false 2022-08-31 485BPOS 0000875186 16.98 23.66 34.93 10.72 3.75 6.19 20.49 4.83 29.08 18.68 10.69 16.80 48.54 4.74 3.92 4.92 19.66 11.08 28.74 20.67 17.46 11.49 18.31 8.26 0.52 0.36 27.15 15.72 22.74 10.06 19.60 3.58 6.34 3.54 14.40 13.07 39.16 18.71 22.43 11.19 7.91 1.70 1.96 5.70 0.59 2.90 3.90 0.46 9.76 8.66 15.64 4.46 7.88 0.07 7.43 14.13 7.00 2.88 14.10 2.01 7.87 2.88 2.25 9.08 0.44 6.59 3.08 2.21 7.51 5.87 5.25 1.21 2.62 8.21 2.58 0.29 4.84 0.54 7.03 3.57 3.15 2.05 8.11 12.70 5.42 1.73 1.63 2.65 2.06 0.11 10.43 5.19 5.34 0000875186 2023-01-01 2023-01-01 0000875186 mspf:S000008429Member 2023-01-01 2023-01-01 0000875186 mspf:S000008429Member mspf:C000023137Member 2023-01-01 2023-01-01 0000875186 mspf:S000008429Member mspf:C000023137Member rr:AfterTaxesOnDistributionsAndSalesMember 2023-01-01 2023-01-01 0000875186 mspf:S000008429Member mspf:C000023137Member rr:AfterTaxesOnDistributionsMember 2023-01-01 2023-01-01 0000875186 mspf:S000008429Member mspf:LipperLargeCapCoreFundsAverageMember 2023-01-01 2023-01-01 0000875186 mspf:S000008429Member mspf:Russell1000IndexMember 2023-01-01 2023-01-01 0000875186 mspf:S000008430Member 2023-01-01 2023-01-01 0000875186 mspf:S000008430Member mspf:BloombergUsMunicipalBondIndexMember 2023-01-01 2023-01-01 0000875186 mspf:S000008430Member mspf:C000023138Member 2023-01-01 2023-01-01 0000875186 mspf:S000008430Member mspf:C000023138Member rr:AfterTaxesOnDistributionsAndSalesMember 2023-01-01 2023-01-01 0000875186 mspf:S000008430Member mspf:C000023138Member rr:AfterTaxesOnDistributionsMember 2023-01-01 2023-01-01 0000875186 mspf:S000008430Member mspf:LipperGeneralInsuredMunicipalDebtFundsAverageMember 2023-01-01 2023-01-01 0000875186 mspf:S000008433Member 2023-01-01 2023-01-01 0000875186 mspf:S000008433Member mspf:C000023141Member 2023-01-01 2023-01-01 0000875186 mspf:S000008433Member mspf:C000023141Member rr:AfterTaxesOnDistributionsAndSalesMember 2023-01-01 2023-01-01 0000875186 mspf:S000008433Member mspf:C000023141Member rr:AfterTaxesOnDistributionsMember 2023-01-01 2023-01-01 0000875186 mspf:S000008433Member mspf:LipperSmallCapCoreFundsAverageMember 2023-01-01 2023-01-01 0000875186 mspf:S000008433Member mspf:Russell2500IndexMember 2023-01-01 2023-01-01 0000875186 mspf:S000008435Member 2023-01-01 2023-01-01 0000875186 mspf:S000008435Member mspf:C000023143Member 2023-01-01 2023-01-01 0000875186 mspf:S000008435Member mspf:C000023143Member rr:AfterTaxesOnDistributionsAndSalesMember 2023-01-01 2023-01-01 0000875186 mspf:S000008435Member mspf:C000023143Member rr:AfterTaxesOnDistributionsMember 2023-01-01 2023-01-01 0000875186 mspf:S000008435Member mspf:LipperInternationalLargeCapCoreFundsAverageMember 2023-01-01 2023-01-01 0000875186 mspf:S000008435Member mspf:MSCIEAFEIndexNetMember 2023-01-01 2023-01-01 0000875186 mspf:S000008436Member 2023-01-01 2023-01-01 0000875186 mspf:S000008436Member mspf:C000023144Member 2023-01-01 2023-01-01 0000875186 mspf:S000008436Member mspf:C000023144Member rr:AfterTaxesOnDistributionsAndSalesMember 2023-01-01 2023-01-01 0000875186 mspf:S000008436Member mspf:C000023144Member rr:AfterTaxesOnDistributionsMember 2023-01-01 2023-01-01 0000875186 mspf:S000008436Member mspf:LipperEmergingMarketsFundsAverageMember 2023-01-01 2023-01-01 0000875186 mspf:S000008436Member mspf:MSCIEmergingMarketsIndexNetreflectsnodeductionforfeesexpensesortaxesMember 2023-01-01 2023-01-01 0000875186 mspf:S000008437Member 2023-01-01 2023-01-01 0000875186 mspf:S000008437Member mspf:BloombergBarclaysUSAggregateBondTMIndexreflectsnodeductionforfeesexpensesortaxesMember 2023-01-01 2023-01-01 0000875186 mspf:S000008437Member mspf:C000023145Member 2023-01-01 2023-01-01 0000875186 mspf:S000008437Member mspf:C000023145Member rr:AfterTaxesOnDistributionsAndSalesMember 2023-01-01 2023-01-01 0000875186 mspf:S000008437Member mspf:C000023145Member rr:AfterTaxesOnDistributionsMember 2023-01-01 2023-01-01 0000875186 mspf:S000008437Member mspf:LipperCoreBondFundsAverageMember 2023-01-01 2023-01-01 0000875186 mspf:S000008438Member 2023-01-01 2023-01-01 0000875186 mspf:S000008438Member mspf:BloombergBarclaysUSCorporateHighYieldBondIndexreflectsnodeductionforfeesexpensesortaxesMember 2023-01-01 2023-01-01 0000875186 mspf:S000008438Member mspf:C000023146Member 2023-01-01 2023-01-01 0000875186 mspf:S000008438Member mspf:C000023146Member rr:AfterTaxesOnDistributionsAndSalesMember 2023-01-01 2023-01-01 0000875186 mspf:S000008438Member mspf:C000023146Member rr:AfterTaxesOnDistributionsMember 2023-01-01 2023-01-01 0000875186 mspf:S000008438Member mspf:LipperHighYieldFundsAverageMember 2023-01-01 2023-01-01 0000875186 mspf:S000008439Member 2023-01-01 2023-01-01 0000875186 mspf:S000008439Member mspf:C000023147Member 2023-01-01 2023-01-01 0000875186 mspf:S000008439Member mspf:C000023147Member rr:AfterTaxesOnDistributionsAndSalesMember 2023-01-01 2023-01-01 0000875186 mspf:S000008439Member mspf:C000023147Member rr:AfterTaxesOnDistributionsMember 2023-01-01 2023-01-01 0000875186 mspf:S000008439Member mspf:FtseNonUsDollarWorldGovernmentBondIndexMember 2023-01-01 2023-01-01 0000875186 mspf:S000008439Member mspf:LipperInternationalIncomeFundsAverageMember 2023-01-01 2023-01-01 0000875186 mspf:S000052236Member 2023-01-01 2023-01-01 0000875186 mspf:S000052236Member mspf:BloombergUsTreasuryInflationProtectedSecuritiesTIPSIndexMember 2023-01-01 2023-01-01 0000875186 mspf:S000052236Member mspf:C000164312Member 2023-01-01 2023-01-01 0000875186 mspf:S000052236Member mspf:C000164312Member rr:AfterTaxesOnDistributionsAndSalesMember 2023-01-01 2023-01-01 0000875186 mspf:S000052236Member mspf:C000164312Member rr:AfterTaxesOnDistributionsMember 2023-01-01 2023-01-01 0000875186 mspf:S000052236Member mspf:LipperInflationProtectedBondFundsAverageMember 2023-01-01 2023-01-01 0000875186 mspf:S000052237Member 2023-01-01 2023-01-01 0000875186 mspf:S000052237Member mspf:C000164313Member 2023-01-01 2023-01-01 0000875186 mspf:S000052237Member mspf:C000164313Member rr:AfterTaxesOnDistributionsAndSalesMember 2023-01-01 2023-01-01 0000875186 mspf:S000052237Member mspf:C000164313Member rr:AfterTaxesOnDistributionsMember 2023-01-01 2023-01-01 0000875186 mspf:S000052237Member mspf:FTSE3MonthUSTreasuryBillIndexreflectsnodeductionforfeesexpensesortaxesMember 2023-01-01 2023-01-01 0000875186 mspf:S000052237Member mspf:LipperUltraShortObligationsFundsAverageMember 2023-01-01 2023-01-01 0000875186 mspf:S000060155Member 2023-01-01 2023-01-01 0000875186 mspf:S000060155Member mspf:C000196891Member 2023-01-01 2023-01-01 0000875186 mspf:S000060155Member mspf:C000196891Member rr:AfterTaxesOnDistributionsAndSalesMember 2023-01-01 2023-01-01 0000875186 mspf:S000060155Member mspf:C000196891Member rr:AfterTaxesOnDistributionsMember 2023-01-01 2023-01-01 0000875186 mspf:S000060155Member mspf:HfrxGlobalHedgeIndexMember 2023-01-01 2023-01-01 xbrli:pure iso4217:USD

