UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 [NO FEE REQUIRED] |

For the fiscal year ended December 31, 2006

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 [NO FEE REQUIRED] |

For the transition period from to

Commission file number 0-12255

YRC WORLDWIDE INC.

(Exact name of registrant as specified in its charter)

| Delaware | 48-0948788 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

| 10990 Roe Avenue, Overland Park, Kansas | 66211 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (913) 696-6100

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, $1 Par Value Per Share

(Title of class)

Securities registered pursuant to Section 12(g) of the Act:

NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by nonaffiliates of the registrant at June 30, 2006 was $2,420,908,490.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

| Class |

Outstanding at January 31, 2007 | |

| Common Stock, $1 Par Value Per Share | 57,209,694 shares |

DOCUMENTS INCORPORATED BY REFERENCE

The following documents are incorporated by reference into the Form 10-K:

1) Proxy Statement related to the 2007 Annual Meeting of Shareholders - Part III

YRC Worldwide Inc.

Form 10-K

Year Ended December 31, 2006

2

This entire annual report, including (among other items) “Item 7, Management’s Discussion of Analysis of Financial Condition and Results of Operations” and certain statements in the Notes to Consolidated Financial Statements contained in “Item 8, Financial Statements and Supplementary Data”, includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (each a “forward-looking statement”). Forward-looking statements include those preceded by, followed by or including the words “should,” “could,” “may,” “expect,” “believe,” “estimate” or similar expressions. Our actual results could differ materially from those projected by these forward-looking statements due to a number of factors, including (without limitation), inflation, inclement weather, price and availability of fuel, sudden changes in the cost of fuel or the index upon which the Company bases its fuel surcharge, competitor pricing activity, expense volatility, including (without limitation) expense volatility due to changes in rail service or pricing of rail service, ability to capture cost reductions, including (without limitation) those cost reduction opportunities arising from acquisitions, changes in equity and debt markets, a downturn in general or regional economic activity, effects of a terrorist attack, and labor relations, including (without limitation), the impact of work rules, work stoppages, strikes or other disruptions, any obligations to multi-employer health, welfare and pension plans, wage requirements and employee satisfaction.

Other factors as well as more details regarding certain of these factors are provided in greater detail in “Item 1A – Risk Factors”.

| Item 1. | Business |

General Description of the Business

YRC Worldwide Inc. (also referred to as “YRC Worldwide”, “the Company”, “we” or “our”), one of the largest transportation service providers in the world, is a holding company that through wholly owned operating subsidiaries offers its customers a wide range of transportation services. The Company adopted the name YRC Worldwide in January 2006 to reflect the fact that its services have expanded to encompass logistics as well as global, national and regional transportation. The YRC Worldwide portfolio of brands provides a comprehensive suite of services for the shipment of industrial, commercial and retail goods domestically and internationally. The brands operate independently in the marketplace, providing customers with a differentiated choice of services and providers. It is our strategy to allow each individual brand to develop its own franchise. We believe that this strategy can result in a greater share of market than we might create under a one brand approach. Additionally, we believe open competition in the marketplace strengthens our individual franchises to a greater extent than restricting the brands from such competition. Our operating subsidiaries, which are also our reportable segments, include the following:

| • | Yellow Transportation, Inc. (“Yellow Transportation”) is a leading transportation services provider that offers a full range of regional, national and international services for the movement of industrial, commercial and retail goods, primarily through centralized management and customer facing organizations. Approximately 44% of Yellow Transportation shipments are completed in two days or less. In addition to the United States, Yellow Transportation also serves parts of Canada, Mexico and Puerto Rico. |

| • | Roadway Express, Inc. (“Roadway”) is a leading transportation services provider that offers a full range of regional, national and international services for the movement of industrial, commercial and retail goods, primarily through regionalized management and customer facing organizations. Approximately 32% of Roadway shipments are completed in two days or less. Roadway owns 100% of Reimer Express Lines Ltd. (“Reimer”), located in Canada, that specializes in shipments into, across and out of Canada. |

| • | YRC Regional Transportation, Inc. (“Regional Transportation”) is a holding company for our transportation service providers focused on business opportunities in the regional and next-day delivery markets. Regional Transportation is comprised of New Penn Motor Express, Inc. (“New Penn”), USF Holland Inc. and USF Reddaway Inc., which provide regional, next-day ground services through a network of facilities located across the United States (“U.S.”); Quebec, Canada; Mexico and Puerto Rico. USF Glen Moore Inc., a provider of truckload services throughout the U.S., is also a subsidiary of Regional Transportation. Approximately 90% of Regional Transportation LTL shipments are completed in two days or less. In 2006, Regional Transportation also included USF Bestway Inc. In February 2007, we consolidated the majority of USF Bestway’s operations into USF Reddaway. |

3

| • | Meridian IQ, Inc. (“Meridian IQ”) is a global logistics management company that plans and coordinates the movement of goods worldwide to provide customers a single source for logistics management solutions. Meridian IQ delivers a wide range of global logistics management services, with the ability to provide customers improved return-on-investment results through flexible, fast and easy-to-implement logistics services and technology management solutions. |

In January 2007, we announced organizational changes that bring the management of Yellow Transportation and Roadway under one organization established as YRC National Transportation. Accordingly, beginning in 2007 we will combine these previously separate segments into one.

For revenue and other information regarding these segments, see the Business Segments note under “Item 8, Financial Statements and Supplementary Data”.

Incorporated in Delaware in 1983 and headquartered in Overland Park, Kansas, we employed approximately 66,000 people as of December 31, 2006. The mailing address of our headquarters is 10990 Roe Avenue, Overland Park, Kansas 66211, and our telephone number is (913) 696-6100. Our website is www.yrcw.com. Through the “SEC Filings” link on our website, we make available the following filings as soon as reasonably practicable after they are electronically filed with or furnished to the Securities and Exchange Commission (“SEC”): our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended. All of these filings may be viewed or printed from our website free of charge.

4

Narrative Description of the Business

Operating Units

Yellow Transportation

Yellow Transportation offers a full range of services for the movement of industrial, commercial, and retail goods and provides transportation services by moving shipments through its regional, national and international networks of service centers, utilizing primarily ground transportation equipment that we own or lease. The Yellow Transportation mission is to be the leading provider of guaranteed, time-definite, defect-free, hassle-free transportation services for business customers worldwide. Yellow Transportation addresses the increasingly complex transportation needs of its customers through service offerings such as:

| • | Exact Express® – a premium expedited and time-definite ground service with an industry-leading 100% satisfaction guarantee; |

| • | Definite Delivery® – a guaranteed on-time service with constant shipment monitoring and proactive notification; |

| • | Standard Ground™ – a ground service with complete coverage of North America; |

| • | Expedited Direct™ – an expedited air forwarding solution for one, two and three-day shipments; |

| • | MyYellow®.com – a leading edge e-commerce web site offering secure and customized online resources to manage transportation activity. |

Yellow Transportation provides transportation services for various categories of goods, which may include (among others) apparel, appliances, automotive parts, chemicals, food, furniture, glass, machinery, metal, metal products, non-bulk petroleum products, rubber, textiles, wood and other manufactured products or components. Yellow Transportation provides both less-than-truckload (“LTL”) and truckload service. Most of Yellow Transportation’s deliveries are LTL service; however, Yellow Transportation also offers truckload services to complement the LTL services, usually to fill back hauls and maximize equipment utilization. Back haul is the process of moving trailers (often empty or partially full) back to their destination after a delivery.

