Legal Notice and Disclaimer

This valuation report (the “Report”) has been prepared by CBRE Limited (“CBRE”) exclusively for Morgan Stanley Collateral Valuation Team, Morgan Stanley Bank N.A., Morgan Stanley Mortgage Capital Holdings LLC (the “Client”) in accordance with the terms of engagement entered into between CBRE and the client dated 10 March 2021 (“the Instruction”). The Report is confidential to the Client and any other Addressees named herein and the Client and the Addressees may not disclose the Report unless expressly permitted to do so under the Instruction.

Where CBRE has expressly agreed (by way of a reliance letter) that persons other than the Client or the Addressees can rely upon the Report (a “Relying Party” or “Relying Parties”) then CBRE shall have no greater liability to any Relying Party than it would have if such party had been named as a joint client under the Instruction.

CBRE’s maximum aggregate liability to the Client, Addressees and to any Relying Parties howsoever arising under, in connection with or pursuant to this Report and/or the Instruction together, whether in contract, tort, negligence or otherwise shall not exceed the lower of:

| (i) | 25% of the value of the property to which the Instruction relates (as at the valuation date); or |

| (ii) | €100,000,000 [One Hundred Million Euros]. |

Subject to the terms of the Instruction, CBRE shall not be liable for any indirect, special or consequential loss or damage howsoever caused, whether in contract, tort, negligence or otherwise, arising from or in connection with this Report. Nothing in this Report shall exclude liability which cannot be excluded by law.

If you are neither the Client, an Addressee nor a Relying Party then you are viewing this Report on a non-reliance basis and for informational purposes only. You may not rely on the Report for any purpose whatsoever and CBRE shall not be liable for any loss or damage you may suffer (whether direct, indirect or consequential) as a result of unauthorised use of or reliance on this Report. CBRE gives no undertaking to provide any additional information or correct any inaccuracies in the Report.

If another CBRE Group entity contributes to the preparation of the Report, that entity may co-sign the Report purely to confirm its role as contributor. The Client, Relying Party or any other Addressees named herein acknowledge that no duty of care, whether existing under the Instruction or under the Report, shall extend to such CBRE Group entity and the Client, Relying Party or any other Addressees named herein hereby waive any right or recourse against such CBRE Group entity whether arising in contract, tort, negligence or otherwise. CBRE shall remain solely liable to the client in accordance with the terms of the Instruction

None of the information in this Report constitutes advice as to the merits of entering into any form of transaction.

If you do not understand this legal notice then it is recommended that you seek independent legal advice.

CONTENTS

| PART I | VALUATION REPORT | 4 |

| VALUATION REPORT | 5 | |

| SOURCES OF INFORMATION AND SCOPE OF WORKS | 12 | |

| VALUATION ASSUMPTIONS | 15 | |

| PART II | PROPERTY REPORT | 21 |

| PART III | APPENDICES | |

| APPENDIX A | ||

| TERMS OF ENGAGEMENT LETTER | ||

| APPENDIX B | ||

| SCHEUDLE OF VALUES | ||

| APPENDIX C | ||

| MARKET REPORT | ||

| APPENDIX D | ||

| SUMMARY VALUATION REPORT |

VALUATION REPORT

CBRE Limited

St Martins Court

10 Paternoster Row

London EC4M 7HP

| Switchboard | +44 20 7182 2000 | |

| Fax | +44 20 7182 2273 |

| “This report was prepared for and may be relied upon by Morgan Stanley Bank, N.A., Morgan Stanley Mortgage Capital Holdings LLC, as client but we agree that this report will, subject to that incoming party first signing and returning to CBRE a reliance letter, be capable of being relied upon by the following: | ||

| (a) The respective affiliates of Morgan Stanley Bank, N.A.; | ||

| (b) each Finance Party (under and as defined in the Senior Facilities Agreement (defined below)); | ||

| (c) each Finance Party (under and defined in the Mezzanine Facilities Agreement (defined below)); | ||

| (d) each successor, assignee and/or a transferee of any Finance Party under the Senior Facilities Agreement and/or the Mezzanine Facilities Agreement (each as defined below), | ||

| (e) each issuer, bond or note trustee, security trustee, agent, manager, hedging counterparty, liquidity facility provider or other support provider in connection with any securitisation (or any other transaction having a similar effect) of either a senior facility provided under any Senior Facilities Agreement (defined below) or a mezzanine facility provided under any Mezzanine Facilities Agreement (defined below), | ||

|

each an “Addressee” and together the “Addressees” In this Report: |

| (a) “Senior Facilities Agreement” means the senior facilities agreement to be entered into between, amongst others, MLET Pledgeco Sarl as Senior Company, Morgan Stanley Principal Funding, Inc as Senior Arranger, and CBRE Loan Services Limited as Senior Facility Agent and Common Security Agent; and | ||

| (b) “Mezzanine Facilities Agreement” means the mezzanine facilities agreement to be entered into between, amongst others, MLET Mezzco Sarl as Mezzanine Company, Eagle Holdco S.à r.l and Coscile Investment S.à r.l. as Mezzanine Arrangers, and LaSalle Investment Management as Mezzanine Facility Agent and Mezzanine Security Agent.” |

www.cbre.co.uk

Registered in England No 3536032 Registered Office St Martin’s Court 10 Paternoster Row London EC4M 7HP

CBRE Limited is regulated by the RICS

| The Property | The MStar portfolio as summarised in the schedule of capital values. | |

| Property Description | 49 assets located across Germany and The Netherlands, as summarised in the schedule of capital values. The portfolio predominantly includes logistics, warehouse, industrial or light industrial assets either used in part or featuring ancillary office, commercial (including showroom / trade counter), storage or space designated as other. One asset in the portfolio would be considered an office asset (Nieuwegen). | |

| Ownership Purpose | Investment | |

| Instruction | To value the unencumbered freehold and leasehold interest in the Property on the basis of Market Value as at the Valuation date in accordance with the terms of engagement entered into between CBRE and the addressee dated 10 March 2021. | |

| Valuation Date | 01 February 2021 | |

| Capacity of Valuer | External Valuer, as defined in the current version of the RICS Valuation – Global Standards effective from 31 January 2020. | |

| Purpose | Secured Lending purposes only | |

|

Where you have advised us that the valuation is required for your use in a particular secured lending transaction, we consent to its use solely for that transaction. Where you have not

revealed to us details of a particular lending transaction, we consent to its use only in a single secured lending decision.

|

||

| Market Value | €570,010,000 (Five Hundred and Seventy Million and Ten Thousand Euros) exclusive of VAT. | |

| Special Assumption | €469,860,000 (Four Hundred and Sixty Nine Eight Hundred and Sixty Thousand Euros) exclusive of VAT. | |

| Vacant Possession Value | ||

|

Where a property is owned by way of a joint tenancy in a trust for sale, or through an indirect investment structure, our Valuation represents the relevant apportioned percentage of ownership of the value of the whole property, assuming full management control. Our Valuation does not necessarily represent the ‘Market Value’ (as defined in RICS Valuation - Global Standards 2020) of the interests in the indirect investment structure through which the Property is held. |

||

| Our opinion of Market Value is based upon the Scope of Work and Valuation Assumptions attached, and has been primarily derived using comparable recent market transactions on arm’s length terms. We consider the current use of the assets to be highest and best in the absence of more thorough investigations into the feasibility of alternatives which did not form part of the scope of works, this includes assessing the underlying land value. | ||

| We have valued the Properties individually and no account has been taken of any discount or premium that may be negotiated in the market if all or part of the portfolio was to be marketed simultaneously, either in lots or as a whole. |

| VALUATION REPORT | 7 | |

| Market conditions explanatory note: Novel Coronavirus (COVID-19) | The outbreak of the Novel Coronavirus (COVID-19), declared by the World Health Organisation as a “Global Pandemic” on the 11th March 2020, continues to impact many aspects of daily life and the global economy – with some real estate markets having experienced lower levels of transactional activity and liquidity. Travel, movement and operational restrictions have been implemented by many countries. In some cases, “lockdowns” have been applied – in varying degrees – to reflect further ‘waves’ of COVID-19. While these may imply a new stage of the crisis, they are not unprecedented in the same way as the initial impact. | |

| The pandemic and the measures taken to tackle COVID-19 continue to affect economies and real estate markets globally. Nevertheless, as at the valuation date, property markets are mostly functioning again, with transaction volumes and other relevant evidence at levels where enough market evidence exists upon which to base opinions of value. Accordingly – and for the avoidance of doubt – our valuation is not reported as being subject to ‘material valuation uncertainty’, as defined by VPS 3 and VPGA 10 of the RICS Valuation – Global Standards. | ||

| For the avoidance of doubt this explanatory note has been included to ensure transparency and to provide further insight as to the market context under which the valuation opinion was prepared. In recognition of the potential for market conditions to move rapidly in response to changes in the control or future spread of COVID-19, we highlight the importance of the valuation date. | ||

| Rental Income | The valuation we have provided reflects the rental income as at the date of valuation, as set out within this report, which you have confirmed to be correct and comprehensive. It also reflects any issues concerning the anticipated cash-flow that you have advised us of, as set out within this report. Given the uncertainties relating to the Covid-19 virus and the current restrictions on business activities, it is likely that there will be significant rental defaults and/or insolvencies leading to voids and a resulting shortfall in rental income. Should this occur, there will be a negative impact on the value of the subject property | |

| Suitability of the property as security for mortgage purposes | We have not been provided with details of the loan amount and loan terms proposed and therefore cannot comment on the suitability of the property for the proposed loan. We recommend that the Bank provides us with these details for our comment. | |

| Compliance with Valuation Standards | The valuation has been prepared in accordance with the current version of the RICS Valuation – Global Standards (incorporating the International Valuation Standards) and the UK national supplement 2018. | |

| We confirm that we have sufficient current local and national knowledge of the particular property market involved, and have the skills and understanding to undertake the Valuation competently. | ||

| Where the knowledge and skill requirements of the Red Book have been met in aggregate by more than one valuer within CBRE, we confirm that a list of those valuers has been retained within the working papers, together with confirmation that each named valuer complies with the requirements of the Red Book. | ||

| This Valuation is a professional opinion and is expressly not intended to serve as a warranty, assurance or guarantee of any particular value of the subject property. Other valuers may reach different conclusions as to the value of the subject property. This Valuation is for the sole purpose of providing the intended user with |

| VALUATION REPORT | 8 | |

| the valuer’s independent professional opinion of the value of the subject property as at the Valuation date. | ||