As filed with the Securities and Exchange Commission on December 29, 2022

Securities Act File No. 033‑40823

Investment Company Act No. 811‑06318

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON D.C. 20549

FORM N-1A

REGISTRATION STATEMENT

UNDER

|

|

|

| THE SECURITIES ACT OF 1933 |

|

|

| Post-effective Amendment No. 86 |

|

☒ |

and/or

REGISTRATION STATEMENT

UNDER

THE INVESTMENT COMPANY ACT OF 1940

(Check appropriate box or boxes)

Morgan Stanley Pathway Funds

2000 Westchester Avenue

Purchase, NY 10577

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code:

(800) 869‑3326

CT Corp

155 Federal Street Suite 700

Boston, MA 02110

(Name and Address of Agent for Service)

It is proposed that this filing will become effective (check appropriate box):

| ☐ |

immediately upon filing pursuant to paragraph (b) |

| ☒ |

on January 1, 2023 pursuant to paragraph (b) |

| ☐ |

60 days after filing pursuant to paragraph (a)(1) |

| ☐ |

On (date) pursuant to paragraph (a)(1) |

| ☐ |

On (date) pursuant to paragraph (a)(3) |

| ☐ |

75 days after filing pursuant to paragraph (a)(2) |

| ☐ |

On (date) pursuant to paragraph (a)(2) of rule 485 |

Morgan Stanley

Pathway Funds

Prospectus

» January 1, 2023

| • |

Large Cap Equity Fund (TLGUX) |

| • |

Small-Mid Cap Equity Fund (TSGUX) |

| • |

International Equity Fund (TIEUX) |

| • |

Emerging Markets Equity Fund (TEMUX) |

| • |

Core Fixed Income Fund (TIIUX) |

| • |

High Yield Fund (THYUX) |

| • |

International Fixed Income Fund (TIFUX) |

| • |

Municipal Bond Fund (TMUUX) |

| • |

Inflation-Linked Fixed Income Fund (TILUX) |

| • |

Ultra-Short Term Fixed Income Fund (TSDUX) |

| • |

Alternative Strategies Fund (TALTX) |

| INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE |

The Securities and Exchange Commission has not approved or disapproved these securities or determined whether this Prospectus is accurate or complete. Any statement to the contrary is a crime.

Morgan Stanley Pathway Funds

Investment objective

Capital appreciation.

Fund fees and expenses

This table describes the fees and expenses you may pay if you buy and hold shares of the Fund.

Annual Advisory Program Fees

(fees paid directly from your investment in the applicable Morgan Stanley-sponsored investment advisory program)

| Maximum annual fees in the Consulting Group Advisor, Select UMA or Portfolio Management investment advisory programs (as a percentage of prior quarter-end net assets)* |

2.00% |

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment in the Fund)

| Management Fees* |

0.60% |

| Distribution (12b-1) Fees |

None |

| Other Expenses |

0.09% |

| Total Annual Fund Operating Expenses |

0.69% |

| Waiver* |

(0.21)% |

| Net Annual Fund Operating Expenses* |

0.48% |

* CGAS (defined herein) has contractually agreed to waive fees and reimburse expenses in order to keep the Fund’s management fees from exceeding the total amount of sub-advisory fees paid by CGAS plus 0.20% based on average net assets. This contractual waiver will only apply if the Fund’s total management fees exceed the total amount of sub-advisory fees paid by CGAS plus 0.20% and will not affect the Fund’s total management fees if they are less than such amount. This fee waiver and/or reimbursement will continue for at least one year from the date of this prospectus or until such time as the Board of Trustees acts to discontinue all or a portion of such waiver and/or reimbursement when they deem such action is appropriate.

Examples

These examples are intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The examples assume that you invest $10,000 in the Fund for the time periods indicated. The examples also assume that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. The effect of the Fund’s contractual fee waiver is only reflected in the first year of the example. The figures are calculated based upon total annual Fund operating expenses and a maximum annual fee of 2.00% for the applicable Morgan Stanley-sponsored investment advisory program through which you invest. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

AFTER

1 YEAR |

AFTER

3 YEARS |

AFTER

5 YEARS |

AFTER

10 YEARS |

| $251 |

$815 |

$1,406 |

$3,007 |

Portfolio turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the above examples, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 20% of the average value of its portfolio.

Principal investment strategies

The Fund will invest, under normal market conditions, at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in the equity securities of large capitalization (or “cap”) companies or in other investments with similar economic characteristics. The Fund defines large cap companies as companies whose market capitalizations typically fall within the range of the Russell 1000® Index. The market capitalization of the companies in large-cap market indices and the Fund’s portfolio changes over time. The Fund may invest up to 10% of its assets in the securities of foreign issuers that are not traded on a U.S. exchange or the U.S. over-the-counter market. The Fund may also lend portfolio securities to earn additional income. Any income realized through securities lending may help Fund performance.

The Fund employs a “multi-manager” strategy whereby portions of the Fund are allocated to professional money managers (each, a “Sub-adviser,” collectively, the “Sub-advisers”) who are responsible for investing the assets of the Fund.

Principal risks of investing in the Fund

Loss of money is a risk of investing in the Fund.

The Fund’s principal risks include:

| • |

Market Risk, which is the risk that stock prices decline overall. Markets are volatile and can decline significantly in response to real or perceived adverse issuer, political, regulatory, market or economic developments in the U.S. and in other countries. Similarly, environmental and public health risks, such as natural disasters, epidemics, pandemics or widespread fear that such events may occur, may impact markets adversely and cause market volatility in both the short and long-term. Market risk may affect a single company, sector of the economy or the market as a whole. |

| • |

Equity Risk, which is the risk that prices of equity securities rise and fall daily due to factors affecting individual companies, particular industries or the equity market as a whole. |

| • |

Exchange-Traded Funds (“ETFs”) Risk, which is the risk of owning shares of an ETF and generally reflects the risks of owning the underlying securities the ETF is designed to track, although lack of liquidity in an ETF could result in its value being more volatile than the underlying portfolio |

| |

securities. When the Fund invests in an ETF, in addition to directly bearing the expenses associated with its own operations, it will bear a pro rata portion of the ETF’s expenses. |

| • |

Investment Style Risk, which means large cap and/or growth stocks could fall out of favor with investors and trail the performance of other types of investments. |

| • |

Foreign Investment Risk, which means risks unique to foreign securities, including less information about foreign issuers, less liquid securities markets, political instability and unfavorable changes in currency exchange rates. |

| • |

Securities Lending Risk, which includes the potential insolvency of a borrower and losses due to the re-investment of collateral received on loaned securities in investments that default or do not perform well. |

| • |

Manager Risk, which is the risk that poor security selection by a Sub-adviser will cause the Fund to underperform. This risk is common for all actively managed funds. |

| • |

Multi-Manager Risk, which is the risk that the investment styles of the Sub-advisers may not complement each other as expected by the Manager. The Fund may experience a higher portfolio turnover rate, which can increase the Fund’s transaction costs and result in more taxable short-term gains for shareholders. |

| • |

Issuer Risk, which is the risk that the value of a security may decline for reasons directly related to the issuer, such as management performance, financial leverage and reduced demand for the issuer’s goods or services. |

| • |

Sector Risk, which is the risk that the value of securities in a particular industry or sector will decline because of changing expectations for the performance of that industry or sector. From time to time, based on market or economic conditions, |

| |

the Fund may have significant positions in one or more sectors of the market. To the extent the Fund invests more heavily in particular sectors, its performance will be especially sensitive to developments that significantly affect those sectors. Individual sectors may be more volatile, and may perform differently, than the broader market. The industries that constitute a sector may all react in the same way to economic, political or regulatory events. |

An investment in the Fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. For more information on the risks of investing in the Fund please see the Fund details section of this Prospectus.