Yellow Transportation, founded in 1924, serves more than 300,000 manufacturing, wholesale, retail and government customers throughout North America. Operating from 330 strategically located facilities with 13,414 doors, Yellow Transportation provides service throughout North America, including within Puerto Rico and Hawaii. The Yellow Transportation affiliates, YRC Services, S. de R.L. de C.V. and Yellow Transportation of Ontario, Inc. and Yellow Transportation of British Columbia, Inc., provide services in Mexico and Canada, respectively. Yellow Transportation’s shipments have an average shipment size of 1,200 pounds and travel an average distance of roughly 1,200 miles.

As of December 31, 2006, approximately 22,000 Yellow Transportation employees are dedicated to operating its system, which supports 280,000 shipments in transit at any time. An operations research and engineering team is responsible for the equipment, routing, sequencing and timing of nearly 64 million miles per month. At December 31, 2006, Yellow Transportation had 7,967 owned tractors, 648 leased tractors, 32,982 owned trailers and 769 leased trailers.

Based in Overland Park, Kansas, Yellow Transportation accounted for 35% of our total operating revenue in 2006, 39% of our total operating revenue in 2005 and 47% of our total operating revenue in 2004.

Roadway

Founded in 1930, Roadway serves more than 300,000 manufacturing, wholesale, retail and government customers throughout North America through its extensive network of 336 service centers with 13,480 doors located throughout North America. Roadway offers long-haul, interregional and regional LTL transportation services on two-day and longer lanes and is a leading transporter of industrial, commercial and retail goods with a variety of innovative services designed to meet customer needs. Roadway provides seamless, general commodity freight service among all 50 states, Canada, Mexico and Puerto Rico, and offers import and export services to more than 100 additional countries worldwide through offshore agents. Reimer Express Lines, a subsidiary of Roadway, provides service in Canada, and the Roadway affiliate, YRC Services, S. de R.L. de C.V, provides services in Mexico. Roadway’s shipments have an average shipment size of 1,200 pounds and travel an average distance of roughly 1,200 miles.

5

Roadway provides transportation services for similar categories of goods as those that Yellow Transportation delivers. Roadway primarily offers LTL service yet also offers truckload services to complement its LTL service, usually to fill back hauls and maximize equipment utilization. In addition, Roadway provides higher margin specialized services, including guaranteed expedited services, time-specific delivery, North American international services, coast-to-coast air delivery, sealed trailers, product returns, cold-sensitive protection and government material shipments. The Roadway suite of time-based services provides customers the flexibility to choose next day and beyond service on the ground or in the air at any hour, day or night, anywhere across North America with extreme reliability. These service offerings include:

| • |

Time-Critical™ Service – a premium expedited and time-definite service via ground or air anywhere in North America with a 100% on-time guarantee, delivery windows as precise as one hour, and options to charter partial or entire aircraft. |

| • |

Time-Critical™ Multi-Day Window Service – a service option providing customers the ability to select any size multiple day delivery window and is guaranteed not to deliver early or late. Multi-Day Window service is ideal for vendors shipping to retailers trying to avoid costly charge-backs when faced with strict window delivery requirements. |

| • |

Time-Advantage™ Service – Roadway’s newest expedited service option providing customers the ability to pick the speed to match their need on the ground or in the air anywhere throughout North America. |

| • |

Sealed Divider™ – a patented, dedicated service providing extra protection and verifiable security in transit through a numbered rod-lock seal system with customers paying only for the space used on the trailer. |

| • | My.Roadway.com – a secure e-commerce web site offering online resources for shipment visibility and management in real time. |

Roadway employed approximately 22,000 employees as of December 31, 2006. At that date, it owned 6,807 tractors and 27,268 trailers and leased 2,064 tractors and 3,183 trailers. Headquartered in Akron, Ohio, Roadway accounted for 34% of our total operating revenue in 2006, 38% of our total operating revenue in 2005 and 46% of our total operating revenue in 2004.

Reimer Express Lines

Founded in 1952, Reimer, a wholly owned subsidiary of Roadway, offers Canadian shippers a selection of direct connections within Canada, throughout North America and around the world. Its network and information systems are completely integrated with those of Roadway. Integration with Roadway enables Reimer to provide seamless cross-border services between Canada, Mexico and the U.S.

YRC Regional Transportation

Regional Transportation is comprised of New Penn, USF Glen Moore, USF Holland and USF Reddaway. In 2006, Regional Transportation also included USF Bestway Inc. In February 2007, we consolidated the majority of USF Bestway’s operations into USF Reddaway. Together, the Regional Transportation companies deliver services in the next-day, second-day and time-sensitive markets nationwide, which are among the fastest-growing transportation segments. The Regional Transportation service portfolio includes:

| • | Regional delivery – including next-day local area delivery and second-day services; consolidation/distribution services; protect-from-freezing and hazardous materials handling; and a variety of other specialized offerings. |

| • | Expedited delivery – including day-definite, hour-definite and time definite capabilities. |

| • | Truckload delivery – including regional, national, dedicated and team-based services. |

| • | Inter-regional delivery – combining our best-in-class regional networks with reliable sleeper teams, Regional Transportation provides reliable, high-value services between our regional operations. |

| • | Cross-border delivery – through strategic partnerships, the Regional Transportation companies provide full-service capabilities between the U.S. and Canada, Mexico and Puerto Rico. |

| • | USFNet.com and NewPenn.com – are both leading edge e-commerce web sites offering secure and customized online resources to manage transportation activity. |

6

The Regional Transportation companies are described as follows:

| • | New Penn Motor Express, headquartered in Lebanon, Pennsylvania, provides local next-day, day-definite, and time-definite services through a network of 23 service centers with 1,213 doors located in the Northeastern United States; Quebec, Canada; and Puerto Rico. New Penn employs over 2,000 people and owns and operates a fleet of nearly 900 tractors and 1,800 trailers. |

| • | USF Glen Moore, headquartered in Carlisle, Pennsylvania, provides spot, dedicated and single-source customized truckload services through the use of company and team-based drivers. USF Glen Moore has two primary domiciles located in Carlisle, Pennsylvania, and Knoxville, Tennessee. USF Glen Moore employs over 750 people and owns and operates a fleet of over 800 tractors and 2,700 trailers. |

| • | USF Holland, headquartered in Holland, Michigan, provides local next-day, regional and expedited services through a network of 74 service centers with 4,542 doors located in the Midwestern, Southeastern and portions of the Northeast United States. They also provide service to the provinces of Ontario and Quebec, Canada. USF Holland employs over 9,500 people and owns and operates a fleet of over 5,000 tractors and 9,000 trailers. |

| • | USF Reddaway, headquartered in Clackamas, Oregon, provides local next-day, regional and expedited services through a network of 57 service centers with 1,309 doors located in California, the Pacific Northwest, and the Rocky Mountain States. Additionally USF Reddaway provides services to Alaska and to the provinces of Alberta and British Columbia, Canada. USF Reddaway employs over 2,800 people and owns and operates a fleet of over 1,300 tractors and 4,000 trailers. |

| • | USF Bestway, headquartered in Scottsdale, Arizona, provided next-day, regional and expedited services through a network of 55 service centers with 1,454 doors located in the Southwest and Midwest areas. In February 2007, we consolidated the majority of USF Bestway’s operations into USF Reddaway. USF Bestway employed over 2,200 people and owned and operated a fleet of over 1,000 tractors and 3,400 trailers. Most of these employees now work for USF Reddaway, and most of this equipment is now utilized by USF Reddaway and USF Holland. The new USF Reddaway, headquartered in Clackamas, Oregon, provides local next-day, regional and expedited services through a network of 94 service centers with 2,441 doors throughout the entire Northwest and Southwest United States. Additionally, USF Reddaway provides services to Alaska and to the provinces of Alberta and British Columbia, Canada. USF Reddaway employs over 4,700 people and owns and operates a fleet of over 2,300 tractors and 7,700 trailers. |

The Regional Transportation companies serve more than 200,000 manufacturing, wholesale, retail and government customers throughout North America. Regional Transportation’s 17,000 employees are dedicated to supporting the delivery of over 15.6 million shipments annually. In addition to over 371 local, company-based sales executives, Regional Transportation has 20 corporate account managers who provide corporate sales services to the entire group of companies. In 2006, each of our four companies was recognized with the prestigious Quest for Quality award by the readers of Logistics Management magazine.

