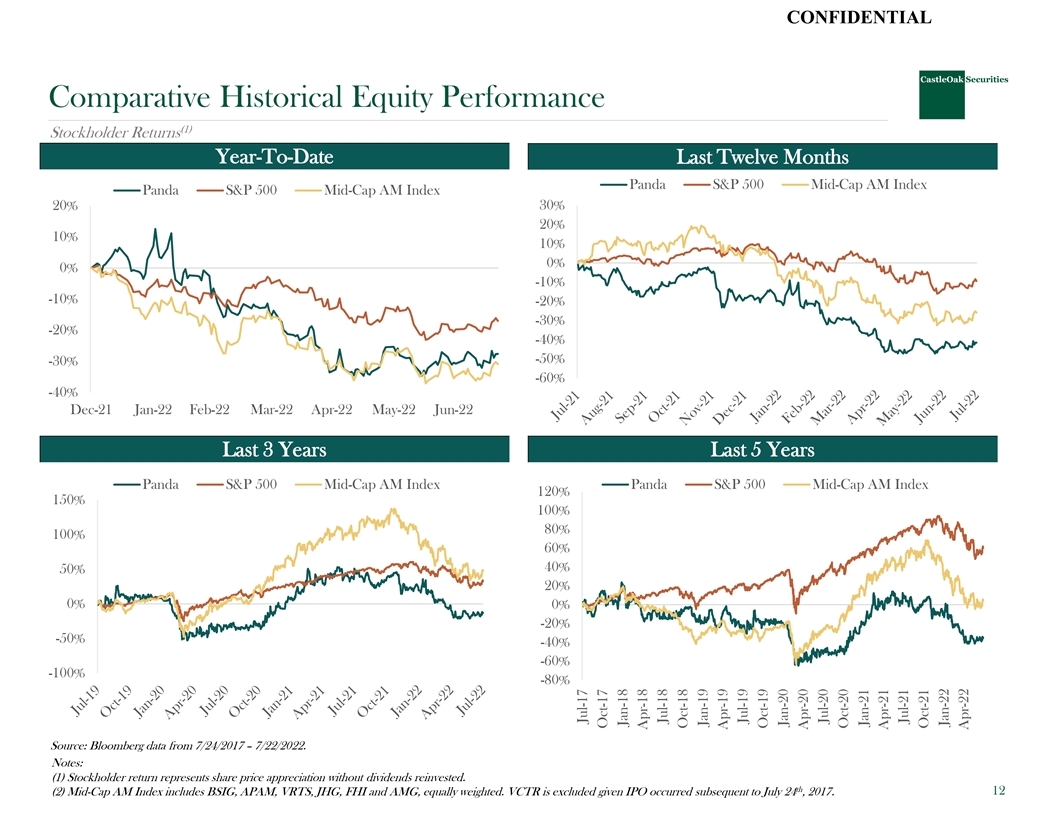

PRELIMINARY BACKGROUND MATERIALS Total Share holder Return 2 Selected Traditional Asset Managers | Last 3 Years 180% 160% Panda (10.5%) (16.8%) (42.9%) (30.0%) Comparables Median¹ 33.1% 52.9% (28.1%) (30.4%) 140% S&P 500 64.8% 33.5% (11.9%) (22.5%) 120% 100% 80% 60% 52.9% 40% 33.5% 20% 0% (20%) (16.8%) (40%) (60%) (80%) Jun-19 Dec-19 Jun-20 Dec-20 Jun-21 Dec-21 Jun-22 Panda Selected Comparables¹ S&P 500 Source: FactSet. Market data as of 16-June-2022. Note: selected comparables represent median total shareholder return of peers; total shareholder return (TSR) represents share price appreciation with dividends reinvested (per FactSet). June 2022 4 ¹ Selected Comparables include AMG, JHG, FHI, APAM, BSIG, VCTR and VRTS. 5-year comparables median TSR excludes VCTR given IPO occurred subsequent to starting date of 16-June-2017.

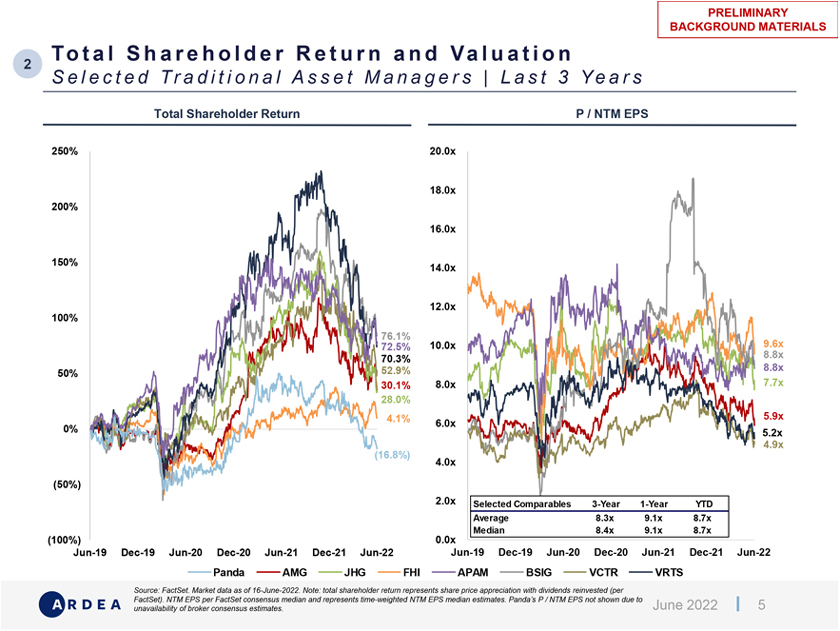

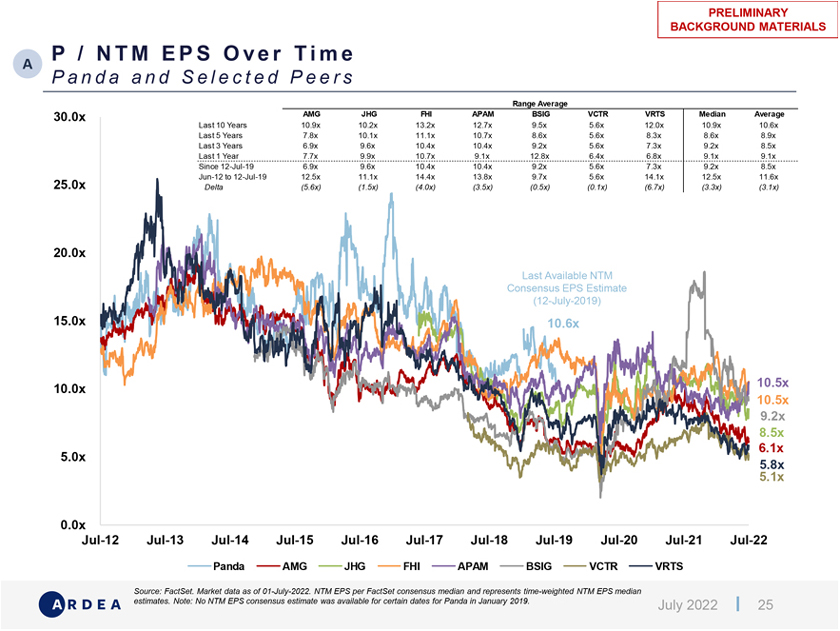

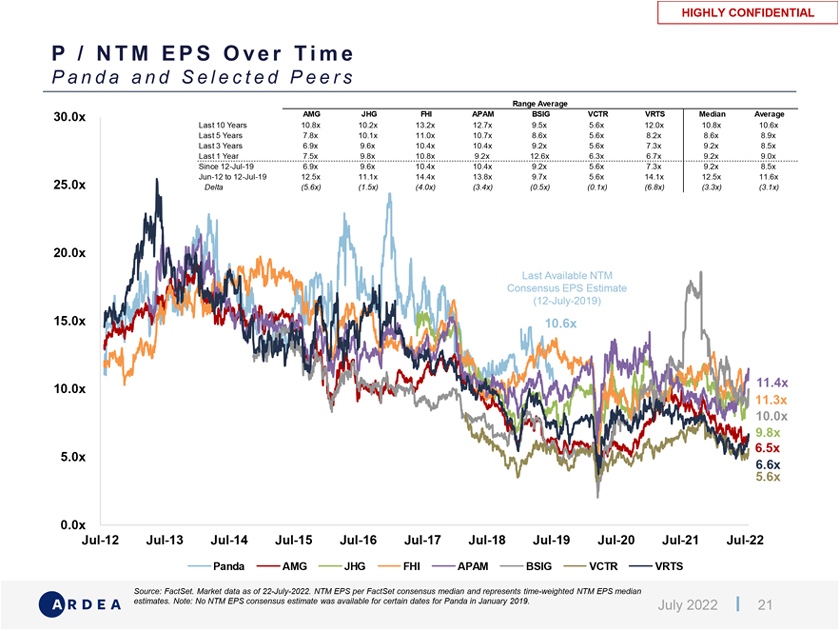

PRELIMINARY BACKGROUND MATERIALS Total Share holder Return and Valuation Selected Traditional Asset Managers | Last 3 Years Total Shareholder Return P / NTM EPS 250% 20.0x 18.0x 200% 16.0x 150% 14.0x 12.0x 100% 76.1% 72.5% 10.0x 9.6x 70.3% 8.8x 52.9% 8.8x 50% 7.7x 30.1% 8.0x 28.0% 4.1% 5.9x 6.0x 0% 5.2x 4.9x (16.8%) 4.0x (50%) 2.0x Selected Comparables 3-Year 1-Year YTD Average 8.3x 9.1x 8.7x Median 8.4x 9.1x 8.7x (100%) 0.0x Jun-19 Dec-19 Jun-20 Dec-20 Jun-21 Dec-21 Jun-22 Jun-19 Dec-19 Jun-20 Dec-20 Jun-21 Dec-21 Jun-22 Panda AMG JHG FHI APAM BSIG VCTR VRTS Source: FactSet. Market data as of 16-June-2022. Note: total shareholder return represents share price appreciation with dividends reinvested (per FactSet). NTM EPS per FactSet consensus median and represents time-weighted NTM EPS median estimates. Panda’s P / NTM EPS not shown due to June 2022 5 unavailability of broker consensus estimates.

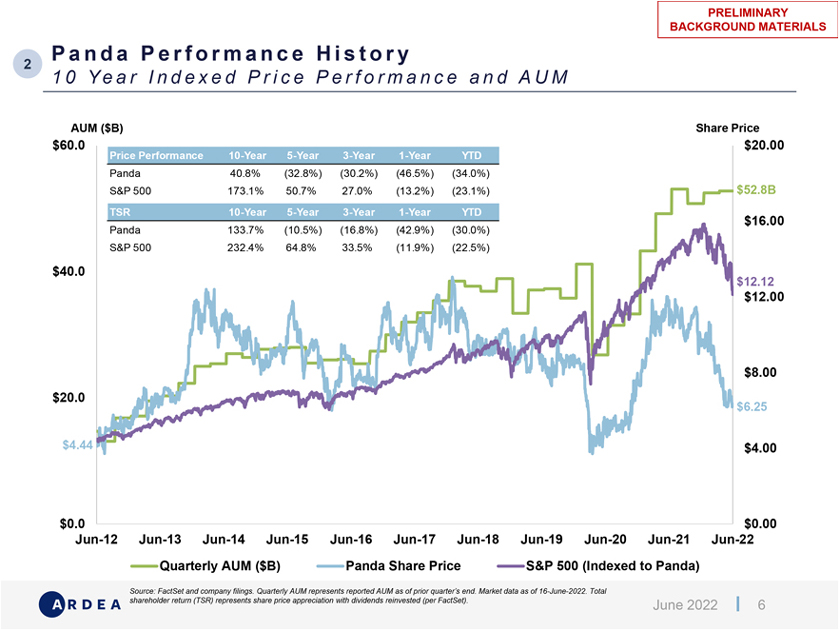

PRELIMINARY BACKGROUND MATERIALS Panda Performance History 2 10 Year Indexed Price Performance and AUM AUM ($B) Share Price $60.0 Price Performance 10-Year 5-Year 3-Year 1-Year YTD $20.00 Panda 40.8% (32.8%) (30.2%) (46.5%) (34.0%) S&P 500 173.1% 50.7% 27.0% (13.2%) (23.1%) $52.8B TSR 10-Year 5-Year 3-Year 1-Year YTD $16.00 Panda 133.7% (10.5%) (16.8%) (42.9%) (30.0%) S&P 500 232.4% 64.8% 33.5% (11.9%) (22.5%) $40.0 $12.12 $12.00 $8.00 $20.0 $6.25 $4.44 $4.00 $0.0 $0.00 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16 Jun-17 Jun-18 Jun-19 Jun-20 Jun-21 Jun-22 Quarterly AUM ($B) Panda Share Price S&P 500 (Indexed to Panda) Source: FactSet and company filings. Quarterly AUM represents reported AUM as of prior quarter’s end. Market data as of 16-June-2022. Total shareholder return (TSR) represents share price appreciation with dividends reinvested (per FactSet). June 2022 6

