FYfalse0001802255NYSEClass A Common Stock, par value $0.001 per shareBasic and diluted net income (loss) per share of Class A and Class B common stock is applicable only for the period subsequent to September 27, 2024, which is the period following the initial public offering (“IPO”) and related Corporate Reorganization (as defined in Note 1 to the Consolidated Financial Statements). See Note 10 Basic and Diluted Loss Per Share for the number of shares used in the computation of net income (loss) per share of Class A and Class B common stock and the basis for the computation of net income (loss) per share. 0001802255 2025-01-01 2025-12-31 0001802255 2024-01-01 2024-12-31 0001802255 2024-12-31 0001802255 2025-12-31 0001802255 2024-09-27 0001802255 2024-09-27 2024-09-27 0001802255 2025-06-30 0001802255 2025-04-01 2025-06-30 0001802255 2023-12-31 0001802255 us-gaap:CommonClassAMember 2024-12-31 0001802255 us-gaap:CommonClassBMember 2024-12-31 0001802255 us-gaap:CommonClassBMember us-gaap:CommonStockMember 2024-12-31 0001802255 us-gaap:CommonClassAMember us-gaap:CommonStockMember 2024-12-31 0001802255 grdn:PharmacyOperationsMember 2024-12-31 0001802255 grdn:PharmacyOperations2024AcquisitionsMember 2024-12-31 0001802255 grdn:PharmacyOperationsMember us-gaap:CustomerListsMember 2024-12-31 0001802255 grdn:PharmacyOperationsMember us-gaap:TrademarksMember 2024-12-31 0001802255 us-gaap:FairValueInputsLevel1Member us-gaap:FairValueMeasurementsRecurringMember 2024-12-31 0001802255 us-gaap:FairValueInputsLevel2Member us-gaap:FairValueMeasurementsRecurringMember 2024-12-31 0001802255 us-gaap:FairValueInputsLevel3Member us-gaap:FairValueMeasurementsRecurringMember 2024-12-31 0001802255 us-gaap:AutomobilesMember 2024-12-31 0001802255 us-gaap:EquipmentMember 2024-12-31 0001802255 us-gaap:OfficeEquipmentMember 2024-12-31 0001802255 us-gaap:LeaseholdImprovementsMember 2024-12-31 0001802255 us-gaap:ComputerEquipmentMember 2024-12-31 0001802255 us-gaap:CustomerListsMember 2024-12-31 0001802255 us-gaap:TrademarksMember 2024-12-31 0001802255 us-gaap:FiniteLivedIntangibleAssetsMember 2024-12-31 0001802255 us-gaap:CommonClassBMember 2025-12-31 0001802255 us-gaap:CommonClassAMember 2025-12-31 0001802255 us-gaap:CommonClassBMember us-gaap:CommonStockMember 2025-12-31 0001802255 us-gaap:CommonClassAMember us-gaap:CommonStockMember 2025-12-31 0001802255 grdn:GuardianPharmacyLLCMember 2025-12-31 0001802255 grdn:PharmacyOperationsMember 2025-12-31 0001802255 us-gaap:LineOfCreditMember 2025-12-31 0001802255 us-gaap:NotesPayableOtherPayablesMember 2025-12-31 0001802255 grdn:PharmacyOperations2025AcquisitionsMember 2025-12-31 0001802255 grdn:PharmacyOperations2024AcquisitionsMember 2025-12-31 0001802255 grdn:PharmacyOperationsMember us-gaap:CustomerListsMember 2025-12-31 0001802255 grdn:PharmacyOperationsMember us-gaap:TrademarksMember 2025-12-31 0001802255 us-gaap:RestrictedStockUnitsRSUMember 2025-12-31 0001802255 us-gaap:FairValueInputsLevel1Member us-gaap:FairValueMeasurementsRecurringMember 2025-12-31 0001802255 us-gaap:FairValueInputsLevel2Member us-gaap:FairValueMeasurementsRecurringMember 2025-12-31 0001802255 us-gaap:FairValueInputsLevel3Member us-gaap:FairValueMeasurementsRecurringMember 2025-12-31 0001802255 us-gaap:OfficeEquipmentMember 2025-12-31 0001802255 us-gaap:ComputerEquipmentMember 2025-12-31 0001802255 us-gaap:AutomobilesMember 2025-12-31 0001802255 us-gaap:EquipmentMember srt:MaximumMember 2025-12-31 0001802255 us-gaap:EquipmentMember srt:MinimumMember 2025-12-31 0001802255 us-gaap:EquipmentMember 2025-12-31 0001802255 us-gaap:LeaseholdImprovementsMember 2025-12-31 0001802255 us-gaap:TrademarksMember srt:MaximumMember 2025-12-31 0001802255 us-gaap:TrademarksMember srt:MinimumMember 2025-12-31 0001802255 us-gaap:CustomerListsMember srt:MaximumMember 2025-12-31 0001802255 us-gaap:CustomerListsMember srt:MinimumMember 2025-12-31 0001802255 us-gaap:CustomerListsMember 2025-12-31 0001802255 us-gaap:TrademarksMember 2025-12-31 0001802255 us-gaap:FiniteLivedIntangibleAssetsMember 2025-12-31 0001802255 grdn:CommonClassAAndClassBMember 2024-01-01 2024-12-31 0001802255 us-gaap:CommonClassBMember 2024-01-01 2024-12-31 0001802255 us-gaap:CommonClassAMember 2024-01-01 2024-12-31 0001802255 us-gaap:RetainedEarningsMember 2024-01-01 2024-12-31 0001802255 us-gaap:CommonClassBMember us-gaap:CommonStockMember 2024-01-01 2024-12-31 0001802255 us-gaap:AdditionalPaidInCapitalMember 2024-01-01 2024-12-31 0001802255 us-gaap:CommonClassAMember us-gaap:CommonStockMember 2024-01-01 2024-12-31 0001802255 grdn:PharmacyOperationsMember 2024-01-01 2024-12-31 0001802255 grdn:PharmacyOperations2024AcquisitionsMember 2024-01-01 2024-12-31 0001802255 grdn:PharmacyOperations2024AcquisitionsMember grdn:ContingentEarnoutPaymentMember 2024-01-01 2024-12-31 0001802255 grdn:PharmacyOperations2024AcquisitionsMember us-gaap:CashMember 2024-01-01 2024-12-31 0001802255 us-gaap:RestrictedStockMember us-gaap:CommonClassBMember 2024-01-01 2024-12-31 0001802255 us-gaap:RestrictedStockMember us-gaap:CommonClassAMember 2024-01-01 2024-12-31 0001802255 grdn:PreIPOawardsMember 2024-01-01 2024-12-31 0001802255 us-gaap:RestrictedStockUnitsRSUMember 2024-01-01 2024-12-31 0001802255 grdn:UnvestedClassAAndBCommonStockMember 2024-01-01 2024-12-31 0001802255 grdn:RestrictedInterestUnitConversionAwardsIssuedInConnectionWithIpoMember 2024-01-01 2024-12-31 0001802255 us-gaap:NoncontrollingInterestMember 2024-01-01 2024-12-31 0001802255 grdn:MembersEquityMember 2024-01-01 2024-12-31 0001802255 us-gaap:FairValueInputsLevel3Member 2024-01-01 2024-12-31 0001802255 us-gaap:PropertyPlantAndEquipmentMember 2024-01-01 2024-12-31 0001802255 us-gaap:DomesticCountryMember 2024-01-01 2024-12-31 0001802255 us-gaap:PostemploymentRetirementBenefitsMember 2024-01-01 2024-12-31 0001802255 us-gaap:BeneficialOwnerMember 2024-01-01 2024-12-31 0001802255 us-gaap:CorporateMember 2024-01-01 2024-12-31 0001802255 us-gaap:SellingGeneralAndAdministrativeExpensesMember 2024-01-01 2024-12-31 0001802255 srt:RevisionOfPriorPeriodReclassificationAdjustmentMember 2024-01-01 2024-12-31 0001802255 grdn:ThirdAmendedAndRestatedLoanAndSecurityAgreementMember 2024-01-01 2024-12-31 0001802255 grdn:CommonClassAAndClassBMember 2025-01-01 2025-12-31 0001802255 us-gaap:CommonClassAMember 2025-01-01 2025-12-31 0001802255 us-gaap:CommonClassBMember 2025-01-01 2025-12-31 0001802255 us-gaap:NoncontrollingInterestMember 2025-01-01 2025-12-31 0001802255 us-gaap:AdditionalPaidInCapitalMember 2025-01-01 2025-12-31 0001802255 us-gaap:RetainedEarningsMember 2025-01-01 2025-12-31 0001802255 us-gaap:CommonClassBMember us-gaap:CommonStockMember 2025-01-01 2025-12-31 0001802255 us-gaap:CommonClassAMember us-gaap:CommonStockMember 2025-01-01 2025-12-31 0001802255 grdn:PharmacyOperationsMember 2025-01-01 2025-12-31 0001802255 us-gaap:NotesPayableOtherPayablesMember 2025-01-01 2025-12-31 0001802255 us-gaap:NotesPayableOtherPayablesMember grdn:ExistingTermLoanMember us-gaap:SecuredOvernightFinancingRateSofrMember 2025-01-01 2025-12-31 0001802255 us-gaap:NotesPayableOtherPayablesMember grdn:NewTermLoanMember us-gaap:SecuredOvernightFinancingRateSofrMember 2025-01-01 2025-12-31 0001802255 grdn:PharmacyOperations2025AcquisitionsMember grdn:DeferredInventoryPaymentsMember 2025-01-01 2025-12-31 0001802255 grdn:PharmacyOperations2025AcquisitionsMember us-gaap:CashMember 2025-01-01 2025-12-31 0001802255 grdn:PharmacyOperations2025AcquisitionsMember grdn:ContingentEarnoutPaymentMember 2025-01-01 2025-12-31 0001802255 grdn:PharmacyOperations2025AcquisitionsMember 2025-01-01 2025-12-31 0001802255 grdn:RestrictedInterestUnitsConversionMember us-gaap:CommonClassBMember 2025-01-01 2025-12-31 0001802255 grdn:RestrictedInterestUnitsConversionMember 2025-01-01 2025-12-31 0001802255 grdn:IncentiveAwardsMember grdn:CommonClassAAndBMember 2025-01-01 2025-12-31 0001802255 us-gaap:RestrictedStockUnitsRSUMember 2025-01-01 2025-12-31 0001802255 grdn:UnvestedClassAAndBCommonStockMember 2025-01-01 2025-12-31 0001802255 grdn:RestrictedInterestUnitConversionAwardsIssuedInConnectionWithIpoMember 2025-01-01 2025-12-31 0001802255 grdn:PreIPOawardsMember 2025-01-01 2025-12-31 0001802255 us-gaap:RestrictedStockUnitsRSUMember 2025-01-01 2025-12-31 0001802255 us-gaap:RestrictedStockMember us-gaap:CommonClassAMember 2025-01-01 2025-12-31 0001802255 us-gaap:RestrictedStockMember us-gaap:CommonClassBMember 2025-01-01 2025-12-31 0001802255 us-gaap:FairValueInputsLevel3Member 2025-01-01 2025-12-31 0001802255 us-gaap:PropertyPlantAndEquipmentMember 2025-01-01 2025-12-31 0001802255 us-gaap:CertificatesOfDepositMember 2025-01-01 2025-12-31 0001802255 us-gaap:DomesticCountryMember 2025-01-01 2025-12-31 0001802255 us-gaap:PostemploymentRetirementBenefitsMember 2025-01-01 2025-12-31 0001802255 us-gaap:BeneficialOwnerMember 2025-01-01 2025-12-31 0001802255 us-gaap:CorporateMember 2025-01-01 2025-12-31 0001802255 us-gaap:SellingGeneralAndAdministrativeExpensesMember 2025-01-01 2025-12-31 0001802255 grdn:ThirdAmendedAndRestatedLoanAndSecurityAgreementMember 2025-01-01 2025-12-31 0001802255 us-gaap:LeaseholdImprovementsMember 2025-01-01 2025-12-31 0001802255 grdn:PharmacyOperations2024AcquisitionsMember 2025-01-01 2025-12-31 0001802255 us-gaap:CommonClassAMember us-gaap:IPOMember 2024-09-27 2024-09-27 0001802255 us-gaap:CommonClassAMember us-gaap:AdditionalPaidInCapitalMember 2024-09-27 2024-09-27 0001802255 us-gaap:CommonClassAMember 2024-09-27 2024-09-27 0001802255 grdn:TwoThousandTwentyFourEquityAndIncentiveCompensationPlanMember 2024-09-27 2024-09-27 0001802255 grdn:TwoThousandTwentyFourEquityAndIncentiveCompensationPlanMember us-gaap:CommonClassAMember 2024-09-27 0001802255 us-gaap:PreferredStockMember 2007-02-28 0001802255 us-gaap:PreferredStockMember 2007-03-01 0001802255 us-gaap:PreferredStockMember 2011-02-11 0001802255 grdn:SixthAmendmentMember us-gaap:LineOfCreditMember 2024-05-13 2024-05-13 0001802255 grdn:ThirdAmendedAndRestatedLoanAndSecurityAgreementMember us-gaap:LineOfCreditMember 2024-05-13 2024-05-13 0001802255 grdn:SixthAmendmentMember us-gaap:LineOfCreditMember us-gaap:SecuredOvernightFinancingRateSofrMember 2024-05-13 2024-05-13 0001802255 grdn:ThirdAmendedAndRestatedLoanAndSecurityAgreementMember us-gaap:LineOfCreditMember us-gaap:SecuredOvernightFinancingRateSofrMember 2024-05-13 2024-05-13 0001802255 grdn:IncentiveAwardsMember grdn:CommonClassAAndBMember 2024-09-27 2024-12-31 0001802255 us-gaap:RestrictedStockUnitsRSUMember 2024-09-27 2024-12-31 0001802255 us-gaap:CommonClassAMember 2025-03-28 2025-03-28 0001802255 us-gaap:CommonClassAMember 2025-09-27 2025-09-27 0001802255 grdn:UnderwrittenSharesMember 2025-04-01 2025-06-30 0001802255 grdn:UnderwrittenSharesMember 2025-06-30 0001802255 grdn:PharmacyOperations2025AcquisitionsMember 2025-01-01 2025-09-30 0001802255 us-gaap:CommonClassBMember 2026-03-02 0001802255 us-gaap:CommonClassAMember 2026-03-02 0001802255 us-gaap:NoncontrollingInterestMember 2023-12-31 0001802255 grdn:MembersEquityMember 2023-12-31 0001802255 us-gaap:FairValueInputsLevel3Member 2023-12-31 0001802255 us-gaap:NoncontrollingInterestMember 2024-12-31 0001802255 us-gaap:AdditionalPaidInCapitalMember 2024-12-31 0001802255 us-gaap:RetainedEarningsMember 2024-12-31 0001802255 grdn:IncentiveAwardsMember grdn:CommonClassAAndBMember 2025-12-31 0001802255 us-gaap:FairValueInputsLevel3Member 2024-12-31 0001802255 us-gaap:FairValueInputsLevel3Member 2025-12-31 0001802255 us-gaap:AdditionalPaidInCapitalMember 2025-12-31 0001802255 us-gaap:RetainedEarningsMember 2025-12-31 0001802255 us-gaap:NoncontrollingInterestMember 2025-12-31 0001802255 grdn:IncentiveAwardsMember grdn:CommonClassAAndBMember 2024-09-26 0001802255 grdn:IncentiveAwardsMember grdn:CommonClassAAndBMember 2024-12-31 0001802255 us-gaap:RestrictedStockUnitsRSUMember 2024-09-26 0001802255 us-gaap:RestrictedStockUnitsRSUMember 2024-12-31 xbrli:shares iso4217:USD xbrli:pure utr:Year utr:Month iso4217:USD xbrli:shares grdn:Segment

