UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 1-K

ANNUAL REPORT PURSUANT TO REGULATION A

For the fiscal year ended December 31, 2022

CWS Investments Inc.

| Virginia | 880822121 | |

| State or other jurisdiction

of incorporation or organization |

(I.R.S. Employer Identification Number) |

5242 Port Royal Rd #1785, North Springfield, VA 22151

703-988-2054

STATEMENTS REGARDING FORWARD-LOOKING INFORMATION AND FIGURES

This Annual Report on Form 1-K, or the Annual Report, of CWS Investments, Inc., a Virginia corporation, contains certain forward-looking statements that are subject to various risks and uncertainties. Forward-looking statements are generally identifiable by use of forward-looking terminology such as “may,” “will,” “should,” “potential,” “intend,” “expect,” “outlook,” “seek,” “anticipate,” “estimate,” “approximately,” “believe,” “could,” “project,” “predict,” or other similar words or expressions. Forward-looking statements are based on certain assumptions, discuss future expectations, describe future plans and strategies, contain financial and operating projections or state other forward-looking information. Our ability to predict results or the actual effect of future events, actions, plans, or strategies is inherently uncertain. Although we believe that the expectations reflected in our forward-looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth or anticipated in our forward-looking statements. Factors that could have a material adverse effect on our forward-looking statements and upon our business, results of operations, financial condition, funds derived from operations, cash available for distribution, cash flows, liquidity and prospects include, but are not limited to, the factors referenced in our offering circular dated July 13, 2022, under the caption “RISK FACTORS” and which are incorporated herein by reference (https://www.sec.gov/edgar/search/#xsl1-A_X01/primary_doc.xml).

When considering forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this report. Readers are cautioned not to place undue reliance on any of these forward-looking statements, which reflect our views as of the date of this report. The matters summarized below and elsewhere in this report could cause our actual results and performance to differ materially from those set forth or anticipated in forward-looking statements. Accordingly, we cannot guarantee future results or performance. Furthermore, except as required by law, we are under no duty to, and we do not intend to, update any of our forward-looking statements after the date of this report, whether as a result of new information, future events or otherwise.

i

Item 1. Business

Unless the context otherwise requires or indicates, references in this annual report to “us,” “we,” “our” or “our Company” refer to CWS Investments, Inc., a Virginia corporation.

The Company was formed in 2022 as a Virginia corporation. The Company will make preferred equity investments in first lien position mortgage notes and contract for deeds throughout the United States with conservative loan to value characteristics. Meaning, the Company only intends to purchase Notes that are fully secured. While the Company will typically only invest in first mortgages, the Company may opportunistically invest in second mortgages, lease options if they meet the aforementioned conservative characteristics. The Company may also invest in Class A and B single family homes and smaller multi-family residential properties. If investing in single family homes and/or multi-family property, the Company expects to do so on a cash basis, but in no event will the Company use leverage in excess of 60% loan to value.

The Company’s investment objectives with respect to acquiring Assets are to effectively deploy the proceeds of the Offering in Assets which are expected to: Preserve and protect each Investor’s contributed; and provide the Investor with a Preferred Return commensurate with the Investor class of preferred stock, as well as provide Investors with a full return of their capital contributions. No assurance can be given that these objectives will be attained or that the Company’s capital will not decrease.

The business in which the Company operates is not dependent on patents, trademarks, franchises, concessions, royalty agreements or labor contracts. To the extent that licenses are required to engage in the business in any particular jurisdiction, Management is experienced in obtaining said license and does not expect the process to hinder or delay the business of the Company. The business of the Company does not involve environmental issues, and as such, does not expect to incur any significant costs relating to environmental compliance.

Company History

As previously stated, the Company was formed in 2022 and has a limited operating history. While the company is newly formed, Mr. Seveney has extensive history in the industry, as more fully set forth below. Neither the Company, its directors, nor any Key Man has been a debtor in any bankruptcy, receivership or similar proceeding. There has not been any material reclassification, merger, consolidation, or purchase or sale of a significant amount of assets of the Company not in the ordinary course of business.

The Mortgage Market

We realize that uncertainty creates opportunity. From an investor perspective, the volatility of the stock market and impending fears of inflation are causing many investors to look for other options. The long-term value of real estate is attractive, and due to constantly changing markets, there will constantly be a significant opportunity in the distressed real estate asset market.

The Secondary Mortgage Market for Investors

Mortgages are originated in the primary market, where home buyers obtain loans from banks, credit unions or other financial institutions. Most lenders pool the loans they have originated and sell these pools to generate funds for continued lending. The secondary distressed mortgage market is a billion-dollar industry in which all types of mortgage loans, prime, sub-prime, conforming and non-conforming, are sold to investors, occasionally individually but most commonly in pools that aggregate multiple mortgages.

1

Buyers of loans in the secondary mortgage market include large institutions as well as smaller investment funds and other professional investors who specialize in mortgage investing. Many large institutional investors repackage mortgages into mortgage-backed securities (MBS) that are in turn sold to other investors. Investors may also purchase loans to hold to maturity in a loan portfolio or produce cash flows that will offset other future liabilities.

Investors can purchase non-performing loans at prices significantly below outstanding balances, otherwise known as “the UPB”. The investor can then rehabilitate the loans or reclaim the property, thus generating an attractive return on the original investment. This is the primary goal of this investor.

Current & Projected Market Conditions

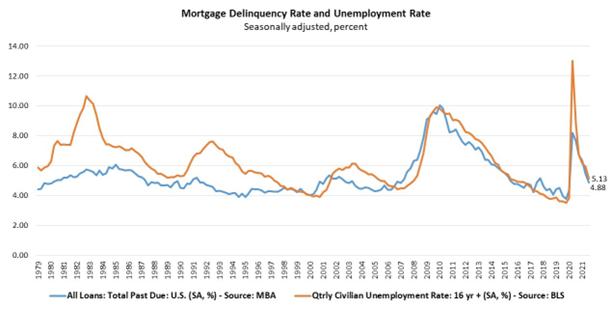

The performance of mortgages is primarily correlated to unemployment. Since the start of the COVID pandemic in 2020, moratoriums were put in place to protect borrowers from losing their homes. These moratoriums have led to a reduction in available inventory on the secondary market and an increase in pricing caused by supply and demand. Since these moratoriums have been lifted, most economists predict mortgage delinquency rates will increase due to the rise in unemployment and interest rates due to inflation risks. These increases should lead to greater inventory on the secondary market.

Acquisition Strategy

Our acquisition strategy is not focused on a single source. We will be focused on targeting banks, private equity firms who hold notes, brokers, auction platforms, other note funds and individual investors.

2

Non-performing loans are mortgages where the borrower is behind on payments. Typically, a loan is considered non-performing when the loan is more than ninety-days past due. Financial institutions will sell these loans as they are not typically staffed to handle a significant number of delinquent loans. We have also found that many banks seek to offload non-performing loans for a multitude of tax planning and general business strategy considerations. These loans can then be purchased at a discount of the balance due thereon. We also target private equity funds. Private Equity funds acquire thousands of delinquent non-performing loans at a significant discount. They will break the loans down into tranches or classes of loans which:

| ● | They manage to a successful conclusion to maximize value and will then liquidate. |

| ● | Immediately look to liquidate due to the loan not meeting its requirements. An example of this is a loan with a $50,000 value takes the same effort and costs to foreclose as a $500,000 loan. Therefore, when incorporating manpower and returns, they focus on loans with most value. |

Like other real estate asset classes, private equity funds investing in mortgage debt are constantly acquiring and liquidating assets for liquidity or in the case of closed-end funds, when they are winding down fund operations. These instances present ideal buying situations. We have also found that these situations also present ideal opportunities to purchase residential properties that the fund obtained and that it needs to offload in order to wind down operations.