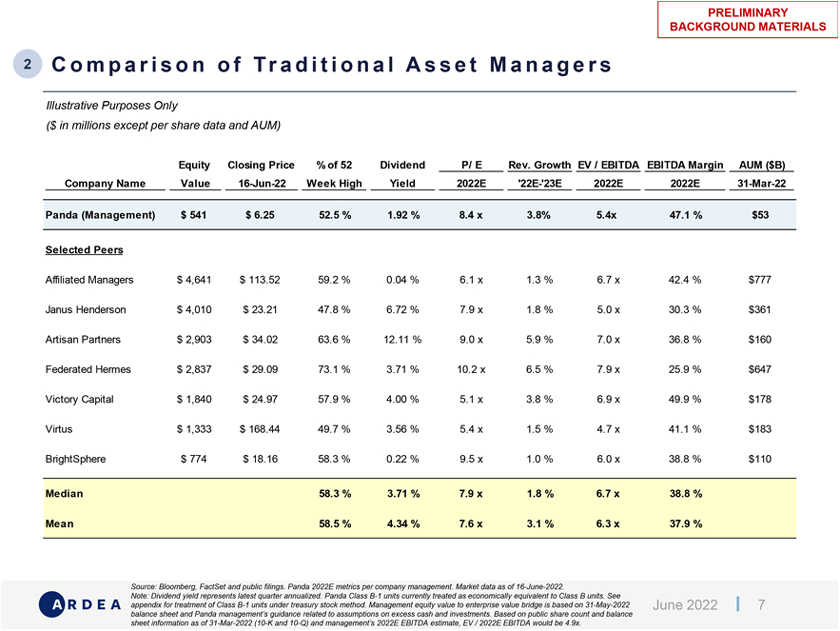

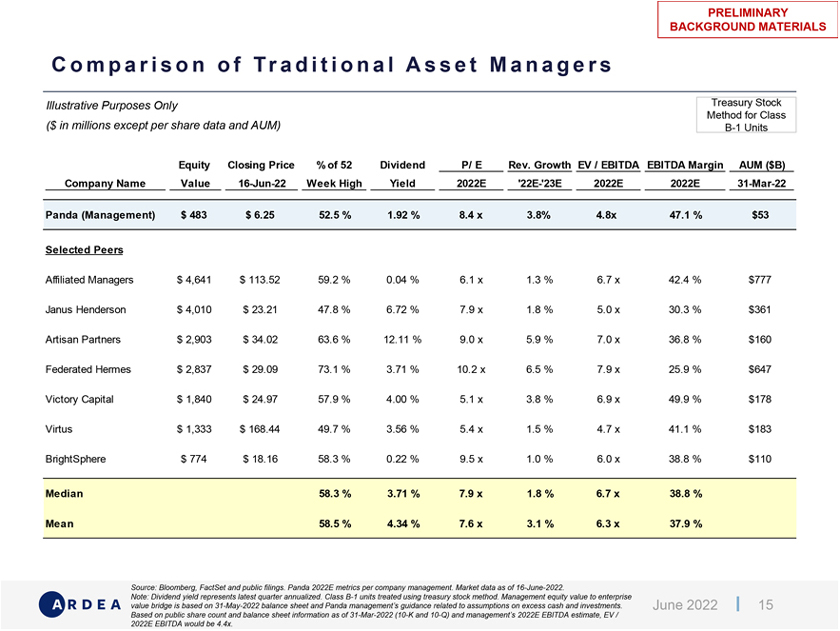

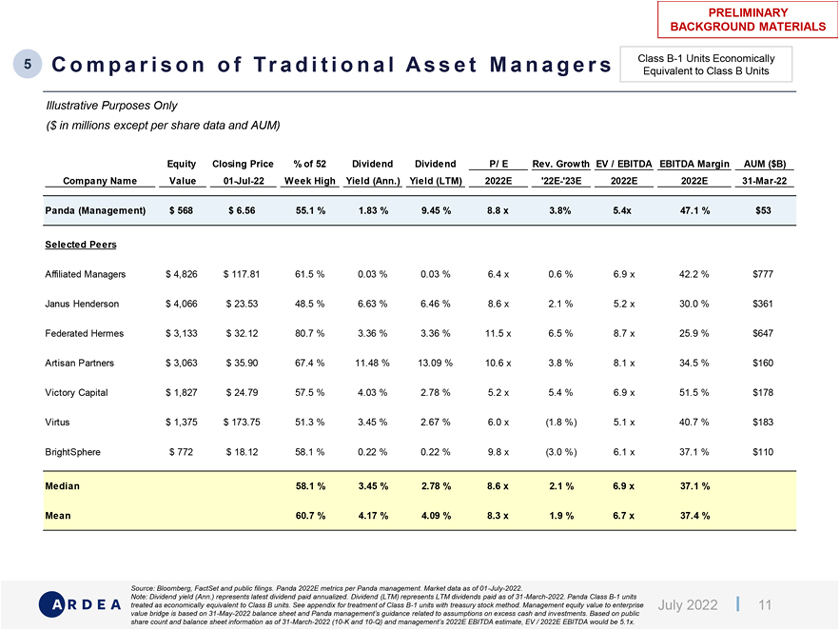

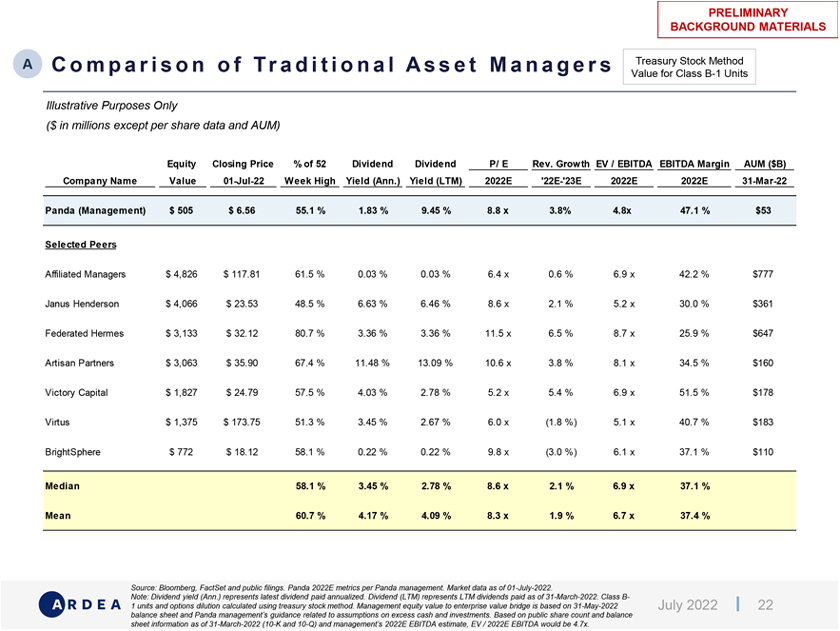

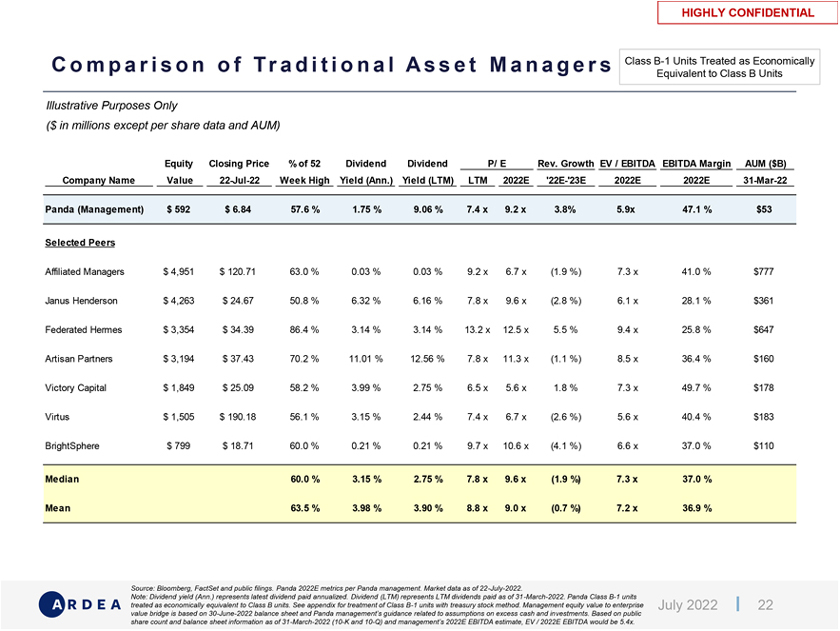

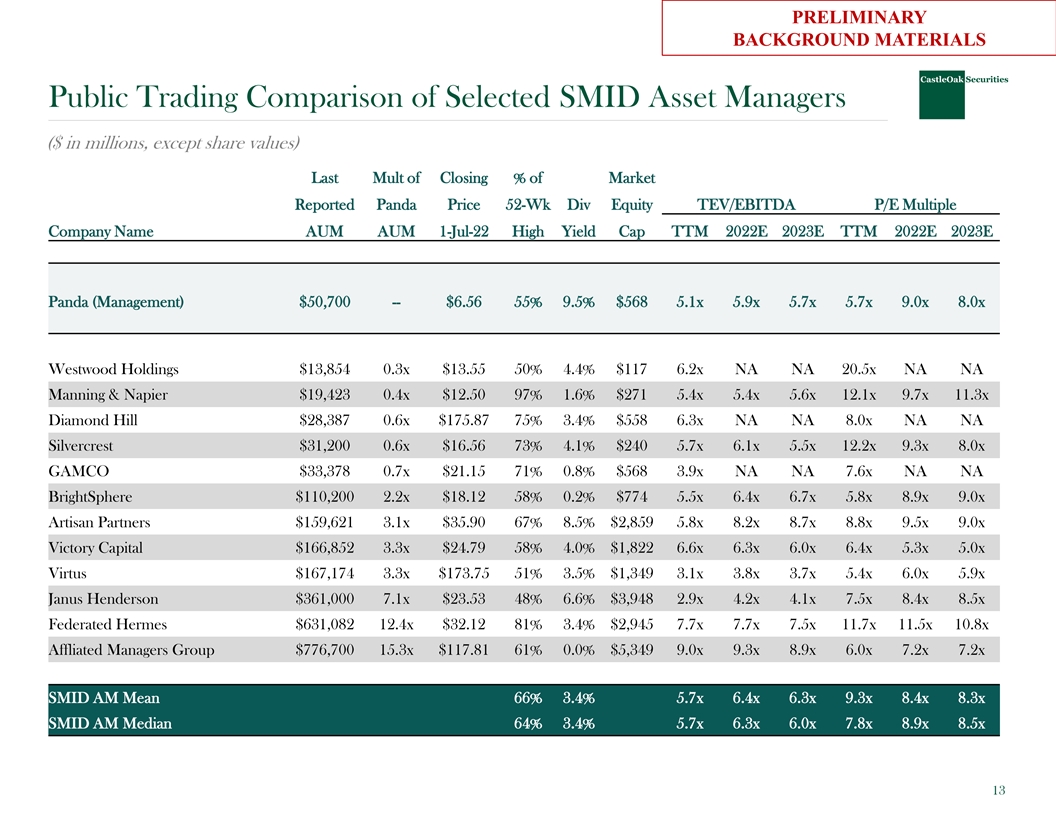

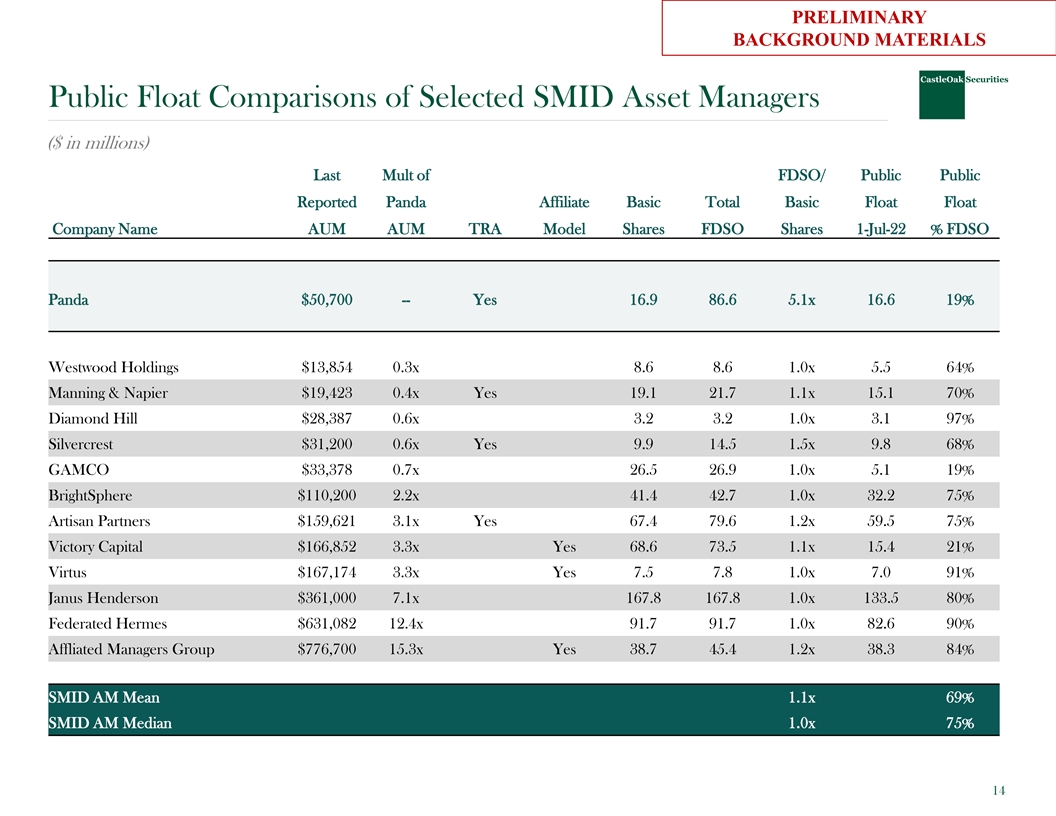

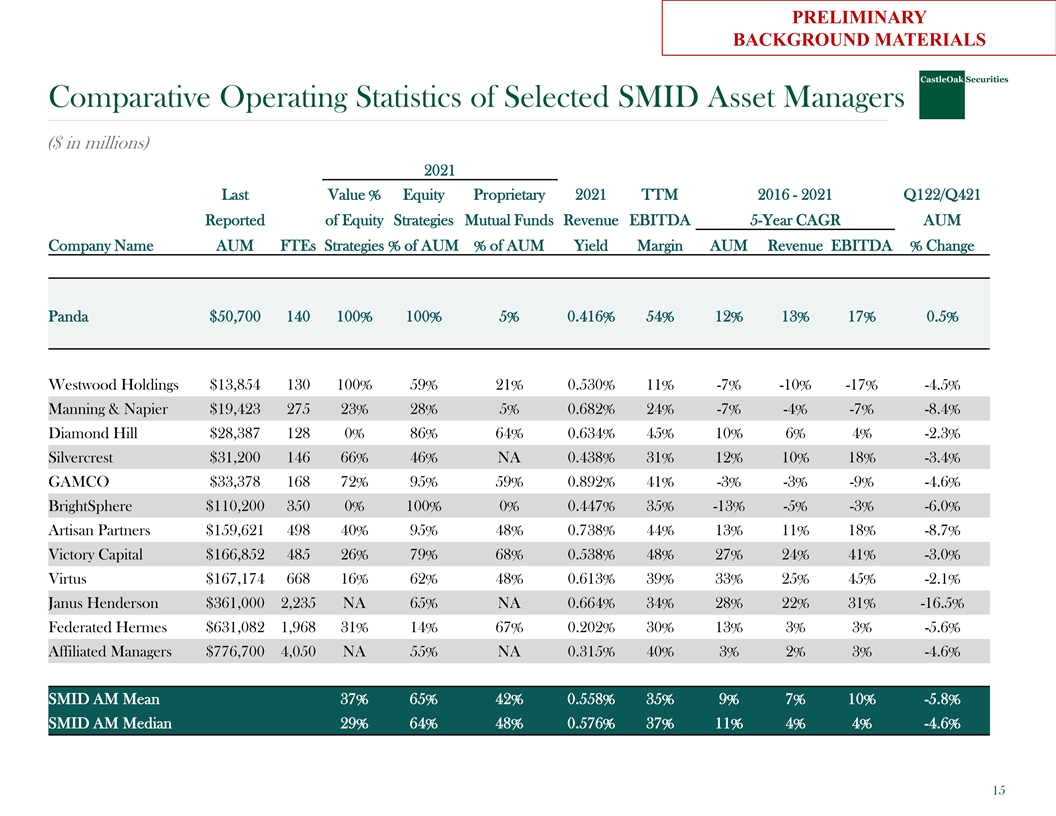

PRELIMINARY BACKGROUND MATERIALS 2 comparison of Traditional Asset Managers Illustrative Purposes Only ($ in millions except per share data and AUM) Equity Closing Price % of 52 Dividend P/ E Rev. Growth EV / EBITDA EBITDA Margin AUM ($B) Company Name Value 16-Jun-22 Week High Yield 2022E ‘22E-‘23E 2022E 2022E 31-Mar-22 Panda (Management) $ 541 $ 6.25 52.5 % 1.92 % 8.4 x 3.8% 5.4x 47.1 % $53 Selected Peers Affiliated Managers $ 4,641 $ 113.52 59.2 % 0.04 % 6.1 x 1.3 % 6.7 x 42.4 % $777 Janus Henderson $ 4,010 $ 23.21 47.8 % 6.72 % 7.9 x 1.8 % 5.0 x 30.3 % $361 Artisan Partners $ 2,903 $ 34.02 63.6 % 12.11 % 9.0 x 5.9 % 7.0 x 36.8 % $160 Federated Hermes $ 2,837 $ 29.09 73.1 % 3.71 % 10.2 x 6.5 % 7.9 x 25.9 % $647 Victory Capital $ 1,840 $ 24.97 57.9 % 4.00 % 5.1 x 3.8 % 6.9 x 49.9 % $178 Virtus $ 1,333 $ 168.44 49.7 % 3.56 % 5.4 x 1.5 % 4.7 x 41.1 % $183 BrightSphere $ 774 $ 18.16 58.3 % 0.22 % 9.5 x 1.0 % 6.0 x 38.8 % $110 Median 58.3 % 3.71 % 7.9 x 1.8 % 6.7 x 38.8 % Mean 58.5 % 4.34 % 7.6 x 3.1 % 6.3 x 37.9 % Source: Bloomberg, FactSet and public filings. Panda 2022E metrics per company management. Market data as of 16-June-2022. Note: Dividend yield represents latest quarter annualized. Panda Class B-1 units currently treated as economically equivalent to Class B units. See appendix for treatment of Class B-1 units under treasury stock method. Management equity value to enterprise value bridge is based on 31-May-2022 June 2022 7 balance sheet and Panda management’s guidance related to assumptions on excess cash and investments. Based on public share count and balance sheet information as of 31-Mar-2022 (10-K and 10-Q) and management’s 2022E EBITDA estimate, EV / 2022E EBITDA would be 4.9x.

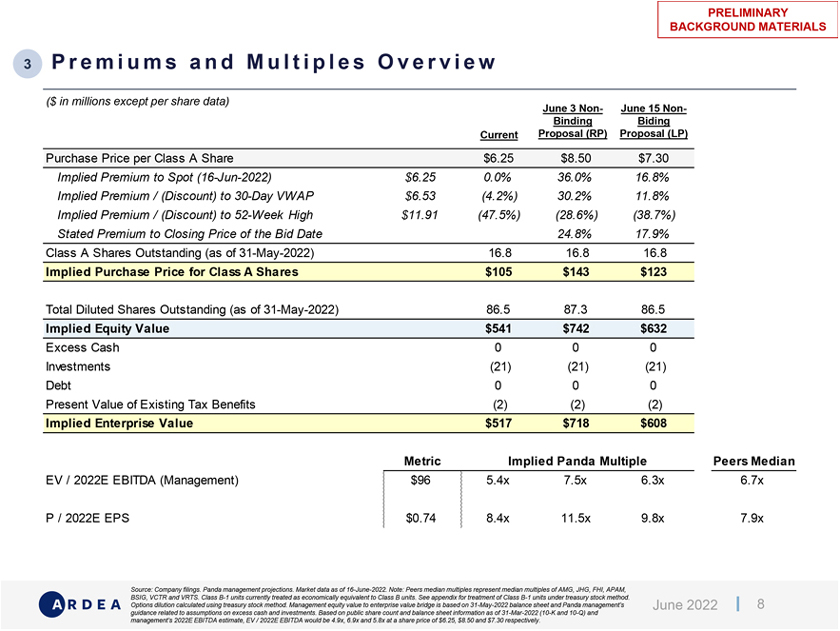

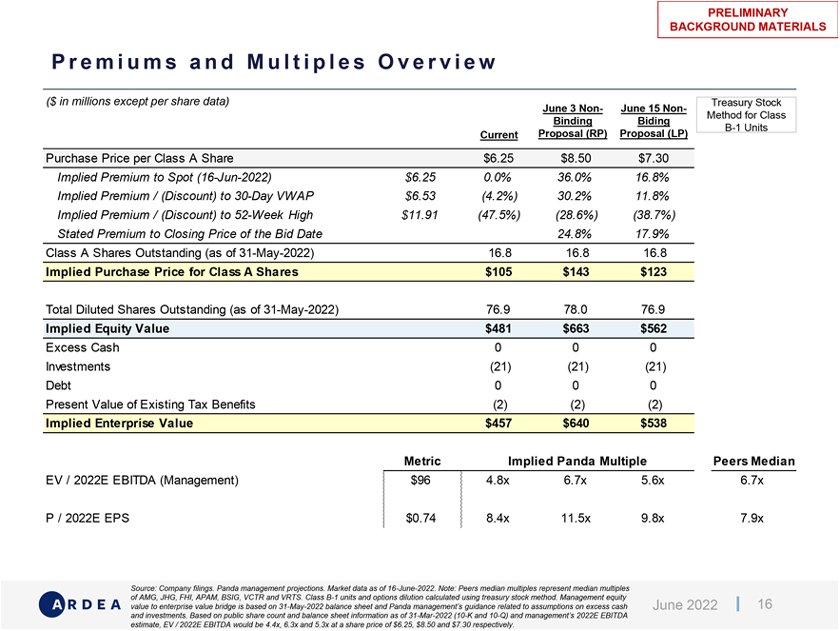

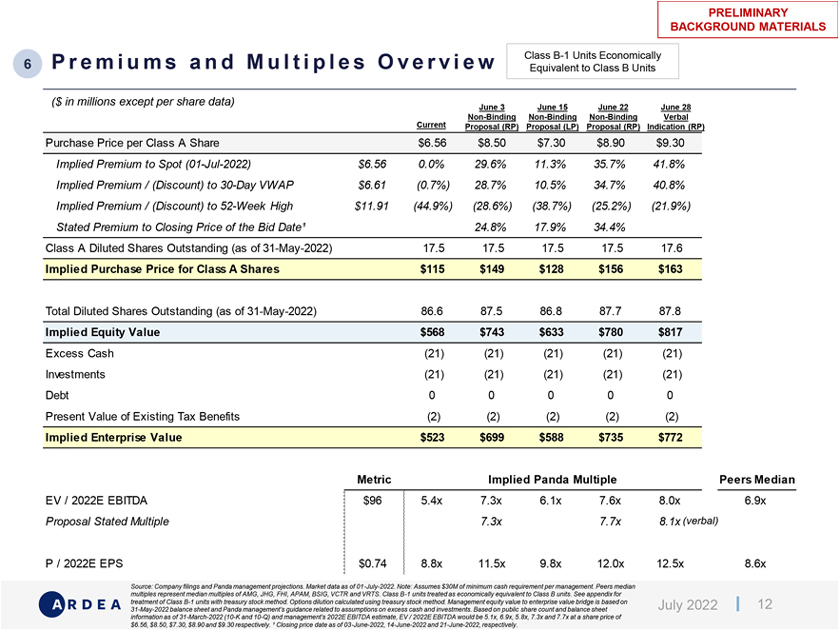

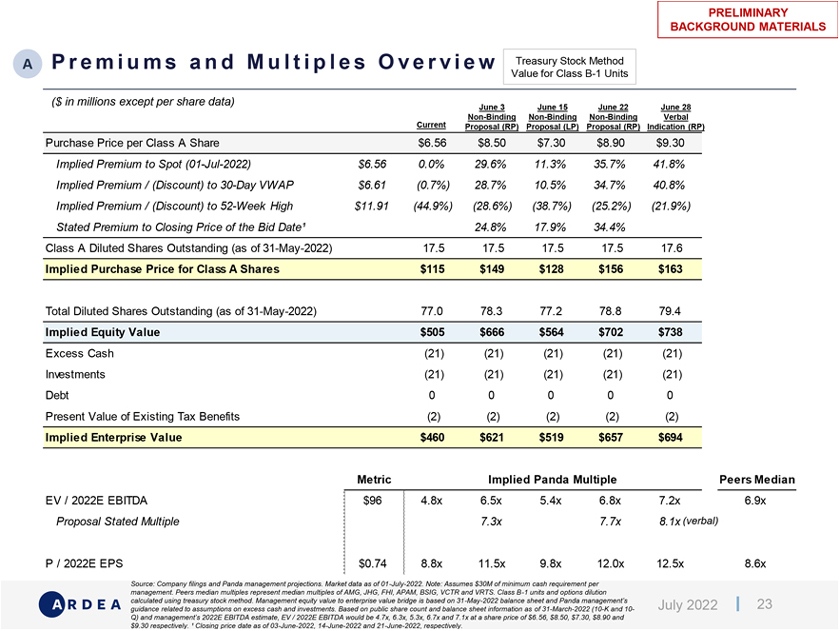

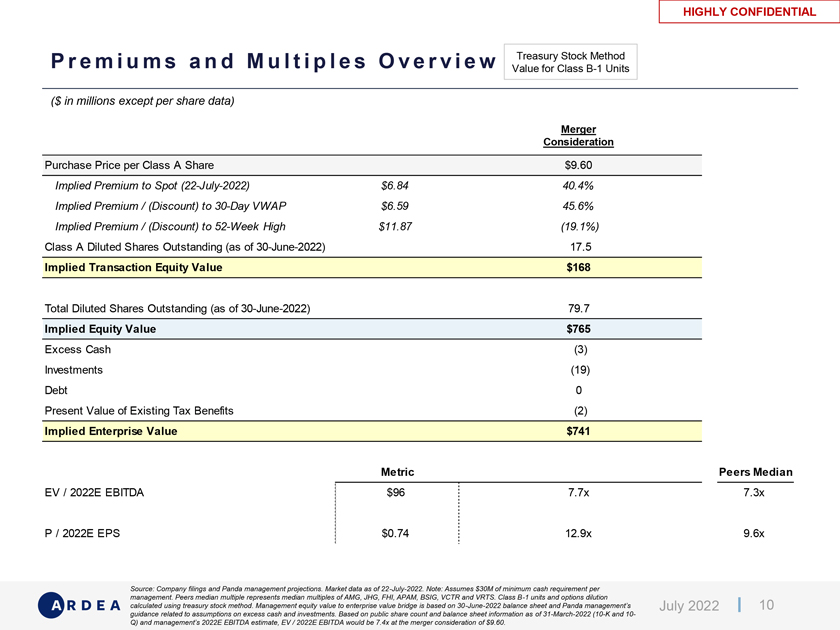

PRELIMINARY BACKGROUND MATERIALS 3 Premiums and Multiples Overview ($ in millions except per share data) June 3 Non- June 15 Non-Binding Biding Current Proposal (RP) Proposal (LP) Purchase Price per Class A Share $6.25 $8.50 $7.30 Implied Premium to Spot (16-Jun-2022) $6.25 0.0% 36.0% 16.8% Implied Premium / (Discount) to 30-Day VWAP $6.53 (4.2%) 30.2% 11.8% Implied Premium / (Discount) to 52-Week High $11.91 (47.5%) (28.6%) (38.7%) Stated Premium to Closing Price of the Bid Date 24.8% 17.9% Class A Shares Outstanding (as of 31-May-2022) 16.8 16.8 16.8 Implied Purchase Price for Class A Shares $105 $143 $123 Total Diluted Shares Outstanding (as of 31-May-2022) 86.5 87.3 86.5 Implied Equity Value $541 $742 $632 Excess Cash 0 0 0 Investments (21) (21) (21) Debt 0 0 0 Present Value of Existing Tax Benefits (2) (2) (2) Implied Enterprise Value $517 $718 $608 Metric Implied Panda Multiple Peers Median EV / 2022E EBITDA (Management) $96 5.4x 7.5x 6.3x 6.7x P / 2022E EPS $0.74 8.4x 11.5x 9.8x 7.9x Source: Company filings. Panda management projections. Market data as of 16-June-2022. Note: Peers median multiples represent median multiples of AMG, JHG, FHI, APAM, BSIG, VCTR and VRTS. Class B-1 units currently treated as economically equivalent to Class B units. See appendix for treatment of Class B-1 units under treasury stock method. Options dilution calculated using treasury stock method. Management equity value to enterprise value bridge is based on 31-May-2022 balance sheet and Panda management’s June 2022 8 guidance related to assumptions on excess cash and investments. Based on public share count and balance sheet information as of 31-Mar-2022 (10-K and 10-Q) and management’s 2022E EBITDA estimate, EV / 2022E EBITDA would be 4.9x, 6.9x and 5.8x at a share price of $6.25, $8.50 and $7.30 respectively.

