Post-Qualification Offering Circular Amendment No. 1

File No. 024-11016

OFFERING CIRCULAR

Up to 12,500,000 Shares of CaliberCos Inc. Series B Preferred Stock convertible into

12,500,000 Shares of CaliberCos Inc. Class A Common Stock

Minimum Individual Investment: 500 Shares $2,000.00

Dated: May 26, 2020

This Post-Qualification Offering Circular Amendment No. 1 (this “PQA”) amends the offering circular of CaliberCos Inc. (the “Company,” “we,” “us,” or “our”) qualified and dated February 28, 2020 and as may be amended and supplemented from time to time (the “Offering Circular”).

The purpose of this PQA is to amend, update and/or replace certain information contained in the Offering Circular. Unless otherwise defined below, capitalized terms used herein shall have the same meanings as set forth in the Offering Circular. See “Incorporation by Reference of Offering Circular” below.

Incorporation by Reference of Offering Circular

The Offering Circular, including this PQA, is part of an offering statement (File No. 024-11016) that we filed with the Securities and Exchange Commission. We hereby incorporate by reference into this PQA all of the information contained in the following:

| 1. | Part II of the Offering Circular, to the extent not otherwise modified or replaced by offering circular supplement and/or post-qualification amendment. |

Note that any statement that we make in this PQA (or have made in the Offering Circular) will be modified or superseded by any inconsistent statement made by us in a subsequent offering circular supplement or post-qualification amendment.

Recent Update

The following disclosure is added on page 3 of the Offering Circular under the Section entitled “Summary – Recent Update”:

Operating Results for Real Estate Services division for the year ended December 31, 2019 (Preliminary and Unaudited)

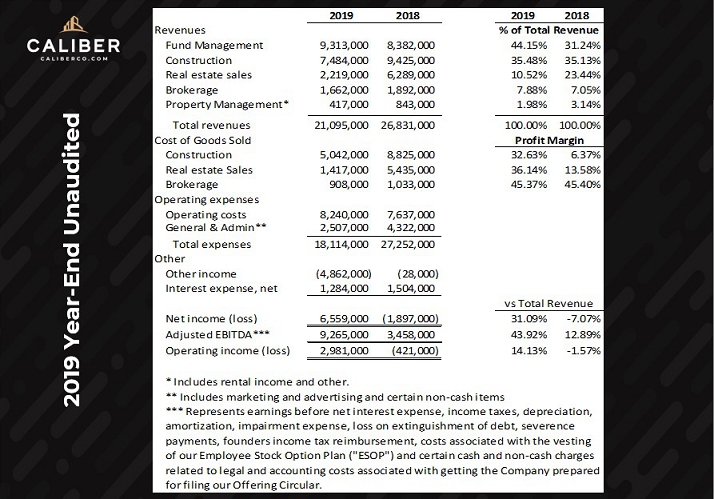

Set forth below are certain preliminary and unaudited estimates of selected financial information for our Real Estate Services division only, for the year ended December 31, 2019 compared to the year ended December 31, 20181. Our audited consolidated financial statements for the year ended December 31, 2019 are not yet available. The following information reflects our preliminary estimates with respect to such results based on currently available information. It is not a comprehensive statement of our financial results and is subject to completion of our financial closing. Our actual results may differ materially from these estimates. These estimates should not be viewed as a substitute for our full annual consolidated financial statements prepared in accordance with U.S. generally accepted accounting principles, or GAAP. Our preliminary estimated results are not necessarily indicative of the results to be expected for any future period. See the sections titled “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for additional information regarding factors that could result in differences between the preliminary estimated financial results and operating data presented below and the actual financial results and other information we will report for the year ended December 31, 2019.

1 The information presented for the year ended December 31, 2018 is derived from our audited December 31, 2018 financial statements except for our presentation of EBITDA and Operating Income contained herein which are unaudited. Certain amounts in 2018 have been reclassified to conform to the presentation of the 2019 preliminary unaudited estimates, including $6,289,000 of real estate sales previously classified in real estate operations and now classified in real estate services.

