UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANY

Investment Company Act file number 811-21528

Cypress Creek Private Strategies Registered Fund, L.P.

(Exact name of registrant as specified in charter)

712 W. 34th Street, Suite 201, Austin, TX 78705

(Address of principal executive offices) (Zip code)

| With a copy to: | ||

| William Prather III | George J. Zornada | |

| Cypress Creek Private Strategies Registered Fund, L.P. | K & L Gates LLP | |

| 712 W. 34th Street, Suite 201 | 1 Congress Street, Suite 2900 | |

| Austin, TX 78705 | Boston, MA 02114 | |

| (Name and address of agent for service) | (617) 261-3231 |

Registrant’s telephone number, including area code: (512) 660-5146

Date of fiscal year end: 3/31/25

Date of reporting period: 3/31/25

Item 1. Reports to Stockholders.

(a)

TABLE OF CONTENTS

|

Cypress Creek Private Strategies Registered Fund, L.P. |

||

|

1 |

||

|

12 |

||

|

13 |

||

|

14 |

||

|

15 |

||

|

16 |

||

|

17 |

||

|

27 |

||

|

33 |

|

Cypress Creek Private Strategies Master Fund, L.P. |

||

|

37 |

||

|

48 |

||

|

49 |

||

|

50 |

||

|

57 |

||

|

58 |

||

|

59 |

||

|

60 |

||

|

78 |

||

|

84 |

Management Discussion of Fund Performance (Unaudited)

Economic and Market Conditions

The year began with a broadly constructive economic outlook: global growth was expected to remain stable, and inflation, while elevated, was on a downward path. This narrative shifted sharply following the U.S. “Liberation Day” announcement on April 2nd, which introduced sweeping global tariffs. The immediate and pronounced reaction across global equity, U.S. Treasury, and global currency markets highlighted the potential disruption to global trade and economic stability. While many of the proposed tariffs are currently paused pending trade negotiations, their scope and timing have introduced significant uncertainty into the economic outlook for the year and beyond. As the U.S. works to redefine key trade relationships, the risk of policy missteps remains elevated. “Liberation Day” tariffs, functioning effectively as a consumption tax on U.S. households, have significant implications for both domestic demand the broader global economic landscape, given the degree of integration in supply chains and financial markets. Despite these macroeconomic headwinds, Cypress Creek Partners remains confident in the resilience of the Fund’s investment strategy. Our focus on creating a diversified and all-weather portfolio across private equity and private real assets is designed to perform through shifting economic regimes. We continue to believe our disciplined, long-term approach positions the Fund to deliver consistent, strong returns amid uncertainty and structural change.1

As it relates to Cypress Creek Partners’ private markets strategy, the Fund’s focus on targeting smaller and less established managers continues to benefit from persistent and acute capital scarcity within this segment. The challenges facing emerging managers extended throughout 2024 and into 2025. According to PitchBook, first-time private equity funds raised an estimated $92 billion in 2024, representing a decline of 20% from 2023 and 40% below the peak in 2017. Moreover, an unprecedented 87% of total private equity fundraising in 2024 was concentrated among experienced sponsors (i.e., firms with four or more prior funds), which is well above the ten-year historical average of 76%. The Fund’s strategy specifically targets those managers most affected by this trend, or those that have raised three or fewer funds, who typically target assets in the highly fragmented lower middle market. Fundraising among these less established firms declined by 41% in 2024, underscoring the continued capital scarcity we have previously highlighted to investors. This trend was even more pronounced within private real assets (excluding real estate), where fundraising activity was particularly weak, with only $9Bn raised during 2024, representing a 79% year-over-year decline. This pronounced capital dislocation, especially within a core pillar of the Fund’s strategy, presents a compelling opportunity. Cypress Creek is well-positioned to deploy capital alongside less established managers operating in sectors marked by fragmentation and undercapitalization, conditions that are historically conducive to value creation through both asset consolidation and operational transformation. The Fund’s differentiated approach to private real assets complements its traditional private equity exposure by offering distinct and less correlated performance. As a result, Cypress Creek remains excited about the Fund’s current opportunity set in private markets and is well-positioned to play offense during this period of constrained capital availability.2

Fund Portfolio Transition

During fiscal year 2025 ended March 31, 2025, Cypress Creek made three new Private Investment (“PI”) portfolio commitments (two in Private Equity and one in Real Assets). Since taking over management of the Fund in 2021, we have made significant progress in repositioning the PI portfolio to align with Cypress Creek’s unique approach alongside less established managers and operators. As of March 31, 2025, 62% of the Fund’s PI NAV and 74% of the Fund’s PI total exposure (NAV plus unfunded commitments) is alongside Cypress Creek Core Managers, up from 47% and 56%, respectively year-over-year. The Core Managers in the PI portfolio, which is the focus of Cypress Creek’s investment strategy, have made a meaningful contribution to the Fund’s overall performance, generating a 19.5%/17.9% (gross/net) annualized return, since March 1, 2021, and for the twelve-month period ending March 31, 2025, 12.6%/11.0% (gross/net) return.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees, service fees, and other expenses by determining the percentage change in net asset value. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only.

1

Fund Performance

For the twelve-month period ending March 31, 2025, Cypress Creek Private Strategies Master Fund, L.P. (the “Fund”), returned 7.6% net of fees and expenses, outperforming the 7.2% return of its public equity based primary benchmark, the MSCI All Country World Total Return Index (the “MSCI ACWI”). The Private Investment (“PI”) portfolio, the focus of the Cypress Creek investment strategy, comprised of Private Equity and Private Real Assets, returned 10.1%/8.4% (gross/net) for the trailing twelve-months ending March 31, 2025, with the Core Managers returning 12.6%/11.0% (gross/net) and the non-core returning 6.1%/4.5% (gross/net). The PI portfolio allocation represents approximately 87% of the Master Fund’s net assets with Core Managers representing 54.1% of the portfolio.

Private Equity

The Private Equity sub-portfolio delivered a 9.6%/7.9% (gross/net) return for the trailing twelve-month period ending March 31, 2025, with the Core Managers returning 9.0%/7.3% (gross/net) and the non-core returning 9.7%/8.1% (gross/net). Private Equity represents 72.1% of the Fund’s total PI portfolio (54% Core Managers), which is overweight relative to a long-term target of 60%. Over the last twelve months, Buyout investments generated a 6.0%/4.3% (gross/net) return, Venture Capital investments generated a 25.1%/23.4% (gross/net) return, Growth Equity investments generated a 20.6%/18.9% (gross/net) return and Debt & Other Categories generated a (5.7%)/(7.4%) (gross/net) return. Within Growth Equity, an investment alongside a first-time fund manager focused on U.S. enterprise software and technology-enabled services business as well as an associated ownership stake in the manager’s business (i.e., GP stake) was the standout performer among the underlying contributors. The long-term portfolio construction excludes Venture Capital, which remains an overweight position in the portfolio due to legacy commitments made as part of the pre-Cypress Creek management of the portfolio.

Private Real Assets

The Private Real Assets sub-portfolio delivered an 11.4%/9.8% (gross/net) return for the trailing twelve-month period ending March 31, 2025, with the Core Managers returning 18.6%/16.9% (gross/net) and the non-core returning (14.3%)/(16.0%) (gross/net). The Private Real Assets allocation represents 27.9% of the Fund’s total PI portfolio (83.5% Core Managers), which is underweight relative to a long-term target of 40%. Infrastructure and Natural Resources, which represent the two go-forward Cypress Creek strategies within this portfolio, contributed positively to overall sub-portfolio returns during the fiscal year. Infrastructure returned 13.0%/11.3% (gross/net) and Natural Resources returned 18.2%/16.5% (gross/net) over the period, while Real Estate, which will not be a part of the go-forward Cypress Creek Private Real Assets strategy, returned (27.1%)/(28.8%) (gross/net). Both Infrastructure and Natural Resources are expected to increase as a percentage of the total Private Real Assets sub-portfolio as legacy commitments to real estate liquidate. Core Managers in the niche infrastructure sector — namely an investment alongside a first-time fund manager focused on the aggregation and professionalization of U.S. boat marinas as well as an associated GP stake in the manager’s business were the strongest performers within the Private Real Assets sub-portfolio, contributing positively to the overall Fund return.

Cash Management

The Fund’s Cash Management (“CM”) portfolio, comprised of cash, hedge funds, and liquid securities, returned 4.8%/3.1% (gross/net) for the trailing twelve-month period ending March 31, 2025, with the Core holdings returning 3.3%/1.6% (gross/net) and non-core holdings returning 23.4/21.7% (gross/net). The CM portfolio allocation represents 17.2% of the Master Fund’s total net assets (95% Core holdings). As discussed at the outset of fiscal year 2025, Cypress Creek made the strategic decision to actively reposition the CM portfolio by redeeming from all historical Core Managers and transition the Fund’s liquidity portfolio to short-term fixed income via a U.S. government money

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees, service fees, and other expenses by determining the percentage change in net asset value. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only.