Other Sources:

Other sources consist of buying from individual investors, smaller note funds and originating new loans. In the past five years, the management team has developed relationships with over twenty-five known funds and note sellers.

Governmental Regulation

The industry in which the Company intends to participate is regulated at both state and federal levels, both with respect to its activities as an issuer of securities and its investing activities. Some of these regulations are discussed in greater detail below under “Risk of Failure to Comply with Securities Laws ” “Relaxed Ongoing Reporting Requirements,” and the other related Risk Factors identified herein. The Company or the Company’s Assets may be subject to governmental regulations in addition to those discussed in the Offering, and new regulations or regulatory agencies may develop that affect the Company’s operations and ability to generate revenue. The Company will attempt to comply with all applicable regulations affecting the markets in which it operates. However, such regulation may become overly burdensome and therefore may have a negative effect on the Company’s ability to perform as illustrated.

Other laws, regulations, such as the Dodd-Frank Wall Street Reform and Consumer Protection Act, and programs at the federal, state, and local levels are under considerations that seek to address the economic climate and real estate and other markets and to impose new regulations on various participants in the financial system. The effect that these or other actions will have on the Company’s business, results of operations, and financial condition and not completely foreseeable at this time. Further, the failure of these or other actions and the financial stability plan to stabilize the economy could harm the Company’s business, results of operations, and financial condition.

3

Profile for Targeted Assets

There is currently over $400B in distressed mortgage notes across the United States. The fund is looking to target a very small component of this market in a strategic manner to acquire non-performing notes that have an upside economic potential with designed exit strategies. We focus to identify and source notes which are undervalued and relate to residences located in favorable neighborhoods. Purchasing notes at below market prices after performing the proper due diligence enables the Company to spread its risk of loss over a greater pool of assets and at lower price points than purchasing notes at higher retail purchase prices.

Benefits of Notes Versus Other Alternative Investments

Passive Cash Flow

Owning a note is easier to manage than a property. When a borrower is paying it is considered “mailbox money”. Compared to owning the physical real estate, owning the secured debt does not subject you to dealing with tenants, toilets and termites.

Portfolio Management

A note portfolio can be managed from any location with internet access. The management consists of a team of professionals consisting of attorneys, a servicing company, realtors and preservation companies. Unlike rentals, where most investors own “in their own backyard”, a note portfolio can be more diversified, but each asset is still managed in the same manner.

Profitability in Varying Market Conditions

Note prices in the marketplace function in relation to supply and demand and are correlated to real estate values. The big difference is with notes, profits increase in a down market as note prices decrease which allows more flexibility to rehab the borrower and get them repaying. Remember – even in a down economy people need a place to live and in many instances their mortgage payment is less than rent.

Collateral

Real estate is one of the safest investments. Unlike stocks that are backed by very little collateral and have high volatility, a note is less volatile and is secured by real physical property.

4

Versatility

With notes, there are numerous exit strategies. The Notes can be resold, modified or taken back by the Lender. The Borrower can refinance the loan and payoff us as the lender.

With non-performing notes, the most advantageous outcome for the borrower and lender is for the borrower to make payments. If we can get the borrower to reperform, the asset increases in value and can be liquidated at higher margins. If the borrower cannot make the current payments on the loan, the lender has multiple options including; loan modification; deed-in-lieu of foreclosure; or foreclosing on the property.

History of Management and the Affiliates

The manager has successful experience managing mortgage note funds. These include business endeavors exempt from registration under Regulation D 506(c) and 506(b). These funds historically have been successful in acquiring assets for the portfolio while managing the required reserves required for potential legal costs, while consistently returning a profit to the investors.

Company Property

The Company does not currently own or lease office-space but reserves the right to do so in the future. The Company relies heavily on digital operations. Management is nearly paperless, with all documents secured and managed digitally. Management utilizes industry proven software that allows it to track and manage its investments with confidence and accuracy.

Legal Proceedings

Legal proceedings are a routine part of the business of the Company. For instance, it is routine that the Company may need to bring a lawsuit against a borrower for the amount due under a debt obligation or to foreclose on the collateralized property. It is also a normal aspect of business that a borrower may preemptively bring a lawsuit seeking to have a debt obligation stricken. These types of lawsuits are not common and in Management’s experience, rarely end in a cancellation of the underlying debt.

Neither the Company, Management, nor any director, officer or affiliate of the Company, nor any owner of record or beneficially of more than five percent of any class of voting securities of the Company, nor any associate of any such director, officer, affiliate of the registrant, or security holder is a party adverse to the Company or any of its subsidiaries or has a material interest adverse to the registrant or any of its subsidiaries. This attestation applies to any administrative or judicial proceedings.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion of our financial condition and results of operations should be read in conjunction with our financial statements and the related notes thereto contained in this Annual Report on Form 1-K (“Annual Report”). The following discussion contains forward-looking statements that reflect our plans, estimates, and beliefs. Our actual results could differ materially from those discussed in the statements regarding forward-looking information and figures. Unless otherwise indicated, the latest results discussed below are as of December 31, 2022.

5

Offering Results and Distributions

The Company issued 660,163 shares of Class A Preferred Stock (“Preferred Shares”) and 34,979 of Bonus Class A Preferred Stock (“Bonus Shares”) at an initial stated price of $10 per share. The Company did not receive monetary compensation for the Bonus Shares issued and is obligated to pay a cumulative cash dividend on each Bonus Share at a per annum rate of 8% of the stated value of such share. All dividends paid to date have been paid from funds received from the issuance of Preferred Shares and Common Stock additional paid-in capital. We have raised total gross offering proceeds of $6,601,630 and paid dividends of $132,956. We expect to continue to pay dividends on Preferred Shares and Bonus Shares on a monthly basis in the near term.

Our Preferred Shares are not currently listed on a national securities exchange or included for quotation on a national securities market, and there is currently no intention to list our Preferred Shares.

Preferred Shares and Bonus Shares are considered redeemable outside of the Company’s control and, therefore, are presented as a Commitment and Contingency in our Balance Sheet outside of Stockholders’ Equity. The terms of redemption on our Preferred Shares can be found in the Limited Right of Liquidity section of our Offering Circular.

Results of Operations

We consider our portfolio to include two segments: Residential Mortgage Loans and Real Estate Property. These segments reflect the way we evaluate our business performance and manage our operations. As of December 31, 2022, our portfolio consisted of 27 non-performing loans, 69 performing loans, and 3 real estate properties. During the operating period, we sold one real estate property, and we had two loans payoff earlier than the contractual maturity date.

For the 12 months beginning January 1, 2022 and ending December 31, 2022 (the “Operating Period”), the Company had a Net Operating Loss (“NOL”) of $882,621. The NOL over the Operating Period was primarily driven by payroll related expenses of $725,146, Advertising and Marketing costs of $54,363, and Accounting fees of $23,925.

Total Revenues and Other Income

The Company was not able to generate revenue preceding the date of SEC Qualification on July 13, 2022. From the date of SEC Qualification through December 31, 2022, the Company generated $53,716 of total revenues and $10,300 of Other Income as presented in the Statement of Operations.

Other Revenue consisted of $14,942 in business credit card cash rewards and $2,500 in forfeited earnest money on the sale of a real estate property.