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Mark One)

| ☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2025

OR

| ☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from

to

Commission file

number 001-42284

Guardian Pharmacy Services, Inc.

(Exact name of Registrant as specified in its charter)

|

|

|

|

|

|

(State or Other Jurisdiction of Incorporation or Organization) |

|

(I.R.S. Employer Identification No.) |

300 Galleria Parkway SE

Suite 800

Atlanta, Georgia 30339

(Address of Principal Executive Offices) (Zip Code)

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

Title of Each Class |

|

Trading Symbol(s) |

|

Name of Each Exchange on Which Registered |

Class A Common Stock, par value $0.001 per share |

|

|

|

The New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation

S-T

(§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a

non-accelerated

filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule

12b-2

of the Exchange Act.

|

|

|

|

|

|

|

| Large accelerated filer |

|

☐ |

|

Accelerated filer |

|

☒ |

|

|

|

|

Non-accelerated filer |

|

☐ |

|

Smaller reporting company |

|

☒ |

|

|

|

|

| Emerging growth company |

|

☐ |

|

|

|

|

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the Registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the Registrant’s executive officers during the relevant recovery period pursuant to

§240.10D-1(b). ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule

12b-2

of the Exchange Act). Yes ☐ No

☒ As of June 30, 2025 (the last business day of the Registrant’s most recently completed second fiscal quarter), the aggregate market value of the Class A common stock held by

non-affiliates

of the Registrant was $

411,599,923, based upon the closing price of such shares on the New York Stock Exchange on such date.

As of March 2, 2026, there were issued and outstanding 36,253,744 shares of the Registrant’s Class A common stock and 27,066,890 shares of the Registrant’s Class B common stock.

Documents incorporated by reference:

Part III of this Annual Report on Form

10-K

incorporates by reference certain information from the Registrant’s Definitive Proxy Statement for its 2026 Annual Meeting of Stockholders to be filed within 120 days after the end of the fiscal year to which this report relates.

GUARDIAN PHARMACY SERVICES, INC.

FORM 10-K

TABLE OF CONTENTS

i

SPECIAL NOTE REGARDING FORWARD-LOOKING

STATEMENTS AND RISK FACTOR SUMMARY

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements are all statements other than those of historical fact. Any statements about our expectations, beliefs, plans, predictions, forecasts, objectives, assumptions, or future events or performance are not historical facts and may be forward-looking. These statements are often, but not always, made through the use of words such as “aims,” “anticipates,” “believes,” “contemplates,” “continues,” “estimates,” “expects,” “intends,” “may,” “plans,” “seeks,” “should,” “will,” “would,” and similar expressions. Although we believe that the expectations reflected in these forward-looking statements are reasonable, these statements are not guarantees of future performance and involve risks and uncertainties which are subject to change based on various important factors, many of which are beyond our control. For more information regarding these risks and uncertainties, as well as certain additional risks that we face, refer to “Risk Factors” and the factors more fully described in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this Annual Report on Form 10-K. Among the factors that could cause actual results to differ materially from those suggested by forward-looking statements are:

| |

• |

|

our ability to effectively execute our business strategies, implement new initiatives and improve efficiency; |

| |

• |

|

our ability to effectively market and sell, customer acceptance of, and competition for, our pharmaceutical and health care services in new and existing markets; |

| |

• |

|

our relationships with pharmaceutical wholesalers and key manufacturers, long-term health care facilities (“LTCFs”) and health plan payors; |

| |

• |

|

our ability to maintain and expand relationships with LTCF operators on favorable terms; |

| |

• |

|

the impact of a national emergency, public health crisis, global pandemic or outbreak of infectious disease on our employees and business and on our supply chain and the LTCFs we serve; |

| |

• |

|

continuing government and private efforts to lower pharmaceutical costs, including by limiting pharmacy reimbursements; |

| |

• |

|

changes in, and our ability to comply with, healthcare and other applicable laws, regulations or interpretations; |

| |

• |

|

further consolidation of managed care organizations and other health plan payors and changes in the terms of our agreements with these parties; |

| |

• |

|

our ability to retain members of our senior management team, our local pharmacy management teams and our pharmacy professionals; |

| |

• |

|

our exposure to, and the results of, claims, legal proceedings and governmental inquiries; |

| |

• |

|

our ability to maintain the security and integrity of our operating and information technology systems and infrastructure (e.g., against cyber-attacks); |

| |

• |

|

product liability, product recall, personal injury or other health and safety issues related to the pharmaceuticals we dispense; |

ii

| |

• |

|

the impact of supply chain and other manufacturing disruptions or trade policies related to the pharmaceuticals we dispense; |

| |

• |

|

the sufficiency of our sources of liquidity and financial resources to fund our future operating expenses and capital expenditure requirements, and our ability to raise additional capital, if needed; |

| |

• |

|

the misuse or off-label use, or errors in the dispensing or administration, of the pharmaceuticals we dispense; |

| |

• |

|

we are a “controlled company” within the meaning of the corporate governance standards of the New York Stock Exchange (“NYSE”) and, as a result, we qualify for exemptions from certain corporate governance standards and the Guardian Founders (as defined below) are able to exert significant control over us; and |

| |

• |

|

the market price of shares of our Class A common stock has experienced, and may in the future experience, substantial volatility due to relatively lower trading volumes and a limited public float. |

New risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this Annual Report on Form 10-K. The results, events and circumstances reflected in the forward-looking statements may not be achieved or occur, and actual results, events or circumstances could differ materially from those described in, or implied by, the forward-looking statements. Therefore, we caution you not to place undue reliance on any forward-looking statements or information. Any forward-looking statements speak only as of the date of this Annual Report on Form 10-K. We undertake no obligation to update any forward-looking statements made in this Annual Report on Form 10-K to reflect events or circumstances after the date of this Annual Report on Form 10-K or to reflect new information or the occurrence of unanticipated events, except as may be required by law.

iii

PART I

Unless the context otherwise requires, the terms “Guardian,” the “Company,” “we,” “us” and “our” when used in this Annual Report on Form 10-K mean (i) prior to the Corporate Reorganization (as defined below), Guardian Pharmacy, LLC, an Indiana limited liability company, together with its subsidiaries and (ii) following the Corporate Reorganization, Guardian Pharmacy Services, Inc., a Delaware corporation, together with its consolidated subsidiaries. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Corporate Reorganization and IPO” for further information regarding the Corporate Reorganization.

References to our certificate of incorporation and bylaws refer to our amended and restated certificate of incorporation and amended and restated bylaws.

