As filed with the Securities and Exchange Commission on April 26, 2023

1940 Act File No. 811-23027

U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-1A

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 | ☒ |

AMENDMENT NO. 9

(CHECK APPROPRIATE BOX OR BOXES)

JOHN HANCOCK COLLATERAL TRUST

(EXACT NAME OF REGISTRANT AS SPECIFIED IN CHARTER)

200 BERKELEY STREET

BOSTON, MASSACHUSETTS 02116

(ADDRESS OF PRINCIPAL EXECUTIVE OFFICES) (ZIP CODE)

REGISTRANT’S TELEPHONE NUMBER, INCLUDING AREA CODE

(800) 225-5291

CHRISTOPHER SECHLER, ESQ.

200 BERKELEY STREET

BOSTON, MASSACHUSETTS 02116

(NAME AND ADDRESS OF AGENT FOR SERVICE)

COPIES OF COMMUNICATIONS TO:

MARK P. GOSHKO, ESQ.

TRAYNE S. WHEELER, ESQ.

K&L GATES LLP

ONE LINCOLN STREET

BOSTON, MASSACHUSETTS 02111-2950

EXPLANATORY NOTES

This Registration Statement on Form N-1A has been filed by John Hancock Collateral Trust (the “Fund”), a series of John Hancock Collateral Trust (the “Trust”) pursuant to Section 8(b) of the Investment Company Act of 1940, as amended (the “1940 Act”). However, beneficial interests of the Fund are not being registered under the Securities Act of 1933, as amended (the “1933 Act”), because such interests will be issued solely by way of a “private placement” exempt from the registration requirements of the 1933 Act, applicable state securities laws pursuant to Rule 506 of Regulation D under the 1933 Act and comparable state law exemptions and/or through private placement transactions that do not involve any “public offering” within the meaning of Section 4(a)(2) of the 1933 Act. With the exception of John Hancock Investment Management LLC and John Hancock Signature Services, Inc., only certain investment companies advised by the investment advisor to the Fund, or by one of its affiliates, that are “accredited investors” within the meaning of Regulation D under the 1933 Act, may invest in the Fund. This Registration Statement does not constitute an offer to sell, or the solicitation of an offer to buy, any interests in the Fund.

This Registration Statement has been prepared as a single document consisting of Parts A, B and C, none of which is to be used or distributed as a stand-alone document. The Fund’s Part A is incorporated by reference into the Fund’s Part B, and Part B is incorporated by reference into the Fund’s Part A.

Dated: April 26, 2023

JOHN HANCOCK COLLATERAL TRUST

PART A

THIS PART A DOES NOT CONSTITUTE AN OFFER TO SELL, OR THE SOLICITATION OF AN OFFER TO BUY, ANY BENEFICIAL INTERESTS IN JOHN HANCOCK COLLATERAL TRUST.

Responses to Items 1, 2, 3, 4 and 13 have not been included pursuant to paragraph 2(b) of Instruction B of the General Instructions to Form N-1A.

ITEM 5. MANAGEMENT

(a) Investment Managers

The name of the investment advisor of the Fund is John Hancock Investment Management LLC (the “Advisor”). The name of the investment subadvisor of the Fund is Manulife Investment Management (US) LLC (“Manulife IM (US)” or the “Subadvisor”).

(b) The portfolio managers, their titles and length of association with the Fund are as follows:

Pearl Natalie Andrada

| • | Fixed income trader of Manulife IM (US) |

| • | Associated with the Fund since 2022 |

| • | Began business career in 2010 |

Bridget Bruce

| ▪ | Fixed income trader of Manulife IM (US) |

| ▪ | Associated with the Fund since 2015 |

| ▪ | Began business career in 2007 |

| 1 |

Christopher Coccoluto

| ▪ | Senior fixed income trader of Manulife IM (US) |

| ▪ | Associated with the Fund since 2015 |

| ▪ | Began business career in 2008 |

Michael Lorizio

| ▪ | Senior fixed income trader of Manulife IM (US) |

| ▪ | Associated with the Fund since 2015 |

| ▪ | Began business career in 1999 |

James Madison

| ▪ | Fixed income trader of Manulife IM (US) |

| ▪ | Associated with the Fund since 2015 |

| ▪ | Began business career in 2005 |

Connor Minnaar, CFA

| ▪ | Associate portfolio manager of Manulife IM (US) |

| ▪ | Associated with the Fund since 2022 |

| ▪ | Began business career in 2002 |

ITEM 6. PURCHASE AND SALE OF FUND SHARES

(a) Purchase of Fund Shares. There is no minimum

initial or subsequent investment requirement for the Fund.