6

Residential Mortgage Loans

The amount of contractual interest income recognized for our performing loans is $25,902. Interest Income recognized due to early loan payoffs is $9,024. In addition, we collected $273 of late fees and $1,075 of recoverable fees paid by the seller prior to our acquisition. The recoverable fees are considered to have no value at acquisition due to the uncertainty of collectability.

Real Estate Properties

We purchased a total of four real estate properties in 2022. The first property we purchased was a single-family residential home located in Johnstown, PA. The Company purchased this property from a related party with the intention of selling the property if the market allowed, and if not, converting it to a rental property. Subsequent to the Company’s acquisition, there was a shortage of inventory in the local real estate market for lower priced homes. The sudden increase in demand drove up the value of the home, which prompted Management to sell the property after a short holding period. A Gain on Sale of Real Estate Property of $10,300 is shown in Other Income in the Statement of Operations related to the sale of the home in Johnstown, PA.

In addition to the Johnstown, PA home, the Company purchased three apartment buildings, each containing four rental units, located in Rutland, VT from a related party. All three apartment buildings were purchased on December 23, 2022. Five units were occupied at the time of acquisition and seven units were vacant. A table of the future contractual amounts due to the Company from the tenants in the five units is in Note 9 Leases in the financial statements. The Company did not recognize any rental income related to the leases acquired with the apartment buildings due to owning them for one week during the Operating Period. In-place Lease Intangible Assets represent the estimated fair value of the net cash flows of leases in place at the time of acquisition, as compared to the net cash flows that would have occurred had the property been vacant at the time of acquisition and subject to lease up. Management assigned a value of $7,500 for each of the five leases acquired, for a total of $37,500 shown in In-place Lease Intangible Asset on the Balance Sheet. The In-place Lease Intangible Asset will be amortized into income on a straight-line basis over the remaining life of the leases.

Expenses

Total Expenses during the Operating Period are $946,637 as shown in the Statement of Operations.

Advertising and Marketing

The Company incurred $1,231,033 in advertising and marketing costs. The total cost of advertising and marketing the offering was $1,176,670 and is charged to equity and is included in Accumulated Deficit in the Balance Sheet in the financial statements. Advertising and marketing costs of $54,363 that is not related to the Offering is shown in the Statement of Operations in the financial statements. We expect the cost of advertising the Offering to decrease in future periods.

7

General and Administrative (G&A)

G&A expenses total $856,263 and are primarily due to payroll related expenses of $725,146 and accounting expenses of $23,925. We recognized depreciation expense of $959 for computer equipment on a straight-line basis using a five-year life.

Residential Mortgage Loan Expenses

Expenses related to our residential mortgage loans is $25,956 and include:

| Due Diligence | $ | 3,363 | ||

| Legal | 5,575 | |||

| Loan Servicing Fees | 10,631 | |||

| Property Inspections | 2,738 | |||

| Title Reports | 2,999 | |||

| Miscellaneous | 650 | |||

| Total | $ | 25,956 |

Real Estate Property Expenses

Expenses related to our real estate property is $10,055 and include:

| Property Tax | $ | 1,227 | ||

| Disposition Expenses | 5,928 | |||

| Miscellaneous | 2,900 | |||

| Total | $ | 10,055 |

Income Taxes

The Company did not recognize any expense for income taxes due to a NOL for the operating period. Our policy related to income taxes can be found in Note 2 Summary of Significant Accounting Policies in the financial statements. The NOL for the operating period generated a tax deferred asset of $227,186. We recognized a full valuation allowance for the tax deferred asset based on the lack of historical income due to being a start-up company, and the uncertainty of being able to offset the carry-forward loss against future income. Further details can be found in Note 3 Income Taxes in the financial statements.

Critical Accounting Policies and Estimates

The discussion and analysis of our financial condition and results of operations are based upon our financial statements, which have been prepared in accordance with U.S. generally accepted accounting principles (“GAAP”). The preparation of financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities. On an on-going basis, we evaluate our estimates, including those related to revenue recognition, impairment of interest receivables and in-place lease assets, valuation of investments, contingent consideration, income taxes and contingencies and litigation, among others. We base our estimates on historical experience and on various other assumptions that we believe to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from those estimates under different assumptions or conditions. The accounting estimates and assumptions discussed in this section are those that we consider to be the most critical to an understanding of our financial statements because they inherently involve significant judgments and uncertainties. For a discussion of our significant accounting policies, refer to Note 2 Summary of Significant Accounting Policies in the notes to the financial statements.

8

Revenue Recognition

We recognize interest income on our mortgage loans based upon whether the loan is in accrual or non-accrual status. The status of our loans is determined by Management and requires a significant amount of judgment related to the future collectability of the contractual principal and interest. Further details on our revenue recognition policy and accrual versus non-accrual status can be found within the section titled Revenue Recognition in Note 2 Summary of Significant Accounting Policies in the financial statements.

Allowance for Residential Mortgage Loans and Real Estate Property Impairment Loss

The allowance for loan losses is reviewed for adequacy based on collateral values, credit quality indicators, and economic conditions among others. We review our mortgage loans periodically, on a loan-by-loan basis, to determine the probability of loss, and record charge-offs after considering such factors as delinquencies, the financial condition of the obligors, the value of the underlying collateral, as well as third party credit enhancements such as guarantees. We did not record an allowance for loan losses as of December 31, 2022.

The Company monitors events and circumstances that could indicate an impairment to the value of its real estate property. We did not record any impairment charges as of December 31, 2022.

Refer to Note 2 Summary of Significant Accounting Policies in the notes to the financial statements within the section titled Impairment of Real Estate Property and Loan Impairment for further details regarding our impairment policies.

Liquidity and Capital Resources

The Company is seeking to raise up to $75,000,000 of capital in its Offering by Selling Class A Preferred Shares to Investors. The Company expects to deploy the majority of the capital to acquire and manage real estate backed loans, as well as other real estate related assets, to include single family homes and smaller, multi-family residential properties.

As of December 31, 2022, the Company’s operations were being funded by Ownership and Investor proceeds from the issuance of its Class A Preferred Shares. The total net amount funded by Ownership was $222,000 and is included in Additional Paid-in Capital on the Balance Sheet.

9

We require capital to fund our investment activities and operating expenses. Our capital sources may include net proceeds from our future Offerings, cash flow from operations, net proceeds from asset repayments and sales and borrowings under credit facilities.

We obtain the capital required to acquire and manage a diversified portfolio of real estate investments and conduct our operations from the proceeds of our Offering. During 2022, we deployed approximately $2.47 million for 102 investments. The total amount of cash deployed for the portfolio of 99 investments as of December 31, 2022 is approximately $2.45 million and we had approximately $2.29 million in cash and cash equivalents.

We anticipate that cash on hand, future cash flows from operations, and proceeds from our potential future Offerings will provide sufficient liquidity to meet future funding commitments and costs of operations.

In the event the company seeks to invest in residential properties, the Company may seek to finance the acquisition if such financing allows the Company to leverage the purchase on favorable terms, while still generating a return. As of December 31, 2022, the company did not seek or obtain any leverage.

If we are unable to raise additional funds, we may have challenges with liquidity and capital resources on a long-term basis. The Company would make fewer investments resulting in less diversification in terms of the type, number and size of investments we make. We may be subject to more fluctuations based on the performance of the specific assets we acquire. Further, we have certain direct and indirect operating expenses. Our inability to raise substantial funds would increase our fixed operating expenses as a percentage of gross income and would limit our ability to make distributions.