Performance

The bar chart below shows how the Fund’s investment results have varied from year to year, and the following table shows how the Fund’s annual total returns for various periods compare to those of the Fund’s benchmark index and Lipper peer group. This information provides some indication of the risks of investing in the Fund. The Fund is available only to investors participating in Morgan Stanley-sponsored investment advisory programs. These programs charge an annual fee (see Annual Advisory Program Fees above). The performance information in the bar chart and table below does not reflect this fee, which would reduce your return. The Fund’s past performance, before and after taxes, does not necessarily indicate how the Fund will perform in the future. For current performance information please see www.morganstanley.com/wealth-investmentsolutions/cgcm.

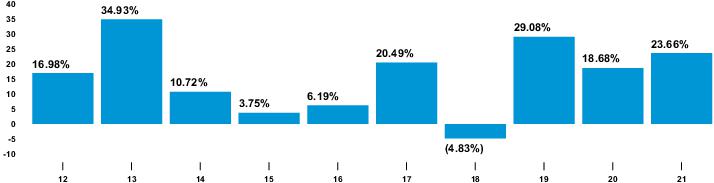

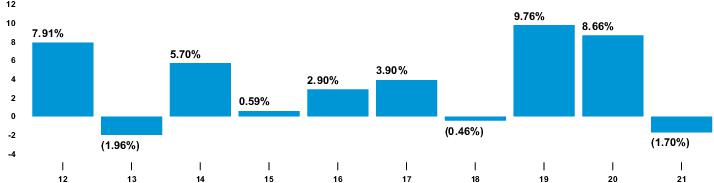

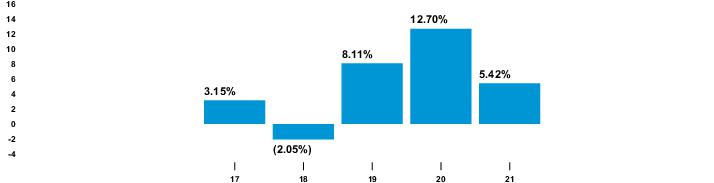

Annual total returns (%) calendar years

Large Cap Equity Fund

Fund’s best and worst calendar quarters

Best: 21.65% in 2nd quarter 2020

Worst: (21.39)% in 1st quarter 2020

Year-to-date: (26.02)% (through 3rd quarter 2022)

Average Annual Total Returns

(for the periods ended December 31, 2021)

| INCEPTION DATE 11/18/1991 |

1 YEAR |

5 YEARS |

10 YEARS |

| Fund (without advisory program fee) |

| Return Before Taxes |

23.66% |

16.78% |

15.38% |

| Return After Taxes on Distributions |

20.27% |

14.75% |

13.11% |

| Return After Taxes on Distributions and Sale of Fund Shares |

15.79% |

13.03% |

12.14% |

| Russell 1000® Index (reflects no deduction for fees, expenses or taxes) |

26.45% |

18.43% |

16.54% |

| Lipper Large-Cap Core Funds Average |

26.63% |

17.59% |

15.44% |

The after-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an individual investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. In some cases, the return after taxes may exceed the return before taxes due to an assumed tax benefit from any losses on a sale of Fund shares at the end of the measurement period.

The Fund’s benchmark is the Russell 1000® Index. The Russell 1000® Index is composed of the 1,000 largest U.S. companies by market capitalization. Unlike the Fund, the benchmark is unmanaged and does not include any fees or expenses. An investor cannot invest directly in an index.

The Fund also compares its performance with the Lipper Large-Cap Core Funds Average, which is a secondary

benchmark and includes funds that invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) greater than 300% of the dollar-weighted median market capitalization of the middle 1,000 securities of the S&P SuperComposite 1500® Index.

Investment adviser

Consulting Group Advisory Services LLC (“CGAS” or the “Manager”), a business of Morgan Stanley Wealth Management (“MSWM”), serves as the investment adviser for the Fund. Subject to Board review, the Manager selects and oversees professional money managers (each a “Sub-adviser,” collectively, the “Sub-advisers”) who are responsible for investing the assets of the Fund. The Sub-advisers are selected based primarily upon the research and recommendation of the Manager, which includes a quantitative and qualitative evaluation of a Sub-adviser’s skills and investment results in managing assets for specific asset classes, investment styles and strategies. The Manager allocates and, when appropriate, reallocates the Fund’s assets among one or more Sub-advisers, continuously monitors and evaluates Sub-adviser performance (including trade execution), performs other due diligence functions (such as an assessment of changes in personnel or other developments at the Sub-advisers), and oversees Sub-adviser compliance with the Fund’s investment objectives, policies and guidelines. The Manager also monitors changes in market conditions and considers whether changes in the allocation of Fund assets or the lineup of Sub-advisers should be made in response to such changes in market conditions. Sub-advisers may also periodically recommend changes or enhancements to the Fund’s investment objectives, policies and guidelines, which are subject to the approval of the Manager and may also be subject to the approval of the Board.

Sub-advisers and portfolio managers

BlackRock Financial Management, Inc. (“BlackRock”)

ClearBridge Investments, LLC (“ClearBridge”)

Columbia Management Investment Advisers, LLC (“Columbia”)

Delaware Investments Fund Advisers, a member of Macquarie Investment Management Business Trust (“DIFA”)

Lazard Asset Management LLC (“Lazard”)

Lyrical Asset Management LP (“Lyrical”)

| PORTFOLIO MANAGERS |

SUB-ADVISER OR ADVISER |

FUND’S PORTFOLIO

MANAGER SINCE |

| Jennifer Hsui, CFA® Managing Director and Senior Portfolio Engineer |

BlackRock |

2018 |

| Paul Whitehead, Managing Director, Co-Head of Index Equity |

BlackRock |

2022 |

| Peter Sietsema, CFA® Director and Senior Portfolio Manager |

BlackRock |

2022 |

| Amy Whitelaw, Managing Director and Senior Portfolio Engineer |

BlackRock |

2017 |

| Peter Bourbeau, Managing Director and Portfolio Manager |

ClearBridge |

2017 |

| Margaret Vitrano, Managing Director and Portfolio Manager |

ClearBridge |

2017 |

| Richard Carter, Senior Portfolio Manager |

Columbia |

2016 |

| Thomas Galvin, CFA®, Senior Portfolio Manager and Head of Focused Large Cap Growth |

Columbia |

2016 |

| Todd Herget, Senior Portfolio Manager |

Columbia |

2016 |

| Kristen E. Bartholdson, Managing Director and Senior Portfolio Manager |

DIFA |

2016 |

| Nikhil G. Lalvani, CFA®, Managing Director, Senior Portfolio Manager and Team Leader |

DIFA |

2016 |

| Robert A. Vogel Jr., CFA®, Managing Director and Senior Portfolio Manager |

DIFA |

2016 |

| Erin Ksenak, Vice President, Portfolio Manager |

DIFA |

2020 |

| Christopher H. Blake, Managing Director and Portfolio Manager/Analyst |

Lazard |

2016 |

| Martin Flood, Managing Director and Portfolio Manager/Analyst |

Lazard |

2016 |

| Jay Levy, Director and Portfolio Manager/ Analyst |

Lazard |

2022 |

| John Mullins, Associate Portfolio Manager |

Lyrical |

2019 |

| Andrew Wellington, Managing Partner and Chief Investment Officer |

Lyrical |

2016 |

| Dan Kaskawits, Associate Portfolio Manager |

Lyrical |

2019 |

Purchase and sale of Fund shares

Purchases of shares of the Fund must be made through an investment advisory program with Morgan Stanley. You may purchase or sell shares of the Fund at net asset value on any day the New York Stock Exchange (“NYSE”) is open by contacting your Morgan Stanley Financial Advisor.

| • |

The minimum initial aggregate investment in the Morgan Stanley-sponsored investment advisory programs is $1,000. |

| • |

There is no minimum on additional investments in the Fund or the applicable investment advisory program through which you invest. |

| • |

Each of the Fund and the Morgan Stanley-sponsored investment advisory programs through which investments in the Fund are offered may vary or waive these investment minimums at any time. |

For more information about the Morgan Stanley-sponsored investment advisory programs, see the About the Funds section of this Prospectus.

Tax information

The Fund’s distributions are generally taxable to you as ordinary income, capital gains, or a combination of the two.

Payments to financial intermediaries

If you purchase shares of the Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your sales person to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

Small-Mid Cap Equity Fund

Investment objective

Capital appreciation.

Fund fees and expenses

This table describes the fees and expenses you may pay if you buy and hold shares of the Fund.

