0001124959falseNoIn order to compute the Corresponding Return to Common Shares Shareholders, the Assumed Portfolio Return is multiplied by the total value of the Fund's assets at the beginning of the Fund's fiscal year to obtain an assumed return to the Fund. From this amount, all interest accrued during the year is subtracted to determine the return available to shareholders. The return available to shareholders is then divided by the total value of the Fund's net assets attributable to Common Shares as of the beginning of the fiscal year to determine the Corresponding Return to Common Shareholders.The Distributor will pay a dealer reallowance for Class A Common Shares from the sales charge. The Distributor will pay a sales commission for Class C Common Shares to authorized dealers from its own assets.Reduced for purchases of $100,000 and over for Class A Common Shares, please see “Sales Charges.”There is no front-end sales charge if you purchase Class A Common Shares in the amount of $500,000 or more. Class A Common Shares purchased in an amount of $500,000 or more are subject to a 1.00% EWC if repurchased by the Fund within 12 months of purchase. Class C Common Shares repurchased by the Fund within the first year after purchase will incur a 1.00% EWC. See “Sales Charges - Early Withdrawal Charge.” No EWC will be charged on redemptions that are due to the closing of shareholder accounts having a value of less than $1,000.Pursuant to the investment management agreement with the Fund, the Investment Adviser is paid a fee of 0.80% of the Fund's Managed Assets. For the description of “Managed Assets,” please see “Description of the Fund – Investment Adviser/Sub-Adviser” earlier in this Prospectus.Because the distribution fees payable by Class C Common Shares may be considered an asset-based sales charge, long-term shareholders in that class of the Fund may pay more than the economic equivalent of the maximum front-end sales charges permitted by the Financial Industry Regulatory Authority.Other Operating Expenses are estimated amounts for the current fiscal year.The Investment Adviser is contractually obligated to limit expenses of the Fund through July 1, 2025 to the following: Class A Common Shares - 0.90% of Managed Assets plus 0.45% of average daily net assets; Class C Common Shares - 0.90% of Managed Assets plus 0.95% of average daily net assets; Class I Common Shares - 0.90% of Managed Assets plus 0.20% of average daily net assets; and Class W Common Shares - 0.90% of Managed Assets plus 0.20% of average daily net assets. The obligation is subject to possible recoupment by the Investment Adviser within 36 months of the waiver or reimbursement. The Investment Adviser is contractually obligated to further limit expenses of the Fund through July 1, 2025 to the following: Class A Common Shares - 0.80% of Managed Assets plus 0.45% of average daily net assets; Class C Common Shares - 0.80% of Managed Assets plus 0.95% of average daily net assets; Class I Common Shares - 0.80% of Managed Assets plus 0.20% of average daily net assets; and Class W Common Shares - 0.80% of Managed Assets plus 0.20% of average daily net assets. These limitations do not extend to interest, taxes, investment-related costs, leverage expenses, extraordinary expenses, and Acquired Fund Fees and Expenses. Termination or modification of these obligations requires approval by the Fund’s Board.If the expenses of the Fund are calculated on the Managed Assets of the Fund (assuming that the Fund has used leverage by borrowing an amount equal to 25% of the Fund’s Managed Assets), the Net Annual Expenses for the Fund would be lower than the expenses shown in the table. Such lower Net Annual Expense ratios would be as follows: 2.99%, 3.49%, 2.74%, and 2.74% for Class A, Class C, Class I, and Class W shares, respectively.

0001124959

2024-06-27

2024-06-27

0001124959

vcif:OtherInvestmentCompanieMember

2024-06-27

2024-06-27

0001124959

vcif:CompanyMember

2024-06-27

2024-06-27

0001124959

vcif:CreditsMember

2024-06-27

2024-06-27

0001124959

vcif:CreditDefaultSwapsMember

2024-06-27

2024-06-27

0001124959

vcif:ValuationOfLoansMember

2024-06-27

2024-06-27

0001124959

vcif:WhenissuedDelayedDeliveryAndForwardCommitmentTransactionsMember

2024-06-27

2024-06-27

0001124959

vcif:MarketMember

2024-06-27

2024-06-27

0001124959

vcif:MarketDisruptionAndGeopoliticalMember

2024-06-27

2024-06-27

0001124959

vcif:PrepaymentAndExtensionMember

2024-06-27

2024-06-27

0001124959

vcif:SecuritiesLendingMember

2024-06-27

2024-06-27

0001124959

vcif:SpecialSituationsMember

2024-06-27

2024-06-27

0001124959

vcif:TemporaryDefensivePositionsMember

2024-06-27

2024-06-27

0001124959

vcif:InterestRateForFloatingRateLoansMember

2024-06-27

2024-06-27

0001124959

vcif:InterestRateSwapsMember

2024-06-27

2024-06-27

0001124959

vcif:CovenantliteLoansMember

2024-06-27

2024-06-27

0001124959

vcif:LimitedLiquidityForInvestorsMember

2024-06-27

2024-06-27

0001124959

vcif:LimitedSecondaryMarketForLoansMember

2024-06-27

2024-06-27

0001124959

vcif:LiquidityMember

2024-06-27

2024-06-27

0001124959

vcif:FloatingRateLoansMember

2024-06-27

2024-06-27

0001124959

vcif:ForeignNonu.s.InvestmentsMember

2024-06-27

2024-06-27

0001124959

vcif:ForeignNonu.s.AndNoncanadianIssuersMember

2024-06-27

2024-06-27

0001124959

vcif:HighyieldSecuritiesMember

2024-06-27

2024-06-27

0001124959

vcif:InterestInLoansMember

2024-06-27

2024-06-27

0001124959

vcif:InterestRateMember

2024-06-27

2024-06-27

0001124959

vcif:CreditFacilityMember

2024-06-27

2024-06-27

0001124959

vcif:CreditLoansMember

2024-06-27

2024-06-27

0001124959

vcif:CurrencyMember

2024-06-27

2024-06-27

0001124959

vcif:DemandForLoansMember

2024-06-27

2024-06-27

0001124959

vcif:DerivativeInstrumentsMember

2024-06-27

2024-06-27

0001124959

vcif:DurationMember

2024-06-27

2024-06-27

0001124959

vcif:LeverageMember

2024-06-27

2024-06-27

0001124959

vcif:ClassACommonSharesMember

2024-06-27

2024-06-27

0001124959

vcif:ClassCCommonSharesMember

2024-06-27

2024-06-27

0001124959

vcif:ClassICommonSharesMember

2024-06-27

2024-06-27

0001124959

vcif:ClassWCommonSharesMember

2024-06-27

2024-06-27

0001124959

vcif:CommonSharesMember

2024-06-27

2024-06-27

0001124959

vcif:PreferredSharesMember

2024-06-27

2024-06-27

0001124959

dei:BusinessContactMember

2024-06-27

2024-06-27

0001124959

vcif:ClassACommonSharesWithRepurchasesAtPeriodEndMember

2024-06-27

2024-06-27

0001124959

vcif:ClassCCommonSharesWithRepurchasesAtPeriodEndEndMember

2024-06-27

2024-06-27

0001124959

vcif:ClassICommonSharesWithRepurchasesAtPeriodEndMember

2024-06-27

2024-06-27

0001124959

vcif:ClassWCommonSharesWithRepurchasesAtPeriodEndMember

2024-06-27

2024-06-27

0001124959

vcif:ClassACommonSharesNoRepurchasesMember

2024-06-27

2024-06-27

0001124959

vcif:ClassCCommonSharesNoRepurchasesMember

2024-06-27

2024-06-27

0001124959

vcif:ClassICommonSharesNoRepurchasesMember

2024-06-27

2024-06-27

0001124959

vcif:ClassWCommonSharesNoRepurchasesMember

2024-06-27

2024-06-27

xbrli:shares

xbrli:pure

iso4217:USD

As filed with the U.S. Securities and Exchange Commission on June 27, 2024

Securities Act File No. 333-219011

Investment Company Act File No. 811-10223

SECURITIES AND EXCHANGE COMMISSION

(Check appropriate box or boxes)

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 |

| Pre-Effective Amendment No. |

| Post-Effective Amendment No. 12 |

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 |

| |

(Exact Name of Registrant as Specified in Charter)