Headquartered in Fairlawn, Ohio, the Regional Transportation companies accounted for 25% of our total operating revenue in 2006, 18% of the total operating revenue in 2005 and New Penn, prior to the creation of Regional Transportation upon the acquisition of USF in 2005, accounted for 4% of our operating revenue in 2004.

Meridian IQ

Meridian IQ is a global logistics management company that plans and coordinates the movement of goods worldwide to provide customers a single source for logistics management solutions. Meridian IQ arranges for and expedites the movement of goods and materials through the supply chain. With the May 2005 acquisition of USF Corporation, Meridian IQ has integrated the USF Logistics business, expanding the breadth and depth of our service offering.

Meridian IQ delivers a wide range of global logistics management services, with the ability to provide customers improved return-on-investment results through flexible, fast and easy-to-implement logistics services and technology management solutions. Meridian IQ has approximately 18,000 transactional and 350 contractual customers.

Meridian IQ offers the following services:

| • | International supply chain services - arranging for the administration, transportation and delivery of goods worldwide; |

| • | Multi-modal brokerage services - providing companies with daily shipment needs with access to volume capacity and specialized equipment at competitive rates; |

| • | Domestic forwarding and expedited services - arranging guaranteed, time-definite transportation for companies within North America requiring time-sensitive delivery options and guaranteed reliability; |

7

| • | Transportation solutions and technology management - web-native transportation management systems enabling customers to manage their transportation network centrally with increased efficiency and visibility. When combined with network consulting and operations management any organization, regardless of size, can outsource transportation functions partially or even entirely with Meridian IQ; and |

| • | Flow-thru distribution, dedicated fleet and dedicated warehouse services - solutions that deliver advance technology, effective facility layouts and efficient operations that maximize product flow, improving cycle-time and cost effectiveness. |

At December 31, 2006, Meridian IQ had more than 2,700 employees, including 2,300 located in North America, 200 located in Asia, 75 located in Latin America, and 130 located in Europe (predominately in the United Kingdom). Based in Overland Park, Kansas, Meridian IQ accounted for 6% of our total operating revenue in 2006, 5% of our total operating revenue in 2005 and 3% of our total operating revenue in 2004.

Shared Services

We have three wholly owned subsidiaries that provide shared support services across the YRC Worldwide enterprise. These are YRC Worldwide Technologies, YRC Worldwide Enterprise Services, and YRC Assurance Co. Ltd (“YRC Assurance”).

YRC Worldwide Technologies is headquartered in Overland Park, Kansas and has approximately 600 employees. YRC Worldwide Technologies and Meridian IQ together provide hosting, infrastructure services and managed transportation business systems development.

YRC Worldwide Enterprise Services, headquartered in Overland Park, Kansas, provides a variety of support services including payroll, cash disbursements and cash receipts through common resources to the consolidated group. This entity employs approximately 1,100 people.

YRC Assurance Co. Ltd., is a captive insurance company domiciled in Bermuda and a wholly owned and consolidated subsidiary of YRC Worldwide Inc. YRC Assurance provides insurance services to certain wholly owned subsidiaries of YRC Worldwide.

In addition, YRC Worldwide provides certain services to its subsidiaries such as legal, risk management, finance and coordination services.

In January 2007, we announced the formation of YRC Enterprise Solutions Group. YRC Enterprise Solutions Group will provide sales and marketing services to our operating subsidiaries for an identified group of large accounts who desire to buy services from more than one of these operating subsidiaries in a coordinated manner.

Each of our shared services organizations charges the operating companies for their services, either based upon usage or on an overhead allocation basis.

Competition

Customers have a wide range of choices. The companies of YRC Worldwide believe that overall brand strategy, service quality, technology, a broad service portfolio, responsiveness and flexibility are important competitive differentiators.

Few U.S.-based transportation companies offer comparable transportation and logistics capabilities. By integrating traditional ground, expedited, air, ocean and managed transportation capabilities, we provide business organizations with a single source answer to shipping challenges globally. Our market studies show a continued preference among customers for transportation logistics providers based on “service value”, which is the relationship between overall quality and price. We believe that we can compete against any transportation and logistics competitor from a value perspective.

Yellow Transportation, Roadway, Regional Transportation, and Meridian IQ operate in a highly competitive environment against a wide range of transportation and logistics service providers. These competitors include global, integrated transportation services providers; global forwarders; national transportation services providers; regional or interregional providers; and small, intraregional transportation companies. The companies of YRC Worldwide also compete against providers within several modes of transportation including: less-than-truckload, truckload, air and ocean cargo, rail, transportation consolidators and privately owned fleets.

8

Ground-based transportation includes private fleets and two “for-hire” carrier groups. The private carrier segment consists of fleets that companies who move their own goods own and operate. The two “for-hire” groups are based on typical shipment sizes that transportation service companies handle. Truckload refers to providers transporting shipments that generally fill an entire 48 or 53 foot trailer, and less-than-truckload or ‘shared load’ refers to providers transporting goods from multiple shippers in a single load that would not fill a full-sized trailer on their own.

Shared load or LTL transportation providers consolidate numerous orders generally ranging from 100 to 10,000 pounds from varying businesses into individual service centers within close proximity to where those shipments originated. Utilizing expansive networks of pickup and delivery operations around these local service centers, shipments are moved between origin and destination utilizing distribution centers when necessary, where consolidation and deconsolidation of loads occurs. Depending on the distance shipped, shared load providers (asset and non-asset based) are often classified into one of four sub-groups:

| • | Regional - Average distance is typically less than 500 miles with a focus on one- and two-day delivery times. Regional transportation companies can move shipments directly to their respective destination centers, which increases service reliability and avoids costs associated with intermediate handling. |

| • | Interregional - Average distance is usually between 500 and 1,000 miles with a focus on two- and three-day delivery times. There is a competitive overlap between regional and national providers in this category as each group sees the interregional segment as a growth opportunity, and there are no providers focusing exclusively on this sector. |

| • | National - Average distance is typically in excess of 1,000 miles with focus on two- to five-day delivery times. National providers rely on interim shipment handling through a network of terminals, which require numerous satellite service centers, multiple distribution centers, and a relay network. To gain service and cost advantages, they often ship directly between service centers, minimizing intermediate handling. |

| • | Global - providing freight forwarding and final mile delivery services to companies shipping to and from multiple regions around the world. This service can be offered through a combination of owned assets or through a purchased transportation or third-party logistics model. |

Competitive cost of entry into the asset-based LTL sector on a small scale, within a limited service area, is relatively small (although more than in other sectors of the transportation industry). The larger the service area, the greater the barriers to entry, due primarily to the need for additional equipment and facilities associated with broader geographic service coverage. Broader market coverage in the competitive transportation landscape also requires increased technology investment and the ability to capture cost efficiencies from shipment density (scale), making entry on a national basis more difficult.

Yellow Transportation, Roadway, and Meridian IQ (through transportation management services) provide service in all four sub-groups. Regional Transportation competes in the regional, interregional and national transportation marketplace. Each brand competes against a number of providers in these markets from small firms with one or two vehicles, to global competitors with thousands of physical assets.