Plan of Operations

In order to operate our Company for 12 months, we estimate that approximately $2.6 million in funds will be required. The Company had approximately $2.2 million in cash as of December 31, 2022. If we fail to generate revenues from our portfolio, we will be required to fund operations with existing proceeds from the issuance of Class A Shares and/or we will be forced to liquidate part of our portfolio to be able to fully carry out our plan of operations.

Off Balance Sheet Arrangements

The Company does not have any off-balance sheet arrangements that have or are reasonable likely to have a current or future effect on our financial condition, changes in financial condition, revenue or expenses, results of operations, liquidity or capital expenditures that are material to an investment in our securities.

10

Trend Information

With interest rates rising rapidly, and inflation still above 5%, a small percentage of our borrowers who were performing were unable to repay their loans. This meant that we had to devote additional time and resources to reaching a resolution on these loans.

While we expect this trend to continue in the short term, we believe there is significant cause for optimism regarding the Company’s and the current portfolios’ potential moving forward. Among these reasons:

| ● | An inverted US Treasury yield curve has historically been a warning sign of impending recession. The US 10-year Treasury yield has been going below the 2-year yield since July of 2022, with the inversion exceeding 80 bps in December, a degree not seen since 1981. In any recession, comes job losses and increased number of defaulted loans. We expect to see an increase in defaulted loans on the market which will allow us to acquire loans at a greater discount | |

| ● | We recently had the collapse of Silicon Valley Bank and Signature Bank. The banks failed partially due to interest rate risks and liquidity. When withdrawals increased on these institutions, they were required to sell off some of their bond portfolios. Due to these being low interest rate bonds acquired when interest rates were near zero, they held significantly less value since current interest and bond rates are significantly higher. This led to these institutions taking major losses on these assets. We believe this trend will continue as long as interest rates remain high which the Federal Reserve has noted they do not intend on lowering the rate in 2023. |

| ● | Almost $1.5 trillion of US commercial real estate debt comes due for repayment before the end of 2025. Estimates are office and retail property valuations could fall as much as 40% from peak to trough, increasing the risk of defaults. Multifamily properties have decreased 15% since their peak in recent months. As much as 70% of the other commercial real estate loans that mature over the next five years are held by banks. Increasing interest rates and decreasing property values will make it extremely difficult for borrowers to refinance and pay off these loans. This may lead to a significant increase in commercial defaults. These banks will be pressured to liquidate these loans as they will have to mark-to-market their value. This will increase the overall supply of defaulted debt in the space which should bring down pricing on commercial loans as well as residential loans. |

| ● | Home prices are higher than they have been in a generation. With interests increasing rapidly and now ranging from 5-7% home affordability is at all-time lows. The combination of higher home prices and mortgage rates between 6.5 and 7.0 percent makes monthly mortgage payments up to 50 percent higher than they would have been on the same property a year earlier. Along with credit markets tightening standards, conditions may lead to home price decreases. This means a loans loan to value may increase and the potential for some loans to be “underwater”, meaning the loan balance is greater than the property value. This trend could impact the profitability of the Company to our Investors. |

Although we have no way of knowing if these trends will continue in the future, we believe that the balance of the evidence shows favorable operating conditions for the Company moving forward.

11

Item 3. Directors and Officers

Executive Officers, Directors and Key Employees

The Company is managed by Christopher Seveney, the President, Chief Executive Officer, Chief Financial Officer and Chairman of the Board. Christopher Seveney is an experienced real estate professional who has been actively buying and selling mortgage notes since 2016. During this time, he has acquired over 500 notes with UPBs in excessive of $75 million in over forty states. Prior to investing in mortgage notes, Christopher built a multimillion dollar portfolio of assets through new construction and rehabilitating existing properties in his own portfolio along with having managed the construction of over $750 million in new construction in his twenty-five year professional career.

The Company also employs Lauren Wells as a full-time employee to assist Mr. Seveney in the management of the Company. Ms. Wells’ title is Vice President of Investor Relations & Strategy where she leads the strategic evaluation of market research and implements, leads and supports the business strategies. She is also responsible for setting the corporate marketing and sales goals.

Ms. Wells earned a Bachelor of Arts from UC Santa Barbara. Starting in 2021, prior to her employment with the Company, she worked side by side with Christopher Seveney in a senior level position on fund management and business strategy for Mr. Seveney’s other funds.

She brings over 10 years of business development, sales and project management experience to the company. Prior to joining the company, she worked as a senior consultant with SAAS startups including Procore and Linkedin to build and scale their sales organizations. This included developing forecasts, defining target markets, identifying acquisition opportunities, and establishing new sources of revenue. Ms. Wells has also been a real estate investor since 2010. During this time, she has helped grow and manage a portfolio of over 100 assets which include both residential real estate and mortgage notes.

12

Management reserves the right to make additional hires in the interests of the Company and in the sole discretion of Management.

| Name | Position | Age | Term of Office | Full or Part Time | ||||

| Christopher Seveney | President, Chief Executive Officer and Chairman of the Board of Directors | 47 | 3 (2022-2025) | Full | ||||

| Lauren Wells | Vice President, Investor Relations & Strategy, Member at Large | 34 | 2 (2022-2024) | Full | ||||

| Jeffrey Laroche1 | Member at Large | 49 | 2 (2022-2024) | Board Only | ||||

| Alan Belniak2 | Member At Large | 48 | 2 (2022-2024) | Board Only |

Management Compensation

The table below presents the annual compensation of each of the two highest paid executive officers and directors of the Company for its current (2022) fiscal year.

| Name | Title | Annual

Cash Compensation | Other Compensation | Total Compensation | ||||||||||

| Christopher Seveney | President, CEO, CFO and Chairman of the Board | $ | 300,000 | 3 | $ | 0 | $ | 300,000 | ||||||

| Lauren Wells | Vice President, Investor Relations & Strategy | $ | 170,000 | Up to $75,000 | 4 | Up to $245,000 | ||||||||

The Company’s directors do not receive additional compensation for their service on the Board or attendance at Board meetings.

| 1 | Non-compensated Member at Large of the Board of Directors. |

| 2 | Non-compensated Member at Large of the Board of Directors. The Company entered into a contract for general marketing consulting services on February 6, 2023. The terms of the contract are $130 per hour not to exceed 20 hours per month. |

| 3 | Mr. Seveney will receive an annual base salary of $300,000 plus additional benefits such as health, life, and disability insurance, as well as retirement benefits in the company 401k plan. Mr. Seveney is the sole common stockholder and therefore is likely to receive additional compensation by way of his entitlement to the common stockholder distributions. Mr. Seveney’s compensation and benefits, just like all other employees, will be a Fund Expense. |

| 4 | Ms. Wells’ employment commenced on March 28, 2022. She is entitled to benefits in the way of health, life, and disability insurance, as well as retirement benefits in the form of the company 401k plan. Ms. Wells is entitled to one-time target bonus of up to $75,000. The target bonus is based off of the total amount raised, or .1% of the total amount raised. |

13

Item 4. Security Ownership of Management and Certain Security Holders

The following table sets out, as of April 1, 2023, the voting securities of the company that are owned by executive officers and directors, and other persons holding more than 10% of any class of the company’s voting securities or having the right to acquire those securities. The table assumes that all options and warrants have vested. The company’s voting securities include all shares of Common Stock.