7337 E. Doubletree Ranch Road, Suite 100

Scottsdale, Arizona 85258

(Address of Principal Executive Offices)

(Number, Street, City, State, Zip Code)

(Registrant’s Telephone Number, including Area Code)

7337 E Doubletree Ranch Road, Suite 100

Scottsdale, Arizona 85258

(Name and Address (Number, Street, City, State, Zip Code) of Agent for Service)

Copies of Communications to:

|

Elizabeth J. Reza

Ropes & Gray LLP

Prudential Tower

800 Boylston Street

Boston, Massachusetts 02199-3600 |

Approximate Date of Proposed Public Offering:

As soon as practicable after the effective date of this Registration Statement.

| |

| Check box if the only securities being registered on this Form are being offered pursuant to dividend or interest reinvestment plans. |

X | Check box if any securities being registered on this Form will be offered on a delayed or continuous basis in reliance on Rule 415 under the Securities Act of 1933 (“Securities Act”), other than securities offered in connection with a dividend reinvestment plan. |

| Check box if this Form is a registration statement pursuant to General Instruction A.2 or a post-effective amendment thereto. |

| Check box if this Form is a registration statement pursuant to General Instruction B or a post-effective amendment thereto that will become effective upon filing with the Commission pursuant to Rule 462(e) under the Securities Act. |

| Check box if this Form is a post-effective amendment to a registration statement filed pursuant to General Instruction B to register additional securities or additional classes of securities pursuant to Rule 413(b) under the Securities Act. |

It is proposed that this filing will become effective (check appropriate box):

| |

| when declared effective pursuant to Section 8(c), or as follows: The following boxes should only be included and completed if the registrant is making this filing in accordance with Rule 486 under the Securities Act. |

| immediately upon filing pursuant to paragraph (b) of Rule 486. |

X | on June 28, 2024 pursuant to paragraph (b) of Rule 486. |

| 60 days after filing pursuant to paragraph (a) of Rule 486. |

| on (date) pursuant to paragraph (a) of Rule 486 . |

If appropriate, check the following box:

| |

| This [post-effective amendment] designates a new effective date for a previously filed [post-effective amendment] [registration statement]. |

| This Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, and the Securities Act registration statement number of the earlier effective registration statement for the same offering is: ______. |

| This Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, and the Securities Act registration statement number of the earlier effective registration statement for the same offering is: ______. |

| This Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, and the Securities Act registration statement number of the earlier effective registration statement for the same offering is: ______. |

Check each box that appropriately characterizes the Registrant:

| |

| Registered Closed-End Fund (closed-end company that is registered under the Investment Company Act of 1940 (“Investment Company Act”)). |

| Business Development Company (closed-end company that intends or has elected to be regulated as a business development company under the Investment Company Act). |

| Interval Fund (Registered Closed-End Fund or a Business Development Company that makes periodic repurchase offers under Rule 23c-3 under the Investment Company Act). |

| A.2 Qualified (qualified to register securities pursuant to General Instruction A.2 of this Form). |

| Well-Known Seasoned Issuer (as defined by Rule 405 under the Securities Act). |

| Emerging Growth Company (as defined by Rule 12b-2 under the Securities Exchange Act of 1934 (“Exchange Act”). |

| If an Emerging Growth Company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of Securities Act. |

| New Registrant (registered or regulated under the Investment Company Act for less than 12 calendar months preceding this filing). |

This Post-Effective Amendment No. 12 (the “Amendment”) to the Registration Statement on Form N-2 of Voya Credit Income

Fund (the “Registrant”) is being filed pursuant to Rule 486(b) under the Securities Act of 1933, as amended, finalizing the

disclosure in compliance with annual updating requirements to the Registrant’s Prospectus and Statement of Additional

Information.

This registration statement incorporates a combined prospectus pursuant to Rule 429, which relates to earlier registration

statements filed by the Registrant on June 28, 2017 (see File No. 333-219011), November 22, 2013 (see File No. 333-192499),

June 27, 2013 (see File No. 333-189639), June 26, 2012 (see File No. 333-175174), June 28, 2011 (see File No. 333-175174),

April 14, 2008 (see File No. 333-150236), June 28, 2007 (see File No. 333-144159), June 30, 2006 (see File No. 333-135548),

June 29, 2005 (see File No. 333-126224), December 6, 2004 (see File No. 333-121014), June 28, 2004 (see File No. 333-116936),

February 23, 2004 (see File No. 333-113012), November 7, 2003 (see File No. 333-110317), September 22, 2003 (see File No.

333-109005), August 15, 2003 (see File No. 333-108020), July 17, 2003 (see File No. 333-107124), July 1, 2002 (see File No.

333-91662) and March 30, 2001 (see File No. 333-54910). This prospectus will also be used in connection with sales of securities

registered by the Registrant under those registration statements.

This Amendment is organized as follows: (a) Prospectus; (b) Statement of Additional Information; and (c) Part C Information

relating to the Registrant.

Class/Ticker:

XSIAX;

XSICX;

XSIIX;

XSIWX

Common Shares

Voya Credit Income Fund (the

“

Fund

”

) is a Delaware Statutory trust that is registered under the Investment Company Act

of 1940, as amended (the

“

1940 Act

”

), as a continuously-offered, diversified, closed-end management investment company.

The Fund’s investment objective is to provide investors with a high level of monthly income.

The Fund allocates its assets among a broad range of credit sectors, including corporate debt securities, loans, high yield

debt securities, and collateralized loan obligations (

“

CLOs

”

). The Fund seeks to achieve its investment objective by investing,

under normal market conditions, at least 80% of its net assets (plus borrowings for investment purposes) in floating-rate

obligations, fixed-income securities, and derivative instruments intended to provide economic exposure to such credit sectors.

The Fund may invest in securities of any credit quality, duration, or maturity and may invest without limit in securities rated

below investment grade. The Fund expects that under normal market conditions its investments in high yield bonds, loans,

CLOs and similar instruments will typically comprise at least half, and potentially substantially all of the investment exposure

of its portfolio.

Debt instruments

in which the Fund invests may include senior or subordinated fixed or floating rate instruments,

unitranche debt, unsecured debt, and structurally subordinated instruments. The Fund may also invest in special situations

investments, such as non-performing

debt instruments

, or

debt instruments

issued by companies undergoing a bankruptcy

or restructuring process. Some of the loans in which the Fund invests may be loans originated directly by the Fund. The

Fund may invest in equity securities: (i) as an incident to the purchase or ownership of loans or fixed rate debt instruments;

or (ii) in connection with a restructuring of a borrower or issuer or its debt.

To seek to increase the yield on the Common

Shares, the Fund employs financial leverage by borrowing money and may also issue preferred shares. See

“

Risk Factors

and Special Considerations - Leverage

”

and

“

Description of the Capital Structure

”

later in the Fund’s prospectus.

This Prospectus applies to the offering of four separate classes of shares of beneficial interest (

“

Common Shares

”

) in the

Fund, designated as Class A Common Shares, Class C Common Shares, Class I Common Shares, and Class W Common

Shares.

The Fund has an interval fund structure and conducts monthly repurchase offers for its Common Shares at net asset value

(

“

NAV

”

) per Common Share in an amount not less than 5% of its outstanding Common Shares each month nor more than

25% of its outstanding Common Shares in any calendar quarter, subject to applicable law, approval of the Fund’s Board of

Trustees, and in accordance with the Fund’s repurchase policy established pursuant to Rule 23c-3 under the 1940 Act.

Risk Factors and Special Considerations – Limited Liquidity for Investors

for further discussion on the Fund’s repurchase policies and related risks.

There is no assurance that you will be able to tender your Common Shares when or in the amount that you desire. Common

Shares are speculative and illiquid securities involving substantial risk of loss. An investment in the Fund is subject to, among

others, the following risks:

The Fund’s Common Shares are not listed on any national securities exchange and it is not anticipated that a secondary

market for the Common Shares will develop. You should generally not expect to be able to sell your Common Shares

(other than through the repurchase process). Thus, an investment in the Fund may not be suitable for investors who may

need the money they invest in a specified timeframe.