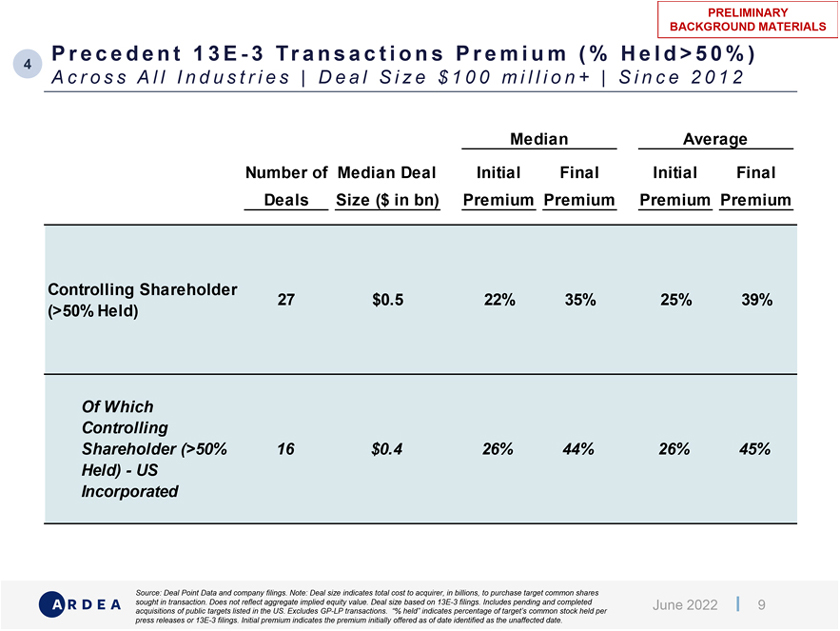

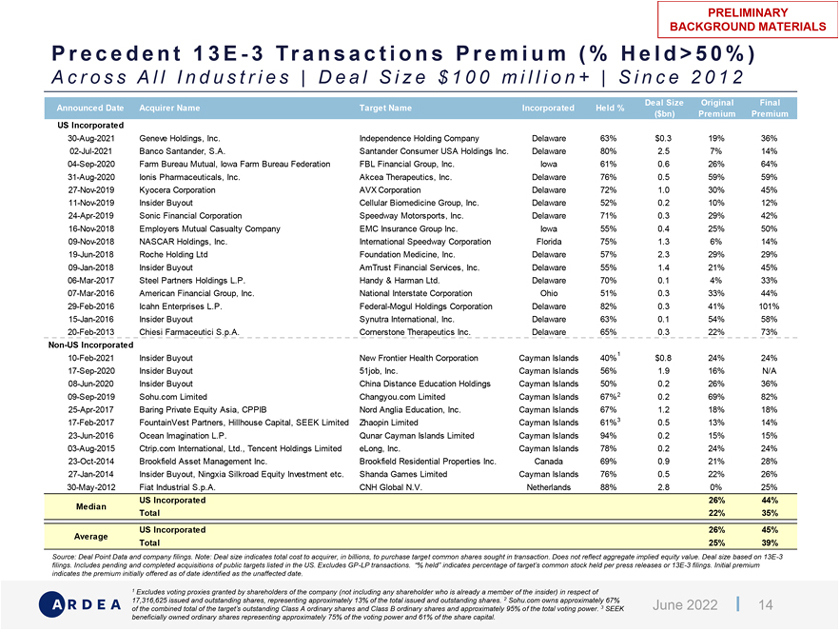

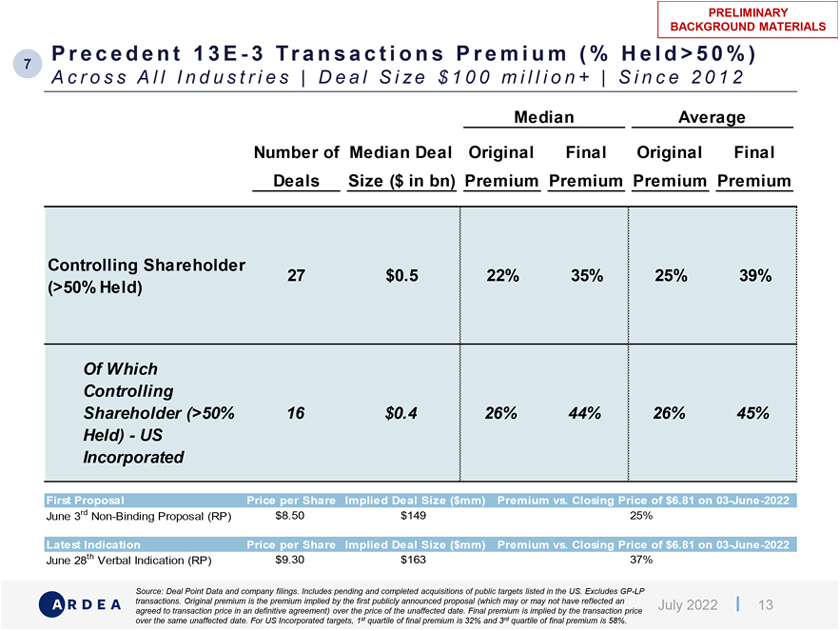

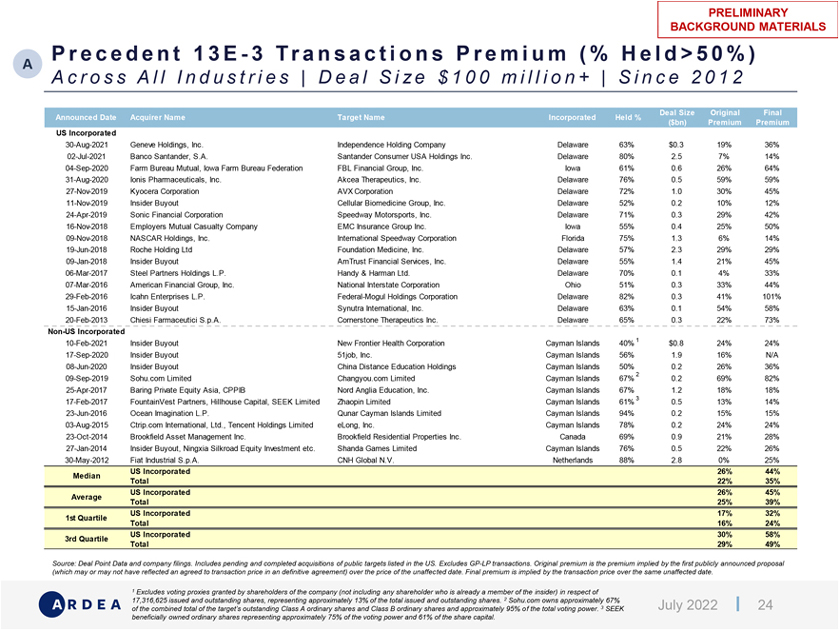

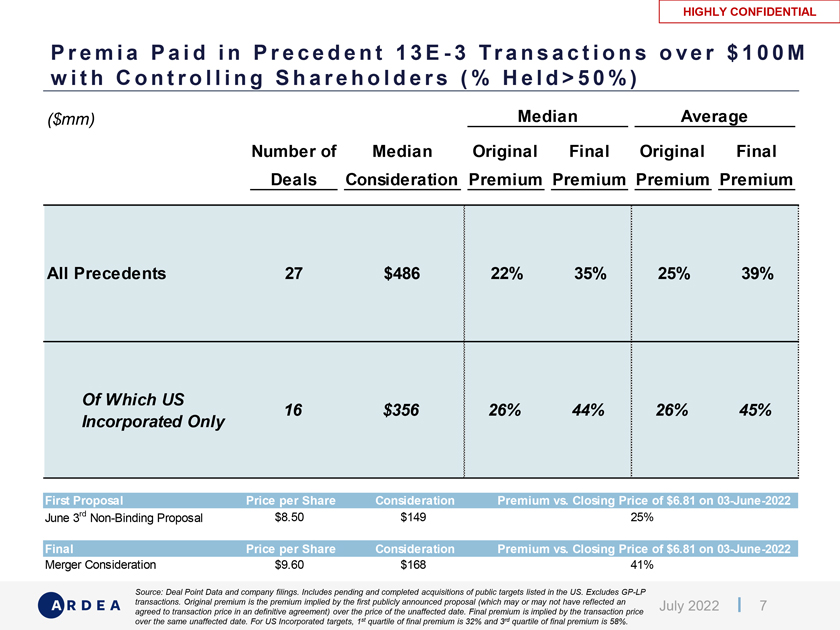

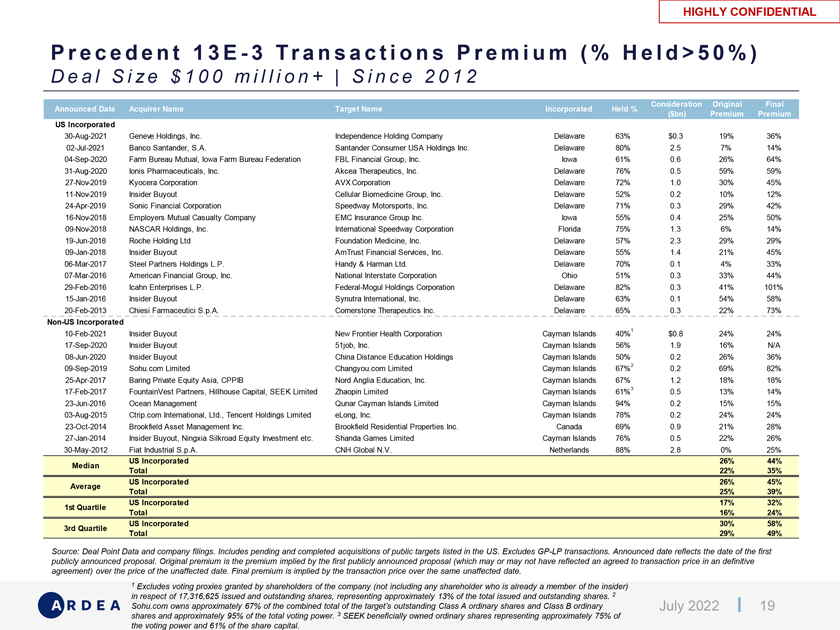

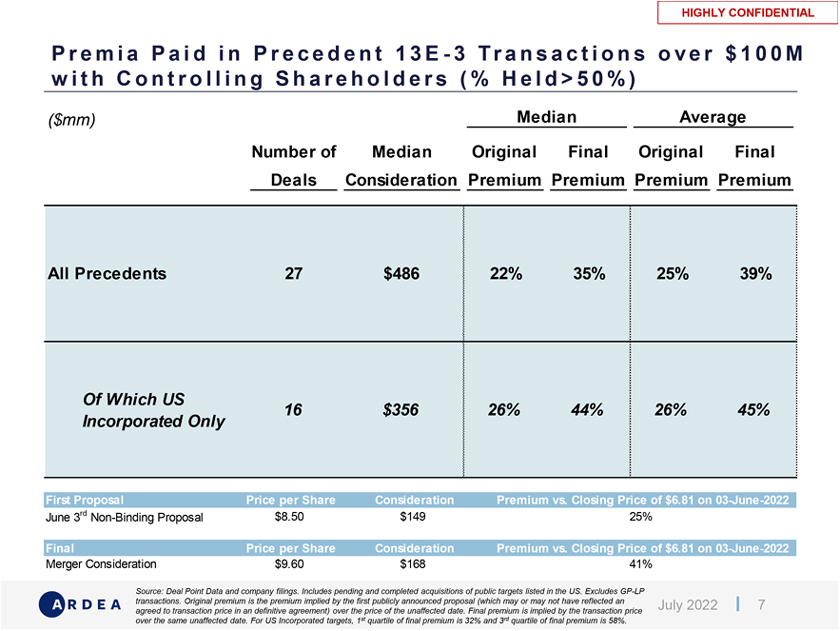

PRELIMINARY BACKGROUND MATERIALS Precedent 13 E-3 TRANSACTIONS Premium (% Held 50%) 4 Across All Industries | Deal Size $ 100 million + | Since 2012 Median Average Number of Median Deal Initial Final Initial Final Deals Size ($ in bn) Premium Premium Premium Premium Controlling Shareholder 27 $0.5 22% 35% 25% 39% (>50% Held) Of Which Controlling Shareholder (>50% 16 $0.4 26% 44% 26% 45% Held)—US Incorporated Source: Deal Point Data and company filings. Note: Deal size indicates total cost to acquirer, in billions, to purchase target common shares sought in transaction. Does not reflect aggregate implied equity value. Deal size based on 13E-3 filings. Includes pending and completed June 2022 9 acquisitions of public targets listed in the US. Excludes GP-LP transactions. “% held” indicates percentage of target’s common stock held per press releases or 13E-3 filings. Initial premium indicates the premium initially offered as of date identified as the unaffected date.

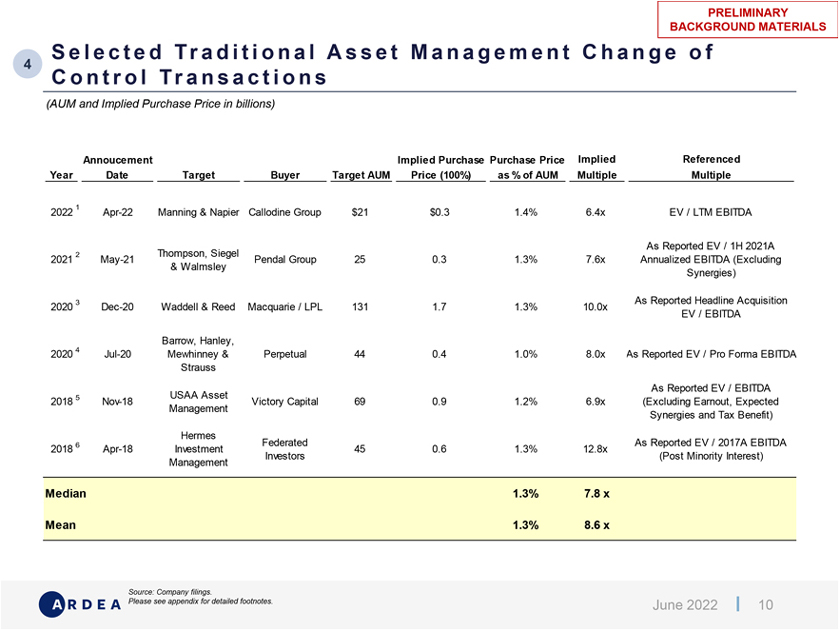

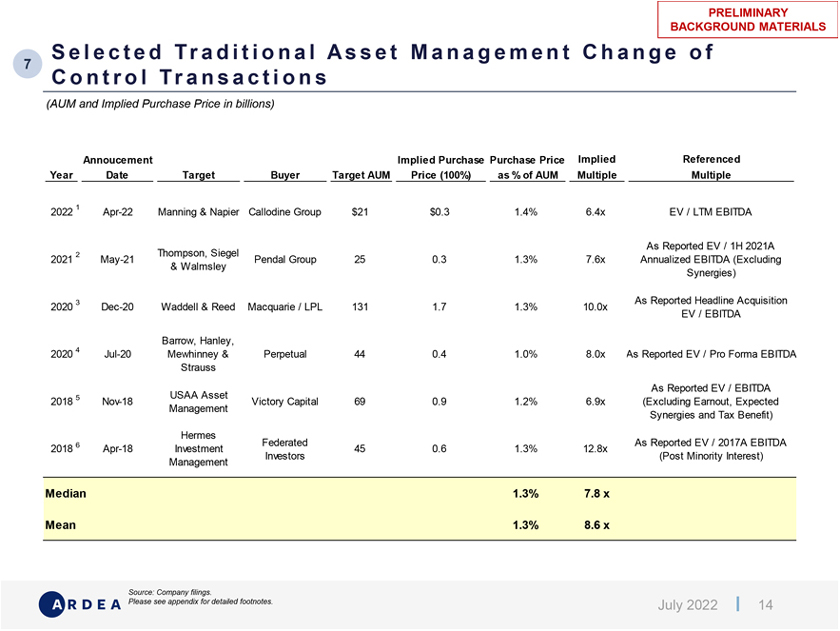

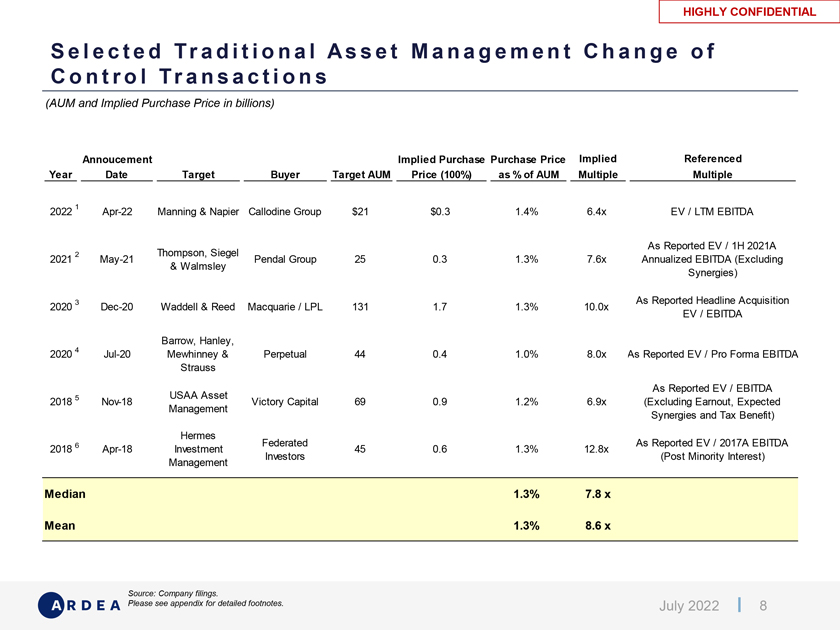

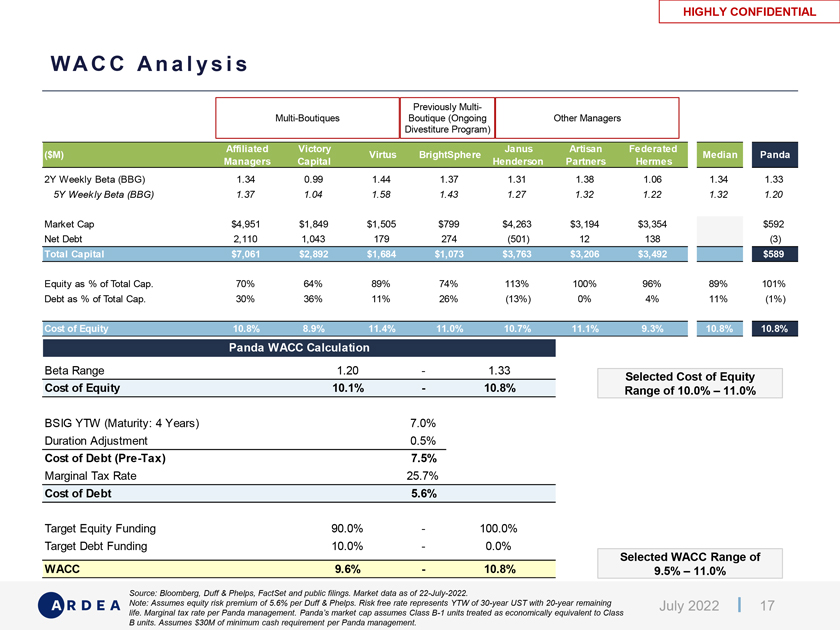

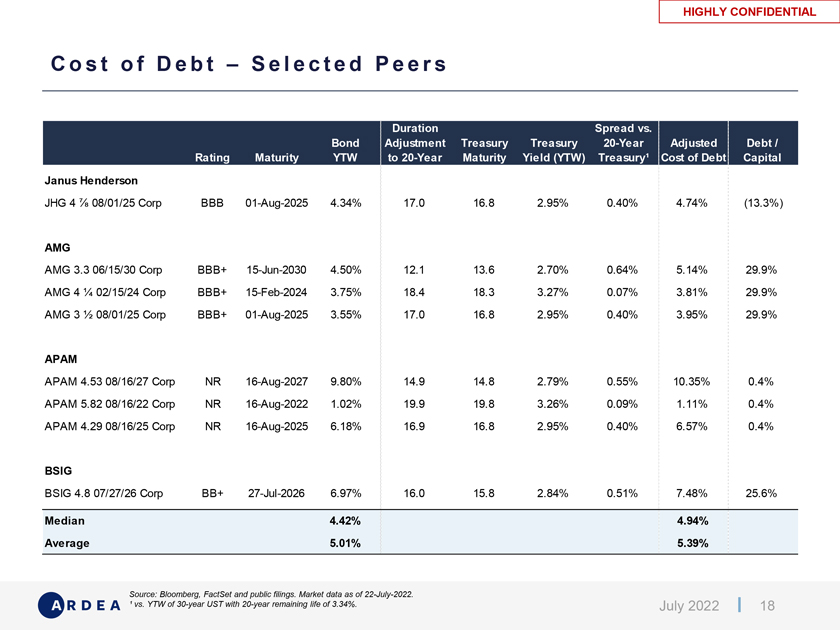

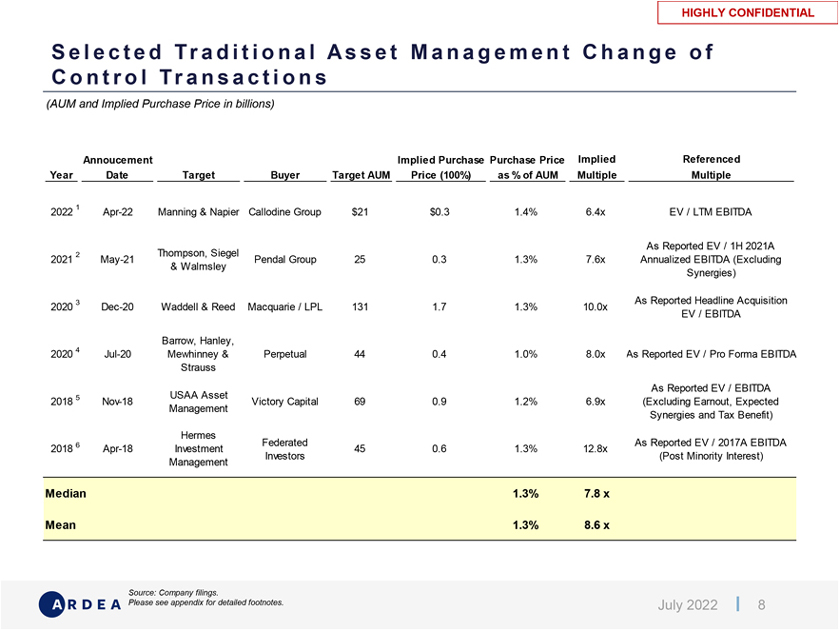

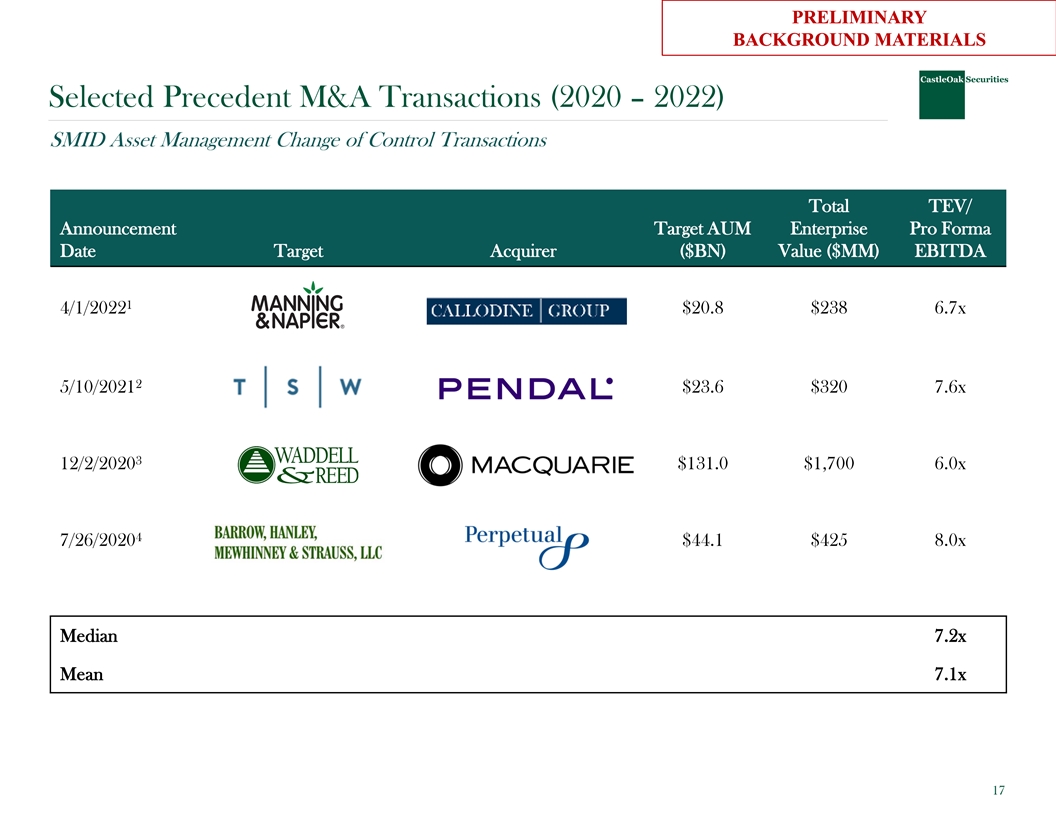

PRELIMINARY BACKGROUND MATERIALS Selected Traditional Asset Management Change of 4 Con trol Transactions (AUM and Implied Purchase Price in billions) Annoucement Implied Purchase Purchase Price Implied Referenced Year Date Target Buyer Target AUM Price (100%) as % of AUM Multiple Multiple 1 2022 Apr-22 Manning & Napier Callodine Group $21 $0.3 1.4% 6.4x EV / LTM EBITDA As Reported EV / 1H 2021A 2 Thompson, Siegel 2021 May-21 Pendal Group 25 0.3 1.3% 7.6x Annualized EBITDA (Excluding & Walmsley Synergies) 3 As Reported Headline Acquisition 2020 Dec-20 Waddell & Reed Macquarie / LPL 131 1.7 1.3% 10.0x EV / EBITDA Barrow, Hanley, 2020 4 Jul-20 Mewhinney & Perpetual 44 0.4 1.0% 8.0x As Reported EV / Pro Forma EBITDA Strauss As Reported EV / EBITDA 5 USAA Asset 2018 Nov-18 Victory Capital 69 0.9 1.2% 6.9x (Excluding Earnout, Expected Management Synergies and Tax Benefit) Hermes 6 Federated As Reported EV / 2017A EBITDA 2018 Apr-18 Investment 45 0.6 1.3% 12.8x Investors (Post Minority Interest) Management Median 1.3% 7.8 x Mean 1.3% 8.6 x Source: Company filings. Please see appendix for detailed footnotes. June 2022 10