The preliminary unaudited estimates of the Real Estate Services division for the year ended December 31, 2019 presented below have been prepared by, and are the responsibility of, management. Marcum LLP, our independent registered public accounting firm, has not audited, reviewed, compiled, or performed any procedures with respect to such preliminary unaudited information. Accordingly, Marcum LLP does not express an opinion or any other form of assurance with respect thereto.

Disclosures with respect to COVID-19

Recently, there is an ongoing outbreak of a novel strain of coronavirus (“COVID-19”) first identified in China which has since spread globally. In March 2020, the World Health Organization declared COVID-19 a pandemic which has resulted in quarantines, travel restrictions, and the temporary closure of stores and business facilities for the past few months domestically and abroad. Given the rapidly expanding nature of the COVID-19 pandemic, we believe there is a risk that our business, results of operations, and financial condition will be adversely affected, especially for our hospitality related investments where we are already starting to experience significant declines in occupancy and reductions in reservations. It is unclear whether the effects of COVID-19 will have a lasting and prolonged effect on asset values in the long term. The extent and pervasiveness of the impact to our results of operations will also depend on future developments and new information that may emerge regarding the duration and severity of COVID-19 and the actions taken by government authorities and other entities to contain COVID-19 or mitigate its impact, almost all of which are beyond our control.

The reduction in travel has adversely affected the hospitality industry on a global basis. Due to the uncertainties associated with the COVID-19 pandemic and the indeterminate length of time it will affect the hospitality industry, we have taken certain proactive measures to address liquidity, capital preservation and cost mitigation:

| · | All of our hotels currently remain open, despite the current low occupancy caused by the COVID-19 disruption. In response to the effects of COVID-19 on our business, we have reduced operating costs (including reducing food and beverage operations in accordance with government regulations and furloughing any non-essential employees) and are expected to continue to remain open so long as incremental savings are achieved as compared to the cost of closure of one or more properties. |

| · | We have been proactively pursuing alternative uses and sources of revenue from our hotel properties such as providing housing for first responders and healthcare workers through our Operation Sleep Safe initiative and providing special government rates for essential workers. |

| · | We have significantly reduced staffing levels at our hotels to further preserve cash. |

| · | We have maintained essential management and sales staffing to allow our hotels to capture new business when the hotel market begins to correct. |

| · | We are acting as an early adopter, to the extent our hotels are brand-franchised, of brand led cleaning and wellness initiatives to re-assure guests of the Company’s commitment to safe travel. |

Trends Affecting Our Business

The Section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations –Trends Affecting Our Business” located on pages 34 and 35 of the Offering Circular is amended to read in full as follows:

The novel strain of coronavirus, COVID-19, is believed to have been first identified in China in late 2019 and has spread globally. The rapid spread has resulted in authorities implementing numerous measures to try to contain the virus, such as travel bans and restrictions, quarantines, shelter in place orders and shutdowns. These measures may continue to impact all or portions of our workforce, operations, investors, suppliers and customers. We have taken steps to manage the effect of the pandemic on our corporate business and on the assets we manage which has included: (i) suspending any unnecessary capital improvements, unless for fire, life and safety; (ii) reducing food and beverage operations in accordance with government regulations; (iii) furloughing any non-essential employees; (iv) participating in the Paycheck Protection Plan program and other Small Business Administration and other governmental relief programs; and (v) having constant communications with lenders to receive additional facilities, convert current reserves into operational reserves and suspend the minimum debt service coverage ratio requirement for a 12 month period.

In recent weeks, the COVID-19 pandemic has also significantly increased economic uncertainty and has led to disruption and volatility in the global capital markets, which could increase the cost of and accessibility to capital. Given that the COVID-19 pandemic has caused a significant economic slowdown it appears increasingly likely that it could cause a global recession, which could be of an unknown duration. While the majority of our operations reside primarily in Arizona and the greater southwest region which has experienced a slower growth in the number of confirmed cases and deaths associated with COVID-19 as compared with more dense populations in the northeastern United States, a global recession would have a significant impact on our ongoing operations and cash flows.