Even though the Fund will offer to repurchase Common Shares on a monthly basis, only a limited number of Common

Shares will be eligible for repurchase by the Fund, so you should consider the Common Shares to be illiquid. Common

Shares will not be redeemable at a shareholder’s option nor will they be exchangeable for shares of any other fund. As a

result, there is no guarantee that you will be able to sell your Common Shares at any given time or in the quantity that

Common Shares are appropriate only for those investors who can tolerate a high degree of risk and do not require a

liquid investment and for whom an investment in the Fund does not constitute a complete investment program.

Common Shares are speculative and involve a high degree of risk, including the risk of a substantial loss of investment.

Risk Factors and Special Considerations

later in this Prospectus to read about the risks you should consider before

The amount of distributions that the Fund may pay, if any, is uncertain.

The Fund may pay distributions in significant part from sources that may not be available in the future and that are unrelated

to the Fund’s performance, such as from offering proceeds and borrowings.

With respect to Class A Common Shares, an investor will pay a sales load of up to 2.50% on the amount invested.

pay the maximum aggregate 2.50% sales load, you must experience a total return on your net investment of 2.56% in

order to recover such sales charges.

The Fund may invest in below investment grade investments (

instruments), securities which are at risk of default

as to the repayment of principal and/or interest at the time of acquisition by the Fund or are rated in the lower rating

categories or are unrated. These investments may be difficult to value and may be illiquid. See

Considerations –Liquidity and High-Yield Securities

later in this Prospectus.

This Prospectus provides important information that you should know about the Fund before investing. You should read

this Prospectus carefully and retain it for future reference. Additional information about the Fund, including the Statement

of Additional Information (

“

SAI

”

), dated June 28, 2024, has been filed with the SEC. The SAI is incorporated by reference

in its entirety into this Prospectus. You may make shareholder inquiries or obtain a free copy of the SAI, annual shareholder

report, and unaudited semi-annual shareholder report by contacting the Fund at 1-800-992-0180 or by writing to the Fund

at 7337 East Doubletree Ranch Road, Suite 100, Scottsdale, Arizona 85258-2034. The Fund's SAI, annual shareholder

report, and unaudited semi-annual shareholder report are also available free of charge on the Fund's website at

www.voyainvestments.com. The Prospectus, SAI, and other information about the Fund are also available on the SEC's

website (www.sec.gov).

The Fund’s investment objective is to provide investors with a high level of monthly income. Market fluctuations and general

economic conditions can adversely affect the Fund. There is no guarantee that the Fund will achieve its investment objective.

Investment in the Fund involves certain risks and special considerations, including risks associated with the Fund's use of

leverage.

Risk Factors and Special Considerations

later in this Prospectus for a discussion of any factors that make

an investment in the Fund speculative or high risk.

Neither the SEC nor any state securities commission has approved or disapproved these securities or determined that this

Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The following synopsis is qualified in its entirety by reference to the more detailed information appearing elsewhere in this

Prospectus.

The Fund is a continuously-offered, diversified, closed-end management investment company registered under the Investment

Company Act of 1940, as amended, and the rules, regulations and applicable exemptive orders thereunder (the

“

1940 Act

”

).

It was organized as a Delaware statutory trust on December 14, 2000. The Fund offers four separate classes of Common

Shares in this Prospectus: Class A, Class C, Class I, and Class W. See

“

Classes of Shares

”

later in this Prospectus.

To provide investors with a high level of monthly income. There is no assurance that the Fund will achieve its investment

objective. The investment objective is fundamental and may not be changed without a majority vote of the shareholders of

the Fund. See

“

Description of the Fund – Fundamental and Non-Fundamental Investment Policies of the Fund

”

later in this

Prospectus.

Investment Adviser/Sub-Adviser

Voya Investments, LLC (

“

Voya Investments

”

or the

“

Investment Adviser

”

), an Arizona limited liability company, is registered

with the SEC as an investment adviser. Voya Investments serves as the investment adviser to, and has overall responsibility

for the management of the Fund. Voya Investments oversees all investment advisory and portfolio management services and

assists in managing and supervising all aspects of the general day-to-day business activities and operations of the Fund,

including, but not limited to, the following: custodial, transfer agency, dividend disbursing, accounting, auditing, compliance,

and related services.

Voya Investments began business as an investment adviser in 1994 and currently serves as investment adviser to certain

registered investment companies, consisting of open- and closed-end registered investment companies and collateralized

loan obligations. Voya Investments is an indirect subsidiary of Voya Financial, Inc. Voya Financial, Inc. is a U.S.-based financial

institution whose subsidiaries operate in the retirement, investment, and insurance industries.

Voya Investments' principal business address is 7337 East Doubletree Ranch Road, Suite 100, Scottsdale, Arizona 85258.

The Investment Adviser receives an annual fee, payable monthly, in an amount equal to 0.80% of the Fund's average daily

gross asset value, minus the sum of the Fund's accrued and unpaid dividends on any outstanding preferred shares and

accrued liabilities (other than liabilities for the principal amount of any borrowings incurred, commercial paper or notes issued

by the Fund and the liquidation preference of any outstanding preferred shares) (

“

Managed Assets

”

). This definition includes

assets acquired through the Fund's use of leverage.

Voya Investment Management Co. LLC (

“

Voya IM

”

or the

“

Sub-Adviser

”

) serves as sub-adviser to the Fund. Voya IM is an

affiliate of the Investment Adviser.

See

“

Investment Management and Other Service Providers - Sub-Adviser and Portfolio Managers

”

later in this Prospectus.

Income dividends on Common Shares accrue and are declared daily and paid monthly. Income dividends will be automatically

reinvested in additional shares of the Fund at the Fund's net asset value (

“

NAV

”

) with no sales charge, unless a shareholder

elects to receive distributions in cash or to purchase shares of another Voya mutual fund. The Fund may make one or more

annual payments from any realized capital gains.

Principal Investment Strategies

The Fund allocates its assets among a broad range of credit sectors, including corporate debt securities, loans, high yield

debt securities, and CLOs. The Fund seeks to achieve its investment objective by investing, under normal market conditions,

at least 80% of its net assets (plus borrowings for investment purposes) in floating-rate obligations, fixed-income securities,

and derivative instruments intended to provide economic exposure to such credit sectors. The Fund will provide shareholders

with at least 60 days’ prior notice of any change in this investment policy.

The Fund may invest in securities of any credit quality, duration, or maturity and may invest without limit in securities rated

below investment grade (securities rated Ba1 or below by Moody’s Investors Service, Inc. (

“

Moody’s

”

), or BB+ or below by

S&P Global Ratings (

“

S&P

”

), or Fitch Ratings, Inc. (

“

Fitch

”

) or unrated securities judged by the Sub-Adviser to be of comparable

quality. Investments rated below investment grade (or similar quality if unrated) are commonly known as high-yielding, high

risk investments or as

“

junk

”

investments.

The Fund expects that under normal market conditions its investments in high yield bonds, loans, CLOs and similar instruments

will typically comprise at least half, and potentially substantially all of the investment exposure of its portfolio.

Debt instruments

in which the Fund invests may include senior or subordinated fixed or floating rate instruments, unitranche debt, unsecured

debt, and structurally subordinated instruments. The Fund may also invest in special situations investments, such as non-performing

debt instruments

, or

debt instruments

issued by companies undergoing a bankruptcy or restructuring process. Some of the

loans in which the Fund invests may be loans originated directly by the Fund. The Fund may invest in equity securities: (i) as

an incident to the purchase or ownership of loans or fixed rate debt instruments; or (ii) in connection with a restructuring of

a borrower or issuer or its debt.

Investment in the Fund involves certain risks and special considerations, including risks

associated with the Fund's use of leverage. See

“

Risk Factors and Special Considerations

”

later in this Prospectus for a

discussion of any factors that make an investment in the Fund speculative or high risk.

The Fund intends to invest across multiple credit sectors and employ multiple strategies, and the Fund’s asset allocations

will change in response to changing market, financial, economic, and political factors and events that the Fund’s Sub-Adviser

believes may affect the values of the Fund’s investments. The allocation of the Fund’s assets to different sectors and issuers

will change over time, potentially rapidly, and the Fund may invest without limit in a single sector or a small number of sectors

of the corporate credit universe. The Fund is not required to invest in each credit sector at all times.