PRELIMINARY BACKGROUND MATERIALS A Appendix June 2022 11

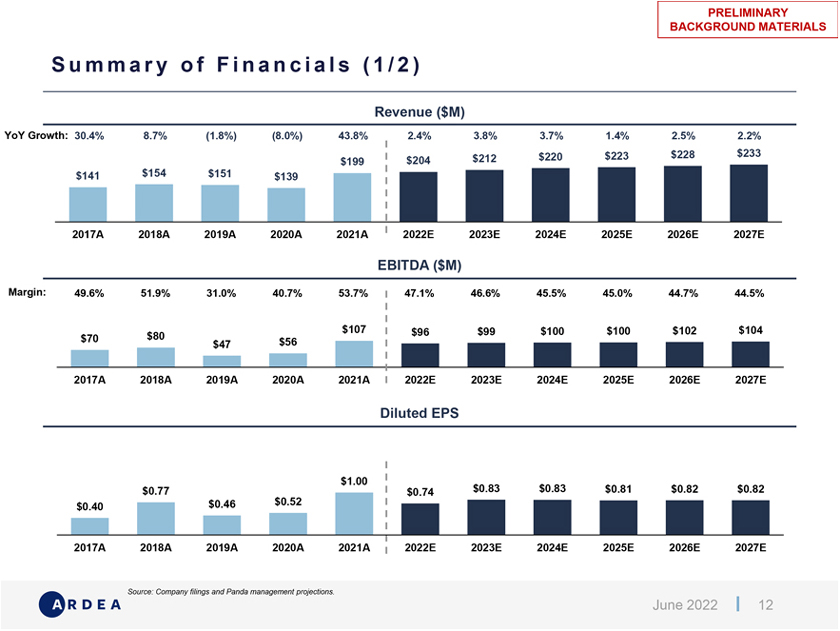

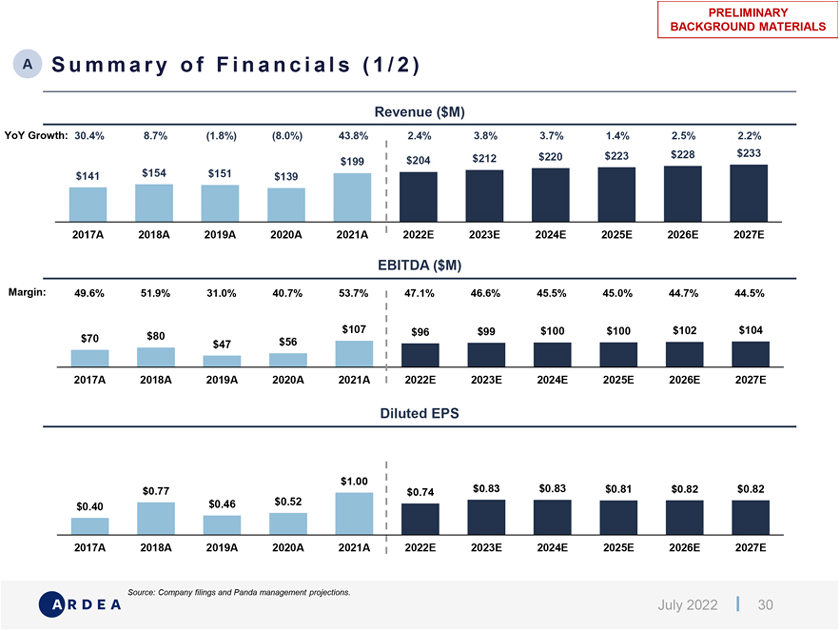

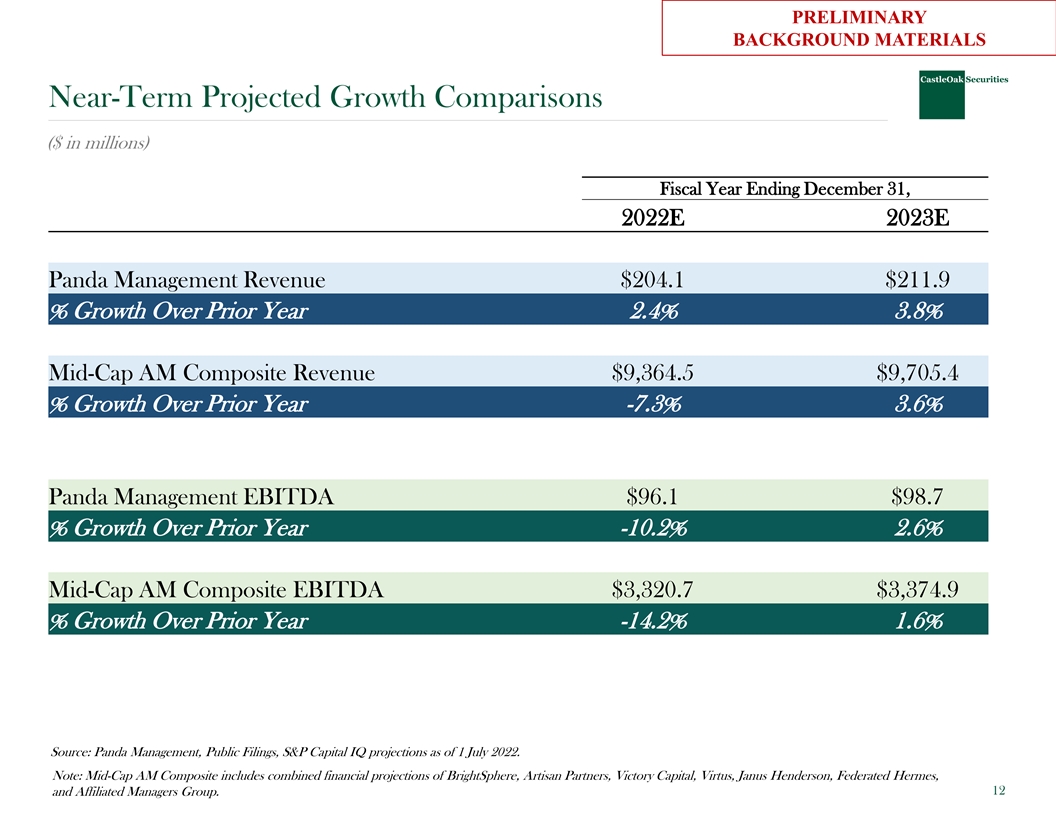

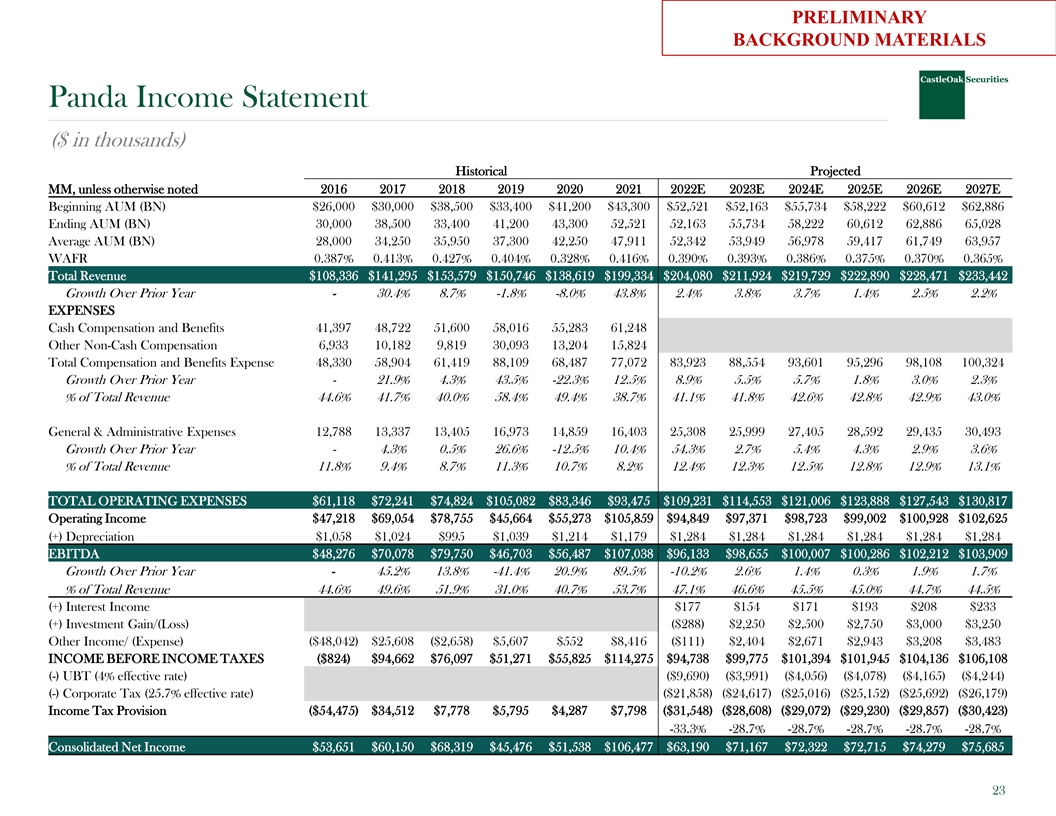

PRELIMINARY BACKGROUND MATERIALS Summary of Financials ( 1 / 2 ) Revenue ($M) YoY Growth: 30.4% 8.7% (1.8%) (8.0%) 43.8% 2.4% 3.8% 3.7% 1.4% 2.5% 2.2% $220 $223 $228 $233 $199 $204 $212 $141 $154 $151 $139 2017A 2018A 2019A 2020A 2021A 2022E 2023E 2024E 2025E 2026E 2027E EBITDA ($M) Margin: 49.6% 51.9% 31.0% 40.7% 53.7% 47.1% 46.6% 45.5% 45.0% 44.7% 44.5% $107 $96 $99 $100 $100 $102 $104 $70 $80 $47 $56 2017A 2018A 2019A 2020A 2021A 2022E 2023E 2024E 2025E 2026E 2027E Diluted EPS $1.00 $0.77 $0.74 $0.83 $0.83 $0.81 $0.82 $0.82 $0.46 $0.52 $0.40 2017A 2018A 2019A 2020A 2021A 2022E 2023E 2024E 2025E 2026E 2027E Source: Company filings and Panda management projections. June 2022 12

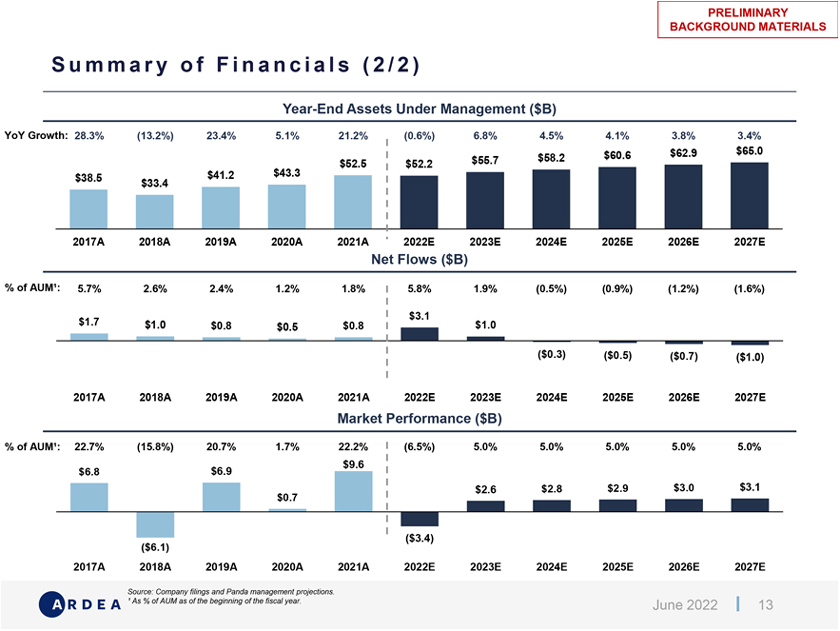

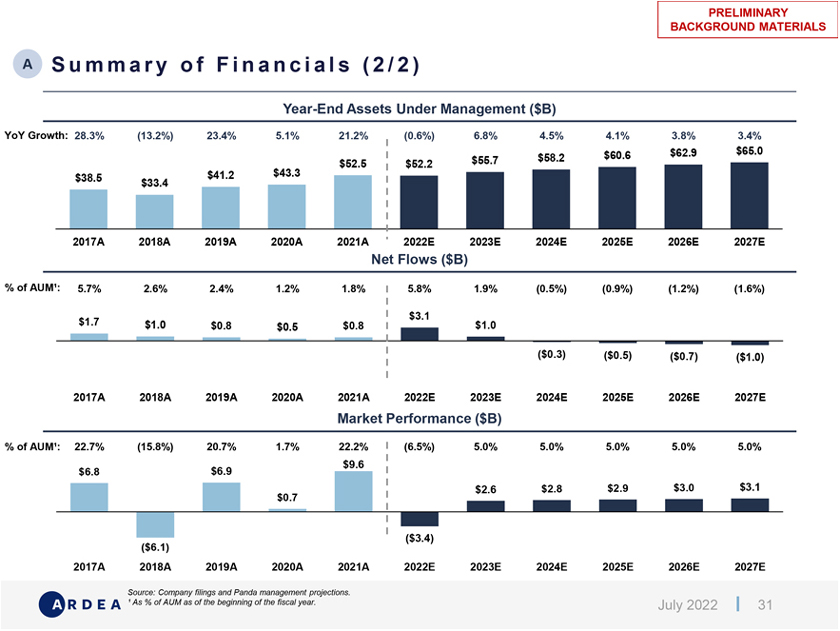

PRELIMINARY BACKGROUND MATERIALS Summary of Financials ( 2 / 2 ) Year-End Assets Under Management ($B) YoY Growth: 28.3% (13.2%) 23.4% 5.1% 21.2% (0.6%) 6.8% 4.5% 4.1% 3.8% 3.4% $60.6 $62.9 $65.0 $55.7 $58.2 $43.3 $52.5 $52.2 $38.5 $41.2 $33.4 2017A 2018A 2019A 2020A 2021A 2022E 2023E 2024E 2025E 2026E 2027E Net Flows ($B) % of AUM¹: 5.7% 2.6% 2.4% 1.2% 1.8% 5.8% 1.9% (0.5%) (0.9%) (1.2%) (1.6%) $3.1 $1.7 $1.0 $0.8 $0.8 $1.0 $0.5 ($0.3) ($0.5) ($0.7) ($1.0) 2017A 2018A 2019A 2020A 2021A 2022E 2023E 2024E 2025E 2026E 2027E Market Performance ($B) % of AUM¹: 22.7% (15.8%) 20.7% 1.7% 22.2% (6.5%) 5.0% 5.0% 5.0% 5.0% 5.0% $9.6 $6.8 $6.9 $2.6 $2.8 $2.9 $3.0 $3.1 $0.7 ($6.1) ($3.4) 2017A 2018A 2019A 2020A 2021A 2022E 2023E 2024E 2025E 2026E 2027E Source: Company filings and Panda management projections. ¹ As % of AUM as of the beginning of the fiscal year. June 2022 13

PRELIMINARY BACKGROUND MATERIALS Precedent 13 E—3 Transactions Premium ( % Held > 5 0 % ) Across All Industries | Deal Size $ 1 0 0 million + | Since 2012 US Incorporated 30-Aug-2021 Geneve Holdings, Inc. Independence Holding Company Delaware 63% $0.3 19% 36% 02-Jul-2021 Banco Santander, S.A. Santander Consumer USA Holdings Inc. Delaware 80% 2.5 7% 14% 04-Sep-2020 Farm Bureau Mutual, Iowa Farm Bureau Federation FBL Financial Group, Inc. Iowa 61% 0.6 26% 64% 31-Aug-2020 Ionis Pharmaceuticals, Inc. Akcea Therapeutics, Inc. Delaware 76% 0.5 59% 59% 27-Nov-2019 Kyocera Corporation AVX Corporation Delaware 72% 1.0 30% 45% 11-Nov-2019 Insider Buyout Cellular Biomedicine Group, Inc. Delaware 52% 0.2 10% 12% 24-Apr-2019 Sonic Financial Corporation Speedway Motorsports, Inc. Delaware 71% 0.3 29% 42% 16-Nov-2018 Employers Mutual Casualty Company EMC Insurance Group Inc. Iowa 55% 0.4 25% 50% 09-Nov-2018 NASCAR Holdings, Inc. International Speedway Corporation Florida 75% 1.3 6% 14% 19-Jun-2018 Roche Holding Ltd Foundation Medicine, Inc. Delaware 57% 2.3 29% 29% 09-Jan-2018 Insider Buyout AmTrust Financial Services, Inc. Delaware 55% 1.4 21% 45% 06-Mar-2017 Steel Partners Holdings L.P. Handy & Harman Ltd. Delaware 70% 0.1 4% 33% 07-Mar-2016 American Financial Group, Inc. National Interstate Corporation Ohio 51% 0.3 33% 44% 29-Feb-2016 Icahn Enterprises L.P. Federal-Mogul Holdings Corporation Delaware 82% 0.3 41% 101% 15-Jan-2016 Insider Buyout Synutra International, Inc. Delaware 63% 0.1 54% 58% 20-Feb-2013 Chiesi Farmaceutici S.p.A. Cornerstone Therapeutics Inc. Delaware 65% 0.3 22% 73% Non-US Incorporated 10-Feb-2021 Insider Buyout New Frontier Health Corporation Cayman Islands 40%1 $0.8 24% 24% 17-Sep-2020 Insider Buyout 51job, Inc. Cayman Islands 56% 1.9 16% N/A 08-Jun-2020 Insider Buyout China Distance Education Holdings Cayman Islands 50% 0.2 26% 36% 09-Sep-2019 Sohu.com Limited Changyou.com Limited Cayman Islands 67%2 0.2 69% 82% 25-Apr-2017 Baring Private Equity Asia, CPPIB Nord Anglia Education, Inc. Cayman Islands 67% 1.2 18% 18% 17-Feb-2017 FountainVest Partners, Hillhouse Capital, SEEK Limited Zhaopin Limited Cayman Islands 61%3 0.5 13% 14% 23-Jun-2016 Ocean Imagination L.P. Qunar Cayman Islands Limited Cayman Islands 94% 0.2 15% 15% 03-Aug-2015 Ctrip.com International, Ltd., Tencent Holdings Limited eLong, Inc. Cayman Islands 78% 0.2 24% 24% 23-Oct-2014 Brookfield Asset Management Inc. Brookfield Residential Properties Inc. Canada 69% 0.9 21% 28% 27-Jan-2014 Insider Buyout, Ningxia Silkroad Equity Investment etc. Shanda Games Limited Cayman Islands 76% 0.5 22% 26% 30-May-2012 Fiat Industrial S.p.A. CNH Global N.V. Netherlands 88% 2.8 0% 25% US Incorporated 26% 44% Median Total 22% 35% US Incorporated 26% 45% Average Total 25% 39% Source: Deal Point Data and company filings. Note: Deal size indicates total cost to acquirer, in billions, to purchase target common shares sought in transaction. Does not reflect aggregate implied equity value. Deal size based on 13E-3 filings. Includes pending and completed acquisitions of public targets listed in the US. Excludes GP-LP transactions. “% held” indicates percentage of target’s common stock held per press releases or 13E-3 filings. Initial premium indicates the premium initially offered as of date identified as the unaffected date. 1 Excludes voting proxies granted by shareholders of the company (not including any shareholder who is already a member of the insider) in respect of 17,316,625 issued and outstanding shares, representing approximately 13% of the total issued and outstanding shares. 2 Sohu.com owns approximately 67% of the combined total of the target’s outstanding Class A ordinary shares and Class B ordinary shares and approximately 95% of the total voting power. 3 SEEK June 2022 14 beneficially owned ordinary shares representing approximately 75% of the voting power and 61% of the share capital.