Annual Advisory Program Fees

(fees paid directly from your investment in the applicable Morgan Stanley-sponsored investment advisory program)

| Maximum annual fees in the Consulting Group Advisor, Select UMA or Portfolio Management investment advisory programs (as a percentage of prior quarter-end net assets)* |

2.00% |

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment in the Fund)

| Management Fees* |

0.80% |

| Distribution (12b-1) Fees |

None |

| Other Expenses |

0.13% |

| Total Annual Fund Operating Expenses |

0.93% |

| Waiver* |

(0.34)% |

| Net Annual Fund Operating Expenses* |

0.59% |

* CGAS (defined herein) has contractually agreed to waive fees and reimburse expenses in order to keep the Fund’s management fees from exceeding the total amount of sub-advisory fees paid by CGAS plus 0.20% based on average net assets. This contractual waiver will only apply if the Fund’s total management fees exceed the total amount of sub-advisory fees paid by CGAS plus 0.20% and will not affect the Fund’s total management fees if they are less than such amount. This fee waiver and/or reimbursement will continue for at least one year from the date of this prospectus or until such time as the Board of Trustees acts to discontinue all or a portion of such waiver and/or reimbursement when they deem such action is appropriate.

Examples

These examples are intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The examples assume that you invest $10,000 in the Fund for the time periods indicated. The examples also assume that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. The effect of the Fund’s contractual fee waiver is only reflected in the first year of the example. The figures are calculated based upon total annual Fund operating expenses and a maximum annual fee of 2.00% for the applicable Morgan Stanley-sponsored investment advisory program through which you invest. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

AFTER

1 YEAR |

AFTER

3 YEARS |

AFTER

5 YEARS |

AFTER

10 YEARS |

| $262 |

$875 |

$1,513 |

$3,228 |

Portfolio turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the above examples, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 41% of the average value of its portfolio.

Principal investment strategies

The Fund will invest, under normal market conditions, at least 80% of its net assets (plus the amount of any borrowing for investment purposes) in the equity securities of small-mid capitalization (or “cap”) companies or in other investments with similar economic characteristics. The Fund defines small-mid cap companies as companies with market caps not exceeding the highest month-end market cap value of any stock in the Russell 2500® or Russell Mid Cap Index for the previous 12 months, whichever is greater. The Fund may invest up to 10% of its assets in the securities of foreign issuers that are not traded on a U.S. exchange or the U.S. over-the-counter market. The Fund may also lend portfolio securities to earn additional income. Any income realized through securities lending may help Fund performance.

The Fund employs a “multi-manager” strategy whereby portions of the Fund are allocated to professional money managers (each, a “Sub-adviser,” collectively, the “Sub-advisers”) who are responsible for investing the assets of the Fund.

Principal risks of investing in the Fund

Loss of money is a risk of investing in the Fund.

The Fund’s principal risks include:

| • |

Market Risk, which is the risk that stock prices decline overall. Markets are volatile and can decline significantly in response to real or perceived adverse issuer, political, regulatory, market or economic developments in the U.S. and in other countries. Similarly, environmental and public health risks, such as natural disasters, epidemics, pandemics or widespread fear that such events may occur, may impact markets adversely and cause market volatility in both the short and long-term. Market risk may affect a single company, sector of the economy or the market as a whole. |

| • |

Equity Risk, which is the risk that prices of equity securities rise and fall daily due to factors affecting individual companies, particular industries or the equity market as a whole. |

| • |

Exchange-Traded Funds (“ETFs”) Risk, which is the risk of owning shares of an ETF and generally reflects the risks of owning the underlying securities the ETF is designed to track, although lack of liquidity in an ETF could result in its value being more volatile than the underlying portfolio |

| |

securities. When the Fund invests in an ETF, in addition to directly bearing the expenses associated with its own operations, it will bear a pro rata portion of the ETF’s expenses. |

| • |

Investment Style Risk, which means small cap and/or growth stocks could fall out of favor with investors and trail the performance of other types of investments. |

| • |

Small-Mid Cap Risk, which refers to the fact that historically, small-mid cap companies tend to be more vulnerable to adverse business and economic events, have been more sensitive to changes in earnings results and forecasts and investor expectations, and experience sharper swings in market values than larger, more established companies. At times, small-mid cap stocks may be less liquid and harder to sell at prices the Sub-advisers believe are appropriate. |

| • |

Foreign Investment Risk, which means risks unique to foreign securities, including less information about foreign issuers, less liquid securities markets, political instability and unfavorable changes in currency exchange rates. |

| • |

Securities Lending Risk, which includes the potential insolvency of a borrower and losses due to the re-investment of collateral received on loaned securities in investments that default or do not perform well. |

| • |

Manager Risk, which is the risk that poor security selection by a Sub-adviser will cause the Fund to underperform. This risk is common for all actively managed funds. |

| • |

Multi-Manager Risk, which is the risk that the investment styles of the Sub-advisers may not complement each other as expected by the Manager. The Fund may experience a higher portfolio turnover rate, which can increase the Fund’s transaction costs and result in more taxable short-term gains for shareholders. |

| • |

Issuer Risk, which is the risk that the value of a security may decline for reasons directly related to the issuer, such as management performance, financial leverage and reduced demand for the issuer’s goods or services. |

| • |

Sector Risk, which is the risk that the value of securities in a particular industry or sector will decline because of changing expectations for the performance of that industry or sector. From time to time, based on market or economic conditions, the Fund may have significant positions in one or more sectors of the market. To the extent the Fund invests more heavily in particular sectors, its performance will be especially sensitive to developments that significantly affect those sectors. Individual sectors may be more volatile, and may perform differently, than the broader market. The industries that constitute a sector may all react in the same way to economic, political or regulatory events. |

An investment in the Fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. For more information on the risks of investing in the Fund please see the Fund details section of this Prospectus.

Performance

The bar chart below shows how the Fund’s investment results have varied from year to year, and the following table shows how the Fund’s annual total returns for various periods compare to those of the Fund’s benchmark index and Lipper peer group. This information provides some indication of the risks of investing in the Fund. The Fund is available only to investors participating in Morgan Stanley-sponsored investment advisory programs. These programs charge an annual fee (see Annual Advisory Program Fees above). The performance information in the bar chart and table below does not reflect this fee, which would reduce your return. The Fund’s past performance, before and after taxes, does not necessarily indicate how the Fund will perform in the future. For current performance information please see www.morganstanley.com/wealth-investmentsolutions/cgcm.

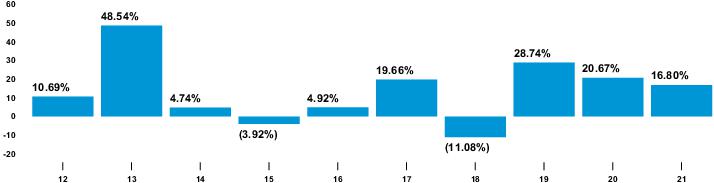

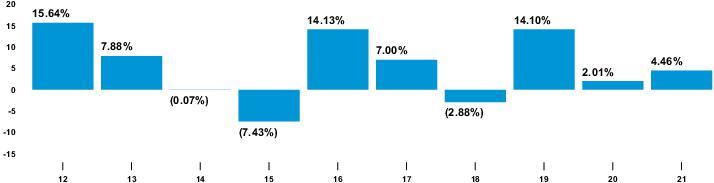

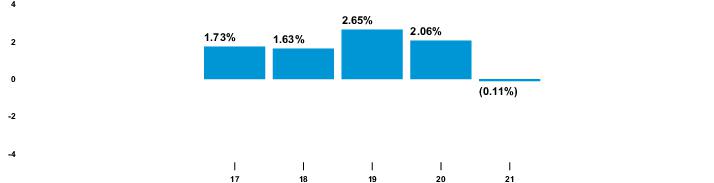

Annual total returns (%) calendar years

Small-Mid Cap Equity Fund

Fund’s best and worst calendar quarters

Best: 25.93% in 4th quarter 2020

Worst: (26.41)% in 1st quarter 2020

Year-to-date: (24.45)% (through 3rd quarter 2022)

Average Annual Total Returns

(for the periods ended December 31, 2021)

| INCEPTION DATE: 11/18/1991 |

1 YEAR |

5 YEARS |

10 YEARS |

| Fund (without advisory program fee) |

| Return Before Taxes |

16.80% |

14.06% |

12.86% |

| Return After Taxes on Distributions |

10.31% |

10.69% |

9.65% |

| Return After Taxes on Distributions and Sale of Fund Shares |

12.52% |

10.24% |

9.51% |

| Russell 2500® Index (reflects no deduction for fees, expenses or taxes) |

18.18% |

13.75% |

14.15% |

| Lipper Small-Cap Core Funds Average |

25.11% |

10.64% |

12.24% |

The after-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an individual investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. In some cases, the return after taxes may exceed the return before taxes due to an assumed tax benefit from any losses on a sale of Fund shares at the end of the measurement period.