Most of the Fund’s investments will be denominated in the U.S. dollar, although the Fund may invest in securities of non-U.S.

companies, and non-U.S. dollar credit instruments and securities.

The Fund may invest in derivative instruments,

including but not limited to, the following:

credit-linked notes, options, futures

contracts, options on futures,

forward contracts,

debt swap agreements, credit default swap agreements,

interest rate swaps,

total return swaps, and currency related derivatives, including currency forwards and currency swaps, subject to applicable

law. The Fund typically uses derivatives to seek to reduce exposures or other risks such as interest rate or currency risk, to

substitute for taking a position in the underlying asset, and/or to enhance returns in the Fund. The Fund may seek to obtain

market exposure to the instruments in which it primarily invests by entering into a series of purchase and sale contracts or

by using other investment techniques (such as buy backs or dollar rolls and reverse repurchase agreements).

The Sub-Adviser may sell securities for a variety of reasons, such as to secure gains, limit losses, or redeploy assets into

opportunities believed to be more promising.

The Fund may lend portfolio securities on a short-term or long-term basis, up to 33

1

∕

3

% of its total assets.

Other Investment Strategies and Policies

Loans in which the Fund invests typically have multiple interest rate reset periods at the same time, with each reset period

applicable to a designated portion of the loan. The maximum duration of an interest rate reset on any loan in which the Fund

may invest is one year. In order to achieve overall reset balance, the Fund will ordinarily maintain a dollar-weighted average

time until the next interest rate adjustment on its loans of 90 days or less.

To seek to increase the yield on the Common Shares, the Fund may engage in lending its portfolio securities. Such lending

will be fully secured by investment-grade collateral held by an independent agent.

The Fund may engage in executing repurchase agreements and reverse repurchase agreements.

To seek to increase the yield on the Common Shares, the Fund employs financial leverage by borrowing money and may also

issue preferred shares. The timing and terms of leverage will be determined by the Investment Adviser or Sub-Adviser under

the supervision of the Fund's Board of Trustees (the

“

Board

”

). See

“

Risk Factors and Special Considerations - Leverage

”

later in this Prospectus.

The Fund may borrow money in an amount permitted under the 1940 Act, including the rules and regulations thereunder, and

under the terms of applicable no-action relief or exemptive orders granted thereunder. The Fund's obligation to holders of its

debt will be senior to its ability to pay dividends on, or repurchase, Common Shares (and preferred shares, if any), or to pay

holders of Common Shares (and preferred shares, if any) in the event of liquidation.

The Fund is authorized to issue an unlimited number of shares of a class of preferred stock in one or more series (

“

Preferred

Shares

”

). The Fund's obligations to holders of any outstanding Preferred Shares will be senior to its ability to pay dividends

on, or repurchase, Common Shares, or to pay holders of Common Shares in the event of liquidation. Under the 1940 Act,

the Fund may issue Preferred Shares so long as immediately after any issuance of Preferred Shares the value of the Fund's

total assets (less all Fund liabilities and indebtedness that is not senior indebtedness) is at least twice the amount of the

Fund's senior indebtedness plus the involuntary liquidation preference of all outstanding Preferred Shares.

The 1940 Act also requires that the holders of any Preferred Shares of the Fund, voting as a separate class, have the right

to:

elect at least two trustees at all times; and

elect a majority of the trustees at any time when dividends on any series of Preferred Shares are unpaid for two full years.

As of June 6, 2024 the Fund had

no

Preferred Shares outstanding. The Fund may consider issuing Preferred Shares during

the current fiscal year or in the future.

The Fund maintains a diversified investment portfolio through an investment strategy which seeks to limit exposure to any

one issuer or industry.

The Fund is diversified, as such term is defined in the 1940 Act. The Fund’s policy to be diversified is a fundamental policy

that may not be changed without shareholder approval. A diversified fund may not, as to 75% of its total assets, invest more

than 5% of its total assets in any one issuer and may not purchase more than 10% of the outstanding voting securities of

any one issuer (other than securities issued or guaranteed by the U.S. government or any of its agencies or instrumentalities,

or other investment companies). The Fund will consider a borrower on a loan, including a loan participation, to be the issuer

of that loan. In addition, with respect to a loan under which the Fund does not have privity with the borrower or would not

have a direct cause of action against the borrower in the event of the failure of the borrower to make payment of scheduled

principal or interest, the Fund will separately meet the foregoing requirements and consider each interpositioned bank (a

lender from which the Fund acquires a loan) to be an issuer of the loan. With respect to no more than 25% of its total assets,

the Fund may make investments that are not subject to the foregoing restrictions.

In addition, a maximum of 25% of the Fund's total assets, measured at the time of investment, may be invested in any one

industry. This investment strategy is also a fundamental policy that may not be changed without shareholder approval.

The Fund continuously offers its Common Shares for sale. Sales are made through selected broker-dealers and financial

services firms which enter into agreements with Voya Investments Distributor, LLC (the

“

Distributor

”

), the Fund's principal

underwriter. Common Shares are sold at a public offering price equal to their NAV per share. The Fund and the Distributor

reserve the right to reject any purchase order. Please note that cash, traveler's checks, third party checks, money orders,

and checks drawn on non-U.S. banks (even if payment may be effected through a U.S. bank) generally will not be accepted

for purchase of Common Shares.

To maintain a measure of liquidity, the Fund will offer to repurchase not less than 5% of its outstanding Common Shares on

a monthly basis (

“

Repurchase Offers

”

). This is a fundamental policy that can not be changed without shareholder approval.

The Fund currently anticipates offerings to repurchase not less than 5% of its outstanding Common Shares each month. The

Fund may not offer to repurchase more than 25% of its outstanding Common Shares in any calendar quarter. Other than the

Fund's monthly repurchase offers, no market for the Fund's Common Shares is expected to exist. The applicable early withdrawal

charge (

“

EWC

”

) will be imposed on certain repurchased Class A Common Shares and Class C Common Shares. See

“

Sales

Charges

”

and

“

Repurchase Offers

”

later in this Prospectus for important information relating to the acceptance of Fund offers

to repurchase Common Shares.

The price of a company’s stock could decline or underperform for many reasons, including, among others, poor

management, financial problems, reduced demand for the company’s goods or services, regulatory fines and judgments, or

business challenges. If a company is unable to meet its financial obligations, declares bankruptcy, or becomes insolvent, its

stock could become worthless.

Loans in which the Fund may invest or to which the Fund may gain exposure indirectly through its investments

in collateralized debt obligations, CLOs or other types of structured securities may be considered

“

covenant-lite

”

loans. Covenant-lite

refers to loans which do not incorporate traditional performance-based financial maintenance covenants. Covenant-lite does

not refer to a loan’s seniority in a borrower’s capital structure nor to a lack of the benefit from a legal pledge of the borrower’s

assets and does not necessarily correlate to the overall credit quality of the borrower. Covenant-lite loans generally do not

include terms which allow a lender to take action based on a borrower’s performance relative to its covenants. Such actions

may include the ability

to

renegotiate and/or re-set the credit spread on the loan with a borrower, and even to declare a

default or force the borrower into bankruptcy restructuring if certain criteria are breached. Covenant-lite loans typically still

provide lenders with other covenants that restrict a borrower from incurring additional debt or engaging in certain actions.

Such covenants can only be breached by an affirmative action of the borrower, rather than by a deterioration in the borrower’s

financial condition. Accordingly, the Fund may have fewer rights against a borrower when it invests in, or has exposure to,

covenant-lite loans and, accordingly, may have a greater risk of loss on such

investments

as compared to investments in, or

exposure to, loans with additional or more conventional covenants.

The Fund could lose money if the issuer or guarantor of a debt instrument in which the Fund invests, or the counterparty

to a derivative contract the Fund entered into, is unable or unwilling, or is perceived (whether by market participants, rating

agencies, pricing services, or otherwise) as unable or unwilling, to meet its financial obligations.