The competition specifically for Meridian IQ includes all of the same types of providers mentioned previously in addition to transportation management systems providers, domestic and international freight forwarders, freight brokers, warehouse management providers, and third party logistics companies.

Regulation

Yellow Transportation, Roadway, Regional Transportation and other interstate carriers were substantially deregulated following the enactment of the Motor Carrier Act of 1980, the Trucking Industry Regulatory Reform Act of 1994, the Federal Aviation Administration Authorization of 1994 and the ICC Termination Act of 1995. Prices and services are now largely free of regulatory controls, although the states retained the right to require compliance with safety and insurance requirements, and interstate motor carriers remain subject to regulatory controls that agencies within the U.S. Department of Transportation impose.

Our operating companies are subject to regulatory and legislative changes, which can affect our economics and those of our competitors. Various state agencies regulate us, and our operations are also subject to various federal, foreign, state, provincial and local environmental laws and regulations dealing with transportation, storage, presence, use, disposal and handling of hazardous materials, discharge of storm-water and underground fuel storage tanks.

We are also subject to regulations to combat terrorism that the Department of Homeland Security and other agencies impose.

9

We believe that our operations are in substantial compliance with current laws and regulations.

We further describe our operations in “Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations”, of this report.

Environmental Matters

Our operations are subject to U.S. federal, foreign, state, provincial and local regulations with regard to air and water quality and other environmental matters. We believe that we are in substantial compliance with these regulations. Regulation in this area continues to evolve and changes in standards of enforcement of existing regulations, as well as the enactment and enforcement of new legislation may require us and our customers to modify, supplement or replace equipment or facilities or to change or discontinue present methods of operation.

During 2006, we spent approximately $5.3 million to comply with U.S. federal, state and local provisions regulating the discharge of materials into the environment or otherwise relating to the protection of the environment (collectively, “Environmental Regulations”). In 2007, we expect to spend approximately $5.8 million to comply with the Environmental Regulations. Based upon current information, we believe that our compliance with Environmental Regulations will not have a material adverse effect upon our capital expenditures, results of operation and competitive position because we have either made adequate reserves for such compliance expenditures or the cost for such compliance is expected to be small in comparison with our overall net worth.

We estimate that we will incur approximately $1.0 million in capital expenditures for environmental control equipment during 2007. We believe that capital expenditures for environmental control equipment for 2007 will not have a material adverse effect upon our financial condition because the aggregate amount of these expenditures is expected to be immaterial.

The Comprehensive Environmental Response, Compensation and Liability Act (known as the “Superfund Act”) imposes liability for the release of a “hazardous substance” into the environment. Superfund liability is imposed without regard to fault and even if the waste disposal was in compliance with the then current laws and regulations. With the joint and several liability imposed under the Superfund Act, a potentially responsible party (“PRP”) may be required to pay more than its proportional share of such environmental remediation. Several of our subsidiaries have been identified as PRPs at various sites discussed below. The U.S. Environmental Protection Agency (the “EPA”) and appropriate state agencies are supervising investigative and cleanup activities at these sites. The EPA has identified Yellow Transportation as a PRP for four locations: Ilada Waste Co., a site at Dupo, IL; Alburn Incinerator, Inc., Chicago, IL; Mercury Refinery, Albany, NY and IWI, Inc., Summit, IL. We estimate that the combined potential costs at these sites will not exceed $0.1 million. With respect to these sites, it appears that Yellow Transportation delivered minimal amounts of waste to these sites, which is de minimis in relation to other respondents. The EPA has identified Roadway as a PRP for five locations: Operating Industries Site, Monterey Park, CA; BEMS Landfill, Mt. Holly, NJ; Double Eagle Site, Oklahoma City, OK; Jones Industrial, South Brunswick, NJ and Berry’s Creek, Carlstadt, NJ. We estimate that combined potential costs at the first four sites will not exceed $0.6 million. The EPA has notified Roadway and 140 other potential parties of their potential responsibility status at the Berry’s Creek site where Roadway owns and operates a service center in the watershed area that discharges into Berry’s Creek. We estimate the Berry’s Creek potential cost to be $0.6 million. The EPA has identified USF Red Star, a non-operating subsidiary, as a PRP at six locations: Champion Chemical, Malboro, NJ; Booth Oil, N. Tonanwanda, NJ; Quanta Resources, Syracuse, NY and three separate landfills in Byron, NJ, Moira, NY and Palmer, MA. We believe the potential combined costs at these sites to be $0.4 million. The EPA has identified New Penn as a PRP for one location, Pennsauken Landfill, Pennsauken, NJ. We believe the potential cost at this site to be immaterial.

While PRPs in Superfund actions have joint and several liabilities for all costs of remediation, it is not possible at this time to quantify our ultimate exposure because the projects are either in the investigative or early remediation stage. Based upon current information, we do not believe that probable or reasonably possible expenditures in connection with the sites described above are likely to have a material adverse effect on our results of operations because:

| • | To the extent necessary, we have established adequate reserves to cover the estimate we presently believe will be our liability with respect to the matter; |

| • | We and our subsidiaries have only limited or de minimis involvement in the sites based upon a volumetric calculation; |

| • | Other PRPs involved in the sites have substantial assets and may reasonably be expected to pay their share of the cost of remediation; |

| • | We have adequate resources to cover the ultimate liability; and |

10

| • | We believe that our ultimate liability is small compared with our overall net worth. |

We are subject to various other governmental proceedings and regulations, including foreign regulations, relating to environmental matters, but we do not believe that any of these matters are likely to have a material adverse effect on our financial condition or results of operation.

This section, “Environmental Matters,” contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. The words “believe”, “expect”, “estimate”, “may” and similar expressions are intended to identify forward-looking statements. Our expectations regarding our compliance with Environmental Regulations and our expenditures to comply with Environmental Regulations, including (without limitation) our capital expenditures on environmental control equipment, and the effect that liability from Environmental Regulation or Superfund sites may have on our financial condition or results of operations, are only our forecasts regarding these matters. These forecasts may be substantially different from actual results, which may be affected by the following factors: changes in Environmental Regulations; unexpected, adverse outcomes with respect to sites where we have been named as a PRP, including (without limitation) the sites described above; the discovery of new sites of which we are not aware and where additional expenditures may be required to comply with Environmental Regulations; an unexpected discharge of hazardous materials in the course of our business or operations; an acquisition of one or more new businesses; a catastrophic event causing discharges into the environment of hydrocarbons; the inability of other PRPs to pay their share of liability for a Superfund site; and a material change in the allocation to us of the volume of discharge and a resulting change in our liability as a PRP with respect to a site.

Economic Factors and Seasonality

Our business is subject to a number of general economic factors that may have a materially adverse effect on the results of our operations, many of which are largely out of our control. These include recessionary economic cycles and downturns in customers’ business cycles, particularly in market segments and industries, such as retail and manufacturing, where we have a significant concentration of customers. Economic conditions may adversely affect our customers’ business levels, the amount of transportation services they need and their ability to pay for our services. We operate in a highly price-sensitive and competitive industry, making pricing, customer service, effective asset utilization and cost control major competitive factors. Yellow Transportation, Roadway, Regional Transportation and Meridian IQ revenues are subject to seasonal variations. Customers tend to reduce shipments after the winter holiday season, and operating expenses as a percent of revenue tend to be higher in the winter months primarily due to colder weather. Generally, the first quarter is the weakest while the third quarter is the strongest. The availability and cost of labor can significantly impact our cost structure and earnings.

Financial Information About Geographic Areas

Our revenue from foreign sources is largely derived from Canada, the United Kingdom, Asia and Mexico. We have certain long-lived assets located in these countries as well. We discuss this information in the “Business Segments” note under “Item 8, Financial Statements and Supplementary Data”, of this report.

| Item 1A. | Risk Factors |

We are subject to general economic factors that are largely out of our control, any of which could significantly reduce our operating margins and income.