| Assumptions | The Property details on which the Valuation is based are as set out in this report. We have made various assumptions as to tenure, letting, taxation, town planning, and the condition and repair of buildings and sites – including ground and groundwater contamination – as set out below. | |

| If any of the information or assumptions on which the Valuation is based are subsequently found to be incorrect, the Valuation figure may also be incorrect and should be reconsidered. | ||

| Variation from Standard Assumptions | None | |

| Special Assumption – Vacant Possession Value | Special Assumptions have been applied. | |

| As requested, we have prepared a valuation of each asset on the special assumption that they are entirely vacant as at the valuation date. | ||

| Special Assumption – Portfolio Sale | As requested, we have prepared a market valuation of the properties under the following assumption of a portfolio sale: | |

| • That that all the properties will be transferred in a single company transaction and as such will not incur any property transfer tax. | ||

| • That other acquisition costs amount to 2.5%. | ||

| • That the subject properties are the company’s sole assets. | ||

| • That the sale of the properties within the company structure will not trigger any latent capital gains tax liabilities. | ||

| • That the company being purchased has no extraordinary responsibilities and is free of any other liabilities. | ||

| • That the company has no employees. | ||

| • That no discount on the purchase price is agreed to reflect any latent capital gains tax liability in the event of future real estate transactions. | ||

| Verification | We recommend that before any financial transaction is entered into based upon these Valuations, you obtain verification of any third-party information contained within our report and the validity of the assumptions we have adopted. | |

| We would advise you that whilst we have valued the Property reflecting current market conditions, there are certain risks which may be, or may become, uninsurable. Before undertaking any financial transaction based upon this Valuation, you should satisfy yourselves as to the current insurance cover and the risks that may be involved should an uninsured loss occur. | ||

| Valuer | The Property has been valued by a valuer who is qualified for the purpose of the Valuation in accordance with the Red Book. | |

| Previous involvement and Conflicts of Interest | As you are aware, we valued the properties on behalf of RBC Europe Limited in December 2019 for secured lending purposes, albeit the instruction was aborted without being finalised. Prior to that we valued the assets for M7 in December 2016. |

| VALUATION REPORT | 9 | |

|

We have disclosed the relevant facts to you and the other clients involved and have received everyone’s confirmation that there is no issue with us valuing these specific assets as part of the instruction. With

the exception of the above, we confirm that we have had no previous material involvement with the property and that copies of our conflict of interest checks have been retained within the working papers.

|

||||

| Reliance | The contents of this Report may only be relied upon by: | |||

| (i) | Addressees of the Report; and | |||

| (ii) | Parties who have received prior written consent from CBRE in the form of a reliance letter; | |||

|

for the specific purpose set out herein and no responsibility is accepted to any third party for the whole or any part of its contents.

|

||||

|

The Valuation shall be disclosed on a non-reliance basis to:

|

||||

|

● The respective agents, trustees and advisers of the Addressees in connection with the transactions described in paragraph 1 above;

|

||||

|

● the respective affiliates, employees, officers, directors and auditors of the Addressees;

|

||||

|

● any prospective purchaser, transferee or assignee of, participant in, or hedge counterparty in respect of, any related loan made under the Senior Facilities

Agreement and/or Mezzanine Facilities Agreement;

|

||||

|

● any servicer of any loan under the Senior Facilities Agreement and/or the Mezzanine Facilities Agreement, and its advisers;

|

||||

|

● any prospective purchaser of any property or shares in an entity that owns any property either directly or indirectly;

|

||||

|

● to any person to whom disclosure is required by law, court order or regulation in connection with legal or arbitration proceedings;

|

||||

|

● any entity that becomes an agent or senior facility agent on behalf of lender-parties to a credit agreement;

|

||||

|

● to any potential issuer of, or potential investor in, commercial mortgage backed securities issued in connection with either a Senior Facilities Agreement

and/or a Mezzanine Facilities Agreement (each a “CMBS Product”);

|

||||

|

● to any rating agency (actually or prospectively) rating any CMBS Product and to any of their respective directors, officers, employees, representatives,

agents, auditors and professional advisers, provided that any such auditor or professional advisor is bound by professional confidentiality obligations to that rating agency;

|

||||

|

● to any person pursuant to the rules of a stock exchange, listing authority or similar body; and

|

||||

|

● any Governmental, banking, taxation or other regulatory authority.

|

||||

| Publication |

Neither the whole nor any part of our report nor any references thereto may be included in any published document, circular or statement nor published in any way without our prior written approval of the form and context in which it will

appear.

|

|||

|

Such publication of, or reference to this report will not be permitted unless it contains a sufficient contemporaneous reference to any departure from the Red Book or the

incorporation of the special assumptions referred to herein.

|

||||

| VALUATION REPORT | 10 | |

| Yours faithfully | Yours faithfully | ||

| Graham MacMillan | Peter Beatty | ||

| Executive Director | Director | ||

| RICS Registered Valuer | RICS Registered Valuer | ||

| For and on behalf of | For and on behalf of | ||

| CBRE Ltd | CBRE Ltd | ||

| +44 (0)20 7182 2699 | +44 (0)20 7182 2288 | ||

| Graham.macmillan@cbre.com | Peter.beatty@cbre.com | ||

| CBRE | |||

| St Martins Court | |||

| 10 Paternoster Row | |||

| London | |||

| EC4M 7HP |

| CBRE – Valuation & Advisory Services | ||

| T: | 020 7182 2000 | |

| F: | 020 7182 2273 | |

| W: | www.cbre.co.uk | |

| VALUATION REPORT | 11 | |

| PORTFOLIO: | MSTAR | ||||||

| ON BEHALF OF: | MORGAN STANLEY | ||||||

| VALUATION DATE: | 01/02/2021 | ||||||

| SCHEDULE OF CAPITAL VALUES | |||||||

| Property Name | Prop ID | Address | Currency | Tenure | Market

Value (01/02/2021) |

Vacant Possession Value (01/02/2021) |

|

| GERMANY | |||||||

| Adam Opel Strasse 12 | deadam | Adam Opel Strasse 12, Frankfurt, 60386, Germany | EUR | Freehold | 28,000,000 | 23,250,000 | |

| Aircom Parc | deairc | Aircom Parc, Ratingen, 40880, Germany | EUR | Freehold | 23,075,000 | 19,100,000 | |

| Albert-Einstein-Strasse 1 | dealbe | Albert-Einstein-Strasse 1, Erkrath, 40699, Germany | EUR | Freehold | 19,075,000 | 15,275,000 | |

| Donatusstrasse 127-129 | dedona | Donatusstrasse 127-129, Pulheim, 50259, Germany | EUR | Freehold | 13,500,000 | 10,000,000 | |

| Feldbachacker 4 | defeld | Feldbachacker 4, Dortmund, 44149, Germany | EUR | Freehold | 8,470,000 | 7,090,000 | |

| Feldheider Strasse 37-45 / 38-78 | defelh | Feldheider Strasse 37-45 / 38-78, Erkrath, 40699, Germany | EUR | Freehold | 16,700,000 | 13,125,000 | |

| Fuggerstrasse 2-6 | defugg | Fuggerstrasse 2-6, Neuss, 41468, Germany | EUR | Freehold | 15,450,000 | 12,400,000 | |

| Gewerkenstrasse 13 | degewe | Gewerkenstrasse 13, Herne, 44628, Germany | EUR | Freehold | 3,440,000 | 2,810,000 | |

| Gobietstrasse 8 | degobi | Gobietstrasse 8, Kassel, 34123, Germany | EUR | Freehold | 9,240,000 | 7,880,000 | |

| Graf-Landsberg-Str. 3,5,9 | degraf | Graf-Landsberg-Str. 3,5,9, Neuss, 41460, Germany | EUR | Freehold | 8,720,000 | 7,230,000 | |

| Hamburger Strasse 17-22 | dehamb | Hamburger Strasse 17-22, Dormagen, 41540, Germany | EUR | Freehold | 14,200,000 | 11,650,000 | |

| Harkortstrasse 12-32 | dehark | Harkortstrasse 12-32, Ratingen, 40880, Germany | EUR | Freehold | 8,780,000 | 6,920,000 | |

| Hertzstr. 2 | dehert01 | Hertzstr. 2, Herrenberg, 71083, Germany | EUR | Freehold | 3,480,000 | 2,780,000 | |

| Hertzstr. 4 | dehert02 | Hertzstr. 4, Herrenberg, 71083, Germany | EUR | Freehold | 12,050,000 | 9,870,000 | |

| Im Boden | deimbo | Im Boden, Hattersheim am Main, 65795, Germany | EUR | Freehold | 4,240,000 | 3,440,000 | |

| Josef-Beyerle-Str. 16 | dejose | Josef-Beyerle-Str. 16, Weil der Stadt, 71263, Germany | EUR | Freehold | 8,060,000 | 6,630,000 | |

| Kelterstr. 67 | dekelt | Kelterstr. 67,, Unterensingen, 72669, Germany | EUR | Freehold | 6,040,000 | 5,270,000 | |

| Kohlstrasse 8 | dekohl | Kohlstrasse 8, Koln, 50827, Germany | EUR | Freehold | 22,375,000 | 18,000,000 | |

| Kolenbeekstieg 1, 2-6 | dekole | Kolenbeekstieg 1, 2-6, Stelle, 21435, Germany | EUR | Freehold | 22,800,000 | 18,900,000 | |

| Kornwestheimer Str. 54 | dekorn | Kornwestheimer Str. 54, Korntal-Münchingen, 70825, Germany | EUR | Freehold | 12,475,000 | 10,200,000 | |

| Rontgenstrasse 3/7 | deront | Rontgenstrasse 3/7, Darmstadt, 64291, Germany | EUR | Freehold | 20,050,000 | 14,150,000 | |

| Siemensstr. 25 | desiem | Siemensstr. 25, Korntal-Münchingen, 70825, Germany | EUR | Freehold | 3,460,000 | 3,460,000 | |

| Germany: Sub-Total | - | EUR | 283,680,000 | 229,430,000 | |||

| ON BEHALF OF: | MORGAN STANLEY | ||||||

| VALUATION DATE: | 01/02/2021 | ||||||

| SCHEDULE OF CAPITAL VALUES | |||||||

| Property Name | Prop ID | Address | Currency | Tenure | Market

Value (01/02/2021) |

Vacant Possession Value (01/02/2021) |

|

| NETHERLANDS | |||||||

| Abraham van Stolkweg 62 | nlabst | Abraham van Stolkweg 62, Rotterdam, 3041 JA, Netherlands | EUR | Freehold | 20,475,000 | 17,675,000 | |