Asset-backed (including

mortgage-backed) securities that are not issued by U.S. government agencies may have a greater risk of default because

they are not guaranteed by either the U.S. government or an agency or instrumentality of the U.S. government. The credit

quality of typical asset-backed securities depends primarily on the credit quality of the underlying assets and the structural

support (if any) provided to the securities.

The Fund may enter into credit default swaps, either as a buyer or a seller of the swap. A buyer of a

credit default swap is generally obligated to pay the seller an upfront or a periodic stream of payments over the term of the

contract until a credit event, such as a default, on a reference obligation has occurred. If a credit event occurs, the seller

generally must pay the buyer the

“

par value

”

(full notional value) of the swap in exchange for an equal face amount of deliverable

obligations of the reference entity described in the swap, or the seller may be required to deliver the related net cash amount

if the swap is cash settled. As a seller of a credit default swap, the Fund would effectively add leverage to its portfolio because,

in addition to its total net assets, the Fund would be subject to investment exposure on the full notional value of the swap.

Credit default swaps are particularly subject to counterparty, credit, valuation, liquidity, and leveraging risks, and the risk that

the swap may not correlate with its reference obligation as expected. Certain standardized credit default swaps are subject

to mandatory central clearing. Central clearing is expected to reduce counterparty credit risk and increase liquidity; however,

there is no assurance that it will achieve that result, and in the meantime, central clearing and related requirements expose

the Fund to different kinds of costs and risks. In addition, credit default swaps expose the Fund to the risk of improper valuation.

The Fund has a policy of borrowing for cash management and liquidity purposes and for the purpose of investment.

The Fund currently is a party to a credit facility with

The Bank of Nova Scotia

that permits the Fund to borrow up to an aggregate

amount of $

40

million. There is no guarantee that the Fund will continue to be a party to a credit facility or a party to a credit

facility upon similar terms and conditions as currently in place for the Fund. In such cases, the Fund may be limited in its

ability to utilize leverage for investment purposes and this may negatively impact performance. The lender under the credit

facility has a security interest in all assets of the Fund. As of June 6, 2024 the Fund had $

20.0

million in outstanding borrowings

under its credit facility.

Interest is payable on the amounts borrowed under the credit facility at a benchmark rate or the federal funds rate, plus a

facility fee on unused commitments. Under the credit facility, the lender has the right to liquidate Fund assets in the event

of default by the Fund, and the Fund may be prohibited from paying dividends in the event of a material adverse event or

condition regarding the Fund, Investment Adviser, or Sub-Adviser until outstanding debts are paid or until the event or condition

is cured.

Prices of the Fund’s investments are likely to fall if the actual or perceived financial health of the borrowers

on, or issuers of, such investments deteriorates, whether because of broad economic or issuer-specific reasons, or if the

borrower or issuer is late (or defaults) in paying interest or principal. The Fund's investments in U.S. dollar-denominated floating

rate secured senior loans are expected to be rated below investment grade. Below investment grade loans commonly known

as high-yielding, high risk investments or as

“

junk

”

investments involve a greater risk that borrowers may not make timely

payment of the interest and principal due on their loans and are subject to greater levels of credit and liquidity risks. They

also involve a greater risk that the value of such loans could decline significantly. If borrowers do not make timely payments

of the interest due on their loans, the yield on the Common Shares will decrease. If borrowers do not make timely payment

of the principal due on their loans, or if the value of such loans decreases, the net asset value will decrease.

To the extent that the Fund invests directly or indirectly in foreign (non-U.S.) currencies or in securities denominated

in, or that trade in, foreign (non-U.S.) currencies, it is subject to the risk that those foreign (non-U.S.) currencies will decline

in value relative to the U.S. dollar or, in the case of hedging positions, that the U.S. dollar will decline in value relative to the

currency being hedged by the Fund through foreign currency exchange transactions.

An increase in demand for loans may benefit the Fund by providing increased liquidity for such loans and

higher sales prices, but it may also adversely affect the rate of interest payable on such loans and the rights provided to the

Fund under the terms of the applicable loan agreement, and may increase the price of loans in the secondary market. A

decrease in the demand for loans may adversely affect the price of loans in the Fund’s portfolio, which could cause the

Fund’s net asset value to decline and reduce the liquidity of the Fund’s loan holdings.

Derivative instruments are subject to a number of risks, including the risk of changes in the market

price of the underlying asset, reference rate, or index credit risk with respect to the counterparty, risk of

loss

due to changes

in market interest rates, liquidity risk, valuation risk, and volatility risk. The amounts required to purchase certain derivatives

may be small relative to the magnitude of exposure assumed by the Fund. Therefore, the purchase of certain derivatives may

have an economic leveraging effect on the Fund and exaggerate any increase or decrease in the net asset value. Derivatives

may not perform as expected, so the Fund may not realize the intended benefits. When used for hedging purposes, the change

in value of a derivative may not correlate as expected with the asset, reference rate, or index being hedged. When used as

an alternative or substitute for direct cash investment, the return provided by the derivative may not provide the same return

as direct cash investment.

One measure of risk for debt instruments is duration. Duration measures the sensitivity of a bond’s price to market

interest rate movements and is one of the tools used by a portfolio manager in selecting debt instruments. Duration measures

the average life of a bond on a present value basis by incorporating into one measure a bond’s yield, coupons, final maturity

and call features. As a point of reference, the duration of a non-callable 7% coupon bond with a remaining maturity of 5 years

is approximately 4.5 years and the duration of a non-callable 7% coupon bond with a remaining maturity of 10 years is approximately

8 years. Material changes in market interest rates may impact the duration calculation. For example, the price of a bond with

an average duration of 5 years would be expected to fall approximately 5% if market interest rates rose by 1%. Conversely,

the price of a bond with an average duration of 5 years would be expected to rise approximately 5% if market interest rates

dropped by 1%.

In the event a borrower fails to pay scheduled interest or principal payments on a floating rate loan

(which can include certain bank loans), the Fund will experience a reduction in its income and a decline in the market value

of such floating rate loan. If a floating rate loan is held by the Fund through another financial institution, or the Fund relies

upon another financial institution to administer the loan, the receipt of scheduled interest or principal payments may be subject

to the credit risk of such financial institution. Investors in floating rate loans may not be afforded the protections of the anti-fraud

provisions of the Securities Act of 1933,

as amended,

and the Securities Exchange Act of 1934,

as amended,

because loans

may not be considered

“

securities

”

under such laws. Additionally, the value of collateral, if any, securing a floating rate loan

can decline or may be insufficient to meet the borrower’s obligations under the loan, and such collateral may be difficult to

liquidate. No active trading market may exist for many floating rate loans and many floating rate loans are subject to restrictions

on resale. Transactions in loans typically settle on a delayed basis and may take longer than 7 days to settle. As a result,

the Fund may not receive the proceeds from a sale of a floating rate loan for a significant period of time. Delay in the receipts

of settlement proceeds may impair the ability of the Fund to meet its redemption obligations, and may limit the ability of the

Fund to repay debt, pay dividends, or to take advantage of new investment opportunities.

Foreign (Non-U.S.) Investments:

Investing in foreign (non-U.S.) securities may result in the Fund experiencing more rapid and

extreme changes in value than a fund that invests exclusively in securities of U.S. companies due, in part, to: smaller markets;

differing reporting, accounting, auditing and financial reporting standards and practices; nationalization, expropriation, or

confiscatory taxation; foreign currency fluctuations, currency blockage, or replacement; potential for default on sovereign debt;

and political changes or diplomatic developments, which may include the imposition of economic sanctions (or the threat of

new or modified sanctions) or other measures by the U.S. or other governments and supranational organizations. Markets

and economies throughout the world are becoming increasingly interconnected, and conditions or events in one market, country

or region may adversely impact investments or issuers in another market, country or region.

Foreign (Non-U.S.) and Non-Canadian Issuers:

Investment in foreign (non-U.S.) borrowers involves special risks, including

that foreign (non-U.S.) borrowers may be subject to: less rigorous regulatory, accounting, and reporting requirements than

U.S. borrowers; differing legal systems and laws relating to creditors’ rights; the potential inability to enforce legal judgments;

economic adversity that would result if the value of the borrower’s foreign (non-U.S.) dollar denominated revenues and assets

were to fall because of fluctuations in currency values; and the potential for political, social, and economic adversity in the

foreign (non-U.S.) borrower’s country.