Overview

We are a leading, highly differentiated pharmacy services company that provides an extensive suite of technology-enabled services designed to help residents of LTCFs adhere to their appropriate drug regimen, which in turn helps reduce the cost of care and improve clinical outcomes. We emphasize high-touch, individualized clinical, drug dispensing and administration capabilities that are tailored to serve the needs of residents in historically lower acuity LTCFs, such as assisted living facilities (“ALFs”), and behavioral health facilities and group homes (collectively “BHFs”). More than two-thirds of our annual revenue for each of the past three years has been generated from residents of ALFs and BHFs, which are our target markets, while the remainder has been generated primarily from residents of skilled nursing facilities (“SNFs”). Additionally, our robust suite of capabilities enables us to serve residents in all types of LTCFs. We are a trusted partner to residents, LTCFs and health plan payors because we help reduce errors in drug administration, manage and ensure adherence to drug regimens, and lower overall healthcare costs. As of December 31, 2025, our 61 pharmacies, 54 of which are full-service, served approximately 205,000 residents in approximately 8,400 LTCFs across 38 states.

Within the U.S. LTCF market, we believe the ALF and BHF sectors present the most attractive opportunity and have the highest growth potential for our business. Certain characteristics of ALFs and BHFs, which are not typical of SNFs, create additional challenges and complexities for pharmacy service providers that Guardian is well suited to address. First, residents at ALFs are typically on a variety of different pharmacy benefit plans, each with a distinct formulary and reimbursement process, covering their complex drug regimens. Second, ALFs often lack staff with formal clinical training and usually do not have an on-site medical director or full-time nurse. Because residents of ALFs rely on off-site physicians to oversee and monitor their health conditions, there is an increased need for coordination among ALF operators, each resident’s physicians and pharmacy service providers. Third, residents in these facilities have the right to choose their own pharmacy, which often leads to multiple pharmacy service providers serving a single ALF. These characteristics are also typical of most BHFs.

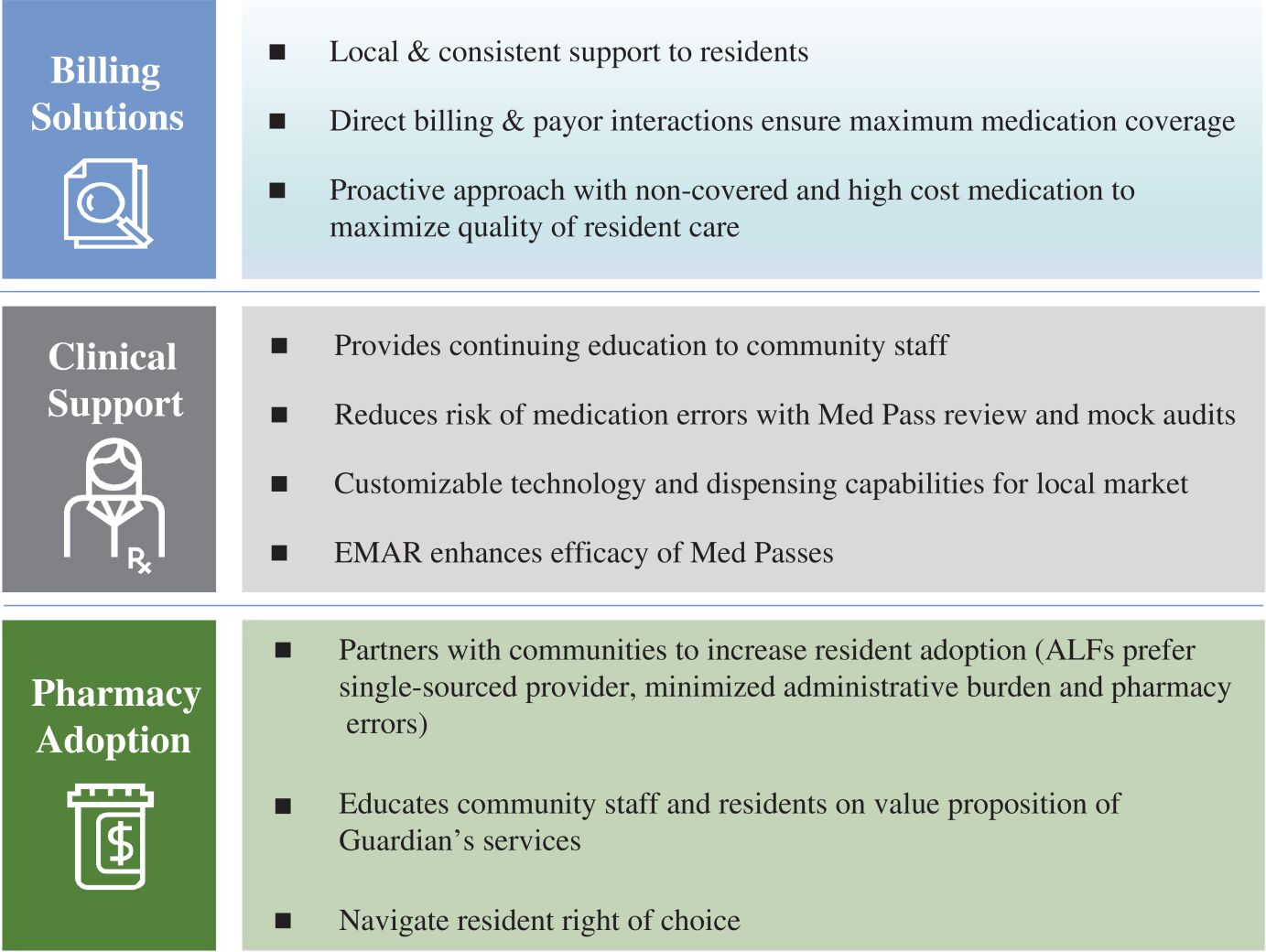

We believe that we enjoy a strong competitive position as a large and purpose-built provider of pharmacy services to ALFs and BHFs. Guardian offers a variety of services that we believe address the challenges that ALFs and BHFs face, and differentiate us from our competitors, providing residents, LTCFs and health plan payors with a compelling value proposition. Our centralized corporate support capabilities empower our local pharmacy operators to offer an extensive suite of high-touch, individualized, consultative pharmacy services, using a portfolio of proprietary data analytics systems and technology designed to help ensure that the right dose of the right medication is provided to the right resident at the right time. Examples of our specialized services include:

| |

• |

|

Assisting residents in optimizing pharmacy benefit plan coverage of their medication by coordinating formulary interchanges with residents’ physicians; |

1

| |

• |

|

Proactively analyzing potential adverse drug interactions and managing potential risks in medication administration; |

| |

• |

|

Providing robotic dispensing and customized compliance solutions, organized by resident and time of administration; |

| |

• |

|

Integrating a resident’s drug regimen with the LTCF’s Electronic Medication Administration Records (“EMARs”) to help ensure adherence; |

| |

• |

|

Providing training for LTCF caregivers to help them administer medications to residents more safely, efficiently and cost-effectively; |

| |

• |

|

Partnering with LTCF operators to increase the number of residents using our services at each facility we serve, which we refer to as “resident adoption,” in order to streamline drug administration and minimize medication management risk; |

| |

• |

|

Conducting mock audits of LTCFs to monitor compliance with drug administration and government regulation; and |

| |

• |

|

Reviewing periodically the drug regimen for each resident by consulting pharmacists. |

We are a trusted partner to:

| |

• |

|

Residents. We help monitor resident drug regimens and coordinate with each resident’s prescribing physicians to confirm clinical appropriateness and to help maximize coverage under the resident’s pharmacy benefit plan. We also partner with each facility to achieve adherence to a resident’s drug regimen. We believe that these services help improve clinical outcomes and reduce hospitalizations and out-of-pocket costs for the resident. |

| |

• |

|

LTCFs / Caregivers. We help caregivers deliver high quality resident care by streamlining the intricacies associated with drug administration and compliance with related regulatory requirements. We accomplish this through the information available from our technology-enabled, proprietary data warehouse, our compliance packaging of the prescriptions we fill and the clinical training we offer to caregivers. |

| |

• |

|

Health Plan Payors. Our services help facilitate proper management of residents’ drug regimens and reduce errors in drug administration, which we believe ultimately results in better clinical outcomes and thereby lowers overall health care costs for health insurance payors. |

2

Our Solution and Value Proposition

We believe that we have purpose-built our capabilities and associated technology tools to address the growing challenges that are specific to our end markets. In addition to the services we provide to LTCFs generally, we provide ALFs and BHFs with tailored services that enhance their abilities as caregivers to their residents. We offer a suite of high-touch consultative pharmacy services, as illustrated in the following chart, using a portfolio of proprietary data analytics systems and technology, to assist our local pharmacies in optimally serving facilities and their residents.

Through our extensive suite of pharmacy services and our service-focused approach, we believe that we offer a compelling value proposition to residents, LTCFs and their respective caregivers, particularly in ALFs and BHFs, and to health plan payors.

3

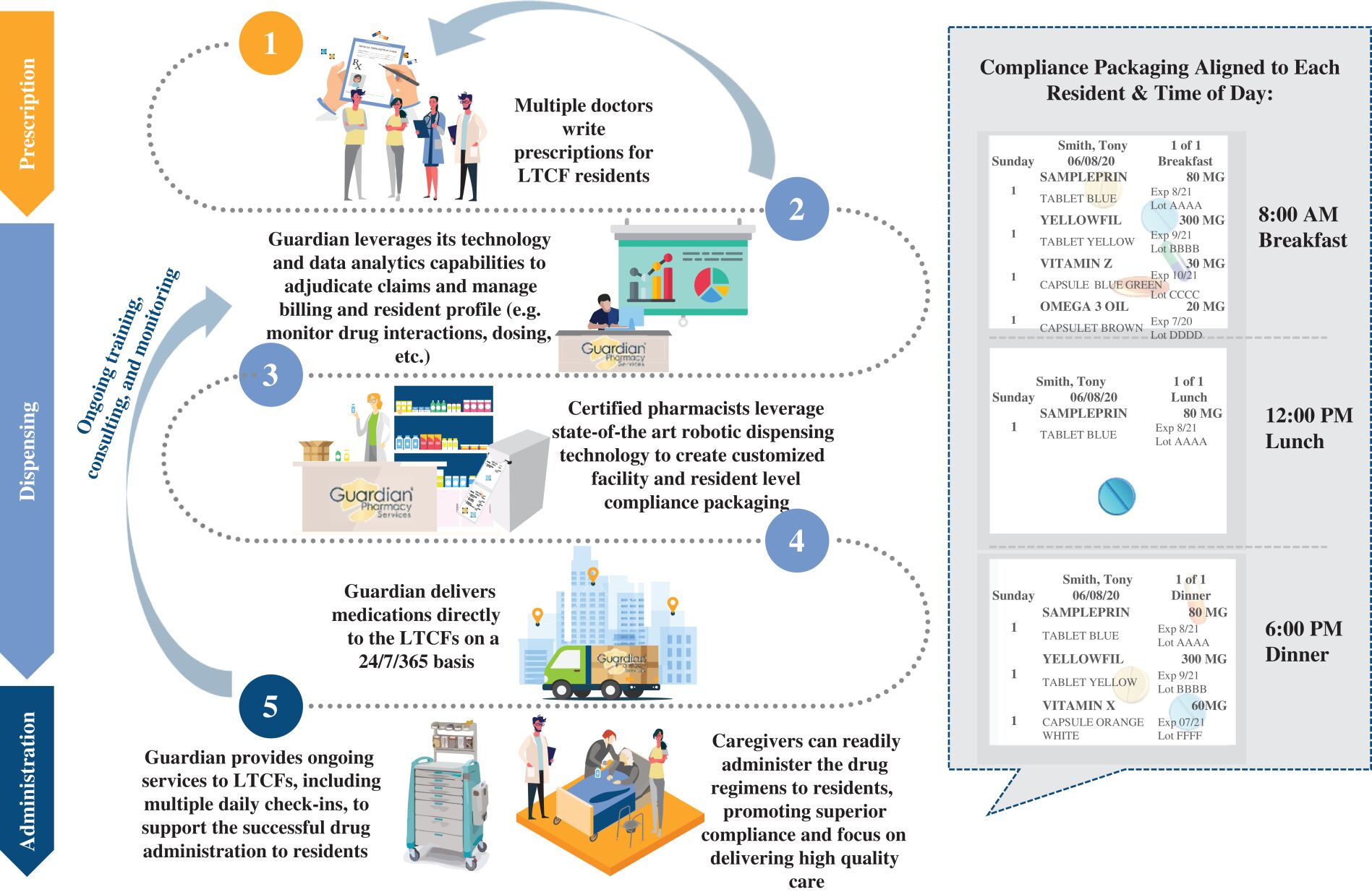

Our Workflow Lifecycle and Pharmacy Support

Through our locally-based pharmacies, we utilize a complex, technology-enabled platform to manage the dispensing and administration of prescriptions to residents of LTCFs over the full prescription lifecycle in order to manage medication risk.