| Argonstraat 22-112 | nlargo01 | Argonstraat 22-112, Zoetermeer, 2718 SM, Netherlands | EUR | Freehold | 10,450,000 | 9,000,000 | |

| Argonstraat 116-166 | nlargo02 | Argonstraat 116-166, Zoetermeer, 2718 SM, Netherlands | EUR | Freehold | 3,220,000 | 2,680,000 | |

| Breguetlaan 67 | nlbreg | Breguetlaan 67, Oude Meer, 1438 BD, Netherlands | EUR | Freehold | 23,400,000 | 19,550,000 | |

| Bunsenstraat 13-23 | nlbuns | Bunsenstraat 13-23, Dordrecht, 3316 GC, Netherlands | EUR | Freehold | 6,730,000 | 5,470,000 | |

| Elftweg 32-54 | nlelft | Elftweg 32-54, Raamsdonksveer, 4941 VP, Netherlands | EUR | Freehold | 3,790,000 | 2,910,000 | |

| Energieweg 75-81 | nleneg | Energieweg 75-81, Zoeterwoude, 2382 NH, Netherlands | EUR | Freehold | 3,690,000 | 3,170,000 | |

| Energieweg 39-41 | nlengie | Energieweg 39-41, Zoeterwoude, 2382 NH, Netherlands | EUR | Freehold | 3,440,000 | 2,820,000 | |

| Goeseelsstraat 6-21 | nlgoes | Goeseelsstraat 6-21, Breda, 4817 MV, Netherlands | EUR | Freehold | 3,190,000 | 2,560,000 | |

| Groot Mijdrechtstraat 37-39 | nlgroo | Groot Mijdrechtstraat 37-39, Mijdrecht, 3641 RV, Netherlands | EUR | Freehold | 10,075,000 | 8,660,000 | |

| Haarlemmerstraatweg 81-137 | nlhaar | Haarlemmerstraatweg 81-137, Halfweg, 1165 MK, Netherlands | EUR | Freehold | 27,600,000 | 24,600,000 | |

| Havenweg 23-40/2-8 Martin Over | nlhave | Havenweg 23-40, 2-8 Martin Ovenweg 1-16, Utrecht, 3555 HZ, Netherlands | EUR | Freehold | 9,310,000 | 7,370,000 | |

| Jarmuiden 22-58 | nljarm | Jarmuiden 22-58, Amsterdam, 1046 AD, Netherlands | EUR | Leasehold | 16,150,000 | 12,725,000 | |

| Kamerlingh Onnesweg 2 | nlkame | Kamerlingh Onnesweg 2, Vianen, 4131 PK, Netherlands | EUR | Freehold | 6,560,000 | 6,450,000 | |

| Lakenblekerstraat 30-62 | nllake | Lakenblekerstraat 30-62, Aalsmeer, 1431 GG, Netherlands | EUR | Freehold | 13,225,000 | 11,100,000 | |

| Mon Plaisir 102-104 | nlmonp | Mon Plaisir 102-104, Etten-Leu, 4879 AT, Netherlands | EUR | Freehold | 3,130,000 | 2,770,000 | |

| Nieuwe Hemweg 20-62 | nlnieu | Nieuwe Hemweg 20-62, Amsterdam, 1013 CX, Netherlands | EUR | Leasehold | 14,425,000 | 13,675,000 | |

| Osloweg 1-107 | nloslo | Osloweg 1-107, Groningen, 9723 BE, Netherlands | EUR | Freehold | 31,000,000 | 22,425,000 | |

| Pampuslaan 96 | nlpamp | Pampuslaan 96, Weesp, 1382 JR, Netherlands | EUR | Freehold | 6,280,000 | 5,170,000 | |

| Ravenswade 54-56 | nlrave | Ravenswade 54-56, Nieuwegein, 3439 LD, Netherlands | EUR | Freehold | 3,220,000 | 2,570,000 | |

| Rijnkade 15-17 | nlrijn | Rijnkade 15-17, Weesp, 1382 GS, Netherlands | EUR | Freehold | 3,770,000 | 3,160,000 | |

| Sluispolderweg | nlslui | Sluispolderweg, Zaandam, 1505 HJ, Netherlands | EUR | Leasehold | 15,150,000 | 12,300,000 | |

| Stepvelden 1-19 | nlstep | Stepvelden 1-19, Roosendaal, 4704 RM, Netherlands | EUR | Freehold | 5,150,000 | 4,240,000 | |

| Strijkviertel | nlstri | Strijkviertel, Utrecht, 3454 PJ, Netherlands | EUR | Freehold | 9,220,000 | 7,550,000 | |

| Stuttgartstraat | nlstru | Stuttgartstraat, Rotterdam, 3047 AS, Netherlands | EUR | Leasehold | 27,200,000 | 24,575,000 | |

| Weidehek 64-70 | nlweid | Weidehek 64-70, Breda, 4824 AS, Netherlands | EUR | Freehold | 3,230,000 | 2,485,000 | |

| Wilgenkade 5-25 | nlwilg | Wilgenkade 5-25, Houten, 3992 LL, Netherlands | EUR | Freehold | 3,250,000 | 2,770,000 | |

| Netherlands: Sub-Total | EUR | 286,330,000 | 240,430,000 | ||||

| TOTAL | EUR | 570,010,000 | 469,860,000 | ||||

SOURCES OF INFORMATION AND SCOPE OF WORKS

| Sources of Information | We have carried out our work based upon information supplied to us by RBC Europe Limited and Morgan Stanley Bank, N.A., understood to have been prepared by Eastdil, Blackstone and other advisors, as set out within this report, which we have assumed to be correct and comprehensive. | |

| Tenancy and Property Related Information |

| - | Detailed tenancy schedule titled ‘Project MStar – November 2020 TS’ |

| - | Revised tenancy schedule titled ‘MStar_TS_30 11 20 EXT v1’ |

| - | Updated status of expiring leases titled ‘Confidential – Mstar_Lease Status’ |

| - | Schedule confirming physical state of asset since inspection titled ‘Confidential – Mstar_Physical State of Assets’ |

| - | Additional information to supplement the tenancy schedule was provided through a query process. |

| Technical Due Diligence |

| - | TDD capital expenditure sourced from a schedule titled ‘MStar Cash Flows 20210119_DRAFT’. |

| - | Draft TDD schedule prepared by Arcadis dated December 2019 titled ‘Project MStar NL & GE - Risk Schedule & Capex - 11.12.2019’. |

| Legal Due Diligence |

| - | Draft version of a Legal Red Flag Report for the Dutch assets prepared by Loyens Loeff, dated 12 February 2021 for The Blackstone Group International Partners LLP |

| - | Draft version of a Legal Red Flag Report for the German assets prepared by Hengeler Mueller, dated 05 February 2021 for The Blackstone Group International Partners LLP |

| Environmental |

| - | Draft Phase 1 Environmental Review reports prepared by Ambiente Ltd, dated December 2019 and January 2020. | |

| - | Summary of Priority Sites with the schedule titled ‘MLET_NL_DE_Env_Summary_FV_010221’. |

| The Property | Our report contains a brief summary of the Property details on which our Valuation has been based. | ||

| Revaluation without Inspection | As instructed, we have not re-inspected the properties for the purpose of this valuation. A schedule of the most recent inspection dates is maintained within our working papers and can be made available if required. We have also stated the most recent date of inspection (December 2019 and January 2020) within the individual property reports. With the exception of three assets summarised below, the owner has confirmed through provision of a schedule that they are not aware of any material changes to the physical attributes of the properties, or the nature of their location, since the last inspection. We have assumed this advice to be correct. | ||

| SOURCES OF INFORMATION AND SCOPE OF WORKS | 12 |

|

| Asset name | Confirmation of no material change of physical state | Comment | ||||

| Aircom Parc | Not confirmed | Changed the windows due to water leakage. | ||||

| Gobietstrasse 8 | Not confirmed | New Roof is being installed, due to leakage in the roof. | ||||

| Kolenbeekstieg 1, 2-6 | Not confirmed | New Roof, due to leakage in the roof. | ||||

| Areas | We have not measured the Properties but have relied upon the floor areas provided to us by the borrower as set out in this report, which we have assumed to be correct and comprehensive and measured in accordance with the latest edition of the RICS Property Measurement standards. | |

| Environmental Matters | We have been provided with Draft Phase 1 Environmental Review reports prepared by Ambiente Ltd, dated December 2019 and January 2020. We have not been provided with updated version of the same. We have reviewed a schedule (referenced in the sources of information) summarising the Priority sites in relation to the below assets. Based on the asset manager comments included therein and assuming that the corresponding action is taken as stated, we are satisfied that the issues are addressed and have therefore assumed these items would not have a material impact on our opinion of value. |

| Asset | Issue | |

| Groot Mijdrechtstraat 37-39, Mijdrecht | Asbestos removal / remediation or survey undertaken | |

| Osloweg 1-107, Groningen | Asbestos remediation, management plan | |

| Pampuslaan 96,118,126 & Hogeweyselaan 97,101,105,119, Weesp | Asbestos remediation | |

| Sluispolderweg 2, 4 & 8, Zaandam | Asbestos works Remediation of historical contamination | |

| Adam-Opel-Str & Ferdinand-Porsche-Str Frankfurt am Main | Asbestos Management and remediation | |

| Aircom Park, Ratingen | Asbestos Management and remediation | |

| Albert-Einstein-Strasse 1, Erkrath | Decommissioning certificates for 2 disused heating oil USTs | |

| SOURCES OF INFORMATION AND SCOPE OF WORKS | 13 |

|

| Gobietstraße 8, Kassel | Decommission oil fired heating system, underground storage tank and pipework and associated pipes | |

| Im Boden 23, Hattersheim am Main | Asbestos Integrity testing on the heating oil tank | |

| Kelterstrasse 67, Unterensingen | Integrity testing on underground storage tanks and pipework | |

| We have not carried out any investigation into the past or present uses of the Property, nor of any neighbouring land, in order to establish whether there is any potential for contamination and have therefore assumed that none exists. | ||

| Services and Amenities | We understand that all main services including water, drainage, electricity and telephone are available to the property. None of the services have been tested by us. | |

| Repair and Condition | We have seen a copy of Technical Due Diligence costs which we understand were prepared by Arcadis. | |

| Town Planning | To the extent possible, we have made planning enquiries only consulting the respective websites, We cannot, therefore, accept responsibility for incorrect information or for material omissions in the information supplied to us. Based on our understanding, the assets would appear to adhere to their designated use. | |