(b) The Fund’s shares are redeemable daily by contacting the Fund’s transfer agent on any business day by written request

or wire transfer.

ITEM 7. TAX INFORMATION

The Fund intends to make distributions taxed as ordinary income or as capital gains.

ITEM 8. FINANCIAL INTERMEDIARY COMPENSATION

Statement omitted.

ITEM 9. INVESTMENT OBJECTIVES, PRINCIPAL INVESTMENT STRATEGIES, RELATED RISKS, AND DISCLOSURE OF PORTFOLIO HOLDINGS

(a) Investment Objective

The Fund’s investment objective is to seek current income, while maintaining adequate liquidity, safeguarding the return of principal and minimizing risk of default. The Fund’s investment objective is not a fundamental policy and may be changed without shareholder approval. There is no assurance that the Fund will achieve its investment objective.

(b) Implementation of Investment Objective

The Fund invests only in U.S. dollar-denominated securities that, at the time of investment, are “eligible securities” as defined by Rule 2a-7 under the Investment Company Act of 1940 (“Rule 2a-7”). These securities may be issued by:

| ▪ | U.S. and foreign companies; |

| ▪ | U.S. and foreign banks; |

| 2 |

| ▪ | U.S. and foreign governments; |

| ▪ | U.S. agencies, states and municipalities; and |

| ▪ | International organizations such as the World Bank and the International Monetary Fund. |

The Fund may also invest in repurchase agreements based on these securities.

The Fund maintains a dollar-weighted average maturity of 60 days or less and a dollar-weighted average life of 120 days or less. Unlike the Fund’s dollar-weighted average maturity, the Fund’s dollar-weighted average life is calculated without reference to the reset dates of variable rate debt obligations held by the Fund.

As stated above, the Fund will invest in “eligible securities” as defined under Rule 2a-7, which include securities issued by another money market fund, government securities or securities that have a remaining maturity of no more than 397 calendar days and are determined by the Fund’s Board or its delegate to present minimal credit risk based on an assessment of the issuer’s credit quality, including the capacity of the issuer or guarantor to meet its financial obligations. The Fund’s Board has adopted procedures by which the Adviser will conduct this initial and ongoing assessment, as required.

The Fund will not acquire any security if, after doing so, more than 5% of its total assets would be invested in illiquid investments. An “illiquid investment” is an investment that the Fund reasonably expects cannot be sold or disposed of in current market conditions in seven calendar days or less without the sale or disposition significantly changing the market value of the investment.

The Fund, at the time of investment, will have at least 10% of its assets in cash, direct obligations of the U.S. government or securities readily convertible to cash within one business day. The Fund, at the time of investment, will have at least 30% of its assets in cash, direct obligations of the U.S. government, including certain government agency securities issued at a discount with remaining maturities of 60 days or less, and securities readily convertible to cash within five business days.

In managing the Fund, the Subadvisor searches aggressively for the best values on securities that meet the Fund’s credit and maturity requirements. The Subadvisor tends to favor corporate securities and looks for relative yield advantages between, for example, a company’s secured and unsecured short-term debt obligations.

In pursuing its investment objective and implementing its investment strategies, the Fund will comply with Rule 2a-7.

Pursuant to Rule 2a-7, the Fund is designated as an “institutional” money market fund and is required to utilize current market-based prices to value its portfolio securities and transact at a floating net asset value (NAV) that uses four-decimal-place precision ($10.0000). Because the share price of the Fund will fluctuate, when a shareholder sells its shares, they may be worth more or less than what the shareholder originally paid for them. Accordingly, a shareholder may recognize capital gain or loss for federal income tax purposes upon the redemption of Fund shares.

In addition, the Fund has adopted policies and procedures to impose liquidity fees on redemptions and/or temporary redemption gates in the event the Fund’s weekly liquid assets were to fall below a designated threshold, if the Fund’s Board determines such liquidity fees or redemption gates are in the best interest of the Fund.