The Fund’s benchmark is the Russell 2500® Index. The Russell 2500® Index includes the smallest 2,500 U.S. companies out of the Russell 3000® Index universe. Unlike the Fund, the benchmark is unmanaged and does not include any fees or expenses. An investor cannot invest directly in an index.

The Fund also compares its performance with the Lipper Small-Cap Core Funds Average, which is a secondary benchmark and includes funds that invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) less than 250% of the dollar-weighted median of the smallest 500 of the middle 1,000 securities of the S&P SuperComposite 1500® Index.

Investment adviser

Consulting Group Advisory Services LLC (“CGAS” or the “Manager”), a business of Morgan Stanley Wealth Management (“MSWM”), serves as the investment adviser for the Fund. Subject to Board review, the Manager selects and oversees professional money managers (each a “Sub-adviser,” collectively, the “Sub-advisers”) who are responsible for investing the assets of the Fund. The Sub-advisers are selected based primarily upon the research and recommendation of the Manager, which includes a quantitative and qualitative evaluation of a Sub-adviser’s skills and investment results in managing assets for specific asset classes, investment styles and strategies. The Manager allocates and, when appropriate, reallocates the Fund’s assets among one or more Sub-advisers, continuously monitors and evaluates Sub-adviser performance (including trade execution), performs other due diligence functions (such as an assessment of changes in personnel or other developments at the Sub-advisers), and oversees Sub-adviser compliance with the Fund’s investment objectives, policies and guidelines. The Manager also monitors changes in market conditions and considers whether changes in the allocation of Fund assets or the lineup of Sub-advisers should be made in response to such changes in market conditions. Sub-advisers may also periodically recommend changes or enhancements to the Fund’s investment objectives, policies and guidelines, which are subject to the approval of the Manager and may also be subject to the approval of the Board.

Sub-advisers and portfolio managers

Aristotle Capital Boston, LLC (“Aristotle”)

BlackRock Financial Management, Inc. (“BlackRock”)

D.F. Dent & Company, Inc. (“DF Dent”)

Neuberger Berman Investment Advisers LLC (“Neuberger”)

Nuance Investments, LLC (“Nuance”)

Westfield Capital Management Company, L.P. (“Westfield”)

| PORTFOLIO MANAGERS |

SUB-ADVISER OR ADVISER |

FUND’S PORTFOLIO

MANAGER SINCE |

| David Adams, CFA®, CEO, Principal and Portfolio Manager |

Aristotle |

2019 |

| Jack McPherson, CFA®, President, Principal and Portfolio Manager |

Aristotle |

2019 |

| Jennifer Hsui, CFA® Managing Director and Senior Portfolio Engineer |

BlackRock |

2018 |

| Paul Whitehead, Managing Director, Co-Head of Index Equity |

BlackRock |

2022 |

| Peter Sietsema, CFA® Director and Senior Portfolio Manager |

BlackRock |

2022 |

| Amy Whitelaw, Managing Director and Senior Portfolio Engineer |

BlackRock |

2017 |

| Matthew F. Dent, CFA®, President |

DF Dent |

2019 |

| Bruce L. Kennedy II, CFA®, Vice President |

DF Dent |

2019 |

| Gary D. Mitchell, Vice President |

DF Dent |

2019 |

| Thomas F. O’Neil, Jr, CFA®, Vice President |

DF Dent |

2019 |

| Benjamin H. Nahum, Managing Director |

Neuberger |

2016 |

| Chad Baumler, CFA®, Vice-President and Co-CIO |

Nuance |

2019 |

| Scott Moore, CFA®, President and Co-CIO |

Nuance |

2019 |

| Darren Schryer, CFA®, CPA, Portfolio Manager |

Nuance |

2020 |

| Jack Meurer, CFA®, Associate Portfolio Manager |

Nuance |

2022 |

| Richard D. Lee, CFA®, Managing Partner and Deputy CIO |

Westfield |

2004 |

| Ethan J. Meyers, CFA®, Managing Partner and Director of Research |

Westfield |

2004 |

| John M. Montgomery, Managing Partner, COO and Portfolio Strategist |

Westfield |

2006 |

| William A. Muggia, President, CEO and CIO |

Westfield |

2004 |

Purchase and sale of Fund shares

Purchases of shares of the Fund must be made through an investment advisory program with Morgan Stanley. You may purchase or sell shares of the Fund at net asset value on any day the New York Stock Exchange (“NYSE”) is open by contacting your Morgan Stanley Financial Advisor.

| • |

The minimum initial aggregate investment in the Morgan Stanley-sponsored investment advisory programs is $1,000. |

| • |

There is no minimum on additional investments in the Fund or the applicable investment advisory program through which you invest. |

| • |

Each of the Fund and the Morgan Stanley-sponsored investment advisory programs through which investments in the Fund are offered may vary or waive these investment minimums at any time. |

For more information about the Morgan Stanley-sponsored investment advisory programs, see the About the Funds section of this Prospectus.

Tax information

The Fund’s distributions are generally taxable to you as ordinary income, capital gains, or a combination of the two.

Payments to financial intermediaries

If you purchase shares of the Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your sales person to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

International Equity Fund

Investment objective

Capital appreciation.

Fund Fees and Expenses

This table describes the fees and expenses you may pay if you buy and hold shares of the Fund.

Annual Advisory Program Fees

(fees paid directly from your investment in the applicable Morgan Stanley-sponsored investment advisory program)

| Maximum annual fees in the Consulting Group Advisor, Select UMA, or Portfolio Management investment advisory programs (as a percentage of average prior quarter-end net assets)* |

2.00% |

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment in the Fund)

| Management Fees* |

0.70% |

| Distribution (12b-1) Fees |

None |

| Other Expenses |

0.15% |

| Total Annual Fund Operating Expenses |

0.85% |

| Waiver* |

(0.18)% |

| Net Annual Fund Operating Expenses* |

0.67% |

* CGAS (defined herein) has contractually agreed to waive fees and reimburse expenses in order to keep the Fund’s management fees from exceeding the total amount of sub-advisory fees paid by CGAS plus 0.20% based on average net assets. This contractual waiver will only apply if the Fund’s total management fees exceed the total amount of sub-advisory fees paid by CGAS plus 0.20% and will not affect the Fund’s total management fees if they are less than such amount. This fee waiver and/or reimbursement will continue for at least one year from the date of this prospectus or until such time as the Board of Trustees acts to discontinue all or a portion of such waiver and/or reimbursement when they deem such action is appropriate.

Examples

These examples are intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The examples assume that you invest $10,000 in the Fund for the time periods indicated. The examples also assume that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. The effect of the Fund’s contractual fee waiver is only reflected in the first year of the example. The figures are calculated based upon total annual Fund operating expenses and a maximum annual fee of 2.00% for the applicable Morgan Stanley-sponsored investment advisory program through which you invest. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

AFTER

1 YEAR |

AFTER

3 YEARS |

AFTER

5 YEARS |

AFTER

10 YEARS |

| $270 |

$866 |

$1,488 |

$3,163 |

Portfolio turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the above examples, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 38% of the average value of its portfolio.

Principal investment strategies

The Fund will invest, under normal market conditions, at least 80% of its net assets (plus the amount of any borrowing for investment purposes) in the equity securities of companies located outside the U.S. The Fund focuses on companies located in developed markets, but also may invest a portion of its assets in securities of companies located in emerging markets. The Fund intends to diversify its assets by investing primarily in securities of issuers located in at least three foreign countries. The Fund may attempt to hedge against unfavorable changes in currency exchange rates by engaging in forward currency transactions or currency swaps and trading currency futures contracts and options on these futures. However, a Sub-adviser (as defined below) may choose not to, or may be unable to, hedge the Fund’s currency exposure. The Fund may also lend portfolio securities to earn additional income. Any income realized through securities lending may help Fund performance.

The Fund employs a “multi-manager” strategy whereby portions of the Fund are allocated to professional money managers (each, a “Sub-adviser,” collectively, the “Sub-advisers”) who are responsible for investing the assets of the Fund.

Principal risks of investing in the Fund

Loss of money is a risk of investing in the Fund.

