SECURITIES AND EXCHANGE COMMISSION

FORM 10-K

(Mark One)

| [X] | ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

or

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

(Commission file number): 001-33635

![]()

GENE BIOTHERAPEUTICS INC.

(Exact name of registrant as specified in its charter)

(State of incorporation) |

(IRS Employer Identification No.) | |

San Diego, California 92121 |

||

(Address of principal executive offices) |

||

Securities

registered under Section

Securities

registered under Section

Common Stock, par value $0.0001 per share

Indicate

by check mark if the

Indicate

by check mark if the

Indicate

by check mark whether the

Indicate

by checkmark whether the Indicate

by check mark whether the Non-accelerated

filer

Emerging

Growth Company

[ ]

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for

complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the Registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. [ ] Indicate

by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). [ ] Yes [X]

No The

aggregate market value of As

of March

TABLE

OF CONTENTS We

are filing this comprehensive Annual Report on Form 10-K for the fiscal year ended December 31, 2019 with expanded financial and

other disclosures in lieu of filing a separate Annual Report on Form 10-K for the fiscal years ended December 31, 2018 and December

31, 2017, and separate Quarterly Reports on Form 10-Q for the quarterly periods ended March 31, June 30, and September 30 during

2019, 2018 and 2017. Unless context requires otherwise, all references in this report to the

Due to financial hardship, we were unable to secure The

filing of this report will not result in us becoming “current” in our reporting requirements under the Securities

Exchange Act of 1934. It is our intention to become current, This

report, including the sections entitled “Business”, “Risk Factors”, and “Management’s Discussion

and Analysis of Financial Condition and Results of Operations,” contains forward-looking statements our

ability to fund operations and business plans, and the timing of any funding or corporate development transactions we may

pursue; the

protection expected from our intellectual property rights and those of others, including actual or potential competitors;

and Caution

should be taken not to place undue reliance on any such forward-looking statements. Forward-looking statements are subject to

certain events, risks, and uncertainties that may be outside of our control that could cause actual results to differ materially

from those expressed in or implied by the forward-looking statements. These factors include, among others, the risks described

under Item 1A and elsewhere in this report, as well as in other reports and documents we file with the United States Securities

and Exchange Commission (the “SEC -2-

●

planned

development pathways and potential commercialization activities or opportunities for our product candidates;

●

the

timing, conduct and outcome of

●

the

anticipated results of our clinical studies and trials, as well as our expectations concerning the safety and efficacy of

our products and product candidates;

●

our

ability to generate revenues, and raise sufficient financing, maintain stock price and valuation, and to regain the listing

of our common stock on a national exchange;

●

our

ability to enter into acceptable relationships with one or more contract manufacturers

●

our

ability to enter into acceptable relationships with one or more development or commercialization partners to advance the commercialization

of new products and product candidates and the timing of any product launches;

●

our

growth, expansion and acquisition strategies, the success of such strategies, and the benefits we believe can be derived from

such strategies;

●

statements

that are not statements of historical facts. -3-

Our

lead product candidate Generx [Ad5FGF-4] is an angiogenic gene therapy product candidate designed for medical revascularization

for the potential treatment of patients with myocardial ischemia and refractory angina due to advanced coronary artery disease History We

were incorporated in Delaware in 2003. In 2006, we changed our name to Cardium Therapeutics Inc. In 2013, we changed the Company’s

name to Taxus Cardium Pharmaceuticals Group Inc. to reflect a broadened business plan During

the period covered by this report, our operations have been conducted principally through operating subsidiaries including the

following: We

entered 2017 in a cash constrained position. At that time, our principal operating goal was to secure the capital necessary to

advance the clinical development and commercialization of Generx. In October 2017 we entered into an agreement with Landmark Pegasus,

Inc. (“Landmark”), a business development and strategic partnering company, to assist us with the previously announced

plans to sell our Excellagen product and assist with the strategic partnering for the development of Generx. In lieu of a cash

engagement fee, we transferred our residual investment in LifeAgain along with our minority equity investment in Healthy Brands

to Landmark, effectively exiting those businesses. In

July 2018, we sold our FDA-cleared Excellagen® product to Olaregen Therapeutix, Inc. (“Olaregen”) for aggregate

consideration of up to $4,000,000. At closing, we received a cash payment of $650,000, the remaining to be paid as royalty payments

of 10% of all worldwide sales of Excellagen totaling up to an additional $3,350,000. As of the date of this report, no royalties

have been received. We retained rights to manufacture, market and sell Excellagen in Greater China, The Russian Federation, and

the Commonwealth of Independent States (Armenia, Azerbaijan, Belarus, Kazakhstan, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan,

and Uzbekistan).

In

April 2020, after the period covered by this report, we transferred our residual rights in Excellagen to Shanxi Taxus Pharmaceuticals

Co. Ltd. (“Shanxi”) in exchange for the release of any rights or claims in ownership interest in Gene Biotherapeutics.

In connection with this transaction, Shanxi agreed to apply its previously funded $600,000 subscription payment as cash consideration

in exchange for the Excellagen ownership rights. Shanxi also released any future rights or claims against us. On

April 10, 2020, after the period covered by this report, our Angionetics, Inc. subsidiary entered into a Distribution and License

Agreement with Shanxi (as amended, the “Shanxi License Agreement”), granting Shanxi certain license rights with respect

to our Generx product candidate. The distribution and license rights commence only after we obtain U.S. FDA approval for marketing

and sale of Generx in the United States. The license rights include (a) a non-exclusive right to manufacture Generx products in

China, and (b) an exclusive right to market and sell Generx products in Singapore, Macau, Hong Kong, Taiwan, any other municipality

other than mainland China where Chinese (Mandarin or Cantonese) is the common language, the Russian Federation, and the Commonwealth

of Independent States (the “CIS”). The Shanxi License Agreement provides for a progress royalty ranging from

5% up to 10% based on annual net sales up to and including $50 million at 5%; 6% for sales ranging greater than $50 million to

$200 million; 8% for sales greater than $200 million to $450 million and at 10% for any sales greater than $450 million of the

Generx product sold by Shanxi in the licensed territory. In

May 2020, after the period covered by this report, we entered into a Preferred Stock Purchase Agreement with Nostrum Pharmaceuticals,

LLC (“Nostrum”), selling Nostrum 1,700,000 shares of our newly authorized Series B Convertible Preferred Stock in

exchange for $1,700,000. Each share of Series B Convertible Preferred Stock is convertible into shares of Common Stock at a conversion

ratio of 0.0113. Consequently the 1,700,000 shares are convertible into an aggregate of 150,442,478 shares of Common Stock. In

addition, Nostrum entered into an agreement with Sabby Healthcare Master Fund Ltd. (“Sabby”), the sole holder of our

outstanding Series A Convertible Preferred Stock, under which Nostrum purchased 220 shares of our Series A Convertible Preferred

Stock from Sabby, which is convertible into 88,496 shares of common stock. Consequently, the 220 shares are convertible into an

aggregate of 19,469,026 shares of Common Stock. Nostrum also agreed to purchase up to 570 additional Series A Convertible Preferred

Stock from Sabby, within one year following the effective date of the transaction. Since May 2020, 397 shares of Series

A Preferred Stock have been converted into 35,132,755 shares of our Common Stock (conversion rate of 88,496), that has

increased our outstanding Common Stock to 49,622,154 shares as of March 31, 2021. As a result of these

transactions, Nostrum currently controls approximately 75.2% of the voting interests of our Company. Nostrum

is a privately held pharmaceutical company engaged in the formulation and commercialization of specialty pharmaceutical products

and controlled release, orally administered, branded and generic drug products. We will use the proceeds from the sale of the

Series B Convertible Preferred Stock to fund working capital requirements in preparation for conducting the U.S. FDA-approved

