Form 10-K: 0001829126-23-004119 compared to 0001213900-22-015781

0001891791

false

FY

2022

0001891791

2022-01-01

2022-12-31

0001891791

2023-06-13

0001891791

2022-12-31

0001891791

2021-12-31

0001891791

2021-01-01

2021-12-31

0001891791

us-gaap:PreferredStockMember

2020-12-31

0001891791

us-gaap:CommonStockMember

2020-12-31

0001891791

us-gaap:AdditionalPaidInCapitalMember

2020-12-31

0001891791

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2020-12-31

0001891791

us-gaap:RetainedEarningsMember

2020-12-31

0001891791

2020-12-31

0001891791

us-gaap:PreferredStockMember

2021-12-31

0001891791

us-gaap:CommonStockMember

2021-12-31

0001891791

us-gaap:AdditionalPaidInCapitalMember

2021-12-31

0001891791

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2021-12-31

0001891791

us-gaap:RetainedEarningsMember

2021-12-31

0001891791

us-gaap:PreferredStockMember

2021-01-01

2021-12-31

0001891791

us-gaap:CommonStockMember

2021-01-01

2021-12-31

0001891791

us-gaap:AdditionalPaidInCapitalMember

2021-01-01

2021-12-31

0001891791

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2021-01-01

2021-12-31

0001891791

us-gaap:RetainedEarningsMember

2021-01-01

2021-12-31

0001891791

us-gaap:PreferredStockMember

2022-01-01

2022-12-31

0001891791

us-gaap:CommonStockMember

2022-01-01

2022-12-31

0001891791

us-gaap:AdditionalPaidInCapitalMember

2022-01-01

2022-12-31

0001891791

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-01-01

2022-12-31

0001891791

us-gaap:RetainedEarningsMember

2022-01-01

2022-12-31

0001891791

us-gaap:PreferredStockMember

2022-12-31

0001891791

us-gaap:CommonStockMember

2022-12-31

0001891791

us-gaap:AdditionalPaidInCapitalMember

2022-12-31

0001891791

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-12-31

0001891791

us-gaap:RetainedEarningsMember

2022-12-31

0001891791

2020-09-01

2020-09-23

0001891791

2020-09-23

0001891791

2022-06-30

0001891791

tggi:ZXGHoldingsLimitedMember

2022-01-01

2022-12-31

0001891791

tggi:HongKongZuixianguiInternationalHoldingCoLtdMember

2022-01-01

2022-12-31

0001891791

tggi:ZuiXianGuiInternationalHoldingShenzhenLtdMember

2022-01-01

2022-12-31

0001891791

tggi:ShenzhenZuiXianGuiBreweryTechnologyLtdMember

2022-01-01

2022-12-31

0001891791

tggi:SpotUSDMember

2022-12-31

0001891791

tggi:SpotUSDMember

2021-12-31

0001891791

tggi:AverageUSDMember

2022-12-31

0001891791

tggi:AverageUSDMember

2021-12-31

0001891791

us-gaap:OfficeEquipmentMember

2022-12-31

0001891791

tggi:DistributionChannelMember

2022-12-31

0001891791

2022-06-01

2022-06-30

0001891791

country:HK

2022-01-01

2022-12-31

0001891791

country:US

2022-01-01

2022-12-31

0001891791

country:US

2021-01-01

2021-12-31

0001891791

country:VG

2022-01-01

2022-12-31

0001891791

country:VG

2021-01-01

2021-12-31

0001891791

country:HK

2021-01-01

2021-12-31

0001891791

tggi:PRCMember

2022-01-01

2022-12-31

0001891791

tggi:PRCMember

2021-01-01

2021-12-31

0001891791

country:US

2022-12-31

0001891791

country:US

2021-12-31

0001891791

country:HK

2022-12-31

0001891791

country:HK

2021-12-31

0001891791

tggi:PRCMember

2022-12-31

0001891791

tggi:PRCMember

2021-12-31

0001891791

tggi:GuizhouZuiXianGuiLiquorCoLtdMember

2022-12-31

0001891791

tggi:GuizhouZuiXianGuiLiquorCoLtdMember

2021-12-31

0001891791

tggi:ShenzhenZuiXianGuiSupplyChainCoLtdMember

2022-12-31

0001891791

tggi:ShenzhenZuiXianGuiSupplyChainCoLtdMember

2021-12-31

0001891791

tggi:ZhiyuLvMember

2022-12-31

0001891791

tggi:ZhiyuLvMember

2021-12-31

0001891791

tggi:ChenRenMember

2022-12-31

0001891791

tggi:ChenRenMember

2021-12-31

0001891791

tggi:ShareExchangeAgreementMember

2022-08-08

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTONWashington, D.C. 20549

FORM 10-KFORM 10-K

(Mark

One)

☒ ☒

ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended

December 31, 2021For the fiscal year ended December 31, 2022

☐☐ TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________________ to ____________________________________ to _______________

Commission File No. 000-56383Commission File No. 000-56383

Trans Global Group,

Inc. TRANS GLOBAL GROUP INC.

(Exact name of registrant as specified in its charter)

| DelawareDelaware |

|

88-029819088-0298190 |

(State or other jurisdiction of

incorporation or organization) |

|

(I.R.S. Employer

Identification No.) |

| |

|

|

|

Room 2701, Block A

Rm 2701, Block A, Zhantao Technology Building , Minzhi Street, Shenzhen 518000, Guangdong, China

Minzhi Street, Shenzhen

Guangdong Province - China

|

518000 |

| (Address of principal executive offices) |

|

(Zip Code) |

(Address of principal executive offices, including zip code)

+86

138 2338 3535

+86 138 2338 3535

(Registrant’(Registrant’s telephone number, including area code)

| N/A |

| (Former name, former address and former fiscal year, if changed since last report) |

Securities registered pursuant to Section 12(bg) of the Act:

| Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

| Common stock |

|

TGGI |

|

OTC Market |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Yes ☐ No ☒

Note

– Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Exchange

Act from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirement for the past 90 days. Yes ☒ No ☐

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes ☒ No ☐

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of ““large accelerated filer,” “” “accelerated filer,” “” “smaller reporting company,”” and ““emerging growth company”” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ |

Accelerated filer ☐☐ |

Accelerated filer |

☐ |

| Non-accelerated filer ☐Non-accelerated filer |

Smaller reporting company ☒☒ |

Smaller reporting company |

☒ |

| |

Emerging growth company ☐ |

Emerging growth company |

☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. Yes ☒ No ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ☐ No ☒

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12(b)-2 of the Exchange Act). Yes ☒ No ☐

Yes ☒ No ☐

The aggregate market value of the voting and non-voting common stock held by non-affiliates computed by reference to the average bid and asked price of such shares on the OTC markets as of March 18June 13, 2022, was approximately $406,078,614.2023, was approximately $14.4 million.

As of

March 18, 2022, there were 20,665,578,306 sharesIndicate the number of shares outstanding of each of the issuer’s classes of common stock, paras value $0.001 per share issued and outstanding.of latest practicable date.

