As filed with the Securities and Exchange Commission on May 4, 2023

Securities Act File No. 033-52742

Investment Company Act File No. 811-07238

FORM N-1A

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

|

|

|

|

|

|

|

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 |

|

☒ |

|

|

|

|

|

Pre-Effective

Amendment No. |

|

☐ |

|

|

|

|

|

Post-Effective Amendment No. 130 |

|

☒ |

|

|

|

|

|

|

and/or

REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 |

|

☒ |

|

|

|

|

|

Amendment No. 131 |

|

☒ |

SUNAMERICA SERIES TRUST

(Exact Name of Registrant as Specified in Charter)

21650 Oxnard Street, 10th Floor

Woodland Hills, California 91367

(Address of Principal Executive Offices) (Zip Code)

(800-858-8850)

(Registrant’s Telephone Number, including area code)

Kathleen D. Fuentes, Esq.

SunAmerica Asset Management, LLC

Harborside 5

185 Hudson

Street, Suite 3300

Jersey City, NJ 07311

(Name and Address for Agent for Service)

Copy to:

Trina Sandoval, Esq.

Corebridge Life & Retirement

21650 Oxnard Street, 10th Floor

Woodland Hills, California 91367

Margery K. Neale, Esq.

Willkie Farr & Gallagher LLP

787 Seventh Avenue

New

York, New York 10019

Approximate Date of Proposed Public Offering: As soon as practicable after this Registration Statement becomes

effective.

It is proposed that this filing will become effective (check appropriate box):

☐ Immediately upon filing pursuant to paragraph (b) of Rule 485

☐ on (date), pursuant to paragraph (b) of Rule 485

☐ 60 days after filing pursuant to paragraph (a)(1)

☒ on July 5, 2023, pursuant to paragraph (a)(1)

☐ 75 days after filing pursuant to paragraph (a)(2)

☐ on (date), pursuant to paragraph (a)(2) of Rule 485

If appropriate, check the following box:

☐ This post-effective amendment designates a new effective date for a previously filed post-effective amendment.

Title of Securities Being Registered: Shares of beneficial interest, no par value.

This filing relates solely to SA Invesco Main Street Large Cap Portfolio.

The information in this Prospectus is not complete and may be changed. We

may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This Prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any

jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MAY 4, 2023

PROSPECTUS

[ ], 2023

SUNAMERICA SERIES TRUST

(Class 1, Class 2 and Class 3 Shares)

SA JPMorgan Large Cap Core Portfolio (formerly, SA Invesco Main Street Large Cap Portfolio)

This Prospectus contains information you should know before investing, including information about risks. Please read it before you invest and

keep it for future reference.

The Securities and Exchange Commission has not approved or disapproved these securities or passed upon the

adequacy of this Prospectus. Any representation to the contrary is a criminal offense.

TABLE OF CONTENTS

i

|

PORTFOLIO SUMMARY: SA JPMORGAN LARGE CAP CORE PORTFOLIO

(FORMERLY, SA

INVESCO MAIN STREET LARGE CAP PORTFOLIO) |

Investment Goal

The Portfolio’s investment

goal is long term capital appreciation.

Fees and Expenses of the Portfolio

This table describes the fees and

expenses that you may pay if you buy, hold and sell shares of the Portfolio. The table and the example below do not reflect the separate account fees charged in the variable annuity or variable life insurance policy (“Variable

Contracts”) in which the Portfolio is offered. If separate account fees were shown, the Portfolio’s annual operating expenses would be higher. Please see your Variable Contract prospectus for more details on the separate account fees.

Annual Portfolio Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Class 1 |

|

|

Class 2 |

|

|

Class 3 |

|

| Management Fees |

|

|

[ |

]% |

|

|

[ |

]% |

|

|

[ |

]% |

| Service (12b-1) Fees |

|

|

[ |

]% |

|

|

[ |

]% |

|

|

[ |

]% |

| Other Expenses |

|

|

[ |

]% |

|

|

[ |

]% |

|

|

[ |

]% |

| Total Annual Portfolio Operating Expenses Before Fee Waivers and/or Expense Reimbursements |

|

|

[ |

]% |

|

|

[ |

]% |

|

|

[ |

]% |

| Fee Waivers and/or Expense Reimbursements1 |

|

|

[ |

]% |

|

|

[ |

]% |

|

|

[ |

]% |

| Total Annual Portfolio Operating Expenses After Fee Waivers and/or Expense Reimbursements1 |

|

|

[ |

]% |

|

|

[ |

]% |

|

|

[ |

]% |

| 1 |

Pursuant to an Advisory Fee Waiver Agreement, effective through April 30, 2025, SunAmerica Asset Management,

LLC (“SunAmerica”) is contractually obligated to waive a portion of its advisory fee on an annual basis with respect to the Portfolio so that the advisory fee rate payable by the Portfolio to SunAmerica is equal to 0.73% of the

Portfolio’s average daily net assets on the first $50 million, 0.68% of the Portfolio’s average daily net assets on the next $200 million and 0.63% of the Portfolio’s average daily net assets over $250 million.

SunAmerica may not recoup any advisory fees waived with respect to the Portfolio pursuant to the Advisory Fee Waiver Agreement. This agreement may be modified or discontinued prior to April 30, 2025 only with the approval of the Board of Trustees of

SunAmerica Series Trust (the “Trust”), including a majority of the trustees who are not “interested persons” of the Trust as defined in the Investment Company Act of 1940, as amended.

|

Expense Example

This Example is intended to help you compare the cost of investing in the Portfolio with the cost of investing in other mutual funds. The

Example assumes that you invest $10,000 in the Portfolio for the time periods indicated and then redeem or hold all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the

Portfolio’s operating expenses remain the same and that all contractual expense limitations and fee waivers remain in effect only for the period ending April 30, 2025. The Example does not reflect charges imposed by the Variable Contract.

If the Variable Contract fees were reflected, the expenses would be higher. See the Variable Contract prospectus for information on such charges. Although your actual costs may be higher or lower, based on these assumptions and the net expenses

shown in the fee table, your costs would be:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

1 Year |

|

|

3 Years |

|

|

5 Years |

|

|

10 Years |

|

| Class 1 |

|

$ |

[ |

] |

|

$ |

[ |

] |

|

$ |

[ |

] |

|

$ |

[ |

] |

| Class 2 |

|

$ |

[ |

] |

|

$ |

[ |

] |

|

$ |

[ |

] |

|

$ |

[ |

] |

| Class 3 |

|

$ |

[ |

] |

|

$ |

[ |

] |

|

$ |

[ |

] |

|

$ |

[ |

] |

Portfolio Turnover

The Portfolio pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A

higher portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in annual portfolio operating expenses or in the Example, affect the Portfolio’s performance.

During the most recent fiscal year, the Portfolio’s portfolio turnover rate was 62% of the average value of its portfolio.

Principal Investment Strategies of the Portfolio

The Portfolio attempts to achieve

its goal by investing, under normal circumstances, at least 80% of its net assets in large capitalization companies. Large capitalization companies are those with market capitalizations similar to companies in the Russell 1000® Index (the “Index”). As of February 28, 2023, the median market capitalization of a company in the Index was

- 1 -

|

| PORTFOLIO SUMMARY: SA JPMORGAN LARGE CAP CORE

PORTFOLIO

(FORMERLY, SA INVESCO MAIN STREET LARGE

CAP PORTFOLIO) |

approximately $12.653 billion and the dollar-weighted average market capitalization of the companies in the Index was approximately $421.385 billion. The Portfolio intends to invest in

equity investments selected for their potential to achieve capital appreciation over the long-term. The Portfolio generally invests in common stocks of U.S. companies and may invest in companies of any market capitalization range.