Our business is subject to a number of general economic factors that may significantly reduce our operating margins and income, many of which are largely out of our control. These include recessionary economic cycles and downturns in customers’ business cycles and changes in their business practices, particularly in market segments and industries, such as retail and manufacturing, where we have a significant concentration of customers. Economic conditions may adversely affect our customers’ business levels, the amount of transportation services they need and their ability to pay for our services. Customers encountering adverse economic conditions represent a greater potential for loss, and we may be required to increase our reserve for bad-debt losses.

The transportation industry is affected by business risks and increasing costs that are largely out of our control, any of which could significantly reduce our operating margins and income.

Businesses operating in the transportation industry are affected by risks and costs increases that are largely out of our control, any of which could significantly reduce our operating margins and income. These factors include weather, excess capacity in the transportation industry, interest rates, fuel prices and taxes, fuel surcharge collection, terrorist attacks, license and registration fees, insurance premiums and self-insurance levels, difficulty in recruiting and retaining qualified drivers, the risk of outbreak of epidemical illnesses, the risk of widespread disruption of our technology systems, and increasing equipment and operational costs.

11

Our results of operations may also be affected by seasonal factors. Because of our self-insurance program, we may be required to accrue or pay additional amounts if the number and severity of claims is greater than originally estimated.

We operate in a highly competitive industry, and our business will suffer if we are unable to adequately address potential downward pricing pressures and other factors that may adversely affect our operations and significantly reduce our operating margins and income.

Numerous competitive factors could impair our ability to maintain our current profitability. These factors include the following:

| • | We compete with many other transportation service providers of varying sizes, some of which have a lower cost structure, more equipment and greater capital resources than we do or have other competitive advantages. |

| • | Some of our competitors periodically reduce their prices to gain business, especially during times of reduced growth rates in the economy, which limits our ability to maintain or increase prices or maintain significant growth in our business. |

| • | Our customers may negotiate rates or contracts that minimize or eliminate our ability to continue to offset fuel price increases through a fuel surcharge on our customers. |

| • | Many customers reduce the number of carriers they use by selecting so-called “core carriers” as approved transportation service providers, and in some instances, we may not be selected. |

| • | Many customers periodically accept bids from multiple carriers for their shipping needs, and this process may depress prices or result in the loss of some business to competitors. |

| • | The trend towards consolidation in the ground transportation industry may create other large carriers with greater financial resources and other competitive advantages relating to their size. |

| • | Advances in technology require increased investments to remain competitive, and our customers may not be willing to accept higher prices to cover the cost of these investments. |

| • | Competition from non-asset-based logistics and freight brokerage companies may adversely affect our customer relationships and prices. |

If our relationship with our employees were to deteriorate, we may be faced with labor disruptions or stoppages, which could adversely affect our business and reduce our operating margins and income and place us at a disadvantage relative to non-union competitors.

Virtually all of our operating subsidiaries have employees who are represented by the International Brotherhood of Teamsters (the “IBT”). These employees represent approximately 70% of our workforce.

Each of Yellow Transportation, Roadway, New Penn and USF Holland employ most of their unionized employees under the terms of a common national master agreement as supplemented by additional regional supplements and local agreements. This current five-year agreement will expire on March 31, 2008. Other unionized employees are employed pursuant to more localized agreements. The IBT represents a number of employees at USF Reddaway under these localized agreements, which have wages, benefit contributions and other terms and conditions that better fit the cost structure and operating models of these business units.

Certain of our subsidiaries are regularly subject to grievances, arbitration proceedings and other claims concerning alleged past and current non-compliance with applicable labor law and collective bargaining agreements.

Neither we nor any of our subsidiaries can predict the outcome of any of the actions, activities or claims discussed above. These actions, activities and claims, if resolved in a manner unfavorable to us, could have a material adverse effect on our financial condition, businesses and results of operations.

Ongoing insurance and claims expenses could significantly reduce our income.

Our future insurance and claims expenses might exceed historical levels, which could significantly reduce our earnings. We currently self-insure for a portion of our claims exposure resulting from cargo loss, personal injury, property damage and workers’ compensation. If the number or severity of claims for which we are self-insured increases, our earnings could be significantly reduced.

12

We will have significant ongoing capital requirements that could reduce our income if we are unable to generate sufficient cash from operations.

The transportation industry is capital intensive. If we are unable to generate sufficient cash from operations in the future, we may have to limit our growth, enter into additional financing arrangements or operate our revenue equipment for longer periods, any of which could reduce our income. Revenue equipment includes, among other things, tractors and trailers. Our ability to incur additional indebtedness could be adversely affected by any increase in requirements that we post letters of credit in support of our insurance policies. See “—Ongoing insurance and claims expenses could significantly reduce our income”. If needed, additional credit capacity to support letters of credit may not be available on terms acceptable to us.

We operate in an industry subject to extensive government regulations, and costs of compliance with, or liability for violation of, existing or future regulations could significantly increase our costs of doing business.

The U.S. Departments of Transportation and Homeland Security and various federal, state, local and foreign agencies exercise broad powers over our business, generally governing such activities as authorization to engage in motor carrier operations, safety and permits to conduct transportation business. We may also become subject to new or more restrictive regulations imposed by the Departments of Transportation and Homeland Security, the Occupational Safety and Health Administration or other authorities relating to engine exhaust emissions, the hours of service that our drivers may provide in any one time period, security and other matters. Compliance with these regulations could substantially impair equipment productivity and increase our costs.

The Environmental Protection Agency has issued regulations that require progressive reductions in exhaust emissions from diesel engines through 2010. These reductions began with diesel engines manufactured late in 2002. The regulations currently include subsequent reductions in the sulfur content of diesel fuel in 2006 and the introduction of emissions after-treatment devices on newly manufactured engines in 2007. In 2010 further measures will be required by the EPA, most likely involving additional emissions after treatment devices. These devices will be required for new vehicles manufactured 2010 and after. These regulations could result in higher prices for tractors and increased fuel and maintenance costs.

We are subject to various environmental laws and regulations, and costs of compliance with, or liabilities for violations of, existing or future regulations could significantly increase our costs of doing business.

Our operations are subject to environmental laws and regulations dealing with, among other things, the handling of hazardous materials, underground fuel storage tanks and discharge and retention of stormwater. We operate in industrial areas, where truck terminals and other industrial activities are located, and where groundwater or other forms of environmental contamination may have occurred. Our operations involve the risks of fuel spillage or seepage, environmental damage, and hazardous waste disposal, among others. If we are involved in a spill or other accident involving hazardous substances, or if we are found to be in violation of applicable laws or regulations, it could significantly increase our cost of doing business. Under specific environmental laws, we could be held responsible for all of the costs relating to any contamination at our past or present terminals and at third party waste disposal sites. If we fail to comply with applicable environmental regulations, we could be subject to substantial fines or penalties and to civil and criminal liability.

The IRS may issue an adverse tax determination concerning a deduction taken by USF (purchased by the Company in May 2005) in connection with its disposition of USF Worldwide.

In 2002, USF Corporation deducted a loss for its worthless investment in the stock of its subsidiary USF Worldwide upon the disposition of that stock for no consideration. IRS has concluded that that deduction should be treated as a capital loss (because IRS questions whether the stock was totally worthless) which would not be fully deductible in 2002 or any other open tax year. We have protested that adjustment and requested an Appeals conference. The additional tax that could result should the loss ultimately be treated as a capital loss is approximately $50 million. USF established a reserve of approximately $19 million prior to our acquisition which has since been adjusted to approximately $18 million. We believe treatment as an ordinary loss is appropriate but have elected to retain the reserve previously established until resolution with the IRS is reached. An acceptable resolution may require litigation. Any tax liability other than $18 million would be an adjustment to the goodwill recorded in the purchase price allocation for the USF acquisition.