2

market fund. As a reminder, this decision was made to concentrate the Fund’s active risk solely within the PI portfolio and reduce the Fund’s overall portfolio complexity. Full redemption proceeds from all four historical Core Managers have now been received as of March 31, 2025, and Cypress Creek is pleased to report the successful transition of the CM to investors. As of March 31, 2025, the CM portfolio was comprised of 95% short-term fixed income holdings and 5.0% liquidating non-core holdings. Despite the clear success and strong performance of the Core Managers in the CM Portfolio, Cypress Creek believes that its decision to reposition the CM portfolio better serves the Fund by maintaining a level of risk and volatility that is representative of a stable value mandate, as the primary role of the CM portfolio is to serve as a liquidity provider for Cypress Creek’s core PI strategy.

Conclusion

We continue to have strong convictions around the execution of our strategy in the global private investment market. Through the execution of this strategy, we seek to source from the market bespoke opportunities alongside less established managers and operating teams with highly specialized experience and investment strategies that we believe have the potential to deliver strong cross-cycle, risk-adjusted returns.3

We remain grateful for your support and are firmly committed to achieving the Master Fund’s objective, which is to preserve capital and to generate consistent long-term appreciation and returns across a market cycle (which is estimated to be five to seven years).

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees, service fees, and other expenses by determining the percentage change in net asset value. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only.

3

Performance (net)

Fund Performance Details

Portfolio Manager: William P. Prather III

|

% Average Annual Total Returns |

Inception Date |

1-year |

5-year |

10-year |

||||

|

Cypress Creek Private Strategies Registered Fund, L.P. |

4/1/2004 |

6.6% |

6.3% |

3.3% |

||||

|

MSCI All World Country Index |

7.2% |

15.2% |

8.8% |

|

CCPS Registered Fund (Net) |

||||||||||||||

|

Returns - TWR |

1-year |

3-year |

5-year |

SI CCP |

||||||||||

|

Portfolio |

6.6 |

% |

3.1 |

% |

6.3 |

% |

4.1 |

% |

||||||

|

Core |

7.8 |

% |

7.2 |

% |

7.0 |

% |

8.2 |

% |

||||||

|

Non-Core |

4.1 |

% |

-1.5 |

% |

3.4 |

% |

0.3 |

% |

||||||

|

|

|

|

|

|||||||||||

|

Private Investments |

7.5 |

% |

3.9 |

% |

8.2 |

% |

5.3 |

% |

||||||

|

Core |

10.0 |

% |

10.7 |

% |

12.8 |

% |

16.8 |

% |

||||||

|

Non-Core |

3.5 |

% |

-1.3 |

% |

4.7 |

% |

1.2 |

% |

||||||

|

|

|

|

|

|||||||||||

|

Private Equity |

6.9 |

% |

3.3 |

% |

9.5 |

% |

4.4 |

% |

||||||

|

Core |

6.3 |

% |

10.9 |

% |

15.5 |

% |

19.1 |

% |

||||||

|

Non-Core |

7.1 |

% |

-0.1 |

% |

7.1 |

% |

1.9 |

% |

||||||

|

|

|

|

|

|||||||||||

|

Buyout |

3.3 |

% |

9.7 |

% |

15.7 |

% |

17.8 |

% |

||||||

|

Growth |

17.9 |

% |

1.1 |

% |

5.4 |

% |

-3.6 |

% |

||||||

|

Venture Capital |

22.5 |

% |

-1.0 |

% |

9.6 |

% |

-0.2 |

% |

||||||

|

Debt & Other |

-8.4 |

% |

-3.3 |

% |

0.2 |

% |

-0.8 |

% |

||||||

|

|

|

|

|

|||||||||||

|

Real Assets |

8.8 |

% |

5.1 |

% |

3.3 |

% |

6.7 |

% |

||||||

|

Core |

15.9 |

% |

10.3 |

% |

8.6 |

% |

8.5 |

% |

||||||

|

Non-Core |

-17.0 |

% |

-9.2 |

% |

-5.0 |

% |

-4.0 |

% |

||||||

|

|

|

|

|

|||||||||||

|

Natural Resources |

15.5 |

% |

6.1 |

% |

5.3 |

% |

9.9 |

% |

||||||

|

Infrastructure |

10.4 |

% |

10.6 |

% |

4.2 |

% |

6.7 |

% |

||||||

|

Real Estate |

-29.8 |

% |

-18.4 |

% |

-11.6 |

% |

-12.1 |

% |

||||||

|

|

|

|

|

|||||||||||

|

Cash Management |

2.2 |

% |

-0.2 |

% |

0.0 |

% |

-0.7 |

% |

||||||

|

Core |

0.6 |

% |

0.4 |

% |

2.1 |

% |

2.0 |

% |

||||||

|

Non-Core |

20.8 |

% |

-2.7 |

% |

-4.8 |

% |

-6.3 |

% |

||||||

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees, service fees, and other expenses by determining the percentage change in net asset value. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only.