Lower-quality securities (including securities that are or have fallen below investment grade and are

classified as

“

junk bonds

”

or

“

high-yield securities

”

) have greater credit risk and liquidity risk than higher-quality (investment

grade) securities, and their issuers' long-term ability to make payments is considered speculative. Prices of lower-quality bonds

or other debt instruments are also more volatile, are more sensitive to negative news about the economy or the issuer, and

have greater liquidity risk and price volatility.

The value and the income streams of interests in loans (including participation interests in lease financings

and assignments in secured variable or floating rate loans) will decline if borrowers delay payments or fail to pay altogether.

A significant rise in market interest rates could increase this risk. Although loans may be fully collateralized when purchased,

such collateral may become illiquid or decline in value.

Changes in short-term market interest rates will directly affect

the

yield on Common Shares. If short-term

market interest rates fall, the yield on Common Shares will also fall. To the extent that the interest rate spreads on loans in

the Fund’s portfolio experience a general decline, the yield on the Common Shares will fall and the value of the Fund’s assets

may decrease, which will cause the Fund’s net asset value to decrease. Conversely, when short-term market interest rates

rise, because of the lag between changes in such short-term rates and the resetting of the floating rates on assets

in

the

Fund’s portfolio, the impact of rising rates will be delayed to the extent of such lag. In the case of inverse securities, the

interest rate paid by such securities generally will decrease when the market rate of interest to which the inverse security is

indexed increases. With respect to investments in fixed rate instruments, a rise in market interest rates generally causes

values of such instruments to fall. The values of fixed rate instruments with longer maturities or duration are more sensitive

to changes in market interest rates.

As of the date of this Prospectus, the United States has recently experienced a rising market interest rate environment, which

may increase the Fund’s exposure to risks associated with rising market interest rates. Rising market interest rates could

have unpredictable effects on the markets and may expose debt and related markets to heightened volatility, which could

reduce liquidity for certain investments, adversely affect values, and increase costs. If dealer capacity in debt and related

markets is insufficient for market conditions, it may further inhibit liquidity and increase volatility in the debt and related

markets. Further, recent and potential changes in government policy may affect interest rates.

Interest Rate for Floating Rate Loans:

Changes in short-term market interest rates will directly affect the yield on investments

in floating rate loans. If short-term market interest rates fall, the yield on the Fund’s shares will also fall. To the extent that

the interest rate spreads on loans in the Fund’s portfolio experience a general decline, the yield on the Fund’s shares will

fall and the value of the Fund’s assets may decrease, which will cause the Fund’s net asset value to decrease. Conversely,

when short-term market interest rates rise, because of the lag between changes in such short-term rates and the resetting

of the floating rates on assets in the Fund’s portfolio, the impact of rising rates will be delayed to the extent of such lag. The

impact of market interest rate changes on the Fund’s yield will also be affected by whether, and the extent to which, the

floating rate loans in the Fund’s portfolio are subject to floors on the secured overnight funding rate (

“

SOFR

”

) base rate on

which interest is calculated for such loans (a

“

benchmark floor

”

). So long as the base rate for a loan remains under the

applicable benchmark floor, changes in short-term market interest rates will not affect the yield on such loans. In addition,

to the extent that changes in market interest rates are reflected not in a change to a base rate such as SOFR but in a change

in the spread over the base rate which is payable on the floating rate loans of the type and quality in which the Fund invests,

the Fund’s net asset value could also be adversely affected. With respect to investments in fixed rate instruments, a rise in

market interest rates generally causes values of such instruments to fall. The values of fixed rate instruments with longer

maturities or duration are more sensitive to changes in market interest rates. As of the date of this Prospectus, the U.S has

recently experienced a rising market interest rate environment, which may increase the Fund’s exposure to risks associated

with rising market interest rates. Rising market interest rates have unpredictable effects on the markets and may expose

debt and related markets to heightened volatility, which could reduce liquidity for certain investments, adversely affect values,

and increase costs. Increased redemptions may cause the Fund to liquidate portfolio positions when it may not be advantageous

to do so and may lower returns. If dealer capacity in debt and related markets is insufficient for market conditions, it may

further inhibit liquidity and increase volatility in the debt and related markets. Further, recent and potential future changes in

government policy may affect interest rates.

An interest rate swap is an agreement that obligates two parties to exchange a series of cash flows

for a specified period of time based upon or calculated by reference to a specified interest rate(s) for a specified amount.

Interest rate swaps involve the risk that changes in market conditions may affect the value of the contract or the cash flows,

and the possible inability or unwillingness of the counterparty to fulfill its obligations under the agreement. An interest rate

swap arrangement may not fully offset adverse changes in interest rates. Interest rate swaps are also subject to liquidity risk

and interest rate risk.

The use of leverage through borrowings or the issuance of Preferred Shares can adversely affect the yield on the

Common Shares. To the extent that the Fund is unable to invest the proceeds from the use of leverage in assets which pay

interest at a rate which exceeds the rate paid on the leverage, the yield on the Common Shares will decrease. In addition,

in the event of a general market decline in the value of assets such as those in which the Fund invests, the effect of that

decline will be magnified in the Fund because of the additional assets purchased with the proceeds of the leverage. Further,

because the fee paid to the Investment Adviser will be calculated on the basis of Managed Assets, the fee will be higher when

leverage is utilized, giving the Investment Adviser an incentive to utilize leverage. The Fund is subject

to

certain restrictions

imposed by lenders to the Fund and may be subject to certain restrictions imposed by guidelines of one or more rating agencies

which may issue ratings for debt or the Preferred Shares issued by the Fund. These restrictions are expected to impose asset

coverage, fund composition requirements and limits on investment techniques, such as the use of financial derivative products

that are more stringent than those imposed on the Fund by the 1940 Act. These restrictions could impede the manager from

fully managing the Fund’s portfolio in accordance with the Fund’s investment objective and policies. As of June 6, 2024 the

Fund had $

20.0

million in outstanding borrowings under its credit facility.

Limited Liquidity For Investors:

The Fund does not repurchase its shares on a daily basis and no market for the Common

Shares is expected to exist. To provide a measure of liquidity, the Fund will normally make monthly repurchase offers for not

less than 5% of its outstanding Common Shares. If more than 5% of Common Shares are tendered, investors may not be

able to completely liquidate their holdings in any one month. Shareholders also will not have liquidity between these monthly

repurchase dates.

Limited Secondary Market for Loans:

Because of the limited secondary market for loans, the Fund may be limited in its

ability to sell loans in its portfolio in a timely fashion and/or at a favorable price. Transactions in loans typically settle on a

delayed basis and typically take longer than 7 days to settle. As a result the Fund may not receive the proceeds from a sale

of a floating rate loan for a significant period of time. Delay in the receipts of settlement proceeds may impair the ability of

the Fund to meet its repurchase obligations and may increase the amounts the Fund may be required to borrow. It may also

limit the ability of the Fund to repay debt, pay dividends, or to take advantage of new investment opportunities.

If a security is illiquid, the Fund might be unable to sell the security at a time when the Fund’s manager might wish

to sell, or at all. Further, the lack of an established secondary market may make it more difficult to value illiquid securities,

exposing the Fund to the risk that the prices at which it sells illiquid securities will be less than the prices at which they were

valued when held by the Fund, which could cause the Fund to lose money. The prices of illiquid securities may be more volatile

than more liquid securities, and the risks associated with illiquid securities may be greater in times of financial stress.

Certain

securities that are liquid when purchased may later become illiquid, particularly in times of overall economic distress or due

to geopolitical events such as sanctions, trading halts, or wars.

The market values of securities will fluctuate, sometimes sharply and unpredictably, based on overall economic conditions,

governmental actions or intervention, market disruptions caused by trade disputes or other factors, political developments,

and other factors. Prices of equity securities tend to rise and fall more dramatically than those of debt instruments. Additionally,

legislative, regulatory or tax policies or developments may adversely impact the investment techniques available to a manager,

add to costs, and impair the ability of the Fund to achieve its investment objectives.