The Portfolio focuses on those equity securities that it considers attractively valued and seeks to outperform its benchmark through superior

stock selection. By emphasizing attractively valued equity securities, the Portfolio seeks to produce returns that exceed those of its benchmark. The Portfolio may also invest in equity securities that the subadviser believes have above-average

growth potential.

In managing the Portfolio, the subadviser employs a three-step process that combines research, valuation and stock

selection. The subadviser takes an in-depth look at company prospects, which is designed to provide insight into a company’s real growth potential. The research findings allow the subadviser to rank the

companies in each sector group according to their relative value. As part of its investment process, the subadviser seeks to assess the impact of environmental, social and governance (ESG) factors on many issuers in the universe in which the

Portfolio invests. The subadviser’s assessment is based on an analysis of key opportunities and risks across industries to seek to identify financially material issues with respect to the Portfolio’s investments in securities and ascertain

key issues that merit engagement with issuers. These assessments may not be conclusive and securities of issuers may be purchased and retained by the Portfolio for reasons other than material ESG factors while the Portfolio may divest or not invest

in securities of issuers that may be positively impacted by such factors.

On behalf of the Portfolio, the subadviser then buys and sells

equity securities, using the research and valuation rankings as a basis. In general, the subadviser buys equity securities that are identified as attractively valued and considers selling them when they appear to be overvalued. Along with attractive

valuation, the subadviser often considers a number of other criteria:

| |

• |

|

catalysts that could trigger a rise in a stock’s price; |

| |

• |

|

high potential reward compared to potential risk; and |

| |

• |

|

temporary mispricings caused by apparent market over-reactions. |

Principal Risks of Investing in the Portfolio

As with any mutual fund, there can

be no assurance that the Portfolio’s investment goal will be met or that the net return on an investment in the Portfolio will exceed what could have been obtained through other investment or savings vehicles. Shares of the Portfolio are not

bank deposits and are not guaranteed or insured by any bank, government entity or the Federal Deposit Insurance Corporation. If the value of the assets of the Portfolio goes down, you could lose money.

The following is a summary of the principal risks of investing in the Portfolio.

Equity Securities Risk. The Portfolio invests principally in equity securities and is therefore subject to the risk that stock prices

will fall and may underperform other asset classes. Individual stock prices fluctuate from day-to-day and may decline significantly.

Large-Cap Companies Risk. Large-cap companies

tend to be less volatile than companies with smaller market capitalizations. In exchange for this potentially lower risk, the Portfolio’s value may not rise as much as the value of portfolios that emphasize smaller companies. Larger, more

established companies may be unable to respond quickly to new competitive challenges, such as changes in technology and consumer tastes. Larger companies also may not be able to attain the high growth rate of successful smaller companies,

particularly during extended periods of economic expansion.

Mid-Cap Companies Risk.

Securities of mid-cap companies are usually more volatile and entail greater risks than securities of large companies.

Value Investing Risk. The subadviser’s judgment that a particular security is undervalued in relation to the company’s

fundamental economic value may prove incorrect.

Growth Stock Risk. Growth stocks may lack the dividend yield associated with value

stocks that can cushion total return in a bear market. Also, growth stocks normally carry a higher price/earnings ratio than many other stocks. Consequently, if earnings expectations are not met, the market price of growth stocks will often decline

more than other stocks.

Sector or Industry Focus Risk. To the extent the Portfolio invests a significant portion of its assets in

one or more sectors or industries at a time, the Portfolio will face a greater risk of loss due to factors affecting sectors or industries than if the Portfolio always maintained wide diversity among the sectors and industries in which it invests.

Issuer Risk. The value of a security may decline for a number of reasons directly related to the issuer, such as management

performance, financial leverage and reduced demand for the issuer’s goods and services.

Market Risk. The Portfolio’s

share price can fall because of weakness in the broad market, a particular industry, or

- 2 -

|

| PORTFOLIO SUMMARY: SA JPMORGAN LARGE CAP CORE

PORTFOLIO

(FORMERLY, SA INVESCO MAIN STREET LARGE

CAP PORTFOLIO) |

specific holdings. The market as a whole can decline for many reasons, including adverse political or economic developments in the United States or abroad, changes in investor psychology, or

heavy institutional selling and other conditions or events (including, for example, military confrontations, war, terrorism, sanctions, disease/virus, outbreaks and epidemics). In addition, the subadviser’s assessment of securities held in the

Portfolio may prove incorrect, resulting in losses or poor performance even in a rising market.

The coronavirus (COVID-19) pandemic and the related governmental and public responses have had and may continue to have an impact on the Portfolio’s investments and net asset value and have led and may continue to lead to

increased market volatility and the potential for illiquidity in certain classes of securities and sectors of the market. Preventative or protective actions that governments may take in respect of pandemic or epidemic diseases may result in periods

of business disruption, business closures, inability to obtain raw materials, supplies and component parts, and reduced or disrupted operations for the issuers in which the Portfolio invests. Government intervention in markets may impact interest

rates, market volatility and security pricing. The occurrence, reoccurrence and pendency of such diseases could adversely affect the economies (including through changes in business activity and increased unemployment) and financial markets either

in specific countries or worldwide.

Management Risk. The Portfolio is subject to management risk because it is an actively-managed

investment portfolio. The Portfolio’s portfolio managers apply investment techniques and risk analyses in making investment decisions, but there can be no guarantee that these decisions or the individual securities selected by the portfolio

managers will produce the desired results.

Affiliated Fund Rebalancing Risk. The Portfolio may be an investment option for other

mutual funds for which SunAmerica serves as investment adviser that are managed as “funds of funds.” From time to time, the Portfolio may experience relatively large redemptions or investments due to the rebalancing of a fund of funds. In

the event of such redemptions or investments, the Portfolio could be required to sell securities or to invest cash at a time when it is not advantageous to do so.

Performance Information

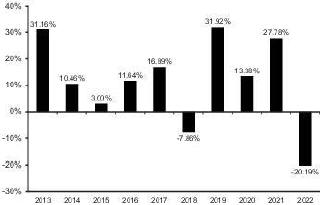

The following bar chart illustrates the risks of investing in the Portfolio by showing changes in the Portfolio’s performance from

calendar year to calendar year and the table compares the Portfolio’s average annual returns to those of the S&P 500® Index and the Russell 1000® Index. Effective [ ], 2023, the S&P 500® Index replaced the

Russell 1000® Index as the performance benchmark against which the Portfolio measures its performance.

Portfolio management believes that the S&P 500® Index is more representative of the securities in which the Portfolio invests. The

Portfolio’s returns prior to [ ], 2023, as reflected in the bar chart and table, are the returns of the Portfolio when it followed different investment strategies under the

name “SA Invesco Main Street Large Cap Portfolio.” Fees and expenses incurred at the contract level are not reflected in the bar chart or table. If these amounts were reflected, returns would be less than those shown. Of course, past

performance is not necessarily an indication of how the Portfolio will perform in the future.

Effective

[ ], 2023, J.P. Morgan Investment Management, Inc. (“JPMorgan”) assumed subadvisory duties of the Portfolio. Prior to

[ ], 2023, Invesco Advisers, Inc. served as subadviser.