4

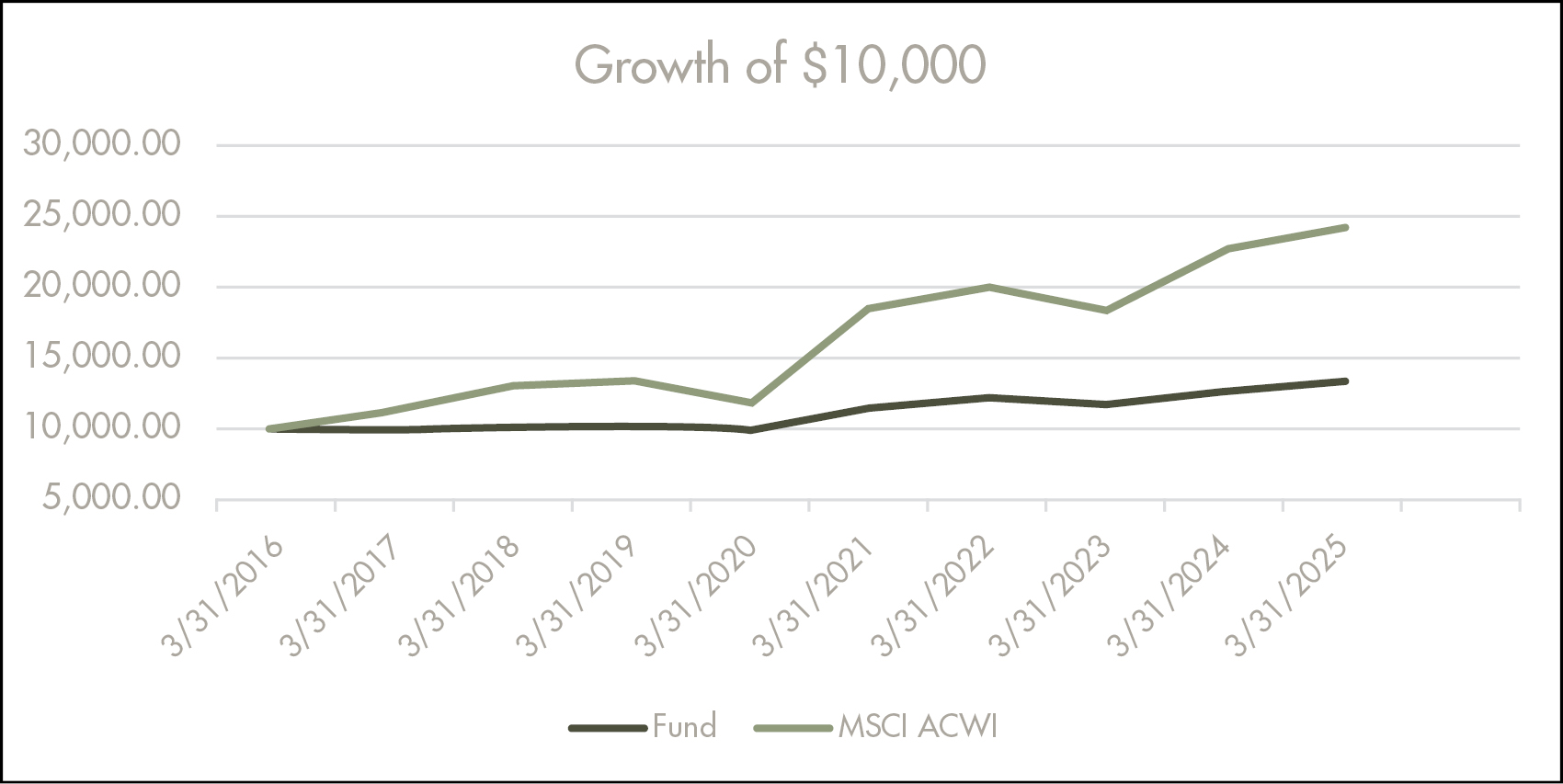

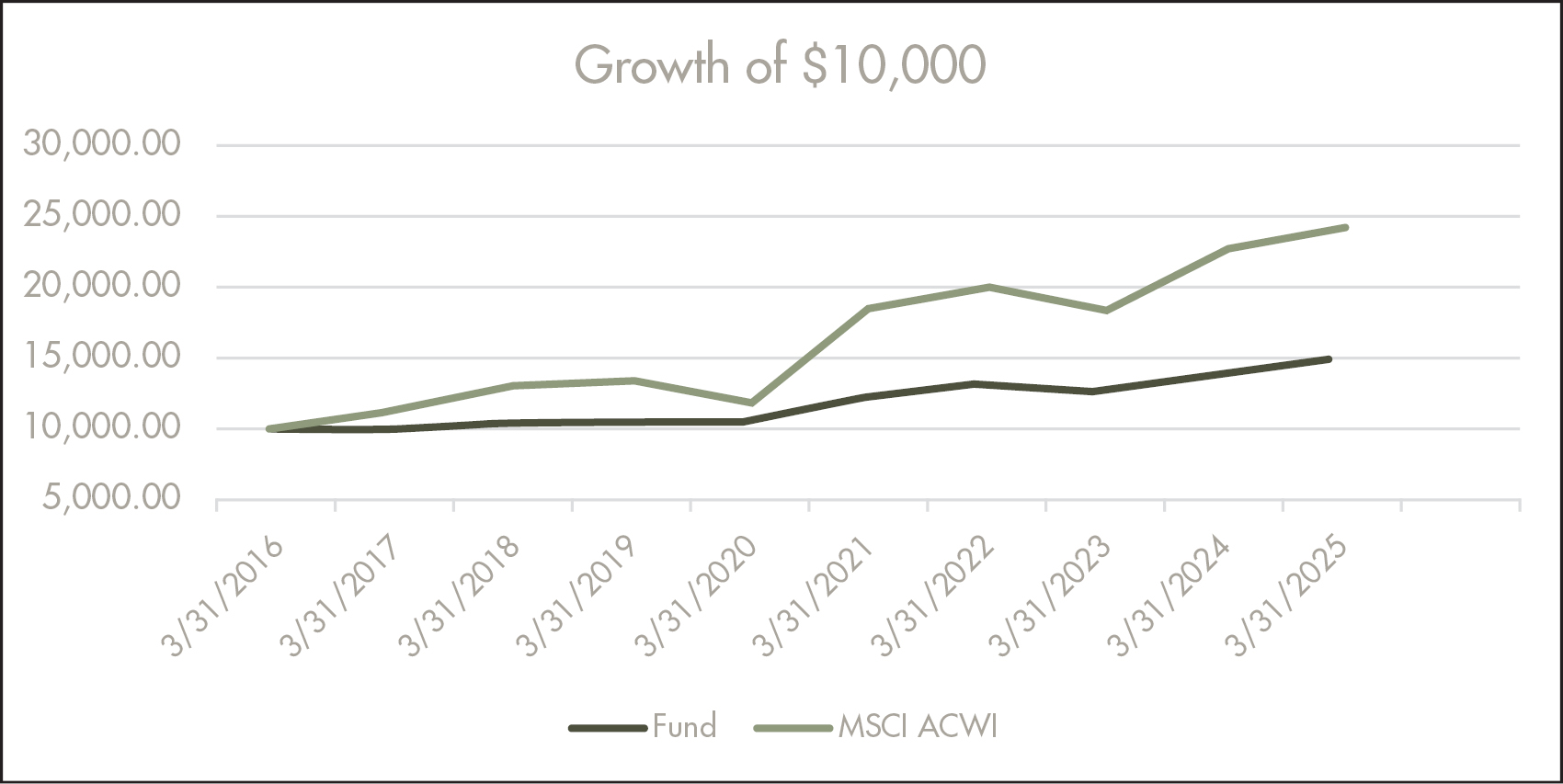

Growth of $10,000

This graph shows the change in value of a hypothetical investment of $10,000 in the Registered Fund for the period indicated. For comparison, the graph also includes the change in value of the same hypothetical investment in the MSCI ACWI.

