As filed with the Securities and Exchange

Commission on April 18, 2025

Registration No. 333-286034

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1/A

Amendment No. 1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

ATIF HOLDINGS LIMITED

(Exact name of registrant as specified in its

charter)

| British Virgin Islands | | 6531 | | Not Applicable |

(State or other jurisdiction of

incorporation or organization) | | (Primary Standard Industrial

Classification Code Number) | | (I.R.S. Employer Identification Number) |

25391 Commercentre Dr., Ste 200

Lake Forest, CA 92630

646-828-8710

(Address, including zip code, and telephone

number, including area code, of registrant’s principal executive offices)

Dr. Kamran Khan

Chief Executive Officer

25391 Commercentre Dr., Ste 200

Lake Forest, CA 92630

646-828-8710

(Name, address, including zip code, and telephone

number, including area code, of agent for service)

With copies to:

Joan Wu, Esq.

Hunter Taubman Fischer & Li LLC

950 Third Avenue, 19th Floor

New York, New York 10022

917-512-0827

Approximate date of commencement of proposed

sale of the securities to the public: As soon as practicable after this registration statement is declared effective.

If any of the securities being registered on this

Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box.

☒

If this Form is filed to register additional securities

for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed

pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of

the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed

pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of

the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant

is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company.

See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company”

and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

| | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this registration

statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment that

specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities

Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission,

acting pursuant to said Section 8(a), may determine.

The information in

this prospectus is not complete and may be changed. Neither we nor the Selling Stockholders may sell these securities until the registration

statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell and is not soliciting

an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED APRIL 18,

2025

PRELIMINARY PROSPECTUS

Restricted Warrants to Purchase up to 2,467,553

Ordinary Shares

Up to 2,467,553 Ordinary Shares underlying the

Restricted Warrants

This prospectus relates to the resale, from time

to time, by the selling stockholders identified in this prospectus under the caption “Selling Stockholders,” of restricted

warrants to purchase up to 2,467,553 Ordinary Shares (the “Restricted Warrants”) of ATIF Holdings Limited (the “Company”),

$0.001 par value (the “Ordinary Shares”), in lieu of a securities purchase agreement (the “SPA”) dated February

4, 2025.

On February 4, 2025, the Company entered into

the SPA with certain non-affiliated institutional investor (the “Purchaser”) pursuant to which the Company agreed to sell

(1) 1,580,000 Ordinary Shares, and (2) certain pre-funded warrants to purchase up to 887,553 Ordinary Shares in a registered direct offering,

and (3) in a concurrent private placement, restricted warrants to purchase an aggregate of up to 2,467,553 Ordinary Shares, for aggregate

gross proceeds of approximately $2.5 million.

For the details about the selling stockholder,

please see “Selling Stockholders.” The selling stockholder may sell these shares from time to time in the principal market

on which our Ordinary Share is traded at the prevailing market price, in negotiated transactions, or through any other means described

in the section titled “Plan of Distribution.” The selling stockholder may be deemed an underwriter within the meaning of the

Securities Act of 1933, as amended, of the Ordinary Shares that they are offering. We will pay the expenses of registering these shares.

We will not receive proceeds from the sale of our shares by the selling stockholder that are covered by this prospectus.

The shares are being registered to permit the

selling stockholder, or its respective pledgees, donees, transferees or other successors-in-interest, to sell the shares from time to

time in the public market. We do not know when or in what amount the selling stockholder may offer the securities for sale. The selling

stockholder may sell some, all or none of the securities offered by this prospectus.

Our Ordinary Shares are quoted on the Nasdaq

Capital Markets under the symbol ZBAI. On April 17, 2025, the closing price of our Ordinary

Shares was $1.01 per share.

The Selling Stockholders may sell their Ordinary

Shares described in this prospectus in a number of different ways, at prevailing market prices or privately negotiated prices and there

is no termination date of the Selling Stockholders’ offering.

You should read this prospectus, together with

additional information described under the headings “Incorporation of Certain Information by Reference” and “Where You

Can Find More Information”, carefully before you invest in any of our securities.

Investing in our securities involves a high

degree of risk. See “Risk Factors” starting on page 4 of this prospectus.

Neither the Securities and Exchange Commission

nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete.

Any representation to the contrary is a criminal offense.

The date of this prospectus is ___, 2025

TABLE OF CONTENTS

You should rely only on the information contained

in this prospectus or in any free writing prospectus that we may specifically authorize to be delivered or made available to you. We and

our Underwriter have not authorized anyone to provide you with any information other than that contained in this prospectus or in any

free writing prospectus we may authorize to be delivered or made available to you. We take no responsibility for, and can provide no assurance

as to the reliability of, any other information that others may give you. This prospectus may only be used where it is legal to offer

and sell our securities. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time

of delivery of this prospectus or any sale of our securities. Our business, financial condition, results of operations and prospects may

have changed since that date. We are not making an offer of these securities in any jurisdiction where the offer is not permitted.

Unless the context otherwise requires, the terms

“ZBAI,” “we,” “us” and “our” in this prospectus refer to ATIF HOLDINGS LIMITED, and “this

offering” refers to the offering contemplated in this prospectus.

PROSPECTUS CONVENTIONS

Except where the context otherwise requires and

for purposes of this prospectus only:

| ● | “ATIF BVI” shall

hereinafter refer to ATIF Holdings Limited, a British Virgin Islands business company. |

| ● | “ATIF USA” shall

hereinafter refer to ATIF Inc., a California corporation and a wholly-owned subsidiary of ATIF. |

| ● | “ATIF Investment”

shall hereinafter refer to ATIF Investment Limited, a British Virgin Islands business company and a wholly-owned subsidiary of ATIF. |

| ● | “ATIF BD” shall

hereinafter refer to ATIF BD LLC, a California limited liability company and a wholly-owned subsidiary of ATIF USA. |

| ● | “ATIF Consulting”

shall hereinafter refer to ATIF Business Consulting LLC, a California LLC and a wholly-owned subsidiary of ATIF USA. |

| ● | “ATIF Management”

shall hereinafter refer to ATIF Business Management LLC, a California LLC and wholly-owned subsidiary of ATIF USA. |

| ● | “we,” “us,”

“Company,” “Group,” or the “registrant” or similar terms used in this registration statement refer

to ATIF, ATIF USA, ATIF Investment, ATIF Consulting, ATIF Management, and ATIF BD, unless the context otherwise indicates. |

| ● | “Affiliated Entities”

shall refer to the ATIF USA, ATIF Consulting, ATIF Management, ATIF Investment and ATIF BD. |

| ● | “China” or “PRC”

are to the People’s Republic of China, including Hong Kong and Macau; however the only time such jurisdictions are not included

in the definition of PRC and China is when we reference to the specific laws that have been adopted by the PRC. The same legal and operational

risks associated with operations in China also apply to operations in Hong Kong. The term “Chinese” has a correlative meaning

for the purpose of this prospectus; |

| ● | “preferred shares,”

or “Preferred Shares” are to the Class A preferred shares of the Company, par value $0.001 per share; |

| ● | “RMB” and “Renminbi”

are to the legal currency of the PRC; |

| ● | “SEC” are to the

Securities and Exchange Commission; |

| ● | “Securities Act”

are to the Securities Act of 1933, as amended; |

| ● | “shares,” “Shares,”

or “Ordinary Shares” are to the Ordinary Shares of the Company, par value $0.001 per share; and |

| ● | “U.S. dollars”

and “$” are to the legal currency of the United States. |

INDUSTRY AND MARKET DATA

This prospectus includes information with respect

to market and industry conditions and market share from third-party sources or based upon estimates using such sources when available.