We believe our business model and strategic approach are built upon several key strengths of Guardian, as further described below.

We utilize a high-touch, resident-centric, superior customer service model to help drive drug regimen adherence and improved clinical outcomes, while managing overall costs.

We work closely with the LTCFs we serve to deliver a pharmacy solution that strives to maximize resident drug adherence while minimizing the incidence of adverse drug events. We manage the adjudication process for every prescription, which we believe instills confidence on the part of both the residents and LTCFs we serve that adverse drug events will be minimized and proper insurance eligibility will be in place. We also assist residents in confirming appropriate pharmacy benefit plan coverage of their medication by coordinating formulary interchanges with residents’ physicians.

To further enhance the quality of pharmacy administration, we customize technology and dispensing solutions to produce compliance packaging specific to each LTCF and each individual resident. In combination with the training we provide to caregivers, this dispensing solution is designed to help ensure that the right dose of the right medication is provided to the right resident at the right time.

We also offer training and continuing education programs to LTCF staff for a fee to educate caregivers on the proper administration of drugs to residents in accordance with the resident’s drug regimen. Additionally, we conduct mock audits for LTCFs to assist in compliance with state and federal regulations and deliver other pharmacy consulting services, including resident drug therapy evaluations.

4

We service LTCFs typically within a radius of 200 miles or less of our pharmacy locations, depending on the metropolitan area. We typically deliver medications to these facilities at a minimum once each day. We provide 24-hour, seven-days a week, on-call pharmacist services for emergency dispensing, delivery, and/or consultation with the facility’s staff or the resident’s attending physician.

We believe that our high-touch model contributes to fewer instances of adverse drug events, decreases in resident hospitalizations and increases in overall drug regimen adherence, which collectively keep residents healthier at a lower cost to their insurers.

We use our technological tools to enhance our ability to serve LTCFs and drive operational efficiencies.

The scale of our business has enabled us to make significant investments to equip our pharmacies with dynamic technologies designed to drive superior operational efficiencies in pharmacy workflow management. Key areas of investment include logistics management, revenue cycle management, automated robotic dispensing technology, compliance packaging, pharmacy workflow software, EMAR integration capabilities, cybersecurity infrastructure and disaster recovery business continuity.

Automated Robotic Dispensing Technology

We have invested significantly in advanced pharmacy automation technologies. The use of automation within our pharmacies leverages our size and distinguishes us from many of our competitors. It increases our dispensing accuracy and speed of pharmaceutical distribution, in addition to providing significant cost benefits. Specifically, we currently have over 100 automated dispensing machines deployed across our network.

Automation reduces the need for human involvement and improves the efficiency of operations and increases accuracy with respect to drug dispensing. It also leverages artificial intelligence and barcode scanning software to detect the correct National Drug Code number (or NDC) and size, shape, and color of pills in order to help flag problems for our pharmacies. It also enables rapid scaling of volumes as new residents are added. Further, our barcoded delivery system facilitates compliance with pharmacy benefit plan requirements by creating an electronic record of delivery.

Compliance Packaging

We offer a compliance packaging service, through which we repackage and dispense prescription and non-prescription pharmaceuticals in accordance with physician orders and deliver the medications to LTCFs for administration to individual residents. This service organizes each resident’s medications into individual unit dose or multi-unit dose packaging in accordance with specific “Med Passes,” or drug distribution rounds that occur at LTCFs at specific times throughout the day. The packaging of drugs for each resident indicates specific drug administration instructions. LTCFs prefer the individual- or multi-unit dose delivery system over the bulk delivery system employed by retail pharmacies because it improves control over the storage and ordering of drugs and reduces errors in drug administration in healthcare facilities. Nurses or caregivers at LTCFs then distribute medications to residents in accordance with physician orders at each Med Pass.

Pharmacy Workflow Software

The pharmacy workflow software we use helps to manage and track drug dispensing via a structured and scalable workflow process, including the use of barcode technology. In addition, the software increases labor productivity and enables our local pharmacies to focus their time and resources on delivering care to residents, which improves overall resident safety. This system improves efficiencies in nursing time, reduces drug waste, and helps to improve resident outcomes, thereby lowering costs for pharmacy benefit plans.

EMAR Integration Capabilities

Our ability to interface with facilities’ EMARs makes documentation and drug administration more efficient. At the time of drug administration, the nurse or caregiver must scan the barcode associated with each

5

resident at the time of drug delivery, which creates a notation on the EMAR system. This helps us ensure the safe and effective delivery of medications to each resident at each Med Pass and helps LTCFs to manage their regulatory requirements.

Cybersecurity, Infrastructure, Disaster Recovery and Business Continuity

We employ multiple levels of protection to minimize the risks associated with cybersecurity, ransomware and data breaches, including firewalls, cloud-based backups, multifactor authentication, encryption software, intrusion testing and security information and event management (“SIEM”) networking monitoring to ensure the integrity of our data and systems. In addition, we maintain recovery and other business continuity procedures, including cloud-based backups, electrical generators, critical systems housed at hardened data centers and geographic redundancy, intended to minimize disruptions to our operations in the event of disaster or other interruptions to our information systems.

We believe that our business model promoting local management autonomy, combined with our centralized corporate support, results in superior service to LTCFs and their residents.

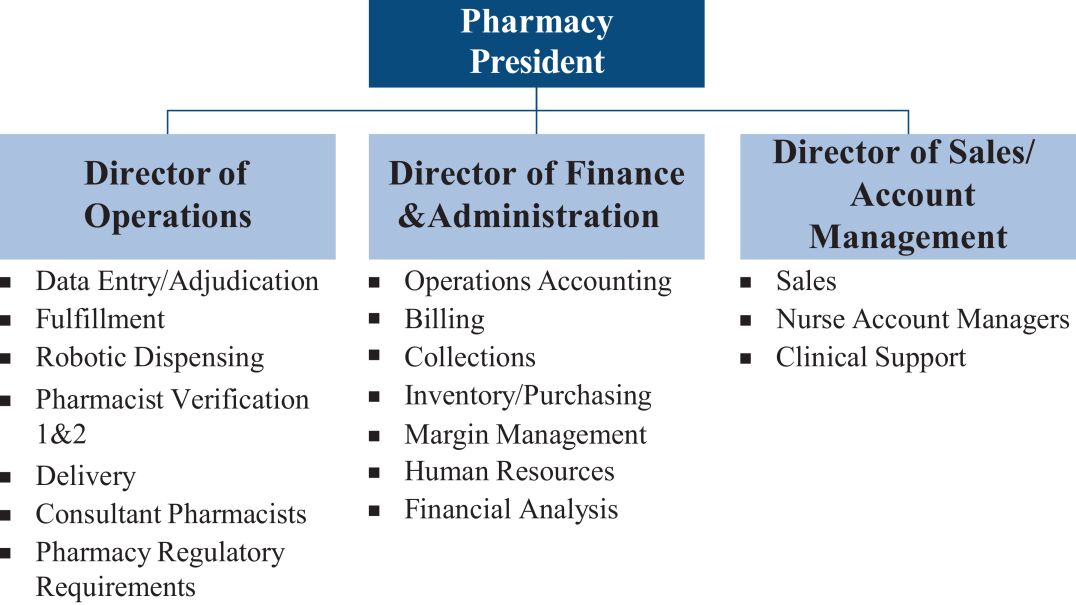

We believe that our pharmacy management model offers local and tailored support to LTCFs and their residents, and enables us to adapt our technology and dispensing capabilities to customer needs in each local market. We provide centralized corporate support to our local pharmacy operators, including data analytics, IT operations, financial oversight and analysis, capital management, leadership support and training, purchasing power, legal/regulatory support, and HR/recruiting assistance. We believe this approach allows us to benefit from local touch and customer-centric decision making thereby enhancing our ability to manage local, regional and national account relationships, improve resident adoption rates in individual facilities and improve drug regimen adherence and compliance.

Specifically, at the pharmacy level, each pharmacy is run by a President, who directly oversees three directors:

As we acquire or organically open new pharmacies, we offer the following support services and training to each of these directors and their local pharmacy management teams:

| |

• |

|

purchasing strategy and tools |

| |

• |

|

health plan payor negotiations |

| |

• |

|

revenue cycle management |

| |

• |

|

business intelligence and analytics |

| |

• |

|

human capital management |

| |

• |

|

treasury, business services and financial accounting |

6

| |

• |

|

operational and regulatory |

We believe this local approach that capitalizes on our national scale distinguishes us from our competitors by eliminating a “one size fits all” approach that may create inefficiencies in a particular local market.