DOCUMENTS INCORPORATED

BY REFERENCE

| Class |

|

Outstanding at June 13, 2023 |

| Common stock, $0.0001 par value |

|

22,131,339,996 |

List hereunder the following

documents if incorporated by reference and the Part of the Form 10-K (e.g., Part I, Part II, etc.) into which the document is incorporated:

(1) any annual report to security holders; (2) any proxy or information statement; and (3) any prospectus filed pursuant to Rule 424(b)

or (c) of the Securities Act of 1933. The listed documents should be clearly described for identification purposes (e.g., annual report

to security holders for fiscal year ended December 24, 1980). Not Applicable

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (the ““Report””), including, without limitation, statements under the heading ““Management’’s Discussion and Analysis of Financial Condition and Results of Operations,”” includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, as amended (the ““Exchange Act””). These forward-looking statements can be identified by the use of forward-looking terminology, including the words ““believes,” “” “estimates,”

“” “anticipates,” “” “expects,” “” “intends,” “” “plans,” “” “may,” “” “will,” “” “potential,”

“” “projects,” “” “predicts,” “” “continue,”” or ““should,”” or, in each case, their negative or other variations or comparable terminology. There can be no assurance that actual results will not materially differ from expectations. Such statements include, but are not limited to, any statements relating to our ability to consummate any acquisition or other business combination and any other statements that are not statements of current or historical facts. These statements are based on management’’s current expectations, but actual results may differ materially due to various factors, including, but not limited to:

| |

●● |

We have no current business operationsThe availability and adequacy of our cash flow to meet our requirements; |

| |

|

|

| |

● |

Economic, competitive, demographic, business and other conditions in our local and have no assets. Unless we obtain additional capital or acquire an operating company, the Company will not be ableregional markets; |

| |

|

|

| |

● |

Changes or developments in laws, regulations or taxes in our industry; |

| |

|

|

| |

● |

Actions taken or omitted to be taken by third parties including our suppliers and competitors, as well as legislative, regulatory, judicial and other governmental authorities; |

| |

|

|

| |

● |

Competition in our industry; |

| |

|

|

| |

● |

The loss of or failure to obtain any license or permit necessary or desirable in the operation of our business; |

| |

|

|

| |

● |

Changes in our business strategy, capital improvements or development plans; |

| |

|

|

| |

● |

The availability of additional capital to support capital improvements and development; and |

| |

|

|

| |

● |

Other risks identified in this report and in our other filings with the Securities and Exchange Commission or to undertake significant business activities.the SEC. |

| |

● |

The Company’s business plan contemplates that it will acquire an operating company in exchange for the majority of its common stock. If that occurs, management will determine the nature of the company that is acquired. Investors in the Company will have to rely on the business acumen of management in determining that the acquisition is in the best interest of the Company. If management lacks sufficient skill to operate successfully, the Company’s shares may lose value. |

The forward-looking statements

contained in this Report are based on our current expectations and beliefs concerning future developments and their potential effects

on us. Future developments affecting us may not be those that we have anticipated. These forward-looking statements involve a number of

risks, uncertainties (some of which are beyond our control) and other assumptions that may cause actual results or performance to

This Annual Report on Form 10-K should be read completely and with the understanding that actual future results may be materially different from those expressed or implied by thesewhat we expect. The forward-looking statements. Should oneincluded in or more of these risksthis Annual Report on Form 10-K are made as of the date or uncertainties materialize,

orof this Annual Report on Form 10-K and should anybe evaluated with consideration of our assumptions prove incorrect, actual results mayany changes occurring after the date of vary in material respects from those projected in thesethis Annual Report on Form 10-K. We will not update forward-looking statements. We undertakeeven though our situation may change in the future and we assume no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

Our financial statements

are stated in United States dollars ($US) and are prepared in accordance with United States Generally Accepted Accounting Principles.

In this annual report,

unless otherwise specified, all references to “common stock” refer to the common shares in our capital stock.

As used in this annual

report, the terms “.

Use of Defined Terms

Except as otherwise indicated by the context, references in this Report to:

| |

● |

The “Company”, “we,” “” “us,” “” “our,””, ““Company” and “Trans Global” mean Trans

Global Group, Inc., unless the context clearly indicates otherwise.

” or “TGGI” are references to Trans Global Group, Inc., a Delaware Corporation; |

| |

|

|

| |

● |

“Common Stock” refer to the common stock, par value of $0.0001, of the Company; |

| |

|

|

| |

● |

“U.S. dollar”, “$”, and “US$” refers to the legal currency of the United States; |

| |

|

|

| |

● |

“Securities Act” refers to the Securities Act of 1933, as amended; and |

| |

|

|

| |

● |

“Exchange Act” refers to the Securities Exchange Act of 1934, as amended. |

PART I

ITEM 1. BUSINESS

General Background of the Company

Trans Global Group, Inc. (the ““Company””) was originally incorporated in Colorado on April 2, 1979 as Teletek, Inc. On April 9, 1993, the Company effected a merger with a newly formed wholly-owned subsidiary (formed March 17, 1993) for the primary purpose of changing its domicile to Delaware. On October 2007, the Company changed its name to Trans Global Group, Inc. The Company reincorporated to Florida from March 2014, through September 2017, and changed its name to Cannabis Consortium, Inc. in September 2017. On September 18, 2017, the Company filed with the State of Delaware to move the Company’’s State of domicile from Florida to Delaware. On September 19, 2017, the Company filed conversion documents with the State of Florida moving its domicile to Delaware. In connection with the change in domicile, the Company changed its name from Cannabis Consortium, Inc. back to Trans Global Group, Inc.

From inception through 1996, the Company was engaged in various facets of the telecommunications industry, including providing long-distance telecommunications services, consisting primarily of direct dial international long-distance telephone transmissions from the United States for commercial customers. In 1996, the Company ceased telecommunications operations.

In 2007, the Company changed management and began seeking new partners or new business ventures.

The Company acquired Ecosafe Insulation of Florida, LLC in October of 2009. Ecosafe was had entered into an agreement to acquire Ecosafe Foam from American Green Group, Inc. The Company elected to not complete that acquisition and in April 2010, acquired two other entities All Weather Insulation, Inc, which was in the business of building spray and injection foam rigs and trailers for the spray and injection foam insulation industry, and Kazore Holdings, Inc., which was in the business of providing conceptual design, custom programming, SEO, campaign management, printing, iPhone application development, email marketing, SMS text marketing and many other marketing strategies both on and off line. On February

3, 2011, the Company entered into a rescission agreement with Kazore Holdings, Inc. dba Full Spectrum Media, effective as of December

31, 2010. On March 31, 2011 the Company entered into a rescission agreement with All Weather Insulation, Inc.

On April On April 1, 2011 the Company purchased the assets and liabilities of FederaLED, LLC, which was in the business of providing cost-effective Light Emitting Diode lighting technology, with a primary focus on the government markets. By September 2017, FederaLED was no longer an active part of the Company, and the domain names were sold off in 2014.

On January 9, 2012 the Company acquired VersaGreen Energy Corporation, which was engaged in the General Construction, Renewable and Solar Energy sector.

During June 2014 the Company entered into two more Share Exchange Agreements one with International Green Building Group, Inc., and the other with Red Fox Bonding, LLC. The closing that took place with International Green Building Group, Inc. was rescinded as of December 31, 2014.