We have not, directly or indirectly, sponsored or participated in the publication of any of such materials. We believe that such information

and estimates are reasonable and reliable. We also assume the information extracted from publications of third-party sources has been

accurately reproduced. We understand that the Company would be liable for the information included in this prospectus if any part of the

information was incorrect, misleading or imprecise to a material extent.

PROSPECTUS SUMMARY

This summary highlights information contained

elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision.

Before investing in our securities, you should carefully read this entire prospectus, including our financial statements and the related

notes and the information set forth under the headings “Risk Factors” and “Management’s Discussion and Analysis

of Financial Condition and Results of Operations” in each case included elsewhere in this prospectus.

Company Overview

Business Overview

We are a British Virgin

Islands business company. We are a business consulting company providing financial consulting services to small and medium-sized enterprises

(“SMEs”) and prior to August 1, 2022, our Affiliated Entity ATIF USA, managed a private equity fund with approximately $1.3

million assets under management (“AUM”). Since our inception in 2015, the main focus of our consulting business has been providing

comprehensive going public consulting services designed to help SMEs become public companies on suitable stock markets and exchanges.

Our goal is to become an international financial consulting company with clients and offices throughout North America and Asia. In order

to expand our business with a flexible business concept and reach our goal of high growth revenue and strong profit growth, on January

4, 2021, we opened an office in California, USA, through our wholly owned subsidiary ATIF USA. Our clients located within United States

are serviced by ATIF USA. ATIF relies on a professional service team, who is rich in business consulting experiences, extensive social

relations, and international integrated services, to make the IPO process as easy as possible for its clients. We operate with competitive

fee schedules and in the cases of clients with attractive financial performance and/or great growth potential, we would offer the option

of paying no fees upfront.

To mitigate the potential

risks arising from the PRC government provision of new guidance to and restrictions on China-based companies raising capital offshore,

we decided to divest our PRC subsidiaries. As of May 31, 2022, we completed the transfer of our equity interest in ATIF Limited, a Hong

Kong corporation (“ATIF HK”) and Huaya Consulting (Shenzhen) Co., Ltd., corporation formed under the laws of the PRC (“Huaya”)

to Mr. Pishan Chi, our former director and CEO, for no consideration.

We have primarily

focused on helping clients going public on the national stock exchanges and OTC Markets in the U.S. As of the date of this prospectus,

we have provided financial consulting services to SMEs in the United States, Mexico, China and Hong Kong. The following table illustrates

the breakdown of our total revenue, organized by customers’ locations for the years ended July 31, 2024 and 2023, and for the six months

ended January 31, 2025 and 2024.

| | |

Year ended

July 31,

2024 | | |

Percentage

of Total | | |

Year ended

July 31,

2023 | | |

Percentage

of Total | |

| | |

Revenue | | |

revenue | | |

Revenue | | |

revenue | |

| Hong Kong | |

| | | |

| | | |

| 600,000 | | |

| 24 | % |

| Mainland China | |

| | | |

| | | |

| | | |

| | |

| USA | |

| 620,000 | | |

| 100 | % | |

| 1,200,000 | | |

| 49 | % |

| Mexico | |

| | | |

| | | |

| 650,000 | | |

| 27 | % |

| Total revenue, net | |

$ | 620,000 | | |

| 100 | % | |

| 2,450,000 | | |

| 100 | % |

| | |

Six months ended

January 31,

2025 | | |

Percentage

of Total | | |

Six months ended

January 31,

2024 | | |

Percentage

of Total | |

| | |

Revenue | | |

revenue | | |

Revenue | | |

revenue | |

| Hong Kong | |

| | |

| | |

| | |

| |

| Mainland China | |

| | |

| | |

| | |

| |

| USA | |

| 200,000 | | |

| 100 | % | |

| 150,000 | | |

| 100 | % |

| Mexico | |

| | | |

| | | |

| | | |

| | |

| Total revenue, net | |

$ | 200,000 | | |

| 100 | % | |

| 150,000 | | |

| 100 | % |

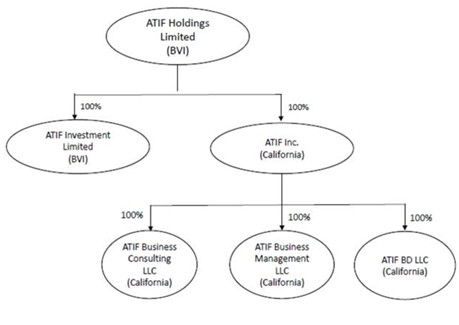

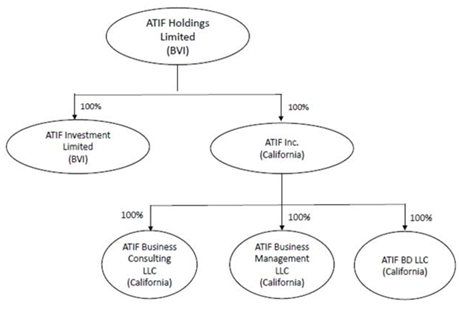

Corporate Structure

The following diagram illustrates our current corporate structure:

Recent Developments

Share Cancellation

On February 3, 2025, the Company and certain investors

(the “Purchasers”) party to a certain securities purchase agreement dated January 15, 2025 (the “SPA”) entered

into a certain letter agreement to buy back and cancel an aggregate of 1,480,000 ordinary shares issued to the Purchasers pursuant to

the SPA in exchange for the payment of an aggregate of $1,850,000 to the Purchasers.

Registered Direct Offering

On February 4, 2025, the Company and certain investors entered

into a certain securities purchase agreement pursuant to which the Company agreed to sell (1) 1,580,000 ordinary shares, par value $0.001

per share (the “Ordinary Shares”), and (2) certain pre-funded warrants to purchase up to 887,553 Ordinary Shares (the “Pre-Funded

Warrants”) in a registered direct offering, and (3) in a concurrent private placement, restricted warrants to purchase an aggregate

of up to 2,467,553 Ordinary Shares (the “Restricted Warrants”), for aggregate gross proceeds of approximately $2.5 million

(the “February Offering”). The February Offering closed on February 5, 2025.

NASDAQ Listing

On November 26, 2024, the Company received a notification

letter from the Nasdaq Listing Qualifications Staff of The NASDAQ Stock Market LLC (“Nasdaq”) notifying the Company that the

minimum bid price per share for its ordinary shares has been below $1.00 for a period of 30 consecutive business days and the Company

therefore no longer meets the minimum bid price requirements set forth in Nasdaq Listing Rule 5550(a)(2). In accordance with Nasdaq Listing

Rule 5810(c)(3)(A), the Company has been provided 180 calendar days, or until April 14, 2025, to regain compliance.

On January 15, 2025, the Company received a notification

letter from Nasdaq stating that the Company has regained compliance with Nasdaq Listing Rule 5550(a)(2) and this matter is now closed.

If the Company fails to maintain compliance with

other listing rules in the future, we could be subject to suspension and delisting proceedings. If our securities lose their status on

The NASDAQ Capital Market, our securities would likely trade in the over-the-counter market. If our securities were to trade on the over-the-counter

market, selling our securities could be more difficult because smaller quantities of securities would likely be bought and sold, transactions

could be delayed, and security analysts’ coverage of us may be reduced. In addition, in the event our securities are delisted, broker-dealers

have certain regulatory burdens imposed upon them, which may discourage broker-dealers from effecting transactions in our securities,

further limiting the liquidity of our securities. These factors could result in lower prices and larger spreads in the bid and ask prices

for our securities. Such delisting from The NASDAQ Capital Market and continued or further declines in our share price could also greatly

impair our ability to raise additional necessary capital through equity or debt financing, and could significantly increase the ownership

dilution to shareholders caused by our issuing equity in financing or other transactions.