(Class 1

Shares)

During the period shown in the bar chart:

|

|

|

|

|

|

|

| Highest Quarterly Return: |

|

June 30, 2020 |

|

|

18.12 |

% |

| Lowest Quarterly Return: |

|

March 31, 2020 |

|

|

-20.48 |

% |

| Year to Date Most Recent Quarter: |

|

[ ] |

|

|

[ |

]% |

Average Annual Total Returns (For the periods ended December 31, 2022)

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

1 Year |

|

|

5 Years |

|

|

10 Years |

|

| Class 1 Shares |

|

|

-20.19 |

% |

|

|

7.04 |

% |

|

|

10.59 |

% |

| Class 2 Shares |

|

|

-20.27 |

% |

|

|

6.90 |

% |

|

|

10.43 |

% |

| Class 3 Shares |

|

|

-20.39 |

% |

|

|

6.78 |

% |

|

|

10.32 |

% |

| S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

-18.11 |

% |

|

|

9.42 |

% |

|

|

12.56 |

% |

| Russell 1000® Index (reflects no deduction for fees, expenses or taxes) |

|

|

-19.13 |

% |

|

|

9.13 |

% |

|

|

12.37 |

% |

- 3 -

|

| PORTFOLIO SUMMARY: SA JPMORGAN LARGE CAP CORE

PORTFOLIO

(FORMERLY, SA INVESCO MAIN STREET LARGE

CAP PORTFOLIO) |

Investment Adviser

The Portfolio’s investment

adviser is SunAmerica.

The Portfolio is subadvised by JPMorgan.

Portfolio Managers

|

|

|

| Name and Title |

|

Portfolio

Manager of the

Portfolio Since |

| Scott Davis

Managing Director and Portfolio Manager |

|

2023 |

| Shilpee Raina

Executive Director and Portfolio Manager |

|

2023 |

| David Small

Managing Director and Portfolio Manager |

|

2023 |

Purchases and Sales of Portfolio Shares

Shares of the Portfolio may only be

purchased or redeemed through Variable Contracts offered by the separate accounts of participating life insurance companies and by other portfolios of the Trust and Seasons Series Trust. Shares of the Portfolio may be purchased and redeemed each day

the New York Stock Exchange is open, at the Portfolio’s net asset value determined after receipt of a request in good order.

The

Portfolio does not have any initial or subsequent investment minimums. However, your insurance company may impose investment or account minimums.

Please consult the prospectus (or other offering document) for your Variable Contract which may contain additional information about purchases and redemptions of Portfolio shares.

Tax Information

The Portfolio will not be subject to U.S. federal income tax so long as it qualifies as a regulated investment company and distributes its

income and gains each year to its shareholders. However, contract holders may be subject to U.S. federal income tax (and a U.S. federal Medicare tax of 3.8% that applies to net investment income, including taxable annuity payments, if applicable)

upon withdrawal from a Variable Contract. Contract holders should consult the prospectus (or other offering document) for the Variable Contract for additional information regarding taxation.

Payments to Broker-Dealers and Other Financial Intermediaries

The Portfolio is not sold directly

to the general public but instead is offered as an underlying investment option for Variable Contracts and to other portfolios of the Trust and Seasons Series Trust. The Portfolio and its related companies may make payments to the sponsoring

insurance company (or its affiliates) for distribution and/or other services. These payments may create a conflict of interest as they may be a factor that the insurance company considers in including the Portfolio as an underlying investment option

in the Variable Contract. The prospectus (or other offering document) for your Variable Contract may contain additional information about these payments.

- 4 -

|

| ADDITIONAL INFORMATION ABOUT THE PORTFOLIO’S INVESTMENT STRATEGIES

AND INVESTMENT RISKS |

The Portfolio’s investment objective, principal investment strategies and principal risks

are summarized in the Portfolio Summary and a full description of each is included below. In addition, the Portfolio may from time-to-time invest in other securities and

use other investment techniques, as detailed below. The risks of these non-principal securities and other investment techniques are included in the section “Glossary” below. In addition to the

securities and investment techniques described in this Prospectus, there are other securities and investment techniques in which the Portfolio may invest in limited instances. These other securities and investment techniques are listed in the

relevant Statement of Additional Information of SunAmerica Series Trust (the “Trust”), which you may obtain free of charge (see back cover).

From time to time, the Portfolio may take temporary defensive positions that are inconsistent with its principal investment strategies, in

attempting to respond to adverse market, economic, political, or other conditions. There is no limit on the Portfolio’s investments in money market securities for temporary defensive purposes. If the Portfolio takes such a temporary defensive

position, it may not achieve its investment goal.

Unless otherwise indicated, investment restrictions, including percentage limitations,

apply at the time of purchase under normal market conditions. You should consider your ability to assume the risks involved before investing in the Portfolio through one of the Variable Contracts. Percentage limitations may be calculated based on

the Portfolio’s total or net assets. “Total assets” means net assets plus liabilities (e.g., borrowings). References to “net assets” in the Portfolio Summary take into account any borrowings for investment purposes by

the Portfolio. If not specified as net assets, the percentage is calculated based on total assets.

The principal investment goal and

strategies for the Portfolio are non-fundamental and may be changed by the Board of Trustees (the “Board”) without shareholder approval. Shareholders will be given at least 60 days’ written

notice in advance of any change to the Portfolio’s investment goal or to its investment strategy that requires 80% of its net assets to be invested in certain securities.

SA JPMorgan Large Cap Core Portfolio. The Portfolio attempts to achieve its goal

by investing, under normal circumstances, at least 80% of its net assets in large capitalization companies. Large capitalization companies are those with market capitalizations similar to companies in the Russell 1000® Index (the “Index”). As of February 28, 2023, the median market capitalization of a company in the Index was approximately $12.653 billion and the dollar-weighted average

market capitalization of the companies in the Index was approximately $421.385 billion. The Portfolio intends to invest in equity investments selected for their potential to achieve capital appreciation over the long-term. The Portfolio

generally invests in common stocks of U.S. companies and may invest in companies of any market capitalization range.

The Portfolio

focuses on those equity securities that it considers attractively valued and seeks to outperform its benchmark through superior stock selection. By emphasizing attractively valued equity securities, the Portfolio seeks to produce returns that exceed

those of its benchmark. The Portfolio may also invest in equity securities that the subadviser believes have above-average growth potential.

In managing the Portfolio, the subadviser employs a three-step process that combines research, valuation and stock selection. The subadviser

takes an in-depth look at company prospects, which is designed to provide insight into a company’s real growth potential. The research findings allow the subadviser to rank the companies in each sector

group according to their relative value. The subadviser also integrates financially material environmental, social and governance (ESG) factors as part of the Portfolio’s investment process (ESG Integration). ESG Integration is the systematic

inclusion of ESG issues in investment analysis and investment decisions. As part of its investment process, the subadviser seeks to assess the impact of ESG factors on many issuers in the universe in which the Portfolio invests. The

subadviser’s assessment is based on an analysis of key opportunities and risks across industries to

- 5 -

|

| ADDITIONAL INFORMATION ABOUT THE

PORTFOLIO’S INVESTMENT STRATEGIES AND INVESTMENT RISKS |

seek to identify financially material issues with respect to the Portfolio’s investments in securities and ascertain key issues that merit engagement with issuers. These assessments may not

be conclusive and securities of issuers that may be negatively impacted by such factors may be purchased and retained by the Portfolio while the Portfolio may divest or not invest in securities of issuers that may be positively impacted by such

factors. In particular, ESG Integration does not change the Portfolio’s investment objective, exclude specific types of industries or companies or limit the Portfolio’s investable universe. The Portfolio is not designed for investors who

wish to screen out particular types of companies or investments or are looking for funds that meet specific ESG goals.