Phase 3 clinical trial for our Generx product candidate, and a portion of these proceeds will be used to complete the financial

statements and disclosures in this report. We believe that Nostrum’s assets and experience in the formulation and commercialization

of pharmaceutical products will facilitate the administration and completion of the Phase 3 clinical trial for Generx on a cost-effective

basis. In

March 2021, after the period covered by this report, the Company entered into an agreement with FUJIFILM Diosynth Biotechnologies

(“FDB”) to manufacture the Generx [Ad5FGF-4] angiogenic gene therapy product candidate for Phase 3 clinical evaluation

for the treatment of refractory angina due to late-stage coronary artery disease. Manufacturing operations will be conducted at

FDB’s facilities in College Station, Texas where FDB will perform technology transfer and process development activities

for Phase 3 clinical and commercial-scale GMP manufacturing of Generx. Accordingly,

our current business is centered around the clinical development and commercialization of Generx for the potential treatment of

patients with myocardial ischemia and refractory angina due to advanced, late-stage coronary artery disease. In the future, we

expect to pursue other potential ischemia-related cardiovascular and cerebral therapeutic opportunities as well as advanced tissue

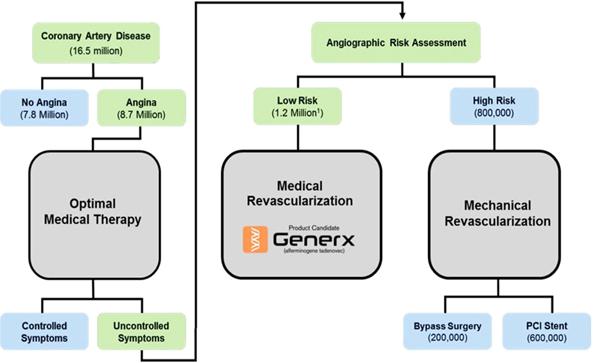

engineering applications. We estimate that there are up to 1.2 million patients in the U.S. with refractory angina, representing

up to $6.0 billion addressable market opportunity, and up to $20.0 billion worldwide. The

Generx Product Candidate Our

lead product candidate, Generx, is a first in class, single dose, angiogenic gene therapy product candidate that is designed to

improve blood flow and to increase the

Medical

Revascularization for Refractory Angina

The

Ad5FGF-4 product candidate The

transfected heart cells then express and release FGF-4 protein, which we believe promotes the growth of new blood vessels and

increased blood flow to ischemic heart tissue. The evidence shows that FGF-4 expressed by Ad5FGF-4 has the capacity to enlarge

pre-existing collateral arterioles (arteriogenesis) and to form new capillary vessels (angiogenesis) when driven by cardiac hemodynamic-impairment

and ischemic stimuli. In a pig model of myocardial ischemia, adenovirus mediated FGF gene therapy promoted increased regional

myocardial blood flow, as measured by contrast echocardiography, that correlated with an increase in capillary number, determined

by histologic assessment. Stimulation of angiogenesis by Ad5FGF-4 has also been demonstrated in an in vitro assay that recapitulates

all phases of the in vivo angiogenesis process and provides a functional bioassay for Ad5FGF-4. This assay demonstrates a synergistic

interaction between FGF-4 expressed by Ad5FGF-4, and endogenous vascular endothelial growth factor (VEGF) in the promotion of

neo-vessel formation, with evidence that FGF-4 controls angiogenesis upstream of VEGF. FGF-4 appears to be a key angiogenic regulatory

protein that stimulates the release and action of other angiogenic factors, including vascular endothelial growth factors (VEGF),

platelet-derived growth factors (PDGF), and hepatocyte growth factor (HGF), to orchestrate and promote the growth of a functional

collateral network in ischemic cardiac tissue. Generx

is administered to patients during a simple one-hour angiogram-like procedure by an interventional Addressable

Market Generx

is expected to initially target patients with refractory angina—chronic and disabling angina that: (1) are no longer responsive

to small molecule anti-anginal drug therapy, Proposed

Generx Treatment Algorithm for Patients with Refractory Angina Consistent

with Positioning in FDA-Cleared U.S. Phase 3 Clinical Trial Given

the widespread use of lipid-lowering drugs in the general population in the U.S., and increasingly worldwide, we now see more

patients reporting angina with little or no evidence of obstructive coronary artery disease based on angiographic diagnostics.

In the past 10 years, the number of ST-Elevation Myocardial Infarction patients has fallen by 50%, bypass surgery is down 40%,

and the use of stents has been reduced by 30%. We believe that this trend away from mechanical revascularization will potentially

increase the opportunity for Generx medical revascularization. The

most recently FDA approved anti-anginal drug with a novel mechanism of action is Ranexa® (ranolazine). It was FDA approved

in 2006 as a treatment for chronic angina as a metabolic modulator designed to reduce the heart’s oxygen demand. Following

FDA approval, Ranexa was acquired by Gilead Sciences for $1.4 billion in 2009. Ranexa is prescribed to be taken twice daily, generally

as a 1000 mg oral tablet and Ranolazine is now available in generic form. To

support our go to market strategy, we conducted a survey of U.S. interventional cardiologists to gauge their experience-based

assessment of the prevalence of refractory angina patients, and their openness to integrate the use of the Generx angiogenic gene

therapy product candidate, upon FDA approval, into their clinical practice. The survey confirmed that all survey responders see

patients with long-term refractory angina, and all were strongly positive and without reservation about adoption of Generx. All

cardiologists surveyed felt there is a current need for Generx to treat refractory angina and they would consider using Generx

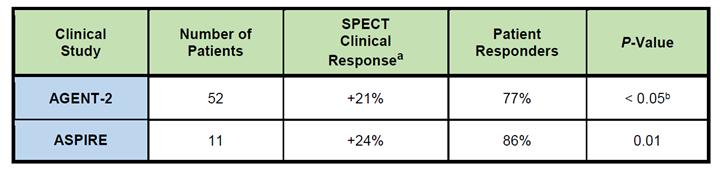

in their daily practice if approved by the FDA. As shown in the following table, the Generx product candidate for medical revascularization

therapy generated statistically significant improvements in cardiac perfusion (measured using SPECT as a reduction in reversible

perfusion defect) as compared to placebo controls in both the U.S-based Phase 2 clinical study (AGENT-2), and a small confirmatory

international study (ASPIRE), and the observed improvements were similar in magnitude to those reported following mechanical revascularization. Generx

AGENT-2 and ASPIRE SPECT Data Generx

Clinical Studies and FDA Developments The

Generx FDA regulatory dossier represents one of the most extensive and advanced DNA-based clinical data platforms ever compiled.

Generx has been evaluated as a treatment for patients with refractory angina in four prior FDA-cleared, multi-center, randomized

and placebo-controlled clinical studies (AGENT 1-4, Phase 1/2 to Phase 2b/3) and one small international study (ASPIRE). The In

these multiple prior clinical studies, the Generx product candidate appeared safe and well-tolerated, and has generated preliminary

findings of efficacy in men and women, in measures of cardiac perfusion, cardiac performance, and angina status, including: (1)

significant improvement in exercise duration by Exercise Treadmill Testing

●

Angionetics,

Inc., an 85% owned subsidiary focused on the late-stage clinical development and commercialization of Generx, an angiogenic

●

Activation

Therapeutics, Inc., a wholly owned subsidiary focused on the development and commercialization of Excellagen®, a patented

U.S. FDA-cleared wound conforming matrix for advanced wound care; and

●

LifeAgain

Insurance Solutions, Inc., a wholly owned subsidiary focused on advanced medical data analytics for developing innovative

insurance and healthcare solutions. -4- -5-

-6-

(1) Range

0.6M – 1.8M [mean 1.2M] McGillion et al., Canadian J Cardiology 28:S20-S41 (2012)

other figures, Benjamin et al., Circulation, American Heart Association, Statistics 2017. -7-

a. Improvement

in RPDS as measured by SPECT imaging at 8 weeks following a single treatment.

b. Grines

et al. JACC 42:1339-47 (2003). Tables 1 and 2. cell permeability that is believed to be activated using nitroglycerin.

| -8- |

On February 3, 2017, the FDA granted the Phase 3 AFFIRM clinical study Fast Track designation. By granting Fast Track designation to the Generx Phase 3 clinical development program, FDA acknowledges that there remains unmet medical need for patients with refractory angina. The limited available therapies for patients with refractory angina primarily address the symptoms of refractory angina by reducing myocardial oxygen demand or transiently increasing blood flow to the ischemic myocardium and require prolonged use or numerous rounds of therapy. Furthermore, available therapies have modest and heterogenous response rates. Generx is unique in its angiogenic biological mechanism of action and disease-modifying potential.