In January 2016, the Company entered into consulting agreements to provide consulting services such as strategic planning and investor relations and to oversee and manage communication and filings for the three (3) companies. In February 2016, the Company rescinded its consulting agreements citing a change in the Company’’s direction.

On February 19, 2016, the Company decided that the Company would need to reverse merge a company with audited financials in order to instill market value into the Company, and on October 5, 2016 control of the Issuer was assumed by Baron Capital Enterprise. On April 21, 2017 control of the Issuer was transferred to the then CEO Matthew Dwyer.

On September 19, 2017, International Green Group, Inc. (formerly known as Rollings.Com, Inc., a subsidiary acquired in November 3, 2010), became Cannabis Consortium, Inc. On January 18, 2017 the Company completed an assignment with Bahamas Development Corporation whereby the two companies exchanged 1,214,000 shares of Cannabis Consortium for 1,214,000 of Bahamas Development Corporation. As a result of the transaction Cannabis Consortium become majority owned by Bahamas Development Corporation. Cannabis Consortium granted the Company exclusive marketing rights to a list of named products through a master distributorship agreement.

In May In May 2018, the Company elected to expand its business development activities and pursue a new line of products which are edible sauces that can be infused with THC and/or CBD. Through 2019, the Company had two different businesses 1) is a plastic manufacturer of its device(s) which can be shipped worldwide and have numerous applications, 2) is the creation of a line of edible sauces that can be infused with CBD and/or THC giving each sauce flavor three product lines.

In November 2019, the Company and Integrated Cannabis Solutions, Inc. began discussions for the sale of certain of the Company’’s IP assets. On April 12, 2019 TGGI, IGPK, and the Seller reached an understanding whereby the attempted acquisition was unsuccessful. The final transaction did not take place and no monies exchanged hands.

The Company can currently

be defined as a “shell” company, whose sole purpose at this time is to locate and consummate a merger or acquisition with

a private entity. The Company will act a holding company, and plans to establish subsidiaries inOn September 23, 2020, Matthew Dwyer, the Company, and Chen Ren entered into that certain Stock Purchase Agreement, pursuant to which Dwyer agreed Hong Kong, and/or the Cayman Islands.

Such subsidiaries will then acquire assets orto return 200,000 shares of anSeries entity actively engaged in business which generates revenuesAA Preferred stock, par value $0.0001 per share to treasury for $150,000, and the Company agreed to issue 20,000 shares of Series B Preferred Stock, of the Company representing approximately 93% of the outstanding voting power to Chen Ren. And Matthew Dwyer resigned as sole officer of the Company (including as President, Chief Executive Officer, Secretary and Treasure) and Chen Ren was appointed as sole officer of the Company (including as President, Chief Executive Officer, Secretary and Treasure) on the same date.

On June 30, 2022, we consummated a share exchange pursuant to a Share Exchange Agreement among the Company and Southsea, the shareholder of ZXGBVI, pursuant to which we acquired all the ordinary shares of ZXGBVI in exchange for its securities. The Company has no particular acquisitions in mind and has not currently entered into any negotiations regarding such

an acquisition. The Company’s officer and director has not engaged in any preliminary contact or discussions with any representative

of any other company regarding the possibilitythe issuance to the shareholder of ZXGBVI of an acquisition or merger betweenaggregate of 1,465,761,690 shares of the Company. andAs such other company as of the date hereof.a result of the transactions contemplated by the Share Exchange, ZXGBVI became a wholly-owned subsidiary of the Company. Such reorganization was completed on August 8, 2022.

The chart below depicts the corporation structure of the Company as of the date of this Annual Report on Form 10-K:

Our major shareholders

and headquarters are located in China and we plan to acquire operating assets and businesses in China. We will face various legal and

operational risks and uncertainties related to having substantially all of our operations in China. In addition, if any of the assets

or businesses that we acquire are on the 2021 Negative List promulgated by the Ministry of Commerce of the PRC (the “MOFCOM”)

and the National Development and Reform Commission of China (“NDRC”), we may not be able to conduct our business through such

subsidiaries without being subject to restrictions imposed by the foreign investment laws and regulations of the PRC

Business Overview

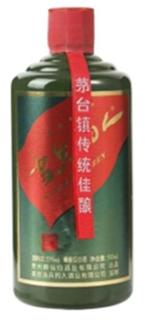

Trans Global Group Inc. is a US holding company incorporated in Delaware. We conduct our business through our PRC subsidiary, “Shenzhen Zui Xian Gui Brewery Technology Limited” (“ZXGSZ”), which is a wine distribution and retail sales company based in Guangdong province, China. “Zui Xian Gui 醉仙归”, the brand name was founded by Mr. Ren Chen, a famous singer and post-80s entrepreneur. He insisted on building Chinese flavored liquor and a Chinese liquor culture, building the brand with special quality and multi liquor culture, and striving to create a healthy and good wine belonging to China and the world.

We are principally engaged in the distribution of high-end liquor for the PRC markets, and international markets in the future, through online and offline channels. The products we distribute include the Zui Xian Gui International Classic, Zui Xian Gui International Premium, Zui Xian Gui International Collection, MOGU DAXIA and DangBing DeRen. Set out below is a brief introduction to the principal products we distribute:

|

|

|

|

|

|

Zui Xian Gui International Classic

53%vol and 500ml |

|

Zui Xian Gui International Premium

53%vol and 500ml |

|

Zui Xian Gui International Collection

53%vol and 500ml |

| |

|

|

|

|

|

|

|

|

|

|

Dangbing Deren

53%vol and 500ml |

|

Mogu Daxia

53%vol and 500ml |

|

|

We sell our products through our distributors. We authorize distribution and classify the dealers according to the purchase amount. Different types of dealers enjoy different discounts. At present, the Company’s dealers are mainly individuals, and a few are legal entities. In terms of retail, we mainly focus on online sales, including online self-operated retail and e-commerce platform which formulates purchase details according to the trade mode of “purchase by sale and zero inventory”. The main purchased materials include customized finished wine, packaging accessories, etc. Our distribution policy table:

| Kind of distributor |

|

Cross the

threshold

(RMB) |

|

|

Discount

rate |

|

| First-class |

|

|

2,000,000 |

|

|

|

50 |

% |

| Second-class |

|

|

1,000,000 |

|

|

|

55 |

% |

| Third-class |

|

|

500,000 |

|

|

|

60 |

% |

| Fourth-class |

|

|

200,000 |

|

|

|

65 |

% |

| Fifth-class |

|

|

50,000 |

|

|

|

70 |

% |

Marketing Plan

We intend to encourage sales of the products we distribute through advertising, marketing and promotion, and we cooperate with certain distribution network in conducting marketing and promotional activities through selected distributors who owned the retail outlets in their local estate with a view to expanding our share and our brand of the PRC market.

The PRC government has

significant authority to exert influence on the ability of a China-based company, Currently, we have already implemented various publicity campaigns such as us, to media advertisements and other promotional activities. We will continue to strategically conduct its business, accept foreign

investments oradvertising, marketing and promotions to list on a U.S. or other foreign exchange. For example, we face risks associated with regulatory approvals of offshore offerings,

anti-monopoly regulatory actions, oversight on cybersecurity and data privacyboost sales of the products, as well as the lack of PCAOB inspection on our auditors.