On behalf of the

Portfolio, the subadviser then buys and sells equity securities, using the research and valuation rankings as a basis. In general, the subadviser buys equity securities that are identified as attractively valued and considers selling them when they

appear to be overvalued. Along with attractive valuation, the subadviser often considers a number of other criteria:

| |

• |

|

catalysts that could trigger a rise in a stock’s price; |

| |

• |

|

high potential reward compared to potential risk; and |

| |

• |

|

temporary mispricings caused by apparent market over-reactions.

|

In addition, the Portfolio may make short-term investments and may invest in derivatives,

including futures, depositary receipts, registered investment companies (including exchange-traded funds (“ETFs”)), master limited partnerships (“MLPs”), money market instruments, restricted securities and illiquid investments.

The Portfolio may invest up to 20% of its assets in foreign investments. Additional risks that the Portfolio may be subject to are as follows:

| |

• |

|

Depositary Receipts Risk |

| |

• |

|

Foreign Investment Risk |

| |

• |

|

Investment Company Risk |

| |

• |

|

Master Limited Partnership Risk |

| |

• |

|

Unseasoned Companies Risk

|

- 6 -

Risk Terminology

Affiliated Fund Rebalancing

Risk. The Portfolio may be an investment option for other mutual funds for which SunAmerica serves as investment adviser that are managed as “funds of funds.” From time to time, the Portfolio may experience relatively large redemptions

or investments due to the rebalancing of a fund of funds. In the event of such redemptions or investments, the Portfolio could be required to sell securities or to invest cash at a time when it is not advantageous to do so.

Counterparty Risk. Counterparty risk is the risk that a counterparty to a security, loan or derivative held by the Portfolio becomes

bankrupt or otherwise fails to perform its obligations due to financial difficulties. The Portfolio may experience significant delays in obtaining any recovery in a bankruptcy or other reorganization proceeding, and there may be no recovery or

limited recovery in such circumstances.

Sector or Industry Focus Risk. To the extent the Portfolio invests a significant portion

of its assets in one or only a few sectors or industries at a time, the Portfolio will face a greater risk of loss due to factors affecting that single or those few sectors or industries than if the Portfolio always maintained wide diversity among

the sectors and industries in which it invests.

Cybersecurity Risk. Intentional cybersecurity breaches include: unauthorized

access to systems, networks, or devices (such as through “hacking” activity); infection from computer viruses or other malicious software code; and attacks that shut down, disable, slow, or otherwise disrupt operations, business processes,

or website access or functionality. In addition, unintentional incidents can occur, such as the inadvertent release of confidential information (possibly resulting in the violation of applicable privacy laws).

A cybersecurity breach could result in the loss or theft of customer data or funds, the inability to access electronic systems (“denial

of services”), loss or theft of proprietary information or corporate data, physical damage to a computer or network system, or costs associated with system repairs. Such incidents could cause the Portfolio, SunAmerica, a subadviser, or other

service providers to incur regulatory penalties, reputational damage, additional compliance costs, or financial loss. In addition, such incidents could affect issuers in which the Portfolio invests, and thereby cause the Portfolio’s investments

to lose value.

Depositary Receipts Risk. Depositary receipts include American Depositary Receipts

(“ADRs”), European Depositary Receipts (“EDRs”), and Global Depositary Receipts (“GDRs”). ADRs are certificates issued by a U.S. bank or trust company and represent the right to receive securities of a foreign issuer

deposited in a domestic bank or foreign branch of a U.S. bank. EDRs (issued in Europe) and GDRs (issued throughout the world) each evidence a similar ownership arrangement. ADRs in which the Portfolio may invest may be sponsored or unsponsored.

There may be less information available about foreign issuers of unsponsored ADRs. Depositary receipts, such as ADRs and other depositary receipts, including GDRs, EDRs, are generally subject to the same risks as the foreign securities that they

evidence or into which they may be converted. Depositary receipts may or may not be jointly sponsored by the underlying issuer. The issuers of unsponsored depositary receipts are not obligated to disclose information that is considered material in

the United States. Therefore, there may be less information available regarding these issuers and there may not be a correlation between such information and the market value of the depositary receipts. Certain depositary receipts are not listed on

an exchange and therefore are subject to illiquidity risk.

Derivatives Risk. A derivative is any financial instrument whose value

is based on, and determined by, another security, index, rate or benchmark (e.g., stock options, futures, caps, floors, etc.). Futures and options are traded on different exchanges. Forward contracts, swaps, and many different types of

options are regularly traded outside of exchanges by financial institutions in what are termed “over the counter”

- 7 -

markets. Other more specialized derivative instruments, such as structured notes, may be part of a public offering. To the extent a derivative is used to hedge another position in the Portfolio,

the Portfolio will be exposed to the risks associated with hedging described below. To the extent an option, futures contract, swap or other derivative is used to enhance return, rather than as a hedge, the Portfolio will be directly exposed to the

risks of the contract. Unfavorable changes in the value of the underlying security, index, rate or benchmark may cause sudden losses. Gains or losses from the Portfolio’s use of derivatives may be substantially greater than the amount of the

Portfolio’s investment. Certain derivatives have the potential for undefined loss. Derivatives are also associated with various other risks, including market risk, leverage risk, hedging risk, counterparty risk, valuation risk, regulatory risk,

illiquidity risk and interest rate risk. The primary risks associated with the Portfolio’s use of derivatives are market risk and counterparty risk.

Credit Risk. The use of many derivative instruments involves the risk that a loss may be sustained as a result of the failure of

another party to the contract (usually referred to as a “counterparty”) to make required payments or otherwise comply with the contract’s terms. Additionally, credit default swaps could result in losses if the subadviser does not

correctly evaluate the creditworthiness of the company on which the credit default swap is based.

Hedging Risk. A hedge is an

investment made in order to reduce the risk of adverse price movements in a currency or other investment, by taking an offsetting position (often through a derivative instrument, such as an option or forward contract). While hedging strategies can

be very useful and inexpensive ways of reducing risk, they are sometimes ineffective due to unexpected changes in the market. Hedging also involves the risk that changes in the value of the related security will not match those of the instruments

being hedged as expected, in which case any losses on the instruments being hedged may not be reduced. For gross currency hedges, there is an additional risk, to the extent that these transactions create exposure to currencies in which the

Portfolio’s securities are not denominated. Moreover, while hedging can reduce or eliminate losses, it can also reduce or eliminate gains.

Illiquidity Risk. Illiquidity risk exists when a particular derivative instrument is

difficult to purchase or sell. If a derivative transaction is particularly large or if the relevant market is illiquid (as is the case with many privately negotiated derivatives), it may not be possible to initiate a transaction or liquidate a

position at an advantageous time or price.

Lack of Availability Risk. Because the markets for certain derivative instruments

(including markets located in foreign countries) are relatively new and still developing, suitable derivatives transactions may not be available in all circumstances for risk management or other purposes. Upon the expiration of a particular

contract, the subadviser may wish to retain the Portfolio’s position in the derivative instrument by entering into a similar contract, but may be unable to do so if the counterparty to the original contract is unwilling to enter into the new

contract and no other suitable counterparty can be found. There is no assurance that the Portfolio will engage in derivatives transactions at any time or from time to time. The Portfolio’s ability to use derivatives may also be limited by

certain regulatory and tax considerations.