Market Disruption and Geopolitical:

The Fund is subject to the risk that geopolitical events will disrupt securities markets

and adversely affect global economies and markets. Due to the increasing interdependence among global economies and

markets, conditions in one country, market, or region might adversely impact markets, issuers and/or foreign exchange rates

in other countries, including the United States. Wars, terrorism, global health crises and pandemics, and other geopolitical

events that have led, and may continue to lead, to increased market volatility and may have adverse short- or long-term effects

on U.S. and global economies and markets, generally. For example, the COVID-19 pandemic resulted in significant market

volatility, exchange suspensions and closures, declines in global financial markets, higher default rates, supply chain disruptions,

and a substantial economic downturn in economies throughout the world. The economic impacts of COVID-19 have created

a unique challenge for real estate markets. Many businesses have either partially or fully transitioned to a remote-working

environment and this transition may negatively impact the occupancy rates of commercial real estate over time. Natural and

environmental disasters and systemic market dislocations are also highly disruptive to economies and markets. In addition,

military action by Russia in Ukraine has, and may continue to, adversely affect global energy and financial markets and therefore

could affect the value of the Fund’s investments, including beyond the Fund’s direct exposure to Russian issuers or nearby

geographic regions. The extent and duration of the military action, sanctions, and resulting market disruptions are impossible

to predict and could be substantial. A number of U.S. domestic banks and foreign (non-U.S.) banks have recently experienced

financial difficulties and, in some cases, failures. There can be no certainty that the actions taken by regulators to limit the

effect of those financial difficulties and failures on other banks or other financial institutions or on the U.S. or foreign (non-U.S.)

economies generally will be successful. It is possible that more banks or other financial institutions will experience financial

difficulties or fail, which may affect adversely other U.S. or foreign (non-U.S.) financial institutions and economies. These

events as well as other changes in foreign (non-U.S.) and domestic economic, social, and political conditions also could adversely

affect individual issuers or related groups of issuers, securities markets, interest rates, credit ratings, inflation, investor sentiment,

and other factors affecting the value of the Fund’s investments. Any of these occurrences could disrupt the operations of the

Fund and of the Fund’s service providers.

Other Investment Companies:

The main risk of investing in other investment companies, including ETFs, is the risk that the

value of an investment company’s underlying investments might decrease. Shares of investment companies that are listed

on an exchange may trade at a discount or premium from their net asset value. You will pay a proportionate share of the

expenses of those other investment companies (including management fees, administration fees, and custodial fees) in addition

to the Fund’s expenses. The investment policies of the other investment companies may not be the same as those of the

Fund; as a result, an investment in the other investment companies may be subject to additional or different risks than those

to which the Fund is typically subject. In addition, shares of ETFs may trade at a premium or discount to net asset value and

are subject to secondary market trading risks. Secondary markets may be subject to irregular trading activity, wide bid/ask

spreads, and extended trade settlement periods in times of market stress because market makers and authorized participants

may step away from making a market in an ETF’s shares, which could cause a material decline in the ETF’s net asset value.

Prepayment and Extension:

Many types of debt instruments are subject to prepayment and extension risk. Prepayment risk

is the risk that the issuer of a debt instrument will pay back the principal earlier than expected. This risk is heightened in a

falling market interest rate environment. Prepayment may expose the Fund to a lower rate of return upon reinvestment of

principal. Also, if a debt instrument subject to prepayment has been purchased at a premium, the value of the premium would

be lost in the event of prepayment. Extension risk is the risk that the issuer of a debt instrument will pay back the principal

later than expected. This risk is heightened in a rising market interest rate environment. This may negatively affect performance,

as the value of the debt instrument decreases when principal payments are made later than expected. Additionally, the Fund

may be prevented from investing proceeds it would have received at a given time at the higher prevailing interest rates.

Loans

typically have a 6-12 month call protection and may be prepaid partially or in full after the call protection period without penalty.

Securities lending involves two primary risks:

“

investment risk

”

and

“

borrower default risk.

”

When lending

securities, the Fund will receive cash or U.S. government securities as collateral. Investment risk is the risk that the Fund

will lose money from the investment of the cash collateral received from the borrower. Borrower default risk is the risk that

the Fund will lose money due to the failure of a borrower to return a borrowed security. Securities lending may result in leverage.

The use of

leverage

may exaggerate any increase or decrease in the net asset value, causing the Fund to be more volatile.

The use of leverage may increase expenses and increase the impact of the Fund’s other risks.

A

“

special situation

”

arises when, in a manager’s opinion, securities of a particular company will appreciate

in value within a reasonable period because of unique circumstances applicable to the company. Special situations investments

often involve much greater risk than is inherent in ordinary investments. Investments in special situation companies may not

appreciate and the Fund’s performance could suffer if an anticipated development does not occur or does not produce the

anticipated result.

Temporary Defensive Positions:

When market conditions make it advisable, the Fund may hold a portion of its assets in

cash and short-term interest bearing instruments. Moreover, in periods when, in the opinion of the manager, a temporary

defensive position is appropriate, up to 100% of the Fund’s assets may be held in cash, short-term interest bearing instruments

and/or any other securities the manager considers consistent with a temporary defensive position. The Fund may not achieve

its investment objective when pursuing a temporary defensive position.

The Fund values its assets every day the New York Stock Exchange is open for regular trading. However,

because the secondary market for floating rate loans is limited, it may be difficult to value loans, exposing the Fund to the

risk that the price at which it sells loans will be less than the price at which they were valued when held by the

Fund

. Reliable

market value quotations may not be readily available for some loans, and determining the fair valuation of such loans may

require more research than for securities that trade in a more active secondary market. In addition, elements of judgment

may play a greater role in the valuation of loans than for more securities that trade in a more developed secondary market

because there is less reliable, objective market value data available. If the Fund purchases a relatively large portion of a

loan, the limitations of the secondary market may inhibit the Fund from selling a portion of the loan and reducing its exposure

to a borrower when the manager deems it advisable to do so. Even if the Fund itself does not own a relatively large portion

of a particular loan, the Fund, in combination with other similar accounts under management by the same portfolio managers,

may own large portions of loans. The aggregate amount of holdings could create similar risks if and when the portfolio managers

decide to sell those loans. These risks could include, for example, the risk that the sale of an initial portion of the loan could

be at a price lower than the price at which the loan was valued by the Fund, the risk that the initial sale could adversely impact

the price at which additional portions of the loan are sold, and the risk that the foregoing events could warrant a reduced

valuation being assigned to the remaining portion of the loan still owned by the Fund.

When-Issued, Delayed Delivery, and Forward Commitment

Transactions

:

When-issued, delayed delivery, and forward commitment

transactions involve the risk that the security the Fund buys will lose value prior to its delivery. These transactions may result

in leverage. The use of leverage may exaggerate any increase or decrease in the net asset value,

causing

the Fund to be

more volatile. The use of leverage may increase expenses and increase the impact of the Fund’s other risks. There also is

the risk that the security will not be issued or that the other party will not meet its obligation. If this occurs, the Fund loses

both the investment opportunity for the assets it set aside to pay for the security and any gain in the security’s price.

WHAT YOU PAY TO INVEST - FUND EXPENSES

This table is intended to assist investors in understanding the various costs and expenses directly or indirectly associated

with investing in the Fund. The cost you pay to invest in the Fund varies depending upon which class of Common

Shares you purchase. In accordance with SEC requirements, the table below shows the expenses of the Fund, including

interest expense on borrowings, as a percentage of the average net assets of the Fund and not as a percentage of

gross assets or Managed Assets. By showing expenses as a percentage of the average net assets, expenses are not

expressed as a percentage of all of the assets that are invested for the Fund. The table below assumes that the Fund

has borrowed an amount equal to 25% of its Managed Assets. For information about the Fund’s expense ratios if the

Fund had not borrowed, see

“

Risk Factors and Special Considerations - Annual Expenses Without Borrowings.

”

Investors

investing in the Fund through an intermediary should consult the Appendix to this Prospectus, which includes information

regarding financial intermediary specific sales charges and related discount policies that apply to purchases through

certain specified intermediaries.