We may be obligated to make additional contributions to multi-employer pension plans.

Yellow Transportation, Roadway, New Penn, USF Holland and USF Reddaway contribute to approximately 20 separate multi-employer pension plans for employees that our collective bargaining agreements cover (approximately 70% of total YRC Worldwide employees). The largest of these plans, the Central States Southeast and Southwest Areas Pension Plan (the “Central States Plan”), provides retirement benefits to approximately 41% of our total employees. Our labor agreements with the IBT determine the amounts of these contributions. The pension plans provide defined benefits to retired participants. We recognize as net pension cost the contractually required contribution for the period and recognize as a liability any contributions due and unpaid.

13

We do not directly manage multi-employer plans. The trusts covering these plans are generally managed by trustees, half of whom the IBT appoints and half of whom various contributing employers appoint.

Under current law regarding multi-employer pension plans, a termination, withdrawal or significant partial withdrawal from any multi-employer plan in an under-funded status would render us liable for a proportionate share of the multi-employer plans’ unfunded vested liabilities. This potential unfunded pension liability also applies to other contributing employers, including our unionized competitors who contribute to multi-employer plans. The plan administrators and trustees do not routinely provide us with current information regarding the amount of each multi-employer pension plan’s funding. However, based on publicly available information, which is often dated, and on the limited information available from plan administrators or plan trustees, which we cannot independently validate, we believe that our portion of the contingent liability in the case of a full withdrawal or termination from all of the multi-employer pension plans to which we contribute would be in a range from $3.0 billion to $4.0 billion on a pre-tax basis. The increase in this estimated range from 2005 reflects a change by the Central States Plan to a more current mortality table in the determination of their unfunded vested benefit liability. Yellow Transportation, Roadway and the applicable subsidiaries of Regional Transportation have no current intention of taking any action that would subject us to withdrawal obligations. If the company did incur withdrawal liabilities, those amounts would generally be payable over periods of up to 20 years.

In 2006, the Pension Protection Act became law and modified both the Internal Revenue Code (as amended, the “Code”) as it applies to multi-employer pension plans and the Employment Retirement Income Security Act of 1974 (as amended, “ERISA”). The Code and ERISA (in each case, as so modified) and related regulations establish minimum funding requirements for multi-employer pension plans. The funding status of these plans is determined by the following factors:

| • | the number of participating active and retired employees |

| • | the number of contributing employers |

| • | the amount of each employer’s contractual contribution requirements |

| • | the investment returns of the plans |

| • | plan administrative costs |

| • | the number of employees and retirees participating in the plan who no longer have a contributing employer |

| • | the discount rate used to determine the funding status |

| • | the actuarial attributes of plan participants (such as age, estimated life and number of years until retirement) |

If any of our multi-employer pension plans fails to:

| • | meet minimum funding requirements |

| • | meet a required funding improvement or rehabilitation plan that the Pension Protection Act may require for certain of our underfunded plans |

| • | obtain from the IRS certain changes to or a waiver of the requirements in how the applicable plan calculates its funding levels or |

| • | reduce pension benefits to a level where the requirements are met |

the Pension Protection Act could require us to make additional contributions to the multi-employer pension plan from five to ten percent of the contributions that our collective bargaining agreement requires until the collective bargaining agreement expires.

If we fail to make our required contributions to a multi-employer plan under a funding improvement or rehabilitation plan or if the benchmarks that an applicable funding improvement plan provides are not met by the end of a prescribed period, the IRS could impose an excise tax on us with respect to the plan. These excise taxes are not contributed to the deficient funds, but rather are deposited in the United States general treasury funds.

Depending on the amount involved, a requirement to increase contributions beyond our contractually agreed rate or the imposition of an excise tax on us could have a material adverse impact on the financial results of YRC Worldwide.

The Central States Plan has applied for, and the IRS has granted, an extension on the amortization of its unfunded liabilities through 2014, subject to Central States Plan improving its funding levels during that period and certain other conditions. The company expects these funding levels and conditions could form the basis of a funding improvement or rehabilitation plan. Assuming that the Central States Plan meets these conditions, it is expected to meet the minimum funding requirements, as the IRS has modified them, through at least 2014, as well as a funding improvement plan. Absent the benefit of the amortization extension that the IRS has granted to the Central States Plan, the Company believes that the plan would not meet the minimum funding requirements that the Code and related regulations require and the ability for the Central States Plan trustees to adopt a funding improvement plan acceptable to the IRS would be uncertain.

14

Our management team is an important part of our business and loss of key personnel could impair our success.

We benefit from the leadership and experience of our senior management team and depend on their continued services to successfully implement our business strategy. Other than our Chief Executive Officer, William D. Zollars, and James D. Staley, head of Regional Transportation, we have not entered into employment agreements for a fixed period with members of our current management. The loss of key personnel could have a material adverse effect on our operating results, business or financial condition.

Our business may be harmed by anti-terrorism measures.

In the aftermath of the terrorist attacks on the United States, federal, state and municipal authorities have implemented and are implementing various security measures, including checkpoints and travel restrictions on large trucks. Although many companies will be adversely affected by any slowdown in the availability of freight transportation, the negative impact could affect our business disproportionately. For example, we offer specialized services that guarantee on-time delivery. If the security measures disrupt or impede the timing of our deliveries, we may fail to meet the needs of our customers, or may incur increased expenses to do so. We cannot assure you that these measures will not significantly increase our costs and reduce our operating margins and income.

| Item 1B. | Unresolved Staff Comments |

We did not have any unresolved staff comments during the current fiscal year.

| Item 2. | Properties |

At December 31, 2006, we operated a total of 970 transportation service centers located in 50 states, Puerto Rico, Canada and Mexico. Of this total, 522 were owned and 448 were leased, generally with renewal terms of three years or less. The number of vehicle back-in doors totaled 35,412, of which 28,684 were at owned facilities and 6,728 were at leased facilities. The transportation service centers vary in size ranging from one to three doors at small local facilities, to over 420 doors at the largest consolidation and distribution facility. We own substantially all of the larger facilities which contain the greatest number of doors. In addition, we and our subsidiaries own and occupy general office buildings in Overland Park, Kansas, Akron, Ohio, Lebanon, Pennsylvania; Carlisle, Pennsylvania; Holland, Michigan and Winnipeg, Manitoba. Our owned transportation service centers and office buildings are unencumbered.

Our facilities and equipment are adequate to meet current business requirements in 2007. Refer to “Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations”, for a more detailed discussion of expectations regarding capital spending in 2007.

| Item 3. | Legal Proceedings |

We discuss legal proceedings in the “Commitments, Contingencies, and Uncertainties” note under “Item 8, Financial Statements and Supplementary Data”, of this report.

| Item 4. | Submission of Matters to a Vote of Security Holders |

We did not submit any matters to the vote of our stockholders during the fourth quarter of the most recent fiscal year.

15

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

Common Stock

As of January 31, 2007, approximately 16,500 shareholders of record held YRC Worldwide common stock. Our only class of stock outstanding is common stock, traded through the NASDAQ Stock Market. Trading activity averaged 1,324,000 shares per day during 2006, down from 1,563,000 per day in 2005. The NASDAQ Stock Market quotes prices for our common stock under the symbol “YRCW.” The high and low prices at which YRC Worldwide common stock traded for each calendar quarter in 2006 and 2005 are shown below.