Leverage Risk. Because many derivatives have a leverage component, adverse changes in

the value or level of the underlying asset, reference rate or index can result in a loss substantially greater than the amount invested in the derivative itself. Certain derivatives have the potential for unlimited loss, regardless of the size of

the initial investment. When the Portfolio uses derivatives for leverage, investments in the Portfolio will tend to be more volatile, resulting in larger gains or losses in response to market changes. Pursuant to Rule

18f-4 under the 1940 Act, the Portfolio must either use derivatives in a limited manner or comply with an outer limit on the amount of leverage-related risk that the Portfolio may obtain based on value-at-risk, among other things.

Management Risk.

Derivative products are highly specialized instruments that require investment techniques and risk analysis that in many cases are different from those associated with stocks and bonds. The use of a derivative requires an understanding not only of

the underlying instrument but also of the derivative itself, without the benefit of observing the performance of the derivative under all possible market conditions.

- 8 -

Market and Other Risks. Like most other investments, derivative instruments are subject

to the risk that the market value of the instrument will change in a way detrimental to the Portfolio’s interest. If the subadviser incorrectly forecasts the values of securities, currencies or interest rates or other economic factors in using

derivatives for the Portfolio, the Portfolio might have been in a better position if it had not entered into the transaction at all. While some strategies involving derivative instruments can reduce the risk of loss, they can also reduce the

opportunity for gain or even result in losses by offsetting favorable price movements in other Portfolio investments. The Portfolio may also have to buy or sell a security at a disadvantageous time or price because the Portfolio is legally required

to maintain offsetting positions or asset coverage in connection with certain derivatives transactions.

Other risks in using derivatives

include the risk of mispricing or improper valuation of derivatives and the inability of derivatives to correlate perfectly with underlying assets, rates and indexes. Many derivatives, in particular privately negotiated derivatives, are complex and

often valued subjectively. Improper valuations can result in increased cash payment requirements to counterparties or a loss of value to the Portfolio. Also, the value of derivatives may not correlate perfectly, or at all, with the value of the

assets, reference rates or indexes they are designed to track. For example, a swap agreement on an ETF may not correlate perfectly with the index upon which the ETF is based because the Portfolio’s return is net of fees and expenses.

Futures Risk. Futures are contracts involving the right to receive or the obligation to deliver assets or money depending on the

performance of one or more underlying assets, instruments or a market or economic index. A futures contract is an exchange-traded legal contract to buy or sell a standard quantity and quality of a commodity, financial instrument, index, etc. at a

specified future date and price. A futures contract is considered a derivative because it derives its value from the price of the underlying commodity, security or financial index. The prices of futures contracts can be volatile and futures

contracts may lack liquidity. In addition, there may be imperfect or even negative correlation between the price of a futures contract and the price of the underlying commodity, security or financial index.

Regulatory Risk. Derivative contracts, including, without limitation, futures, swaps and

currency forwards, are subject to regulation under the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank Act”) in the United States and under comparable regimes in Europe, Asia and other

non-U.S. jurisdictions. Under the Dodd-Frank Act, with respect to uncleared swaps, swap dealers are required to collect variation margin from the Portfolio and may be required by applicable regulations to

collect initial margin from the Portfolio. Both initial and variation margin may be comprised of cash and/or securities, subject to applicable regulatory haircuts. Shares of investment companies (other than money market funds) may not be posted as

collateral under these regulations. In addition, regulations adopted by global prudential regulators that are now in effect require certain bank-regulated counterparties and certain of their affiliates to include in certain financial contracts,

including many derivatives contracts, terms that delay or restrict the rights of counterparties, such as the Portfolio, to terminate such contracts, foreclose upon collateral, exercise other default rights or restrict transfers of credit support in

the event that the counterparty and/or its affiliates are subject to certain types of resolution or insolvency proceedings. The implementation of these requirements with respect to derivatives, along with additional regulations under the Dodd-Frank

Act regarding clearing and mandatory trading and trade reporting of derivatives, generally have increased the costs of trading in these instruments and, as a result, may affect returns to investors in the Portfolio.

Tax Risk. The use of certain derivatives may cause the Portfolio to realize higher amounts of ordinary income or short-term capital

gain, to suspend or eliminate holding periods of positions, and/or to defer realized losses, potentially increasing the amount of taxable distributions, and of ordinary income distributions in particular. The Portfolio’s use of derivatives may

be limited by the requirements for taxation of the Portfolio as a regulated investment company. The tax treatment of derivatives may be affected by changes in legislation, regulations or other legal authority that could affect the character, timing

and amount of the Portfolio’s taxable income or gains and distributions to shareholders.

- 9 -

Equity Securities Risk. Equity securities represent an ownership position in a company.

The prices of equity securities fluctuate based on changes in the financial condition of the issuing company and on market and economic conditions. If you own an equity security, you own a part of the company that issued it. Companies sell equity

securities to get the money they need to grow.

Stocks are one type of equity security. Generally, there are three types of stocks:

| |

• |

|

Common stock — Each share of common stock represents a part of the ownership of the company. The

holder of common stock participates in the growth of the company through increasing stock price and receipt of dividends. If the company runs into difficulty, the stock price can decline and dividends may not be paid. |

| |

• |

|

Preferred stock — Each share of preferred stock usually allows the holder to get a set dividend

before the common stock shareholders receive any dividends on their shares. |

| |

• |

|

Convertible preferred stock — A stock with a set dividend which the holder may exchange for a

certain amount of common stock |

Stocks are not the only type of equity security. Other equity securities include but are

not limited to convertible securities, depositary receipts, warrants, rights and partially paid shares, investment company securities, real estate securities, convertible bonds and ADRs, EDRs and GDRs.

Equity securities are subject to the risk that stock prices will fall over short or extended periods of time. Although the stock market has

historically outperformed other asset classes over the long term, the stock market tends to move in cycles. Individual stock prices fluctuate from day-to-day and may

underperform other asset classes over an extended period of time. Individual companies may report poor results or be negatively affected by industry and/or economic trends and developments. The prices of securities issued by such companies may

suffer a decline in response. These price movements may result from factors affecting individual companies, industries or the securities market as a whole. In addition, the

performance of different types of equity securities may rise or decline under varying market conditions — for example, “value” stocks may perform well under circumstances in which

the prices of “growth” stocks in general have fallen, or vice versa.

ESG Investment Risk. The Portfolio’s adherence

to its ESG criteria and application of related analyses when selecting investments may impact the Portfolio’s performance, including relative to similar funds that do not adhere to such criteria or apply such analyses. Additionally, the

Portfolio’s adherence to its ESG criteria and application of related analyses in connection with identifying and selecting investments may require subjective analysis and may be more difficult if data about a particular company or market is

limited, such as with respect to issuers in emerging markets countries. The Portfolio may invest in companies that do not reflect the beliefs and values of any particular investor. Socially responsible norms differ by country and region, and a

company’s ESG practices or the subadviser’s assessment of such may change over time.

Foreign Investment Risk. Foreign

investments are investments of issuers that are economically tied to a non-U.S. country. Except as otherwise described in the Portfolio’s principal investment strategies or as determined by the

Portfolio’s subadviser, the Portfolio will deem an issuer to be economically tied to a non-U.S. country by looking at a number of factors, including the domicile of the issuer’s senior management,

the primary stock exchange on which the issuer’s security trades, the country from which the issuer produced the largest portion of its revenue, and its reporting currency. Foreign Investments include, but are not limited to, securities issued

by foreign governments or their agencies and instrumentalities, foreign corporate and government bonds, foreign equity securities, securities issued by foreign investment companies and passive foreign investment companies, and ADRs or other similar

securities that represent interests in foreign equity securities, such as EDRs and GDRs. The Portfolio’s investments in foreign securities may also include securities from emerging market issuers.