| Titles, Tenures and Lettings | Details of title/tenure under which the Property is held and of lettings to which it is subject are as supplied to us. We have not generally examined nor had access to all the deeds, leases or other documents relating thereto. Where information from deeds, leases or other documents is recorded in this report, it represents our understanding of the relevant documents. We should emphasise, however, that the interpretation of the documents of title including relevant deeds, leases and planning consents is the responsibility of your legal adviser. | |

| We have not conducted credit enquiries on the financial status of any tenants. We have, however, reflected our general understanding of purchasers’ likely perceptions of the financial status of tenants. |

| SOURCES OF INFORMATION AND SCOPE OF WORKS | 14 |

|

| Capital Values | The Valuation has been prepared on the basis of “Market Value”, which is defined in the Red Book as: | |

| “The estimated amount for which an asset or liability should exchange on the Valuation date between a willing buyer and a willing seller in an arm’s-length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion.” | ||

| The valuation represents the figure that would appear in a hypothetical contract of sale at the valuation date. No adjustment has been made to this figure for any expenses of acquisition or realisation - nor for taxation which might arise in the event of a disposal. | ||

| No account has been taken of any inter-company leases or arrangements, nor of any mortgages, debentures or other charge. | ||

| No account has been taken of the availability or otherwise of capital based Government or European Community grants. | ||

| Rental Values | Unless stated otherwise rental values indicated in our report are those which have been adopted by us as appropriate in assessing the capital value and do accord with the definition of Market Rent in the Red Book, which is as follows: | |

| “The estimated amount for which an interest in real property should be leased on the Valuation date between a willing lessor and a willing lessee on appropriate lease terms in an arm’s-length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion.”. | ||

| The Property | Where appropriate we have regarded the shop fronts of retail and showroom accommodation as forming an integral part of the building. | |

| Landlord’s fixtures such as lifts, escalators, central heating and other normal service installations have been treated as an integral part of the building and are included within our Valuations. | ||

| Process plant and machinery, tenants’ fixtures and specialist trade fittings have been excluded from our Valuations. | ||

| All measurements, areas and ages quoted in our report are approximate. | ||

| Environmental Matters | In the absence of any information to the contrary, we have assumed that: | |

| a) the property is not contaminated and is not adversely affected by any existing or proposed environmental law; | ||

| b) any processes which are carried out on the property which are regulated by environmental legislation are properly licensed by the appropriate authorities. | ||

| c) the property is either not subject to flooding risk or, if it is, that sufficient flood defences are in place and that appropriate building insurance could be obtained at a cost that would not materially affect the capital value. | ||

| d) invasive species such as Japanese Knotweed are not present on the Property. | ||

| VALUATION ASSUMPTIONS | 15 | |

| Repair and Condition | In the absence of any information to the contrary, we have assumed that: | |

| [a] there are no abnormal ground conditions, nor archaeological remains, present which might adversely affect the current or future occupation, development or value of the property; | ||

| [b] the property is free from rot, infestation, structural or latent defect; | ||

| [c] no currently known deleterious or hazardous materials or suspect techniques have been used in the construction of, or subsequent alterations or additions to, the property; and | ||

| [d] the services, and any associated controls or software, are in working order and free from defect. | ||

| We have otherwise had regard to the age and apparent general condition of the property. Comments made in the property details do not purport to express an opinion about, or advise upon, the condition of uninspected parts and should not be taken as making an implied representation or statement about such parts. | ||

| Title, Tenure, Lettings, Planning, Taxation and Statutory & Local Authority requirements | Unless stated otherwise within this report, and in the absence of any information to the contrary, we have assumed that: | |

| (a) the property possesses a good and marketable title free from any onerous or hampering restrictions or conditions; | ||

| (b) the building has been erected either prior to planning control, or in accordance with planning permissions, and has the benefit of permanent planning consents or existing use rights for their current use; | ||

| (c) the property is not adversely affected by town planning or road proposals; | ||

| (d) the building complies with all statutory and local authority requirements including building, fire and health and safety regulations, and that a fire risk assessment and emergency plan are in place; | ||

| (e) all rent reviews are upward only and are to be assessed by reference to full current market rents; | ||

| (f) there are no tenant’s improvements that will materially affect our opinion of the rent that would be obtained on review or renewal; | ||

| (g) tenants will meet their obligations under their leases, and are responsible for insurance, payment of business rates, and all repairs, whether directly or by means of a service charge; | ||

| (h) there are no user restrictions or other restrictive covenants in leases which would adversely affect value; | ||

| (i) where appropriate, permission to assign the interest being valued herein would not be withheld by the landlord where required; | ||

| (j) vacant possession can be given of all accommodation which is unlet or is let on a service occupancy. |

| VALUATION ASSUMPTIONS | 16 | |

VALUATION METHODOLOGY

We have summarised general comments regarding the valuation methodology and approach below, which may in part also be referenced within the individual property reports:

For all assets within the portfolio, we have arrived at our opinion of value adopting the Traditional investment capitalisation method of valuation. Within this approach, we have applied an income weighted average equivalent yield to our opinion of net income, reflecting the comparable evidence within the market for guidance on capital rates and values per sq m. This has been selected as the primary method given the fundamentals of this portfolio providing standard investment assets within the corresponding sector and the specified choice of our selected method was not a requirement within the scope of works. The DCF (Discounted Cashflow) method is an equally suitable alternative, albeit we have not assessed values under this method as part of this instruction.

We have based the current tenancy / income profile on the excel schedules provided as summarised within the Source of Information. Upon expiry, we assume that the space would be re-let on similar lease terms at our opinion of Market Rent. The assumptions in relation to voids and costs as summarised below are aligned with common market practice in each jurisdiction. Within the traditional method of valuation, aside from those stated below, we do not allow for extensive or recurring explicit costs within the cashflow given the underlying implicit approach derived from the traditional method of valuation.

As referenced above, we have considered comparable market rental and sales evidence to the extent it is available. Limitations of transparency in this regard, particularly within the German market, can restrict both the number of transactions we are able to reference and the level of available detail. We have provided evidence of which we are aware within the individual property reports, based primarily on a combination of asset type, location, date of the transaction and income profile. The primary check is on yield if we are able to analyse the income credentials, whilst using the capital rate per sq m as either an alternative benchmark or a sense check.

In terms of sale period, we would assume a range of between 6-15 months for the German assets and ranged between 3 to 6 and 9 to 12 months for The Netherlands.

Void, Rent Free and Cost Assumptions

In approaching our valuation, we have adopted current voids over vacant space ranging between 3 and 18 months, inclusive of rent-free allowance. Three assets have a void of between 3 and 6 months reflecting the re-letting prospects, including Stuttgartstraat, Argonstraat 116-166 and Breguetlaan 67, whilst the remainder of assets with vacant space have a current void of at least 12 months. We have only applied explicit voids where we are aware of tenancy risks. This includes adopting an expiry to four assets ranging between 3 and 12 months, including Energieweg 75-81, Havenweg 23-40, Ravenswade 54-56 and Strijkviertel. For the remainder of the portfolio we have not made allowances for explicit expiry voids on short term income given the largely multi-let nature of the portfolio which will likely be accustomed to tenant turnover, with a tendency for short term lease agreements and given the positive occupational sentiment within the Industrial and Logistics sector at present. Where current and expiry voids have been incorporated, an additional allowance for costs as a revenue deduction for the duration of the void has been factored within our valuation as summarised below.

Capital expenses within our valuation include outstanding current rent-free periods or step rent adjustments, based on the rent roll provided, dated 30 November 2020, which we assume to be correct. We have also included the immediate and short-term (0-5 years) capital expenditure requirements as assessed by Arcadis, less 2020 spend, as a one-off capital cost effective from the valuation date. In relation to three of the four assets which are held by way of a leasehold title, we have either allowed for the annual ground rent deduction as a revenue cost (Nieuw Hemweg and Sluispolderweg) or a capital expense to ‘buy off’ the ground rent as a discounted bulk sum in the future (Jarmuiden). Assumptions applied against the current or expiry voids include letting fees as a percentage of rental value upon renewal or re-letting (equating to 10 to 25% of rental value). For the German assets, we have applied a separate Tenant Incentive capital expense as a proportionate rate per sq m (between €10 and €50 per sq m) on renewal or re-letting as would be anticipated within the market.

We have incorporated consistent allowances for general non-recoverable revenue costs within our valuations for each country, as summarised within the individual property reports, in accordance with local market practice

| VALUATION METHODOLOGY | 17 | |

and experience of similar assets. For The Netherlands, this includes allowances for certain explicit costs, whilst German costs are more general. The majority of costs remain unchanged against each property with the exception of Maintenance applied to German assets which varies depending on a combination of perceived asset condition, age of the property and correspondence with the borrower. Maintenance has been deferred by 5 years given the allowance for immediate and short-term capital expenditure. It is therefore not factored within the day 1 cost totals.

| Country | Cost |

| Netherlands & Germany | Management (annual rate equating to 2% of rental value); |

| Netherlands and Germany | Maintenance (Annual rates of €1.75 to €6 per sq m deferred by 5 years); |

| Netherlands | Management Costs on Voids (annual rate equating to 2% of rental value until lease start); |

| Netherlands | Property Tax (annual rate equating to 2% of rental value); |

| Netherlands | Water Tax (annual rate equating to 0.25% of rental value); |

| Netherlands | Insurance (annual rate equating to 1.25% of rental value); |

| Netherlands | Sewage Charge (annual rate equating to 0.25% of rental value; |

| Germany | Other costs (annual rate of 0.5% of rental value); |

| Germany | Non-Recoverable on Voids (monthly rates of €0.50 to €1 per sq m until lease start). |

Purchasers Costs

Assuming a standard property disposal, the total purchasers costs including agents and legal fees, as a proportion of the Market Value, adopted in Netherlands equate to 9% and in Germany equates to a range of between 6.25% and 12%, with variation depending on the specific region.

| VALUATION METHODOLOGY | 18 | |

MARKET VALUE - SPECIAL ASSUMPTION OF A PORTFOLIO SALE

You have also asked us to consider the value should the Portfolio transact as a whole. Portfolio and platform trades have been increasingly common in the market place in recent years, for this asset class in particular. Whether a portfolio holds a premium to individual asset value or not, is specific to individual purchasers. It is very subjective, not something readily evidenced as all purchasers will interpret separately, therefore it is very difficult to quantify. That said, when a portfolio does trade as a whole, it is usually as a corporate structure which would benefit from reduced transaction costs, no asset level transfer tax or equivalent although other costs are incurred. In this case we are able to compare the portfolio trades which have taken place in the market.