In July 2020, we submitted a protocol amendment to FDA, refining some of the patient inclusion criteria and clarifying ETT stopping criteria for enrolled patients. In addition, an adaptive trial design was incorporated to allow for interim analysis and re-estimation of sample size required to achieve the primary efficacy endpoint of statistically significant improvement in ETT with Generx compared to Placebo at 6 months. Based on further statistical analysis of historical ETT data, the target sample size was reduced from 320 patients, without an interim analysis, to 160 patients with an interim analysis after 80 patients have been enrolled. The adaptive design allows for an increase in sample size up to 226 total patients if needed to reach statistical significance.

On a global basis, over 650 patients have been enrolled in four FDA-cleared clinical studies of Generx at over 100 medical centers in the U.S., Western Europe, and Asia, 455 of whom received a one-time intracoronary administration of Generx. Based on these studies, and other pre-clinical and further international clinical evaluations, our Generx product candidate appears to be safe and well-tolerated and has generated preliminary efficacy findings in men and women, based on multiple efficacy measures within patient subset groups. Long-term safety follow-up has generated over 2,500 patient years of safety data. With the successful completion of the planned AFFIRM Phase 3 clinical study, the Generx clinical research will have evaluated over 800 patients in clinical study protocols. Based on our FDA Fast-Track designation, and our established manufacturing processes, we believe that we would be in a position to initiate the submission to the FDA of a rolling Biologics License Application (“BLA”).

FDA Registration Pathway

For

registration purposes, the FDA has classified our Generx product candidate to be an “anti-anginal” medication as a

treatment for patients who have been diagnosed with stable exertional angina due to coronary artery disease and who are no longer

responsive to current pharmaceutical therapy and mechanical interventional therapy. FDA approval of anti-anginal drugs and biologicals

requires statistically significant efficacy improvements in exercise capacity as measured by ETT compared to a placebo control

group. Developing a new and innovative anti-anginal is a challenging process and FDA approvals have been few and far between.

In the

In 2006, following a 21-year clinical and commercial development process, the FDA approved Ranexa (ranolazine), a small molecule drug in tablet form that is taken twice daily with a new mechanism of action described as metabolic modulation, to reduce the heart’s oxygen demand. Based on the Ranexa package insert, the CARISA clinical study showed that Ranexa was safe and well tolerated by refractory angina patients and that patients treated with Ranexa showed an improvement in the primary efficacy endpoint ETT of +24 seconds (+28%) compared to the placebo control over the 12- week study period. Based on our retrospective subset analysis of data from the Generx AGENT-3 clinical study, and the FDA-cleared Ad5FGF-4 Phase 3 AFFIRM clinical study design, the Generx product candidate offers the potential to meet or exceed the ETT efficacy data reported in the Ranexa CARISA clinical study. As a result, we plan to submit a BLA following successful completion of the Phase 3 AFFIRM study.

| -9- |

Generx Competitive Advantage

We believe that the most significant factors in the field of new drugs and biologics are safety and efficacy as well as relative cost, and ease of administration as compared to other products, product candidates or approaches that may be useful for treating a particular disease condition. We believe that our Generx product candidate competes favorably against the current standard of care in each of these areas:

| ● | Safety. The FDA-cleared Phase 3 AFFIRM study is preceded in the U.S. by four completed and one early discontinued study. On a global basis, over 650 patients have been enrolled in FDA-approved studies, 455 of whom received a one-time intracoronary administration of Generx, which has consistently been found to be safe and well-tolerated (based on over 2,500 patient years of safety data). Efficient uptake in the heart following intracoronary administration of Generx has been demonstrated in preclinical studies (~98% first pass extraction) and clinical studies (~90% first pass extraction). Administration of Ad5FGF-4 after stent implantation in a preclinical model of atherosclerosis and hypercholesterolemia found no evidence of increased neointima formation (restenosis) with both bare metal and drug-eluting stents. Fever is an expected side effect of adenoviral gene therapy and has been observed in ~8% of patients receiving Ad5FGF-4, occurring within the first few days after study product administration and resolving with no treatment or with antipyretic medication. No other adverse events have been associated with intracoronary administration Ad5FGF-4. | |

| ● | Effectiveness. A central finding from the Generx AGENT clinical development program is that cardiac ischemia drives Generx transfection into heart cells, and that regional cardiac ischemia is an essential precursor to support the growth of collateral blood vessels for treatment response to Generx angiogenic gene therapy. Our delivery strategy is to distribute Ad5FGF-4 throughout the microvascular circulation of the heart under conditions of transient ischemia to enhance uptake, with the angiogenic response being selective to ischemic zones. An angiogenic response to Generx has been demonstrated in preclinical studies, in which increased regional myocardial blood flow was identified by contrast echocardiography and correlated with increased vessel number, determined histologically. In clinical studies SPECT imaging has demonstrated cardiac perfusion improvements approximately up to 75% of the perfusion levels achieved from classic mechanical revascularization. The clinical response is observed in patients within four to eight weeks following administration, and it is anticipated that once formed, new vessels will persist as long as there is blood flow through the vessel. | |

| ● | Cost-Effective Manufacture. We have established and validated the Generx cGMP (defined below) manufacturing process, which is not expected to require significant additional capital investment or major process modifications for commercial manufacture. Product stability enables manufacture in large, cost-effective batch sizes. Based on our established manufacturing process, we are in a position to competitively price our Generx product candidate in alignment with cardiac stents. | |

| ● | Fits within Current Medical Practice. Generx therapy is designed to easily fit within the current practice of medicine, as a ready-to-use, one-time treatment, administered by interventional cardiologists during an approximately one-hour, out-patient, angiogram-like procedure. There are approximately 1.0 million angiogram procedures performed in the U.S. each year. Through our extensive clinical efforts, we have established appropriate dose levels, enhanced delivery techniques and simplified product administration. With regulatory approval, Generx could be the first FDA-approved gene therapy for an otherwise healthy population that would be universally affordable within healthcare medical reimbursement programs and for private pay environments. |

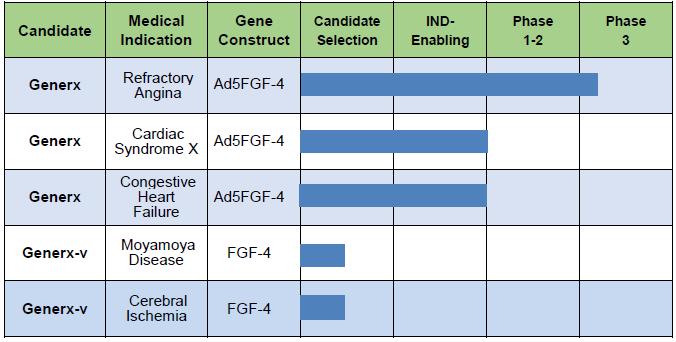

Additional Indications

Following our planned initial registration for refractory angina there are other potential ischemia-related cardiovascular and cerebral therapeutic opportunities that we may consider advancing forward with based on our angiogenic technology platform using varying dose levels and differing routes of administration.