Such risks could result in a material change in our operations and/or the value of our Stocks or could significantly limitour own corporate image. We will also continue to place advertisements in different media outlets to further strengthen brand awareness. We endeavour to organize various types of marketing and promotional activities by collaborating with retail distributors within our distribution network or otherwise.

We also plan on other public relation activities such as liquor tasting gatherings on a regular basis with a view to strengthening our relationship with distributors and consumers and to promote appreciation of liquor as part of the Chinese culture.

Competitive Strengths

Our Director believes that our success is attributed to, among other things, the following competitive strengths:

Well-established distribution network in the PRC

Our Director believes that one of our key competitive strengths is our well-established distribution network and channel management. In particular, our Director believes that our expertise lies in our knowledge and experience of channel management specific to the PRC domestic market.

For the year ended December 31, 2022, we transacted with 238 customers, including wholesale distributors (also known as “four-class distributors” and “five-class distributors”) who purchase our liquor products for further distribution to the end users. All of these customers had distribution agreements with or completely

hinder our ability to offer or continue to offer Stocks and/or other securities to investors and cause the value of such securities to

significantly decline or be worthless. See “Risk Factors — Risks Associated with doing business in China.”

The PRC government has

significant oversight and discretion over the conduct of our business and may intervene with or influence our operations as the government

deems appropriate to further regulatory, political and societal goals. See “Risk Factors — Risks Associated

with doing business in China — Uncertainties with respect tous during the same period. These distributors will then sell the products in their retail outlets in the PRC. All of these customers had distribution agreements with us during the same period.

Our effective marketing strategy in the PRC

Another critical competitive strength lies in our effective marketing and sales strategies. Our Director believes that our market experience enables us to provide our suppliers with timely market information such as feedback on consumer preferences so that they may develop new products to cater for the changing market needs. We have collaborated with selected retail outlets such as supermarkets and restaurants in the PRC in launching marketing and promotional activities.

Our Director believes that our effective marketing strategy and our market know-how have enhanced our relationships with both our suppliers and distributors and have enabled us to create value for our distribution network.

Governmental Regulations in Relation to the Company’s Businesses

This section summarizes the principal PRC laws, rules and regulations related to our business and operations.

Regulations relating to Anti-Monopoly and Competition

On September 11, 2020, the Anti-Monopoly Commission of the State Council issued Anti-Monopoly Compliance Guideline for Business Operators, which requires business operators to establish anti-monopoly compliance management systems under the PRC Anti-Monopoly Law to manage anti-monopoly compliance risks.

On August 17, 2021, the State Administration for Market Regulation, or the SAMR, issued a discussion draft of Provisions on the Prohibition of Unfair Competition on the Internet, under which business operators should not use data or algorithms to hijack traffic or influence users’ choices, or use technical means to illegally capture or use other business operators’ data. Furthermore, business operators are not allowed to (i) fabricate or spread misleading information to damage the reputation of competitors, or (ii) employ marketing practices such as fake reviews or use coupons or “red envelopes” to entice positive ratings.

On February 7, 2021, the Anti-Monopoly Commission of the State Council published Anti-Monopoly Guidelines for the Internet Platform Economy Sector that specified circumstances where an activity of an internet platform will be identified as monopolistic act as well as concentration filing procedures for business operators. According to the PRC Anti-Monopoly Law, if a business operator carries out a concentration in violation of the law, the relevant authority shall order the business operator to terminate the concentration, dispose of the shares or assets or transfer the business within a specified time limit, or take other measures to restore the pre-concentration status, and impose a fine of up to RMB500,000.

On October 23, 2021, the Standing Committee of the National People’s Congress issued a discussion draft of the amended Anti-Monopoly Law, which proposes to increase the fines for illegal concentration of business operators to no more than ten percent of its last year’s sales revenue if the concentration of business operator has or may have an effect of excluding or limiting competitions, or a fine of up to RMB5 million if the concentration of business operator does not have an effect of excluding or limiting competition. The draft also proposes that the relevant authority shall investigate a transaction where there is any evidence that the concentration has or may have the effect of eliminating or restricting competitions, even if such concentration does not reach the filing threshold.

Regulations Relating to Food Business Operations

We operate our business in China under a legal regime consisting of the PRC legal systemNational People’s Congress, including uncertainties regarding the enforcement

of laws, and sudden or unexpected changes in laws and regulations in China could adversely affect us and limit the legal protections available

to you and us.” The PRC government has recently published new policies that significantly affected certain industries such as the

education and internet industries, and we cannot rule out the possibility that it will in the future release regulations or policies regarding

the industry of our future PRC subsidiaries that could adversely affect our business, financial condition and results of operations. Furthermore,

the PRC government has recently indicated an intent to exert more oversight and control over overseas securities offerings and other capital

markets activities and foreign investment in China-based companies like us. Any such action, once taken by the PRC government, could significantly

limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to

significantly decline or in extreme cases, become worthless. See “Risk Factors — Risks Associated with doing

business in China — The recent state government interference into business activities on U.S. listed Chinese companies may negatively

impact our existing and future operations in China; — Uncertainties with respect to the PRC legal system, including uncertainties

regarding the enforcement of laws, and sudden or unexpected changes in laws and regulations in China could adversely affect us and limit

the legal protections available to you and us.”

We are currently not

required to obtain permission from any of the PRC authorities to and issue our common stock shares to foreign investors. We will determine

following acquisitionwhich is the country’s highest legislative body; the State Council, which is the highest authority of the executive branch of the PRC central government; and several ministries and agencies under its authority, including the Ministry of Industry and Information Technology, State Administration For Industry & Commerce, State Administration of Taxation and their respective local offices. This section summarizes the principal PRC regulations related to our business.

| Type |

|

Name |

|

Effective Date |

|

Content |

|

Updates |

| President Order 21 of 2015 |

|

Food Safety Law |

|

October 1, 2015 |

|

The Food Safety Law is the foundational law and the most important food safety law for alcoholic products in China. A great majority of wine regulations are drafted in conformity to the requirements of this law. |

|

Revised on December 29, 2018 |

| AQSIQ Order 144 of 2011 |

|

Measures for Administration of Imported/Exported Food Safety |

|

March 1, 2012 |

|

This rule oversees the safety of imported and exported food. |

|

Revised on 11/23/2018 |

| CFDA Order 16 of 2015 |

|

Measures for Administration of Food Production Licensing |

|

October 1, 2015

|

|

This rule requires all food producers in China to procure a production license. |

|

Replaced by the State Administration for Market Regulation Order 24 in 2020 |

| AQSIQ Order 27 of 2012 |

|

Administrative Provisions on Inspections and Supervisions of Labelling of Imported/Exported Pre-packaged Foods |

|

June 1, 2012

|

|

This rule provides guidelines that governs all pre-packaged foods. |

|

|

| AQSIQ Notice on December 23, 2004 |

|

Rules for Inspection on Production Licensing of Wines and Fruit Wines |

|

January 1, 2005

|

|

This rule sets forth inspection procedures on production licensing of wines and fruit wines. |

|

|

Regulations Relating to M&A Rules and Overseas Listings

On August 8, 2006, six PRC regulatory agencies, including the China Securities Regulatory Commission, or the CSRC, adopted the Regulations on Mergers of Domestic Enterprises by Foreign Investors, or the M&A Rules, which became effective on September 8, 2006 and was amended on June 22, 2009. Foreign investors shall comply with the M&A Rules when they purchase equity interests of a domestic company or subscribe the increased capital of a domestic company, thus changing the nature of the domestic company into a foreign-invested enterprise; or when the foreign investors establish a foreign-invested enterprise in the PRC, purchase the assets of any subsidiaries whether we or such subsidiaries are required to obtain permission or approval from the PRC authorities

including CSRC or Cyberspace Administration of China (the “CAC”) for any acquired operations. As we currently have no such

subsidiaries, we have not yet applied for or received any denial for any operations. However, recently, the General Office of the Central