Corporate Information

Our principal executive office is located at 25391

Commercentre Dr., Ste 200, Lake Forest, CA 92630. Our telephone number at that address is 308-888-8888. Our company website is https://ir.atifus.com.

Our NASDAQ symbol is “ZBAI,” and we make our SEC filings available on the Investor Relations page of our website, https://ir.atifus.com.

Information contained on our website is not part of this prospectus.

THE OFFERING

| Ordinary Shares being offered by Selling Stockholders |

Up to 2,467,553 Ordinary Shares underlying the

Restricted Warrants, which can be exercised at a price of $1.20 per share.

The Selling Stockholders may sell their Ordinary

Shares at prevailing market prices or privately negotiated prices. We will not receive any proceeds from the sales by the Selling Stockholders. |

| |

|

| Use of Proceeds |

We will not receive any proceeds from the sale of shares by the Selling Stockholders. |

| |

|

| Trading Symbol |

ZBAI |

| |

|

| Risk Factors |

The securities offered by this prospectus are speculative and involve

a high degree of risk and investors purchasing securities should not purchase the securities unless they can afford the loss of

their entire investment. You should read “Risk Factors,” beginning on page 4 for a discussion of factors to consider

before deciding to invest in our securities. |

| |

|

| Transfer Agent |

Transhare Corporation |

RISK FACTORS

Investing in our securities involves a high

degree of risk. Before you make a decision to invest in our securities, you should consider carefully the risks described below. You should

also carefully consider the risk factors set forth under “Risk Factors” described in our most recent annual report on Form

10-K, filed on November 13, 2024, as supplemented and updated by subsequent quarterly reports on Form 10-Q and current reports on Form

8-K that we have filed with the SEC, together with all other information contained or incorporated by reference in this prospectus and

any applicable prospectus supplement and in any related free writing prospectus in connection with a specific offering, before making

an investment decision. Each of the risk factors could materially and adversely affect our business, operating results, financial condition

and prospects, as well as the value of an investment in our securities, and the occurrence of any of these risks might cause you to lose

all or part of your investment.

Because we are a small company, the requirements

of being a public company, including compliance with the reporting requirements of the Securities Exchange Act of 1934, as amended (the

“Exchange Act”), and the requirements of the Sarbanes-Oxley Act and the Dodd-Frank Act, may strain our resources, increase

our costs and distract management, and we may be unable to comply with these requirements in a timely or cost-effective manner.

As a public company with listed equity securities,

we must comply with the federal securities laws, rules and regulations, including certain corporate governance provisions of the Sarbanes-Oxley

Act of 2002 (the “Sarbanes-Oxley Act”) and the Dodd-Frank Act, related rules and regulations of the SEC and the NASDAQ,

with which a private company is not required to comply. Complying with these laws, rules and regulations occupies a significant amount

of the time of our Board of Directors and management and significantly increases our costs and expenses. Among other things, we must:

| ● | maintain a system of internal

control over financial reporting in compliance with the requirements of Section 404 of the Sarbanes-Oxley Act and the related rules and

regulations of the SEC and the Public Company Accounting Oversight Board; |

| ● | comply with rules and regulations

promulgated by the NASDAQ; |

| ● | prepare and distribute periodic

public reports in compliance with our obligations under the federal securities laws; |

| ● | maintain various internal compliance

and disclosures policies, such as those relating to disclosure controls and procedures and insider trading in our ordinary shares; |

| ● | involve and retain to a greater

degree outside counsel and accountants in the above activities; |

| ● | maintain a comprehensive internal

audit function; and |

| ● | maintain an investor relations

function. |

Future sales of our ordinary shares, whether by us or our shareholders,

could cause our share price to decline

If our existing shareholders sell, or indicate

an intent to sell, substantial amounts of our ordinary shares in the public market, the trading price of our ordinary shares could decline

significantly. Similarly, the perception in the public market that our shareholders might sell of our ordinary shares could also depress

the market price of our ordinary shares. A decline in the price of our ordinary shares might impede our ability to raise capital through

the issuance of additional of our ordinary shares or other equity securities. In addition, the issuance and sale by us of additional of

our ordinary shares or securities convertible into or exercisable for our ordinary shares, or the perception that we will issue such securities,

could reduce the trading price for our ordinary shares as well as make future sales of equity securities by us less attractive or not

feasible. The sale of ordinary shares issued upon the exercise of our outstanding options and warrants could further dilute the holdings

of our then existing shareholders.

Securities analysts may not cover our ordinary

shares and this may have a negative impact on the market price of our ordinary shares

The trading market for our ordinary shares will

depend, in part, on the research and reports that securities or industry analysts publish about us or our business. We do not have any

control over independent analysts (provided that we have engaged various non-independent analysts). We do not currently have and may never

obtain research coverage by independent securities and industry analysts. If no independent securities or industry analysts commence coverage

of us, the trading price for our ordinary shares would be negatively impacted. If we obtain independent securities or industry analyst

coverage and if one or more of the analysts who covers us downgrades our ordinary shares, changes their opinion of our shares or publishes

inaccurate or unfavorable research about our business, our share price would likely decline. If one or more of these analysts ceases coverage

of us or fails to publish reports on us regularly, demand for our ordinary shares could decrease and we could lose visibility in the financial

markets, which could cause our share price and trading volume to decline.

You may experience future dilution as a result of future equity

offerings or other equity issuances

We may in the future issue additional of our ordinary

shares or other securities convertible into or exchangeable for of our ordinary shares. We cannot assure you that we will be able to sell

of our ordinary shares or other securities in any other offering or other transactions at a price per share that is equal to or greater

than the price per share paid by investors in this offering. The price per share at which we sell additional of our ordinary shares or

other securities convertible into or exchangeable for our ordinary shares in future transactions may be higher or lower than the price

per share in this offering.

If we fail to comply with the continued

listing requirements of NASDAQ, we would face possible delisting, which would result in a limited public market for our shares and make

obtaining future debt or equity financing more difficult for us.

On November 26, 2024, the Company received a notification

letter from the Nasdaq Listing Qualifications Staff of The NASDAQ Stock Market LLC (“Nasdaq”) notifying the Company that the

minimum bid price per share for its ordinary shares has been below $1.00 for a period of 30 consecutive business days and the Company

therefore no longer meets the minimum bid price requirements set forth in Nasdaq Listing Rule 5550(a)(2). In accordance with Nasdaq Listing

Rule 5810(c)(3)(A), the Company has been provided 180 calendar days, or until April 14, 2025, to regain compliance.

On January 15, 2025, the Company received a notification

letter from Nasdaq stating that the Company has regained compliance with Nasdaq Listing Rule 5550(a)(2) and this matter is now closed.

If the Company fails to maintain compliance with

other listing rules in the future, we could be subject to suspension and delisting proceedings. If our securities lose their status on

The NASDAQ Capital Market, our securities would likely trade in the over-the-counter market. If our securities were to trade on the over-the-counter

market, selling our securities could be more difficult because smaller quantities of securities would likely be bought and sold, transactions

could be delayed, and security analysts’ coverage of us may be reduced. In addition, in the event our securities are delisted, broker-dealers

have certain regulatory burdens imposed upon them, which may discourage broker-dealers from effecting transactions in our securities,

further limiting the liquidity of our securities. These factors could result in lower prices and larger spreads in the bid and ask prices

for our securities. Such delisting from The NASDAQ Capital Market and continued or further declines in our share price could also greatly

impair our ability to raise additional necessary capital through equity or debt financing, and could significantly increase the ownership

dilution to shareholders caused by our issuing equity in financing or other transactions.