Name and Address of Beneficial Owner | Title of Class | Amount and Nature

of | Amount

and Nature of Beneficial Ownership Acquirable | Percent | ||||||||||

| Christopher

Seveney 5242 Port Royal Rd #1785, North Springfield, VA 22151 | Common Stock | 1,000,000 | 0 | 100 | % | |||||||||

Item 5. Interest of Management and Others in Certain Transactions

Chris Seveney is the President and CEO and is responsible for the day to day operations of the Company. Mr. Seveney is the sole owner of the common stock. Mr. Seveney is also one of several owners of BIFI Loan Servicing LLC (“BIFI”). The Company contracts with BIFI to provide loan servicing and other related services for notes held by the Company in those states in which BIFI is licensed to provide such services. BIFI was formed in 2021 and since then has been engaged in the servicing of loans for third parties. The Company intends to pay BIFI such fees as are customary in the industry and as are further set forth in the Servicing Agreement, set forth in the Servicing Agreement, attached as an exhibit to the Offering.

Mr. Seveney is also a principal in other companies involved in affiliated businesses including 7E Investments LLC, Sunnyhill Ventures 2020 LLC, Sunnyhill Mortgage Note Fund 2021 LLC, Y&R I Opportunity Fund LLC, Y&R 2022 LLC, Greyt Estates LLC, Onyx & Shadow Equities LLC, Integrity Mortgage Note Fund LLC, MFT RE Holdings LLC. The majority of the investments purchased by the Company in 2022 were purchased from the portfolio of some of these companies.

Item 6. Other Information

The Company is finalizing terms with a third party broker-dealer to replace the existing broker-dealer of record. The scope of work for the existing Broker-Dealer was for compliance only. The new Broker-Dealer will be for compliance as well as assist in capital raising efforts. The new broker-dealer would receive commissions from sales of shares. The Company will be allocating the remaining costs budgeted in the original offering for marketing to these Broker-Dealer fees to offset the fees charged by the Broker-Dealer. These financial adjustments will be reflected in future filings.

As provided for in a February 2, 2023 Form D Filing, the Company is offering an additional $75,000,000 of Class B, C, and D Securities through a Regulation D 506c offering.

14

Item 7. Financial Statements

REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS

Board of Directors

CWS Investments Inc.

Opinion

We have audited the financial statements of CWS Investments Inc. (a Virginia corporation) (the “Company”), which comprise the balance sheet as of December 31, 2022, and the related statements of operations, changes in stockholders’ deficit, and cash flows from February 22, 2022 (inception) to December 31, 2022, and the related notes to the financial statements. In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2022, and the results of its operations and its cash flows from February 22, 2022 (inception) to December 31, 2022 in accordance with accounting principles generally accepted in the United States of America.

Basis for opinion

We conducted our audit of the financial statements in accordance with auditing standards generally accepted in the United States of America (US GAAS). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are required to be independent of the Company and to meet our other ethical responsibilities in accordance with the relevant ethical requirements relating to our audit. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Responsibilities of management for the financial statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America, and for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is required to evaluate whether there are conditions or events, considered in the aggregate, that raise substantial doubt about the Company’s ability to continue as a going concern for one year after the date the financial statements are issued.

15

Auditor’s responsibilities for the audit of the financial statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance but is not absolute assurance and therefore is not a guarantee that an audit conducted in accordance with US GAAS will always detect a material misstatement when it exists. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. Misstatements are considered material if there is a substantial likelihood that, individually or in the aggregate, they would influence the judgment made by a reasonable user based on the financial statements.

In performing an audit in accordance with US GAAS, we:

| ● | Exercise professional judgment and maintain professional skepticism throughout the audit. |

| ● | Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. |

| ● | Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control. Accordingly, no such opinion is expressed. |

| ● | Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluate the overall presentation of the financial statements. |

| ● | Conclude whether, in our judgment, there are conditions or events, considered in the aggregate, that raise substantial doubt about the Company’s ability to continue as a going concern for a reasonable period of time. |

We are required to communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit, significant audit findings, and certain internal control-related matters that we identified during the audit.

Supplementary information

Our audit was conducted for the purpose of forming an opinion on the financial statements as a whole. The supplemental schedule of mortgage loans on real estate as of December 31, 2022 is presented for purposes of additional analysis and is not a required part of the financial statements. Such supplementary information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures. These additional procedures included comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with US GAAS. In our opinion, the supplementary information is fairly stated, in all material respects, in relation to the financial statements as a whole.

/s/ GRANT THORNTON LLP

Philadelphia, Pennsylvania

April 28, 2023

16

CWS Investments Inc.

Balance Sheet

As of December 31,2022

| ASSETS | ||||

| Residential Mortgage Loans, Held-for-Sale, Net | $ | 1,963,271 | ||

| Real Estate Property, Net (Building and Land) | 434,378 | |||

| In-place Lease Intangible Assets | 37,500 | |||

| Cash and Cash Equivalents | 2,292,583 | |||

| Interest Receivable | 13,391 | |||

| Contribution Receivable | 11,000 | |||

| Other Receivables | 16,160 | |||

| Prepaid Expenses | 52,895 | |||

| Due From Related Parties | 11,598 | |||

| Furniture and Equipment, Net | 6,553 | |||

| Total Assets | 4,839,329 | |||

| LIABILITIES, REDEEMABLE SERIES A PREFERRED STOCK, AND STOCKHOLDERS’ DEFICIT | ||||

| Accounts Payable | $ | 87,798 | ||

| Credit Card Obligations | 173,157 | |||

| Accrued Liabilities | 56,275 | |||

| Total Liabilities | 317,230 | |||

| Commitments and Contingencies | ||||

| Series A Preferred Stock, 695,142 Shares at Redemption Value | 6,601,630 | |||

| Stockholders’ Deficit | ||||

| Common Stock 1,000,000 Shares Authorized, 1,000,000 Shares Outstanding; Zero Par Value Per Share | - | |||

| Additional Paid-in Capital | - | |||

| Accumulated Deficit | (2,079,531 | ) | ||

| Total Stockholders’ Deficit | (2,079,531 | ) | ||

| TOTAL LIABILITIES, REDEEMABLE SERIES A PREFERRED STOCK, AND STOCKHOLDERS’ DEFICIT | $ | 4,839,329 | ||

See accompanying notes to the financial statements

17

CWS Investments Inc.

Statement of Operations

From Inception (February 22, 2022) to December 31, 2022

| REVENUES | ||||

| Mortgage Loans: | ||||

| Interest Income | $ | 34,926 | ||

| Late Fees and Other | 1,348 | |||

| Other Revenue | 17,442 | |||

| Total Revenues | 53,716 | |||

| OPERATING EXPENSES | ||||

| General and Administrative | 856,263 | |||

| Mortgage Loan Expenses | 25,956 | |||

| Real Estate Property Expenses | 10,055 | |||

| Advertising and Marketing | 54,363 | |||

| Total Operating Expenses | 946,637 | |||

| OTHER INCOME | ||||

| Gain on Sale of Real Estate Property | 10,300 | |||

| Total Other Income | 10,300 | |||

| LOSS BEFORE TAXES | (882,621 | ) | ||

| Income Tax Expense | - | |||

| NET LOSS | $ | (882,621 | ) | |

| Series A Preferred Stock Dividends | (132,956 | ) | ||

| NET LOSS AVAILABLE TO COMMON STOCKHOLDER | $ | (1,015,577 | ) | |

See accompanying notes to the financial statements

18

CWS Investments Inc.