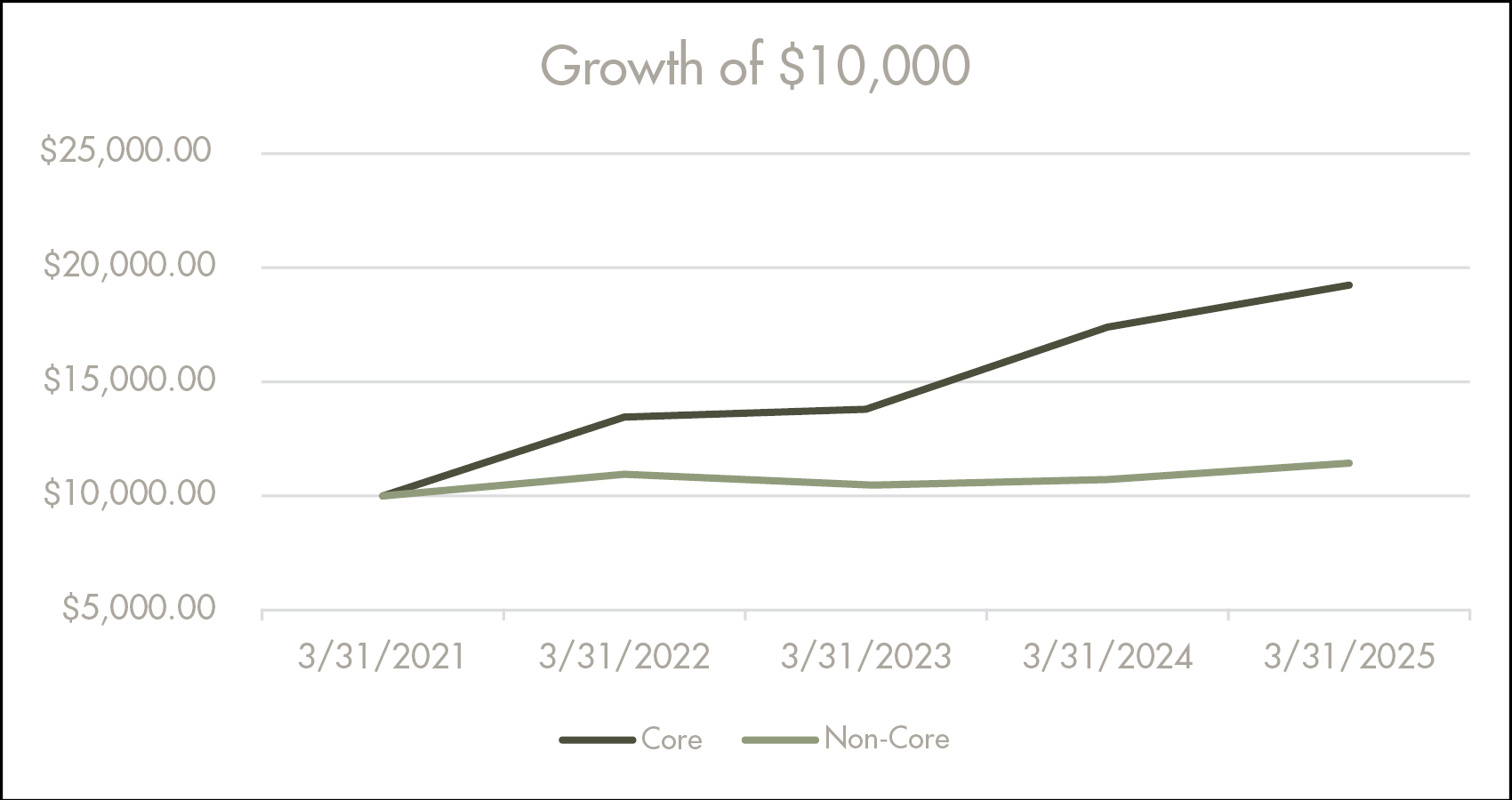

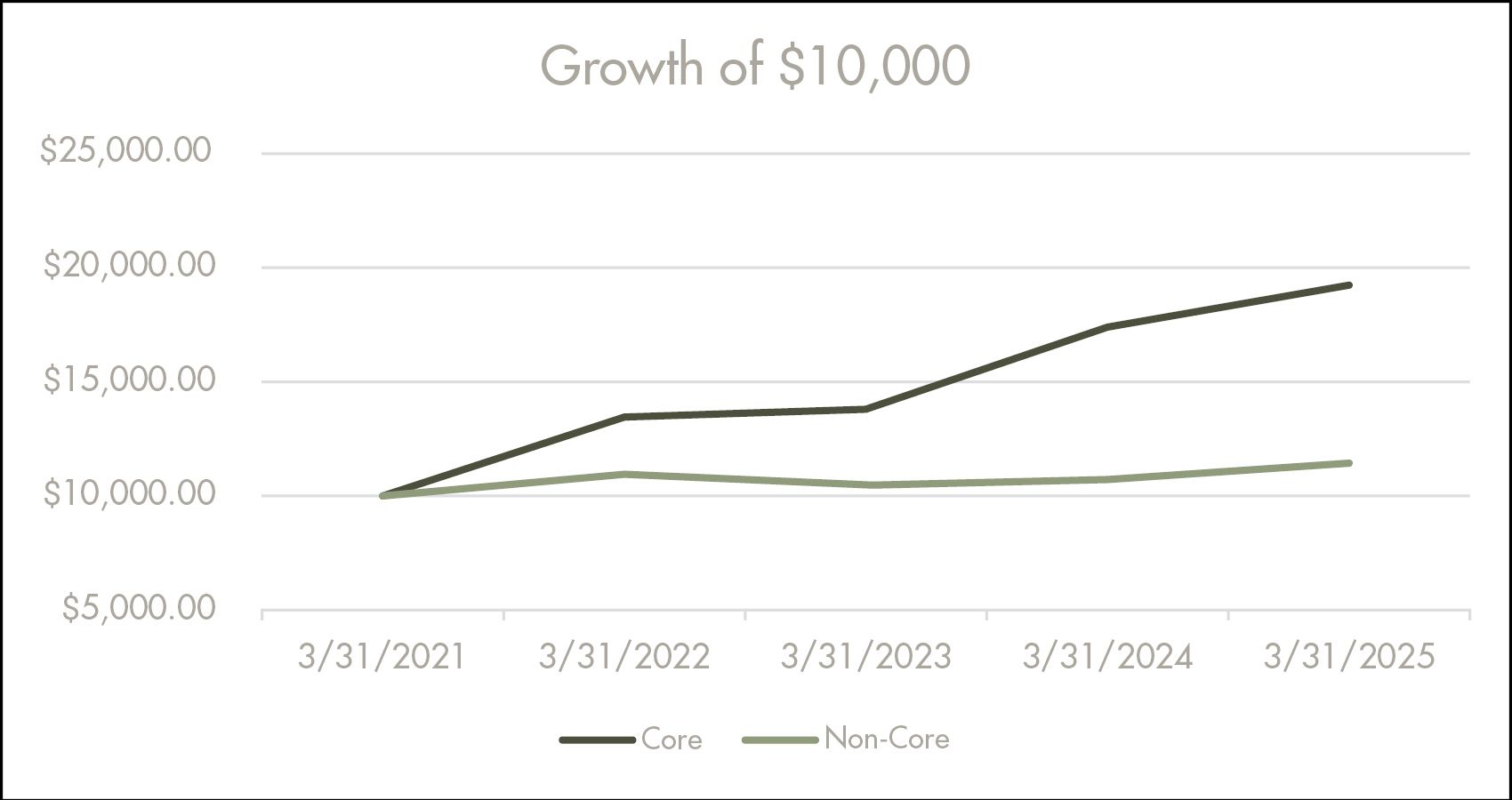

This graph shows the gross change in value of a hypothetical investment of $10,000 in the Core Private Investments Portfolio of the Master Fund for the period indicated. For comparison, the graph also includes the gross change in value of the same hypothetical investment in the Non-Core Private Investments Portfolio.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees, service fees, and other expenses by determining the percentage change in net asset value. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only.

5

Fund Profile4

|

Asset Class Allocation |

% of 3/31/25 |

Geographic Allocation |

% of 3/31/25 |

|||||||||

|

Private Equity |

59.7 |

% |

Asia |

3.7 |

% |

|||||||

|

Real Assets |

23.1 |

% |

Europe |

3.9 |

% |

|||||||

|

Cash Management |

17.2 |

% |

Global |

19.4 |

% |

|||||||

|

|

North America |

72.6 |

% |

|||||||||

|

|

Rest of World |

0.5 |

% |

|||||||||

|

Structure |

% of 3/31/25 |

||||

|

Co-invest |

21.2 |

% |

|||

|

Direct |

11.9 |

% |

|||

|

Fund |

66.9 |

% |

|||

Investment Objective, Principal Strategies, and Principal Risks

Investment Objective & Principal Strategies

The Master Fund’s investment objective is to preserve capital and to generate consistent long-term appreciation and returns across a market cycle (which is estimated to be five to seven years). The Master Fund attempts to achieve this objective through investments primarily in private assets globally. To achieve its objective, the Master Fund provides its Partners, through the Master Fund, with access to high quality private markets asset classes, investments, portfolio construction, and liquidity management. The Master Fund generally pursues its investment objective by allocating assets to Investments, which include primary and secondary subscriptions or commitments to private partnerships managed by investment managers as well as direct investments in the equity or debt of a private or public companies (“Direct Platforms”) (collectively, “Investments”). The Master Fund may seek to hedge all or a portion of the Master Fund’s foreign currency, interest rate, or other risks. Depending on market conditions and the views of the Adviser, the Master Fund may or may not hedge all or a portion of its currency, interest rate, or other exposures.

The Master Fund’s Investments fall within two principal strategies: Private Investments and Cash Management. Private Investments strategies employed include (i) Private Equity and (ii) Real Assets. Cash Management strategies employed include (i) Cash and Cash Equivalents, (ii) Hedge Funds, and (iii) Other Liquid Strategies.

Private Investments

Private Equity. Private equity Investments seeks to generate capital appreciation, particularly during periods of rising economic growth, through investments in private companies seeking capital across various strategies, primarily buyout, growth equity, private debt, and venture capital.

Real Assets. Real asset investments seek to generate capital appreciation, particularly in times of rising inflation, through assets which are generally tangible in nature, and provide explicit or implicit cash flow visibility along with some level of inflation protection. The definition of ‘Real Assets’ varies across industries but typically includes infrastructure, natural resources, and real estate.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees, service fees, and other expenses by determining the percentage change in net asset value. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only.

6

Cash Management

Cash and Cash Equivalents. Fund assets which are cash or can be readily converted into cash, including bank accounts and marketable securities (debt securities with maturities of less than 90 days, such as commercial paper), U.S. Treasury bills, and short-term government bonds with a maturity date of three months or less, among others.

Hedge Funds. Predominantly liquid alternative investments using pooled funds which employ different strategies to generate attractive returns either on an absolute basis or over a specified benchmark. Hedge funds may be actively managed or make use of derivatives and leverage in both domestic and international markets. The Master Fund will selectively invest in Hedge Funds across event driven, global macro, and relative value strategies.

Other Liquid Securities. Entails Investments in a variety of liquid, listed equity, and fixed income strategies, either held directly or through a pooled vehicle. These Investments will typically be held as long-only positions where the Adviser believes there is an opportunity for capital appreciation. These securities have more inherent volatility than other positions in the Cash Management portfolio and may include equities, bonds, commodities, currencies, and exchange-traded funds.

Principal Risks

Broad Investment Mandate

The investment strategy of the Master Fund is opportunistic in nature and covers a broad range of asset classes and geographic regions. A purchaser of Interests must rely upon the ability of the Adviser to identify, structure, and implement investments consistent with the Master Fund’s overall investment objective and policies at such times as they determine. Without limiting the foregoing, the Master Fund may make investments throughout the capital structure, such as mezzanine securities, senior secured debt, bank debt, unsecured debt, convertible bonds, and preferred and common stock and across numerous asset classes such as public equity, structured equity, minority private equity, venture capital, commodities, real estate, natural resources, infrastructure, hybrid derivative instruments, litigation finance, and credit. It is expected that, in light of the Master Fund’s investment objective, the Master Fund will often make equity, credit, and/or debt investments which, from time to time, may involve serving on governance-related committees or in similar positions which involve control or influence over the underlying entity in which the Master Fund invests. Additionally, the Master Fund will be permitted to invest (and may actually invest) in any number of companies operating in a wide range of industries, geography and/or activities.

Master/Feeder Structure

The Master Fund may accept investments from other investors (including other feeder funds), in addition to the Master Fund. The Master Fund currently has other investors that are feeder funds managed by the Adviser or its affiliates, and it may have additional investors in the future. Because each feeder fund can set its own transaction minimums, feeder-specific expenses, and other conditions, one feeder fund could offer access to the Master Fund on more attractive terms, or could experience better performance, than another feeder fund. Smaller feeder funds may be harmed by the actions of larger feeder funds. For example, a larger feeder fund will have more voting power than the Master Fund over the operations of the Master Fund. If the Master Fund conducts repurchase offers, and if other feeder funds tender for a significant portion of their shares in a repurchase offer, the assets of the Master Fund will decrease. This could cause the Master Fund’s expense ratio to increase to the extent contributions to the Master Fund does not offset the cash outflows.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees, service fees, and other expenses by determining the percentage change in net asset value. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only.

7

Risk Allocations

The Adviser has broad discretion to make allocations to Investments executing different strategies and other than limitations on illiquid investments is not constrained with respect to the allocation to individual strategies or asset classes. There is no assurance that its decisions in this regard will be successful. In addition, the Master Fund may be limited in its ability to make changes to allocations due to the subscription and redemption provisions of the Investments, including notice periods and limited subscription and redemption dates, the ability of the Investments to suspend and postpone redemptions, and lockups on redemptions imposed by certain Investments. In addition, any such allocations will be made by the Adviser based on information previously provided by the Investments. If such information is inaccurate or incomplete, it is possible that the Master Fund’s allocation to the asset classes from a risk/reward perspective may not reflect the Adviser’s intended allocations. This could have a material adverse effect on the ability of the Adviser to implement the investment objective of the Master Fund and the Master Fund.