Techniques employed by short sellers may

drive down the market price of our ordinary shares.

Short selling is the practice of selling securities

that the seller does not own but rather has borrowed from a third party with the intention of buying identical securities back at a later

date to return to the lender. The short seller hopes to profit from a decline in the value of the securities between the sale of the borrowed

securities and the purchase of the replacement shares, as the short seller expects to pay less in that purchase than it received in the

sale. As it is in the short seller’s interest for the price of the security to decline, many short sellers publish, or arrange for

the publication of, negative opinions regarding the relevant issuer and its business prospects in order to create negative market momentum

and generate profits for themselves after selling a security short. These short attacks have, in the past, led to selling of shares in

the market.

Public companies listed in the United States that

have a substantial majority of their operations in China have been the subject of short selling. Much of the scrutiny and negative publicity

has centered on allegations of a lack of effective internal control over financial reporting resulting in financial and accounting irregularities

and mistakes, inadequate corporate governance policies or a lack of adherence thereto and, in many cases, allegations of fraud. As a result,

many of these companies are now conducting internal and external investigations into the allegations and, in the interim, are subject

to shareholder lawsuits and/or SEC enforcement actions.

We may in the future be, the subject of unfavorable

allegations made by short sellers. Any such allegations may be followed by periods of instability in the market price of our ordinary

shares and negative publicity. If and when we become the subject of any unfavorable allegations, whether such allegations are proven to

be true or untrue, we could have to expend a significant amount of resources to investigate such allegations and/or defend ourselves.

While we would strongly defend against any such short seller attacks, we may be constrained in the manner in which we can proceed against

the relevant short seller by principles of freedom of speech, applicable federal or state law or issues of commercial confidentiality.

Such a situation could be costly and time-consuming and could distract our management from growing our business. Even if such allegations

are ultimately proven to be groundless, allegations against us could severely impact our business operations and shareholder’s equity,

and the value of any investment in our ordinary shares could be greatly reduced or rendered worthless.

We do not intend

to apply for any listing of the Restricted Warrants on any exchange or nationally recognized trading system, and we do not expect a market

to develop for the Restricted Warrants.

We do not intend to apply for any listing of the

Restricted Warrants on Nasdaq Stock Market or any other securities exchange or nationally

recognized trading system, and we do not expect a market to develop for the Restricted Warrants.

Without an active market, the liquidity of the Restricted Warrants

will be limited. Further, the existence of the Restricted Warrants may act to reduce both the trading volume and the trading price of

the Ordinary Shares.

Except as otherwise

provided in the Restricted Warrants, holders of the Restricted Warrants purchased in this offering will have no rights as our shareholders.

The Restricted Warrants

offered in this offering do not confer any rights as shareholders of our company on their holders, such as voting rights or the right

to receive dividends, but rather merely represent the right to acquire the Ordinary Shares at a

fixed price for a limited period of time. Specifically, a holder of a Restricted Warrant

may exercise the right to acquire one Ordinary Share and pay a nominal exercise price at

any time. Upon exercise of the Restricted Warrants, their holders will be entitled to exercise

the rights of a holder of the Ordinary Shares only as to matters for which the record date occurs after the exercise date.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements

that involve risks and uncertainties, including statements based on our current expectations, assumptions, estimates and projections about

us, our industry and the regulatory environment in which we and companies integral to our ecosystem operate. The forward-looking statements

are contained principally in the sections entitled “Prospectus Summary,” “Risk Factors,” “Use of Proceeds,”

“Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business.”

These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements

to be materially different from those expressed or implied by the forward-looking statements. In some cases, these forward-looking statements

can be identified by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,”

“estimate,” “intend,” “plan,” “believe,” “potential,” “continue,”

“is/are likely to” or other similar expressions. The forward-looking statements included in this prospectus relate to, among

others:

| ● | risks and uncertainties associated

with our research and development activities, including our clinical trials and preclinical studies; |

| ● | the timing or likelihood of

regulatory filings and approvals or of alternative regulatory pathways for our drug candidates; |

| ● | the potential market opportunities

for commercializing our drug candidates; |

| ● | our expectations regarding

the potential market size and the size of the patient populations for our drug candidates, if approved for commercial use, and our ability

to serve such markets; |

| ● | estimates of our expenses,

future revenue, capital requirements and our needs for additional financing; |

| ● | our ability to develop, acquire

and advance our product candidates into, and successfully complete, clinical trials and preclinical studies and obtain regulatory approvals; |

| ● | the implementation of our business

model and strategic plans for our business and drug candidates; |

| ● | the initiation, cost, timing,

progress and results of future preclinical studies and clinical trials, and our research and development programs; |

| ● | the terms of future licensing

arrangements, and whether we can enter into such arrangements at all; |

| ● | timing and receipt or payments

of licensing and milestone revenues, if any; |

| ● | the scope of protection we

are able to establish and maintain for intellectual property rights covering our drug candidates and our ability to operate our business

without infringing the intellectual property rights of others; |

| ● | regulatory developments in

the United States and foreign countries; |

| ● | the performance of our third

party suppliers and manufacturers; |

| ● | our ability to maintain and

establish collaborations or obtain additional funding; |

| ● | the success of competing therapies

that are currently or may become available; |

| ● | our ability to continue as

a going concern; |

| ● | the

effect of the ongoing COVID-19 pandemic; |

| ● | our financial performance; and |

| ● | developments and projections

relating to our competitors and our industry. |

We caution you that the forward-looking statements

highlighted above do not encompass all of the forward-looking statements made in this prospectus or in the documents incorporated by reference

in this prospectus.

There are important factors that could cause actual

results to vary materially from those described herein as anticipated, estimated or expected, including, but not limited to: the effects

of the COVID-19 outbreak, including on the demand for our products; the duration of the COVID-19 outbreak and severity of such outbreak

in regions where we operate; the pace of recovery following the COVID-19 outbreak; our ability to implement cost containment

and business recovery strategies; the adverse effects of the COVID-19 outbreak on our business or the market price of our Ordinary

Shares; competition in the industry in which we operate and the impact of such competition on pricing, revenues and margins, volatility

in the securities market due to the general economic downturn; SEC regulations which affect trading in the securities of “penny

stocks,” and other risks and uncertainties described herein and the risk factors set forth in “Risk Factors”, in our

Annual Report on Form 10-K for the fiscal year 2024, and elsewhere in the documents incorporated by reference into this prospectus. Moreover,

we operate in a very competitive and challenging environment. New risks and uncertainties emerge from time to time, and it is not possible

for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this prospectus

and in the documents incorporated by reference in this prospectus. We cannot assure you that the results, events and circumstances reflected

in the forward-looking statements will be achieved or occur, and actual results, events or circumstances could differ materially from

those described in the forward-looking statements. Except as required by law, we assume no obligation to update any forward-looking statements

publicly, or to update the reasons actual results could differ materially from those anticipated in any forward- looking statements, even

if new information becomes available in the future. Depending on the market for our stock and other conditional tests, a specific safe

harbor under the Private Securities Litigation Reform Act of 1995 may be available. Notwithstanding the above, Section 27A of the Securities

Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange

Act”) expressly state that the safe harbor for forward-looking statements does not apply to companies that issue penny stock. Because

we may from time to time be considered to be an issuer of penny stock, the safe harbor for forward-looking statements may not apply to

us at certain times.

The forward-looking statements contained in this

prospectus and in the documents incorporated by reference in this prospectus relate only to events as of the date on which the statements

are made. We do not undertake any obligation to release publicly any revisions to such forward-looking statements to reflect events or

circumstances after the date of this prospectus or to reflect the occurrence of unanticipated events. We may not actually achieve the

plans, intentions or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward-looking

statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint

ventures, other strategic transactions or investments we may make.