Potential Pipeline of Generx (Ad5FGF-4) Medical Indications

| -10- |

Cardiac Syndrome X. A meta-analysis study [Vermeltfoort et al., Clinical Research in Cardiology. 2010; 99:475-81] reported that approximately 20% of patients who have a coronary angiography due to ongoing angina do not have obvious large vessel disease, a condition generally referred to as Cardiac Syndrome X (“CSX”). Patients with CSX are presumed to have coronary disease that is diffuse and/or affects smaller vessels within the heart. CSX is therefore sometimes referred to as “microvascular angina”. CSX cannot be addressed using traditional surgical approaches such CABG or PCI. We believe patients with CSX may potentially benefit from Generx microvascular angiogenic gene therapy, and plan to conduct a U.S.-based safety and efficacy study under the current FDA-approved IND. There are approximately 200,000 patients in the U.S. with CSX, 65% of whom are women.

Congestive Heart Failure. Congestive Heart Failure is a clinical syndrome that occurs when the heart is unable to pump sufficiently to maintain blood flow to meet the body’s needs. Common causes of heart failure include coronary artery disease, heart attack, high blood pressure, atrial fibrillation, valvular heart disease, excess alcohol use, infection, and cardiomyopathy of an unknown cause. In prior clinical studies of Generx in patients with myocardial ischemia and refractory angina, approximately 50% of enrolled patients were also diagnosed with mild congestive heart failure. The rationale supporting the application of angiogenic therapy for heart failure is based on the fact that mild and/or intermittent ischemia in the sub-endocardium (inner wall) can and often does occur in congestive heart failure with almost all primary causes. In a preclinical model of heart failure due to chronic sub-endocardial ischemia, a single administration of Generx resulted in significant improvement in cardiac function [McKirnan et al., Cardiac Vascular Regeneration. 2000; 1:11-21]. These preclinical findings support the potential use of Generx [Ad5FGF-4] angiogenic gene therapy as a non-surgical treatment option for heart failure. We are evaluating a Phase 2 clinical study of Generx angiogenic therapy for the treatment of patients with certain forms of congestive heart failure due to ischemic cardiomyopathy.

Moyamoya Disease & Cerebral Ischemia. Moyamoya disease (“MMD”) is a chronic occlusive, cerebrovascular disease that is characterized by progressive stenosis at the terminal portion of the internal carotid artery and an abnormal network of collateral vessels at the base of the brain. Pursuant to the Orphan Drug Act of 1983, MMD is an orphan indication, with <1 case per 100,000 in the U.S. The prevalence of MMD is much higher in East Asian countries than in Western countries. The highest prevalence of MMD is found in Japan at 3.16 per 100,000. Currently, there is no known medical treatment capable of reversing or stabilizing progression of MMD. Surgical revascularization such as extracranial-intracranial bypass is the preferred procedure for MMD patients with the main goal of preventing further ischemic injury by increasing collateral blood flow to hypo-perfused areas of the cortex. Collateral vessels are seen to sprout from bypassed vessels, thus providing increased blood flow to ischemic regions of the brain. We believe that Generx may potentially offer a new and simpler medical revascularization approach to the treatment of MMD, with a view toward further clinical development of angiogenic gene therapeutics for patients with a broader range of cerebral ischemic conditions, including vascular dementia. Preclinical studies have demonstrated that adenovectors can transfect cells in the brain, and we are investigating potential routes of administration to MMD patients that include, (1) adjunctive application of Ad5FGF-4 during burr hole surgery to augment collateralization, and (2) infusion into the carotid artery, to target ischemic regions and stimulate collateral vessel formation.

Angiogenic Research Initiative for COVID-19.

Early research has provided evidence of respiratory, neurological, and cardiac abnormalities in patients who have had severe COVID-19 immunological response requiring acute care (including protracted hospitalization and the need for mechanical ventilation). For patients who have survived and seek to return to normal life, several continuing residual adverse medical conditions appear to persist.

While the scientific literature remains uncertain, it has been suggested that mechanisms by which COVID-19 could lead to cardiovascular morbidity include direct myocardial injury as a result of inflammatory cascade or cytokine release, acute coronary syndrome from acute inflammation-triggered destabilization of atheroma, microvascular damage due to disseminated intravascular coagulation and thrombosis, direct entry of SARS-CoV-2 into myocardial cells via ACE2 receptors, and hypoxemia combined with metabolic demands of acute illness leading to myocardial injury akin to a myocardial infarction.

Based

on these preliminary insights, Gene Biotherapeutics’ research is focused on the design of an observational clinical study

to evaluate if COVID-19 may exacerbate microvascular damage and perfusion impairment in patients with pre-existing coronary artery

disease and cardiac reversible perfusion defects (“RPD”) prior to COVID-19 infection. We are proposing to assess

the damage using SPECT (Single-Photon Emission Computed Tomography) imaging to evaluate changes in

| -11- |

Commercialization Business Strategy

We

are committed to applying our first-mover scientific and clinical development leadership position in the field of angiogenic gene

therapy for the treatment of patients with a variety of cardiovascular conditions which are related by insufficient cardiac perfusion

and other potential ischemia-related cerebral therapeutic opportunities as well as advanced tissue engineering applications. The

core elements of our

| ● | Following U.S. registration for refractory angina, initiate the registration process to market and sell Generx in China, the Russian Federation, and the CIS with our current strategic partners, and consider registration in other prioritized regional markets; | |

| ● | Following FDA approval, we would also plan to (1) enter a strategic agreement(s) to market and sell Generx in other countries worldwide, or (2) undertake a terminal value transaction covering the sale of Generx to an established strategic player which has established worldwide marketing, sales, and distribution capabilities; | |

| ● | Expand the initial

labeling of Generx by initiating a Phase 2 clinical study to support the use of Generx for patients with CSX, which

is characterized by symptomatic angina in the absence of large coronary artery obstruction, and for certain forms | |

| ● | Advance our pre-clinical

research which is focused on applying our Ad5FGF-4 technology platform as a potential treatment for patients with MMD,

an orphan medical |

| ||

| ● | Establish a Generx

patient registry and conduct additional clinical studies to evaluate the safety and clinical efficacy of repeat dosing of

Generx in patients as their coronary artery disease advances causing additional perfusion defects |

| ||

| ● | Initiate additional studies to assess the potential long-term prognostic benefits of refractory angina patients receiving angiogenic therapy through medical revascularization. |

Government Regulation

Gene

therapy biologics are subject to extensive regulation in the United States under the federal Food, Drug, and Cosmetic Act. In

addition, biologics are also regulated under the Public Health Service Act. Both statutes and their corresponding regulations

govern, among other things, the testing, manufacturing, distribution, safety, efficacy, labeling, storage, record keeping, advertising

and other promotional practices involving biologics or new drugs. FDA approval or other clearances must be obtained before clinical

testing, and before manufacturing and marketing

Any

product candidate we develop will require regulatory approvals on a country-by-country basis before human trials and additional

regulatory approvals before marketing. The FDA receives reports on the progress of each phase of testing, and it may require the modification, suspension,

or termination of trials if an unwarranted risk is present to patients. If the FDA imposes a clinical hold, trials may not recommence

without FDA authorization and then only under terms authorized by the FDA. The IND application process can thus result in substantial

delay and expense.

| -12- |

Our

Generx product candidate is a gene therapy product, which is a relatively new category of therapeutics.