Dependence on the Adviser and the Investment Managers

The Adviser invests certain assets of the Master Fund into Investments managed by the investment managers, and the Adviser has the sole authority and responsibility for the selection of the investment managers. The success of the Master Fund depends upon the ability of the Adviser to develop and implement investment strategies that achieve the investment objective of the Master Fund and the Master Fund. In addition, the Adviser may be dependent on key personnel. To the extent that any key personnel were to depart, the Adviser’s ability to successfully develop and implement investment strategies may be negatively impacted.

Limited Liquidity; Closed-end Fund & Master Fund

The Master Fund is a non-diversified, closed-end management investment company designed primarily for long-term investors, and is not intended to be a trading vehicle. You should not invest in the Master Fund if you need a liquid investment. The Master Fund invests substantially all of its investable assets in the Master Fund, which is an illiquid investment. Closed-end funds differ from open-end management investment companies (commonly known as mutual funds) in that investors in a closed-end fund do not have the right to redeem their shares on a daily basis at a price based on NAV. In order to be able to meet daily redemption requests, mutual funds are subject to more stringent liquidity requirements than closed-end funds. In particular, a mutual fund generally may not invest more than 15% of its net assets in illiquid securities, while a closed-end fund, such as the Master Fund, may invest all or substantially all of its assets in illiquid investments (as is the Master Fund’s investment practice). The Adviser believes that unique investment opportunities exist in the market for Investments, which generally are illiquid.

An investment in the Master Fund provides limited liquidity since the Interests are not freely transferable and Partners may not cause the Master Fund to redeem their Interests. The Master Fund may offer to repurchase Interests from the Partners. Distributions of proceeds upon the repurchase of a Partner’s Interests may be subject to restrictions imposed upon withdrawals under the terms of the Investments or, in the event that the Master Fund and/or the Adviser has engaged one or more sub-advisers, restrictions imposed by investment advisory agreements pursuant to which the Master Fund’s assets are invested. An investment in the Master Fund is suitable only for certain sophisticated investors that do not need liquidity.

If the Master Fund conducts repurchase offers, and if a significant number of Partners sought to have their Interests repurchased at the same time, the illiquidity that results from the Master Fund’s significant investment in long-term investments, which ordinarily cannot be liquidated without significant discount, if at all, may prevent the Master Fund from repurchasing more than a specified amount of Interests.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees, service fees, and other expenses by determining the percentage change in net asset value. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only.

8

Payment for repurchased Interests of the Master Fund may require the Master Fund to liquidate all or a portion of one or more of the Investments earlier than the Adviser would otherwise liquidate these holdings, potentially resulting in losses, and may increase the Master Fund’s portfolio turnover. In addition, to the extent that the Master Fund ever were to repurchase significant amounts of Interests, the illiquidity of the remaining portfolio would increase, a factor that the Board would consider when determining the amount of Interests to repurchase. The Adviser intends to take measures (subject to such policies as may be established by the Investment Committee) to attempt to avoid or minimize potential losses and turnover resulting from the repurchase of Interests. In the event the Master Fund ever winds down investment operations and terminate, the Master Fund would be unable to offer to repurchase all Interests immediately and Partners would receive the value of their Interests over time as the Master Fund liquidated its assets, which could require a significant period to realize certain illiquid assets.

Non-Diversified Status

The Master Fund is a “non-diversified” investment company. Thus, there are no percentage limitations imposed by the Investment Company Act on the percentage of the Master Fund’s assets that may be invested in the securities of any one issuer. Although the Adviser follows a general policy of seeking to diversify the Master Fund’s capital among multiple investment funds, the Adviser may depart from such policy from time to time and one or more investment funds may be allocated a relatively large percentage of the Master Fund’s assets. The Master Fund will limit the percentage of assets held of any one investment fund, at the time of investment, to an amount that is in accordance with any regulatory restrictions applicable to the Master Fund. As a consequence of a large investment in a particular investment fund, losses suffered by such an investment fund could result in a higher reduction in the Master Fund’s capital than if such capital had been more proportionately allocated among a larger number of investment funds.

Risks of Investment Activities Generally

All securities investing and trading activities risk the loss of capital. No assurance can be given that the Master Fund’s or any Investment’s investment activities will be successful or that the Partners will not suffer losses.

Limited Operating History of Investments

Investments may have limited operating histories and the information the Master Fund will obtain about such investments may be limited. As such, the ability of the Adviser to evaluate past performance or to validate the investment strategies of such Investment will be limited. Moreover, even to the extent an Investment has a longer operating history, the past investment performance of any of the Investments should not be construed as an indication of the future results of such investments or the Master Fund, particularly as the investment professionals responsible for the performance of such investments may change over time. This risk is related to, and enhanced by, the risks created by the fact that the Adviser relies upon information provided to it by the issuer of the securities that is not, and cannot be, independently verified. Further, the results of other funds or accounts managed by the Adviser, which have or have had an investment objective similar to or different from that of the Master Fund, may not be indicative of the results that the Master Fund achieves.

The Master Fund may invest a portion of its assets in the securities of less established companies. Investments in such early-stage companies may involve greater risks than generally are associated with investments in more established companies. To the extent there is any public market for the securities held by the Master Fund, such securities may be subject to more abrupt and erratic market price movements than those of larger, more established companies. Less established companies tend to have lower capitalizations and fewer resources and, therefore, often are more vulnerable to financial failure. Such companies also may have shorter operating histories on which to judge future performance and in many cases, if operating, will have negative cash flow. There can be no assurance that any such losses will be offset by gains (if any) realized on the Master Fund’s other investments, and any such Investments should be considered highly speculative and may result in the loss of the Master Fund’s entire investment therein.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees, service fees, and other expenses by determining the percentage change in net asset value. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only.

9

Unspecified Investments; Dependence on the Adviser

The Adviser has complete discretion to select the Investments as opportunities arise. The Master Fund, and, accordingly, Partners, must rely upon the ability of the Adviser to identify and implement Investments consistent with the Master Fund’s investment objective. Partners will not receive or otherwise be privy to due diligence or risk information prepared by or for the Adviser in respect of the Investments. The Adviser has the authority and responsibility for asset allocation, the selection of Investments, and all other investment decisions for the Master Fund. The success of the Master Fund depends upon the ability of the Adviser to develop and implement investment strategies that achieve the investment objective of the Master Fund. Partners will have no right or power to participate in the management or control of the Master Fund or the Investments, or the terms of any such investments. There can be no assurance that the Adviser will be able to select or implement successful strategies or achieve their respective investment objectives.

Effective March 1, 2021, the Investment team managing the Master Fund changed as a result of an acquisition of the Adviser to the Master Fund by Cypress Creek Partners (and/or an affiliate thereof). The current Portfolio Manager of the Master Fund is William P. Prather III. Mr. Prather has been responsible for the management of the Master Fund since March 1, 2021. He previously served as the Head of Natural Resources and Infrastructure portfolio at the University of Texas/Texas A&M Investment Management Company (“UTIMCO”), and prior to that was a portfolio manager at BlackRock Inc.

Endnotes and Additional Disclosures

General

The views expressed in this letter are those of the Portfolio Manager and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Cypress Creek Partners and the Master Fund disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Cypress Creek Partners fund. This commentary may contain statements that are not historical facts, referred to as “forward-looking statements”. The Master Fund’s actual future results may differ significantly from those stated in any forward-looking statement, depending on factors such as changes in securities or financial markets or general economic conditions, the volume of sales and purchases of Fund Interests, the continuation of investment advisory, administrative, and service contracts, and other risks discussed from time to time in the Master Fund’s filings with the United States Securities and Exchange Commission.

This letter is provided solely for informational purposes and is exclusively intended for use by existing Fund investors and/or pre-qualified prospective Fund investors with whom the Master Fund or an authorized intermediary acting on behalf of the Master Fund has a pre-existing substantive relationship. Neither this letter nor the information contained therein constitutes an offer to sell or a solicitation of any offer to buy any securities. Any offering or solicitation will be made only to eligible investors and pursuant to the current version of the applicable Private Placement Memorandum and other governing documents, all of which must be read in their entirety.

Performance figures shown for periods less than one year are cumulative (not annualized). Historical performance track record for the Fund prior to March 1, 2021, was achieved by the adviser and its then investment management team.

The Master Fund Profile is subject to change due to active management employed by the Adviser.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees, service fees, and other expenses by determining the percentage change in net asset value. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only.

10

Index Definitions

MSCI All Country World Index (“ACWI”). The MSCI ACWI is a global equity index designed to represent the performance of the full opportunity set of large- and mid-cap companies across 23 developed markets and 24 emerging markets countries. With 2,558 constituents, and an average market capitalization of $29.9 billion (median market capitalization of $8.1 billion), the index covers approximately 85% of the global investable equity opportunity set. This index is calculated on a net USD total return-basis, which reflects the re-investment of dividends, interest, and other income converted to USD and after the deduction of withholding taxes5.

Footnotes

1 “World Economic Outlook, April 2025: A Critical Juncture amid Policy Shifts.” IMF, 22 Apr. 2025.

2 “2024 Annual Global Private Market Fundraising Report” | Pitchbook, 4 Mar. 2025.