USE OF PROCEEDS

Unless otherwise indicated

in a prospectus supplement, we intend to use the net proceeds from the sale of the securities under this prospectus for general corporate

purposes, which may include, among other things, repayment of debt, repurchases of ordinary shares, capital expenditures, the financing

of possible acquisitions or business expansions, increasing our working capital and the financing of ongoing operating expenses and overhead.

DETERMINATION OF OFFERING PRICE

The selling stockholders may sell these shares

in the over-the-counter market or otherwise, at market prices prevailing at the time of sale, at prices related to the prevailing market

price, or at negotiated prices. We will not receive any proceeds from the sale of shares by the selling stockholders.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis should

be read together with our financial statements and the related notes appearing elsewhere in this prospectus. This discussion contains

forward-looking statements reflecting our current expectations that involve risks and uncertainties. Actual results and the timing of

events could differ materially from those discussed in our forward-looking statements as a result of many factors, including those set

forth under “Risk Factors” and elsewhere in this prospectus.

Overview

Business Overview

We are a British Virgin

Islands business company. We are a business consulting company providing financial consulting services to small and medium-sized enterprises

(“SMEs”) and prior to August 1, 2022, our Affiliated Entity ATIF USA, managed a private equity fund with approximately $1.3

million assets under management (“AUM”). Since our inception in 2015, the main focus of our consulting business has been providing

comprehensive going public consulting services designed to help SMEs become public companies on suitable stock markets and exchanges.

Our goal is to become an international financial consulting company with clients and offices throughout North America and Asia. In order

to expand our business with a flexible business concept and reach our goal of high growth revenue and strong profit growth, on January

4, 2021, we opened an office in California, USA, through our wholly owned subsidiary ATIF USA. Our clients located within United States

are serviced by ATIF USA. ATIF relies on a professional service team, who is rich in business consulting experiences, extensive social

relations, and international integrated services, to make the IPO process as easy as possible for its clients. We operate with competitive

fee schedules and in the cases of clients with attractive financial performance and/or great growth potential, we would offer the option

of paying no fees upfront.

To mitigate the potential

risks arising from the PRC government provision of new guidance to and restrictions on China-based companies raising capital offshore,

we decided to divest our PRC subsidiaries. As of May 31, 2022, we completed the transfer of our equity interest in ATIF Limited, a Hong

Kong corporation (“ATIF HK”) and Huaya Consulting (Shenzhen) Co., Ltd., corporation formed under the laws of the PRC (“Huaya”)

to Mr. Pishan Chi, our former director and CEO, for no consideration.

We have primarily

focused on helping clients going public on the national stock exchanges and OTC Markets in the U.S. As of the date of this prospectus,

we have provided financial consulting services to SMEs in the United States, Mexico, China and Hong Kong. The following table illustrates

the breakdown of our total revenue, organized by customers’ locations for the years ended July 31, 2024 and 2023, and the six months

ended January 31, 2025 and 2024.

| | |

Year ended

July 31,

2024 | | |

Percentage

of Total | | |

Year ended

July 31,

2023 | | |

Percentage

of Total | |

| | |

Revenue | | |

revenue | | |

Revenue | | |

revenue | |

| Hong Kong | |

| | | |

| | | |

| 600,000 | | |

| 24 | % |

| Mainland China | |

| | | |

| | | |

| | | |

| | |

| USA | |

| 620,000 | | |

| 100 | % | |

| 1,200,000 | | |

| 49 | % |

| Mexico | |

| | | |

| | | |

| 650,000 | | |

| 27 | % |

| Total revenue, net | |

$ | 620,000 | | |

| 100 | % | |

| 2,450,000 | | |

| 100 | % |

| | |

Six months ended

January 31,

2025 | | |

Percentage

of Total | | |

Six months ended

January 31,

2024 | | |

Percentage

of Total | |

| | |

Revenue | | |

revenue | | |

Revenue | | |

revenue | |

| Hong Kong | |

| | |

| | |

| | |

| |

| Mainland China | |

| | |

| | |

| | |

| |

| USA | |

| 200,000 | | |

| 100 | % | |

| 150,000 | | |

| 100 | % |

| Mexico | |

| | | |

| | | |

| | | |

| | |

| Total revenue, net | |

$ | 200,000 | | |

| 100 | % | |

| 150,000 | | |

| 100 | % |

NASDAQ Listing

On November 26, 2024, the Company received a notification

letter from the Nasdaq Listing Qualifications Staff of The NASDAQ Stock Market LLC (“Nasdaq”) notifying the Company that the

minimum bid price per share for its ordinary shares has been below $1.00 for a period of 30 consecutive business days and the Company

therefore no longer meets the minimum bid price requirements set forth in Nasdaq Listing Rule 5550(a)(2). In accordance with Nasdaq Listing

Rule 5810(c)(3)(A), the Company has been provided 180 calendar days, or until April 14, 2025, to regain compliance.

On January 15, 2025, the Company received a notification

letter from Nasdaq stating that the Company has regained compliance with Nasdaq Listing Rule 5550(a)(2) and this matter is now closed.

If the Company fails to maintain compliance with

other listing rules in the future, we could be subject to suspension and delisting proceedings. If our securities lose their status on

The NASDAQ Capital Market, our securities would likely trade in the over-the-counter market. If our securities were to trade on the over-the-counter

market, selling our securities could be more difficult because smaller quantities of securities would likely be bought and sold, transactions

could be delayed, and security analysts’ coverage of us may be reduced. In addition, in the event our securities are delisted, broker-dealers

have certain regulatory burdens imposed upon them, which may discourage broker-dealers from effecting transactions in our securities,

further limiting the liquidity of our securities. These factors could result in lower prices and larger spreads in the bid and ask prices

for our securities. Such delisting from The NASDAQ Capital Market and continued or further declines in our share price could also greatly

impair our ability to raise additional necessary capital through equity or debt financing, and could significantly increase the ownership

dilution to shareholders caused by our issuing equity in financing or other transactions.

Registered Direct Offering

On February 4, 2025, ATIF Holdings Limited (the

“Company”) entered into certain securities purchase agreement (the “Purchase Agreement”) with certain non-affiliated

institutional investor (the “Purchaser”) pursuant to which the Company agreed to sell (1) 1,580,000 ordinary shares, par value

$0.001 per share (the “Ordinary Shares”), and (2) certain pre-funded warrants to purchase up to 887,553 Ordinary Shares (the

“Pre-Funded Warrants”) in a registered direct offering, and (3) in a concurrent private placement, restricted warrants to

purchase an aggregate of up to 2,467,553 Ordinary Shares (the “Restricted Warrants”), for aggregate gross proceeds of approximately

$2.5 million (the “Offering”).

Summary of Critical Accounting Policies

Basis of Presentation

The interim unaudited condensed consolidated financial

statements are prepared and presented in accordance with accounting principles generally accepted in the United States (“U.S. GAAP”).

The unaudited condensed consolidated balance

sheets as of January 31, 2025 and for the unaudited condensed consolidated statement of operations and comprehensive loss for the six

months ended January 31, 2025 and 2024 have been prepared without audit, pursuant to the rules and regulations of the SEC and pursuant

to Regulation S-X. Certain information and footnote disclosures, which are normally included in annual financial statements prepared

in accordance with U.S. GAAP, have been omitted pursuant to those rules and regulations. The unaudited condensed consolidated financial

statements should be read in conjunction with the audited financial statements and the notes thereto, included in the Form 10-K for the

fiscal year ended July 31, 2024, which was filed with the SEC on November 13, 2024.