After

the completion of trials of a new drug or biologic product, we will have to secure FDA marketing approval. The New Drug Application

(“NDA”) or BLA must include results of product development, laboratory, animal and human studies, and

manufacturing information. The testing and approval processes require substantial time and effort and there can be

Notwithstanding

the submission of all relevant data, the FDA may ultimately decide that the NDA or BLA does not satisfy its regulatory criteria

for approval and may require additional

In

addition to FDA approval for the commercialization of our product candidates, our business is subject to state and federal laws

regarding environmental protection and hazardous substances, including the Occupational Safety and Health Act, the Resource Conservancy

and Recovery Act and the Toxic Substances Control Act

To

the extent that we conduct operations outside the United States, any such operations would be similarly regulated by various agencies

and entities in the countries in which we operate. The regulations of these countries may conflict with those in the United States

and may vary from country to country. In markets outside the United States, we may be required to obtain approvals, licenses,

or certifications from a country

Competition

The

pharmaceutical industry is intensely competitive. Our

Our

Generx

| -13- |

We

are aware of products currently

Ranexa |

| ● | The Neovasc Reducer™ (“Reducer”) is a stainless steel, hourglass-shaped medical device that is implanted into the coronary sinus using a procedure similar to that used for stent implantation. It is designed to create a focal narrowing in the coronary sinus, resulting in increased back pressure and redistribution of blood into ischemic myocardium. In 2015, results from a Phase 2 study (the “COSIRA” study; N=104) were published, reporting that significantly more patients in the treatment group, as compared to control, had an improvement in CCS class and quality of life at 6 months, but no significant improvement in exercise time. In December 2018, Neovasc announced publication of 12-year follow-up data from 7 patients demonstrating sustained improvement of angina class compared with baseline status. The Reducer is currently available only in the European Union, receiving CE mark designation in 2011. In October 2018, Neovasc announced that the Reducer™ was granted Breakthrough Device designation by the U.S. FDA, and in December 2019, Neovasc announced submission to FDA of a Premarket Approval application (PMA) for the treatment of refractory angina. On October 27, 2020, an 18 member FDA Advisory Committee reviewed the PMA submission, voting 17 to 1 “against” on the issue of a reasonable assurance of effectiveness, voting 14 to 4 “in favor” that the Reducer is safe when used as intended, and voting 13 to 3 “against” (2 abstained) on whether the relative benefits outweighed the relative risks. | |

| ● | Caladrius Biosciences is developing an autologous CD34+ stem cell product candidate for refractory angina (“CLBS14”). Caladrius acquired an exclusive worldwide license to data and regulatory filings for the late stage CD34+ cell therapy program from Shire plc in March 2018. CD34+ therapy is thought to work by increasing microvascular blood flow in the heart muscle via the development and formation of new blood vessels. Cells are collected from patients after drug-induced mobilization, followed by isolation, concentration, and formulation prior to intramyocardial injection guided by mapping catheter (NOGA). CLBS14 has been studied in Phase 1, Phase 2 and Phase 3 randomized, double-blind placebo-controlled clinical trials that reveal significant improvements in exercise capacity and angina frequency. According to public records, initiation of a Phase 3 confirmatory trial is postponed pending access to sufficient capital to complete the study uninterrupted. | |

| In May 2020, Caladrius announced positive results from a 20-patient Phase 2 proof of concept study with CD34+ cell therapy (CLBS16) in patients with CSX. Data showed statistically significant improvement in coronary flow reserve correlating with symptom relief after a single intracoronary injection of CLBS16. | ||

| ● | XyloCor Therapeutics is developing an adenovirus-based gene therapy encoding a hybrid gene for human vascular endothelial growth factor (“XC001”) for patients with refractory angina. XC001 is designed to relieve angina by promoting angiogenesis. In July 2020, XyloCor announced dosing of the first patients in the initial Phase 1/2 dose-escalation clinical study. XC001 is administered by transthoracic epicardial injection. | |

| ● | BioCardia Inc. is developing the CardiAmp™ Cell Therapy System, which provides an autologous bone marrow-derived stem cell therapy for the treatment of chronic myocardial ischemia. In July 2020, BioCardia announced activation of a Phase 3 clinical trial studying percutaneously injected cells for the treatment of refractory angina and chronic myocardial ischemia. | |

| ● | Juventas

Therapeutics is developing a non-viral, plasmid gene therapy product candidate (JVS-100) that expresses stromal cell-derived

factor-1 (“SDF-1”) for the treatment of advanced ischemic heart failure. SDF-1 has been shown to create

a homing signal that recruits the body |

| Manufacturing

Strategy

|

We

will rely on contract manufacturing for the Generx product candidate. Based on the FDA clearance of the Generx Phase 3 clinical

study protocol, all significant

| -14- |

We

have been actively advancing our Generx product candidate’s engineering and process technology in preparation for commercialization.

The adenovector Ad5FGF-4 is propagated in suspension cultures of fully characterized HEK 293 cells using serum-

Generx’s

long-term product stability (at the current storage temperature of -70

In

March 2021, the Company entered into an agreement with FUJIFILM Diosynth Biotechnologies (“FDB”) to manufacture the

Generx [Ad5FGF-4] angiogenic gene therapy product candidate for Phase 3 clinical evaluation for the treatment of refractory angina

due to late-stage coronary artery disease. Manufacturing operations will be conducted at FDB’s facilities in College Station,

Texas where FDB will perform technology transfer and process development activities for Phase

Marketing and Sales

Our

product candidates, such as Generx, must undergo clinical trials before any marketing and sales can begin. If we should obtain

marketing approvals, we do not currently have the financial resources and internal capabilities to market and sell Generx. Commercialization

Relationships Huapont

Life Sciences Co. Ltd (“Huapont”). Huapont is a China-based company focused on the research and development of

new and innovative healthcare products, and the manufacture, marketing and sale of leading pharmaceutical products, active pharmaceutical

ingredients, and a portfolio of safe and effective agricultural herbicides serving the agricultural business throughout the U.S.

and South American markets. Huapont’s pharmaceutical business includes dermatology products, cardiovascular products, anti-tuberculosis

agents, autoimmune-related products, and oncology-related products. Huapont’s API business involves the production and sale

of bulk pharmaceutical chemicals, pharmaceutical intermediates, and preparations of Western medicines, with current annual revenues

of approximately U.S. $1.5 billion, and approximately 12,000 employees operating throughout Mainland China. Huapont is listed

on the Shenzhen Stock Exchange (002004.SZ) and carries a current market capitalization of approximately U.S. $1.7 billion. In

July 2016, Pineworld Capital Limited, an investment fund affiliated with Huapont acquired a 15% preferred stock equity interest

in our Angionetics, Inc. subsidiary (the entity that holds the Generx product) in exchange for a $3.0 million investment. Concurrently

with that investment, Angionetics entered into a Distribution and License Agreement, granting Huapont an exclusive license to

clinically develop, manufacture, market and sell the Generx angiogenic gene therapy product candidate in mainland China. The distribution

and license rights commence only after we obtain U.S. FDA approval for marketing and sale of Generx in the United States. Once

the license is effective, Huapont has agreed, at its expense, to use commercially reasonable efforts to conduct clinical trials,

make regulatory filings and take such other actions as may be necessary to commercialize Generx in mainland China. The Distribution

and License Agreement calls for Huapont to make quarterly royalty payments at a rate of 10% of net sales of Generx products in

mainland China, reducing to a 5% royalty based on the volume of annual sales. The royalty payments commence on the first commercial

sale and expire on the earlier of the termination of any patent or regulatory exclusivity in China or fifteen years after the

first commercial sale. The term of the agreement continues (unless terminated for breach) until Huapont has no remaining payment

obligations to Angionetics. Upon expiration (but not an earlier termination) Huapont shall have a perpetual, non-exclusive, fully

paid-up, and royalty-free license to Generx in mainland China. Olaregen

Therapeutix Inc. In July 2018, we sold our Excellagen product to Olaregen for aggregate consideration of up to $4,000,000.