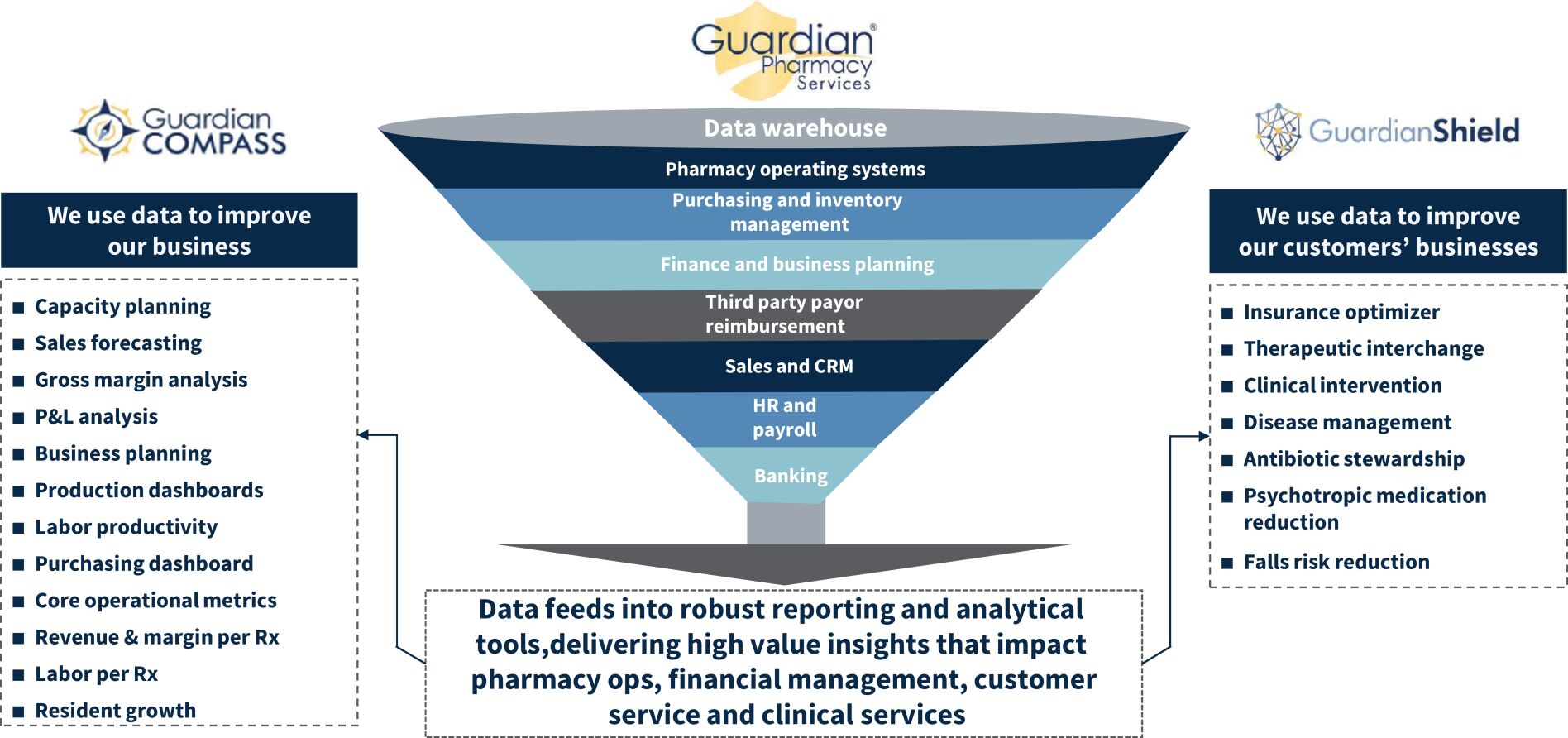

Leveraging Our Data Warehouse to Deliver Insights

Our business model is supported by our proprietary centralized data warehouse, which facilitates the delivery of our technology-enabled services to LTCFs and their residents. Our data warehouse collects and consolidates extensive data related to pharmacy operating systems, purchasing and inventory management, finance and business planning, pharmacy benefit plan reimbursement, sales and customer relationship management, human resources and payroll, and banking. Information is analyzed and interpreted on a daily or real-time basis and reports, dashboards and analytics are available to team members throughout Guardian. We use these analytics and associated metrics to proactively plan and manage our business.

Specifically, our Guardian Compass platform offers insights to enhance efficiencies for our pharmacies, including proprietary real-time operational dashboards and metrics. Our suite of GuardianShield products offers customer and clinical services that benefit both the residents we serve and their caregivers.

Guardian Compass

Guardian Compass includes dashboards created using data from our data warehouse to help our local pharmacies plan, track and optimize their business operations. The data and metric-driven approach enhances our ability to make decisions regarding labor productivity, capacity planning, and sales forecasting. Guardian Compass also provides tools that improve our local pharmacies’ ability to purchase pharmaceuticals effectively. Detailed assessments regarding the aggregate cost of dispensing drugs and the cost per prescription further assist our pharmacies in improving operations.

We track various individual pharmacy-based operating metrics including financial revenue per Rx, labor per Rx, resident count trends and adoption rate trends per facility among others.

7

GuardianShield Programs

GuardianShield offers a suite of specialized services, enhanced by actionable analytics, that drive accuracy, efficiency, safety, and savings for LTCFs and create benefits for both residents and LTCF staff. It is comprised of ten programs, eight of which are currently in use, and two of which are in the development phase, all of which are made possible through the data warehouse. The eight active programs are: the Insurance Optimizer Program, the Antibiotic Stewardship Program, the Psychotropic Medication Reduction Program, the Therapeutic Interchange Program, the Medication Spend Analyzer Program, the Adoption Rate Tracker Program, the Clinical Intervention Tracker Program and the Order Entry QA Analyzer. The two programs in development are: the Falls Risk Management Program and Disease State Management. The data analytics tools and customer service we are able to offer through GuardianShield have downstream benefits for LTCFs and pharmacy benefit plans that we believe are unmatched in the industry.

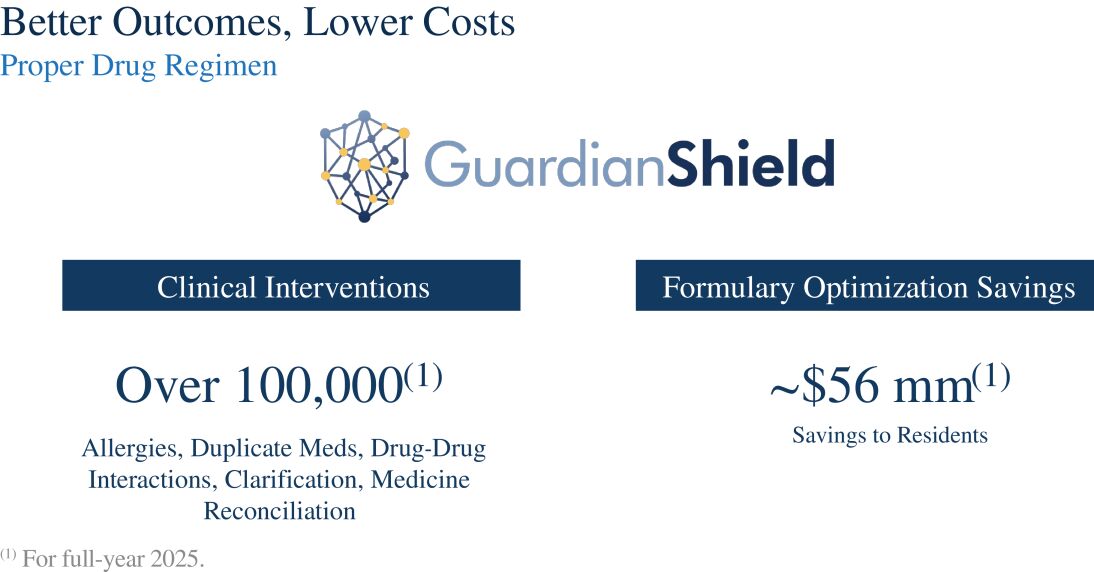

The Insurance Optimizer Program provides information to help residents choose their pharmacy benefit plans, and helps get essential, non-covered medications covered on a pharmacy benefit plan’s formulary. This program also provides analytics reports to residents in the facilities we serve to quantify their savings. Such data helps with pharmacy adoption, which in turn eases the challenges associated with ALFs and BHFs having to coordinate with multiple pharmacies to supply drugs to residents.

The Antibiotic Stewardship Program combines the extensive clinical experience of our consultant pharmacists with advanced reporting and data analytics to offer a robust antibiotic therapy management program. This helps prevent overuse of antibiotics and other medications, helping pharmacy benefit plans and the facilities we serve.

The Psychotropic Medication Reduction Program capitalizes on our pharmacists’ clinical knowledge and our advanced data analytics capabilities to promote the appropriate use of psychotropic medications (including antipsychotics, anxiolytics, antidepressants, and hypnotics) for the benefit of residents we serve. In understanding the frequency with which such drugs are prescribed to each resident, we are able to help the facilities we serve comply with government regulations pertaining to psychotropic medications.

The Therapeutic Interchange Program allows drug substitutions to therapeutically equivalent drugs to lower costs for SNFs. In addition to the savings generated, this program offers extensive reporting capabilities to track and highlight savings and missed opportunities.

We also offer a Medication Spend Analyzer to break down the monthly drug spending for each of the LTCFs we work with. This assists LTCFs with crucial cost management functions and makes us a valued partner in the process of serving their residents.

For the ALF communities we serve, we seek to maximize the number of residents in those communities who use us for their medication needs, and resident adoption rate is a key metric we use to gauge our effectiveness. Our Adoption Rate Tracker provides information to our pharmacies and ALF communities to help them understand the current opportunity and increase the number of residents we serve in those communities. Higher resident adoption rates mean higher organic growth for us and improved safety and efficiency for the communities and residents.

As a LTCF pharmacy, we use our Clinical Intervention Program to take extra steps to process prescriptions. Whether it is a full medication reconciliation, duplicate therapy resolution, or clinical issue resolution we take measures to help improve resident outcomes and save money. This program has analytics reports to show the frequency of these interactions and thus demonstrate the value we bring our residents, communities, and third-party payors.

Finally, we offer an Order Entry QA Analyzer, which is designed to utilize real-time rules- engine technology to examine prescriptions and detect omissions and/or errors before they become a customer service problem. This service adds substantial value for the LTCFs and pharmacy benefit plans we work with, and

8

ultimately, the residents we serve, as we help residents avoid adverse drug reactions and complications resulting from, and the additional costs associated with, the improper dosage or incorrect administration to residents.

Below are select examples of the insights and analytics we are able to produce from our GuardianShield platform for the year ended December 31, 2025 on a Company-wide basis.

Advances to GuardianShield

We continuously strive to advance the capabilities of GuardianShield, and are actively developing new predictive tools to assist LTCFs and our pharmacies. Chief among these advancements are the Falls Risk Management Program and Disease State Management services.

The Falls Risk Management Program is being designed to review each resident’s medications and demographic information to identify those residents with the highest risk of falling. The program will then pinpoint the highest probability causative factors related thereto, which will help enable those residents to receive the medications and/or treatment necessary to help minimize this risk. This program is designed to help optimize residents’ health while lowering health care costs for pharmacy benefit plans.

The Disease State Management Program is being designed to use data to identify residents at LTCFs who are on sub-optimal medication regimens. These regimens will then be subject to a targeted review by our consultant pharmacists, who will work to optimize the drugs each resident takes. This program is expected to improve the overall health of the residents we serve and lower health care costs for the pharmacy benefit plans with whom we work.

Our Market Opportunity

We believe we have an attractive market opportunity for continued growth. Based on prescription volume information reported by NIC MAP Vision (“NIC MAP”) for ALFs and memory care facilities (“ALF/MC”) as of December 31, 2025, we believe we are the largest LTCF pharmacy in the United States in terms of market share serving ALF/MC, with an approximate 13.0% market share nationally. IBISWorld, an independent publisher of industry research reports, estimated that U.S. institutional pharmacy market revenues for 2025 would be approximately $24.3 billion. The U.S. institutional pharmacy market is comprised of pharmacies that provide a range of distribution and drug administration services to residents of nursing homes and other healthcare environments that do not have on-site pharmacies. The Centers for Medicare & Medicaid Services (“CMS”) mandates rules and service capabilities to qualify for participation as a Part D Network LTC Pharmacy (“Part D NLTCP”) provider, as differentiated from traditional Part D and commercial reimbursement. CMS designates an institutional level of care as a “distinct pharmacy setting” and requires payors to compensate designated long-term care pharmacies for the specific services they are required to provide to LTCF residents. In addition, CMS requires that payors maintain network adequacy to serve LTCF residents. This LTCF institutional pharmacy market is currently served by Guardian, two national pharmacy services providers historically focused on serving the needs of SNFs, several regional providers, and over 1,200 independent pharmacies.