Committee of a domestic company and operate the assets; or when the foreign investors purchase the asset of a domestic company, establish a foreign-invested enterprise by injecting such assets and operate the assets. The M&A Rules purport, among other things, to require offshore special purpose vehicles formed for overseas listing purposes through acquisitions of PRC domestic companies and controlled by PRC companies or individuals, to obtain the approval of the CSRC prior to publicly listing their securities on an overseas stock exchange.

According to the Anti-Monopoly Law which took effect as at August 1, 2008, where the concentration of business operators reaches the Communist Party of China and the General Office of the State Council jointly issued the “Opinions on Severely Cracking

Down on Illegal Securities Activities According to Law,” or the Opinions, which was made available to the public on July 6, 2021.

The Opinions emphasized the need to strengthen the administration over illegal securities activities, and the need to strengthen the supervision

over overseas listings by Chinese companies. Effective measures, such as promoting the construction of relevant regulatory systems will

be taken to deal with the risks and incidents of China-concept overseas listed companies, and cybersecurity and data privacy protection

requirements and similar matters. The Opinions and any related implementing rules to be enacted may subject us to compliance requirement

in the future. Given the current regulatory environment in the PRC, we are still subject to the uncertainty of interpretation and enforcement

of the rules and regulations in the PRC, which can change quickly with little advance notice, and any future actions of the PRC authorities.

In addition, we cannot assure you that relevant PRC government agencies would reach the same conclusion as we do or as advised by our

PRC legal counsel. If we are wrong with regards to our interpretation of the PRC laws and regulations, or if the CSRC, the CAC or other

regulatory PRC agencies later promulgate new rules requiring that we obtain their approvals to issue our common stock to foreign investors,

we may be unable to obtain a waiver of such approval requirements, if and when procedures are established to obtain such a waiver. Any

uncertainties and/or negative publicity regarding such an approval requirement could have a material adverse effect on the trading price

of our securities. See “Risk Factors—Risks associated with doing business in China – Uncertainties with respect to the

PRC legal system, including uncertainties regarding the enforcement of laws, and sudden or unexpected changes in laws and regulations

in China could adversely affect us and limit the legal protections available to you and us; – The PRC legal system is evolving,

and the resulting uncertainties could adversely affect us; – The approval of the CSRC or other PRC regulatory agencies may be required

in connection with this registration under PRC law.”

Business Objectives

of the Company

Since April 30, 2021,

current management (which includes possible participation by our majority shareholder) has determined to direct its efforts and limited

resources to pursue potential new business opportunities. The Company does not intend to limit itself to a particular industry and has

not established any particular criteria upon which it shall consider a business opportunity.

The Company’s purpose

is to seek, investigate and, if such investigation warrants, acquire an interest in business opportunities presented to it by persons

or firms who or which desire to seek the perceived advantages of an issuer who has complied with the Exchange Act. The Company will not

restrict its search to any specific business, industry, or geographical location and the Company may participate in a business venture

of virtually any kind or nature and we have not established any particular criteria upon which we consider a business opportunity. This

discussion of the proposed business herein is purposefully general and is not meant to be restrictive of the Company’s virtually

unlimited discretion to search for and enter into potential business opportunities. Management anticipates that it may be able to participate

in only one potential business venture because the Company has nominal assets and limited financial resources.

Management of the Company,

which may also include the majority shareholder of the Company (“Management”) would have substantial flexibility in identifying

and selecting a prospective new business opportunity. The Company is dependent on the judgment of its management in connection with this

process. There are many criteria that management may deem relevant. In connection with an evaluation of a prospective or potential business

opportunity, management may be expected to conduct a due diligence review. A business combination may involve a company which may be financially

unstable or in its early stages of development or growth. In evaluating a prospective business opportunity, we would consider, among other

factors, the following:

| |

● |

costs associated with pursuing a new business opportunity; |

| |

● |

the growth potential of the new business opportunity; |

| |

● |

experiences, skills and availability of additional personnel necessary to pursue a potential new business opportunity; |

| |

● |

necessary capital requirements; |

| |

● |

the competitive position of the new business opportunity; |

| |

● |

stage of business development; |

| |

● |

the market acceptance of the potential products and services; |

| |

● |

proprietary features and degree of intellectual property; and |

| |

● |

the regulatory environment that may be applicable to any prospective business opportunity. |

The foregoing criteria

are not intended to be exhaustive and there may be other criteria that Management may deem relevant. In connection with an evaluation

of a prospective or potential business opportunity, Management may be expected to conduct a due diligence review.

The time and costs required

to pursue new business opportunities, which includes negotiating and documenting relevant agreements and preparing requisite documents

for filing pursuant to applicable securities laws, can not be ascertained with any degree of certainty.

Management intends to

devote such time as it deems necessary to carry out the Company’s affairs. The exact length of time required for the pursuit of

any new potential business opportunities is uncertain. No assurance can be made that we will be successful in our efforts. We cannot project

the amount of time that our Management will devote to the Company’s plan of operation.

Prospective investors

in the Company’s common stock will not have an opportunity to evaluate the specific merits or risks of any of the one or more business

combinations that we may undertake. A business combination may involve the acquisition of or merger with a company which needs to raise

substantial additional capital by means of being a publicly trading company, while avoiding what it may deem to be adverse consequences

of undertaking a public offering itself. These include time delays, significant expense, voting control issues and compliance with various

federal and state securities laws.

The Company intends to

conduct its activities to avoid being classified as an “Investment Company” under the Investment Company Act of 1940, and

therefore avoid application of the costly and restrictive registration and other provisions of the Investment Company Act of 1940 and

the regulations promulgated thereunder.

We voluntarily filed

the Registration Statement on Form 10 to make information concerning ourselves more readily available to the public and to become eligible

for listing on the OTCQB market sponsored by OTC Markets. Management believes that being a reporting company under the Securities Exchange

Act will enhance our efforts to acquire or merge with an operating business.

As a result of our registration

with the SEC, we will be obligated to file interim and periodic reports including an annual report with audited financial statements.

This obligation will substantially increase the expenses incurred by the Company.

Any company that is merged

into or acquired by us will become subject to the same reporting requirements as we. Thus, if we successfully complete an acquisition

or merger, the acquired entity must have audited financial statements for at least the two most recent fiscal years, or if the acquired

company has been in business for less than two years, audited financial statements must be available from its inception. This requirement

limits our possible acquisitions or merger opportunities because many private companies either do not have audited financial statements

or are unable to produce audited statements without long delay and substantial expense.