- 10 -

Investments in foreign countries are subject to a number of risks. A principal risk is that

fluctuations in the exchange rates between the U.S. dollar and foreign currencies may negatively affect the value of an investment. In addition, there may be less publicly available information about a foreign company and it may not be subject to

the same uniform accounting, auditing and financial reporting standards as U.S. companies. Foreign governments may not regulate securities markets and companies to the same degree as the U.S. government. Foreign investments will also be affected by

local political or economic developments and governmental actions by the United States or other governments. Consequently, foreign securities may be less liquid, more volatile and more difficult to price than U.S. securities. These risks are

heightened for emerging markets issuers. Historically, the markets of emerging market countries have been more volatile than more developed markets; however, such markets can provide higher rates of return to investors. The Portfolio may also be

subject to the following risks:

Foreign Currency Risk. Currency transactions include the purchase and sale of currencies to

facilitate the settlement of securities transactions and forward currency contracts, which are used to hedge against changes in currency exchange rates or to enhance returns. Portfolios buy foreign currencies when they believe the value of the

currency will increase. If it does increase, they sell the currency for a profit. If it decreases, they will experience a loss. The Portfolio may also buy foreign currencies to pay for foreign securities bought for the Portfolio or for hedging

purposes. Because the Portfolio’s foreign investments are generally held in foreign currencies, the Portfolio could experience gains or losses based solely on changes in the exchange rate between foreign currencies and the U.S. dollar. Such

gains or losses may be substantial.

The Portfolio may not fully benefit from or may lose money on forward currency transactions if

changes in currency exchange rates do not occur as anticipated or do not correspond accurately to changes in the value of the Portfolio’s holdings. The Portfolio’s ability to use forward foreign currency transactions successfully depends

on a number of factors, including the forward foreign currency transactions being available at prices that are not too costly, the availability of liquid markets and the ability of the

Portfolio managers to accurately predict the direction of changes in currency exchange rates. Currency exchange rates may be volatile and may be affected by, among other factors, the general

economics of a country, the actions of U.S. and foreign governments or central banks, the imposition of currency controls and speculation. A security may be denominated in a currency that is different from the currency where the issuer is domiciled.

Currency transactions are subject to counterparty risk, which is the risk that the other party in the transaction will not fulfill its contractual obligation.

The value of the Portfolio’s foreign investments may fluctuate due to changes in currency exchange rates. A decline in the value of

foreign currencies relative to the U.S. dollar generally can be expected to depress the value of the Portfolio’s non-U.S. dollar-denominated securities.

In addition, currency management strategies, to the extent that they reduce the Portfolio’s exposure to currency risks, may also reduce

the Portfolio’s ability to benefit from favorable changes in currency exchange rates. Using currency management strategies for purposes other than hedging further increases the Portfolio’s exposure to foreign investment losses. Currency

markets generally are not as regulated as securities markets. In addition, currency rates may fluctuate significantly over short periods of time, and can reduce returns.

Illiquidity Risk. An illiquid investment is any investment that the Portfolio reasonably expects cannot be sold or disposed of in

current market conditions in seven calendar days or less without the sale or disposition significantly changing the market value of the investment. When there is little or no active trading market for specific types of securities, it can become more

difficult to sell the securities at or near their perceived value. In such a market, the value of such securities and the Portfolio’s share price may fall dramatically. Portfolios that invest in

non-investment grade fixed income securities and emerging market country issuers will be especially subject to the risk that during certain periods, the liquidity of particular issuers or industries, or all

securities within a particular investment category, will shrink or disappear suddenly and without warning as a result of adverse economic, market or political events, or adverse investor perceptions. Derivatives may also be subject to illiquidity

risk.

- 11 -

Investment Company Risk. Registered investment companies are investments by the

Portfolio in other investment companies, including ETFs, which are registered in accordance with the federal securities laws. The risks of the Portfolio owning other investment companies, including ETFs, generally reflect the risks of

owning the underlying securities they are designed to track. Disruptions in the markets for the securities underlying the other investment companies purchased or sold by the Portfolio could result in losses on the Portfolio’s investment in such

securities. Other investment companies also have management fees that increase their costs versus owning the underlying securities directly. See also “ETF Risk.”

Issuer Risk. The value of a security may decline for a number of reasons directly related to the issuer, such as management

performance, financial leverage and reduced demand for the issuer’s goods and services.

Unseasoned Companies Risk.

Unseasoned companies are companies that have operated (together with their predecessors) less than three years. The securities of such companies may have limited liquidity, which can result in their being priced higher or lower than might otherwise

be the case. In addition, investments in unseasoned companies are more speculative and entail greater risk than do investments in companies with established operating records.

Management Risk. The Portfolio is subject to management risk because it is an actively-managed investment portfolio. The

Portfolio’s portfolio managers apply investment techniques and risk analyses in making investment decisions, but there can be no guarantee that these decisions or the individual securities selected by the portfolio managers will produce the

desired results.

Fundamental Analysis is a method of evaluating a security or company by attempting to measure its intrinsic value

by examining related economic, financial and other qualitative and quantitative factors. The factors that the adviser or subadviser may examine include a company’s financial condition (e.g., balance sheet strength, cash flow and

profitability trends), earnings

outlook, strategy, management, and overall economic and market conditions.

Growth Stock Risk. A “Growth” philosophy is a strategy of investing in securities believed to offer the potential for capital

appreciation. It focuses on securities of companies that are considered to have a historical record of above-average growth rate, significant growth potential, above-average earnings growth or value, the ability to sustain earnings growth, or that

offer proven or unusual products or services, or operate in industries experiencing increasing demand. Growth stocks can be volatile for several reasons. Since the issuers of growth stocks usually reinvest a high portion of earnings in their own

business, growth stocks may lack the dividend yield associated with value stocks that can cushion total return in a bear market. Also, growth stocks normally carry a higher price/earnings ratio than many other stocks. Consequently, if earnings

expectations are not met, the market price of growth stocks will often decline more than other stocks. However, the market frequently rewards growth stocks with price increases when expectations are met or exceeded.

Value Investing Risk. A “Value” philosophy is a strategy of investing in securities that are believed to be undervalued in

the market. It often reflects a contrarian approach in that the potential for superior relative performance is believed to be highest when fundamentally solid companies are out of favor. The selection criteria is generally calculated to identify

stocks of companies with solid financial strength that have low price-earnings ratios and have generally been overlooked by the market, or companies undervalued within an industry or market capitalization category. The subadviser’s judgment, or

sub-subadviser’s methodology indication, as applicable, that a particular security is undervalued in relation to the company’s fundamental economic value may prove incorrect.

Market Risk. The Portfolio’s share price can fall because of weakness in the broad market, a particular industry, or specific

holdings. The market as a whole can decline for many reasons, including adverse political or economic developments in the United States or abroad, changes in investor psychology, or heavy institutional selling and other conditions or events

- 12 -

(including, for example, military confrontations, war, terrorism, sanctions, disease/virus, outbreaks and epidemics). The prospects for an industry or company may deteriorate because of a variety

of factors, including disappointing earnings or changes in the competitive environment. In addition, SunAmerica’s or the subadviser’s assessment of securities held in the Portfolio may prove incorrect, resulting in losses or poor

performance even in a rising market. Finally, the Portfolio’s investment approach could fall out of favor with the investing public, resulting in lagging performance versus other comparable portfolios.