In the opinion of the management, the accompanying

condensed consolidated financial statements reflect all normal recurring adjustments, which are necessary for a fair presentation of

financial results for the interim periods presented. The Company believes that the disclosures are adequate to make the information presented

not misleading. The accompanying condensed consolidated financial statements have been prepared using the same accounting policies as

used in the preparation of the Company’s consolidated financial statements for the year ended July 31, 2024. The results of operations

for the six months ended January 31, 2025 and 2024 are not necessarily indicative of the results for the full years.

The unaudited condensed consolidated financial

statements of the Company include the accounts of the Company and its subsidiaries. All intercompany balances and transactions have been

eliminated upon consolidation.

Results of Operations for the Years Ended July 31, 2024 and

2023

The following table summarizes

the results of our operations for the fiscal years ended July 31, 2024 and 2023, respectively, and provides information regarding the

dollar and percentage increase or (decrease) during such periods.

| | |

For the years ended | | |

Changes | |

| | |

July 31,

2024 | | |

July 31,

2023 | | |

Amount

Increase

(Decrease) | | |

Percentage

Increase

(Decrease) | |

| Revenues - third parties | |

$ | 420,000 | | |

$ | 1,150,000 | | |

$ | (730,000 | ) | |

| (63 | )% |

| Revenues - a related party | |

| 200,000 | | |

| 1,300,000 | | |

| (1,100,000 | ) | |

| (85 | )% |

| Revenues | |

$ | 620,000 | | |

$ | 2,450,000 | | |

$ | (1,830,000 | ) | |

| (75 | )% |

| | |

| | | |

| | | |

| | | |

| | |

| Operating expenses: | |

| | | |

| | | |

| | | |

| | |

| Selling expenses | |

| 333,500 | | |

| 207,238 | | |

| 126,262 | | |

| 61 | % |

| General and administrative expenses | |

| 2,265,612 | | |

| 2,241,626 | | |

| 23,986 | | |

| 1 | % |

| (Reversal of provision) provision against accounts receivable due from a related party | |

| (19,103 | ) | |

| 762,000 | | |

| (781,103 | ) | |

| (103 | )% |

| Total operating expenses | |

| 2,580,009 | | |

| 3,210,864 | | |

| (630,855 | ) | |

| (20 | )% |

| | |

| | | |

| | | |

| | | |

| | |

| Loss from operations | |

| (1,960,009 | ) | |

| (760,864 | ) | |

| 1,199,145 | | |

| 158 | % |

| | |

| | | |

| | | |

| | | |

| | |

| Other income (expenses): | |

| | | |

| | | |

| | | |

| | |

| Interest income, net | |

| 26 | | |

| 1,874 | | |

| (1,848 | ) | |

| (99 | )% |

| Other (expenses) income, net | |

| (846,871 | ) | |

| 314,518 | | |

| (1,161,389 | ) | |

| (369 | )% |

| Provision against due from buyers of LGC | |

| - | | |

| (2,654,767 | ) | |

| (2,654,767 | ) | |

| (100 | )% |

| (Loss) gain from investment in trading securities | |

| (381,370 | ) | |

| 192,102 | | |

| (573,472 | ) | |

| (299 | )% |

| Gain from disposal of subsidiaries and VIE | |

| - | | |

| 56,038 | | |

| (56,038 | ) | |

| (100 | )% |

| Total other expense, net | |

| (1,228,215 | ) | |

| (2,090,235 | ) | |

| (862,020 | ) | |

| (41 | )% |

| | |

| | | |

| | | |

| | | |

| | |

| Loss before income taxes | |

| (3,188,224 | ) | |

| (2,851,099 | ) | |

| 337,125 | | |

| 12 | % |

| | |

| | | |

| | | |

| | | |

| | |

| Income tax provision | |

| (3,300 | ) | |

| (31,200 | ) | |

| (27,900 | ) | |

| (89 | )% |

| Net loss | |

$ | (3,191,524 | ) | |

$ | (2,882,299 | ) | |

$ | 309,225 | | |

| 11 | % |

Revenues. Our

total revenue decreased by approximately $1.8 million, or 75%, from approximately $2.5 million in fiscal year 2023, to approximately $0.6

million in fiscal year 2024, primarily attributable to a decrease of approximately $0.7 million and $1.1 million, respectively, from consulting

services to third parties and related parties.

The decrease in revenues from

third parties was primarily because we provided listing related consulting services for seven customers and earned consulting service

fees of approximately $0.4 million for the fiscal year ended July 31, 2024, while we provided phase completed phase I and phase II services

for two customers and earned consulting service fees of approximately $1.2 million for the fiscal year ended July 31, 2023. The phase

I and phase II service fees are higher than listing related consulting services, because the phase I and phase II services take longer

time.

The decrease in revenues from

related parties was primarily because we provided consulting services to less customers on behalf of related parties. For the fiscal year

ended July 31, 2024 and 2023, we provided consulting services to one and two customers on behalf of a related party, respectively.

Selling expenses. Selling

expenses increased by approximately $0.1 million, or 61%, from approximately $0.2 million in year ended July 31, 2023 to approximately

$0.3 million in the same period ended July 31, 2024. Our selling expenses primarily consisted of promotion and advertising expenses. The

increase in our selling expenses was primarily due to an increase of amortization expenses of approximately $0.1 million for TV promotion

videos.

As a percentage of sales,

our selling expenses were 54% and 8% of our total revenues for the fiscal years ended July 31, 2024 and 2023, respectively.

General and administrative

expenses. Our general and administrative expenses kept stable at $2.3 million and $2.2 million For the fiscal years ended July

31, 2024 and 2023, respectively. Our general and administrative expenses primarily consisted of salary and welfare expenses of management

and administrative team, professional expenses, office expenses, operating lease expenses. The increase in general and administrative

expenses was primarily due to an increase of legal expenses of approximately $0.5 million for legal proceedings with both Boustead Securities,

LLC and J.P Morgan Securities LLC, partially offset by a decrease of approximately $0.2 million in rental expenses because we modified

an office lease agreement, a decrease of approximately $0.1 million in payroll expenses because we adjusted monthly payroll expenses to

Mr. Jun Liu from $20,000 to $1 since February 2024, and a decrease of approximately $0.1 million in office expenses.

As a percentage of sales,

our general and administrative expenses were 365% and 91% of our total revenues for the fiscal years ended July 31, 2024 and 2023, respectively.

(Reversal of provision)

provision against accounts receivable due from a related party. For the fiscal year ended July 31, 2023, we provided full provision

of $762,000 against the accounts receivable due from Huaya as the management assessed it is remote to collect the outstanding balance.

For the fiscal year ended July 31, 2024, we reversed provision of $19,103 because Huaya paid salary expenses of $19,103 on our behalf.

Provision against due

from buyers of LGC. For the fiscal year ended July 31, 2023, we provided full provision of $2,654,767 against the balances due

from buyers of LGC as the management assessed it is remote to collect the outstanding balance. The balance due from buyers of LGC arose

from our disposition of 51.2% of the equity interest of LGC in January 2021. We did not incur such expenses for the fiscal year ended

July 31, 2024.

Loss (gain) from investment

in trading securities. Loss (gains) from investment in trading securities represented fair value changes from investment in trading

securities, which was measured at market price. For the fiscal years ended July 31, 2024 and 2023, we recorded an investment loss of approximately

$0.4 million and an investment gain of approximately $0.2 million, respectively.

Income taxes.