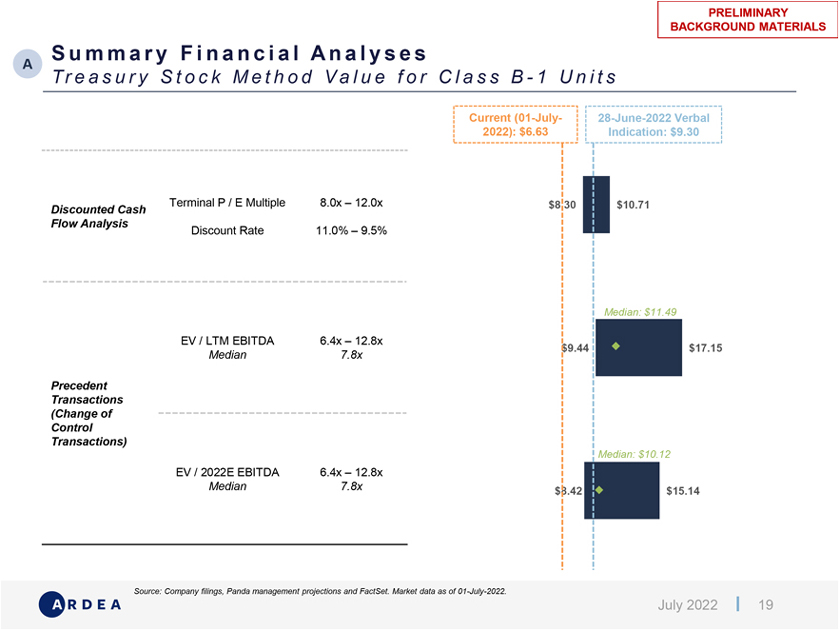

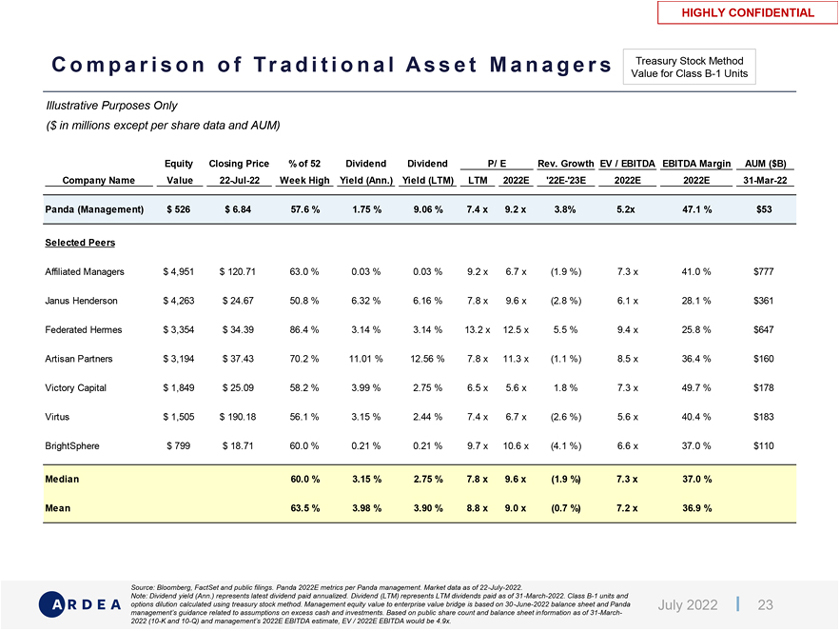

PRELIMINARY BACKGROUND MATERIALS Comparison of Traditional Asset Managers Illustrative Purposes Only Treasury Stock ($ in millions except per share data and AUM) Method for Class B-1 Units Equity Closing Price % of 52 Dividend P/ E Rev. Growth EV / EBITDA EBITDA Margin AUM ($B) Company Name Value 16-Jun-22 Week High Yield 2022E ‘22E-‘23E 2022E 2022E 31-Mar-22 Panda (Management) $ 483 $ 6.25 52.5 % 1.92 % 8.4 x 3.8% 4.8x 47.1 % $53 Selected Peers Affiliated Managers $ 4,641 $ 113.52 59.2 % 0.04 % 6.1 x 1.3 % 6.7 x 42.4 % $777 Janus Henderson $ 4,010 $ 23.21 47.8 % 6.72 % 7.9 x 1.8 % 5.0 x 30.3 % $361 Artisan Partners $ 2,903 $ 34.02 63.6 % 12.11 % 9.0 x 5.9 % 7.0 x 36.8 % $160 Federated Hermes $ 2,837 $ 29.09 73.1 % 3.71 % 10.2 x 6.5 % 7.9 x 25.9 % $647 Victory Capital $ 1,840 $ 24.97 57.9 % 4.00 % 5.1 x 3.8 % 6.9 x 49.9 % $178 Virtus $ 1,333 $ 168.44 49.7 % 3.56 % 5.4 x 1.5 % 4.7 x 41.1 % $183 BrightSphere $ 774 $ 18.16 58.3 % 0.22 % 9.5 x 1.0 % 6.0 x 38.8 % $110 Median 58.3 % 3.71 % 7.9 x 1.8 % 6.7 x 38.8 % Mean 58.5 % 4.34 % 7.6 x 3.1 % 6.3 x 37.9 % Source: Bloomberg, FactSet and public filings. Panda 2022E metrics per company management. Market data as of 16-June-2022. Note: Dividend yield represents latest quarter annualized. Class B-1 units treated using treasury stock method. Management equity value to enterprise value bridge is based on 31-May-2022 balance sheet and Panda management’s guidance related to assumptions on excess cash and investments. June 2022 15 Based on public share count and balance sheet information as of 31-Mar-2022 (10-K and 10-Q) and management’s 2022E EBITDA estimate, EV / 2022E EBITDA would be 4.4x.

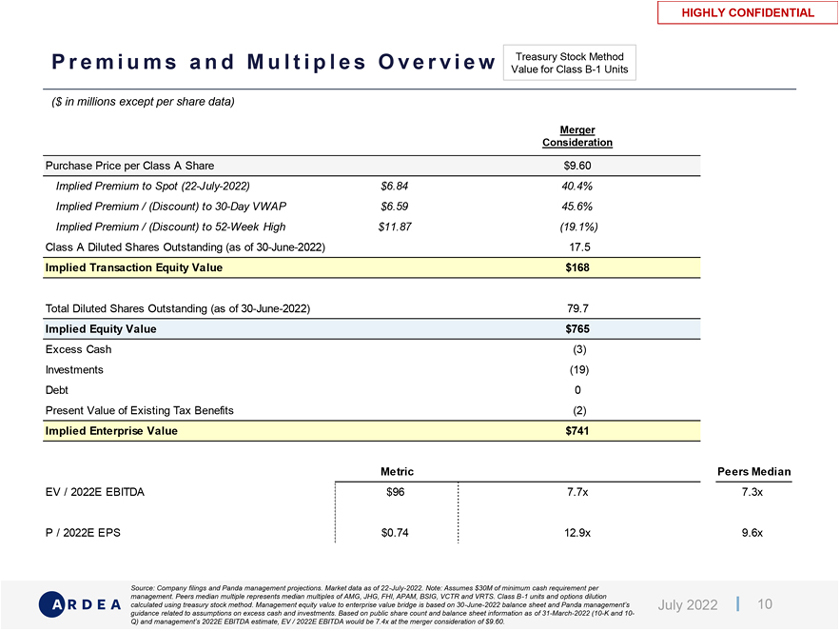

PRELIMINARY BACKGROUND MATERIALS Premium sand Multiples Overview ($ in millions except per share data) Treasury Stock June 3 Non- June 15 Non- Method for Class Binding Biding B-1 Units Current Proposal (RP) Proposal (LP) Purchase Price per Class A Share $6.25 $8.50 $7.30 Implied Premium to Spot (16-Jun-2022) $6.25 0.0% 36.0% 16.8% Implied Premium / (Discount) to 30-Day VWAP $6.53 (4.2%) 30.2% 11.8% Implied Premium / (Discount) to 52-Week High $11.91 (47.5%) (28.6%) (38.7%) Stated Premium to Closing Price of the Bid Date 24.8% 17.9% Class A Shares Outstanding (as of 31-May-2022) 16.8 16.8 16.8 Implied Purchase Price for Class A Shares $105 $143 $123 Total Diluted Shares Outstanding (as of 31-May-2022) 76.9 78.0 76.9 Implied Equity Value $481 $663 $562 Excess Cash 0 0 0 Investments (21) (21) (21) Debt 0 0 0 Present Value of Existing Tax Benefits (2) (2) (2) Implied Enterprise Value $457 $640 $538 Metric Implied Panda Multiple Peers Median EV / 2022E EBITDA (Management) $96 4.8x 6.7x 5.6x 6.7x P / 2022E EPS $0.74 8.4x 11.5x 9.8x 7.9x Source: Company filings. Panda management projections. Market data as of 16-June-2022. Note: Peers median multiples represent median multiples of AMG, JHG, FHI, APAM, BSIG, VCTR and VRTS. Class B-1 units and options dilution calculated using treasury stock method. Management equity 16 value to enterprise value bridge is based on 31-May-2022 balance sheet and Panda management’s guidance related to assumptions on excess cash June 2022 and investments. Based on public share count and balance sheet information as of 31-Mar-2022 (10-K and 10-Q) and management’s 2022E EBITDA estimate, EV / 2022E EBITDA would be 4.4x, 6.3x and 5.3x at a share price of $6.25, $8.50 and $7.30 respectively.

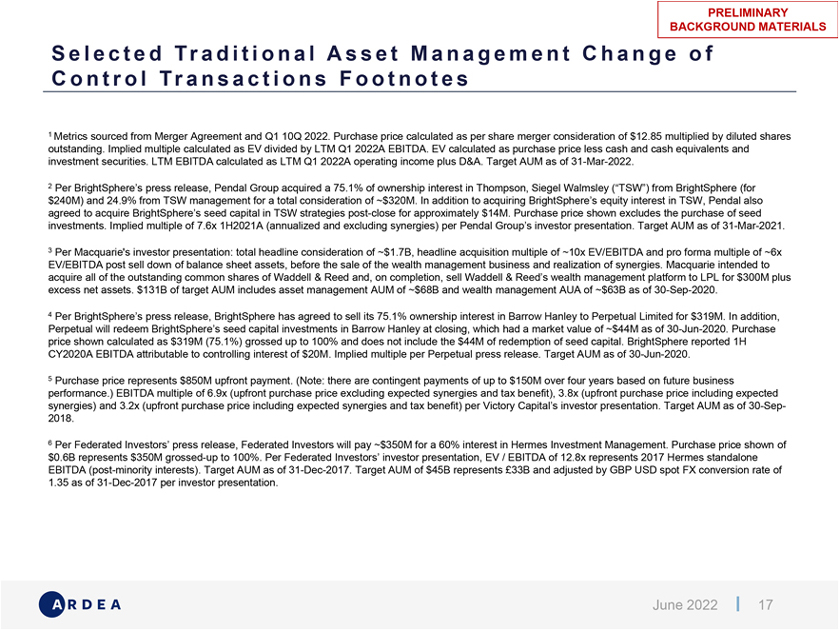

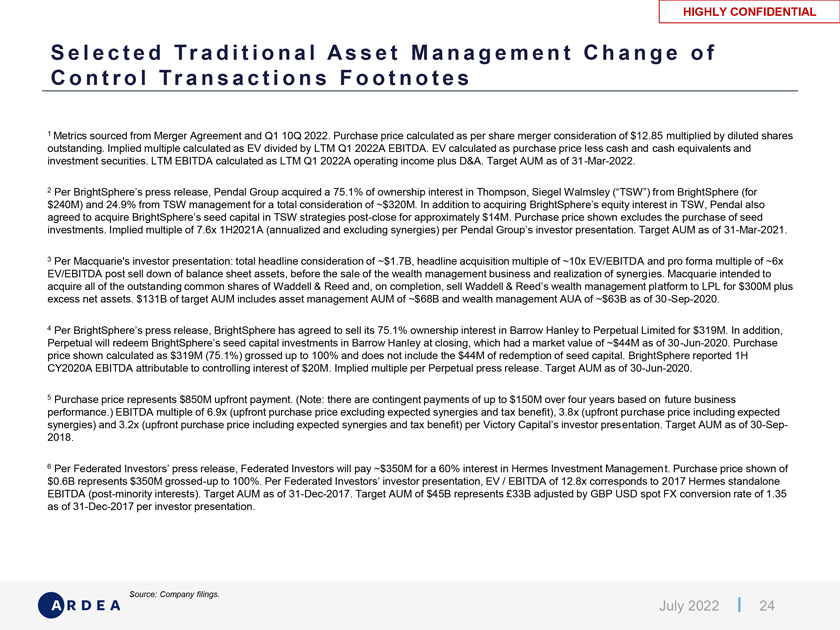

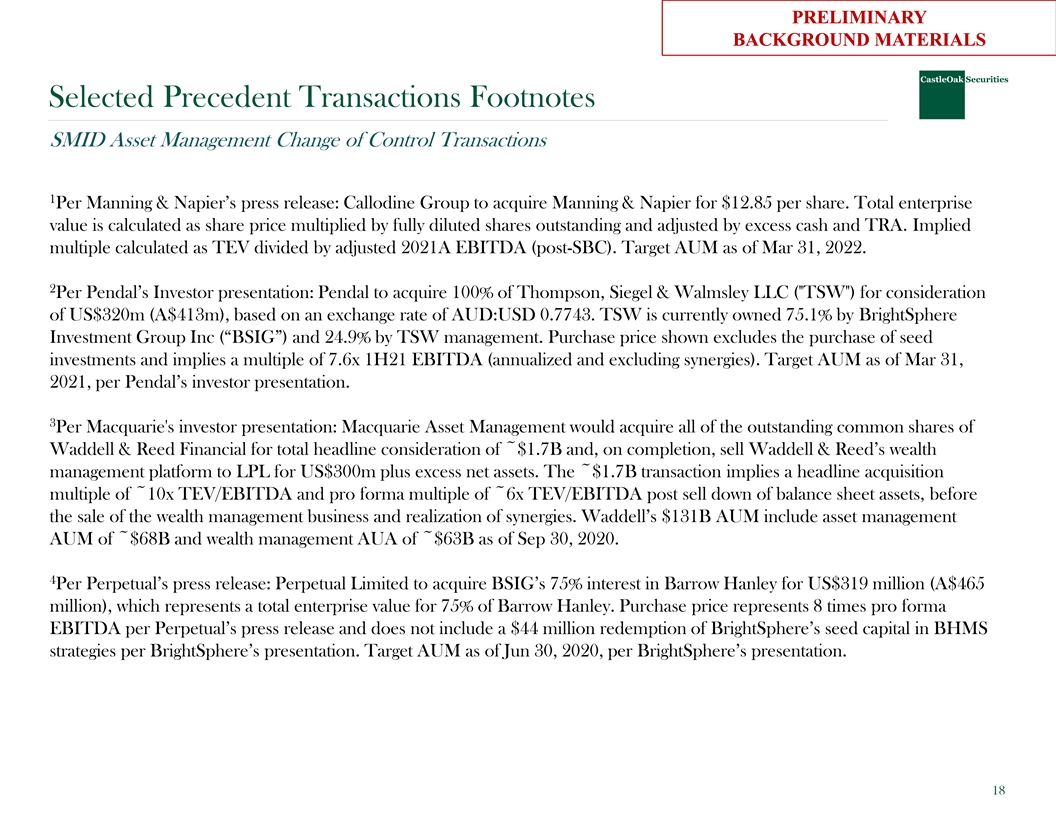

PRELIMINARY BACKGROUND MATERIALS Selected Traditional Asset Management Change of Control Transactions Footnotes 1 Metrics sourced from Merger Agreement and Q1 10Q 2022. Purchase price calculated as per share merger consideration of $12.85 multiplied by diluted shares outstanding. Implied multiple calculated as EV divided by LTM Q1 2022A EBITDA. EV calculated as purchase price less cash and cash equivalents and investment securities. LTM EBITDA calculated as LTM Q1 2022A operating income plus D&A. Target AUM as of 31-Mar-2022. 2 Per BrightSphere’s press release, Pendal Group acquired a 75.1% of ownership interest in Thompson, Siegel Walmsley (“TSW”) from BrightSphere (for $240M) and 24.9% from TSW management for a total consideration of $320M. In addition to acquiring BrightSphere’s equity interest in TSW, Pendal also agreed to acquire BrightSphere’s seed capital in TSW strategies post-close for approximately $14M. Purchase price shown excludes the purchase of seed investments. Implied multiple of 7.6x 1H2021A (annualized and excluding synergies) per Pendal Group’s investor presentation. Target AUM as of 31-Mar-2021. 3 Per Macquarie’s investor presentation: total headline consideration of $1.7B, headline acquisition multiple of 10x EV/EBITDA and pro forma multiple of 6x EV/EBITDA post sell down of balance sheet assets, before the sale of the wealth management business and realization of synergies. Macquarie intended to acquire all of the outstanding common shares of Waddell & Reed and, on completion, sell Waddell & Reed’s wealth management platform to LPL for $300M plus excess net assets. $131B of target AUM includes asset management AUM of $68B and wealth management AUA of $63B as of 30-Sep-2020. 4 Per BrightSphere’s press release, BrightSphere has agreed to sell its 75.1% ownership interest in Barrow Hanley to Perpetual Limited for $319M. In addition, Perpetual will redeem BrightSphere’s seed capital investments in Barrow Hanley at closing, which had a market value of $44M as of 30-Jun-2020. Purchase price shown calculated as $319M (75.1%) grossed up to 100% and does not include the $44M of redemption of seed capital. BrightSphere reported 1H CY2020A EBITDA attributable to controlling interest of $20M. Implied multiple per Perpetual press release. Target AUM as of 30-Jun-2020. 5 Purchase price represents $850M upfront payment. (Note: there are contingent payments of up to $150M over four years based on future business performance.) EBITDA multiple of 6.9x (upfront purchase price excluding expected synergies and tax benefit), 3.8x (upfront purchase price including expected synergies) and 3.2x (upfront purchase price including expected synergies and tax benefit) per Victory Capital’s investor presentation. Target AUM as of 30-Sep-2018. 6 Per Federated Investors’ press release, Federated Investors will pay $350M for a 60% interest in Hermes Investment Management. Purchase price shown of $0.6B represents $350M grossed-up to 100%. Per Federated Investors’ investor presentation, EV / EBITDA of 12.8x represents 2017 Hermes standalone EBITDA (post-minority interests). Target AUM as of 31-Dec-2017. Target AUM of $45B represents Ł33B and adjusted by GBP USD spot FX conversion rate of 1.35 as of 31-Dec-2017 per investor presentation. June 2022 17

DISCLAIMER Ardea Partners LP (“Ardea”) has prepared and provided these materials and Ardea’s related oral presentation (collectively, the “Confidential Information”) solely for the information and assistance of the Special Committee of the Board of Directors of Panda (the “Company”) in connection with their consideration of the matters referred to herein. Without Ardea’s prior written consent, the Confidential Information, and Ardea’s preparation and provision of such Confidential Information, may not be used for any other purpose or disclosed or otherwise referred to in any manner. The Confidential Information is (a) for discussion purposes only and (b) speaks only as of the date it is given, reflecting prevailing economic, monetary, market and other conditions as in effect on, and the information made available to Ardea as of, such date. Ardea assumes no responsibility for updating or revising the Confidential Information. The views expressed herein are subject to change based upon a number of factors, including economic, monetary, market and other conditions and the Company’s and any prospective counterparty’s business and prospects. Analyses based upon forecasts of future results are not necessarily indicative of actual future results, which may be significantly more or less favorable than suggested by these analyses, and Ardea does not assume responsibility if future results are materially different from those forecast. The Confidential Information is incomplete without reference to, and should be viewed solely in conjunction with, the oral briefing provided by Ardea, if any. The Confidential Information has been prepared using publicly available information and information in reports, due diligence materials, forecasts, projections and other materials provided by or on behalf of the Company and/or any prospective counterparty. Ardea does not assume responsibility for and has relied on, without independent verification, the accuracy and completeness of such information. Ardea has not, and does not, provide advice for tax, legal, regulatory or accounting matters and the Company will remain solely responsible for all aspects of due diligence in connection with the Transaction and the commercial assumptions on which any advice provided by Ardea is based. The Confidential Information does not address the underlying business decision of the Company to engage in any transaction or the relative merits of any strategic alternatives referred to herein as compared to any other alternative that may be available to the Company. Ardea and its affiliates and/or their respective employees, as well as investment funds in which any of them may have a financial interest, may at any time, directly or indirectly, hold long or short positions and may trade or otherwise effect transactions for their own accounts or the accounts of customers, in debt or equity securities, senior loans and/or derivative products relating to the Company or its affiliates, potential parties to a Transaction and their affiliates or persons that are competitors, customers or suppliers of the Company. Nothing herein or any previous or existing relationship between the Company and Ardea will be deemed to create a fiduciary duty or fiduciary or agency relationship between Ardea and the Company, its security holders, affiliates, employees or creditors. June 2022 18

Exhibit (c)(2)

PRELIMINARY BACKGROUND MATERIALS Project Panda Presentation to the Special Committee of the Board of Directors July 6, 2022

Agenda Items–ª1 Summary of Proposals â–ª2 Summary Financial Analyses â–ª 3 Discounted Cash Flow Analysis â–ª4 Present Value of Future Share Price and Dividends â–ª5 Trading Overview â–ª 6 Premiums and Multiples Overview â–ª 7 Selected Financial Benchmarks â–ª A Appendix July 2022 2