Statement of Cash Flows

From Inception (February 22, 2022) to December 31, 2022

| CASH FLOWS FROM OPERATING ACTIVITIES | ||||

| Net Loss | $ | (882,621 | ) | |

| Adjustments to Reconcile Net Loss to Net Cash Used in Operating Activities: | ||||

| Furniture and Equipment: Accumulated Depreciation | 959 | |||

| Gain on Sale of Real Estate Property | (10,300 | ) | ||

| Purchase of Residential Mortgage Loans, Held-for-Sale | (1,993,988 | ) | ||

| Loan Costs | (9,727 | ) | ||

| Principal Payments on Residential Mortgage Loans, Held-for-Sale | 23,214 | |||

| Principal from Payoff of Residential Mortgage Loans, Held-for-Sale | 17,230 | |||

| Changes in Operating Assets and Liabilities | ||||

| Contribution Receivable | (11,000 | ) | ||

| Other Receivables | (16,160 | ) | ||

| Prepaid Expenses | (52,895 | ) | ||

| Due From Related Parties | (11,598 | ) | ||

| Interest Receivable | (13,391 | ) | ||

| Credit Card Obligations | 173,157 | |||

| Accrued Liabilities | 56,275 | |||

| Accounts Payable | 87,798 | |||

| Net Cash Used in Operating Activities | (2,643,047 | ) | ||

| CASH FLOWS FROM INVESTING ACTIVITIES | ||||

| Purchases of Furniture and Equipment | (7,512 | ) | ||

| Purchases of Real Estate Properties and In-place Lease Intangible Assets | (479,078 | ) | ||

| Proceeds from Sale of Real Estate Property | 17,500 | |||

| Net Cash Used in Investing Activities | (469,090 | ) | ||

| CASH FLOWS FROM FINANCING ACTIVITIES | ||||

| Issuance of Series A Preferred Shares | 6,601,630 | |||

| Contributions from Common Stockholder | 344,000 | |||

| Distributions to Common Stockholder | (122,000 | ) | ||

| Offering Costs | (1,285,954 | ) | ||

| Distributions to Preferred Stockholders | (132,956 | ) | ||

| Net Cash Provided by Financing Activities | 5,404,720 | |||

| Net Increase in Cash and Cash Equivalents | 2,292,583 | |||

| Cash and Cash Equivalents, at Inception (February 22, 2022) | - | |||

| CASH AND CASH EQUIVALENTS, AT December 31, 2022 | $ | 2,292,583 | ||

See accompanying notes to the financial statements

19

CWS Investments Inc.

Statement of Changes in Stockholders’ Deficit

From Inception (February 22, 2022) to December 31, 2022

| Preferred Stock | Common Stock | Additional Paid-in Capital | Accumulated Deficit | Total Stockholders’ Deficit | ||||||||||||||||

| Balance at Inception (February 22, 2022) | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||||

| Issuance of Common Stock | - | - | 344,000 | - | 344,000 | |||||||||||||||

| Issuance of Series A Preferred Shares | 6,601,630 | - | - | - | 6,601,630 | |||||||||||||||

| Reclassification of Preferred Stock at Redemption Value | (6,601,630 | ) | - | - | (6,601,630 | ) | ||||||||||||||

| Offering Costs | - | - | (89,044 | ) | (1,196,910 | ) | (1,285,954 | ) | ||||||||||||

| Distributions to Preferred Stockholders | - | - | (132,956 | ) | (132,956 | ) | ||||||||||||||

| Distributions to Common Stockholder | - | - | (122,000 | ) | - | (122,000 | ) | |||||||||||||

| Net Loss | - | - | - | (882,621 | ) | (882,621 | ) | |||||||||||||

| Balance at December 31, 2022 | $ | - | $ | - | $ | - | $ | (2,079,531 | ) | $ | (2,079,531 | ) | ||||||||

See accompanying notes to the financial statements

20

CWS Investments Inc.

Notes to the Financial Statements

1. ORGANIZATION AND BUSINESS

Nature of Operations and Offering of Securities

CWS Investments Inc. (the “Company”) is a Virginia based corporation formed on February 22, 2022. The Company acquires and manages real estate backed loans, as well as other real estate related assets, to include single family homes and smaller, multi-family residential properties. The Company purchases performing and non-performing (distressed) promissory notes, lines of credit, and land installment contracts secured by real property at a significant discount to their unpaid principal balances and to their current and future market values. The Company typically only invests in first mortgages but may opportunistically invest in second mortgages and lease options.

The Company is offering $75,000,000 in Series A Redeemable Preferred Stock (“Class A Share”) at an offering price of $10 per share (the “Offering”). The Offering is being conducted pursuant to Regulation A of Section 3(6) of the Securities Act of 1933, as amended, for Tier 2 offerings. The Offering will terminate on the earlier of 12 months from the date the offering circular was qualified by the Securities and Exchange Commission (“SEC”) (which date may be extended for an additional two years in the Company’s sole discretion) or the date when all Class A Shares have been sold. The Offering Circular was qualified by the SEC on July 13, 2022 and will terminate on or before July 13, 2023.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The Company’s financial statements are prepared in accordance with accounting principles generally accepted in the United States (U.S. GAAP). The Company adopted the calendar year as its basis of reporting.

Use of Estimates

The preparation of the Company’s financial statements in conformity with U.S. GAAP requires the Company to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Significant estimates and assumptions are required in the determination of revenue recognition; valuation of accounts receivable; impairment of loans; income taxes; and contingencies and litigation, among others. Some of these judgments can be subjective and complex, and consequently, actual results may differ from these estimates. For any given individual estimate or assumption made by the Company, there may also be other estimates or assumptions that are reasonable.

21

The Company regularly evaluates its estimates and assumptions using historical experience and other factors, including the economic environment. As future events and their effects cannot be determined with precision, the Company’s estimates and assumptions may prove to be incomplete or inaccurate, or unanticipated events and circumstances may occur that might cause changes to those estimates and assumptions. Market conditions, such as illiquid credit markets, health crises such as the COVID-19 global pandemic, volatile equity markets, and economic downturns, can increase the uncertainty already inherent in the Company’s estimates and assumptions. The Company adjusts its estimates and assumptions when facts and circumstances indicate the need for change. Those changes generally will be reflected in our financial statements on a prospective basis unless they are required to be treated retrospectively under the relevant accounting standard. It is possible that other professionals, applying reasonable judgment to the same facts and circumstances, could develop and support a range of alternative estimated amounts.

Risks and Uncertainties

Industry Risk

Real estate is notoriously speculative and unpredictable. Most or all the assets purchased by the Company are backed by real estate. If the real estate market declines, the Company might not be able to pay dividends or even redeem outstanding Class A Preferred Stock at its stated redemption price. The real estate industry has seen numerous ebbs and flows over the past two decades, to include the notorious downturn in 2007-2009. These events impact the ability of the Company to generate revenue and in turn, distribute dividends and proceeds.

Risks Relating to Real Estate Loans

The ultimate performance and value of the Company’s investments will depend upon, in large part, the underlying borrower on the mortgage’s ability to perform and the Company’s ability to operate any given property so that it produces sufficient cash flows necessary to generate profits. Revenues and cash flows may be adversely affected by: changes in national or local economic conditions; changes in local real estate market conditions due to changes in national or local economic conditions or changes in local property market characteristics, including, but not limited to, changes in the supply of and demand for competing properties within a particular local property market; competition from other properties offering the same or similar services; changes in interest rates and the credit markets which may affect the ability to finance, and the value of, investments; the on-going need for capital improvements, particularly in older building structures; changes in real estate tax rates and other operating expenses; changes in governmental rules and fiscal policies, civil unrest, acts of God, including earthquakes, hurricanes, and other natural disasters, acts of war, or terrorism, which may decrease the availability of or increase the cost of insurance or result in uninsured losses; changes in governmental rules and fiscal policies which may result in adverse tax consequences, unforeseen increases in operating expenses generally or increases in the cost of borrowing; decreases in consumer confidence; government taking investments by eminent domain; various uninsured or uninsurable risks; the bankruptcy or liquidation of Borrowers or tenants; adverse changes in zoning laws; the impact of present or future environmental legislation and compliance with environmental laws.