With these in mind, we have also valued the portfolio under the special assumption of a corporate portfolio transaction, benefiting from reduced transaction costs – assuming transaction costs equating to 2.5% of Market Value. This would include fees in relation services from advisors including agents, legals and other (including taxation).

On such a basis, the Market Value on the Special Assumption of a Portfolio sale as at the Valuation Date, 01 February 2021 is:

€603,200,000 (Six Hundred and Three Million Two Hundred Thousand Euros) exclusive of VAT.

We are confident that if the portfolio were introduced to the market as a whole there would be a significant level of interest in it, the potential buyers however being different pools of equity to those interested in individual assets.

| MARKET VALUE - SPECIAL ASSUMPTION OF A PORTFOLIO SALE | 19 | |

PROPERTY REPORTS

| PROPERTY ID: | deadam - Adam Opel Strasse 12 | |

| ON BEHALF OF: | MORGAN STANLEY | |

| VALUATION DATE: | 01-Feb-2021 | FINAL |

Adam Opel Strasse 12 - Adam Opel Strasse 12, Frankfurt, 60386, Germany

| VALUATION METRICS | (currency - EUR) |

| Metric | Value |

| Market Value | 28,000,000 |

| Market Value (per sq m) | 925 |

| Net Initial Yield | 4.36% |

| Reversionary Yield | 5.38% |

| Equivalent Yield | 4.80% |

| Gross Income (p.a.) | 1,386,502 |

| Gross Income (p.a.) (per sq m) | 46 |

| *Adj. Gross Income | 1,386,502 |

| Adj. Gross Income (per sq m) | 46 |

| Net Income (p.a.) | 1,313,072 |

| Net Income (p.a.) (per sq m) | 43 |

| Gross Rental Value | 1,748,484 |

| Gross Rental Value (per sq m) | 58 |

| Capital Expenditure | -3,506,086 |

| Transaction Costs | 7.51% |

| Over / Under Rented | -3.45% |

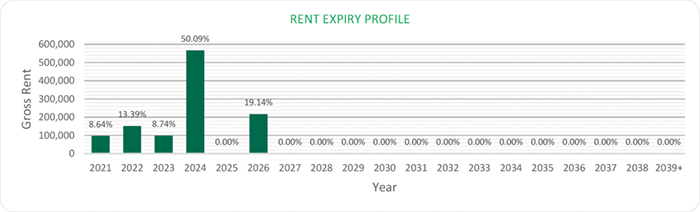

KEY FACTS

| Metric | Value | |

| Total Area (sq m) | 30,273 | |

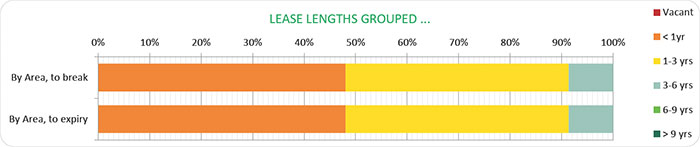

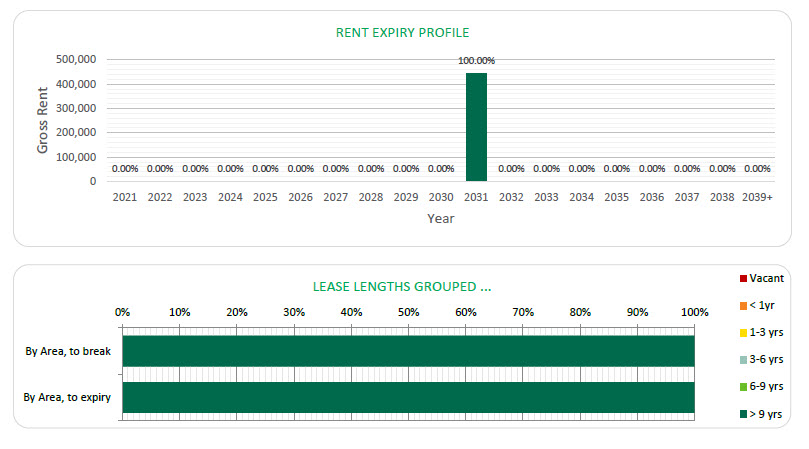

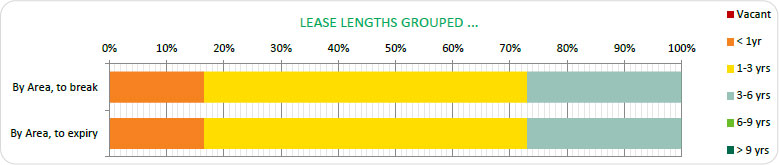

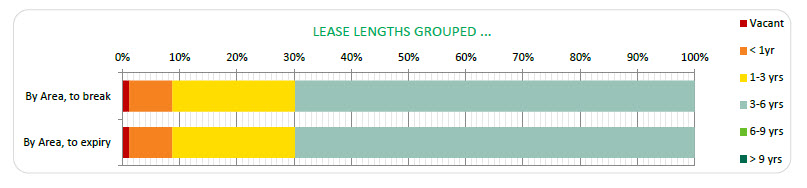

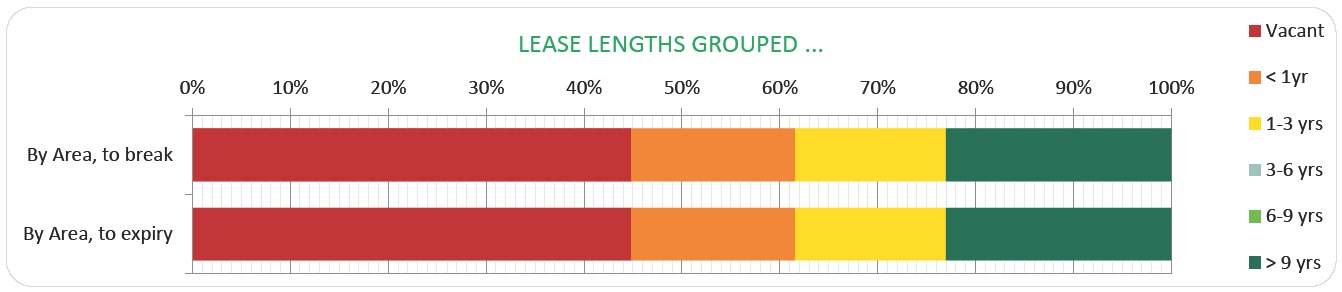

| WAULT to Break by Rent | 2.47 | |

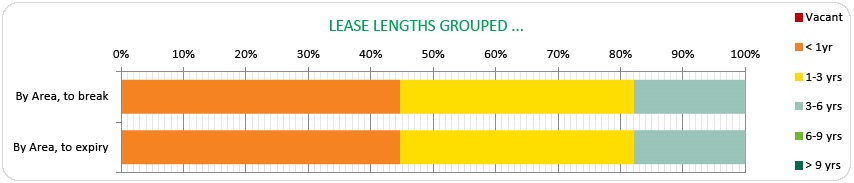

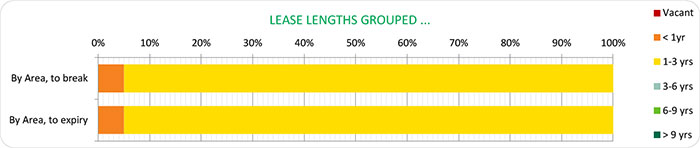

| WAULT to Break by ERV | 2.53 | |

| WAULT to Expiry by Rent | 2.47 | |

| WAULT to Expiry by ERV | 2.53 | |

| Percentage of Vacancy (Area) | 16.36% | |

| Percentage of Vacancy (ERV) | 17.87% | |

| ** | Number of Tenants | 39 |

| Current Voids (months) | 12 | |

| * Adjusted Gross Income equates to the Gross Income excluding any rent free periods | |

| LEASES RANKED BY RENT | ** Total tenant lines within our valuation. May differ to number of individual tenants |

| Printed 09/03/2021 19:42 | |

| PROPERTY ID: | deadam - Adam Opel Strasse 12 | |

| ON BEHALF OF: | MORGAN STANLEY | |

| VALUATION DATE: | 01-Feb-2021 | FINAL |

| Printed 09/03/2021 19:42 | |

| ON BEHALF OF: | MORGAN STANLEY |

| PROJECT NAME: | MSTAR |

PROPERTY REPORT

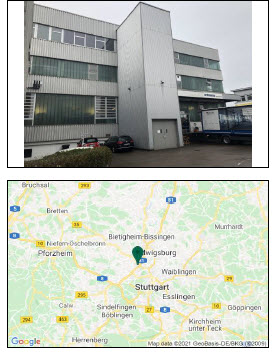

60386 FRANKFURT, ADAM-OPEL-STRASSE 12

| INSPECTED BY: | INSPECTION DATE: | VALUATION DATE: | PROPERTY TYPE |

| MARIA CHIGRYAY | 13/01/20 | 01/02/21 | WAREHOUSE |

KEY VALUATION FACTORS

| STRENGTHS | WEAKNESSES |

|

■ Strong local economy and above-average purchasing power within macro location;

■ Excellent location within the important logistics region Rhine−Main/Frankfurt;

■ Situated centrally with good connection to road, motorway network and public transportation;

■ Established commercial area within the city;

■ Diversified multi-let income profile. |

■ High vacancy rate of around 16% (by area);

■ Limited third-party usability;

■ Outdated fit-out of let areas does not meet current market requirements;

■ WAULT of less than 3 years.