We are incorporated in the British Virgin Islands. Under the current laws of the British Virgin Islands, we are not subject to tax on

income or capital gains in the British Virgin Islands. Additionally, upon payments of dividends to the shareholders, no British Virgin

Islands withholding tax will be imposed.

ATIF Inc, ATIF BD, ATIF BC

and ATIF BM were established in the U.S and are subject to federal and state income taxes on its business operations. The federal tax

rate is 21% and state tax rate is 8.84%. We also evaluated the impact from the recent tax reforms in the United States, including the

Coronavirus Aid, Relief, and Economic Security Act (“CARES Act”) and Health and Economic Recovery Omnibus Emergency Solutions

Act (“HERO Act”), which were both passed in 2020, No material impact on the ATIF US is expected based on our analysis. We

will continue to monitor the potential impact going forward.

Income tax expense was $3,300

for the fiscal years ended July 31, 2024, because three of our US subsidiaries are subject to state taxes during the year of 2024. Income

tax expense was $31,200 for the fiscal years ended July 31, 2023, because our USA subsidiaries were making taxable income during the year

of 2023.

Net loss. As

a result of foregoing, net loss was approximately $3.2 million for the fiscal year ended July 31, 2024, an increase of $0.3 million from

net loss of $2.9 million in fiscal year 2023.

Liquidity and Capital Resources

To date, we have financed

our operations primarily through cash flows from operations, working capital loans from our major shareholders, proceeds from our initial

public offering, and equity financing through public offerings of our securities. We plan to support our future operations primarily from

cash generated from our operations and cash on hand. However, the Company may need to raise the cash flow from related parties, and there

is no assurance that the Company will be able to obtain funds on commercially acceptable terms, if at all.

Liquidity and Going concern

For the years ended July 31,

2024 and 2023, the Company reported a net loss of approximately $3.2 million and $2.9 million, respectively, and operating cash outflows

approximately $0.1 million and $2.3 million. In assessing the Company’s ability to continue as a going concern, the Company monitors

and analyzes its cash and its ability to generate sufficient cash flow in the future to support its operating and capital expenditure

commitments. Because of losses from operations, cash out from operating activities, and the requirement of additional capital to fund

our current operating plan at July 31, 2024, these factors indicate the existence of an uncertainty that raises substantial doubt about

the Company’s ability to continue as a going concern.

As of July 31, 2024, the Company

had cash of $1.2 million, short-term investment in trading securities of $0.4 million, due from a related party of $0.9 million and accounts

receivables of $0.2 million due from a related party, which were highly liquid. On the other hand, the Company had current liabilities

of $1.0 million. The Company’s cash on hand could well cover the current liabilities. The Company’s ability to continue as

a going concern is dependent on management’s ability to successfully execute its business plan, which includes increasing revenue

while controlling operating cost and expenses to generate positive operating cash flows and obtain financing from outside sources.

The consolidated financial

statements have been prepared on a going concern basis, which contemplates the realization of assets and satisfaction of liabilities in

the ordinary course of business. The financial statements do not include any adjustments relating to the recoverability and classification

of recorded asset amounts or the amounts and classification of liabilities that might result from the outcome of the uncertainties described

above.

We have not declared nor paid

any cash dividends to our shareholders. We do not plan to pay any dividends out of our restricted net assets as of July 31, 2024.

The following table sets forth summary of our cash

flows for the years indicated:

| | |

For the Years Ended

July 31, | |

| | |

2024 | | |

2023 | |

| Net cash used in operating activities | |

| (120,483 | ) | |

| (2,333,899 | ) |

| Net cash (used in) provided by investing activities | |

| (1,579,955 | ) | |

| 459,816 | |

| Net cash provided by financing activities | |

| 2,343,792 | | |

| 729,968 | |

| Net increase (decrease) in cash | |

| 643,354 | | |

| (1,144,115 | ) |

| Cash, beginning of year | |

| 606,022 | | |

| 1,750,137 | |

| Cash, end of year | |

$ | 1,249,376 | | |

$ | 606,022 | |

Operating Activities

Net cash used in operating

activities was approximately $0.1 million in fiscal year ended July 31, 2024. Net cash used in operating activities was primarily comprised

of net loss of approximately $3.2 million, adjusted for loss of approximately $0.4 million from investment in trading securities, and

net changes in our operating assets and liabilities, principally comprising of (i) a decrease of accounts receivable of approximately

$0.7 million due from third parties and $0.4 million due from a related party, respectively. The decrease was because we collected outstanding

balance due from customers, (ii) a decrease of prepaid expenses and other current assets of approximately $0.3 million, which was due

to amortization of advertising service fees, and (iii) an increase of accrued expenses and other current liabilities of approximately

$1.3 million.

Net cash used in operating

activities was approximately $2.3 million in fiscal year ended July 31, 2023. Net cash used in operating activities was primarily comprised

of net loss of approximately $2.9 million, adjusted for provision of approximately $2.7 million against due from buyers of LGC, and provision

of approximately $0.8 million against accounts receivable due from a related party, and net changes in our operating assets and liabilities,

principally comprising of (i) an increase of accounts receivable of approximately $0.7 million due from third parties and approximately

$0.6 million due from a related party, respectively. The increase was in line with increase of revenues, and (ii) a decrease of accrued

expenses and other current liabilities of approximately $2.0 million as the Company was no longer liable to an investment bank for loss

making since disposal of ATIF GP.

Investing Activities

Net cash used in investing

activities was approximately $1.6 million in fiscal year 2024, primarily consisting of loans of approximately $0.9 million made to a related

party and investment of approximately $0.7 million in trading securities.

Net cash provided by investing

activities was approximately $0.4 million in fiscal year 2023, primarily consisting of proceeds of approximately $0.3 million from disposal

of investments in two equity securities, redemption of $94,799 from short-term investments, proceeds of $72,000 from disposal of property

and equipment, and collection of loans of $59,000 from a related party, partially offset against loans of approximately $0.1 million made

to a related party.

Financing Activities

Net cash provided by financing

activities was approximately $2.3 million in fiscal year 2024, which was provided by proceeds of approximately $2.3 million from issuance

of ordinary shares pursuant to a private placement

Net cash provided by financing

activities was approximately $0.7 million in fiscal year 2023, which was provided by borrowings of approximately $0.7 million from a related

party.

Critical Accounting Policies and Estimate

We prepare our audited consolidated

financial statements in accordance with U.S. GAAP, which requires our management to make estimates that affect the reported amounts of

assets, liabilities and disclosures of contingent assets and liabilities at the balance sheet dates, as well as the reported amounts of

revenues and expenses during the reporting periods. As a result, management is required to routinely make judgments and estimates about

the effects of matters that are inherently uncertain. Actual results may differ from these estimates under different conditions or assumptions.

Critical accounting policy

is both material to the presentation of financial statements and requires management to make difficult, subjective or complex judgments

that could have a material effect on financial condition or results of operations. Accounting estimates and assumptions may become critical

when they are material due to the levels of subjectivity and judgment necessary to account for highly uncertain matters or the susceptibility

of such matters to change, and that have a material impact on financial condition or operating performance.

Critical accounting estimates

are estimates that require us to make assumptions about matters that were highly uncertain at the time the accounting estimate were made

and if different estimates that we reasonably could have used in the current period, or changes in the accounting estimate that are reasonably

likely occur from period to period, have a material impact on the presentation of our financial condition, changes in financial condition

or results of operations. Due to the level of activity and lack of complex transactions, we believe there are currently no critical accounting

policies and estimates that affect the preparation of our financial statements.