9

We believe that in long-term care settings, proper coordination of drug administration is critical to managing the overall health and wellbeing of residents. Residents of LTCFs can be at high risk for adverse drug events given the complex mix of medications prescribed by the various physicians responsible for their care. Lapses in care or incorrect drug administration can result in serious adverse drug events, which can in turn result in hospitalization and have significant implications on both quality and duration of life, in addition to the overall cost of healthcare.

In comparison to historically higher acuity settings such as SNFs, ALFs in particular face challenges in the pharmacy administration lifecycle. ALFs were initially conceived of as senior living facilities providing stimulation, hospitality and community for elderly individuals who no longer desired, or were capable of, independent living. However, over time, these facilities have expanded their services to increasingly address the health needs of an ever-growing number of older and higher acuity residents who need assistance with medical care and activities of daily living.

With increasing levels of acuity, ALF residents today require greater assistance in maintaining their drug regimens, and consistency and accuracy in drug administration is now a key service that ALFs provide to their residents. There are several specific ongoing industry trends that we believe will continue to drive the increased need for ALFs, as well as BHFs, to act as caregivers, and in turn help drive demand for the associated and critical pharmacy services that we provide:

Aging Demographics and Increases in the Number of Assisted Living Residents

The aging of the U.S. population has been well documented, with Census projections for significant growth in the U.S. elderly population. Specifically, by 2050, the 65+ age group is projected to grow to 82 million people, which represents a greater than 47% increase over the same population group in 2022. The increase in the elderly population is expected to result in significant increases in move-ins to ALFs and, accordingly, drive increases in the number of prescriptions that are fulfilled by institutional pharmacies.

Increasing Median Ages of ALF Residents, Requiring Greater Emphasis on Healthcare Delivery and Associated Coordination of Complex Drug Regimens

Coupled with the significant increases in move-ins to ALFs generally are the increases in the number of more elderly and frail individuals that are moving into and residing in ALFs. Of the more than 1 million U.S. residents residing in ALFs, more than half are above 85 years old, with an additional 31% aged between 75 to 84. These increases in the age demographics of ALF residents have been driven by both later average initial admission age for residents and significant increases in overall life expectancy. As a result of these trends, the resident ALF population tends to have more complex medical needs than in previous generations. Chief among these needs is the coordination and effective management of pharmacy services that are fundamental to the effective treatment and overall cost management of medical care for these individuals.

Increasingly Complex Medication Regimens

In general, older residents face more critical health conditions, including chronic illness, increased disability and multiple medical diagnoses—for a longer period of time. As a result, there is growing demand for not only long-term care facilities, but also for caregivers who are able to help navigate the complex medication regimens of this elderly population. In turn, these caregivers require more sophisticated pharmacy capabilities and an extensive range of pharmacy workflow services to ensure proper medication adherence and delivery of care.

Highly Fragile Population of Individuals with Behavioral Health Needs at BHFs

Similarly, BHFs serve as caretakers for a highly fragile population of individuals with behavioral health needs. Oftentimes, these residents are suffering from intellectual and developmental disorders or mental health challenges such as schizophrenia, depression, and anxiety-related afflictions. Pharmaceutical drugs are often first

10

line therapies for these individuals, and the proper administration of and compliance with drug regimens is essential to maintaining their health. The overall mental fragility of BHF residents puts them at high risk for hospitalization or other acute episodes of care that present significant costs to health plan payors. Lapses in the proper administration of their drugs only add to this risk.

Increases in ALF and BHF Desire to Contract with Value-Added Scaled Pharmacy Providers

Though ALF and BHF residents are entitled to a choice in their pharmacy provider, ALF and BHF providers and especially large multi-facility LTCF operators have recognized the enhanced value in having scaled and integrated pharmacy networks service the needs of their caregivers and residents. Often, in the absence of a sophisticated provider, pharmaceuticals are simply delivered to residential settings without an associated suite of services to help ensure successful drug administration (e.g., resident compliance, documentation, data collection, ALF and BHF staff training, etc.). LTCFs and residents are seeking assistance to help monitor and ensure ongoing adherence with their increasingly complex medication regimens.

Extension of Drug Coverage via Medicare Part D Helps Drive the Need for Pharmacy Services Companies

Medicare Part D legislation has significantly changed the way in which prescription drugs are financed and reimbursed, thereby directly impacting the performance of pharmacies serving LTCFs.

Part D created significant changes for assisted living residents who are dually eligible for both Medicare and Medicaid (“dual-eligibles”), given the new benefit shifting their drug coverage from Medicaid to Medicare and requiring enrollment in private health care plans. This expands the pharmaceutical drug coverage of these residents, which they would not have previously had or which Medicaid would have had to pay, and yields more favorable reimbursement rates for pharmacy services companies.

Financial and Administrative Impact of Medicare Part D

Medicare Part D has also resulted in the increased variation around formularies and drug management processes for residents and providers. The complex nature of the Medicare Part D program and the confusion residents have around coverage directly impacts the ability of ALFs and group homes to run operations. The numerous administrative burdens associated with the transition takes time away from resident care, poses regulatory threats to providers and makes it more difficult to ensure optimal drug therapy for residents.

Of the more than 1 million residents residing in ALFs in the United States, we serve approximately 140,000, with the remainder of the residents we serve residing in other types of LTCFs. We believe that our existing market share, the size of our market opportunity, our strategic approach to high-touch, individualized services and favorable market dynamics provides us with a significant opportunity for future growth.

While our national competitors have primarily focused on SNFs, we believe we enjoy a strong competitive position as a large and purpose-built provider of pharmacy services to ALFs and BHFs. The following chart outlines the key differences in the characteristics of ALFs, BHFs and SNFs and illustrates some of the challenges specific to these facilities.

Key Characteristics of LTCFs

|

|

|

|

|

| |

|

ALFs and BHFs |

|

SNFs |

| Resident Ability to Choose Pharmacy Provider |

|

Each ALF resident has the right to choose his or her own pharmacy benefit plan and provider |

|

Most SNFs encourage their residents to select the SNF’s contracted pharmacy provider |

11

|

|

|

|

|

| |

|

ALFs and BHFs |

|

SNFs |

| Level of Staff Experience |

|

Typically, minimal clinical training for caregivers / staff members |

|

Experienced staff members, including an on-site medical director and a registered nurse (RN), as well as a licensed practical nurse (LPN) or certified nursing assistant (CNA) required to administer medications |

|

|

|

| Access to a Medical Provider |

|

Most ALF residents maintain their physician relationships, with office visits |

|

Each SNF contracts with a medical director that is regularly on site |

Our Growth Strategy

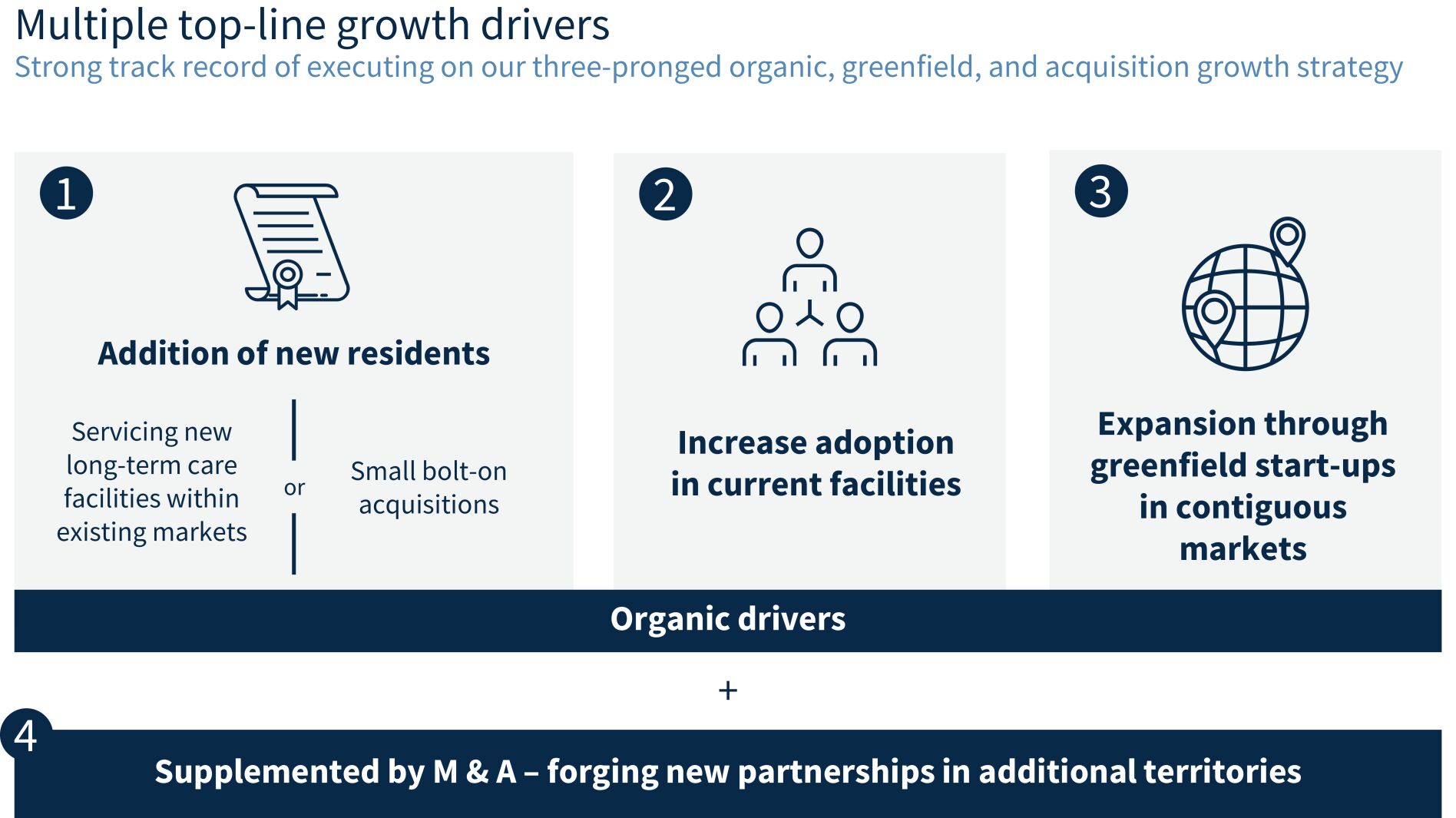

Our core growth strategy is focused on increasing the number of residents we serve. Historically, this has been driven by both organic growth and acquired growth. Organic growth represents the increase in the number of residents served at existing locations, start-up greenfield locations and acquired locations subsequent to the acquisition date.

The four key pillars that we expect to continue to drive our growth are additions of new residents, increased adoption in current facilities, expansion through greenfield start-ups (each of which are organic drivers), and forging new partnerships in additional territories through acquisitions.

Increase number of ALF accounts we serve.

Our sales teams actively engage in marketing efforts to build relationships with local, regional and national ALFs and BHFs. Our local ALF target customers typically operate a single ALF or a small number of ALFs but are generally characterized by their focus on a specific local area. Conversely, large multi-location ALFs operate with a regional or national footprint. We currently serve facilities operated by Brookdale Senior Living, Life Care Services, Sunrise Senior Living and numerous other regional and national providers. We believe that our customer-oriented business model, which is able to serve large numbers of residents across geographic regions,

12

provides a competitive advantage as we continue to develop and expand relationships with ALF operators. In particular, we believe there are significant opportunities to expand our business serving local, regional and national ALF accounts. As we continue to build out our national footprint, we believe we are an increasingly attractive provider to ALF operators that value our services and approach, but prefer a vendor with a broad geographic reach.