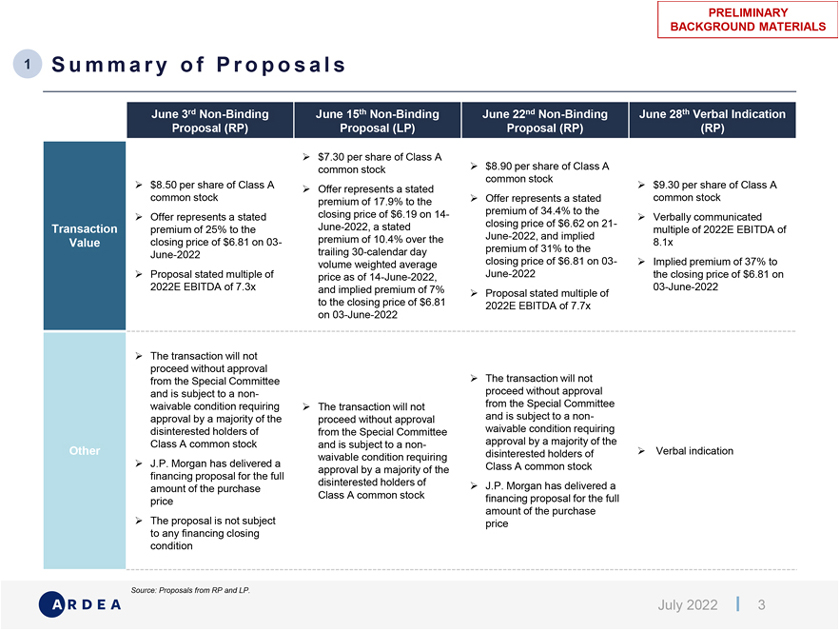

PRELIMINARY BACKGROUND MATERIALS 1 Summary of Proposals N June 3rd Non-Binding June 15th Non-Binding June 22nd Non-Binding June 28th Verbal Indication Proposal (RP) Proposal (LP) Proposal (RP) (RP) ? $7.30 per share of Class A ? $8.90 per share of Class A common stock common stock ? $8.50 per share of Class A ?Offer represents a stated ? $9.30 per share of Class A common stock premium of 17.9% to the ?Offer represents a stated common stock closing price of $6.19 on 14- premium of 34.4% to the ? Offer represents a stated ? Verbally communicated June-2022, a stated closing price of $6.62 on 21-Transaction premium of 25% to the multiple of 2022E EBITDA of premium of 10.4% over the June-2022, and implied Value closing price of $6.81 on 03- 8.1x trailing 30-calendar day premium of 31% to the June-2022 volume weighted average closing price of $6.81 on 03- ? Implied premium of 37% to ? Proposal stated multiple of price as of 14-June-2022, June-2022 the closing price of $6.81 on 2022E EBITDA of 7.3x and implied premium of 7% 03-June-2022 to the closing price of $6.81 ? Proposal stated multiple of on 03-June-2022 2022E EBITDA of 7.7x ? The transaction will not proceed without approval from the Special Committee ? The transaction will not and is subject to a non- proceed without approval waivable condition requiring ? The transaction will not from the Special Committee approval by a majority of the proceed without approval and is subject to a non-disinterested holders of from the Special Committee waivable condition requiring Class A common stock and is subject to a non- approval by a majority of the ? Other disinterested holders of Verbal indication waivable condition requiring ? J.P. Morgan has delivered a Class A common stock approval by a majority of the financing proposal for the full disinterested holders of ? J.P. Morgan has delivered a amount of the purchase Class A common stock financing proposal for the full price amount of the purchase ? The proposal is not subject price to any financing closing condition Source: Proposals from RP and LP. July 2022 3

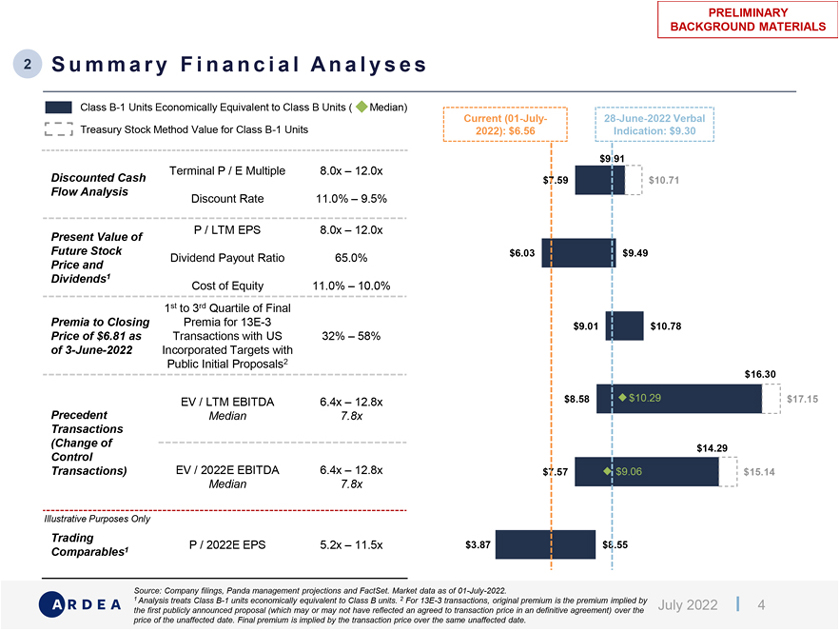

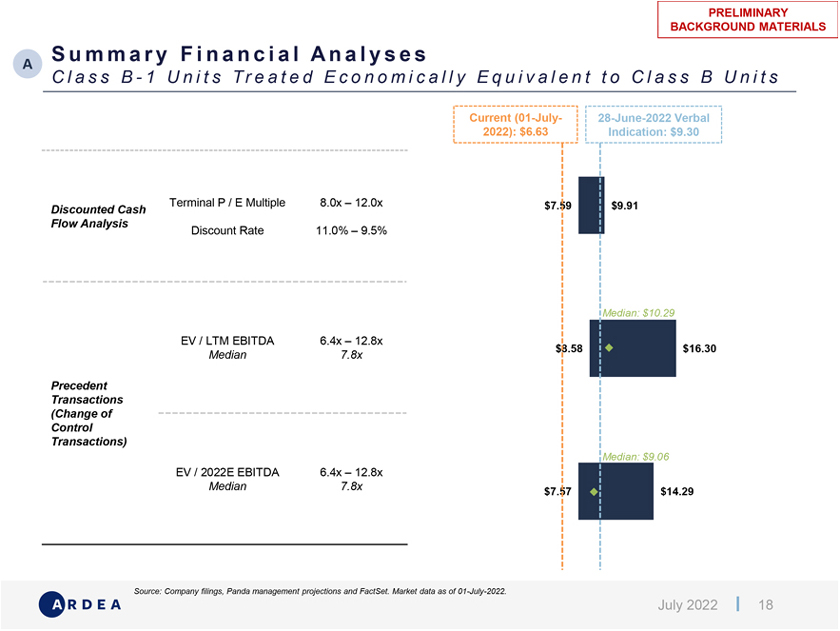

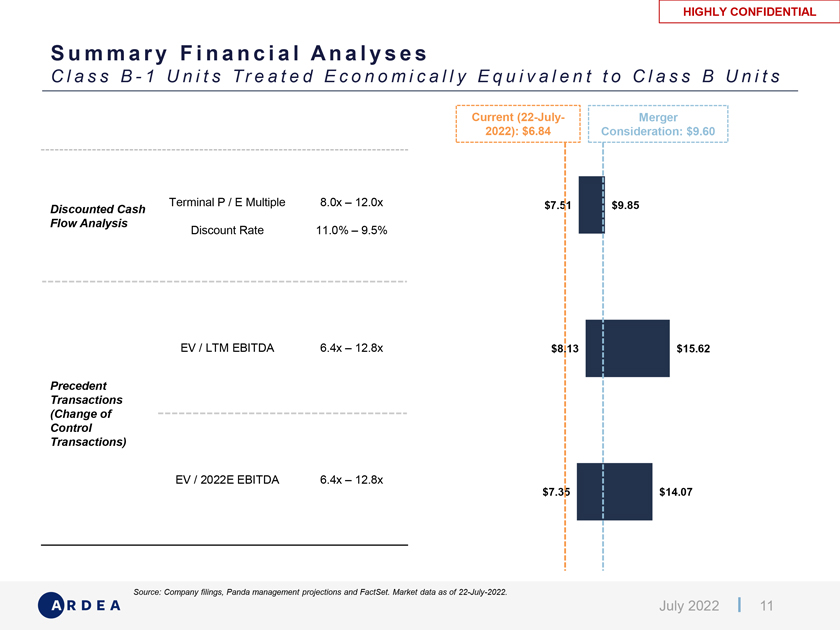

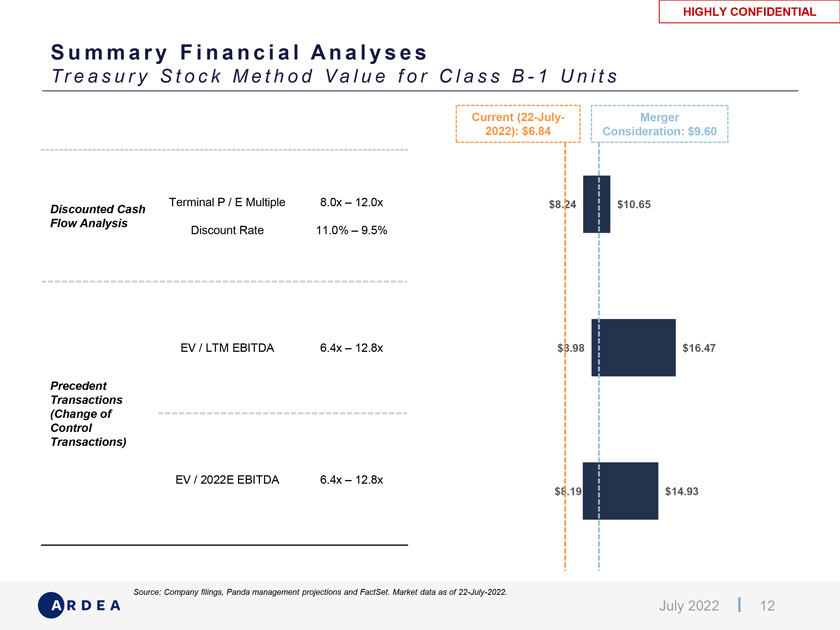

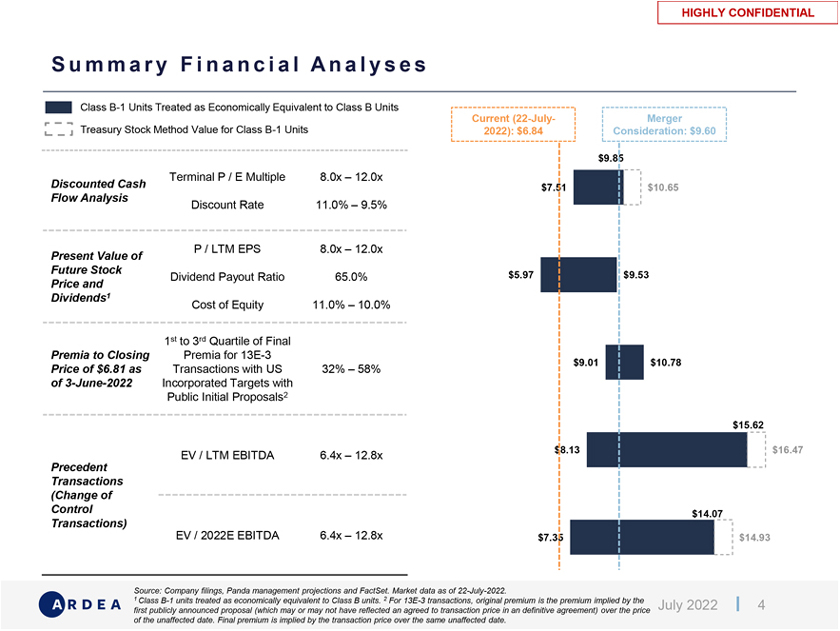

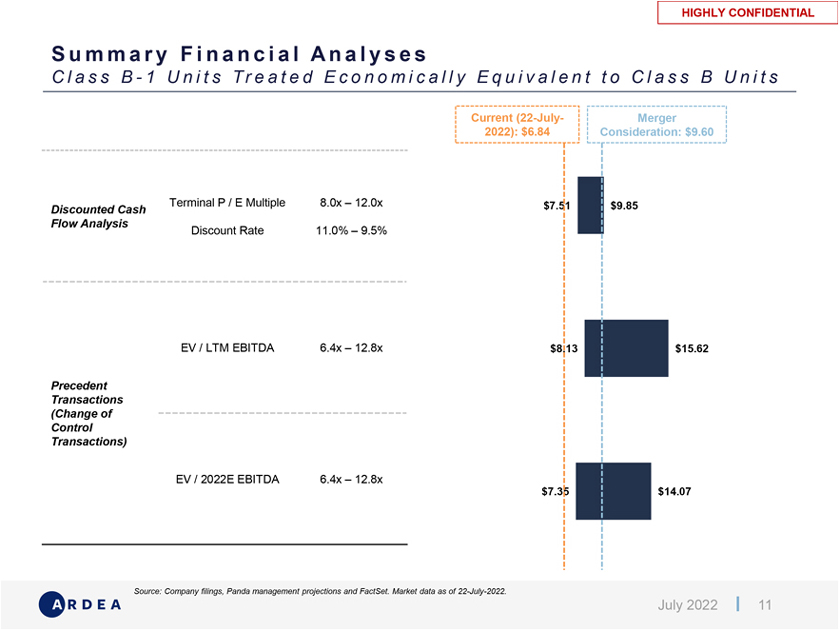

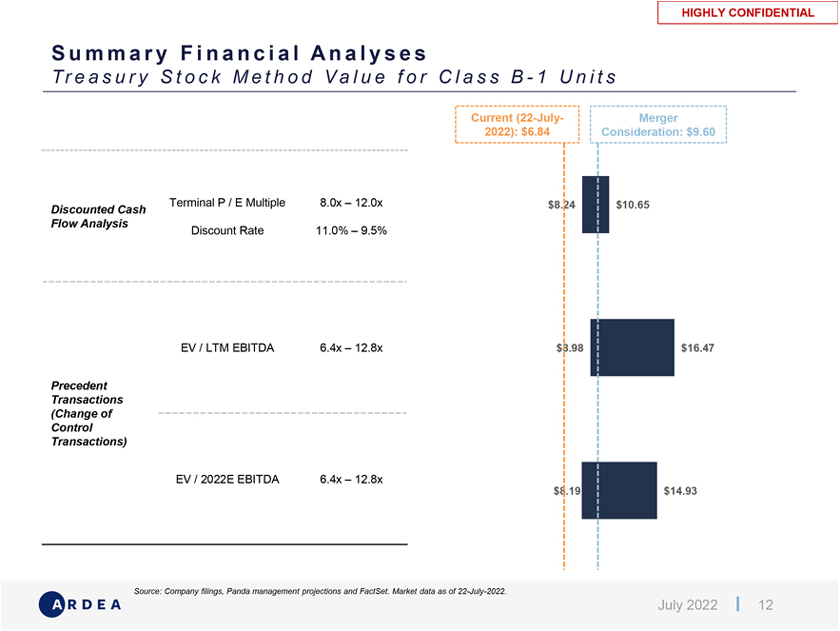

PRELIMINARY BACKGROUND MATERIALS 2 Summary Financial Analyses Class B-1 Units Economically Equivalent to Class B Units ( Median) Current (01-July- 28-June-2022 Verbal Treasury Stock Method Value for Class B-1 Units 2022): $6.56 Indication: $9.30 $9.91 Terminal P / E Multiple 8.0x – 12.0x Discounted Cash $7.59 $10.71 Flow Analysis Discount Rate 11.0% – 9.5% P / LTM EPS 8.0x – 12.0x Present Value of Future Stock $6.03 $9.49 Dividend Payout Ratio 65.0% Price and Dividends1 Cost of Equity 11.0% – 10.0% 1st to 3rd Quartile of Final Premia to Closing Premia for 13E-3 $9.01 $10.78 Price of $6.81 as Transactions with US 32% – 58% of 3-June-2022 Incorporated Targets with Public Initial Proposals2 $16.30 EV / LTM EBITDA 6.4x – 12.8x $8.58 $10.29 $17.15 Precedent Median 7.8x Transactions (Change of $14.29 Control Transactions) EV / 2022E EBITDA 6.4x – 12.8x $7.57 $9.06 $15.14 Median 7.8x Illustrative Purposes Only Trading P / 2022E EPS 5.2x – 11.5x $3.87 $8.55 Comparables1 Source: Company filings, Panda management projections and FactSet. Market data as of 01-July-2022. 1 Analysis treats Class B-1 units economically equivalent to Class B units. 2 For 13E-3 transactions, original premium is the premium implied by July 2022 4 the first publicly announced proposal (which may or may not have reflected an agreed to transaction price in an definitive agreement) over the price of the unaffected date. Final premium is implied by the transaction price over the same unaffected date.