At closing, we received a cash payment of $650,000, and we will be entitled to receive royalty payments of 10% of worldwide net

sales

| -15- |

On

April 10, 2020, our Activation Therapeutics, Inc. subsidiary entered into a License and Patent Assignment Agreement with Shanxi

(the “Shanxi Assignment Agreement”) pursuant to which we transferred of all of our residual rights and assets related

to our Excellagen product to Shanxi. Under the terms of the Shanxi Assignment Agreement, we transferred all our license rights

to manufacture, use, market and sell Excellagen to

Nostrum Pharmaceuticals,

LLC. In May 2020, after the period covered by this report, we entered into a Preferred Stock Purchase Agreement with

Nostrum selling 1,700,000 shares of our newly authorized Series B Convertible Preferred Stock in exchange for $1,700,000. The

shares of Series B Convertible Preferred Stock are convertible into an aggregate of 150,442,478 shares of Common Stock. In

addition, Nostrum entered into an agreement with the holder of our outstanding Series A Convertible Preferred Stock, under

which Nostrum purchased 220 shares of our Series A Convertible Preferred Stock, convertible into an aggregate of 19,469,026

shares of Common Stock and agreed to purchase up to 570 additional Series A Convertible Preferred Stock. Since May 2020, such

holder has converted 397 shares of Series A Convertible Preferred Stock into 35,132,755 shares of our Common

stock, that has increased our outstanding Common Stock to 49,622,154 shares as of March 31, 2021. As a result

of these transactions, Nostrum currently controls approximately 75.2% of the voting interests of our Company. Nostrum

is a privately held pharmaceutical company engaged in the formulation and commercialization of specialty pharmaceutical

products and controlled release, orally administered, branded and generic drug products. We believe that Nostrum’s

assets and experience in the formulation and commercialization of pharmaceutical products will facilitate the administration

and completion of the AFFIRM Phase 3 clinical trial on a cost-effective basis. However, we do not have

Intellectual Property and Licensing-

In

connection with the Schering portfolio, we acquired the rights to certain patents owned by the University of California related

to the use of the catheter as part of

In

June 2016 we entered into a Distribution and License Agreement with an affiliate of Huapont whereby we granted the Huapont affiliate

an exclusive license to clinically develop

| -16- |

In

July 2018, we sold our

As

of December 31, 2019, we had Available

Information Our

website address is www.genebiotherapeutics.com. We make available, free of charge, through our website our Annual Report on Form

10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant

to Section You

should carefully review and consider the risks described below, as well as the other information in this report and in other reports

and documents we file with the SEC when evaluating our business and future prospects. The risks and uncertainties described below

are not the only ones we face. Additional risks and uncertainties, not presently known to us, or that we currently perceive as

immaterial or remote, may also occur. If any of the following risks or any additional risks and uncertainties actually occur,

our business could be materially harmed, and our financial condition, results of operations and future growth prospects could

be materially and adversely affected. In that event, the market price of our Risks

Related to the Development of Product Candidates The

regulatory approval processes of the FDA are inherently unpredictable, and if we are ultimately unable to obtain regulatory approval

for our product candidates, we may never generate revenue or achieve profitability. To

generate revenues, we must successfully complete clinical trials of our product candidates Generally,

there is a high rate of failure for drug candidates proceeding through clinical trials. We

cannot be certain that any of our product candidates will be successful in clinical trials or receive regulatory approval. Further,

our product candidates may not receive regulatory approval even if

ITEM

1A. RISK

FACTORS

●

The

FDA may disagree with the design or implementation of our clinical trials;

●

We

may be unable to demonstrate sufficiently to the FDA that our product candidate is safe

●

The

results of our clinical trials may not meet the level of statistical significance required by the FDA for approval; -17-

●

The

approval policies or regulations of the FDA may change significantly, in a manner rendering our clinical data insufficient

for approval. on the performance of costly post-marketing clinical trials, may approve a product candidate with a label that does not include

the labeling claims necessary or desirable for the successful commercialization of that product candidate or may restrict its

distribution. Any of the foregoing scenarios could materially harm the commercial prospects for our product candidates.

Clinical trials are expensive, time-consuming, and difficult to design and implement, and involve an uncertain outcome.

Before obtaining marketing approval from the FDA or other comparable foreign regulatory authorities for the sale of our product candidates, we must complete pre-clinical development and extensive clinical trials to demonstrate the safety and efficacy of our product candidates. Clinical testing is expensive and can take many years to complete, and its outcome is inherently uncertain. Failure can occur at any time during the clinical trial process. Although we are planning for certain clinical trials relating to Generx and our other product candidates, there can be no assurance that the FDA will accept our proposed trial designs.

We may experience delays in our clinical trials, and we do not know whether planned clinical trials will begin on time, need to be redesigned, enroll patients on time or be completed on schedule, if at all. Clinical trials can be delayed for a variety of reasons, including delays related to:

| ● | the FDA disagreeing as to the design or implementation of our clinical studies; | |

| ● | reaching mutually acceptable agreements with prospective contract research organizations (“CROs”); | |

| ● | securing a sufficient number of clinical trial sites on acceptable terms; | |

| ● | clinical sites deviating from trial protocol or dropping out of a trial; | |

| ● | obtaining institutional review board (“IRB”), approval at each site, or independent ethics committee, approval at any sites outside the United States; | |

| ● | securing sufficient quantities of our product candidate from third party contract manufacturers to support the trial; | |

| ● | any changes to our manufacturing process that may be necessary or desired; | |

| ● | addressing patient safety concerns that arise during the course of a trial; | |

| ● | imposition of a clinical hold by regulatory authorities, including as a result of unforeseen safety issues or side effects or failure of trial sites to adhere to regulatory requirements; | |

| ● | the occurrence of serious adverse events in trials of the same class of agents conducted by other companies or institutions; | |

| ● | changes to clinical trial protocols; |

| -18- |

| ● | lack of adequate funding to continue the clinical trial. |

If the third parties that we rely on for pre-clinical and clinical trial support do not successfully perform their contractual legal and regulatory duties or meet expected deadlines, we may not be able to obtain regulatory approval for or commercialize our product candidates.

We

have relied upon and plan to continue to rely upon third-party medical institutions, clinical investigators, contract laboratories

and other third party CROs to monitor and manage data for our ongoing preclinical and clinical programs. We rely on these parties

Regulatory

authorities enforce these GCPs through periodic inspections of trial sponsors, principal investigators, and trial sites. If we

or any of our CROs fail to comply with applicable GCPs, the clinical data generated in our clinical trials In

addition, our CROs are not our employees, and except for remedies available to us under our agreements with such CROs, we cannot

control whether or not they devote sufficient time and resources to our on-going clinical, non-clinical and preclinical programs.