The Fund’s principal risks include:

| • |

Market Risk, which is the risk that stock prices decline overall. Markets are volatile and can decline significantly in response to real or perceived adverse issuer, political, regulatory, market or economic developments in the U.S. and in other countries. Similarly, environmental and public health risks, such as natural disasters, epidemics, pandemics or widespread fear that such events may occur, may impact markets adversely and cause market volatility in both the short and long-term. Market risk may affect a single company, sector of the economy or the market as a whole. |

| • |

Equity Risk, which is the risk that prices of equity securities rise and fall daily due to factors affecting individual companies, particular industries or the equity market as a whole. |

| • |

Foreign Investment Risk, which means risks unique to foreign securities, including less information about foreign issuers, less liquid securities markets, political instability and unfavorable changes in currency exchange rates. |

| • |

Currency Risk, which refers to the risk that as a result of the Fund’s investments in securities denominated in, and/or receiving revenues in, foreign currencies, those currencies will decline in value relative to the U.S. dollar or, in the case of hedged positions, the U.S. dollar will decline in value relative to the currency hedged. |

| • |

Forwards, Futures, Options and Swaps Risk, which means that the Fund’s use of forwards, futures, options and swaps to enhance returns or hedge against market declines subjects the Fund to potentially greater volatility and/or losses. Even a small investment in forwards, futures, options or swaps can have a large impact on the Fund’s interest rate, securities market and currency exposure. Therefore, using forwards, futures, options or swaps can disproportionately increase losses and reduce opportunities for gains when interest rates, stock prices or currency rates are changing. The Fund may not fully benefit from or may lose money on its investment in forwards, futures, options or swaps if changes in their value do not correspond accurately to changes in the value of the Fund’s holdings. Investing in forwards, futures, options or swaps can also make the Fund’s assets less liquid and harder to value, especially in declining markets. The Fund may hold illiquid securities that may be difficult to sell and may be required to be fair valued. |

| • |

Emerging Markets Risk, emerging markets countries, which are generally defined as countries that may be represented in a market index such as the MSCI Emerging Markets Index (Net) or having per capita income in the low to middle ranges, as determined by the World Bank. In addition to foreign investment and currency risks, emerging markets may experience rising interest rates, or, more significantly, rapid inflation or hyperinflation. Emerging market securities may present market, credit, liquidity, legal, political and other risks different from, or greater than, the risks of investing in developed foreign countries. The Fund also could experience a loss from settlement and custody practices in some emerging markets. |

| • |

Small and Mid Cap Risk, which refers to the fact that historically, small and mid cap stocks tend to be more vulnerable to adverse business and economic events, more sensitive to changes in earnings results and forecasts and investor expectations and will experience sharper swings in market values than larger, more established companies. At times, small and mid cap stocks may be less liquid and harder to sell at prices the Sub-advisers believe are appropriate. |

| • |

Securities Lending Risk, which includes the potential insolvency of a borrower and losses due to the re-investment of collateral received on loaned securities in investments that default or do not perform well. |

| • |

Manager Risk, which is the risk that poor security selection by a Sub-adviser will cause the Fund to underperform. This risk is common for all actively managed funds. |

| • |

Multi-Manager Risk, which is the risk that the investment styles of the Sub-advisers may not complement each other |

| |

as expected by the Manager. The Fund may experience a higher portfolio turnover rate, which can increase the Fund’s transaction costs and result in more taxable short-term gains for shareholders. |

| • |

LIBOR Transition Risk refers to the fact that the elimination of the London Inter-Bank Offered Rate (“LIBOR”) rate may adversely affect the interest rates on, and value of, certain Fund investments that are tied to LIBOR. The U.K. Financial Conduct Authority stopped compelling or inducing banks to submit certain LIBOR rates and will do so for the remaining LIBOR rates immediately after June 30, 2023. Alternatives to LIBOR are established or in development in most major currencies and markets are slowly responding to these new rates. It is difficult to predict the full impact of the transition away from LIBOR on the Fund. |

| • |

Issuer Risk, which is the risk that the value of a security may decline for reasons directly related to the issuer, such as management performance, financial leverage and reduced demand for the issuer’s goods or services. |

| • |

Sector Risk, which is the risk that the value of securities in a particular industry or sector will decline because of changing expectations for the performance of that industry or sector. From time to time, based on market or economic conditions, the Fund may have significant positions in one or more sectors of the market. To the extent the Fund invests more heavily in particular sectors, its performance will be especially sensitive to developments that significantly affect those sectors. Individual sectors may be more volatile, and may perform differently, than the broader market. The industries that constitute a sector may all react in the same way to economic, political or regulatory events. |

An investment in the Fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. For more information on the risks of investing in the Fund please see the Fund details section of this Prospectus.

Performance

The bar chart below shows how the Fund’s investment results have varied from year to year, and the following table shows how the Fund’s annual total returns for various periods compare to those of the Fund’s benchmark index and Lipper peer group. This information provides some indication of the risks of investing in the Fund. The Fund is available only to investors participating in Morgan Stanley-sponsored investment advisory programs. These programs charge an annual fee (see Annual Advisory Program Fees above). The performance information in the bar chart and table below does not reflect this fee, which would reduce your return. The Fund’s past performance, before and after taxes, does not necessarily indicate how the Fund will perform in the future. For current performance information please see www.morganstanley.com/wealth-investmentsolutions/cgcm.

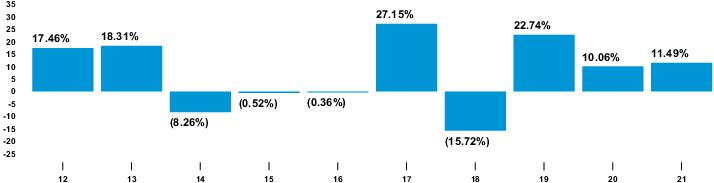

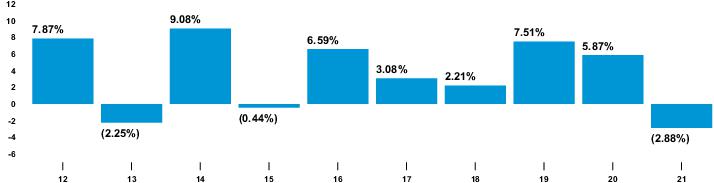

Annual total returns (%) calendar years

International Equity Fund

Fund’s best and worst calendar quarters

Best: 17.79% in 4th quarter 2020

Worst: (25.29)% in 1st quarter 2020

Year-to-date: (28.08)% (through 3rd quarter 2022)

Average Annual Total Returns

(for the periods ended December 31, 2021)

| INCEPTION DATE: 11/18/1991 |

1 YEAR |

5 YEARS |

10 YEARS |

| Fund (without advisory program fee) |

| Return Before Taxes |

11.49% |

10.05% |

7.39% |

| Return After Taxes on Distributions |

8.79% |

9.21% |

6.81% |

| Return After Taxes on Distributions and Sale of Fund Shares |

7.90% |

7.92% |

5.96% |

| MSCI EAFE® Index (Net) (reflects no deduction for fees, expenses or taxes) |

11.26% |

9.55% |

8.03% |

| Lipper International Large-Cap Core Funds Average |

10.75% |

9.34% |

7.13% |

The after-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an individual investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. In some cases, the return after taxes may exceed the return before taxes due to an assumed tax benefit from any losses on a sale of Fund shares at the end of the measurement period.

The Fund’s benchmark is the MSCI EAFE® Index (Net). The Benchmark is a composite portfolio of equity total returns for developed countries in Europe and the Far East and Australia and New Zealand. Unlike the Fund, the benchmark is unmanaged and does not include any fees or expenses. An investor cannot invest directly in an index.

The Fund also compares its performance with the Lipper International Large-Cap Core Funds Average. The Lipper International Large-Cap Core Funds Average is composed of funds that, by fund practice, invest at least 75% of their equity assets in companies strictly outside of the U.S., with market capitalizations (on a three-year weighted basis) greater than the 250th largest companies in the S&P/Citigroup World ex-U.S. Broad Market® Index (“BMI®”). Large cap core securities typically have an average price-to-cash ratio, price-to-book ratio, and three year sales-per-year growth value, compared to S&P/Citigroup World ex-U.S. BMI®.