The Company’s common

stock is subject to quotation on the OTC Markets Group, Inc. Pink Open Market Platform (“Pink Sheets”) under the symbol TGGI.

There is currently only a limited trading market in the Company’s shares, nor do we believe that any active trading market has existed

for approximately the last five years. There can be no assurance that there will be an active trading market for our securities following

the effective date of this Registration Statement under the Securities Exchange Act of 1934, as amended (“Exchange Act”).

In the event that an active trading market commences, there can be no assurance as to the market price of our shares of common stock,

whether the trading market will provide liquidity to investors, or whether any trading market will be sustained.

General Overview

Competition.

In identifying, evaluating,

and selecting a target business, we expect to encounter intense competition from other entities having a business objective similar to

ours. The Company will remain an insignificant participant among the firms which engage in the acquisition of business opportunities.

There are many established venture capital and equity financial concerns which have significantly greater financial and personnel resources

and technical expertise than the Company. In view of the Company’s combined extremely limited financial resources and limited management

availability, the Company will continue to be at a significant competitive disadvantage compared to the Company’s competitors. Many

of these entities are well established and have extensive experience identifying and effecting business combinations, either directly

or through affiliates. Many if not virtually most of these competitors possess far greater financial, human, and other resources compared

to our resources. While we believe that there are numerous potential target businesses that we may identify, our ability to compete in

acquiring certain of the more desirable target businesses will be limited by our limited financial and human resources. Our inherent competitive

limitations are expected by management to give others an advantage in pursuing the acquisition of a target business that we may identify

and seek to pursue. Further, any of these limitations may place us at a competitive disadvantage in successfully negotiating a business

combination. Management believes that our status as a reporting public entity with potential access to the United States public equity

markets may give us a competitive advantage over certain privately held entities having a similar business objective in acquiring a desirable

target business with growth potential on favorable terms.

If we succeed in effecting

a business combination, there will be, in all likelihood, intense competition from existing competitors of the business we acquire. In

particular, certain industries which experience rapid growth frequently attract an increasingly larger number of competitors, including

those with far greater financial, marketing, technical and other resources than the initial competitors in the industry in which we seek

to operate. The degree of competition characterizing the industry of any prospective target business cannot presently be ascertained.

We cannot assure you that, subsequent to a business combination, we will have the resources to compete effectively, especially to the

extent that the target business is in a high-growth industry.

Employees

As of March 1, 2022,

we employed a total of 0 full-time employees and 1 consultant. None of our employees are covered by a collective bargaining agreement.

The need for employees and their availability will be addressed in connection with the decision whether or not to acquire or participate

in specific business opportunities.

Conflicts of Interest.

The Company’s management

is not required to commit its full time to the Company’s affairs. As a result, pursuing new business opportunities may require a

longer period of time than if management would devote full time to the Company’s affairs. Management is not precluded from serving

as an officer or director of any other entity that is engaged in business activities similar to those of the Company. Management has not

identified and is not currently negotiating a new business opportunity for us. In the future, management may become associated or affiliated

with entities engaged in business activities similar to those we intend to conduct. In such event, management may have conflicts of interest

in determining to which entity a particular business opportunity should be presented. In the event that the Company’s management

has multiple business affiliations, our management may have legal obligations to present certain business opportunities to multiple entities.

In the event that a conflict of interest shall arise, management will consider factors such as reporting status, availability of audited

financial statements, current capitalization, and the laws of jurisdictions. If several business opportunities or operating entities approach

management with respect to a business combination, management will consider the foregoing factors as well as the preferences of the management

of the operating company. However, management will act in what we believe will be in the best interests of the shareholders of the Company.

The Company shall not enter into a transaction with a target business that is affiliated with management.

Challenges with Having

Operations in China

Trans Global Group, Inc.

is a Delaware holding company that plans to conduct substantially all of its operations and business in China through PRC based subsidiaries.

As a result, our ability to pay dividends and to service any debt we may incur overseas largely depends upon dividends paid PRC subsidiaries

to us. If any PRC subsidiary incurs debt on its own behalf, the instruments governing its debt may restrict its ability to pay dividends

to us. In addition, a PRC subsidiary is permitted to pay dividends to us only out of its retained earnings, if any, as determined in accordance

with the Accounting Standards for Business Enterprise as promulgated by the Ministry of Finance of the PRC, or the PRC GAAP.filing thresholds stipulated by the State Council, business operators shall file a declaration with the SAMR, and no concentration shall be implemented until the SAMR clears the anti-monopoly filing. Pursuant to the Notice of the General Office of the State Council on the Establishment of the Security Review System for Mergers and Acquisitions of Domestic Enterprises by Foreign Investors and the Security Review Rules issued by the General Office of the State Council on February 3, 2011 and became effective on March 3, 2011, mergers and acquisitions by foreign investors that raise “national defense and security” concerns, and mergers and acquisitions through which foreign investors may acquire de facto control over domestic enterprises that raise “national security” concerns, are subject to strict review by the PRC government authorities. On August 25, 2011, the MOFCOM issued the Provisions of the Ministry of Commerce for the Implementation of the Security Review System for Mergers and Acquisitions of Domestic Enterprises by Foreign Investors, which provides that if a foreign investor’s merger or acquisition of a domestic enterprise falls within the scope of security review specified in the Notice of the General Office of the State Council on the Establishment of the Security Review System for Mergers and Acquisitions of Domestic Enterprises by Foreign Investors, the foreign investor shall file an application with MOFCOM for security review. Whether a foreign investor’s merger or acquisition of a domestic enterprise falls within the scope of security review or not shall be determined based on the substance and actual influence of the merger or acquisition transaction. No foreign investor is allowed to substantially avoid the security review in any way, including but not limited to, holding shares on behalf of others, trust arrangements, multi-level reinvestment, leasing, loans, contractual control, or overseas transactions.

Such structure involves

unique risks to investors in our common stock. For a detailed description of the risk, see “Risk Factors”, including the risks

described under the subsections headed “Risks Related to Our Business and Industry”, “Risks associated with doing business

in China” and “Risks Related to the Market for our stock”. In particular, as we are to be a China-based company incorporated

in Delaware, we face various legal and operational risks and uncertainties related to being based in and having substantially all of our

operations in China. The PRC government has significant authority to exert influence on the ability of a China-based company, such as

us, to conduct its business, accept foreign investments or list on a U.S. or other foreign exchange. For example, we face risks associated

with regulatory approvals of offshore offerings, anti-monopoly regulatory actions, oversight on cybersecurity and data privacy, as well

as the lack of PCAOB inspection on our auditors. Such risks could result in a material change in our operations and/or the value of our

Stocks or could significantly limit or completely hinder our ability to offer or continue to offer Stocks and/or other securities to investors

and cause the value of such securities to significantly decline or be worthless. The PRC government also has significant oversight and

discretion over the conduct of our business and our operations may be affected by evolving regulatory policies as a result. The PRC government

has recently published new policies that significantly affected certain industries, and we cannot rule out the possibility that it will

in the future release regulations or policies regarding our industry that could adversely affect our business, financial condition and

results of operations. Furthermore, the PRC government has recently indicated an intent to exert more oversight and control over overseas

securities offerings and other capital markets activities and foreign investment in China-based companies like us. These risks could result

in a material change in our operations and the value of our common stocks, or could significantly limit or completely hinder our ability

to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or become worthless.