On March 27, 2020, the Coronavirus Aid, Relief, and Economic Security Act (the “CARES Act”) was enacted. The CARES Act is an approximately $2 trillion emergency economic stimulus package in response to the COVID-19 pandemic, which among other things contains numerous income tax provisions. Some of these tax provisions are expected to be effective retroactively for years ending before the date of enactment. The Company is currently evaluating the implications of the Act.

The ultimate magnitude of COVID-19, including the extent of its impact on our financial and operational results, which could be material, will depend on the length of time that the pandemic continues, its effect on demand drivers for our investments, the extent to which it affects our ability to raise capital into our investment products, and the effect of governmental regulations imposed in response to the pandemic, as well as uncertainty regarding all of the foregoing.

In December 2017, the President signed the Tax Cuts and Jobs Act (“TCJA”), providing a significant overhaul to the U.S. federal tax code. We expect the TCJA to be a net positive impact to the U.S. economy. In particular, Congress established the Qualified Opportunity Zone program (the “QOZ Program”), which provides preferential tax treatment to taxpayers who invest eligible capital gains into qualified opportunity funds (“QOFs”). The Caliber Tax Advantaged Opportunity Zone Fund, LP is a QOF that has invested its capital into qualified opportunity zones (“QOZs”) and will continue to take advantage of this program. IRS and Treasury regulations are forthcoming, and we will continue to monitor and evaluate the interpretations as they are issued.

Our success at raising new capital into our funds is impacted by the extent to which new investors see alternative assets as a viable option for capital appreciation and/or income generation. The stock market remained volatile and unpredictable throughout 2019 and 2018 as evidenced by the Chicago Board of Exchange (Cboe) Volatility Index that reported variances in average market highs and lows between 55% and 75% during the years ended December 31, 2019 and 2018. As the markets continue to demonstrate unpredictable trends, we believe the increasing appetite for stable real assets will be a continuing trend.

Since our ability to raise new capital into our funds is dependent upon the availability and willingness of investors to direct their investment dollars into our products, our financial performance is sensitive in part to changes in overall economic conditions that affect investment behaviors. For example, the potential adverse effects of COVID-19 have resulted in an immediate and sharp slowdown in the U.S. economy which has created uncertainty as to the economic outlook. These factors could reduce the availability of investment dollars being allocated to alternative investments.

While we have had historical successes, there can be no assurance that fundraises for our new and existing funds will experience similar success. Our business depends in large part on our ability to raise capital from investors. If we were unable to raise such capital, we would be unable to collect management fees or deploy such capital into investments, which would materially reduce our revenues and cash flow and adversely affect our financial condition.

We remain confident about our ability to find, identify, and source new investment opportunities that meet the requirements and return profile of our investment funds despite headwinds associated with increased asset valuations, competition and increased overall cost of credit. We continue to identify strategic acquisitions on off-market terms and anticipate that this trend will continue as we begin to branch outside of Arizona. We are at a point in our deal cycle where some of our funds have begun to exit significant parts of their portfolios while other are approaching a potential harvesting phase. We have complemented these cycles with other newer funds that will maintain management fees while providing continued sources of activity for our construction and development segment. We expect this trend to continue through 2020, and therefore by the end of the year we expect management fees and construction fees to have increased year over year.

COVID-19 has caused public health officials to recommend precautions to mitigate the spread of the virus, that has caused us to recently shut down access to our corporate office and enact remote work arrangements for all our employees. Construction activities continue to be considered essential services under updated CDC guidelines; however, there is significant uncertainty surrounding the ultimate duration of these closures and whether government authorities will increase precautions by reducing activities that are considered essential. The impact of these temporary closures on our ability to generate and earn management fees remains uncertain and we may be limited in our ability to continue to complete our construction and development contracts during this period.