■ Potential pre-emption right in favour of the City of Frankfurt.

|

| OPPORTUNITIES | THREATS |

|

■ The continuing positive development of the overall economy could lead to an increase in achievable rents;

■ High redevelopment potential due to excellent location with demand from a wide range of sectors;

■ Improvement of income profile by letting vacant spaces and re-letting occupied units on market terms. |

■ Significant capital expenditure could be incurred in the near future (due to advanced building age). |

LOCATION & SITUATION

| LOCATION | Frankfurt am Main is considered the most important banking and finance location in Germany. The concentration of firms from this sector has resulted in its leading position on the office market, which was the first in Germany to achieve international status. The city is also dominated by “ Messe Frankfurt”, with its leading international trade fairs in the automotive and book industries among others. Frankfurt Airport serves as a major international hub for freight |

| ON BEHALF OF: | MORGAN STANLEY |

| PROJECT NAME: | MSTAR |

| and passenger traffic and its main operator Fraport is the most important employer in the region. | ||

| Frankfurt am Main lies at the centre of the important logistics region Rhine−Main/Frankfurt. With its dense motorway and rail network, two inland ports and most notably the international airport with its large air cargo section, the city itself provides a comprehensive logistics infrastructure. The region benefits considerably from its central location both in Germany and in Europe as a whole. In fact, the Rhine−Main/Frankfurt logistics region compares to the logistics regions of Hamburg and “Bremen and North Sea ports” due to its gateway function – largely benefitting from the airport. The popularity of the region among logistics operators and industrial firms is reflected in limited floor space supply and the rental rates for logistics facilities either in the city area or around the airport, which are the highest in Germany after Munich. The city’s key benefit for the logistics business is its comprehensive infrastructure. Current building activities, by contrast, are concentrated in the suburbs and integrated conurbation. | ||

| More than 1.53 million sq m of modern logistics facilities were completed in the logistics region between 2015 and 2019. The commercial areas south of the city and within vicinity of the airport play a very prominent role in this context, but demand for space is also keen on the city’s northern periphery. The most important logistics locations within the city area, apart from the airport, are the districts Fechenheim, Rödelheim, Höchst and Gutleutviertel. | ||

| Within the city of Frankfurt, the subject property is situated in an established commercial area in the Ostend district, which is mainly used for industrial and retail purposes, including numerous showrooms and workshops as well as walk-in stores. The commercial area is centrally located, having the main railway station situated approx. 6.5 km away to the west. | ||

| The motorway connection can be described as good due to the close proximity to the motorway A661. The nearest airport is situated in Frankfurt around 23 km away and reachable in approx. 20 minutes. The airport offers national and international connections. Further, the surroundings offer a number of bus and tram stops. |

PROPERTY DESCRIPTION

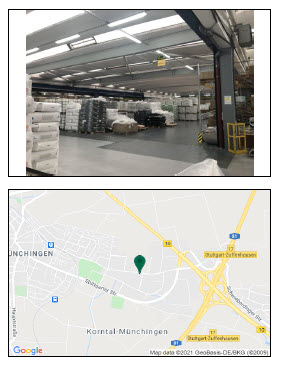

| DESCRIPTION | The current buildings were developed between 1970 and 1974 on agricultural / open land and have been used primarily for storage, wholesale and distribution since construction. The subject property has a total site area of 41,044 sq m, with a total lettable area of 30,273 sq m. | |

|

The site covers an area of approx. 4.1 hectares and comprises five warehouse buildings with associated office areas (Warehouses A – E), and one 5-storey office building (in the eastern part of the site). |

||

| Some of the warehouses are equipped with roller shutter doors and loading ramps. The buildings are surrounded by parking and loading areas covered with brick paving. The buildings do not have basements. A currently unused |

| ON BEHALF OF: | MORGAN STANLEY |

| PROJECT NAME: | MSTAR |

|

site-owned railway siding is located to the adjacent south/south west of Warehouses A and C.

The buildings cover approx. 70% of the property. Approx. 25% of the site is covered with brick paving (loading areas and parking) and a further ~5% of the property comprises landscaping (grass and bushes/trees).

Summary of known specification:

|

|||

| Characteristic | Result | ||

| Built / Renovation | 1970 - 1974 | ||

| Eaves Height | 5.4 metres | ||

| No. of loading Doors | n/a | ||

| Loading Door Ratio | n/a | ||

| Yard Depth | Approx. 10 to 20 metres | ||

| Cross-Dock | None | ||

| Warehouse (% of GLA) | 78% | ||

| Site Coverage Ratio | Approx. 70% | ||

| |

Source: Phase I Environmental Review dated December 2019; the information gathered during the site inspection. |

||

| ACCOMMODATION | We have not measured the property, but as instructed, we have relied upon floor areas made available to us. | ||||

| Unit description | Primary use | Status | Area (sq m) | ||

| Office | Office | LET | 3,818.82 | ||

| Office | Office | VACANT | 2,498.74 | ||

| Other | Storage | LET | 235.50 | ||

| Other | Storage | VACANT | 128.00 | ||

| Warehouse | Storage | LET | 21,262.84 | ||

| Warehouse | Storage | VACANT | 2,326.38 | ||

| Total | 30,270.28* | ||||

|

*some areas are subject to rounding in the valuation |

|||||

DUE DILIGENCE

| STATE OF REPAIR | CBRE have not undertaken a structural survey, nor tested the services. The property was subject to an inspection for valuation purposes in early 2020. |

| ON BEHALF OF: | MORGAN STANLEY |

| PROJECT NAME: | MSTAR |

| As you are aware, the property has not been re-inspected for the purposes of this report, nor have we been provided with updated TDD. We have therefore relied on the information provided by the Borrower, including a Capex schedule dated 12 June 2019 and schedule with revised budget of capex dated 19 January 2021. Based on the latter which indicates TDD assessment less completed spend in 2020, we have included the immediate and 2-5 years capex of €3,313,000 within our valuation. | ||

| According to our own limited inspection for valuation purposes, our opinion regarding the state of repair would substantiate the assessment by Arcadis. Based on our impression gained during the inspection, we are of the opinion that the buildings are in a fair condition, in line with the year of construction. | ||

|

ENVIRONMENTAL CONSIDERATIONS |

We have summarised the findings from a schedule provided in relation to ‘Priority sites’ within the front section of this report. | |

|

We have been made aware that although not registered in the register of contaminated sites, indications for potential contamination exist at this property likely in relation to in particular due to their current or former use. If future excavation works are carried out at these Properties, this could lead to additional costs. However, no action is required on the current use of the Properties. As such we have assumed this does not have a material impact on our opinion of value given the valuation is prepared taken the current use into consideration.

According to the Draft Environmental Due Diligence report dated 13 December 2019, prepared by Ambiente Ltd., there are currently no known ground/soil contaminations. However, the following risks for contamination have been identified:

|

||

|

On-site:

● Potential for contamination from currently unused railway sidings adjacent south/south west of warehouses A and C;

● Potential risks from the site having been part of a larger anti-aircraft defence facility (mostly located off-site to the northwest) in WWII.

Off-site:

● Potential for migration of contamination from neighbouring off-site former and current industrial uses, including fuel filling station.

In addition, there is a risk of the following building pollutants:

● Potential for contamination from suspected Made Ground at the property;

● Known asbestos containing materials within the building fabric.

We have been instructed not to make any investigations in relation to the presence or potential presence of contamination in land or buildings or the potential presence of other environmental risk factors and to assume that if investigations were made to an appropriate extent then nothing would be discovered sufficient to affect value. |

| ON BEHALF OF: | MORGAN STANLEY |

| PROJECT NAME: | MSTAR |

| We have not carried out investigation into past uses, either of the properties or of any adjacent lands, to establish whether there is any potential for contamination from such uses or sites, or other environmental risk factors and have therefore assumed that none exists. Should our assumption prove to be incorrect, we reserve the right to amend our valuation accordingly. | ||

| TENURE | We have had sight of the Draft Red Flag Legal Report prepared by Hengeler Mueller, dated 05 February 2021. Based on the information provided, we understand the property is held freehold. | |

|

We understand the property may still be subject to a pre-emption right in favour of the City of Frankfurt whereby they have the option to ‘repurchase’ the property at a price understood to be capped at €5,456,220.63. We understand the ‘priority notice was deleted on 27 April 2018. In the consent declaration (Löschungsbewilligung) dated 19 March 2018 regarding the deletion of the priority notice the city of Frankfurt am Main approved the deletion of the priority notice but did not explicitly waive the contractual repurchase right which, therefore, might still be in place.’ We would highlight that for the purposes of this valuation, the repurchase cap has not been factored within our opinion of value contained herein and highlight as a potential risk.

We also understand that the City of Frankfurt retains an option to access and utilise railway tracks within the site at a cost. Albeit we have assumed this does not impact on the operation of the occupiers nor have a material impact on our value.

In approaching our valuation, we have assumed that there are no onerous legal conditions affecting the property which have a material impact on our opinion of value. |

| ON BEHALF OF: | MORGAN STANLEY |

| PROJECT NAME: | MSTAR |

| INCOME PROFILE | The rental contracts have not been made available to us. The information is based on the rent schedule dated on 20 November 2020. | |

|

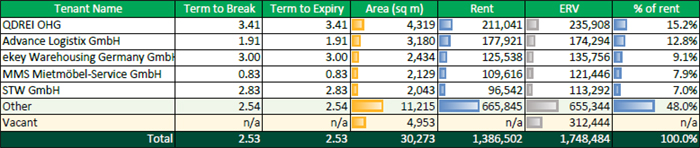

The property is leased to thirty tenants (ABZ International GmbH, Advance Logistix GmbH, ALFAPACK GmbH, Befestigungstechnik Gramm GmbH, Daniel Seddig, Deltec International Courier GmbH, Deutsche BP AG, ekey Warehousing Germany GmbH, Finance Office Frankfurt GmbH, Getränke Quelle Bornheim GmbH, Globe Shopper Activation GmbH, Horst Georg Findt Parkett-Fachgroßhandel, Korfu Foods GmbH & Co.KG, Kramm Büro-Systeme Büro Kramm GmbH, Lebensmittel Import- und Vertriebsgesellschaft Asimex GmbH, Lehmann, Jan, Michael Schmidt, Mikhail Smirnov, Mileway Germany Subco GmbH MMS Mietmöbel-Service GmbH, Ömer Ögüt, Paul Blümler + Elyas El Jazouli, QDREI OHG, reifencom GmbH, Silke Jackels, STW GmbH, VaGo GmbH, vinehouse.de, Wärmetechnik Löwe GmbH, WWD Dienstleistung GmbH). 2,499 sq m of office space, 2,326 sq m of warehouse space and 128 sq m of other space, equalling 16.4% of total space, are vacant.