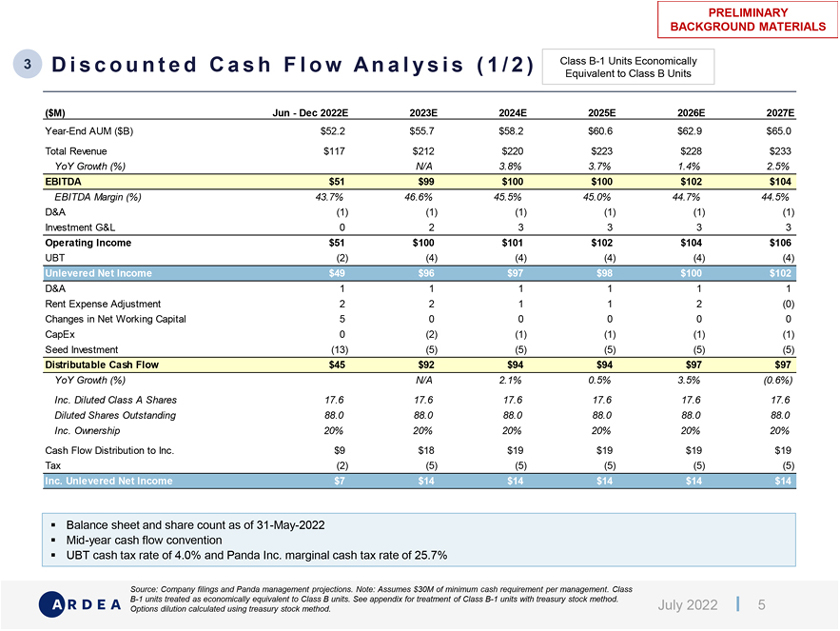

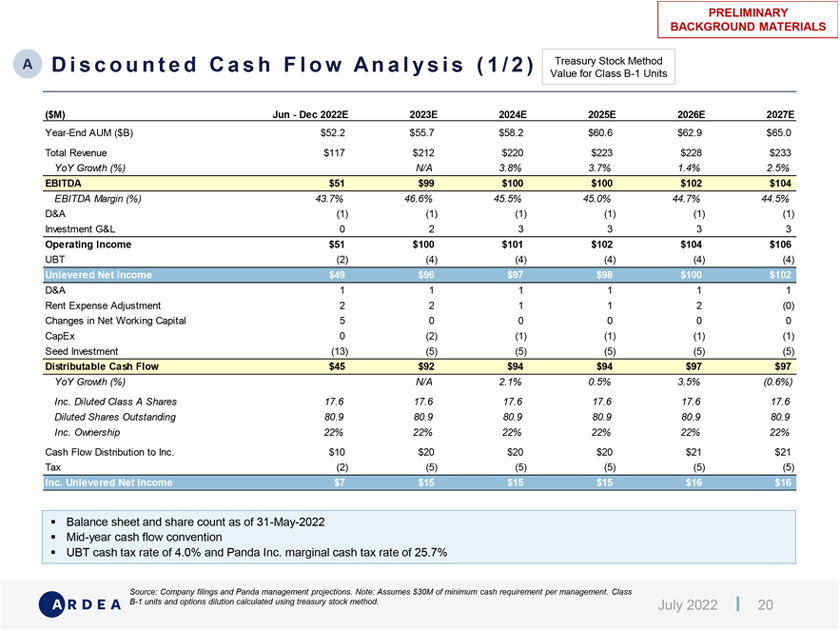

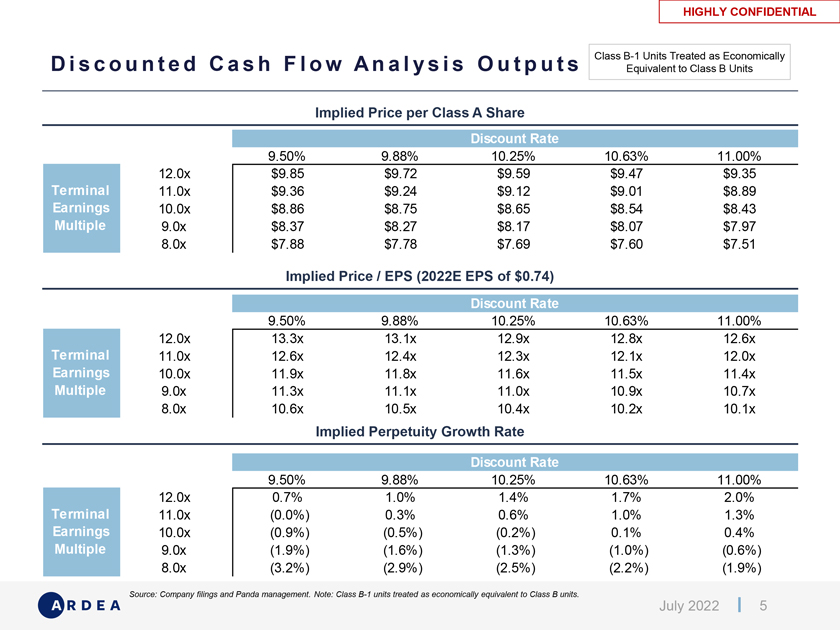

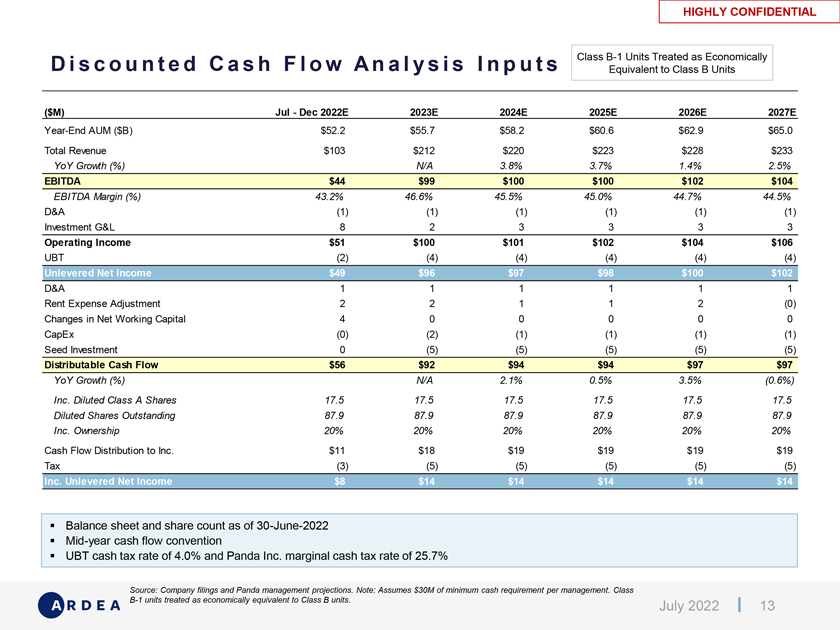

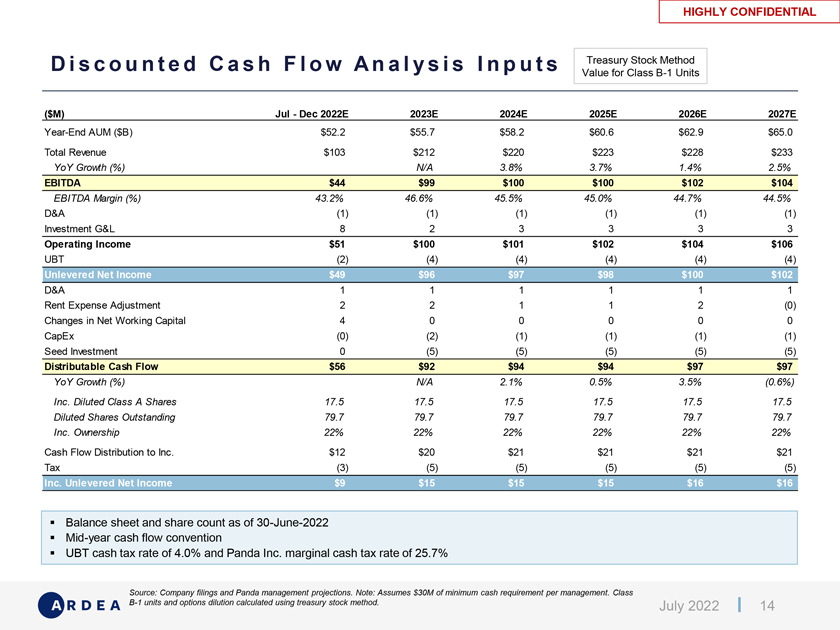

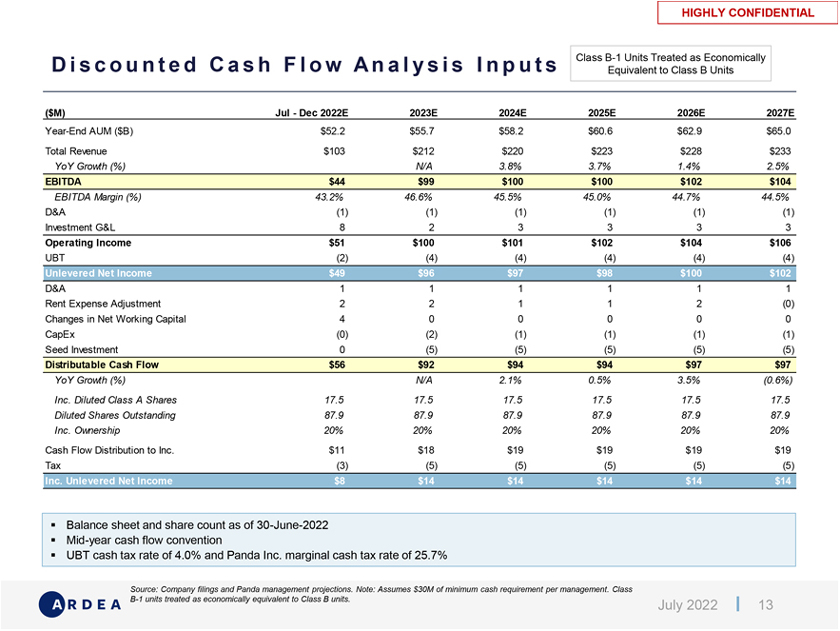

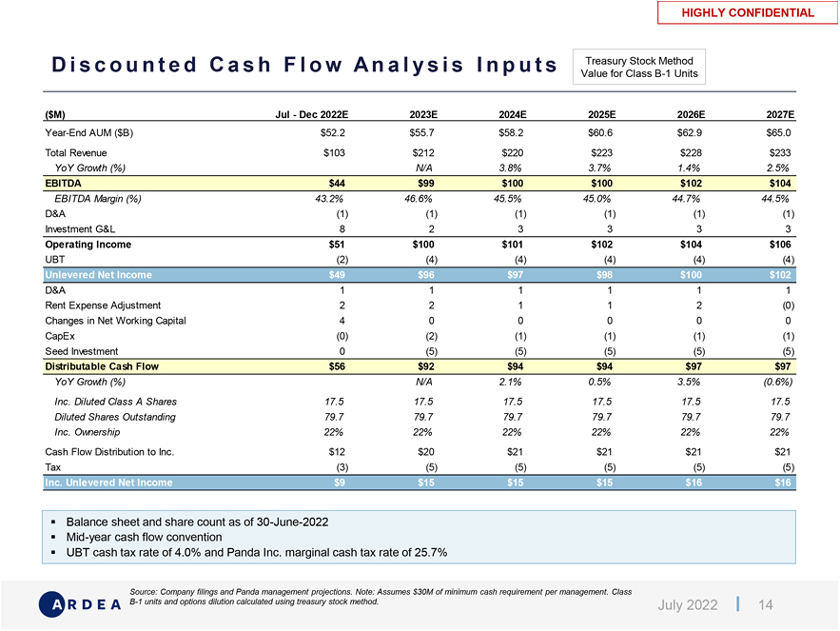

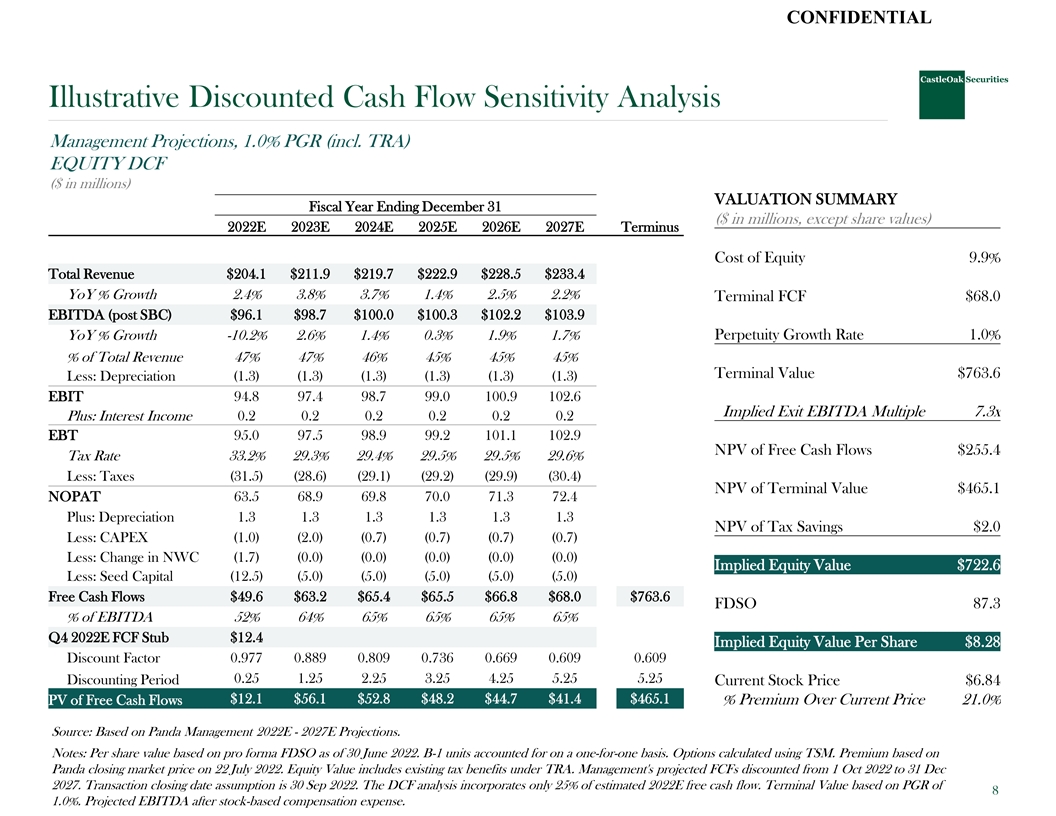

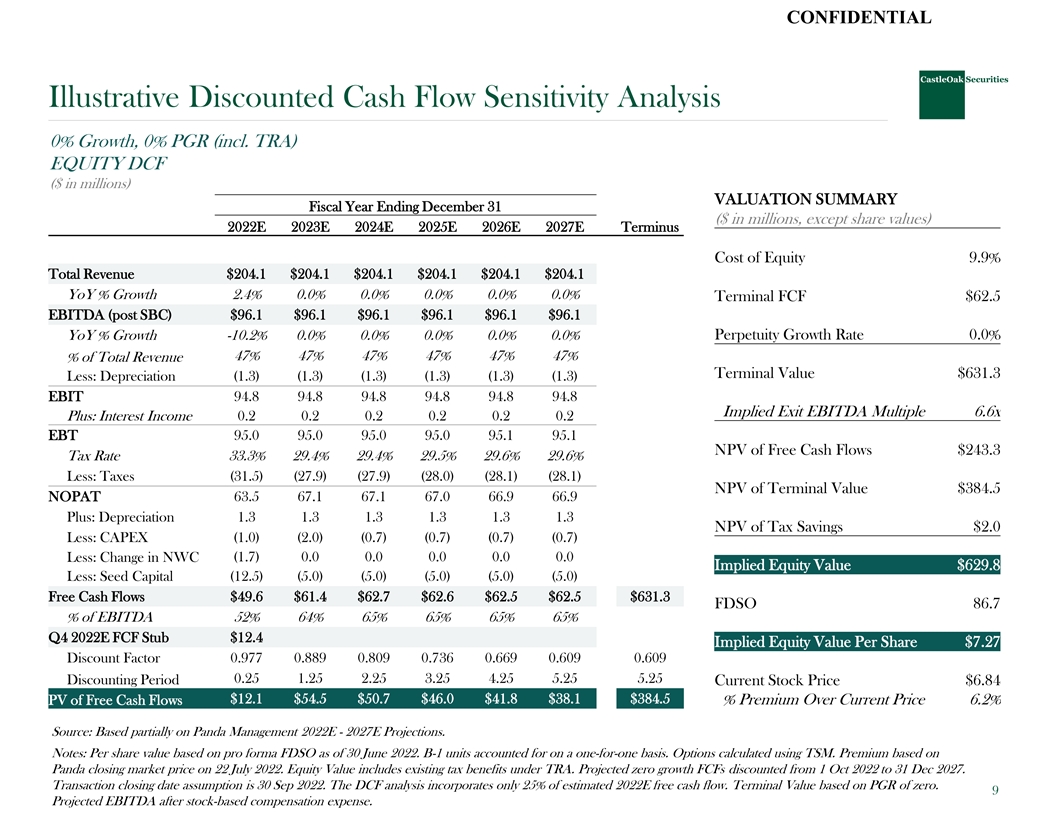

PRELIMINARY BACKGROUND MATERIALS PRELIMINARY BACKGROUND MATERIALS 3 Discounted Cash Flow Analysis ( 1 / 2 ) Class B-1 Units Economically Equivalent to Class B Units ($M) Jun—Dec 2022E 2023E 2024E 2025E 2026E 2027E Year-End AUM ($B) $52.2 $55.7 $58.2 $60.6 $62.9 $65.0 Total Revenue $117 $212 $220 $223 $228 $233 YoY Growth (%) N/A 3.8% 3.7% 1.4% 2.5% EBITDA $51 $99 $100 $100 $102 $104 EBITDA Margin (%) 43.7% 46.6% 45.5% 45.0% 44.7% 44.5% D&A (1) (1) (1) (1) (1) (1) Investment G&L 0 2 3 3 3 3 Operating Income $51 $100 $101 $102 $104 $106 UBT (2) (4) (4) (4) (4) (4) Unlevered Net Income $49 $96 $97 $98 $100 $102 D&A 1 1 1 1 1 1 Rent Expense Adjustment 2 2 1 1 2 (0) Changes in Net Working Capital 5 0 0 0 0 0 CapEx 0 (2) (1) (1) (1) (1) Seed Investment (13) (5) (5) (5) (5) (5) Distributable Cash Flow $45 $92 $94 $94 $97 $97 YoY Growth (%) N/A 2.1% 0.5% 3.5% (0.6%) Inc. Diluted Class A Shares 17.6 17.6 17.6 17.6 17.6 17.6 Diluted Shares Outstanding 88.0 88.0 88.0 88.0 88.0 88.0 Inc. Ownership 20% 20% 20% 20% 20% 20% Cash Flow Distribution to Inc. $9 $18 $19 $19 $19 $19 Tax (2) (5) (5) (5) (5) (5) Inc. Unlevered Net Income $7 $14 $14 $14 $14 $14 ? Balance sheet and share count as of 31-May-2022 ? Mid-year cash flow convention ? UBT cash tax rate of 4.0% and Panda Inc. marginal cash tax rate of 25.7% Source: Company filings and Panda management projections. Note: Assumes $30M of minimum cash requirement per management. Class B-1 units treated as economically equivalent to Class B units. See appendix for treatment of Class B-1 units with treasury stock method. July 2022 5 Options dilution calculated using treasury stock method.

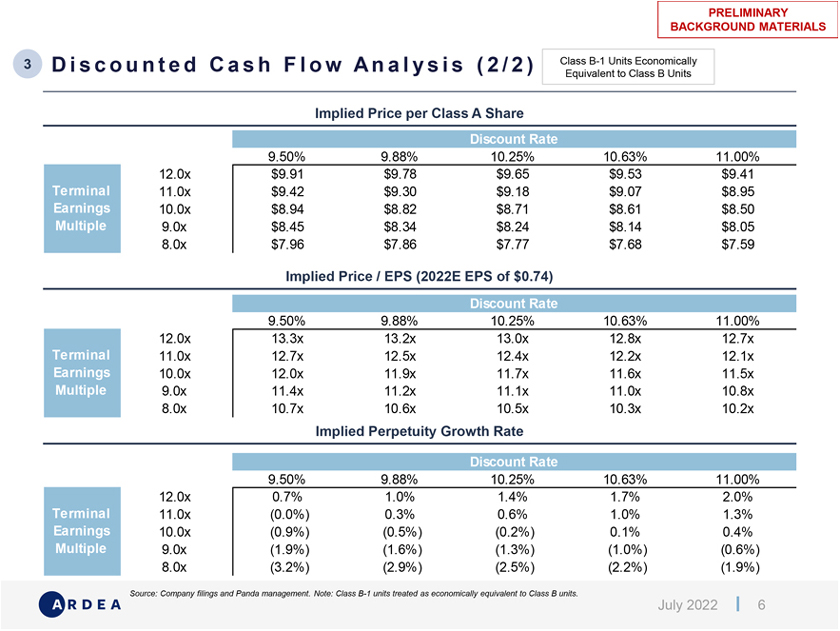

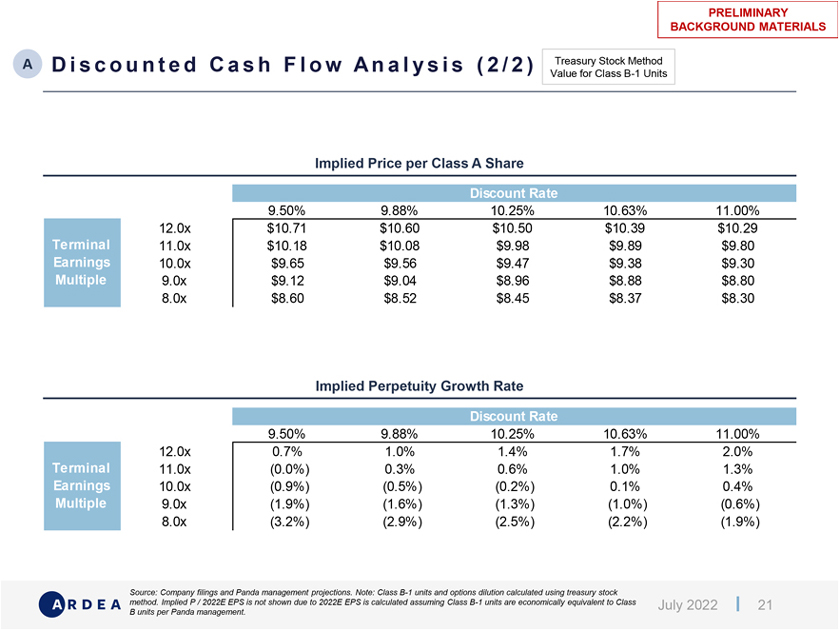

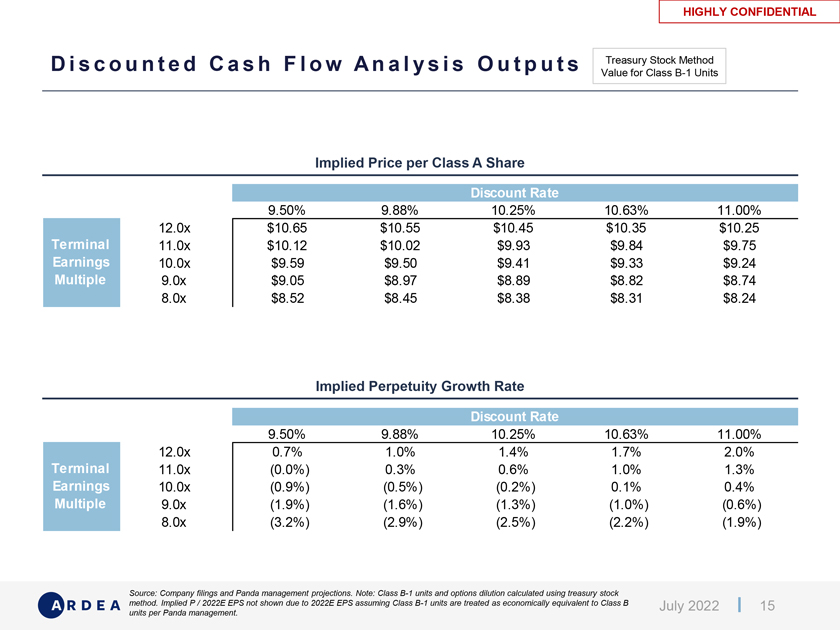

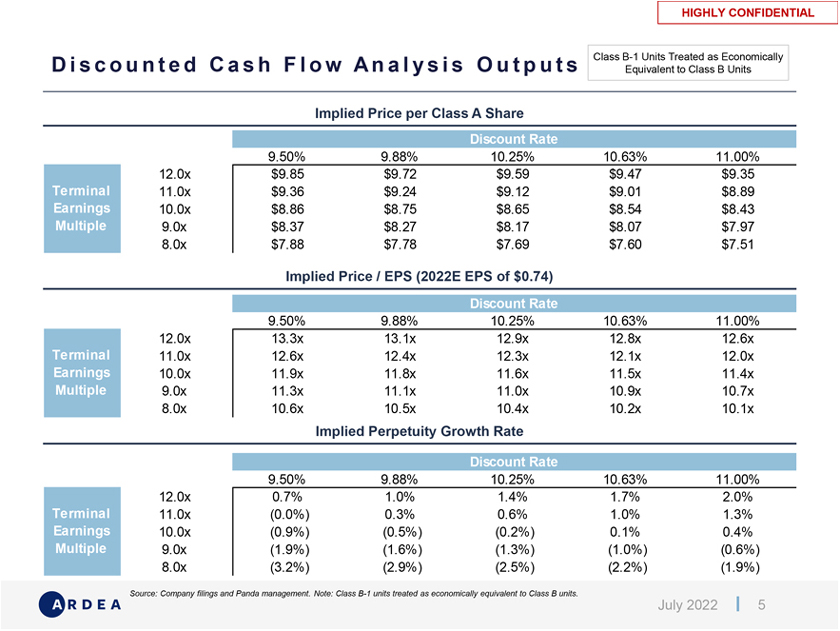

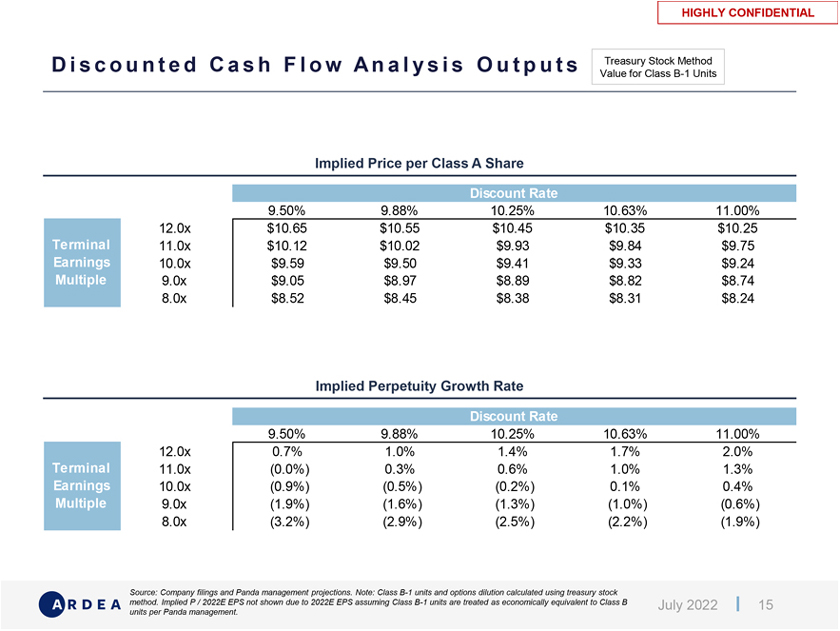

PRELIMINARY BACKGROUND MATERIALS 3 D i s c o u n t e d C a s h F l o w A n a l y s i s ( 2 / 2 ) Class B-1 Units Economically Equivalent to Class B Units Implied Price per Class A Share Discount Rate $8.7 9.50% 9.88% 10.25% 10.63% 11.00% 12.0x $9.91 $9.78 $9.65 $9.53 $9.41 Terminal 11.0x $9.42 $9.30 $9.18 $9.07 $8.95 Earnings 10.0x $8.94 $8.82 $8.71 $8.61 $8.50 Multiple 9.0x $8.45 $8.34 $8.24 $8.14 $8.05 8.0x $7.96 $7.86 $7.77 $7.68 $7.59 Implied Price / EPS (2022E EPS of $0.74) Discount Rate 9.50% 9.88% 10.25% 10.63% 11.00% 12.0x 13.3x 13.2x 13.0x 12.8x 12.7x Terminal 11.0x 12.7x 12.5x 12.4x 12.2x 12.1x Earnings 10.0x 12.0x 11.9x 11.7x 11.6x 11.5x Multiple 9.0x 11.4x 11.2x 11.1x 11.0x 10.8x 8.0x 10.7x 10.6x 10.5x 10.3x 10.2x Implied Perpetuity Growth Rate Discount Rate ($0.0) 9.50% 9.88% 10.25% 10.63% 11.00% 12.0x 0.7% 1.0% 1.4% 1.7% 2.0% Terminal 11.0x (0.0%) 0.3% 0.6% 1.0% 1.3% Earnings 10.0x (0.9%) (0.5%) (0.2%) 0.1% 0.4% Multiple 9.0x (1.9%) (1.6%) (1.3%) (1.0%) (0.6%) 8.0x (3.2%) (2.9%) (2.5%) (2.2%) (1.9%) Source: Company filings and Panda management. Note: Class B-1 units treated as economically equivalent to Class B units. July 2022 6