Quarterly Financial Information (unaudited)

| (in thousands, except per share data) |

First Quarter |

Second Quarter |

Third Quarter |

Fourth Quarter (b) |

|||||||||||

| 2006 |

|||||||||||||||

| Operating revenue |

$ | 2,374,161 | $ | 2,565,779 | $ | 2,571,087 | $ | 2,407,663 | |||||||

| Losses (gains) on property disposals, net |

882 | (3,226 | ) | 2,427 | (8,443 | ) | |||||||||

| Operating income |

87,828 | 172,281 | 177,591 | 107,734 | |||||||||||

| Net income |

42,136 | 92,252 | 95,785 | 46,459 | |||||||||||

| Diluted earnings per share |

0.71 | 1.58 | 1.64 | 0.80 | |||||||||||

| Common stock: |

|||||||||||||||

| High |

51.54 | 45.32 | 44.43 | 42.49 | |||||||||||

| Low |

37.10 | 36.07 | 35.27 | 36.40 | |||||||||||

| 2005 (a) |

|||||||||||||||

| Operating revenue |

$ | 1,677,961 | $ | 2,088,846 | $ | 2,491,650 | $ | 2,483,100 | |||||||

| Losses (gains) on property disposals, net |

(3,234 | ) | 1,250 | 1,638 | (5,042 | ) | |||||||||

| Operating income |

89,989 | 135,818 | 156,787 | 153,716 | |||||||||||

| Net income |

49,893 | 76,105 | 85,285 | 76,847 | |||||||||||

| Diluted earnings per share |

0.96 | 1.38 | 1.42 | 1.30 | |||||||||||

| Common stock: |

|||||||||||||||

| High |

63.40 | 60.43 | 56.17 | 49.03 | |||||||||||

| Low |

51.01 | 47.89 | 39.25 | 40.23 | |||||||||||

| (a) | Includes the results of all YRC Worldwide entities including USF entities from the date of acquisition, May 24, 2005. |

| (b) | The 2006 amounts reflect lower employee benefits expense of $12 million for a change in a non-union vacation payout practice, lower depreciation expense of $14 million for revised depreciation policies and higher acquisition charges of $13 million related to the USF Red Star multi-employer pension plan withdrawal liability. |

Purchases of Equity Securities by the Issuer

We consider several factors in determining when to make share repurchases including, among other things, our cash needs and the market price of the stock. In April 2006, our Board of Directors authorized a $100 million share repurchase program. During September 2006, we purchased and converted to treasury stock 521,100 shares of common stock at a cost of approximately $20 million with an average price paid per share of $38.34.

In September 2005, our Board of Directors authorized a $50 million share repurchase program. During the fourth quarter of 2005, we purchased and converted to treasury stock 1,064,382 shares of common stock at a cost of approximately $50 million.

The following table presents the total number of shares repurchased during fiscal year 2005 by month and the average price paid per share:

| Fiscal Period |

Total Number of Shares Purchased |

Average Price Paid per Share | |||

| November 1, 2005, through November 30, 2005 |

832,917 | $ | 47.46 | ||

| December 1, 2005, through December 31, 2005 |

231,465 | $ | 45.08 | ||

| Total Fiscal 2005 |

1,064,382 | $ | 46.95 | ||

16

We did not declare any cash dividends on our common stock in 2006 or 2005.

The information required by this item with respect to information regarding our equity compensation plans is included under the caption “Equity Compensation Plan Information” in our Proxy Statement related to the 2007 Annual Meeting of Shareholders and is incorporated herein by reference.

17

Common Stock Performance

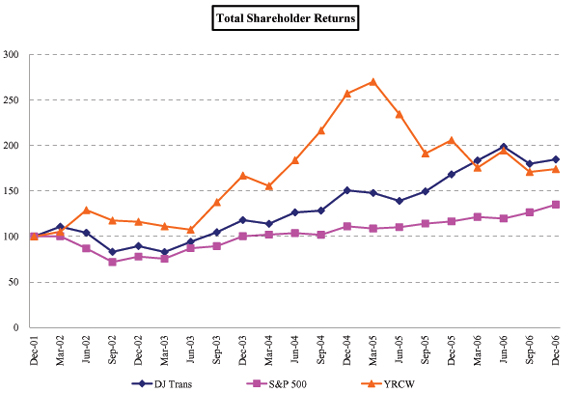

Set forth below is a line graph comparing the yearly percentage change in the cumulative total stockholder return of the Company’s common stock against the cumulative total return of the S&P Composite-500 Stock Index and the Dow Jones Transportation Average Stock Index for the period of five years commencing December 31, 2001 and ending December 31, 2006.

| DJ Trans Index |

S&P 500 Index |

YRC Worldwide Inc. | ||||

| Dec-01 |

100 | 100 | 100 | |||

| 111 | 100 | 105 | ||||

| 104 | 87 | 129 | ||||

| 83 | 72 | 118 | ||||

| Dec-02 |

90 | 78 | 116 | |||

| 83 | 75 | 111 | ||||

| 94 | 87 | 107 | ||||

| 105 | 89 | 138 | ||||

| Dec-03 |

118 | 100 | 167 | |||

| 114 | 102 | 156 | ||||

| 126 | 104 | 184 | ||||

| 128 | 102 | 216 | ||||

| Dec-04 |

151 | 111 | 257 | |||

| 148 | 109 | 270 | ||||

| 139 | 110 | 234 | ||||

| 150 | 114 | 191 | ||||

| Dec-05 |

168 | 117 | 206 | |||

| 184 | 121 | 176 | ||||

| 199 | 120 | 194 | ||||

| 180 | 127 | 171 | ||||

| Dec-06 |

185 | 135 | 174 |

18

| Item 6. | Selected Financial Data |

| (in thousands except per share data) |

2006 | 2005(a) | 2004 | 2003(b) | 2002(c) | |||||||||||||||

| For the Year |

||||||||||||||||||||

| Operating revenue |

$ | 9,918,690 | $ | 8,741,557 | $ | 6,767,485 | $ | 3,068,616 | $ | 2,624,148 | ||||||||||