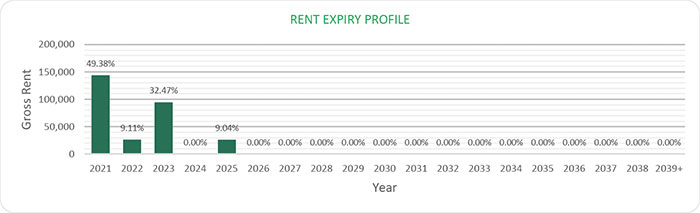

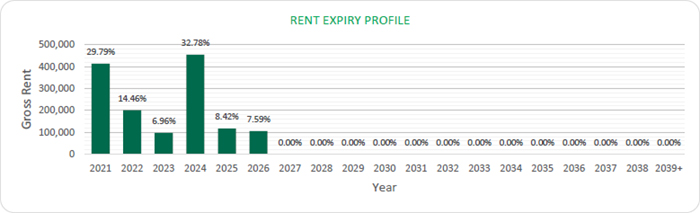

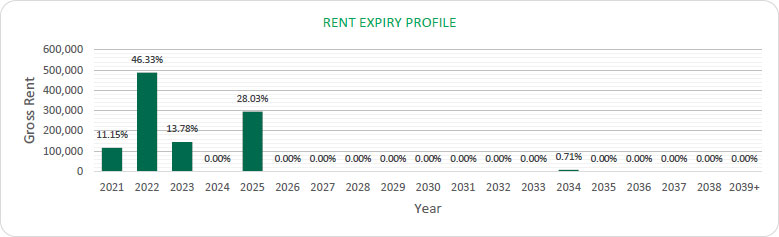

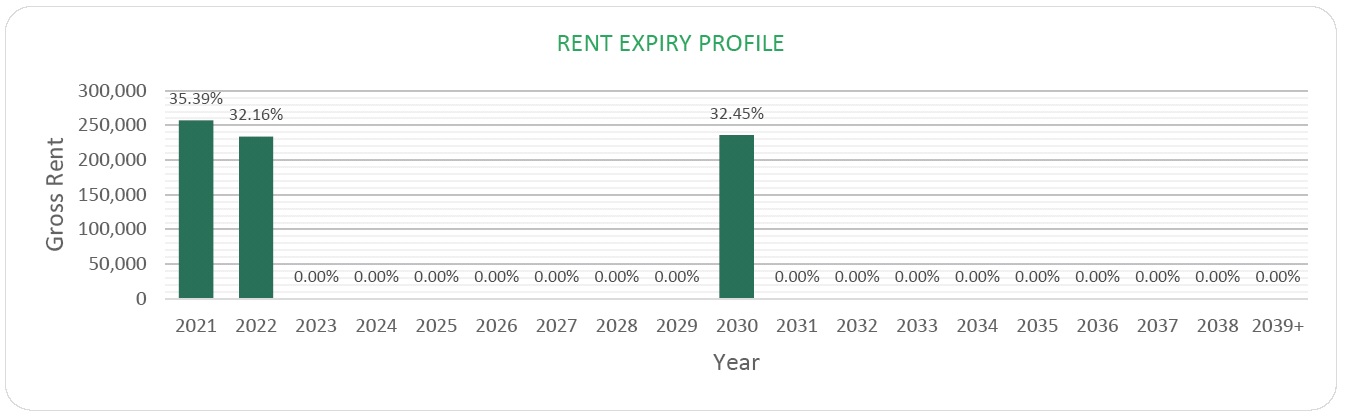

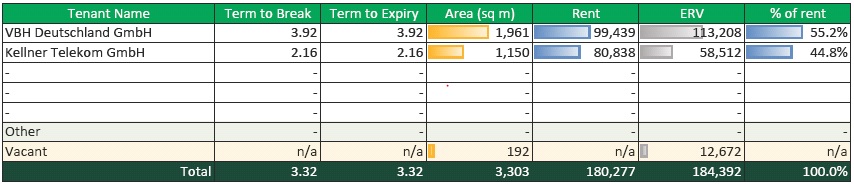

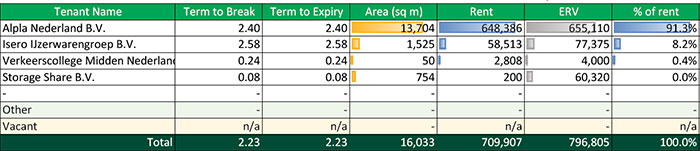

The property has a WAULT of 2.53 years (to breaks) as at the date of valuation. The total gross current rent generated by the property is €1,386,502 per annum whilst our opinion of total gross market rent is €1,748,484 per annum. The property is considered under-rented even after factoring current vacancy.

The main tenant, with about 14% of the total rental space and about 15% of the total rental income, is “QDREI OHG”. |

VALUATION CONSIDERATIONS

|

COSTS AND ADJUSTMENTS

|

Based on the information provided or our knowledge of the market, in approaching our valuation, we made allowances for the following capital and non-recoverable costs. In all cases, we have cited whether they are deducted as at the date of valuation or whether they take effect at a later date.

Capital Expenditure:

|

||||

| Type & Calculation | Source | Effective | Amount | ||

|

Capital Expenditure: Fixed Amount |

Technical Due Diligence |

On Valuation |

€3,313,000 | ||

| No Repeat | |||||

| Rent Free | CBRE Estimate | On Valuation / | €65,445 | ||

| No Repeat | |||||

| Tenant Incentives | CBRE Estimate | On lease start / renewal | €49,530 | ||

| No Repeat | |||||

| Letting Fees: 25%

of Rental Value |

CBRE Estimate | On lease start / renewal |

€78,111 | ||

| ON BEHALF OF: | MORGAN STANLEY |

| PROJECT NAME: | MSTAR |

| No Repeat | |||||

| TOTAL: ON VALUATION |

€3,506,086 | ||||

| Revenue Deductions: | |||||

| Type & Calculation | Source | Effective | Annual Amount | ||

| Maintenance: €2.75 per sq m |

CBRE Estimate | On Valuation + Delay 60 Months In perpetuity |

€83,251 | ||

| Management 2.0% of rental value |

CBRE Estimate | On Valuation In perpetuity |

€ 34,970 | ||

| Void Costs:

€0.50 per sq m |

CBRE Estimate | On Valuation On all voids |

€ 29,718 | ||

|

Other Costs: 0.5% of rental value |

CBRE Estimate | On Valuation In perpetuity |

€ 8,742 | ||

| TOTAL: ON VALUATION |

€73,430 | ||||

| VALUATION METHODOLOGY – MARKET VALUE | We have had regard to the most recent letting transactions and occupational demand for the region within which the subject property is located, including the property itself if of relevance. The rental rates for comparable premises (Warehouse) range between €48.00 and €62.28 per sq m per annum, depending on the duration of lease contract, building specifications and age. Within the evidence table appended, we would highlight the property in and around Frankfurt as being of greatest relevance in terms of property characteristics. | |

| Comparable number two is located in Dreieich and shows similar micro location characteristics. Therefore, the location can be assessed as comparable. The warehouse building has a total lettable area of 4,800 sq m. Similar to the subject property, the comparable premises is well connected to the road and public transportation network. The building is partly outdated and has a similar fit-out to the subject property. We have adopted the following rental rates within our valuation: |

| Use | Letting-Status | Rental Area (sq m) | ERV per sq m | ERV (Total) | ||

| Office | LET | 3,818.82 | €72.00 /sq m pa | €274,955.04 pa | ||

| Office | VACANT | 2,498.74 | €72.00 /sq m pa | €179,909.28 pa | ||

| Other | LET | 235.50 | €54.00 /sq m pa | €12,717.00 pa | ||

| Other | VACANT | 128.00 | €54.00 /sq m pa | €6,912.00 pa | ||

| Warehouse | LET | 21,262.84 | €54.00 /sq m pa | €1,148,193.36 pa | ||

| ON BEHALF OF: | MORGAN STANLEY |

| PROJECT NAME: | MSTAR |

| Warehouse | LET | 2,326.38 | €54.00 /sq m pa | €125,624.52 pa | ||

| Total* | 30,270.28 | €57.76 /sq m pa | €1,748,311.20 pa | |||

|

|

* The total amount of ERV and rental area may differ from the calculation printout due to rounding differences. | |||||

| We have arrived at our opinion of Market Value adopting the Traditional investment capitalisation method of valuation. Within this approach, we apply an income weighted average equivalent yield to our opinion of net income, reflecting the comparable evidence within the market for guidance on capital rates and values per sq m. | ||

| We would like to highlight investment comparable number one, two and three. We would highlight that there is a lack of detail relating to the income profile of the assets and therefore limits on assessing the yield profile. Our principal consideration is therefore on the rate per sq m. There is no further better evidence we are aware of and could highlight in relation to this property. | ||

| The first investment comparable is located in Mannheim with a similar micro location. The distance to the motorway differs only by few minutes by car, which makes the micro location of the properties comparable. The property has a lettable area of around 3,189 sq m and thus not comparable to the subject property in terms of size (with larger lettable area being more favourable). It was sold for approx. EUR 2,890,000 (equating to around EUR 906 per sq m) in Q4 2020. Given the relativity of lot size and resulting buyer pool, we would also cite the third comparable in Fritzlar which is in an inferior location, selling for a capital rate of €912 per sq m but more aligned in total lot size. Whilst it is more dated, investment comparable number two is located in Mannheim and also of relevance. The property has good connections to public transport. The distance to the motorway is 10 minutes by car, meaning the micro location is fairly comparable. The property has a lettable area of around 21,999 sq m and was sold for about EUR 18,000,000 (equating to ~EUR 818 per sq m) in Q2 2019. Due to the micro location and the lot size, we consider the property to be comparable but since the date of sale, the market has continued to improve which should be reflected within our valuation. Based on the above stated facts we have considered these assets in approaching our valuation. | ||

| For the valuation of this asset, we have applied the following Equivalent Yield: | ||

| - 4.8% | ||

| This results in a Net Initial Yield of 4.36% and a capital rate per sq m of €925. The Net Initial Yield is currently being influenced by the level of vacancy. | ||

| On the assumption that there are no unusual factors of which we are unaware and on the basis of the comments and assumptions specified in this report, CBRE is of the opinion that the Market Value (rounded) of the subject property, is: | ||

| €28,000,000 | ||

| (Twenty-eight million Euros) | ||

| The unrounded net capital value is €28,022,976. The gross unrounded capital value is €33,630,785 including €3,506,086 of capital costs and € 2,101,723 purchaser’s costs (7.50%) respectively. |

| ON BEHALF OF: | MORGAN STANLEY |

| PROJECT NAME: | MSTAR |

| Our opinion of Market Value is based upon the Scope of Work and Valuation Assumptions attached and has been primarily derived using comparable recent market transactions on arm’s length terms. | ||

| VALUATION METHODOLOGY – VACANT POSSESSION VALUE | The constituent inputs in terms of rental value and non-recoverable costs largely align with the Market Value approach. The key exception being that we have adopted a special assumption that the property is 100% vacant/non-income producing as at the valuation date. This value is predominantly derived using the traditional investment method of valuation but critically benchmarking the resultant capital rate per sq m against the prevailing evidence. | |