Increase resident adoption of our services in ALF accounts.

We measure, analyze and track resident adoption rates at each ALF we serve. Each of our pharmacies has a dedicated management team focused on increasing our resident adoption through targeted marketing efforts, leveraging internally generated data, and demonstrating our value proposition to ALFs, residents and caregivers. Through our direct marketing efforts to ALFs and residents, we have achieved a resident adoption rate of 89% at ALFs we serve as of December 31, 2025. We believe our success in increasing resident adoption is one of our key strengths.

Ongoing geographic expansion.

For both our acquisition program and our greenfield initiatives, we focus on expanding our market share and increasing profitability through strategic evaluation and implementation of opportunities to acquire and build out new pharmacies in existing and underserved markets.

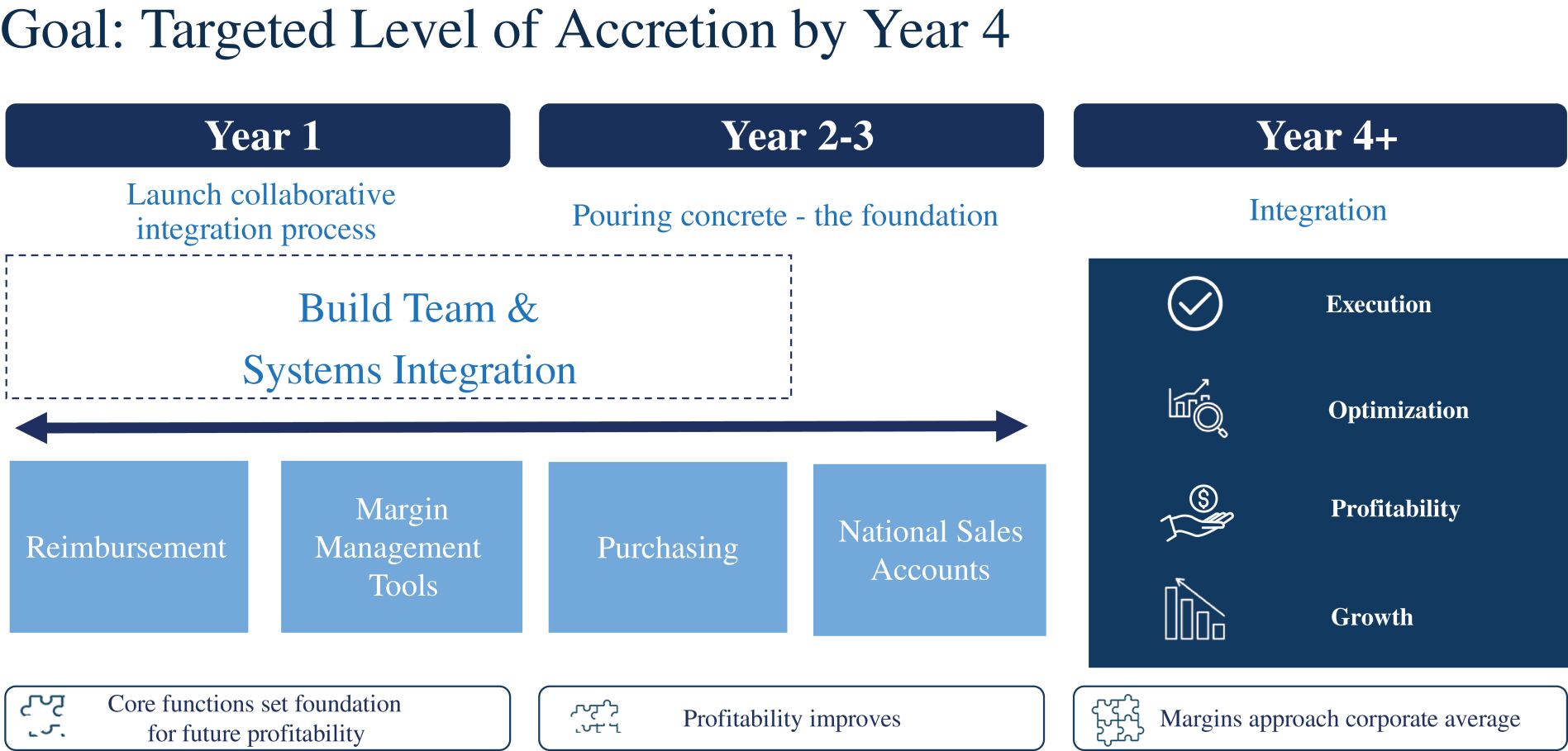

Our geographic expansion to date has relied on a two-pronged business development strategy comprised of (1) finding qualified local pharmacy operators to partner with and (2) growing with our existing pharmacy operators into new markets. Once we have identified a new partner, we seek to either acquire their pharmacy or develop a startup pharmacy with them. In addition, we seek to grow into new markets with our existing pharmacy partners through acquisitions or startups.

Additionally, we have a robust M&A function with a demonstrated track record of both successful identification of integration of superior qualified pharmacies that are compatible with our platform. Specifically, we seek to partner with pharmacies that are customer-focused, are located in attractive markets (including those close to our large, multi-location ALF accounts) and are led by skilled clinical operators with a growth mindset. Following acquisition, we embark on a standardized multi-year integration process that begins with centralizing pharmacy operations and ultimately transforms core functions and sets the foundation for superior growth and profitability.

13

Upon acquisition, we are typically able to significantly enhance the profitability and margin of the acquired pharmacy by implementing our IT services and leveraging our purchasing, revenue cycle management and national sales capabilities. These synergies are often substantially realized over a 48-month period from acquisition and represent a substantial opportunity for us and our acquired pharmacy partners.

In the future, we anticipate that we will structure our acquisitions and greenfield start-ups in a manner similar to our business development strategy prior to our IPO. Prior owners of the pharmacies we acquire and the local pharmacy operators we partner with to open greenfield start-up pharmacies will hold minority equity interests in these businesses. A portion of the consideration in an acquisition of an existing pharmacy may be paid in shares of our Class B common stock. Further, employees of the pharmacies may be issued incentive equity interests in that pharmacy. After a period of time sufficient to allow the subsidiary pharmacy to adopt our operating practices and integrate within our business, we would expect to purchase those minority equity interests. Upon such purchases, these pharmacies would become our wholly-owned subsidiaries. In each case, the purchase price for the buyout would be formula-based and we expect that such buyout would be within three to five years after the initial acquisition or greenfield start-up. We also expect that a portion of the consideration for such purchases would be paid in shares of our Class B common stock.

We believe our business development model provides us with a material advantage in attracting and completing acquisitions, particularly when pharmacy owners have multiple competitive sale alternatives. Our post-closing minority ownership structure and the autonomy that comes with our local management model promote continued seller participation in the growth of the business in a meaningful way. We believe the same holds true in our greenfield start-up pharmacy initiatives. The structure incentivizes our new pharmacy operators, and the subsidiary pharmacy’s employees to whom subsidiary equity is issued, to promote the subsidiary’s growth and adoption of our proven operating strategies as we complete full integration and ownership of the pharmacy. By empowering local management, we believe this structure also fosters entrepreneurial practices consistent with those that have contributed to our successful organic growth.

Our Experienced Management Team

We have an exceptional leadership team, both at the corporate and local levels, with a proven history of industry leadership and operational excellence.

| |

• |

|

Highly experienced and entrepreneurial executive leadership. We are led by highly experienced and entrepreneurial executive officers, each of whom has more than 30 years of experience founding and leading successful companies in the pharmacy industry. Prior to our inception, Fred Burke, our President and Chief Executive Officer, David Morris, our Executive Vice President and Chief Financial Officer, and Kendall Forbes, our Executive Vice President of Sales & Operations, began working together in 1993 on a previous pharmacy venture that was acquired by Bindley Western in 1999. |

| |

• |

|

Experienced local pharmacy leadership teams. We have strong management teams in place at the local level, with the majority of local pharmacy presidents having been in their positions for over a decade. The importance and strength of our local leadership was highlighted during the COVID-19 pandemic as local management teams were empowered to make decisions in real-time that were specific to the evolving pandemic-driven conditions and regulations in their markets, in order to maintain our high service levels for our customers and residents. |

| |

• |

|

Strong corporate support group. We are supported by a team of more than 120 corporate employees who collectively bring deep experience in relevant areas such as technology, pharmacy operations, supply chain, data analytics, legal, regulatory/compliance, revenue cycle management and network contracting, purchasing, sales and marketing, real estate, human resources, leadership development and finance. |

| |

• |

|

Support from a sophisticated group of investors. We have been supported by Bindley Capital Partners, LLC, a private investment firm led by William Bindley, who serves as our Chairman of the Board and has provided significant strategic leadership. Mr. Bindley, a pioneer in the healthcare services industry, |

14

| |

was the founder, chairman and chief executive officer of Bindley Western, a pharmaceutical distribution and services company acquired by Cardinal Health, Inc. for $2.1 billion in 2001. He also served as an executive and the chairman of Priority Healthcare Corporation, a specialty pharmacy services company that was spun-off from Bindley Western in 1998 and acquired by Express Scripts, Inc. for $1.3 billion in 2005. In addition, Cardinal Equity Partners, along with Fred Burke, David Morris and Kendall Forbes, have made significant capital investments in Guardian. Collectively, this group of investors has extensive experience and expertise in the healthcare services industry. |

Servicing New Areas of Care

We believe our investments in human capital, technology, and services capabilities position us to continue to pursue rapid innovation and potentially expand our business as a health care service provider in the post-acute care sector. While to date we have primarily focused on serving the LTCF markets, we recognize the continued evolution of healthcare delivery in which alternate sites of care are increasingly relevant. For example, we believe that our core capabilities and value proposition is applicable to the large and expanding IDD, hospice and PACE end markets. We have test initiatives ongoing in these adjacent markets. Such initiatives are in the nascent stages and have generated only immaterial revenues to date.

Customers

Our customers are LTCFs and their residents. For the year ended December 31, 2025, we provided pharmacy services to approximately 205,000 residents in approximately 8,400 LTCFs across 38 states. We have established relationships with both local and large multi-facility LTCF operators, and we are generally the primary source of pharmaceuticals for the residents of the facilities we serve.

Our customers depend on pharmacies like ours to provide the necessary pharmacy products and services and to play an integral role in monitoring resident medication regimens and safety. We dispense pharmaceuticals in resident-specific packaging in accordance with physician instructions.

No single customer comprised more than 10% of our consolidated revenues in the last five fiscal years.