3 Cypress Creek defines the referenced terms as follows: Private Investments includes Private Equity, Real Assets and Private Debt sub-portfolios. Private Equity includes private investment strategies such as buyouts, growth equity, and venture capital, among others. Real Assets represents private investment strategies such as infrastructure, natural resources (e.g., agriculture/farmland, energy, metals, and mining, etc.), and real estate. Cash Management includes hedge funds including event driven, global macro, and relative value strategies, long-only liquid strategies, liquid securities, and cash. Anchor Partnership refers to an approach in which Cypress Creek will serve as an early and meaningful investor for new or developing managers. In addition to capital investments, Cypress Creek works consultatively with the target managers to actively contribute to their growth, collaborating in key functional areas that include but are not limited to compliance, reporting, asset allocation, risk management, and capital raising. As a result of these long-term, strategic relationships, Cypress Creek may benefit from advantaged economics and allocation/access rights. Core Managers represent managers and related investments where Cypress Creek expects to maintain an active ongoing investment relationship and the Investment Committee has approved of the manager. New/developing fund managers are managers raising their first-time private investment fund or up to a potential fourth fund. Lower-middle market private investing is focused on managers with a target capacity below $1 billion, which generally implies equity tickets in individual transactions of below $100 million, subject to variation.

4 Geographic Allocation and Structure figures are illustrative of the Private Investments portfolio-only

5 As of April 2025

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees, service fees, and other expenses by determining the percentage change in net asset value. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only.

11

Report of Independent Registered Public Accounting Firm

To the Partners and the Board of Directors of

Cypress Creek Private Strategies Registered Fund, L.P.

Opinion on the Financial Statements

We have audited the accompanying statement of assets, liabilities and partners’ capital of Cypress Creek Private Strategies Registered Fund, L.P. (the Fund) as of March 31, 2025, the related statements of operations and cash flows for the year then ended, the statements of changes in partners’ capital for each of the two years in the period then ended, and the related notes to the financial statements (collectively, the financial statements), and the financial highlights for the years ended March 31, 2025, March 31, 2024 and March 31, 2023, the period from January 1, 2022 to March 31, 2022 and for the year ended December 31, 2021. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Fund as of March 31, 2025, the results of its operations and its cash flows for the year then ended, the changes in partners’ capital for each of the two years in the period then ended, and the financial highlights for the years ended March 31, 2025, March 31, 2024 and March 31, 2023, the period from January 1, 2022 to March 31, 2022 and for the year ended December 31, 2021, in conformity with accounting principles generally accepted in the United States of America.

The financial highlights for the year ended December 31, 2020, for the Fund were audited by other auditors. Those auditors expressed an unqualified opinion on those financial statements and financial highlights in their report dated February 26, 2021.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements and financial highlights based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Fund in accordance with U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

/s/ RSM US LLP

We have served as the auditor of one or more Cypress Creek Partners investment companies since 2021.

Chicago, Illinois

May 30, 2025

12

CYPRESS CREEK PRIVATE STRATEGIES REGISTERED FUND, L.P.

Statement of Assets, Liabilities and Partners’ Capital

March 31, 2025

|

Assets |

|

||

|

Investment in the Master Fund, at fair value |

$ |

86,772,207 |

|

|

Total assets |

|

86,772,207 |

|

|

Liabilities and Partners’ Capital |

|

||

|

Servicing Fees payable |

|

50,565 |

|

|

Administration fees payable |

|

4,875 |

|

|

Accounts payable and accrued expenses |

|

84,712 |

|

|

Total liabilities |

|

140,152 |

|

|

Partners’ capital |

|

86,632,055 |

|

|

Total liabilities and partners’ capital |

$ |

86,772,207 |

See accompanying notes to financial statements.

13

CYPRESS CREEK PRIVATE STRATEGIES REGISTERED FUND, L.P.

Statement of Operations

Year Ended March 31, 2025

|

Net investment income allocated from the Master Fund |

|

|

||

|

Interest income |

$ |

1,057,675 |

|

|

|

Dividend income (net of foreign tax withholding) |

|

838,448 |

|

|

|

Expenses |

|

(1,533,590 |

) |

|

|

Net investment income allocated from the Master Fund |

|

362,533 |

|

|

|

Expenses of the Registered Fund |

|

|

||

|

Servicing Fees |

|

587,942 |

|

|

|

Professional fees |

|

121,579 |

|

|

|

Administration fees |

|

19,500 |

|

|

|

Other expenses |

|

43,423 |

|

|

|

Total expenses of the Registered Fund |

|

772,444 |

|

|

|

Net investment loss of the Registered Fund |

|

(409,911 |

) |

|

|

Net realized and unrealized gain (loss) from investments and foreign currency allocated from the Master Fund |

|

|

||

|

Net realized gain (loss) from investments and foreign currency transactions |

|

5,121,907 |

|

|

|

Change in unrealized appreciation/depreciation from investments and foreign currency translations |

|

688,569 |

|

|

|

Net realized and unrealized gain (loss) from investments and foreign currency allocated from the Master Fund |

|

5,810,476 |

|

|

|

Net increase in partners’ capital resulting from operations |

$ |

5,400,565 |

|

See accompanying notes to financial statements.

14

|

Year Ended |

Year Ended |

|||||||

|

Increase (decrease) in partners’ capital from operations |

|

|

|

|

||||

|

Investment loss – net |

$ |

(409,911 |

) |

$ |

(1,624,964 |

) |

||

|

Net realized gain from investments and foreign currency |

|

5,121,907 |

|

|

2,827,313 |

|

||

|

Unrealized appreciation from investments and foreign currency |

|

688,569 |

|

|

5,015,978 |

|

||

|

Contributions |

|

1,105,764 |

|

|

1,069,983 |

|

||

|

Withdrawals |

|

(2,142,697 |

) |

|

(1,936,480 |

) |

||

|

Total increase |

|

4,363,632 |

|

|

5,351,830 |

|

||

|

Net assets |

|

|

|

|

||||

|

Beginning of Year |

|

82,268,423 |

|

|

76,916,593 |

|

||

|

End of Year |

$ |

86,632,055 |

|

$ |

82,268,423 |

|

||

See accompanying notes to financial statements.

15

CYPRESS CREEK PRIVATE STRATEGIES REGISTERED FUND, L.P.

Statement of Cash Flows

Year Ended March 31, 2025

|

Cash flows from operating activities |

|

|

||

|

Net increase in partners’ capital resulting from operations |

$ |

5,400,565 |

|

|

|

Adjustments to reconcile net increase in partners’ capital resulting from operations to net cash provided by operating activities |

|

|

||

|

Net realized and unrealized (gain)/loss from investments and foreign currency allocated from the Master Fund |

|

(5,810,476 |

) |

|

|

Net investment (gain)/loss allocated from the Master Fund |

|

(362,533 |

) |

|

|

Withdrawals from the Master Fund |

|

1,864,846 |

|

|

|

Change in operating assets and liabilities |

|

|

||

|

Servicing Fees payable |

|

(43,059 |

) |

|

|

Administration fees payable |

|

4,875 |

|

|

|

Accounts payable and accrued expenses |

|

(17,285 |

) |

|

|

Net cash provided by operating activities |

|

1,036,933 |

|

|

|

Cash flows from financing activities |

|

|

||

|

Withdrawals |

|

(1,036,933 |

) |

|

|

Net cash used in financing activities |

|

(1,036,933 |

) |

|

|

Net change in cash and cash equivalents |

|

— |

|

|

|

Cash and cash equivilents |

|

|

||

|

Beginning of year |

|

— |

|

|

|

End of year |

$ |

— |

|

|

|

Supplemental schedule of non-cash financing activities |

|

|

||

|

Distribution reinvestment |

$ |

1,105,764 |

|

See accompanying notes to financial statements.

16

1. Organization

The Cypress Creek Private Strategies Registered Fund, L.P. (the “Registered Fund”), a Delaware limited partnership registered under the Investment Company Act of 1940, as amended (the “1940 Act”), commenced operations on March 10, 2004, as a non-diversified, closed-end management investment company. The Registered Fund was created to serve as a feeder fund for the Cypress Creek Private Strategies Master Fund, L.P. (the “Master Fund”). For convenience, reference to the Registered Fund may include the Master Fund, as the context requires.

The Registered Fund’s investment objective is to preserve capital and to generate consistent long-term appreciation and returns across a market cycle (which is estimated to be five to seven years). The Registered Fund pursues its investment objective by investing substantially all of its assets in the Master Fund. The Master Fund generally pursues the investment objective by allocating assets to investments, which include primary and secondary subscriptions or commitments to private partnerships managed by third-party investment managers (“Investment Managers”), as well as direct investments in the equity or debt of private or public companies (“Direct Platforms”). The Master Fund’s financial statements, Schedule of Investments, and notes to the financial statements, included elsewhere in this report, should be read in conjunction with this report. The percentage of the Master Fund’s partnership interests owned by the Registered Fund on March 31, 2025, was 36.04%.