Acquiring new assets includes being able to negotiate favorable loans on both a short and long-term basis. We forecast and project our returns using assumptions about, among other things, the types of loans that we can expect the market to extend for a particular type of asset. This becomes more complex when the asset also requires construction financing. We may also need to refinance existing loans that are due to mature. Factors that affect these arrangements include the interest rate and economic environment, the estimated fair value of the real property, and the profitability of the asset’s historical operations. It is uncertain at this time what effect the COVID-19 pandemic will have on our ability to obtain favorable financing on our new and existing assets. For example, the potential adverse effects of COVID-19 across the U.S. market may be underestimated. The actual effects are dependent on many factors that may be beyond the control of the authorities in the United States. The potential adverse effects of any of these factors would likely result in greater economic uncertainty which would affect the credit and capital markets and might impact our access to capital resources at an affordable cost to meet our needs. These capital market conditions may affect the renewal or replacement of our credit agreements, some of which have maturity dates occurring within the next 12 months. The Company’s liquidity may be negatively impacted if leisure and business travel do not resume normal activities and the Company may be required to pursue additional sources of financing to meet its financial obligations. Obtaining such financing is not guaranteed and is largely dependent on market conditions and other factors.

The demand from investors is dependent upon the type of asset, the type of return it will generate (current cash flow, long term capital gains, or both) and the actual return earned by our Fund investors relative to other comparable or substitute products. General economic factors and conditions, including the general interest rate environment and unemployment rates, may affect an investor’s ability and desire to invest in real estate. For example, a significant interest rate increase could cause a projected rate of return to be insufficient after considering other risk exposures. Additionally, if weakness in the economy emerges and actual or expected default rates increase, investors in our Funds may delay or reduce their investments. However, we believe our approach to investing and the capabilities that Caliber manages throughout the deal cycle will continue to offer an attractive value proposition to investors.

COVID-19 is beginning to show downward pressure on the performance of our investment assets, most notably in hospitality and to a lesser extent multi-family. Future restrictions on leisure and business travel, the financial health of our tenants and their ability to pay rent, port closures and increased border controls or closures, could continue to limit the ability of our assets under management to generate positive cash flows and have a material adverse effect on our financial condition, cash flows and results of operations. There is no certainty that measures taken by government authorities will be sufficient to mitigate the risks posed by the virus, and our ability to perform critical functions could be harmed. In the near term, we anticipate that this will impact our ability to earn and collect carried interest on our respective asset’s operating cash flows; however, it is uncertain whether or not the impact of COVID-19 will have a prolonged or permanent impact on longer term asset valuations.

PART III

INDEX TO EXHIBITS

SIGNATURES

Pursuant to the requirements of Regulation A, the issuer certifies that it has reasonable grounds to believe that it meets all of the requirements for filing on Form 1-A and has duly caused this offering statement to be signed on its behalf by the undersigned, thereunto duly authorized, in the City of Scottsdale, State of Arizona, on May 26, 2020.

| CALIBERCOS INC. | |||

| By: | /s/ John C. Loeffler, II | ||

| Name: | John C. Loeffler, II | ||

| Title: | Chief Executive Officer | ||

This offering statement has been signed by the following persons in the capacities and on the dates indicated.

| Name and Signature | Title | Date |

| /s/ John C. Loeffler, II |

Chief Executive Officer and Chairman of the Board (Principal Executive Officer) |

May 26, 2020 |

| John C. Loeffler, II | ||

|

* |

Chief Operating Officer, Secretary and Director |

May 26, 2020 |

|

Jennifer Schrader

|

||

|

* |

Chief Financial Officer (Principal Financial and Accounting Officer) |

May 26, 2020 |

|

Jade Leung |

| * By: /s/ John C. Loeffler, II | Attorney-in-fact | May 26, 2020 |

| John C. Loeffler, II |