Customer Relationships

Our relationships with SNFs are memorialized in written agreements between Guardian and the owner of the respective facility. These contracts generally range from one to three years in duration and typically renew automatically for subsequent renewal terms. The SNF contracts can be terminated by either party generally upon 60 days’ notice. Similarly, our relationships with ALFs and BHFs are generally memorialized in written agreements between Guardian and the owner of the respective community that designate Guardian as the “preferred provider” of that community owner. Unlike a SNF contract where virtually all of the residents in the skilled facility would be served by us, the ALF and BHF contract does not automatically grant us the right to serve those residents. Instead, our sales team must still market our pharmacy services to the individual residents in that community, each of whom has the right of choice to their pharmacy provider. These contracts generally range from one to three years in duration and typically renew automatically for subsequent renewal terms. These contracts can be terminated by either party generally upon 30 days’ notice. Most LTCF contracts specify certain facility-wide services that we may provide for a fee, including EMAR support, consulting services and training. These contracts all generally have similar provisions surrounding compliance with Health Insurance Portability and Accountability Act of 1996 (“HIPAA”) obligations upon termination, limitation of liability and other standard contractual terms.

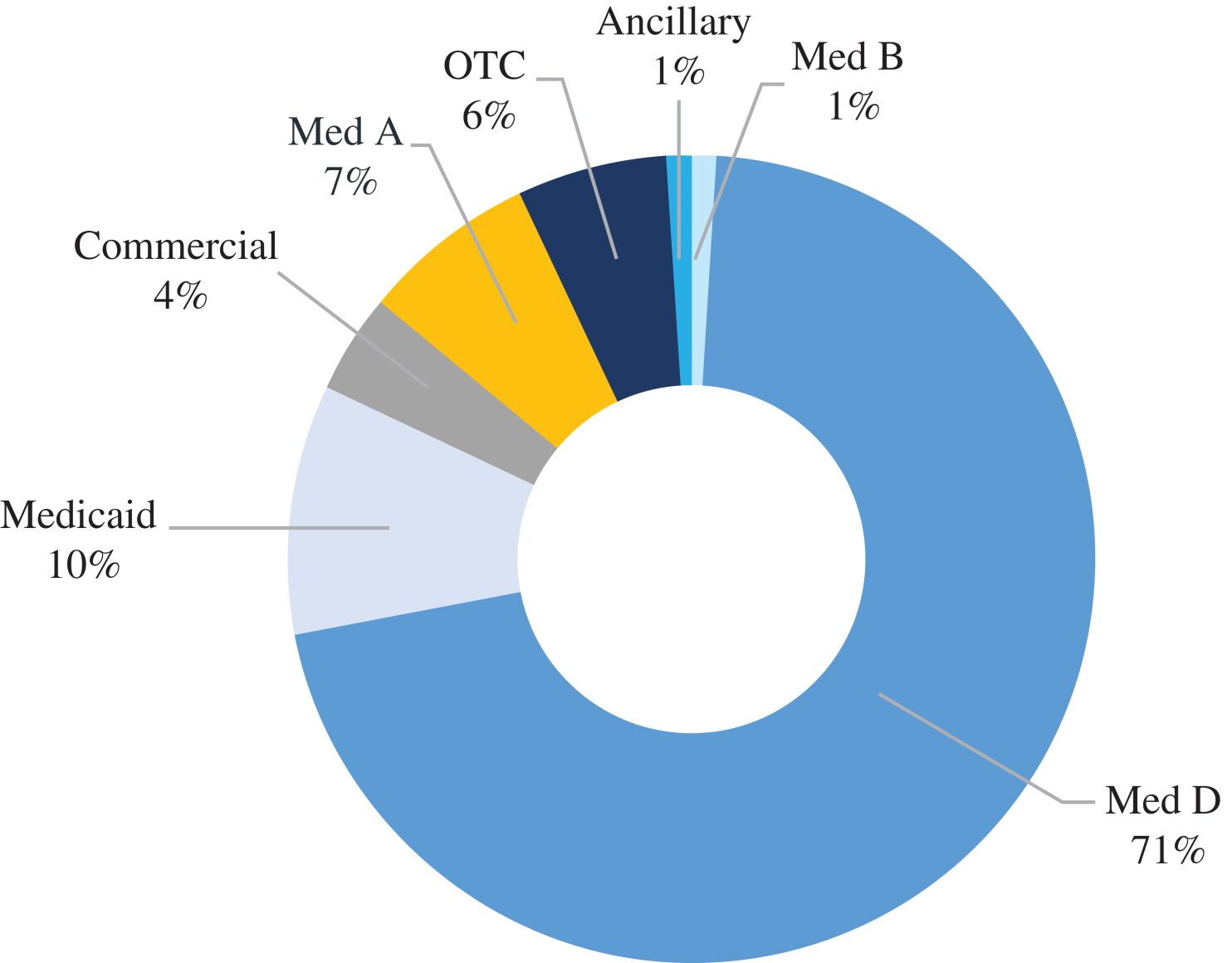

Payor Mix and Reimbursement

We derive revenues from multiple government and commercial payor sources, which we believe have a generally stable reimbursement profile. In particular, for the year ended December 31, 2025, approximately 71% of our revenue was derived from Medicare Part D. CMS mandates 10 rules and service capabilities to qualify for

15

participation as a Part D NLTCP provider, as differentiated from traditional Part D and commercial reimbursement. These required capabilities involve extended drug control and distribution systems that include items such short-cycle dispensing, compliance packaging, 24/7 support and delivery, medication regimen review, maintaining a comprehensive inventory of Part D drugs, maintaining emergency kits and retrospective billing for patient copays and coverage gaps, known as the “donut hole.” CMS designates an institutional level of care as a “distinct pharmacy setting” and requires payors to compensate designated long-term care pharmacies for the specific services they are required to provide LTCF residents. In addition, CMS requires that payors maintain network adequacy to serve LTCF residents. We believe Medicare Part D payors recognize the value that LTCF pharmacies like Guardian provide, including helping to ensure that residents adhere to the right drug regimens, which helps improve clinical outcomes and reduce the overall cost of care. We believe that, consequently, Medicare Part D plans generally offer more favorable and stable contract terms for LTCF pharmacies relative to commercial plans that are offered to retail pharmacies.

Set forth below are our revenues by payor for the year ended December 31, 2025.

Suppliers, Inventory, and Supplier and Manufacturer Rebates

We believe our purchasing scale creates a cost advantage over smaller competitors within our industry. Historically, we have purchased most of the brand name and generic pharmaceuticals we dispense from wholesale distributors with whom we have prime vendor agreements at discounted prices based on contracts negotiated by us directly; and in some cases, based upon prices accessed through group purchasing organization contracts. Our primary wholesale distributor relationships currently include Cardinal Health, Inc., McKesson Corporation, Smith Drug Company, and Morris and Dickson Co. L.L.C., in addition to various generic drug manufacturers. Additionally, we purchase some generic pharmaceuticals directly from their manufacturers. We seek to maintain an on-site inventory of pharmaceuticals and supplies at our local pharmacies to ensure prompt delivery to the facilities we serve.

16

Guardian receives a modest amount of rebates from pharmaceutical manufacturers and distributors of pharmaceutical products associated with dispensing their products. Rebates are designed to prefer, protect, or maintain a manufacturer’s products that are dispensed by the pharmacy under its formulary.

Government Regulation

Our pharmacies and the LTCFs we serve are subject to numerous federal, state and local regulations. These regulations encompass many areas, including licensing requirements, professional standards, quality control, drug dispensing, day-to-day operations and reimbursement, and in many cases apply differently depending on the type of LTCF in question. ALFs offer assisted living services for people who need help with daily care. These services may include access to prepared meals, assistance with personal care, drug administration and medication management, housekeeping, laundry, and social and recreational activities. SNFs, which are licensed healthcare residences for individuals who require a higher level of medical care than can be provided in an ALF, provide medical care—including drug administration and rehabilitation services such as physical, occupational, and speech therapy—through healthcare providers such as registered nurses, licensed practical nurses, and certified nurse’s assistants. Consequently, SNFs are heavily regulated by the federal government and by certain state governments. BHFs provide medical and personal care to residents with complex medical needs, including those with intellectual and developmental disabilities. We regularly monitor and assess the impact on our operations of new or proposed regulations and changes in the interpretation or application of existing regulations. As a pharmacy provider for LTCFs, we focus our attention on both regulations applicable to our pharmacy business as well as regulations that pertain to the institutions we serve.

Regulations That Affect Guardian Directly

Licensure

Operating a pharmacy within a state requires licensure by the respective state’s board of pharmacy. As of December 31, 2025, we had pharmacy licenses for each pharmacy we operate, and to our knowledge, all issued licenses remain valid and in good standing. In addition, states regulate out-of-state pharmacies that fill prescriptions for in-state patients (including residents). Where applicable, our pharmacies hold the requisite licenses to deliver to out-of-state patients (including residents). Our pharmacies are also registered with the appropriate state and federal authorities, such as the U.S. Drug Enforcement Administration (the “DEA”), pursuant to statutes governing the regulation of controlled substances.

Federal and State Laws Affecting the Repackaging, Labeling and Interstate Shipping of Drugs

In November 2013, the federal government enacted the Drug Quality and Security Act (“DQSA”), which, in pertinent part, was designed to facilitate drug tracing throughout the pharmaceutical supply chain. Specifically, Title II of the DQSA, the Drug Supply Chain Security Act (“DSCSA”) requires us and other supply chain stakeholders to participate in an electronic, secure interoperable system, that will identify and trace certain prescription drug products as they are distributed within the United States. The DSCSA established federal standards with which pharmacies must comply that require prescription drugs to be labeled and tracked at the package level. These standards preempt state and local requirements related to tracing drugs through the distribution system. Prior exemptions applicable to some product tracing requirements for large dispensers ended in 2025. Consequently, we are subject to the enhanced drug distribution security requirements of the DSCSA, such as: product tracing requirements for dispensers of prescription drugs, including receipt, storage, and provision of transaction information, history, and statement and verification processes; and obligations to implement systems to identify potential “suspect” or “illegitimate” products and to utilize secure, interoperable, electronic systems.

In addition, under the Comprehensive Drug Abuse Prevention and Control Act of 1970, as a dispenser of controlled substances, we are subject to various requirements, including registration with the DEA, inventory and transaction reporting filing, and maintenance of adequate security measures. In addition, we are required to

17

comply with all the relevant requirements of the Controlled Substances Act for the transfer and shipment of pharmaceuticals.

Supply chain laws and regulations such as the DQSA and DSCSA could increase the overall regulatory burden and costs associated with our dispensing business. Although we believe we are in compliance with applicable federal and state regulations currently in effect, these regulations may be interpreted, applied, or expanded in the future in a manner inconsistent with our business practices, which could adversely affect our results of operations, cash flows, and financial condition.

The DEA, the U.S. Food and Drug Administration (the “FDA”), and various state regulatory authorities have broad enforcement powers, including the ability to seize or recall products and impose significant criminal, civil and administrative sanctions for violations of these laws and regulations. We have received all necessary regulatory approvals and believe that our pharmacy operations are in substantial compliance with applicable federal and state dispensing requirements. Any changes to the current regulatory and legal paradigm could increase the overall regulatory burden and costs associated with our business.

CMS Regulations Affecting Guardian’s Provision of Pharmacy Services for Certain LTCF Customers

We are subject to a CMS rule, entitled “Medicare and Medicaid Programs, Reform of Requirements for Long-Term Care Facilities,” as amended and modified from time to time, that, among other things, revised the requirements for LTCF participation in the Medicare and Medicaid programs. The rule imposes several requirements that are specific to our pharmacy services business within certain LTCFs (e.g., pharmacist review of medical records and reporting of irregularities) and also imposes certain requirements upon LTCFs themselves, which are more fully described in “Government Regulation—Regulations That Affect Our Customers” below.

Laws Affecting Referrals and Business Practices