Investment adviser

Consulting Group Advisory Services LLC (“CGAS” or the “Manager”), a business of Morgan Stanley Wealth Management (“MSWM”), serves as the investment adviser for the Fund. Subject to Board review, the Manager selects and oversees professional money managers (each a “Sub-adviser,” collectively, the “Sub-advisers”) who are responsible for investing the assets of the Fund. The Sub-advisers are selected based primarily upon the research and recommendation of the Manager, which includes a quantitative and qualitative evaluation of a Sub-adviser’s skills and investment results in managing assets for specific asset classes, investment styles and strategies. The Manager allocates and, when appropriate, reallocates the Fund’s assets among one or more Sub-advisers, continuously monitors and evaluates Sub-adviser performance (including trade execution), performs other due diligence functions (such as an assessment of changes in personnel or other developments at the Sub-advisers), and oversees Sub-adviser compliance with the Fund’s investment objectives, policies and guidelines. The Manager also monitors changes in market conditions and considers whether changes in the allocation of Fund assets or the lineup of Sub-advisers should be made in response to such changes in market conditions. Sub-advisers may also periodically recommend changes or enhancements to the Fund’s investment objectives, policies and guidelines, which are subject to the approval of the Manager and may also be subject to the approval of the Board.

Sub-advisers and portfolio managers

BlackRock Financial Management, Inc. (“BlackRock”)

Causeway Capital Management LLC (“Causeway”)

Schroder Investment Management North America Inc. (“Schroders”)

Victory Capital Management, Inc. (“Victory Capital”)

Walter Scott & Partners Limited (“Walter Scott”)

| PORTFOLIO MANAGERS |

SUB-ADVISER OR ADVISER |

FUND’S PORTFOLIO

MANAGER SINCE |

| Jennifer Hsui, CFA® Managing Director and Senior Portfolio Engineer |

BlackRock |

2018 |

| Paul Whitehead, Managing Director, Co-Head of Index Equity |

BlackRock |

2022 |

| Peter Sietsema, CFA® Director and Senior Portfolio Manager |

BlackRock |

2022 |

| Amy Whitelaw, Managing Director and Senior Portfolio Engineer |

BlackRock |

2017 |

| Brian Cho, Portfolio Manager |

Causeway |

2021 |

| Jonathan P. Eng, Portfolio Manager |

Causeway |

2014 |

| Harry W. Hartford, President and Portfolio Manager |

Causeway |

2014 |

| Sarah H. Ketterer, Chief Executive Officer and Portfolio Manager |

Causeway |

2014 |

| Ellen Lee, Portfolio Manager |

Causeway |

2015 |

| Conor S. Muldoon, CFA®, Portfolio Manager |

Causeway |

2014 |

| Steven Nguyen, Portfolio Manager |

Causeway |

2019 |

| Alessandro Valentini, CFA®, Portfolio Manager |

Causeway |

2014 |

| James Gautrey, CFA®, Portfolio Manager |

Schroders |

2014 |

| Simon Webber, CFA®, Portfolio Manager |

Schroders |

2011 |

| Daniel B. LeVan, CFA®, Chief Investment Officer of Trivalent Investments, a Victory Capital investment franchise |

Victory Capital |

2017 |

| John W. Evers, CFA®, Senior Portfolio Manager |

Victory Capital |

2017 |

| Jane Henderson, Managing Director |

Walter Scott |

2021 |

| Charles Macquaker, Executive Director - Investment |

Walter Scott |

2021 |

| Roy Leckie, Executive Director – Investment & Client Service |

Walter Scott |

2021 |

| Maxim Skorniakov |

Walter Scott |

2022 |

| Fraser Fox |

Walter Scott |

2022 |

Purchase and sale of Fund shares

Purchases of shares of the Fund must be made through an investment advisory program with Morgan Stanley. You may purchase or sell shares of the Fund at net asset value on any day the New York Stock Exchange (“NYSE”) is open by contacting your Morgan Stanley Financial Advisor.

| • |

The minimum initial aggregate investment in the Morgan Stanley-sponsored investment advisory programs is $1,000. |

| • |

There is no minimum on additional investments in the Fund or the applicable investment advisory program through which you invest. |

| • |

Each of the Fund and the Morgan Stanley-sponsored investment advisory programs through which investments in the Fund are offered may vary or waive these investment minimums at any time. |

For more information about the Morgan Stanley-sponsored investment advisory programs, see the About the Funds section of this Prospectus.

Tax information

The Fund’s distributions are generally taxable to you as ordinary income, capital gains, or a combination of the two.

Payments to financial intermediaries

If you purchase shares of the Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your sales person to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

Emerging Markets Equity Fund

Investment objective

Long-term capital appreciation.

Fund Fees and Expenses

This table describes the fees and expenses you may pay if you buy and hold shares of the Fund.

Annual Advisory Program Fees

(fees paid directly from your investment in the applicable Morgan Stanley-sponsored investment advisory program)

| Maximum annual fees in the Consulting Group Advisor, Select UMA, or Portfolio Management investment advisory programs (as a percentage of average prior quarter-end net assets)* |

2.00% |

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment in the Fund)

| Management Fees* |

0.90% |

| Distribution (12b-1) Fees |

None |

| Other Expenses |

0.25% |

| Total Annual Fund Operating Expenses |

1.15% |

| Waiver* |

(0.34)% |

| Net Annual Fund Operating Expenses* |

0.81% |

* CGAS (defined herein) has contractually agreed to waive fees and reimburse expenses in order to keep the Fund’s management fees from exceeding the total amount of sub-advisory fees paid by CGAS plus 0.20% based on average net assets. This contractual waiver will only apply if the Fund’s total management fees exceed the total amount of sub-advisory fees paid by CGAS plus 0.20% and will not affect the Fund’s total management fees if they are less than such amount. This fee waiver and/or reimbursement will continue for at least one year from the date of this prospectus or until such time as the Board of Trustees acts to discontinue all or a portion of such waiver and/or reimbursement when they deem such action is appropriate.

Examples

These examples are intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The examples assume that you invest $10,000 in the Fund for the time periods indicated. The examples also assume that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. The effect of the Fund’s contractual fee waiver is only reflected in the first year of the example. The figures are calculated based upon total annual Fund operating expenses and a maximum annual fee of 2.00% for the applicable Morgan Stanley-sponsored investment advisory program through which you invest. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

AFTER

1 YEAR |

AFTER

3 YEARS |

AFTER

5 YEARS |

AFTER

10 YEARS |

| $284 |

$940 |

$1,620 |

$3,434 |

Portfolio turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the above examples, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 14% of the average value of its portfolio.

Principal investment strategies

The Fund will invest, under normal market conditions, at least 80% of its net assets (plus the amount of any borrowing for investment purposes) in equity securities of issuers organized, domiciled or with substantial operations in emerging markets countries, which are defined as countries included in an emerging markets index by a recognized index provider, such as the MSCI Emerging Markets Index (Net), or characterized as developing or emerging by any of the World Bank, the United Nations, the International Finance Corporation, or the European Bank for Reconstruction and Development. Certain emerging market countries may also be classified as “frontier” market countries, which are a subset of emerging countries with even smaller national economies. To diversify its investments, the Fund invests primarily in securities of issuers located in at least three foreign countries. The Fund also may invest a portion of its assets in closed-end investment companies that invest in emerging markets. The Fund may attempt to hedge against unfavorable changes in currency exchange rates by engaging in forward currency transactions and trading currency futures contracts and options on these futures; however, a Sub-adviser (as defined below) may choose not to, or may be unable to, hedge the Fund’s currency exposure. The Fund may also lend portfolio securities to earn additional income. Any income realized through securities lending may help Fund performance.

The Fund employs a “multi-manager” strategy whereby portions of the Fund are allocated to professional money managers (each, a “Sub-adviser,” collectively, the “Sub-advisers”) who are responsible for investing the assets of the Fund.

Principal risks of investing in the Fund

Loss of money is a risk of investing in the Fund.