| Operating income |

545,434 | 536,310 | 361,601 | 88,602 | 46,864 | |||||||||||||||

| Losses (gains) on property disposals, net |

(8,360 | ) | (5,388 | ) | (4,547 | ) | (167 | ) | 425 | |||||||||||

| Reorganization and acquisition charges |

26,302 | 13,029 | — | 3,124 | 8,010 | |||||||||||||||

| Interest expense |

87,760 | 63,371 | 43,954 | 20,606 | 7,211 | |||||||||||||||

| Asset backed securitization (“ABS”) facility charges |

— | — | — | — | 2,576 | |||||||||||||||

| Income from continuing operations (after tax) |

276,632 | 288,130 | 184,327 | 40,683 | 23,973 | |||||||||||||||

| Net income (loss) |

276,632 | 288,130 | 184,327 | 40,683 | (93,902 | ) | ||||||||||||||

| Depreciation and amortization expense(f) |

274,184 | 250,562 | 171,468 | 87,398 | 79,334 | |||||||||||||||

| Net capital expenditures from continuing operations |

303,057 | 256,435 | 164,289 | 99,134 | 82,830 | |||||||||||||||

| Net cash from operating activities from continuing operations |

532,304 | 497,677 | 435,718 | 155,736 | 25,808 | |||||||||||||||

| At Year-End |

||||||||||||||||||||

| Net property and equipment |

2,269,846 | 2,205,792 | 1,422,718 | 1,403,268 | 564,976 | |||||||||||||||

| Total assets |

5,952,237 | 5,734,189 | 3,627,169 | 3,463,229 | 1,042,985 | |||||||||||||||

| Long-term debt, less current portion |

1,058,496 | 1,113,085 | 403,535 | 836,082 | 50,024 | |||||||||||||||

| ABS facility |

225,000 | 374,970 | — | 71,500 | 50,000 | |||||||||||||||

| Total debt, including ABS facility |

1,283,496 | 1,488,055 | 657,935 | 909,339 | 124,285 | |||||||||||||||

| Total shareholders’ equity (g) |

2,192,549 | 1,936,488 | 1,214,191 | 1,002,085 | 359,958 | |||||||||||||||

| Measurements |

||||||||||||||||||||

| Basic per share data: |

||||||||||||||||||||

| Income from continuing operations |

4.82 | 5.30 | 3.83 | 1.34 | 0.86 | |||||||||||||||

| Net income (loss) |

4.82 | 5.30 | 3.83 | 1.34 | (3.35 | ) | ||||||||||||||

| Average common shares outstanding – basic |

57,361 | 54,358 | 48,149 | 30,370 | 28,004 | |||||||||||||||

| Diluted per share data: |

||||||||||||||||||||

| Income from continuing operations |

4.74 | 5.07 | 3.75 | 1.33 | 0.84 | |||||||||||||||

| Net income (loss) |

4.74 | 5.07 | 3.75 | 1.33 | (3.31 | ) | ||||||||||||||

| Average common shares outstanding – diluted |

58,339 | 56,905 | 49,174 | 30,655 | 28,371 | |||||||||||||||

| Debt to capitalization |

36.9 | % | 43.5 | % | 35.1 | % | 47.6 | % | 25.7 | % | ||||||||||

| Debt to capitalization, less cash |

35.5 | % | 42.1 | % | 31.2 | % | 45.4 | % | 21.0 | % | ||||||||||

| Shareholders’ equity per share |

38.33 | 33.80 | 24.66 | 20.97 | 12.17 | |||||||||||||||

| Common stock price range: |

||||||||||||||||||||

| High |

51.54 | 63.40 | 56.49 | 36.96 | 32.21 | |||||||||||||||

| Low |

35.27 | 39.25 | 29.77 | 21.18 | 18.31 | |||||||||||||||

| Other Data |

||||||||||||||||||||

| Average number of employees |

66,000 | 68,000 | 50,000 | 50,000 | (d) | 23,000 | ||||||||||||||

| Operating ratio: |

||||||||||||||||||||

| Yellow Transportation |

94.0 | % | 92.5 | % | 94.0 | % | 95.7 | % | 97.2 | % | ||||||||||

| Roadway |

93.7 | % | 93.7 | % | 94.9 | % | — | — | ||||||||||||

| Regional Transportation |

94.2 | % | 94.5 | % | 87.0 | % | (e | )— | — | |||||||||||

| Meridian IQ |

97.8 | % | 96.6 | % | 98.2 | % | 99.8 | % | 103.3 | % | ||||||||||

| (a) | Includes the results of all YRC Worldwide entities including USF entities from the date of acquisition, May 24, 2005. |

| (b) | Includes the results of all YRC Worldwide entities including Roadway and New Penn entities from the date of acquisition, December 11, 2003. |

| (c) | In 2002, we completed the spin-off of SCS Transportation, Inc. (“SCST”) now known as Saia Inc. Financial Summary data for 2002 presents SCST as a discontinued operation. |

| (d) | In 2003, prior to the acquisition of Roadway on December 11, 2003, we had an average of 25,000 employees. |

| (e) | Includes the results of New Penn only in 2004. |

| (f) | Depreciation lives and salvage values were revised effective July 1, 2006. See Property and Equipment footnote. |

| (g) | SFAS No. 158 was adopted effective December 31, 2006. See Employee Benefits – Pension and Other Postretirement Benefit Plans footnote. |

19

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

“Management’s Discussion and Analysis of Financial Condition and Results of Operations” contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. See the introductory section immediately prior to “Part I” of this Annual Report on Form 10-K regarding these statements.

Overview

YRC Worldwide Inc. (also referred to as “YRC Worldwide”, “the Company”, “we” or “our”), one of the largest transportation service providers in the world, is a holding company that through wholly owned operating subsidiaries offers its customers a wide range of transportation services. These operating subsidiaries are primarily represented by Yellow Transportation and Roadway, both leading transportation service providers offering a full range of regional, national and international services; YRC Regional Transportation, a holding company for our transportation service providers focused on business opportunities in the regional and next-day delivery markets; and Meridian IQ, a global logistics management company that plans and coordinates the movement of goods worldwide to provide customers a single source for logistics management solutions. These companies represent our reporting segments and are more fully described in “Item 1 – Business”.

The following management’s discussion and analysis explains the main factors impacting our results of operations, liquidity and capital expenditures and the critical accounting policies of YRC Worldwide. This information should be read in conjunction with the accompanying financial statements and notes thereto, as well as our detailed discussion of risk factors included in Item 1A.

Our Operating Environment

We operate in a highly competitive environment, yet one where we believe the right value proposition for our customers permits us to recover our cost of capital over the business cycle. Over the last several years significant changes have occurred in our environment, including: consolidation and liquidation of LTL carriers; the increased presence of large global, service providers; and increasing needs and demands of our customers. We continue to proactively address these changes through our strategy of being a global transportation services provider. Over the last few years we have expanded our service offerings and completed multiple acquisitions of asset and non-asset-based companies. In 2003, we acquired Roadway which roughly doubled our presence in the LTL sector and allowed us to focus on opportunities to reduce costs. In 2005, we acquired USF and created our Regional Transportation group which enhanced our service offerings and further increased the opportunities for significant synergies. During the latter part of 2005, we expanded globally by completing a freight forwarding joint venture with a Chinese corporation. In 2006, we announced our name change to YRC Worldwide Inc. to reflect the fact that our services have expanded to become a global transportation and logistics provider. In January 2007, we announced the consolidation of management of our national LTL companies, Yellow Transportation and Roadway, and the creation of our Enterprise Solutions Group to increase customer focus and service improvements. This combination will allow more focus on offering our entire portfolio of services to our customers.

We will continue to face challenges in the environment that we operate, primarily due to the changing competitive landscape and meeting our stakeholders’ demands. Specific economic areas that impact our ability to generate profits and cash flows include the levels of consumer spending, manufacturing and overall economic activity. We monitor these areas primarily through several common economic indices, including the gross domestic product (“GDP”) and the industrial production index (“IPI”). Real GDP measures the value of goods and services produced in the U.S., excluding inflation, and the IPI measures the physical units and inputs into the U.S. production process. Over time these measures have been good indicators for general levels of freight volume available in our markets. We manage the impact of our customers’ spending, manufacturing and economic activity through, among others, pricing discipline, cost management programs, maintaining adequate debt capacity, investment in technology and continuous improvement programs. We continue to be well positioned in the transportation industry with a strong ability to take advantage of the positive economic conditions.

Acquisitions and Investments

USF Corporation

On May 24, 2005, YRC Worldwide completed the acquisition of USF Corporation (“USF”), headquartered in Chicago, IL, through the merger (the “Merger”) of a wholly owned subsidiary of YRC Worldwide with and into USF, resulting in USF becoming a wholly owned subsidiary of YRC Worldwide. USF, a leader in the transportation industry, specializes in high-value next-day, regional and national LTL transportation, third-party logistics, and premium regional and national truckload transportation. The company serves the North American market, including the United States, Canada and Mexico, as well as the U.S. territories of Puerto Rico and Guam under the following brands: USF Holland, USF Reddaway, USF Glen Moore and USF Logistics. The

20

acquisition further advances YRC Worldwide as one of the leading transportation services companies in the world. The combined entity offers customers a broad range of transportation services including next day, inter-regional, national and international capabilities.