22

Redeemable Shares

All of the Series A Preferred Shares sold in the Offering contain a redemption feature which allows for the redemption of such shares after a four year holding period (“Lock-up Period”) at the election of the holder. In accordance with ASC 480, conditionally redeemable Class A Preferred Shares (including Class A Preferred Shares that feature redemption rights that are either within the control of the holder or subject to redemption upon the occurrence of uncertain events not solely within the Company’s control) are classified as temporary equity. Ordinary liquidation events, which involve the redemption and liquidation of all of the entity’s equity instruments, are excluded from the provisions of ASC 480. The Company recognizes changes in redemption value immediately as they occur. However, while Series A Preferred Shares that are redeemed prior to the Lock-up Period are subject to a penalty or discount to the redemption value, such Series A Preferred Shares have been presented at the original sales price of $10 per share. Further, Bonus Preferred Shares received by qualifying early investors have no redemption value until after the Lock-up Period and, as such, 34,979 of redeemable Bonus Shares are stated at $0 redemption value on the Balance Sheet and will be immediately accreted to their $10 per share redemption value following completion of the Lock-up Period. Accordingly, 695,142 Series A Preferred Shares subject to possible redemption at the redemption amount were presented at redemption value as temporary equity, outside of the shareholders’ deficit section of the Company’s balance sheet as of December 31, 2022.

Organizational Costs

In accordance with Financial Accounting Standards Board (“FASB”) Accounting Standards Codification ASC 720, organizational costs, including accounting fees, legal fees, and costs of incorporation, are expensed as incurred.

Interest Receivable

The amount of mortgage loan interest recognized, but not collected, is included in Interest Receivable in the Balance Sheet. The amount of interest income recognized, but not collected, is $13,391 as of December 31, 2022.

The Company analyzes interest receivable balances on a timely basis, or at least monthly, to determine collectability. If an interest receivable amount is deemed uncollectible, then the Company writes off that uncollectible amount of the interest receivable through a reversal of interest income. The Company did not write off any interest income during 2022.

Other Receivable

The Company incurs and pays loan expenses considered to be recoverable from borrowers. Expenses include, but are not limited to; forced placed insurance, property taxes, legal, and utility bills. Proper documentation is provided to the loan servicer and subsequently, the recoverable expense is added to the loan balance. The recoverable expense may be collected directly from the borrower, may reduce proceeds in the event of foreclosure, or may reduce/increase the gain/loss upon sale of the loan. The amount of recoverable expenses outstanding at December 31, 2022 is $16,160 and is included in Other Receivables in the Balance Sheet.

23

Cash and Cash Equivalents

The Company considers all highly liquid investments with an original maturity date of three months or less at the date of purchase to be cash equivalents. There were no such investments as of December 31, 2022. As of December 31, 2022, the cash balance of $2,292,583 was deposited with well-known and stable financial institutions.

The Company’s cash balances in bank deposit accounts, at times, may exceed federally insured limits. The Company is subject to credit risk to the extent any financial institution with which it conducts business is unable to fulfill contractual obligations on its behalf. Management monitors the financial condition of such financial institutions and does not anticipate any losses from these counterparties.

In-Place Lease Intangible Assets

In-place lease intangible assets result when a lease is assumed as part of a real estate acquisition. The fair value of in-place leases consists of the following components, as applicable (1) the estimated cost to replace the leases (including loss of rent, estimated commissions and legal fees paid in similar leases), and (2) the above or below market cash flow of the leases, determined by comparing the projected cash flows of the leases in place at the time of acquisition to projected cash flows of comparable market-rate leases. The In-place Lease Intangible Assets, as shown in the Balance Sheet, represent lease contracts Management considered to be above market value at the time of assumption. In-place Lease Intangible Assets are amortized on a straight-line basis as increases to rental income over the remaining term of the leases. Should a tenant terminate a lease, the unamortized portion of the lease intangible is recognized immediately as an expense.

Accrued Liabilities

The Company recognized Accrued Liabilities of $56,275 in the Balance Sheet as of December 31, 2022. Accrued Liabilities include payroll liabilities of $50,592 and legal costs incurred of $5,683.

Income Taxes

The Company uses the asset and liability method of ASC 740 to account for income taxes. Under this method, deferred income taxes are determined based on the differences between the tax basis of assets and liabilities and their reported amounts in the financial statements which will result in taxable or deductible amounts in future years and are measured using the currently enacted tax rates and laws. A valuation allowance is provided to reduce net deferred tax assets to the amount that, based on available evidence, is more likely than not to be realized.

The recognition of certain net deferred tax assets of our reporting entities are dependent upon, but not limited to, the future profitability of the reporting entity, when the underlying temporary differences will reverse, and tax planning strategies. Further, Management’s judgment regarding the use of estimates and projections is required in assessing the Company’s ability to realize the deferred tax assets relating to NOL carryforwards.

24

For the year ended December 31, 2022, 100% of the distributions received by both the common and preferred stockholders were classified as return of capital for income tax purposes.

ASC Topic 740 clarifies the accounting for uncertainty in income taxes recognized in an enterprise’s financial statements. It requires a recognition threshold and measurement attribute for financial statement disclosure of tax positions taken, or expected to be taken, in an income tax return. This interpretation also provides guidance on derecognition, classification, interest and penalties, accounting in interim periods, disclosure, and transition. Management has considered all positions expected to be taken on the 2022 tax returns, and concluded that tax positions taken will more likely than not be sustained at the full amount upon examination. Accordingly, the Company has concluded that there are no significant uncertain tax positions requiring recognition in its financial statements. The Company expects no significant increases or decreases in unrecognized tax benefits due to changes in tax positions within one year of December 31, 2022. If any income tax exposure was identified, the Company would recognize an estimated liability for income tax items that meet the criteria for accrual.

The Company has not been assessed interest or penalties by any major tax jurisdictions. If any interest and penalties related to income tax assessments arose, the Company would record them as income tax expense.

Revenue Recognition

For performing mortgage loans in accrual status, interest income includes interest at stated rates based on the contractual payment terms of the loan. If a loan is prepaid, the Company immediately recognizes the amount of interest calculated in the payoff statement as an increase to interest income. The Company recognized $34,926 of interest income related to accrual loans during 2022 which is included in Mortgage Loans: Interest Income in the Statement of Operations.

For non-performing loans in non-accrual status, interest income recognition is suspended until, in the opinion of management, a full recovery of the contractual principal and interest is expected. When a loan is in non-accrual status, all payments received are applied to principal. If a loan in non-accrual status is prepaid, the Company immediately recognizes the increase or decrease in the proceeds received versus the carrying value of the loan as a gain (loss) in other income. The Company did not recognize any income related to loans in non-accrual status during 2022.

The Company recognized $17,442 of Other Revenue in the Statement of Operations which included $14,942 of cash rewards on its business credit cards and $2,500 of earnest money forfeited during the sales process of real estate property.