The Endowment Fund GP, L.P., a Delaware limited partnership, serves as the general partner of the Registered Fund (the “General Partner”). To the fullest extent permitted by applicable law, the General Partner has irrevocably delegated to a board of directors (the “Board” and each member a “Director”) its rights and powers to monitor and oversee the business affairs of the Registered Fund, including the complete and exclusive authority to oversee and establish policies regarding the management, conduct, and operation of the Registered Fund’s business. A majority of the Directors are independent of the General Partner and its management. To the extent permitted by applicable law, the Board may delegate any of its rights, powers, and authority to, among others, the officers of the Registered Fund, the Adviser (as hereinafter defined), or any committee of the Board. The General Partner has X% capital interest in the Registered Fund.

The Board is authorized to engage an investment adviser and it has selected Endowment Advisers, L.P. d/b/a Cypress Creek Partners (the “Adviser”), to manage the Registered Fund’s portfolio and operations, pursuant to an investment management agreement (the “Investment Management Agreement”). The Adviser is a Delaware limited partnership that is registered as an investment adviser under the Investment Advisers Act of 1940, as amended (the “Advisers Act”). Under the Investment Management Agreement, the Adviser is responsible for the establishment of an investment committee, which is responsible for developing, implementing, and supervising the Registered Fund’s investment program subject to the ultimate supervision of the Board. In addition to investment advisory services, the Adviser also functions as the servicing agent of the Registered Fund (the “Servicing Agent”) and as such provides or procures investor services and administrative assistance for the Registered Fund. The Adviser can delegate all or a portion of its duties as Servicing Agent to other parties, who would in turn act as sub-servicing agents.

Under the Registered Fund’s organizational documents, the Registered Fund’s officers and Directors are indemnified against certain liabilities arising out of the performance of their duties to the Registered Fund. In the normal course of business, the Registered Fund enters into contracts with service providers, which also provide for indemnifications by the Registered Fund. The Registered Fund’s maximum exposure under these arrangements is unknown, as this would involve any future potential claims that may be made against the Registered Fund. However, based on experience, the General Partner expects that risk of loss to be remote.

17

CYPRESS CREEK PRIVATE STRATEGIES REGISTERED FUND, L.P.

Notes to Financial Statements, continued

March 31, 2025

2. Summary of Significant Accounting Policies

Basis of Presentation

The accounting and reporting policies of the Registered Fund conform with U.S. generally accepted accounting principles (“U.S. GAAP”). The accompanying financial statements reflect the financial position of the Registered Fund and the results of its operations. The Registered Fund is an investment company that follows the investment company accounting and reporting guidance under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies.”

Segment Reporting

During this reporting period, the Registered Fund adopted FASB Accounting Standards Update 2023-07, Segment Reporting (“Topic 280”) — Improvements to Reportable Segment Disclosures (“ASU 2023-07”). Adoption of the new standard impacted the disclosures on financial statements only and did not affect the Registered Fund’s financial position or the results of the Registered Fund’s operations. An operating segment is defined in Topic 280 as a component of a public entity that engages in business activities from which it may recognize revenues and incur expenses, has operating results that are regularly reviewed by the public entity’s chief operating decision maker (“CODM”) to make decisions about resources to be allocated to the segment and assess its performance, and has discrete financial information available. The Registered Fund’s Adviser acts as the Registered Fund’s CODM. The Registered Fund represents a single operating segment, as the CODM monitors the operating results of the Registered Fund as a whole and the Registered Fund’s long-term strategic asset allocation is pre-determined in accordance with the terms of its defined investment strategy which is executed by the Registered Fund’s portfolio managers. The financial information in the form of the Registered Fund’s portfolio composition via its investment in the Master Fund, the Registered Fund’s total returns, expense ratios and changes in net assets (i.e., changes in net assets resulting from operations, subscriptions and redemptions), which are used by the CODM to assess the segment’s performance versus the Registered Fund’s comparative benchmarks and to make resource allocation decisions for the Registered Fund’s single segment, is consistent with the information presented within the Registered Fund’s financial statements and the financial highlights. Segment assets are reflected on the accompanying statement of assets and liabilities as “net assets” and significant segment expenses are listed on the accompanying statement of operations.

Use of Estimates

The financial statements have been prepared in conformity with U.S. GAAP, which requires management to make estimates and assumptions relating to the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results may differ from those estimates and such differences may be significant.

Cash and Cash Equivalents

The Registered Fund considers all unpledged temporary cash investments with a maturity date at the time of purchase of three months or less to be cash equivalents.

Investment Transactions and Related Investment Income

The Registered Fund records monthly its pro-rata share of income, expenses, changes in unrealized appreciation and depreciation, and realized gains and losses derived from the Master Fund.

18

CYPRESS CREEK PRIVATE STRATEGIES REGISTERED FUND, L.P.

Notes to Financial Statements, continued

March 31, 2025

The Registered Fund records investment transactions on a trade-date basis.

Investments that are held by the Registered Fund are marked to fair value at the date of the financial statements, and the corresponding change in unrealized appreciation/depreciation is included in the Statement of Operations.

Investment Valuation

The valuation of the Registered Fund’s investments is determined as of the close of business at the end of each reporting period, generally monthly. The valuation of the Registered Fund’s investments is calculated by UMB Fund Services, Inc., the Registered Fund’s independent administrator (the “Administrator”).

The Board is responsible for overseeing the Registered Fund’s valuation policies, making recommendations to the Adviser on valuation-related matters, and overseeing implementation by the Adviser of such valuation policies.

Pursuant to Rule 2a-5 under the 1940 Act, the Board has delegated day-to-day management of the valuation process to the Adviser as the appointed Valuation Designee, which has established a valuation committee (the “Adviser Valuation Committee”) to carry out this function. The Valuation Designee is subject to the oversight of the Board. The Valuation Designee is responsible for assessing and managing key valuation risk, and is generally to review valuation methodologies, valuation determinations, and any information provided by the Adviser or the Administrator.

The Registered Fund invests substantially all of its assets in the Master Fund. Investments in the Master Fund are recorded at fair value based on the Registered Fund’s proportional share of the Master Fund’s partners’ capital. Valuation of the investments held by the Master Fund is discussed in the Master Fund’s notes to financial statements, included in this report.

Investment Income

For investments in securities, dividend income is recorded on the ex-dividend date, net of withholding taxes. Interest income is recorded as earned on the accrual basis and includes amortization of premiums or accretion of discounts.

Fund Expenses

Unless otherwise voluntarily or contractually assumed by the Adviser or another party, the Registered Fund bears all expenses incurred in its business, directly or indirectly through its investment in the Master Fund, including, but not limited to, the following: all costs and expenses related to investment transactions and positions for the Registered Fund’s account; legal fees; compliance fees; accounting, auditing and tax preparation fees; recordkeeping and custodial fees; costs of computing the Registered Fund’s net asset value; fees for data and software providers; research expenses; costs of insurance; registration expenses; offering costs; expenses of meetings of partners; directors fees; all costs with respect to communications to partners; transfer taxes; and other types of expenses as may be approved from time to time by the Board.

Income Taxes

The Registered Fund is organized and operates as a limited partnership and is not subject to income taxes as a separate entity. Such taxes are the responsibility of the individual partners. Accordingly, no provision for income taxes has been made in the Registered Fund’s financial statements. Investments in foreign securities may result in foreign taxes being withheld by the issuer of such securities.

For the current open tax years, and for all major jurisdictions, management of the Registered Fund has evaluated the tax positions taken or expected to be taken in the course of preparing the Registered Fund’s tax returns to determine whether the tax positions will “more-likely-than-not” be sustained by the Registered Fund upon challenge by the applicable tax

19

CYPRESS CREEK PRIVATE STRATEGIES REGISTERED FUND, L.P.

Notes to Financial Statements, continued

March 31, 2025

authority. Tax positions not deemed to meet the more-likely-than-not threshold and that would result in a tax benefit or expense to the Registered Fund would be recorded as a tax benefit or expense in the current period. For the year ended March 31, 2025, the Registered Fund did not recognize any amounts for unrecognized tax benefit/expense. A reconciliation of unrecognized tax benefit/expense is not provided herein, as the beginning and ending amounts of unrecognized tax benefit/expense are zero, with no interim additions, reductions, or settlements. Tax positions taken in tax years which remain open under the statute of limitations (generally three years for federal income tax purposes and four years for state income tax purposes) are subject to examination by federal and state tax jurisdictions.

3. Fair Value Measurements

The Registered Fund records its investment in the Master Fund at fair value. Investments of the Master Fund are recorded at fair value discussed further in the Master Fund’s notes to financial statements, included in this report.

4. Partners’ Capital

Issuance of Interests

Upon receipt from an eligible investor of an initial or additional application for interests (the “Interests”), which will generally be accepted as of the first day of each month, the Registered Fund will issue new Interests. The Interests have not been registered under the Securities Act of 1933, as amended (the “Securities Act”), or the securities laws of any state. The Registered Fund issues Interests only in private placement transactions in accordance with Regulation D or other applicable exemptions under the Securities Act. No public market exists for the Interests, and none is expected to develop. The Registered Fund is not required, and does not intend, to hold annual meetings of its partners. The Interests are subject to substantial restrictions on transferability and resale and may not be transferred or resold except as permitted under the Registered Fund’s limited partnership agreement. The Registered Fund reserves the right to reject any applications for subscription of Interests.