You should pay special attention to the subsection headed “Risks associated with doing business in China” below.

Recent Regulatory

Developments

Draft Rules Regarding

Overseas Listing

On December

On December 24, 2021, the CSRC issued the Administrative Provisions of the State Council Regarding the Overseas Issuance and Listing of Securities by Domestic Enterprises (Draft for Comments) (the ““Draft Administrative Provisions””) and the Measures for the Overseas Issuance of Securities and Listing Record-Filings by Domestic Enterprises (Draft for Comments) (the ““Draft Filing Measures””), collectively with the

Draft Administrative Provisions, the ““Draft Rules Regarding Overseas Listing”), both of Regulations,” which are subject tocurrently published for public comments and have not taken effect yetonly. The Draft Rules Regarding Overseas Listing lay out the filing regulation arrangement for bothRegulations require that companies applying for overseas issuance, listing and post-listing capital operations, including IPO, multi-listing, spin-off listing, SPAC, refinancing, issuance for asset acquisitions, equity incentives, and changes of control and other stipulated transactions, shall be subject to statutory procedures, such as filing and information reporting requirement. Overseas issuance and listings include direct and indirect overseas listing, and clarify the determination criteria for indirect overseas issuance and listings. Where an enterprise whose principal business activity are conducted in PRC seeks to issue and list its shares in the name of an overseas enterprise based on equity, assets, income or other similar rights and interests of the relevant PRC domestic enterprise, such activities are deemed an indirect overseas issuance and listing in overseas markets.

The Draft Rules Regardingunder the Draft Overseas Listing stipulate that the Chinese-based companies, or the issuer, shall fulfill the filing proceduresRegulations. According to the Draft Overseas Listing Regulations, among other things, after making initial applications with overseas stock markets for offerings or listings, all China-based companies shall file with the CSRC within three working days

after the issuer makes an application for initial public offering and listing in a foreign exchange. The required filing materials forwith an initial public offering and listing shallthe CSRC include but not limited to:(without limitation): (i) record-filing reportreports and related undertakings; regulatory opinions,

record-, (ii) compliance certificates, filing, or approval and other documents issuedfrom by competent regulatory authoritiesthe primary regulator of relevant industriesthe applicants’ businesses (if applicable);, and(iii) security assessment opinionopinions issued by relevant regulatory authoritiesrelated departments (if applicable);, (iv) PRC legal opinion;opinions, and (v) prospectus. In addition, an issuer

who issues overseas listed securities after initial public offering shall, within three working days after the completion of the issuance,

submit required filing materials to the CSRC, including but not limited to: filing report and relevant commitment; and domestic legal

opinion. Furthermore, an overseas offering and listing isoverseas offerings and listings may be prohibited underfor such China-based companies when any of the following circumstancesapplies: (1) if the intended securities offeringofferings and listing islistings are specifically prohibited by nationalthe laws and, regulations and relevant provisionsor provision of the PRC; (2) if the intended securities offeringofferings and listinglistings may constitute a threat to, or endangersendanger national security as reviewed and determined by competent authorities under the State Council in accordance with lawlaws; (3) if there are material ownership disputes over theapplicants’ equity interests, major assets, and core technology,

etc. oftechnologies, or the issuerothers; (4) if, in the past three years, theapplicants’ domestic enterpriseenterprises or its controlling shareholders, orde actualfacto controllers have committed corruption, bribery, embezzlement, misappropriation of property, or other criminal offenses disruptive to the order of the socialist market economy, or are currently under judicial investigation for suspicion of criminal offenses, or are under investigation for suspicion of major violations; (5) if, in the past three years, any directors, supervisors, or senior executives of applicants have been subject to administrative punishments for severe violations, or are currently under judicial investigation for suspicion of criminal offenses, or are under investigation for suspicion of major violations; (6) other circumstances as prescribed by the State Council. The Draft AdministrationAdministrative Provisions defines

the legal liabilities of breaches such as failure in fulfilling filing obligations or fraudulent filing conducts, imposingfurther stipulate that a fine between RMB 1 million and RMB 10 million may be imposed if an applicant fails to fulfill the filing requirements with the CSRC or conducts an overseas offering or listing in violation of the Draft Rules Regarding Overseas Listings, and in cases of severe violations, a parallel order to suspend relevant businessbusinesses or halt operationoperations for rectification may be issued, revokeand relevant business permits or operational license. revoked.

At of the date of this

Registration Statement, the Draft Rules Regarding Overseas Listings have not been promulgated, and we have not been required to obtain

permission or filing from the PRC government authorities for any of our offerings. However, there is uncertainty in connection with whether

we are required to obtain permissions or filing from the PRC government authorities with respect of our operations and/or offering once

we have acquired our target PRC subsidiaries. In the event that the Draft Rules Regarding Overseas Listing take effect, we or any of our

subsidiaries may be subject to the filing and compliance requirements, we cannot assure you that any of us will be able to receive clearance

of such filing requirements in a timely manner, or at all. Any failure of us to fully comply with new regulatory requirements may significantly

limit or completely hinder our ability to offer our securities, cause significant disruption to our business operations, severely damage

our reputation, materially and adversely affect our financial condition and results of operations and cause our securities to significantly

decline in value or become worthless. See “Risk Factors—The approval of the CSRC or other PRC regulatory agencies may be required

under PRC law.”

Measures to Expanding

Efforts in Anti-Monopoly Enforcement

The PRC Anti-Monopoly

enforcement agencies have in recent years strengthened enforcement under the PRC Anti-Monopoly Law. In March 2018, the State Administration

for Market Regulation (the “SAMR”), was formed as a new governmental agency to take over, among other things, the Anti-Monopoly

enforcement functions from the relevant departments under the MOFCOM, the National Development Reform Committee (“NDRC”) and

the State Administration for Industry and Commerce (the “SAIC”), respectively. Since its inception, the SAMR has continued

to strengthen Anti-Monopoly enforcement. In December 2018, the SAMR issued the Notice on Anti-Monopoly Enforcement Authorization, which

grants authorities to its province-level branches to conduct Anti-Monopoly enforcement within their respective jurisdictions. In September

2020, the SAMR issued Anti-Monopoly Compliance Guideline for Operators, which requires, under the PRC Anti-Monopoly Law, operators to

establish Anti-Monopoly compliance management systems to prevent Anti-Monopoly compliance risks. On February 7, 2021, the Anti-Monopoly

Commission of the State Council officially promulgated the Anti-Monopoly Guidelines for Internet Platforms. Pursuant to an official interpretation

from the Anti-Monopoly Commission of the State Council, the Anti-Monopoly Guidelines for Internet Platforms mainly covers five aspects,

including general provisions, monopoly agreements, abusing market dominance, concentration of undertakings, and abusing of administrative

powers eliminating or restricting competition. On October 23, 2021, the SAMR released a draft amendment of Anti-Monopoly Law (the “AML”)

for public comments for the first time since the 2008 AML came into effect. This is the second round of published draft amendments to

the AML, which followed the previous set open for public consultation by the SAMR in January 2020. The draft amendments to the AML set

out new substantive rules including safe harbor for monopoly agreements, introduced “stop-the-clock” mechanism and enhanced

personal liability and monetary penalties for substantive violations.