The Fund’s principal risks include:

| • |

Market Risk, which is the risk that stock prices decline overall. Markets are volatile and can decline significantly in response to real or perceived adverse issuer, political, regulatory, market or economic developments in the U.S. and in other countries. Similarly, environmental and public health risks, such as natural disasters, epidemics, pandemics or widespread fear that such events may occur, may impact markets adversely and cause market volatility in both the short and long-term. Market risk may affect a single company, sector of the economy or the market as a whole. |

| • |

Equity Risk, which is the risk that prices of equity securities rise and fall daily due to factors affecting individual companies, particular industries or the equity market as a whole. |

| • |

Foreign Investment Risk, which means risks unique to foreign securities, including less information about foreign issuers, less liquid securities markets, political instability and unfavorable changes in currency exchange rates. |

| • |

Emerging Markets and Frontier Markets Risk, emerging markets countries, which are generally defined as countries that may be represented in a market index such as the MSCI Emerging Markets Index (Net) or having per capita income in the low to middle ranges, as determined by the World Bank. Certain emerging market countries may also be classified as “frontier” market countries, which are a subset of emerging countries with even smaller national economies. In addition to foreign investment and currency risks, emerging markets may experience rising interest rates, or, more significantly, rapid inflation or hyperinflation. Emerging market securities may present market, credit, liquidity, legal, political and other risks different from, or greater than, the risks of investing in developed foreign countries. The Fund also could experience a loss from settlement and custody practices in some emerging markets. These risks tend to be even more prevalent in frontier market countries. The economies of frontier market countries tend to be less correlated to global economic cycles than the economies of more developed countries and their markets have lower trading volumes and may exhibit greater price volatility and illiquidity. A small number of large investments in these markets may affect these markets more than more developed markets. Frontier market countries may also be more affected by government activities than more developed countries. For example, the governments of frontier market countries may exercise substantial influence within the private sector or subject investments to government approval, and governments of other countries may impose or negotiate trade barriers, exchange controls, adjustments to relative currency values and other measures that adversely affect a frontier market country. Governments of other countries may also impose sanctions or embargoes on frontier market countries. |

| |

Although all of these risks are generally heightened with respect to frontier market countries, they also apply to emerging market countries. |

| • |

Currency Risk, which refers to the risk that as a result of the Fund’s investments in securities denominated in, and/or receiving revenues in, foreign currencies, those currencies will decline in value relative to the U.S. dollar or, in the case of hedged positions, the U.S. dollar will decline in value relative to the currency hedged. |

| • |

Forwards, Futures and Options Risk, which means that the Fund’s use of forwards, futures and options to enhance returns or hedge against market declines subjects the Fund to potentially greater volatility and/or losses. Even a small investment in forwards, futures or options can have a large impact on the Fund’s Interest rate, securities market and currency exposure. Therefore, using forwards, futures or options can disproportionately increase losses and reduce opportunities for gains when interest rates, stock prices or currency rates are changing. The Fund may not fully benefit from or may lose money on its investment in forwards, futures or options if changes in their value do not correspond accurately to changes in the value of the Fund’s holdings. Investing in forwards, futures or options can also make the Fund’s assets less liquid and harder to value, especially in declining markets. The Fund may hold illiquid securities that may be difficult to sell and may be required to be fair valued. |

| • |

Closed-End Investment Company Risk, which means that since closed-end investment companies issue a fixed number of shares they typically trade on a stock exchange or over-the-counter at a premium or discount to their net asset value per share. The Fund will also bear its pro rata portion of any costs of a closed-end fund in which it invests. |

| • |

Securities Lending Risk, which includes the potential insolvency of a borrower and losses due to the re-investment of collateral received on loaned securities in investments that default or do not perform well. |

| • |

Strategy Risk, the Fund invests a portion of its assets in stocks believed by a Sub-adviser to be undervalued, but that may not realize their perceived value for extended periods of time or may never realize their perceived value. The Fund also invests a portion of its assets in stocks believed by a Sub-adviser to have the potential for growth, but that may not realize such perceived growth potential for extended periods of time or may never realize such perceived growth potential. Such stocks may be more volatile than other stocks because they can be more sensitive to investor perceptions of the issuing company’s growth potential. The stocks in which the Fund invests may respond differently to market and other developments than other types of stocks. |

| • |

Manager Risk, which is the risk that poor security selection by a Sub-adviser will cause the Fund to underperform. This risk is common for all actively managed funds. |

| • |

Multi-Manager Risk, which is the risk that the investment styles of the Sub-advisers may not complement each other as expected by the Manager. The Fund may experience a |

| |

higher portfolio turnover rate, which can increase the Fund’s transaction costs and result in more taxable short-term gains for shareholders. |

| • |

Issuer Risk, which is the risk that the value of a security may decline for reasons directly related to the issuer, such as management performance, financial leverage and reduced demand for the issuer’s goods or services. |

| • |

LIBOR Transition Risk, refers to the fact that the elimination of the London Inter-Bank Offered Rate (“LIBOR”) rate may adversely affect the interest rates on, and value of, certain Fund investments that are tied to LIBOR. The U.K. Financial Conduct Authority stopped compelling or inducing banks to submit certain LIBOR rates will do so for the remaining LIBOR rates immediately after June 30, 2023. Alternatives to LIBOR are established or in development in most major currencies and markets are slowly responding to these new rates. It is difficult to predict the full impact of the transition away from LIBOR on the Fund. |

| • |

Sector Risk, which is the risk that the value of securities in a particular industry or sector will decline because of changing expectations for the performance of that industry or sector. From time to time, based on market or economic conditions, the Fund may have significant positions in one or more sectors of the market. To the extent the Fund invests more heavily in particular sectors, its performance will be especially sensitive to developments that significantly affect those sectors. Individual sectors may be more volatile, and |

| |

may perform differently, than the broader market. The industries that constitute a sector may all react in the same way to economic, political or regulatory events. |

An investment in the Fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. For more information on the risks of investing in the Fund please see the Fund details section of this Prospectus.

Performance

The bar chart below shows how the Fund’s investment results have varied from year to year, and the following table shows how the Fund’s annual total returns for various periods compare to those of the Fund’s benchmark index and Lipper peer group. This information provides some indication of the risks of investing in the Fund. The Fund is available only to investors participating in Morgan Stanley-sponsored investment advisory programs. These programs charge an annual fee (see Annual Advisory Program Fees above). The performance information in the bar chart and table below does not reflect this fee, which would reduce your return. The Fund’s past performance, before and after taxes, does not necessarily indicate how the Fund will perform in the future. For current performance information please see www.morganstanley.com/wealth-investmentsolutions/cgcm.

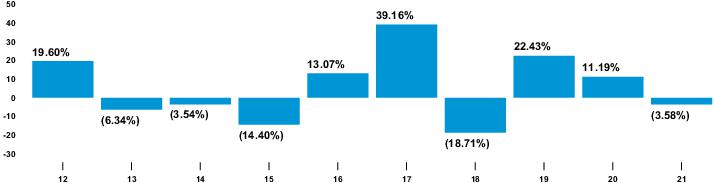

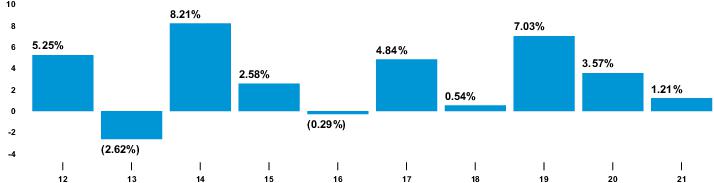

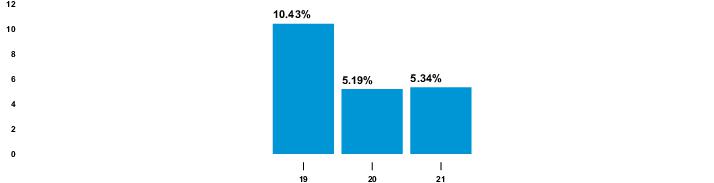

Annual total returns (%) calendar years

Emerging Markets Equity Fund

Fund’s best and worst calendar quarters

Best: 19.72% in 4th quarter 2020

Worst: (26.64)% in 1st quarter 2020

Year-to-date: (30.04)% (through 3rd quarter 2022)

Average Annual Total Returns

(for the periods ended December 31, 2021)

| INCEPTION DATE: 4/21/1994 |

1 YEAR |

5 YEARS |

10 YEARS |

| Fund (without advisory program fee) |

| Return Before Taxes |

(3.58)% |

8.23% |

4.50% |

| Return After Taxes on Distributions |

(4.48)% |

7.79% |

3.96% |

| Return After Taxes on Distributions and Sale of Fund Shares |

(1.34)% |

6.59% |

3.63% |

| MSCI Emerging Markets Index (Net) (reflects no deduction for fees, expenses or taxes) |

(2.54)% |

9.87% |

5.49% |

| Lipper Emerging Markets Funds Average |

(0.57)% |

10.27% |

5.83% |

The after-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an individual investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. In some cases, the return after taxes may exceed the return before taxes due to an assumed tax benefit from any losses on a sale of Fund shares at the end of the measurement period.

The Fund’s benchmark is the MSCI Emerging Markets Index (Net). The benchmark is composed of equity total returns of countries with low to middle per capita incomes, as determined by the World Bank. Unlike the Fund, the benchmark is unmanaged and does not include any fees or expenses. An investor cannot invest directly in an index.

The Fund also compares its performance with the Lipper Emerging Markets Funds Average. The Lipper Emerging