If CROs do not successfully carry out their contractual duties or obligations or meet expected deadlines, if they need to be replaced

or if the quality or accuracy of the clinical data, they obtain is compromised due to the failure to adhere to our clinical protocols,

regulatory requirements or for other reasons, our clinical trials may be extended, delayed, or terminated and we may not be able

to obtain regulatory approval for or successfully commercialize our product candidates If

any If

we are unable to enroll patients in our clinical trials, our research and development efforts could be adversely affected. The

timely completion of clinical trials in accordance with their protocols depends, among other things, on our ability to enroll

a sufficient number of patients who remain in the study until its conclusion. We may experience difficulties in patient enrollment

in our clinical trials for a variety of reasons. Patient enrollment is affected by many factors including: Many

pharmaceutical companies are conducting clinical trials in patients with the disease indications that our potential drug products

target. As a result, we must compete with them for clinical sites, physicians and the limited number of patients who fulfill the

stringent requirements for participation in clinical trials. Also, due to the confidential nature of clinical trials, we do not

We

may be unable to maintain sufficient clinical trial liability insurance to fully insure against liabilities arising out of clinical

We

will require all patients enrolled in our clinical trials to sign consents, which explain various risks involved with participating

in the trial. However, patient consents provide only a limited level of protection, and it may be alleged that the consent did

not address or did not adequately address a risk that the patient suffered from. Additionally, we will generally be required to

indemnify the clinical product manufacturers, clinical trial centers, medical professionals and other parties conducting related

activities in connection with losses they may incur through their involvement in the clinical trials. We may not be able to obtain

or maintain product liability insurance on acceptable terms or with adequate coverage against potential liabilities. Our

inability to retain sufficient clinical trial liability insurance at an acceptable cost to protect against potential liability

claims could prevent or inhibit our ability to conduct clinical trials for product candidates we develop. We may be unable to

obtain appropriate levels of such insurance. Even if we do secure clinical trial liability insurance for our programs, we may

not be able to achieve sufficient levels of such insurance. Any claim that may be brought against us could result in a court judgment

or settlement in an amount that is not covered, in whole or in part, by our insurance or that is more than the limits of our insurance

coverage. We expect we will supplement our clinical trial coverage with product liability coverage in connection with the commercial

launch of Generx or other product candidates we develop in the future; however, we may be unable to obtain such increased coverage

on acceptable terms or at all. If we are found liable in a clinical trial lawsuit or a product liability lawsuit in the future,

we will have to pay any amounts awarded by a court or negotiated in a settlement that exceed our coverage limitations or that

are not covered by our insurance, and we may not have, or be able to obtain, sufficient capital to pay such amounts. We

currently have only one significant product candidate—our Generx product candidate—and our business is substantially

dependent on its success. We

do not currently have any viable product candidates other than Generx. Accordingly, our success is substantially dependent on

our ability to successfully secure marketing approval and to commercialize Generx. If we fail to secure marketing approval for

Generx, we could be forced to try to secure an alternative product candidate. Our internal research and development capabilities

are limited and will initially be focused on the Phase 3 Generx clinical trial. We may evaluate, acquire, license, develop and/or

market additional product candidates and technologies. We do not currently have substantial resources to procure additional technologies.

The success of this strategy depends partly upon our ability to identify, select, and acquire promising pharmaceutical product

candidates and products. The process of proposing, negotiating, and implementing a license or acquisition of a product candidate

or approved product is lengthy and complex. Other companies, including some with substantially greater financial, marketing and

sales resources, may compete with us for the license or acquisition of product candidates and approved products. We have limited

resources to identify and execute the acquisition or in-licensing of third-party products, businesses and technologies and integrate

them into our current infrastructure. Moreover, we may devote resources to potential acquisitions or in-licensing opportunities

that are never completed, or we may fail to realize the anticipated benefits of such efforts. We may not be able to acquire the

rights to additional product candidates on terms that we find acceptable, or at all. If we are unable to receive marketing approval

and successfully commercialize Generx we may not be able to secure rights to another viable product candidate and may be forced

to cease operations. Interim

“top-line” and preliminary data from our clinical trials may change as more patient data become available and are

subject to verification procedures that could result in material changes in the final data. From

time to time, we may publicly disclose interim top-line or preliminary data from our clinical trials, which is based on a preliminary

analysis of then-available data, and the results and related findings and conclusions are subject to change following a more comprehensive

review of the data related to the particular study or trial. We also make assumptions, estimations, calculations, and conclusions

as part of our analyses of data, and we may not have received or had the opportunity to evaluate all data fully and carefully.

As a result, the top-line, or preliminary results that we report may differ from future results of the same studies, or different

conclusions or considerations may qualify such results once additional data have been received and fully evaluated. Top-line or

preliminary data also remain subject to verification procedures that may result in the final data being materially different from

the top-line or preliminary data we previously published. As a result, top-line and preliminary data should be viewed with caution

until the final data are available. Regulatory

agencies may not accept or agree with our assumptions, estimates, calculations, conclusions, or analyses or may interpret or weigh

the importance of data differently, which could impact the value of the particular program, the approvability or commercialization

of the particular product candidate or product and our company in general. In addition, the information we choose to publicly

disclose regarding a particular study or clinical trial is based on what is typically extensive information, and you or others

may not agree with what we determine is material or otherwise appropriate information to include in our disclosure. If

the interim, top-line or preliminary data that we report differ from actual results, or if others, including regulatory authorities,

disagree with the conclusions reached, our ability to obtain approval for, and commercialize, our product candidates may be harmed,

which could harm our business, operating results, prospects, or financial condition. We

have obtained Fast Track Designation for Generx, but that designation may not lead to a faster development, regulatory review,

or approval. If

a product is intended for the treatment of a serious condition and nonclinical or clinical data demonstrate the potential to address

unmet medical need for this condition, a product sponsor may apply for FDA Fast Track designation. We have obtained Fast Track

designation for Generx for investigation into the treatment of refractory angina, providing opportunity for expedited clinical

development and regulatory review. Fast Track Designation does not ensure that we will receive marketing approval or that approval

will be granted within any particular timeframe. We may not experience a faster development or regulatory review or approval process

with Fast Track designation compared to conventional FDA procedures. In addition, the FDA may withdraw Fast Track designation

if it believes that the designation is no longer supported by data from our clinical development program. Fast Track designation

alone does not guarantee qualification for the FDA’s priority review procedures. If

the FDA does not conclude that our product candidates satisfy the requirements for the 505(b)(2) regulatory approval pathway,

or if the requirements for approval of any of our product candidates under Section 505(b)(2) are not as we expect, the approval

pathway for our product candidates will likely take significantly longer, cost significantly more, and encounter significantly

greater complications and risks than anticipated, and in any case may not be successful. We

intend to seek FDA approval through the 505(b)(2) regulatory pathways for Generx. Section 505(b)(2) of the Food Drug and Cosmetics

Act permits the filing of an NDA where at least some of the information required for approval comes from studies that were not

conducted by or for the applicant. If the FDA does not allow us to pursue the 505(b)(2) regulatory pathways for our product candidates

as anticipated, we may need to conduct additional clinical trials, provide additional data and information, and meet additional

standards for regulatory approval. If this were to occur, the time and financial resources required to obtain FDA approval for

our product candidates would likely substantially increase. Moreover, the inability to pursue the 505(b)(2) regulatory pathways

could result in new competitive products reaching the market faster than our product candidates, which could materially adversely

impact our competitive position and prospects. Even if we can pursue the 505(b)(2) regulatory pathways for a product candidate,

we cannot assure you that we will receive the requisite or timely approvals for commercialization of such product candidate. In

addition, we expect that our competitors will file citizens’ petitions with the FDA in an effort to persuade the FDA that

our product candidates, or the clinical studies that support their approval, contain deficiencies. Such actions by our competitors

could delay or even prevent the FDA from approving any NDA that we submit under Section 505(b)(2). Our

product candidates may cause undesirable side effects or have other properties that could delay or prevent their regulatory approval,

limit the commercial profile of an approved label, or result in other significant negative consequences. Undesirable

side effects caused by our product candidates could cause us or regulatory authorities to interrupt, delay or halt clinical trials

and could result in a more restrictive label or the delay or denial of regulatory approval by the FDA or other comparable foreign

authorities. The clinical evaluation of Generx and our other product candidates in patients is still in the early stages and it

is possible that there may be side effects associated with their use. Results of our trials could reveal a high and unacceptable

severity and prevalence of side effects. In such an event, we, the FDA, the IRBs at the institutions in which our studies are

conducted, or the Data Safety Monitoring Board could suspend or terminate our clinical trials, or the FDA or comparable foreign

regulatory authorities could order us to cease clinical trials or deny approval of our product candidates for any or all targeted