The coronavirus (COVID-19) pandemic and the related governmental and public responses have had and may

continue to have an impact on the Portfolio’s investments and net asset value and have led and may continue to lead to increased market volatility and the potential for illiquidity in certain classes of securities and sectors of the market.

Preventative or protective actions that governments may take in respect of pandemic or epidemic diseases may result in periods of business disruption, business closures, inability to obtain raw materials, supplies and component parts, and reduced or

disrupted operations for the issuers in which the Portfolio invests. Government intervention in markets may impact interest rates, market volatility and security pricing. The occurrence, reoccurrence and pendency of such diseases could adversely

affect the economies (including through changes in business activity and increased unemployment) and financial markets either in specific countries or worldwide.

Market Capitalization Risk. Companies are determined to be large-cap companies, mid-cap companies, or small-cap companies based upon the total market value of the outstanding common stock (or similar securities) of the company at the time of purchase. The

market capitalization of the companies in the Portfolio and the indices described below change over time. The Portfolio determines relative market capitalizations using U.S. standards. Accordingly, the Portfolio’s

non-U.S. investments may have large capitalizations relative to market capitalizations of companies based outside the United States. The Portfolio will not automatically sell or cease to purchase stock of a

company that it already owns just because the company’s market capitalization grows or falls outside this range.

Large-Cap Companies Risk. Large-cap companies tend to go in and out of favor based on market and economic conditions. Large-cap companies tend to be less volatile than companies with smaller market

capitalizations. In exchange for this potentially lower risk, the Portfolio’s value may not rise as much as the value of portfolios that emphasize smaller companies. Larger, more established companies may be unable to respond quickly to new

competitive challenges, such as changes in technology and consumer tastes. Larger companies also may not be able to attain the high growth rate of successful smaller companies, particularly during extended periods of economic expansion.

Mid-Cap Companies Risk. The risk that mid-cap

companies, which usually do not have as much financial strength as very large companies, may not be able to do as well in difficult times. Investing in mid-cap companies may be subject to special risks

associated with narrower product lines, more limited financial resources, fewer experienced managers, dependence on a few key employees, and a more limited trading market for their stocks, as compared with larger companies. Securities of mid-cap companies are also subject to the risks of small-cap companies, to a lesser extent.

Master Limited Partnerships (“MLPs”) Risk. MLPs are companies in which ownership interests are publicly traded. MLPs often

own several properties or businesses (or directly own interests) that are related to real estate development and oil and gas industries, but they also may finance motion pictures, research and development and other projects. Generally, a MLP is

operated under the supervision of one or more managing general partners. Limited partners (including the Portfolio if it invests in a MLP) are not involved in the

day-to-day management of the partnership. They are allocated income and capital gains associated with the partnership project in accordance with the terms established in

the partnership agreement. The value of MLPs fluctuate based on prevailing market conditions and the success of the MLP. In addition, unlike owners of common stock of a corporation, owners of common units have limited voting rights and have no

ability to annually elect directors. In the event of liquidation, common units have preference over subordinated units, but not over debt or preferred units, to the remaining assets of the MLP.

- 13 -

About the Indices

Unlike mutual funds, the indices do

not incur expenses. If expenses were deducted, the actual returns of the indices would be lower.

The Russell 1000® Index measures the performance of the 1,000 largest companies in the Russell 3000® Index, which represents approximately 93% of the total market capitalization of the Russell 3000® Index.

The S&P 500®

Index tracks the common stock performance of 500 large-capitalization companies publicly traded in the United States. S&P Style Indices divide the complete market capitalization of each parent index into growth and value segments. The

constituents for the growth and value segments are drawn from the S&P 500® Index. A stock can be in both the growth and value segments.

- 14 -

Information about the Investment Adviser and Manager

SunAmerica serves as investment

adviser and manager for all the portfolios of the Trust. SunAmerica selects the subadvisers for the portfolios, manages the investments for certain portfolios, oversees the subadvisers’ management of certain portfolios, provides various

administrative services and supervises the daily business affairs of each portfolio. SunAmerica is a limited liability company organized under the laws of Delaware, and managed, advised or administered assets in excess of $71.14 billion as of

January 31, 2023. SunAmerica is an indirect, wholly-owned subsidiary of Corebridge Financial, Inc. (“Corebridge”), which is a majority-owned subsidiary of American International Group, Inc. (“AIG”), a U.S.-based

international insurance organization, and is located at Harborside 5, 185 Hudson Street, Suite 3300, Jersey City, New Jersey 07311.

AIG,

the parent of Corebridge, has announced its intention to sell all of its interest in Corebridge over time (such divestment, the “Separation Plan”). On September 19, 2022, AIG sold a portion of its interest in Corebridge in an initial

public offering of Corebridge common stock, following which AIG’s interest in Corebridge is approximately 78%. While AIG and Corebridge believe that Corebridge’s initial public offering did not result in a transfer of a controlling block

of outstanding voting securities of SunAmerica or Corebridge (“a Change of Control Event”), it is anticipated that one or more of the transactions contemplated by the Separation Plan will ultimately be deemed a Change of Control Event

resulting in the assignment and automatic termination of the current investment advisory and management agreement. To ensure that SunAmerica may continue to provide advisory services to the Portfolio without interruption, at a meeting held on

October 13, 2022, the Board approved a new investment advisory and management agreement with SunAmerica, in connection with the Separation Plan. The Board also agreed to call and hold a joint meeting of shareholders on January 19, 2023,

for shareholders of the Portfolio to (1) approve the new investment advisory and management agreement with SunAmerica that would be effective

after the first Change of Control Event, and (2) approve any future investment advisory and management agreements approved by the Board and that have terms not materially different from the

then-current agreement, in the event there are subsequent Change of Control Events arising from completion of the Separation Plan that terminate the investment advisory and management agreement after the first Change of Control Event. Approval of a

future investment advisory and management agreement means that shareholders may not have another opportunity to vote on a new agreement with SunAmerica even upon a change of control, as long as no single person or group of persons acting together

gains “control” (as defined in the 1940 Act) of SunAmerica. At the January 19, 2023 meeting, shareholders of the Portfolio approved the new and future investment advisory and management agreements.

SunAmerica has received an exemptive order from the SEC that permits SunAmerica, subject to certain conditions, to enter into subadvisory

agreements relating to the Portfolio with unaffiliated subadvisers approved by the Board without obtaining shareholder approval. The exemptive order also permits SunAmerica, subject to the approval of the Board but without shareholder approval, to

employ unaffiliated subadvisers for new or existing portfolios, change the terms of subadvisory agreements with unaffiliated subadvisers or continue the employment of existing unaffiliated subadvisers after events that would otherwise cause an

automatic termination of a subadvisory agreement. Shareholders will be notified of any changes that are made pursuant to the exemptive order within 60 days of hiring a new subadviser or making a material change to an existing subadvisory agreement.

The order also permits the Portfolio to disclose fees paid to subadvisers on an aggregate, rather than individual, basis. In addition, pursuant to no-action relief, the SEC staff has extended multi-manager

relief to any affiliated subadviser, provided certain conditions are met. The Portfolio’s shareholders have approved the Portfolio’s reliance on the no-action relief. SunAmerica will determine if and

when the Portfolio should rely on the no-action relief.

SunAmerica may terminate any subadvisory

agreement with a subadviser without shareholder approval.