As the Anti-Monopoly

Guidelines for Internet Platforms and the amendments to the AML are newly published, we are unable to estimate its specific impact on

our business, financial condition, results of operations and prospects and future acquisition of PRC subsidiaries. We cannot assure you

that our business operations will comply with such regulations and authorities’ requirements in all respects. Any failure or perceived

failure by us to comply such regulations and authorities’ requirements may result in governmental investigations or enforcement

actions, lawsuits or claims against us and could have an adverse effect on our business, financial condition and results of operations

upon our future acquisition of PRC subsidiaries.

Cybersecurity Measures

and Draft Regulation Regarding Cyber Data Security

On December 28, 2021,

the CAC, published the Measures for Cybersecurity Review (2021), which will come into effect on February 15, 2022 and replace the current

Measures for Cybersecurity Review (2020). The Measures for Cyber Security Review specifies that the procurement of network products and

services by operator of critical information infrastructure and the activities of data process carried out by Internet platform operator

that raise or may raise “national security” concerns are subject to strict cyber security review by Office of Cyber Security

Review established by the CAC. Before critical information infrastructure operator purchases internet products and services, it should

assess the potential risk of national security that may be caused by the use of such products and services. If such use of products and

services may give raise to national security concerns, it should apply for a cyber security review by the Cyber Security Review Office

and a report of analysis of the potential effect on national security shall be submitted when the application is made. In addition, Internet

platform operators that possess the personal data of over one million users must apply for a review by the Cyber Security Review Office,

if they plan listing of companies in foreign countries. The CAC may voluntarily conduct cyber security review if any network products

and services and activities of data process affects or may affect national security. It may take approximately 70 business days in maximum

for the general cybersecurity review upon the delivery of their applications, which may be subject to extensions for a special review.

In addition, on November

14, 2021, the Administration Regulations on Cyber Data Security (Draft for Comments) (《网络数据安全管理条例(征求意见稿)》

) (the “Draft Regulation”) was proposed by the CAC for public comments until December 13, 2021. The Draft Regulation stipulates

that data processors which process the personal information of at least one million users must apply for a cybersecurity review if they

plan listing of companies in foreign countries, and the Draft Regulation further requires the data processors that carry out the following

activities to apply for cybersecurity review in accordance with the relevant laws and regulations: (i) the merger, reorganization or division

of internet platform operators that have gathered a large number of data resources related to national security, economic development

and public interests affects or may affect national security; (ii) the listing of the data processor in Hong Kong affects or may affect

the national security; and (iii) other data processing activities that affect or may affect national security. Any failure to comply with

such requirements may subject us to, among others, suspension of services, fines, revoking relevant business permits or business licenses

and penalties. As advised by our PRC legal counsel, since the CAC is still seeking comments on the Draft Regulation from the public as

of the date of the Annual Report, the Draft Regulation (especially its operative provisions) and its anticipated adoption or effective

date are subject to further changes with substantial uncertainty.Regulations Relating to Value-added Telecommunications Services

As the Measures for Cyber

Security Review and the Draft Regulation are newly published, the exact scope of “critical information infrastructure operators”

and “data processing operators” under the draft measures and the current regulatory regime remains unclear, and the PRC government

authorities may have wide discretion in the interpretation and enforcement of these laws. Currently, the Measures for Cyber Security Review

and the Draft Regulation have not materially affected our business and operations, but in anticipation of the strengthened implementation

of cybersecurity laws and regulations and the continued expansion of our business, our future PRC subsidiary faces potential risks if

we are deemed as a critical information infrastructure operator or data processing operator under the PRC cybersecurity laws and regulations.

In such case, we must fulfill certain obligations as required under the PRC cybersecurity laws and regulations, including, among others,

storing personal information and other important data collected and produced within the PRC territory as part of our operations in China

(as we currently do in our operations), and we may be subject to lengthy cybersecurity review and other enhanced regulatory requirements

when purchasing internet products and services or conducting data processing activities. We may face challenges in addressing such enhanced

regulatory requirements and make necessary changes to our internal policies and practices in data privacy and cybersecurity matters. See

“Risk Factors — Risks Related to Our Business and Industry — We may be liable for improper

collection, use or appropriation of personal information provided by our customers.”

As of the date of this

filing of the Annual Report, we have no operating subsidiaries involved in any investigations on cybersecurity review initiated by the

CAC based on the draft measures, and we have not received any inquiry, notice, warning, sanctions in such respect or any regulatory objections

to this registration. As of the date of this registration statement, recent regulatory actions by China’s government related to

data security or anti-monopoly have not materially impacted our ability to conduct our business, accept foreign investments or list on

a U.S. or other foreign exchanges. Based on existing PRC laws and regulations, as advised by our PRC legal counsel, neither we nor our

subsidiaries are currently subject to any pre-approval requirement from the CAC to operate our business or conduct this registration,

subject to PRC government’s interpretation and implementation of the Measures for Cyber Security Review and the Draft Regulation

after it takes effect. However, we cannot assure you that relevant PRC government agencies, including the CAC, would reach the same conclusion

as we do or as advised by our PRC legal counsel.

Governmental Regulations

in Relation to the Company’s Businesses

This section set forth

a summary of the principal PRC laws and regulations relevant to our business and operations in China.

Regulations Related

to Foreign Investment

Guidance Catalogue

of Industries for Foreign Investment

Investment activities

in the PRC by foreign investors are principally governed by the Guidance Catalogue of Industries for Foreign Investment, or the Guidance

Catalog, which was promulgated and is

Pursuant to the Provisions on Administration of Foreign-Invested Telecommunications Enterprises which was promulgated by the State Council on December 11, 2001 and most recently amended from time to time by Ministry of Commerceon March 29, 2022, or MOFCOMthe FITE Regulations, and the National Development and Reform

Commission, or NDRC. The Guidance Catalog lays out the basic framework for foreign investment in China, classifying businesses into three

categories with regard to foreign investment: “encouraged,” “restricted” and “prohibited”. Industries

not listed in the catalog are generally deemed as falling into a fourth category “permitted” unless specifically restricted

by other PRC laws.

In addition, in June

2018 the MOFCOM and the NDRC promulgated the Special Management Measures (Negative List) for the Access of Foreign Investment, or the

Negative List, which became effective on July 28, 2018 and was further updated on June 30, 2019, June 23, 2020 and January 1, 2022.

Foreign Investment

Law

On March 15, 2019, the

National People’s Congress approved the Foreign Investment Law of the PRC, or the Foreign Investment Law, which came into effect

on January 1, 2020 and replaced the trio of existing laws regulating foreign investment in China, namely, the Sino-foreign Equity Joint

Venture Enterprise Law of the PRC, the Sino-foreign Cooperative Joint Venture Enterprise Law of the PRC and the Wholly Foreign-invested