indications. While

we are not presently aware of any side effects from the use of Generx, possible serious side effects of gene transfer include

viral or gene product toxicity resulting in inflammation or other injury to the heart or other parts of the body. The development

or worsening of cancer in a patient could potentially be a perceived or actual side effect of gene therapy technologies. Furthermore,

there is a possibility of side effects or decreased effectiveness associated with an immune response toward any viral vector or

gene used in gene therapy. The possibility of such response may increase if there is a need to deliver the viral vector more than

once. Treatment-related

side effects could also affect patient recruitment or the ability of enrolled patients to complete the clinical trial or result

in potential product liability claims. In addition, these side effects may not be appropriately recognized or managed by the treating

medical staff. We expect to have to train medical personnel using our product candidates to understand the side effect profiles

for our clinical trials and upon any commercialization of any of our product candidates. Inadequate training in recognizing or

managing the potential side effects of our product candidates could result in patient injury or death. Any of these occurrences

may harm our business, financial condition, and prospects significantly. If

we elect or are forced to suspend or terminate any planned clinical trial of Generx or any other of our product candidates, the

commercial prospects for that product will be harmed and our ability to generate product revenue from that product may be delayed

or eliminated. Furthermore, any of these events could prevent us or our partners from achieving or maintaining market acceptance

of the affected product and could substantially increase the costs of commercializing our product candidates and impair our ability

to generate revenue from the commercialization of these products. Risks

Related to Product Commercialization Even

if we obtain regulatory approvals to commercialize Generx or other product candidates, our product candidates may not be accepted

by physicians or the medical community in general. Our

ongoing business depends on the success of our technologies and product candidates. Gene-based therapy, like our Generx product

candidate, is a relatively new and rapidly evolving medical approach. Biotechnology and pharmaceutical companies have successfully

developed and commercialized only a limited number of biologic-based products and to date only a limited number of cellular and

gene therapy products have been approved by the U.S. FDA. Our product candidates, and the technology underlying them, are new

and unproven and there is no guarantee that health care providers or patients will be interested in our products even if they

are approved for use. We

cannot be certain that Generx or any other product candidate we successfully develop will be accepted by physicians, hospitals,

and other health care facilities. The degree of market acceptance of any drugs we develop depends on a number of factors, including: If

the market does not accept our products or product candidates, when and if we are able to commercialize them, then we may never

become profitable. It is difficult to predict the future growth of our business, if any, and the size of the market for our product

candidates because the market and technology are continually evolving. There can be no assurance that our technologies and product

candidates will prove superior to technologies and products that may currently be available or may become available in the future

or that our technologies or research and development activities will result in any commercially profitable products. If our products

do not gain market acceptance, we may not be able to fund future operations either through operating or financing activities. Even

if we obtain marketing approval for Generx or another product candidate, we will still face extensive and ongoing regulatory requirements

which could significantly impact our operations. Any

product candidate for which we obtain marketing approval, along with the manufacturing processes, post-approval clinical data,

labeling, packaging, distribution, adverse event reporting, storage, recordkeeping, export, import, advertising, and promotional

activities for such product, among other things, will be subject to extensive and ongoing requirements of and review by the FDA

and other regulatory authorities. These requirements include submissions of safety and other post-marketing information and reports,

establishment registration and drug listing requirements, continued compliance with cGMP requirements relating to manufacturing,

quality control, quality assurance and corresponding maintenance of records and documents, requirements regarding the distribution

of samples to physicians and recordkeeping and GCP requirements for any clinical trials that we conduct post-approval. Even

if marketing approval of a product candidate is granted, the approval may be subject to limitations on the indicated uses for

which the product candidate may be marketed or to the conditions of approval, including a requirement to implement a REMS. If

any of our product candidates receives marketing approval, the accompanying label may limit the approved indicated use of the

product candidate, which could limit sales of the product candidate. The FDA may also impose requirements for costly post-marketing

studies or clinical trials and surveillance to monitor the safety or efficacy of a product. Violations of the Federal Food, Drug,

and Cosmetic Act, or FDCA, relating to the promotion of prescription drugs may lead to FDA enforcement actions and investigations

alleging violations of federal and state healthcare fraud and abuse laws, as well as state consumer protection laws. Later

discovery of previously unknown adverse events or other problems with our products, manufacturers or manufacturing processes or

failure to comply with regulatory requirements, could result in: Further,

the FDA’s policies may change, and additional government regulations may be enacted that could impose extensive and ongoing

regulatory requirements and obligations on any product candidate for which we obtain marketing approval. If we are slow or unable

to adapt to changes in existing requirements or the adoption of new requirements or policies, or if we are not able to maintain

regulatory compliance, we may lose any marketing approval that we may have obtained, which would adversely affect our business,

prospects, and ability to achieve or sustain profitability. Healthcare

reform measures could hinder or prevent our product candidates’ commercial success. New

laws, regulations and judicial decisions, or new interpretations of existing laws, regulations, and decisions, that relate to

healthcare availability, methods of delivery or payment for products and services, or sales, marketing, or pricing, may limit

our potential revenue, and we may need to revise our research and development programs. The continuing efforts of the U.S. and

foreign governments, insurance companies, managed care organizations and other payors of health care services to contain or reduce

health care costs may adversely affect our ability to set prices for our products which we believe are fair, and our ability to

generate revenues and achieve and maintain profitability. We cannot predict the reform initiatives that may be adopted in the

future or whether initiatives that have been adopted will be repealed or modified. Further

federal and state proposals and health care reforms are likely which could limit the prices that can be charged for the product

candidates that we develop and may further limit our commercial opportunities. Our proposed products may not be considered cost-effective,

and coverage and reimbursement may not be available or sufficient to allow us to sell our proposed products on a profitable basis.

Our results of operations could be materially adversely affected by proposed healthcare reforms, by the Medicare prescription

drug coverage legislation, by the possible effect of such current or future legislation on amounts that private insurers will

pay and by other health care reforms that may be enacted or adopted in the future. We

intend to rely on third parties to produce commercial supplies of any approved product candidate, and our commercialization of

any future product could be stopped or delayed or made less profitable if third party manufacturers fail to obtain approval of

the FDA or comparable regulatory authorities or fail to provide us with drug product in sufficient quantities or at acceptable

prices. The

manufacture of biotechnology and pharmaceutical products is complex and requires significant expertise, capital investment, process

controls and know-how. Common difficulties in biotechnology and pharmaceutical manufacturing may include: We

do not currently have nor do we plan to acquire the infrastructure or capability internally to produce an adequate supply of compounds

to meet future requirements for clinical trials and commercialization of our products or to produce our products in accordance

with cGMP prescribed by the FDA. Drug manufacturing facilities are subject to inspection before the FDA will issue an approval

to market a new drug product, and all of the manufacturers that we intend to use must adhere to the cGMP regulations prescribed

by the FDA. We

expect to rely on third-party manufacturers for clinical supplies of our product candidates that we may develop. These third-party

manufacturers will be required to comply with cGMPs, and other applicable laws and regulations. We will have no control over the

ability of these third parties to comply with these requirements, or to maintain adequate quality control, quality assurance and

qualified personnel. If the FDA or any other applicable regulatory authorities do not approve the facilities of these third parties

for the manufacture of our other product candidates or any products that we may successfully develop, or if it withdraws any such

approval, or if our suppliers or contract manufacturers decide they no longer want to supply or manufacture for us, we may need

to find alternative manufacturing facilities, in which case we might not be able to identify manufacturers for clinical or commercial

supply on acceptable terms, or at all. Any of these factors would significantly impact our ability to develop, obtain regulatory

approval for or market our product candidates and adversely affect our business. Manufacturing

biologic products is subject to a multitude of manufacturing risks, any of which could substantially increase our costs and limit

supply of our products. We