Allocation of Profits and Losses

For each fiscal period net profits or net losses of the Registered Fund, including allocations from the Master Fund, are allocated among and credited to or debited against the capital accounts of all partners as of the last day of each fiscal period in accordance with the partners’ respective capital account ownership percentage for the fiscal period. Net profits or net losses are measured as the net change in the value of the partners’ capital of the Registered Fund, including any change in unrealized appreciation or depreciation of investments and income, net of expenses, and realized gains or losses during a fiscal period. Net profits or net losses are allocated after giving effect for any initial or additional applications for Interests, which generally occur at the beginning of the month, or any repurchases of Interests.

Distribution Reinvestment Program

Pursuant to the Fund’s distribution reinvestment plan (the “DRP”), all distributions paid to a partner will be automatically reinvested and retained as part of the partner’s interest in the Fund unless a partner has elected not to participate in the DRP. Election not to participate in the DRP, and to have all distributions, if any, paid directly to the partner rather than having such distribution reinvested in the Fund, must be made by indicating such election in the subscription agreement or by notifying the Fund.

On October 31, 2024, the Registered Fund paid a distribution in the amount of $2,136,849 in which $1,031,085 was paid out to partners based on capital balance in cash and $1,105,764 was reinvested in the Fund, depending on the partner’s election.

20

CYPRESS CREEK PRIVATE STRATEGIES REGISTERED FUND, L.P.

Notes to Financial Statements, continued

March 31, 2025

Repurchase of Interests

A partner will not be eligible to have the Registered Fund repurchase all or any portion of an Interest at the partner’s discretion at any time. Periodically, the Adviser, which also serves as the investment adviser of the Master Fund, recommends to the Board that the Registered Fund offer to repurchase such Interests during the period, pursuant to written tenders by partners.

The Board retains the sole discretion to accept or reject the recommendation of the Adviser and to determine the amount of Interests, if any, that will be purchased in any tender offer that it does approve. Since the Registered Fund’s assets are invested in the Master Fund, the ability of the Registered Fund to have its Interests in the Master Fund be repurchased would be subject to the Master Fund’s repurchase policy. The Master Fund’s repurchase policy is substantially similar to the Registered Fund’s repurchase policy as any tender offer by the Master Fund is subject to the sole discretion of the Board. In addition, the Registered Fund may determine not to conduct a repurchase offer each time the Master Fund conducts a repurchase offer. In the event Interests are repurchased, there will be a substantial period of time between the date as of which partners must tender their Interests for repurchase and the date they can expect to receive payment for their Interests from the Registered Fund.

5. Investments in Portfolio Securities

As of March 31, 2025, all of the investments made by the Registered Fund were in the Master Fund.

6. Administration Agreement

In consideration for administrative, accounting, and recordkeeping services, the Registered Fund pays the Administrator a monthly administration fee based on a fixed annual rate. The Administrator also provides compliance, transfer agency, and other investor related services at an additional cost. The total administration fee incurred for the year ended March 31, 2025, was $19,500, of which $4,875 was outstanding as a payable at March 31, 2025.

7. Investment Advisory Fees and Affiliated Transactions

Management Fee

In consideration of the advisory and other services provided by the Adviser to the Master Fund and the Registered Fund, the Master Fund pays the Adviser a management fee (the “Management Fee”). The Management Fee is equal to the fee schedule below on an annualized basis of the Master Fund’s partners’ capital based on the Master Fund’s partners’ capital at the end of each month, payable quarterly in arrears:

|

Partners’ Capital: |

Management Fee |

|

|

First $150 million |

1.00% |

|

|

Next $250 million (up to $400 million) |

0.90% |

|

|

Next $300 million (up to $700 million) |

0.80% |

|

|

Next $300 million (up to $1,000 million) |

0.70% |

|

|

Next $250 million (up to $1,500 million) |

0.60% |

|

|

Amounts in excess of $1,500 million |

0.50% |

So long as the Registered Fund invests all of its investable assets in the Master Fund, the Registered Fund will not pay the Adviser directly any Management Fee; however, should the Registered Fund not have all of its investments in the Master Fund, it may be charged the Management Fee directly. The Registered Fund’s partners bear an indirect portion of the Management Fee paid by the Master Fund. The Management Fee decreases the net profits or increases the net losses of the Master Fund and indirectly the Registered Fund as the fees reduce the capital accounts of the Master Fund’s partners.

21

CYPRESS CREEK PRIVATE STRATEGIES REGISTERED FUND, L.P.

Notes to Financial Statements, continued

March 31, 2025

Incentive Fee

The Adviser is eligible to receive an incentive fee from the Master Fund representing 10% of the return of the Master Fund in excess of a 6% net return annually, based on the limited partner interests in the Master Fund; calculated and accrued monthly and payable annually. The Master Fund incurred $355,561 in incentive fees for the year ended March 31, 2025, of which $128,493 was allocated to the Registered Fund.

Servicing Fee

In consideration for providing or procuring investor services and administrative assistance to the Registered Fund, the Adviser receives a servicing fee (the “Servicing Fee”) equal to 0.70% (on an annualized basis) of each partner’s capital account balance, calculated at the end of each month, payable quarterly in arrears.

The Adviser may engage one or more sub-servicing agents to provide some or all of the services. Compensation to any sub-servicing agent is paid by the Adviser. The Adviser or its affiliates also may pay a fee out of their own resources to sub-servicing agents.

For the year ended March 31, 2025, $587,942 was incurred for Servicing Fees, of which $50,565 was outstanding as a payable at March 31, 2025.

Placement Agents

The Registered Fund may engage one or more placement agents (each, a “Placement Agent”) to solicit investments in the Registered Fund. On September 1, 2024 Vigilant Distributors, LLC, a broker dealer, was engaged by the Registered Fund to serve as a Placement Agent. Prior to September 1, 2024 Foreside Financial Services, LLC, a broker-dealer, was engaged by the Registered Fund to serve as a Placement Agent. A Placement Agent may engage one or more sub-placement agents. The Adviser or its affiliates may pay a fee out of their own resources to Placement Agents and sub-placement agents.

8. Financial Highlights

|

Year Ended |

Year Ended |

Year Ended |

Period Ended |

Year Ended |

Year Ended |

|||||||||||||||||||

|

Net investment loss to average partners’ capital(1) |

|

(0.49 |

)% |

|

(2.09 |

)% |

|

(1.46 |

)% |

|

(2.49 |

)% |

|

(2.33 |

)% |

|

(2.25 |

)% |

||||||

|

Expenses to average partners’ capital(1) |

|

2.75 |

%(2) |

|

2.95 |

%(2) |

|

2.63 |

% |

|

2.84 |

% |

|

2.91 |

% |

|

2.88 |

% |

||||||

|

Portfolio turnover(3) |

|

12.01 |

% |

|

13.16 |

% |

|

9.95 |

% |

|

1.25 |

% |

|

29.70 |

% |

|

7.58 |

% |

||||||

|

Total return(4) |

|

6.60 |

% |

|

8.17 |

% |

|

(4.89 |

)% |

|

0.26 |

% |

|

6.73 |

% |

|

10.32 |

% |

||||||

|

Partners’ capital, end of period (000s) |

$ |

86,632 |

|

$ |

82,268 |

|

$ |

76,917 |

|

$ |

81,702 |

|

$ |

81,944 |

|

$ |

95,920 |

|

||||||

An investor’s return and operating ratios may vary from those reflected based on the timing of capital transactions.

____________

* The Registered Fund has changed its fiscal year end from December 31 to March 31. This period represents the 3-month period from January 1, 2022 to March 31, 2022.

(1) Ratios are calculated by dividing the indicated amount by average partners’ capital measured at the end of each month during the period. Ratios include allocations of net investment loss and expenses from the Master Fund. Ratios are annualized for periods less than 12 months.

22

CYPRESS CREEK PRIVATE STRATEGIES REGISTERED FUND, L.P.

Notes to Financial Statements, continued

March 31, 2025

(2) For the year ended March 31, 2025 and March 31, 2024, the expense ratio includes incentive fees of 0.15% and 0.33%, respectively.

(3) The Registered Fund is invested exclusively in the Master Fund, therefore this ratio reflects the portfolio turnover of the Master Fund, which is for the period indicated.

(4) The total return of the Registered Fund is calculated as geometrically linked monthly returns for each month in the period. Not annualized for periods less than 12 months.

9. Investment-Related Risks

All securities investing and trading activities risk the loss of capital. No assurance can be given that the Master Fund’s or any investment fund’s investment activities will be successful or that the Partners will not suffer losses.

In general, these principal risks exist whether the investment is made by an investment fund or held by the Master Fund directly and therefore for convenience purposes, the description of such risks in terms of an investment fund is intended to include the same risks for investments made directly by the Master Fund. It is possible that an investment fund (or the Master Fund) will make (or hold) an investment that is not described below, and any such investment will be subject to its own particular risks. For purposes of this discussion, references to the activities of the investment funds should generally be interpreted to include the activities of an Investment Manager. The risks and considerations described below are intended to reflect the Master Fund’s anticipated holdings.

Secondary Investment Risk