| In approaching our valuation under the Special Assumption that the property is entirely vacant (Vacant Possession Value), we have adopted a total void period of 12 months inclusive of rent free or tenant incentives and targeted an equivalent yield of 5.3%. | ||

| This results in a net rounded value of €23,250,000, equating to €768 per sq m. | ||

| ESTIMATED REINSTATEMENT ASSESSMENT | The property has not been inspected by a suitably qualified building surveyor from CBRE, nor have we carried out a full Reinstatement Cost Assessment. For indicative purposes only we estimate that the reinstatement cost of insurance purposes would be in the region of €50,036,557 (rounded, excl. VAT) on a day one basis, including fees but excluding VAT and inflation. | |

| This figure should be compared with the current sum insured and if a material discrepancy exists we suggest that a full Reinstatement Cost Assessment is carried out. |

| ON BEHALF OF: | MORGAN STANLEY |

| PROJECT NAME: | MSTAR |

RENTAL EVIDENCE

| PROPERTY ADDRESS |

PROPERTY USE |

DATE | TOTAL AREA (SQ M) |

TENANT | LEASE LENGTH (YEARS) |

BREAK OPTION |

RENT (P.A) (€) |

MONTHLY RENTAL RATE PER SQ M (€) |

RELATIVE QUALITY |

| 60386 Frankfurt am Main |

Distribution hall |

Q4 2020 | 3,000 | n/a | n/a | n/a | n/a | 4.00 | Better (directly in the Rhine - Main region) |

| 63303 Dreieich |

Warehouse | Q4 2020 | 4,800 | n/a | n/a | n/a | n/a | 4.85 | Comparable (micro location) |

| 68647 Biblis | Warehouse | Q4 2019 | 66,808 | n/a | n/a | n/a | 3,319,021 | 4.14 | Comparable (micro location) |

| 63293 Neu- Isenburg |

Warehouse | Q4 2019 | 1,365 | n/a | n/a | n/a | 85,032 | 5.19 | Similar (distance to the motorway) |

| 68642 Buerstadt |

Distribution hall |

Q2 2018 | 73,830 | n/a | 10 | n/a | 3,729,891 | 4.21 | Similar (distance to the motorway) |

| ON BEHALF OF: | MORGAN STANLEY |

| PROJECT NAME: | MSTAR |

SALES EVIDENCE

| PROPERTY ADDRESS | PROPERTY USE |

DATE | TOTAL AREA (SQ M) |

WAULT (YEARS) |

PASSING RENT PER ANNUM |

PURCHASE PRICE (€) |

NET INITIAL YIELD (%) |

CAPITAL RATE PER SQ M (€) |

RELATIVE QUALITY |

| 68199 Mannheim |

Warehouse | Q4 2020 | 3,189 | n/a | n/a | 2,890,000 | n/a | 906 | Similar (micro location) |

| 63743 Aschaffenburg |

Warehouse | Q4 2020 | 7,881 | n/a | n/a | 7,950,000 | n/a | 1,009 | Slightly inferior (macro location) |

| 34560 Fritzlar | Warehouse | Q1 2020 | 42,000 | n/a | n/a | 38,304,000 | n/a | 912 | Slightly inferior (macro location) |

| 68159 Mannheim |

Warehouse | Q2 2019 | 21,999 | n/a | n/a | 18,000,000 | n/a | 818 | Similar (micro location) |

| PROPERTY ID: | deairc - Aircom Parc | |

| ON BEHALF OF: | MORGAN STANLEY | |

| VALUATION DATE: | 01-Feb-2021 | FINAL |

Aircom Parc - Aircom Parc, Ratingen, 40880, Germany

| VALUATION METRICS | (currency - EUR) |

| Metric | Value |

| Market Value | 23,075,000 |

| Market Value (per sq m) | 885 |

| Net Initial Yield | 5.51% |

| Reversionary Yield | 6.36% |

| Equivalent Yield | 6.20% |

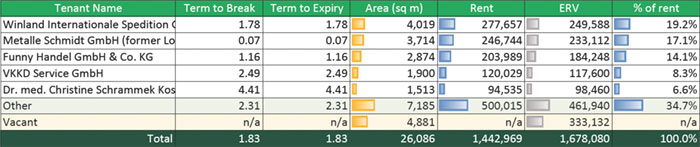

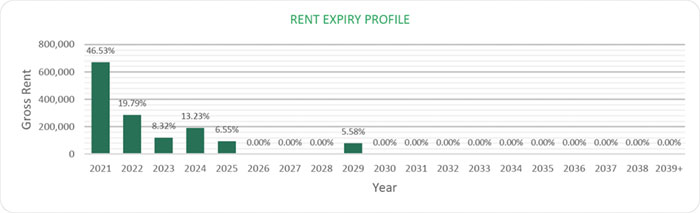

| Gross Income (p.a.) | 1,442,969 |

| Gross Income (p.a.) (per sq m) | 55 |

| *Adj. Gross Income | 1,442,969 |

| Adj. Gross Income (per sq m) | 55 |

| Net Income (p.a.) | 1,371,731 |

| Net Income (p.a.) (per sq m) | 53 |

| Gross Rental Value | 1,678,080 |

| Gross Rental Value (per sq m) | 64 |

| Capital Expenditure | -655,308 |

| Transaction Costs | 8.00% |

| Over / Under Rented | 7.29% |

| KEY FACTS | ||

| Metric | Value | |

| Total Area (sq m) | 26,086 | |

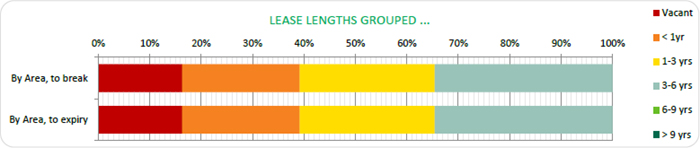

| WAULT to Break by Rent | 1.83 | |

| WAULT to Break by ERV | 1.83 | |

| WAULT to Expiry by Rent | 1.83 | |

| WAULT to Expiry by ERV | 1.83 | |

| Percentage of Vacancy (Area) | 18.71% | |

| Percentage of Vacancy (ERV) | 19.85% | |

| ** | Number of Tenants | 25 |

| Current Voids (months) | 12 | |

| * Adjusted Gross Income equates to the Gross Income excluding any rent free periods | |

| LEASES RANKED BY RENT | ** Total tenant lines within our valuation. May differ to number of individual tenants |

| Printed 09/03/2021 19:42 | |

| PROPERTY ID: | deairc - Aircom Parc | |

| ON BEHALF OF: | MORGAN STANLEY | |

| VALUATION DATE: | 01-Feb-2021 | FINAL |

| Printed 09/03/2021 19:42 | |

| ON BEHALF OF: | MORGAN STANLEY | |

| PROJECT NAME: | MSTAR | |

PROPERTY REPORT

40885 RATINGEN, SIEMENSSTRASSE 18 (AIRCOM PARK)

| INSPECTED BY: | INSPECTION DATE: | VALUATION DATE: | PROPERTY TYPE |

| MARK-PHILIPP HELCK | 08/01/2020 | 01/02/2021 | INDUSTRIAL PARK |

KEY VALUATION FACTORS

| STRENGTHS | WEAKNESSES |

| ■ | Well established commercial / logistics location; | |

| ■ | Risk limitation through multi-tenant concept; | |

| ■ | Good access to the motorways A524 (1.5 km), A52 (4.0 km) and A3 (5.0km); | |

| ■ | Property is more or less let at market rent level. |

| ■ | WAULT of 1.83 years (to breaks); | |

| ■ | Buildings contain asbestos and PCB; | |

| ■ | Vacancy rate of 18.71% (by area). |

| OPPORTUNITIES | THREATS |

| ■ | The continuing positive development of the overall economy could lead to an increase in achievable rents; | |

| ■ | Letting of the vacant office space at market conditions could improve income profile. |

| ■ | Fluctuations in the world economy and the global capital markets could have negative effects on German real estate market purchase prices; | |

| ■ | Potentially high fluctuation and re-letting costs due to short remaining lease terms. |

LOCATION & SITUATION

| LOCATION | The city of Ratingen is the largest city in the district of Mettmann and borders on the urban areas of Dusseldorf, Duisburg, Muelheim and Essen. Due to its central location within the Rhine-Ruhr region, Ratingen is very well connected in terms of infrastructure. Ratingen stands out in the Mettmann district as a location specialized in trade and services with international local companies. In addition, Ratingen is considered the region's hotspot for the IT and telecommunications sectors. The relevant logistics locations in the region are located along the A3 and A1 motorways and on the Rhine (Cologne, Duesseldorf, Neuss, Leverkusen). The Ratingen location is, however, benefiting from the increasingly scarce supply of logistics space in the neighbouring markets of Duesseldorf and Duisburg and its proximity to Duesseldorf Airport. | |

|

Ratingen belongs to the logistics region Duisburg/ Lower Rhine. The urban areas in the Duisburg/Lower Rhine region are served by a dense motorway |

| ON BEHALF OF: | MORGAN STANLEY | |

| PROJECT NAME: | MSTAR | |

|

network. This enables the region to supply the Rhineland and provides a rapid connection to Cologne/Bonn and the Ruhr district. The outer suburban areas, too, have adequate access to motorways. As a hinterland hub for containers from seaports, the region is especially well equipped with inland ports and container terminals along the Rhine. The Port of Duisburg (Duisport) is Europe’s largest inland port and Germany’s most important transshipment hub for seaport-hinterland transportation. Equally, the Ports of Emmerich and Neuss, for instance, also have container transshipment facilities. For the transportation of time-critical goods by air freight, the region has access to Duesseldorf Airport which is one of Germany’s busiest cargo airports. All told, the Duisburg/Lower Rhine region has one of the most efficient infrastructures and is one of the most flexible logistics regions in Germany. |

||

|

Within the city of Ratingen, the subject property is situated in an area, which is mainly used for logistic and industrial purposes. The direct surroundings consist of industrial companies, logistics service providers and retailers. |

||

|

The motorway connection can be described as good because of the proximity to the motorways A524, A52 and A3. The next airport is situated in Dusseldorf around 6.5 km away and reachable in approximately 10 minutes. The airport offers national and international connections. |

PROPERTY DESCRIPTION

| DESCRIPTION |

The subject site covers an area of approximately 4.4 hectares and comprises four warehouse buildings. In total, the warehouse properties comprise 19 units each building houses a two-storey frontage with office space. Parking and yard areas are located in front and adjacent to the buildings. |

|

|