- 15 -

A discussion regarding the basis for the Board’s approval of the investment advisory

agreement for the Portfolio is available in the Trust’s Annual Report to shareholders for the period ended January 31, 2023. In addition to serving as investment adviser and manager of the Trust, SunAmerica serves as adviser, manager

and/or administrator for the series of each of Seasons Series Trust and VALIC Company I.

Management Fee. For the fiscal year ended

January 31, 2023, the Portfolio paid SunAmerica a fee, before any advisory fee waivers, equal to 0.73% of average daily net assets.

Commission Recapture Program. Through expense offset arrangements resulting from broker commission recapture, a portion of the

Portfolio’s “Other Expenses” have been reduced. The “Other Expenses” shown in the Portfolio’s Annual Portfolio Operating Expenses table in the Portfolio Summary do not take into account this expense reduction and are,

therefore, higher than the actual expenses of the Portfolio. The Portfolio participated in the commission recapture program for the period ended January 31, 2023.

Information about the Subadviser

The investment manager(s) and/or

management team(s) that have primary responsibility for the day-to-day management of the Portfolio are set forth herein. Unless otherwise noted, a management team’s

members share responsibility in making investment decisions on behalf of the Portfolio and no team member is limited in his/her role with respect to the management team.

SunAmerica compensates the subadviser out of the advisory fees that it receives from the Portfolio. SunAmerica may terminate any agreement

with the subadviser without shareholder approval.

A discussion regarding the basis for the Board’s approval of the subadvisory

agreement for the Portfolio will be available in the Trust’s [Semi-]Annual Report to shareholders for the period ending [ ], 2023.

The Statement of Additional Information provides information regarding the portfolio managers

listed in this Prospectus, including other accounts they manage, their ownership interest in the Portfolio, and the structure and method used by the adviser/subadviser to determine their compensation.

J.P. Morgan Investment Management Inc. (JPMorgan) is a Delaware corporation and is an indirect, wholly-owned subsidiary of JPMorgan

Chase & Co. JPMorgan is located at 383 Madison Avenue, New York, NY 10179. JPMorgan provides investment advisory services to a substantial number of institutional and other investors, including other registered investment advisers. As of

December 31, 2022, JPMorgan together with its affiliated companies had approximately $2.36 trillion in assets under management.

The

Portfolio is managed by Scott Davis, David Small and Shilpee Raina.

Mr. Davis has been an employee since 2006 and has been a

portfolio manager since 2013. Previously, he was an analyst in the U.S. Equity Research Group. Mr. Small, an employee since 2005 and a portfolio manager since 2016, was the Associate Director of U.S. Equity Research from July 2015 to July 2016

and is currently the Head of U.S. Equity Research. In addition, Mr. Small previously was the insurance analyst on the Fundamental Research Team from 2008 to 2016. Ms. Raina is a portfolio manager on the Large Cap Core Equity Strategy

within the US Equity Group. An employee since 2005, Ms. Raina was previously a research analyst on the JPMorgan Equity Income and U.S. Value Funds, concentrating on the consumer sectors.

Information about the Distributor

AIG Capital Services, Inc. (the

“Distributor”) distributes the Portfolio’s shares and incurs the expenses of distributing the Portfolio’s shares under a Distribution Agreement with respect to the Portfolio, none of which are reimbursed by or paid for by the

Portfolio. The Distributor is located at Harborside 5, 185 Hudson Street, Suite 3300, Jersey City, NJ 07311.

- 16 -

Custodian, Transfer and Dividend Paying Agent

State Street Bank and Trust

Company, Boston, Massachusetts, acts as Custodian of the Trust’s assets. VALIC Retirement Services

Company is the Trust’s Transfer and Dividend Paying Agent and in so doing performs certain bookkeeping, data processing and administrative services.

- 17 -

Shares of the Portfolio are not offered directly to the public. Instead, shares are currently

issued and redeemed only in connection with investments in and payments under Variable Contracts offered by life insurance companies affiliated with SunAmerica, the Trust’s investment adviser and manager. All shares of the Trust are owned by

“Separate Accounts” of the life insurance companies, certain portfolios of the Trust and certain series of Seasons Series Trust. If you would like to invest in the Portfolio, you must purchase a Variable Contract from one of the life

insurance companies. The Trust offers three classes of shares: Class 1, Class 2 and Class 3 shares. This Prospectus offers all three classes of shares. Certain classes of shares are offered only to existing contract owners and are not

available to new investors. In addition, not all portfolios are available to all contract owners.

You should be aware that the Variable

Contracts involve fees and expenses that are not described in this Prospectus, and that the contracts also may involve certain restrictions and limitations. You will find information about purchasing a Variable Contract and the Portfolio available

to you in the prospectus that offers the Variable Contracts.

The Trust does not foresee a disadvantage to contract owners arising out of

the fact that the Trust offers its shares for Variable Contracts through the various life insurance companies. Nevertheless, the Board intends to monitor events in order to identify any material irreconcilable conflicts that may possibly arise and

to determine what action, if any, should be taken in response. If such a conflict were to occur, one or more insurance company separate accounts might withdraw their investments in the Trust. This might force the Trust to sell portfolio securities

at disadvantageous prices.

Service (12b-1) Plan

Class 2 and Class 3

shares of the Portfolio are subject to a Rule 12b-1 Plan that provides for service fees payable at the annual rate of up to 0.15% and 0.25%, respectively, of the average daily net

assets of such class of shares. The service fees will be used to compensate the life insurance companies for costs associated with the servicing of either Class 2 or Class 3 shares,

including the cost of reimbursing the life insurance companies for expenditures made to financial intermediaries for providing service to contract owners who are the indirect beneficial owners of the Portfolio’s Class 2 or Class 3

shares. Because these fees are paid out of the Portfolio’s Class 2 or Class 3 assets on an ongoing basis, over time these fees will increase the cost of your investment and may cost you more than paying other types of sales charges.

Transaction Policies

Valuation of shares. The net asset value per share (“NAV”) for the Portfolio and each class is determined each business day at

the close of regular trading on the New York Stock Exchange (“NYSE”) (generally 4:00 p.m., Eastern Time) by dividing the net assets of each class by the number of such class’s outstanding shares. The NAV for the Portfolio’s class

of shares also may be calculated on any other day in which there is sufficient liquidity in the securities held by the Portfolio. As a result, the value of the Portfolio’s shares may change on days when you will not be able to purchase or

redeem your shares. The value of the investments held by the Portfolio are determined by SunAmerica, as the “valuation designee”, pursuant to its valuation procedures. The Board of Trustees oversees the valuation designee and at least

annually reviews its valuation policies and procedures.

Investments for which market quotations are readily available are valued at their

market price as of the close of regular trading on the NYSE for the day, unless the market quotations are determined to be unreliable. Securities and other assets for which market quotations are unavailable or unreliable are valued by the valuation

designee at fair value in accordance with valuation procedures. There is no single

- 18 -

standard for making fair value determinations, which may result in prices that vary from those of other funds. In addition, there can be no assurance that fair value pricing will reflect actual

market value and it is possible that the fair value determined for a security may differ materially from the value that could be realized upon the sale of the security. Investments in registered investment companies that do not trade on an exchange

are valued at the end of the day net asset value per share. Investments in registered investment companies that trade on an exchange are valued at the last sales price or official closing price as of the close of the customary trading session on the

exchange where the security principally traded. The prospectus for any such open-end funds should explain the circumstances under which these funds use fair value pricing and the effect of using fair value

pricing.

As of the close of regular trading on the NYSE, securities traded primarily on security exchanges outside the United States are