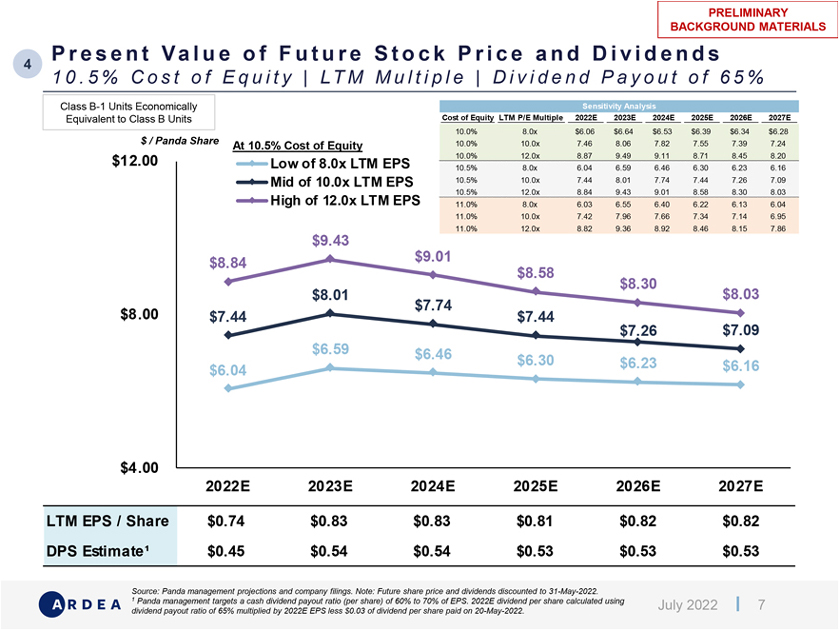

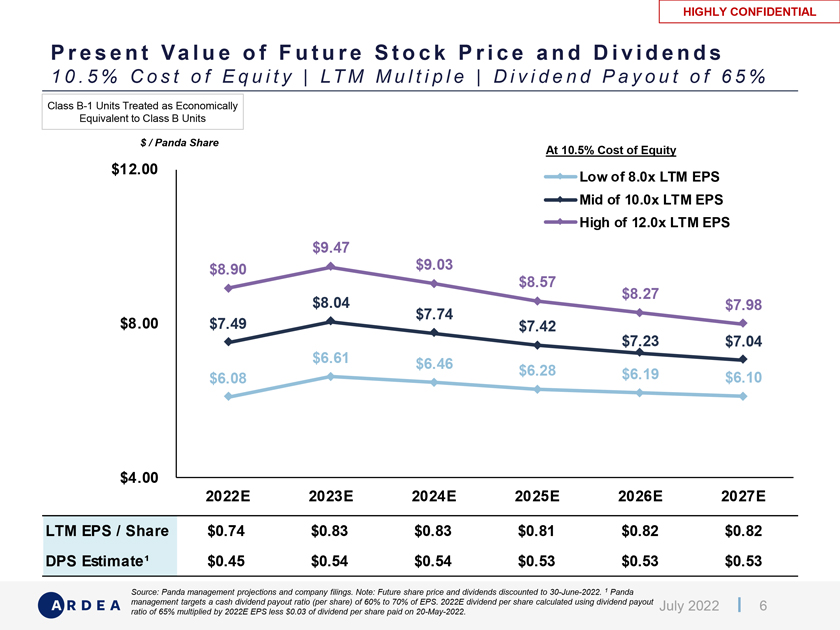

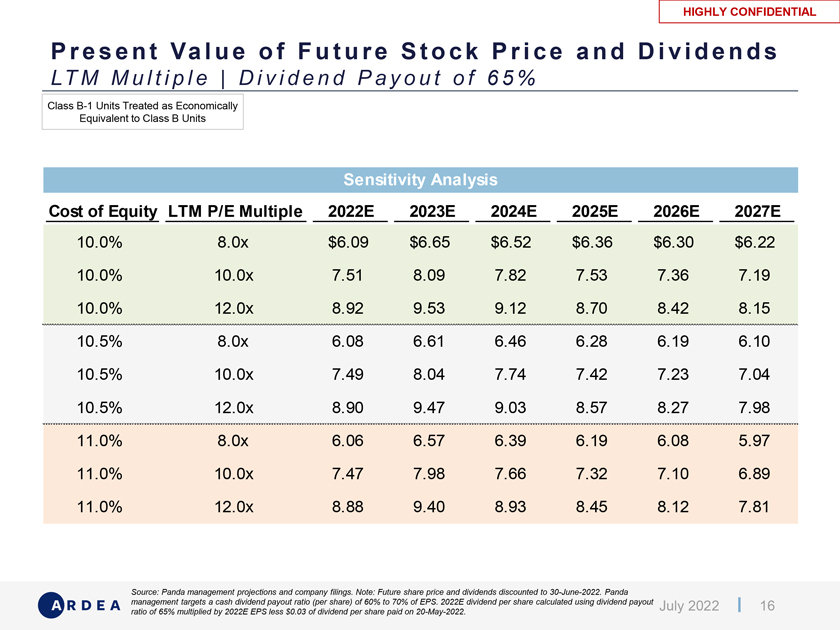

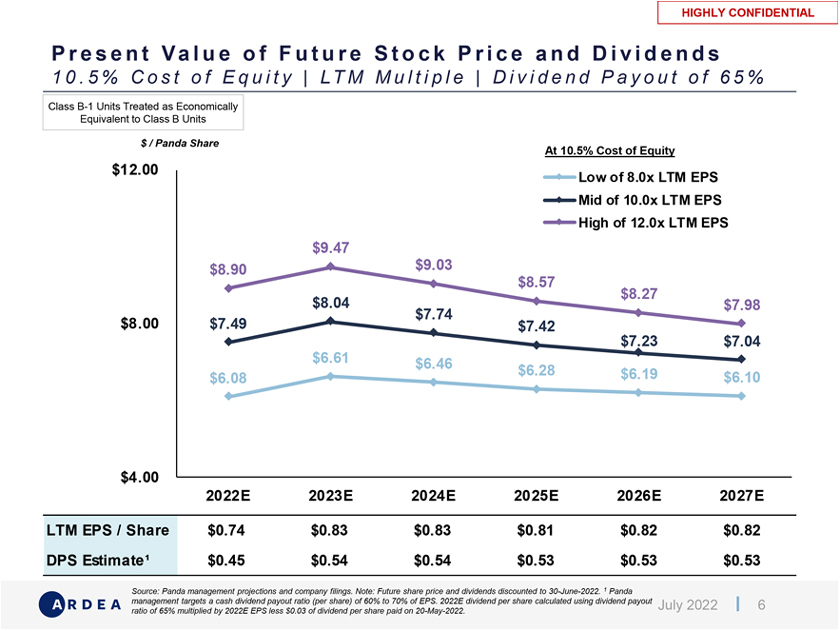

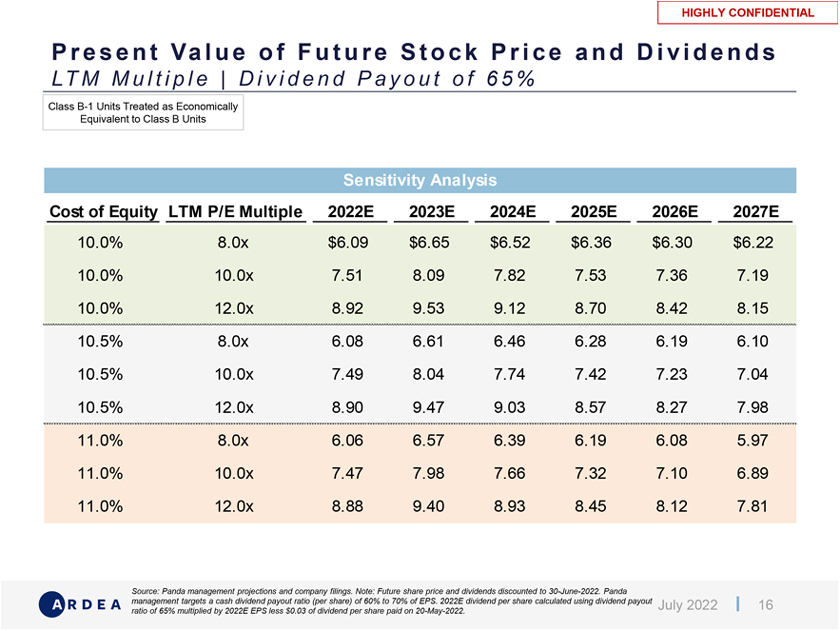

BACKGROUND MATERIALS PRELIMINARY BACKGROUND MATERIALS P r e s e n t Va l u e o f F u t u r e S t o c k P r i c e a n d D i v i d e n d s 4 1 0 . 5 % C o s t o f E q u i t y | LT M M u l t i p l e | D i v i d e n d P a y o u t o f 6 5 % Class B-1 Units Economically Sensitivity Analysis Equivalent to Class B Units Cost of Equity LTM P/E Multiple 2022E 2023E 2024E 2025E 2026E 2027E 10.0% 8.0x $6.06 $6.64 $6.53 $6.39 $6.34 $6.28 $ / Panda Share At 10.5% Cost of Equity 10.0% 10.0x 7.46 8.06 7.82 7.55 7.39 7.24 $12.00 10.0% 12.0x 8.87 9.49 9.11 8.71 8.45 8.20 Low of 8.0x LTM EPS 10.5% 8.0x 6.04 6.59 6.46 6.30 6.23 6.16 Mid of 10.0x LTM EPS 10.5% 10.0x 7.44 8.01 7.74 7.44 7.26 7.09 10.5% 12.0x 8.84 9.43 9.01 8.58 8.30 8.03 High of 12.0x LTM EPS 11.0% 8.0x 6.03 6.55 6.40 6.22 6.13 6.04 11.0% 10.0x 7.42 7.96 7.66 7.34 7.14 6.95 11.0% 12.0x 8.82 9.36 8.92 8.46 8.15 7.86 $9.43 $8.84 $9.01 $8.58 $8.30 $8.01 $8.03 $7.74 $8.00 $7.44 $7.44 $7.26 $7.09 $6.59 $6.46 $6.30 $6.23 $6.16 $6.04 $4.00 2022E 2023E 2024E 2025E 2026E 2027E LTM EPS / Share $0.74 $0.83 $0.83 $0.81 $0.82 $0.82 DPS Estimate¹ $0.45 $0.54 $0.54 $0.53 $0.53 $0.53 Source: Panda management projections and company filings. Note: Future share price and dividends discounted to 31-May-2022. 1 Panda management targets a cash dividend payout ratio (per share) of 60% to 70% of EPS. 2022E dividend per share calculated using July 2022 7 dividend payout ratio of 65% multiplied by 2022E EPS less $0.03 of dividend per share paid on 20-May-2022.

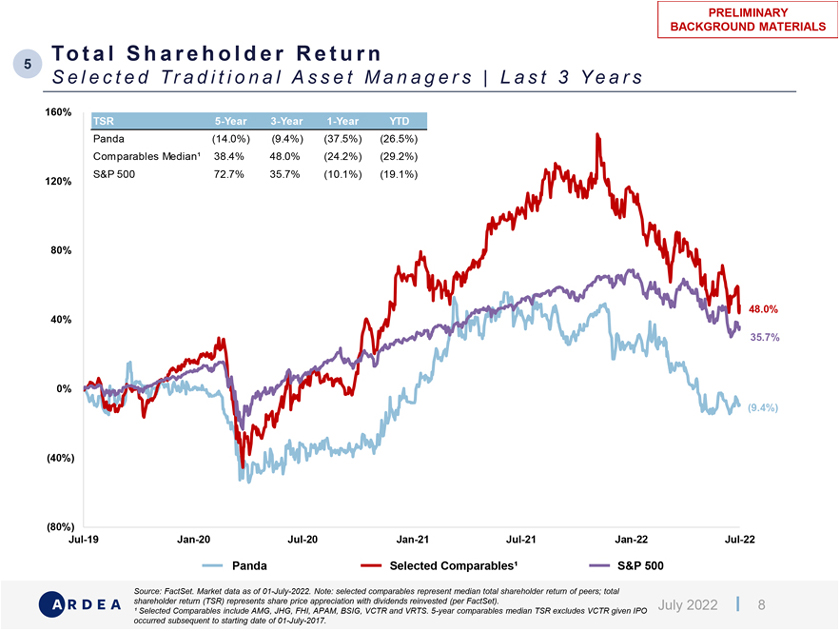

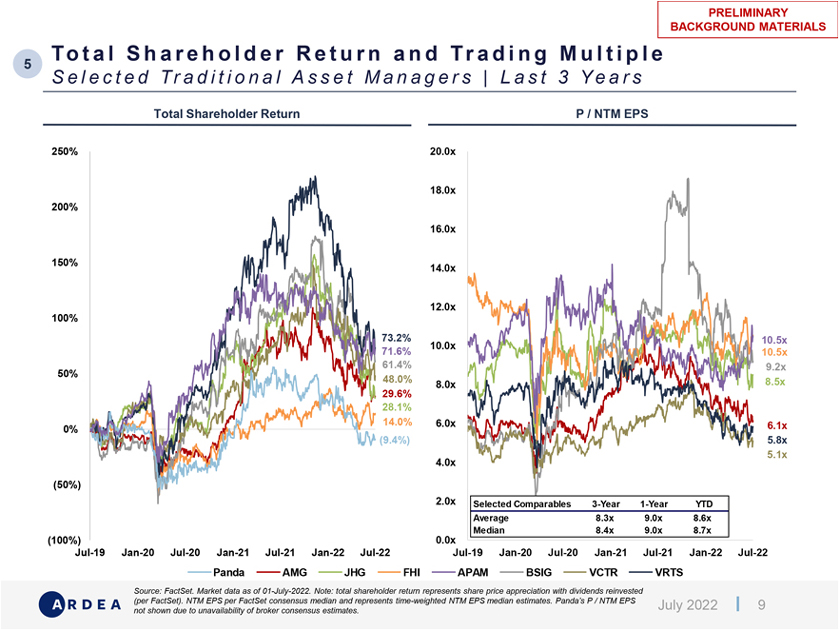

PRELIMINARY BACKGROUND MATERIALS To t a l S h a r e h o l d e r R e t u r n 5 S e l e c t e d Tr a d i t i o n a l A s s e t M a n a g e r s | L a s t 3 Y e a r s 160% TSR 5-Year 3-Year 1-Year YTD Panda (14.0%) (9.4%) (37.5%) (26.5%) Comparables Median¹ 38.4% 48.0% (24.2%) (29.2%) S&P 500 72.7% 35.7% (10.1%) (19.1%) 120% 80% 48.0% 40% 35.7% 0% (9.4%) (40%) (80%) Jul-19 Jan-20 Jul-20 Jan-21 Jul-21 Jan-22 Jul-22 Panda Selected Comparables¹ S&P 500 Source: FactSet. Market data as of 01-July-2022. Note: selected comparables represent median total shareholder return of peers; total shareholder return (TSR) represents share price appreciation with dividends reinvested (per FactSet). July 2022 8 ¹ Selected Comparables include AMG, JHG, FHI, APAM, BSIG, VCTR and VRTS. 5-year comparables median TSR excludes VCTR given IPO occurred subsequent to starting date of 01-July-2017.

PRELIMINARY BACKGROUND MATERIALS To t a l S h a r e h o l d e r R e t u r n a n d Tr a d i n g M u l t i p l e 5 S e l e c t e d Tr a d i t i o n a l A s s e t M a n a g e r s | L a s t 3 Y e a r s Total Shareholder Return P / NTM EPS 250% 20.0x 18.0x 200% 16.0x 150% 14.0x 12.0x 100% 73.2% 10.5x 10.0x 71.6% 10.5x 50% 61.4% 9.2x 48.0% 8.5x 29.6% 8.0x 28.1% 14.0% 6.0x 6.1x 0% (9.4%) 5.8x 5.1x 4.0x (50%) 2.0x Selected Comparables 3-Year 1-Year YTD Average 8.3x 9.0x 8.6x Median 8.4x 9.0x 8.7x (100%) 0.0x Jul-19 Jan-20 Jul-20 Jan-21 Jul-21 Jan-22 Jul-22 Jul-19 Jan-20 Jul-20 Jan-21 Jul-21 Jan-22 Jul-22 Panda AMG JHG FHI APAM BSIG VCTR VRTS Source: FactSet. Market data as of 01-July-2022. Note: total shareholder return represents share price appreciation with dividends reinvested (per FactSet). NTM EPS per FactSet consensus median and represents time-weighted NTM EPS median estimates. Panda’s P / NTM EPS July 2022 9 not shown due to unavailability of broker consensus estimates.

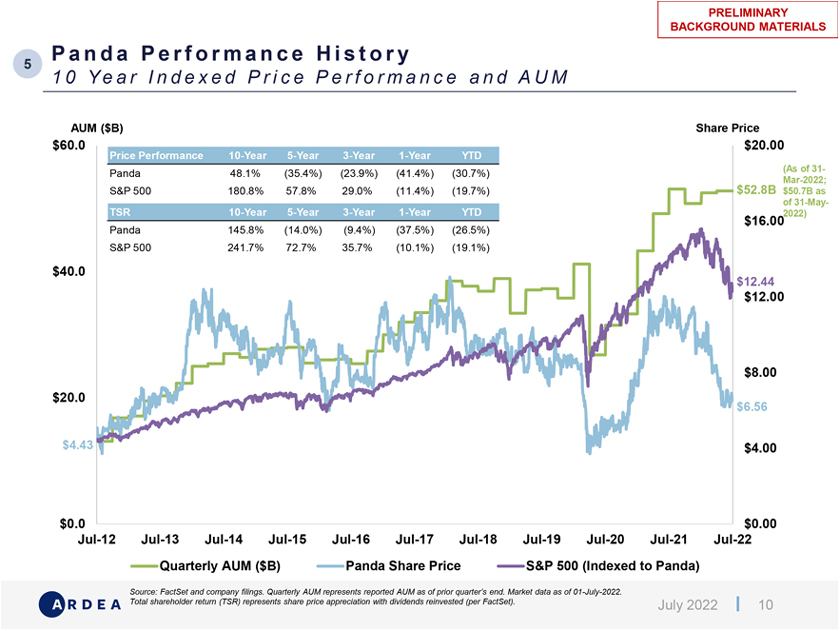

PRELIMINARY BACKGROUND MATERIALS P a n d a P e r f o r m a n c e H i s t o r y 5 1 0 Y e a r I n d e x e d P r i c e P e r f o r m a n c e a n d A U M AUM ($B) Share Price $60.0 Price Performance 10-Year 5-Year 3-Year 1-Year YTD $20.00 Panda 48.1% (35.4%) (23.9%) (41.4%) (30.7%) (As of 31-$52.8B Mar-2022; S&P 500 180.8% 57.8% 29.0% (11.4%) (19.7%) $50.7B as of 31-May- TSR 10-Year 5-Year 3-Year 1-Year YTD 2022) $16.00 Panda 145.8% (14.0%) (9.4%) (37.5%) (26.5%) S&P 500 241.7% 72.7% 35.7% (10.1%) (19.1%) $40.0 $12.44 $12.00 $8.00 $20.0 $6.56 $4.43 $4.00 $0.0 $0.00 Jul-12 Jul-13 Jul-14 Jul-15 Jul-16 Jul-17 Jul-18 Jul-19 Jul-20 Jul-21 Jul-22 Quarterly AUM ($B) Panda Share Price S&P 500 (Indexed to Panda) Source: FactSet and company filings. Quarterly AUM represents reported AUM as of prior quarter’s end. Market data as of 01-July-2022. Total shareholder return (TSR) represents share price appreciation with dividends reinvested (per FactSet). July 2022 10