Results of Operations for the Three

and Six Months Ended January 31, 2025 and 2024

Comparison of Operation Results

for the Three Months ended January 31, 2025 and 2024

The following table summarizes

the results of our operations for the three months ended January 31, 2025 and 2024, respectively, and provides information regarding

the dollar and percentage increase or (decrease) during such periods.

| | |

For the three months ended

January 31, | | |

Changes | |

| | |

2025 | | |

2024 | | |

Amount

Increase

(Decrease) | | |

Percentage Increase (Decrease) | |

| | |

| | |

| | |

| | |

| |

| Revenues | |

| 200,000 | | |

| 25,000 | | |

| 175,000 | | |

| 700 | % |

| | |

| | | |

| | | |

| | | |

| | |

| Operating expenses | |

| | | |

| | | |

| | | |

| | |

| Selling expenses | |

| (48,000 | ) | |

| (93,000 | ) | |

| 45,000 | | |

| (48 | )% |

| General and administrative expenses | |

| (502,797 | ) | |

| (479,516 | ) | |

| (23,281 | ) | |

| 5 | % |

| Total operating expenses | |

| (550,797 | ) | |

| (572,516 | ) | |

| 21,719 | | |

| (4 | )% |

| | |

| | | |

| | | |

| | | |

| | |

| Loss from operations | |

| (350,797 | ) | |

| (547,516 | ) | |

| 196,719 | | |

| (36 | )% |

| | |

| | | |

| | | |

| | | |

| | |

| Other (expenses) income | |

| | | |

| | | |

| | | |

| | |

| Interest (expenses) income | |

| 3 | | |

| 23 | | |

| (20 | ) | |

| (87 | )% |

| Other (expense) income | |

| (265,941 | ) | |

| 59,185 | | |

| (325,126 | ) | |

| (549 | )% |

| (Loss) gain from investment in trading securities | |

| (1,286,722 | ) | |

| 80,670 | | |

| (1,367,392 | ) | |

| (1695 | )% |

| Total other (expense) income | |

| (1,552,660 | ) | |

| 139,878 | | |

| (1,692,538 | ) | |

| (1210 | )% |

| | |

| | | |

| | | |

| | | |

| | |

| Loss before income taxes | |

| (1,903,457 | ) | |

| (407,638 | ) | |

| (1,495,819 | ) | |

| 367 | % |

| | |

| | | |

| | | |

| | | |

| | |

| Income tax expenses | |

| - | | |

| - | | |

| - | | |

| | |

| Net loss | |

| (1,903,457 | ) | |

| (407,638 | ) | |

| (1,495,819 | ) | |

| 367 | % |

Revenues. Our

total revenue increased by approximately $0.2 million, or 700%, from $25,000 for the three months ended January 31, 2024, to $0.2 million

in for the three months ended January 31, 2025.

For the three months ended

January 31, 2025, we provided IPO assistance services to one customer and recognized revenues of $0.2 million. For the three months ended

January 31, 2024, we provided IPO assistance services to one customer and recognized revenues of $25,000.

Selling expenses. Our

selling expenses primarily consisted of advertising and promotion expenses. For the three months ended January 31, 2025, our selling

expenses was $48,000, representing a decrease of $45,000, or 48%, from $93,000 for the three months ended January 31, 2024. The decrease

was primarily due to a decrease of amortization expenses of $45,000 for TV promotion videos.

General and administrative

expenses. Our general and administrative expenses primarily consisted of salary and welfare expenses of management and administrative

team, professional expenses, office expenses, operating lease expenses. Our general and administrative expenses increased by $23,281,

or 5%, from approximately $0.5 million for the three months ended January 31, 2024, to $0.5 million for the three months ended January

31, 2025.

Loss (gain) from investment

in trading securities. Loss (gain) from investment in trading securities represented fair value changes from investment

in trading securities, which was measured at market price. For the three months ended January 31, 2025 and 2024, we recorded an investment

loss of approximately $1.3 million and an investment gain of approximately $0.1 million, respectively.

Income taxes. We

are incorporated in the British Virgin Islands. Under the current laws of the British Virgin Islands, we are not subject to tax on income

or capital gains in the British Virgin Islands. Additionally, upon payments of dividends to the shareholders, no British Virgin Islands

withholding tax will be imposed.

ATIF Inc, ATIF BD, ATIF

BC and ATIF BM were established in the U.S and are subject to federal and state income taxes on their business operations. The federal

tax rate is 21% and state tax rate is 8.84%. ATIF BD, a corporation registered in Delaware is subject to a franchise tax. We also evaluated

the impact from the recent tax reforms in the United States, including the Coronavirus Aid, Relief, and Economic Security Act (“CARES

Act”) and Health and Economic Recovery Omnibus Emergency Solutions Act (“HERO Act”), which were both passed in 2020,

No material impact on the ATIF US is expected based on our analysis. We will continue to monitor the potential impact going forward.

For the three months ended

January 31, 2025 and 2024, we did not recognize income tax expenses.

Net income (loss). As

a result of foregoing, net loss was approximately $1.9 million for the three months ended January 31, 2025, an increase of loss of approximately

$1.5 million from net loss of $0.4 million for the three months ended January 31, 2024.

Comparison of Operation

Results for the Six Months ended January 31, 2025 and 2024

The following table summarizes

the results of our operations for the six months ended January 31, 2025 and 2024, respectively, and provides information regarding the

dollar and percentage increase or (decrease) during such periods.

| | |

For the six months ended

January

31, | | |

Changes | |

| | |

2025 | | |

2024 | | |

Amount

Increase

(Decrease) | | |

Percentage

Increase

(Decrease) | |

| | |

| | |

| | |

| | |

| |

| Revenues | |

| 200,000 | | |

| 150,000 | | |

| 50,000 | | |

| 33 | % |

| | |

| | | |

| | | |

| | | |

| | |

| Operating expenses | |

| | | |

| | | |

| | | |

| | |

| Selling expenses | |

| (120,000 | ) | |

| (165,000 | ) | |

| 45,000 | | |

| (27 | )% |

| General and administrative expenses | |

| (951,906 | ) | |

| (1,189,295 | ) | |

| 237,389 | | |

| (20 | )% |

| Total operating expenses | |

| (1,071,906 | ) | |

| (1,354,295 | ) | |

| 282,389 | | |

| (21 | )% |

| | |

| | | |

| | | |

| | | |

| | |

| Loss from operations | |

| (871,906 | ) | |

| (1,204,295 | ) | |

| 332,389 | | |

| (28 | )% |

| | |

| | | |

| | | |

| | | |

| | |

| Other income (expenses) | |

| | | |

| | | |

| | | |

| | |

| Interest (expenses) income | |

| (15 | ) | |

| 23 | | |

| (38 | ) | |

| (165 | )% |

| Other (expense) income | |

| (260,046 | ) | |

| 199,905 | | |

| (459,951 | ) | |

| (230 | )% |

| Loss from investment in trading securities | |

| (1,138,564 | ) | |

| (28,734 | ) | |

| (1,109,830 | ) | |

| 3862 | % |

| Total other (expense) income | |

| (1,398,625 | ) | |

| 171,194 | | |

| (1,569,819 | ) | |

| (917 | )% |

| | |

| | | |

| | | |

| | | |

| | |

| Loss before income taxes | |

| (2,270,531 | ) | |

| (1,033,101 | ) | |

| (1,237,430 | ) | |

| 120 | % |

| | |

| | | |

| | | |

| | | |

| | |

| Income tax expenses | |

| - | | |

| - | | |

| - | | |

| | |

| Net loss | |

| (2,270,531 | ) | |

| (1,033,101 | ) | |

| (1,237,430 | ) | |

| 120 | % |

Revenues. Our

total revenue increased by $50,000 from approximately $0.2 million for the six months ended January 31, 2024, to $0.2 million in six