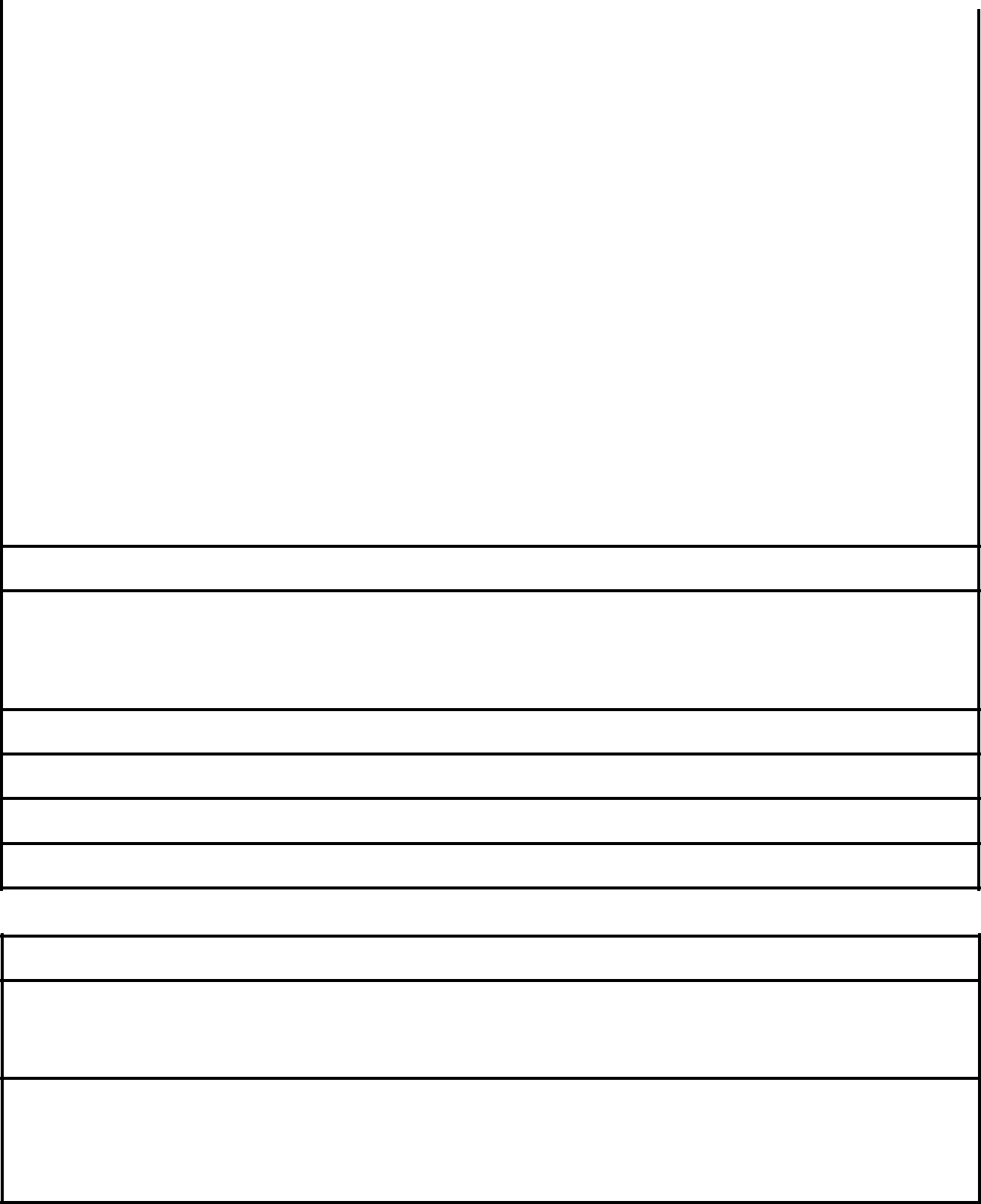

Fees and Expenses of the Fund

| | | | |

Shareholder Transaction Expenses | | | |

Maximum sales charge on your investment (as a percentage of offering price) | | | | |

Dividend Reinvestment and Cash Purchase Plan Fees | | | | |

| | | | |

| | | | |

Annual Expenses (as a percentage of average net assets attributable to Common Shares) | | | |

| | | | |

| | | | |

| | | | |

Interest Expense on Borrowed Funds | | | | |

| | | | |

| | | | |

Fee Waivers/Reimbursements/Recoupment | | | | |

| | | | |

The Distributor will pay a dealer reallowance for Class A Common Shares from the sales charge. The Distributor will pay a sales commission for Class C Common Shares to

authorized dealers from its own assets.

Reduced for purchases of $100,000 and over for Class A Common Shares, please see

“

Sales Charges.

”

There is no front-end sales charge if you purchase Class A Common Shares in the amount of $500,000 or more. Class A Common Shares purchased in an amount of $500,000

or more are subject to a 1.00% EWC if repurchased by the Fund within 12 months of purchase. Class C Common Shares repurchased by the Fund within the first year after

purchase will incur a 1.00% EWC. See

“

Sales Charges - Early Withdrawal Charge.

”

No EWC will be charged on redemptions that are due to the closing of shareholder accounts

having a value of less than $1,000.

Pursuant to the investment management agreement with the Fund, the Investment Adviser is paid a fee of 0.80% of the Fund's Managed Assets. For the description of

“

Managed

Assets,

”

please see

“

Description of the Fund – Investment Adviser/Sub-Adviser

”

earlier in this Prospectus.

Because the distribution fees payable by Class C Common Shares may be considered an asset-based sales charge, long-term shareholders in that class of the Fund may pay

more than the economic equivalent of the maximum front-end sales charges permitted by the Financial Industry Regulatory Authority.

Other Operating Expenses are estimated amounts for the current fiscal year.

The Investment Adviser is contractually obligated to limit expenses of the Fund through

July 1, 2025

to the following: Class A Common Shares - 0.90% of Managed Assets

plus 0.45% of average daily net assets; Class C Common Shares - 0.90% of Managed Assets plus 0.95% of average daily net assets; Class I Common Shares - 0.90% of

Managed Assets plus 0.20% of average daily net assets; and Class W Common Shares - 0.90% of Managed Assets plus 0.20% of average daily net assets. The obligation is

subject to possible recoupment by the Investment Adviser within 36 months of the waiver or reimbursement. The Investment Adviser is contractually obligated to further limit

expenses of the Fund through

July 1, 2025

to the following: Class A Common Shares - 0.80% of Managed Assets plus 0.45% of average daily net assets; Class C Common

Shares - 0.80% of Managed Assets plus 0.95% of average daily net assets; Class I Common Shares - 0.80% of Managed Assets plus 0.20% of average daily net assets; and

Class W Common Shares - 0.80% of Managed Assets plus 0.20% of average daily net assets. These limitations do not extend to interest, taxes, investment-related costs,

leverage expenses, extraordinary expenses, and Acquired Fund Fees and Expenses. Termination or modification of these obligations requires approval by the Fund’s Board.

If the expenses of the Fund are calculated on the Managed Assets of the Fund (assuming that the Fund has used leverage by borrowing an amount equal to 25% of the Fund’s

Managed Assets), the Net Annual Expenses for the Fund would be lower than the expenses shown in the table. Such lower Net Annual Expense ratios would be as follows:

2.99

%,

3.49

%,

2.74

%, and

2.74

% for Class A, Class C, Class I, and Class W shares, respectively.

WHAT YOU PAY TO INVEST - FUND EXPENSES

The following Examples show the amount of the expenses that an investor in the Fund would bear on a $1,000 investment

in the Fund that is held for the different time periods in the table. In the first table, it is assumed that the $1,000

remains invested over the entire 10-year period. As a result, no EWCs are included in the listed expense amounts.

The second table assumes that the $1,000 investment is tendered and repurchased at the end of each period shown.

As a result, EWCs are imposed on certain of those repurchases.

The Examples assume that all dividends and other distributions are reinvested at NAV and that the percentage amounts

listed under Net Annual Expenses in the previous table remain the same in the years shown (except that the Fee

Waivers/Reimbursements only apply for the first year). The tables and the assumption in the Examples of a 5% annual

return are required by regulations of the SEC applicable to all investment companies. The assumed 5% annual return