Rental income is recognized according to the guidance in ASU 2016-02, Leases (Topic 842) on a straight-line basis over the term of the lease. The Company did not recognize any rental income in 2022 due to the short duration (one week) of the lease period being applicable to the time period covered by the financial statements.

25

Credit Card Obligations

The Company utilizes business credit card accounts to finance marketing, advertising, and other general and administrative expenses. Credit card financing provides additional liquidity for the Company as well as cash back rewards on purchases. The Company did not incur any interest expense during 2022 related to credit card financing. The Company’s credit card obligations of $173,157 is shown in Credit Card Obligations in the Balance Sheet as of December 31, 2022.

Accrued Liabilities

The Company recognized Accrued Liabilities of $56,275 in the Balance Sheet as of December 31, 2022. Accrued Liabilities include payroll liabilities of $50,592 and legal costs incurred of $5,683.

Offering Costs

Offering costs consist of specific incremental costs, including legal, underwriting, marketing, and other costs directly attributable to an offering the Company commenced during July 2022 under Regulation A+. Offering Costs of $1,285,954 were charged to equity during 2022.

Advertising and Marketing Costs

The Company expenses advertising and marketing costs as incurred. Total Advertising and Marketing Costs incurred during 2022 are $54,363 and are included in Advertising and Marketing in the Statement of Operations.

Furniture and Equipment

Property and equipment are stated at cost less accumulated depreciation. Depreciation is recorded over the estimated useful life of the assets principally by the straight-line method. Expenditures for major additions and improvements are capitalized, while minor replacements, maintenance, and repairs are charged to expense as incurred.

Depreciation is recorded over the estimated useful lives of the assets involved using the straight-line method. As of December 31, 2022, the Company’s Furniture and Equipment, Net in the Balance Sheet consists of the following:

| Asset | Estimated Useful Life | Cost | Carrying Value | |||||||

| Computer Equipment | 5 years | 7,512 | 6,302 | |||||||

26

Residential Mortgage Loans

Loan Classification

Loans are considered performing loans when Management expects to receive all of the contractually specified principal and interest payments. Loans are considered non-performing when Management does not expect to receive all of the contractually specified principal and interest payments. The Company works with borrowers of non-performing loans in an effort to convert the loan to performing, and then liquidate the loan at a higher margin. If a borrower cannot make payments on a loan, the Company has multiple options including loan modification, deed-in-lieu of foreclosure, or foreclosing on the property. The Company invests heavily in non-performing mortgage loans with the intention of liquidating the loan after converting the loan to performing, loan modification, or through foreclosure. The Company’s business model is to buy then sell or foreclose on its loans after a short holding period and, therefore, classifies its loans as held-for-sale. The Company accounts for all of its loans under ASC 948 Financial Services – Mortgage Banking. Loans are recorded at the lower of cost or market upon acquisition and subsequently at each reporting date. Loan acquisition costs are deferred and included as part of the carrying balance of the loan until the loan is sold.

Loan Servicing

The Company contracts with various loan servicing companies to service the Company’s mortgage loans. The loan servicing companies are entitled to a monthly servicing fee for each loan as well as other fees that are standard in the loan servicing business. The Company incurred $10,631 of loan servicing fees in 2022 and is included in Mortgage Loan Expenses in the Statement of Operations.

Loan Impairment

Loans considered held-for-sale are evaluated for impairment by Management at each reporting date. A valuation allowance is recorded to the extent that the fair value of the loan is less than the amortized cost basis. No valuation allowance was recorded as of December 31, 2022.

From time to time, Management negotiates and enters into loan modifications with borrowers whose loans are delinquent (non-performing). Modifications may include lowering monthly payments, deferring some principal balances to maturity, modifying the maturity date, and/or reclassifying loan charges. The Company recognizes the effects of any loan modifications in the financial statements immediately. The Company did not have any loan modifications in 2022 and, therefore had no effect on the financial statements. The Company did not forgive, partially or in full, any portion of loan principal balances in 2022.

27

Real Estate Property

Real Estate Owned

Real estate owned (“REO”) is property acquired in full or partial settlement of loan obligations generally through foreclosure and is recorded at acquisition at the property’s fair value less estimated costs to sell. The fair value estimates are derived from information available in the real estate markets including similar property, and often require the experience and judgment of third parties such as real estate appraisers and brokers. The estimates figure materially in calculating the value of the property at acquisition, the level of charge to the allowance for loan losses and any subsequent valuation reserves. After acquisition, costs incurred relating to the development and improvement of property are capitalized to the extent they do not cause the recorded value to exceed the net realizable value, whereas costs relating to holding and disposition of the property are expensed as incurred. REO is analyzed periodically for changes in fair values and any subsequent write down is charged as an expense on the statements of income. Any recovery in the fair value subsequent to such a write down is recorded, not to exceed the value recorded at acquisition. The Company did not have REO property as of December 31, 2022 but considers REO property to be a vital part of the business going forward. As of December 31, 2022, foreclosure procedures had been initiated on 7 mortgage loans with an aggregate carrying value of $47,873.

Real Estate Purchase Price Allocations

Upon the acquisition of real estate properties which do not constitute the definition of a business, the Company recognizes the assets acquired, the liabilities assumed, and any noncontrolling interest as of the acquisition date, measured at their relative fair values. Acquisition-related costs are capitalized in the period incurred and are recorded to the components of the real estate assets acquired. In determining fair values for multifamily apartment acquisitions, the Company assesses the acquisition-date fair values of all tangible assets, identifiable intangible assets and assumed liabilities using methods like those used by independent appraisers (e.g., discounted cash flow analysis) and which utilize appropriate discount and/or capitalization rates and available market information. In determining fair values for single-family residential home acquisitions, the Company utilizes information obtained from county tax assessment records and available market information to assist in the determination of the fair value of land and buildings. Estimates of future cash flows are based on several factors including historical operating results, known and anticipated trends, and market and economic conditions. The fair value of tangible assets of an acquired property considers the value of the property as if it was vacant.

Intangible assets include the value of in-place leases, which represents the estimated fair value of the net cash flows of leases in place at the time of acquisition, as compared to the net cash flows that would have occurred had the property been vacant at the time of acquisition and subject to lease-up. The Company amortizes the value of in-place leases to expense over the remaining non-cancelable term of the respective leases.

Estimates of the fair values of the tangible assets, identifiable intangibles and assumed liabilities require the Company to make significant assumptions to estimate market lease rates, property operating expenses, carrying costs during lease-up periods, discount rates, market absorption periods, prevailing interest rates and the number of years the property will be held for investment. The use of inappropriate assumptions could result in an incorrect valuation of acquired tangible assets, identifiable intangible assets and assumed liabilities, which could impact the amount of the Company’s net income (loss). Differences in the amount attributed to the fair value estimate of the various assets acquired can be significant based upon the assumptions made in calculating these estimates.

28

Impairment of Real Estate Property

The Company continually monitors events and changes in circumstances that could indicate that the carrying amounts of the Company’s real estate and related intangible assets may not be recoverable. When indicators of potential impairment suggest that the carrying value of real estate and related intangible assets may not be recoverable, the Company assesses the recoverability of the assets by estimating whether the Company will recover the carrying value of the asset through its undiscounted future cash flows and its eventual disposition. Based on this analysis, if the Company does not believe that it will be able to recover the carrying value of the real estate and related intangible assets and liabilities, the Company will record an impairment loss to the extent that the carrying value exceeds the estimated fair value of the real estate and related intangible assets. No impairment charges were recorded in 2022.

Lessor