The information in this prospectus is not complete and may be changed. These

securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer

or sale is not permitted.

SUBJECT TO COMPLETION, DATED DECEMBER 20, 2022

PRELIMINARY PROSPECTUS

$ Securitized Utility Tariff Bonds, Series 2023-A

Evergy Missouri West, Inc.

Sponsor, Depositor and Initial Servicer

Central Index Key Number: 0001955722

Evergy Missouri West Storm Funding I, LLC

Issuing Entity

Central Index Key Number: 0001955844

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Tranche |

|

Expected Weighted

Average Life (Years) |

|

Principal

Amount Offered |

|

Scheduled

Final

Payment Date |

|

Final Maturity

Date |

|

Interest Rate |

|

Initial Price to

Public (1) |

|

Underwriting

Discounts and

Commissions |

|

Proceeds to Issuing

Entity (Before

Expenses) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (1) |

Interest on the securitized utility tariff bonds will accrue

from , 2023 and must be paid by the purchaser if the bonds are delivered after that date. |

The total initial price to the public is $ .

The total amount of the underwriting discounts and commissions is $ . The total amount of proceeds to the issuing entity before

deduction of expenses (estimated to be $ ) is $ . The

distribution frequency is semi-annually. The first expected payment date is .

Investing in the Securitized Utility Tariff Bonds involves risks. Please read “Risk

Factors” beginning on page 17 in this prospectus to read about factors you should consider before buying the securitized utility tariff bonds.

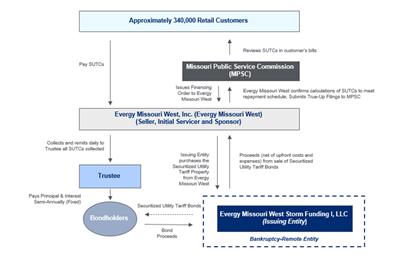

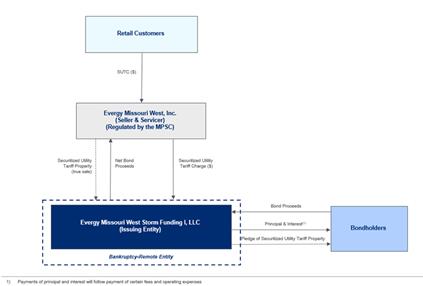

Evergy Missouri West, Inc., as “sponsor”, is offering

$ Securitized Utility Tariff Bonds, Series 2023-A, referred to herein as the “securitized utility tariff

bonds” or “bonds”, in tranches to be issued by Evergy Missouri West Storm Funding I, LLC, as the “issuing

entity”. Evergy Missouri West, Inc. is also the “seller”, initial “servicer” and “depositor” with regard to the securitized utility tariff bonds.

The securitized utility tariff bonds are senior secured obligations of the issuing entity supported by “securitized utility tariff property”, which includes the right to a special, irrevocable

non-bypassable charge, known as “securitized utility tariff charges”, and paid by all existing or future retail customers receiving electrical service from the electrical corporation or its

successors or assignees under commission-approved rate schedules, except for customers receiving electrical service under special contracts as of August 28, 2021, even if a retail customer elects to purchase electricity from an alternative

electricity supplier following a fundamental change in regulation of public utilities in this state. The Securitization Law (as defined below) requires that securitized utility tariff charges be adjusted (or

“trued-up”) at least annually, and the Missouri Public Service Commission (the “MPSC”) has authorized the securitized utility tariff charges to be adjusted more frequently to

ensure the expected recovery of securitized utility tariff charge revenues sufficient to timely provide all scheduled payments of principal and interest on the securitized utility tariff bonds and related financing costs, as described further in

this prospectus. Credit enhancement for the securitized utility tariff bonds will be provided by such “true-up” mechanisms as well as by accounts held under the indenture.

The securitized utility tariff bonds will be issued pursuant to Section 393.1700 of the Revised Statutes of Missouri (the

“Securitization Law”), and an irrevocable financing order issued by the MPSC on November 17, 2022, which became effective on November 27, 2022, approving the issuance of the securitized utility tariff bonds (the

“financing order”). The financing order is irrevocable and the MPSC shall neither reduce, impair, postpone, terminate, or otherwise adjust the securitized utility tariff charges authorized under a financing order, except for the true-up adjustments to the securitized utility tariff charges.

The securitized utility tariff bonds

represent obligations only of the issuing entity, Evergy Missouri West Storm Funding I, LLC, and do not represent obligations of the sponsor or any of its affiliates other than the issuing entity. The securitized utility tariff bonds are secured by

the collateral, consisting principally of the securitized utility tariff property acquired pursuant to the sale agreement and funds on deposit in the collection account for the securitized utility tariff bonds and related subaccounts. Please read

“Security for the Securitized Utility Tariff Bonds” in this prospectus. Neither the State of Missouri nor its political subdivisions are liable for the securitized utility tariff bonds, and the bonds are not a debt or general

obligation of the State of Missouri or any of its political subdivisions, agencies or instrumentalities, nor are they indebtedness of the State of Missouri or any agency or political subdivision. The securitized utility tariff bonds do not,

directly, indirectly, or contingently, obligate the State of Missouri or any agency, political subdivision, or instrumentality of the State of Missouri to levy any tax or make any appropriation for payment of the securitized utility tariff bonds,

other than in their capacity as consumers of electricity.

Interest will accrue on the securitized utility tariff bonds from the date of

issuance. The securitized utility tariff bonds are scheduled to pay principal and interest semi-annually on and

of each year. The first scheduled payment date is . On

each payment date, each securitized utility tariff bond will be entitled to payment of principal, sequentially, but only to the extent funds are available in the collection account after payment of certain fees and expenses and after payment of

interest.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE

SECURITIES OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The

underwriters expect to deliver the securitized utility tariff bonds through the book-entry facilities of The Depository Trust Company for the accounts of its participants, including Clearstream Banking, S.A. and Euroclear Bank SA/NV, as operator of

the Euroclear System, against payment in immediately available funds on or about , 2023.

Joint Book-Running Managers

The date of this prospectus is , 2023