If the Fund’s weekly liquid assets fall below 30% of its total assets, the Fund may, but is not required to, impose liquidity fees of up to 2% of the value of the shares redeemed and/or temporarily suspend redemptions. If the Fund’s weekly liquid assets fall below 10% of its total assets at the end of any business day, the Fund is required to impose a liquidity fee of 1% on all redemptions beginning on the

| 3 |

next business day, unless the Board determines that imposing such a fee would not be in the best interests of the Fund. Please see Item 11 herein for additional information.

You could lose money by investing in the Fund. Because the share price of the Fund will fluctuate, when you sell your shares, they may be worth more or less than what you originally paid for them. The Fund may impose a fee upon the sale of your shares or may temporarily suspend your ability to sell shares if the Fund’s liquidity falls below required minimums because of market conditions or other factors. An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation (“FDIC”) or any other government agency. The Fund’s sponsor has no legal obligation to provide financial support to the Fund, and you should not expect that the sponsor will provide financial support to the Fund at any time.

(c) Risks

An investment in the Fund is not a bank deposit and is not insured or guaranteed by the FDIC or any other government agency. The Fund is managed pursuant to the investment policies and limitations described in this Registration Statement. The value of the Fund’s shares could go down in price, meaning that a shareholder could lose money by investing in the Fund. Many factors influence the Fund’s performance, and they are described in more detail below. The Fund’s investment strategy may not produce the intended results.

Instability in the financial markets has led many governments, including the U.S. government, to take a number of unprecedented actions designed to support certain financial institutions and segments of the financial markets that have experienced extreme volatility and, in some cases, a lack of liquidity. Federal, state, and other governments, and their regulatory agencies or self-regulatory organizations, may take actions that affect the regulation of the instruments in which the Fund invests, or the issuers of such instruments, in ways that are unforeseeable. Legislation or regulation may also change the way in which the Fund itself is regulated. Such legislation or regulation could limit or preclude the Fund’s ability to achieve its investment objective. In addition, political events within the United States and abroad could negatively impact financial markets and the Fund’s performance. Further, certain municipalities of the United States and its territories are financially strained and may face the possibility of default on their debt obligations, which could directly or indirectly detract from the Fund’s performance.

Governments or their agencies may also acquire distressed assets from financial institutions and acquire ownership interests in those institutions. The implications of government ownership and disposition of these assets are unclear, and such a program may have positive or negative effects on the liquidity, valuation, and performance of the Fund’s portfolio holdings. Furthermore, volatile financial markets can expose the Fund to greater market and liquidity risk, increased transaction costs, and potential difficulty in valuing portfolio instruments held by the Fund.

The Fund’s main risk factors are listed below in alphabetical order, not in order of importance. For further details about Fund risks, including additional risk factors that are not discussed in this Part A because they are not considered primary risk factors, see Part B.

Changing distribution levels risk. The distribution amounts paid by the Fund generally depend on the amount of income and/or dividends paid by the Fund’s investments. As a result of market, interest rate and other circumstances, the amount of cash available for distribution by the Fund and the Fund’s distribution rate may vary or decline. The risk of such variability is accentuated in currently prevailing market and interest rate circumstances.

Credit quality risk. The Fund invests exclusively in high-quality debt securities (those that are “eligible securities” under Rule 2a-7). Fixed-income securities are subject to the risk that the issuer of the security will not repay all or a portion of the principal borrowed and will not make all interest payments. If the credit quality of a fixed-income security deteriorates after the Fund has purchased the security, the market value

| 4 |

of the security may decrease and lead to a decrease in the value of the Fund’s investments; however, the Fund will not be required to dispose of the security.

U.S. government securities are subject to varying degrees of credit risk depending upon whether the securities are supported by the full faith and credit of the United States; the ability to borrow from the U.S. Treasury; only by the credit of the issuing U.S. government agency, instrumentality, or corporation; or otherwise supported by the United States. For example, issuers of many types of U.S. government securities (e.g., the Federal Home Loan Mortgage Corporation (Freddie Mac), Federal National Mortgage Association (Fannie Mae), and Federal Home Loan Banks), although chartered or sponsored by Congress, are not funded by congressional appropriations, and their fixed-income securities, including asset-backed and mortgage-backed securities, are neither guaranteed nor insured by the U.S. government. An agency of the U.S. government has placed Fannie Mae and Freddie Mac into conservatorship, a statutory process with the objective of returning the entities to normal business operations. It is unclear what effect this conservatorship will have on the securities issued or guaranteed by Fannie Mae or Freddie Mac. As a result, these securities are subject to more credit risk than U.S. government securities that are supported by the full faith and credit of the United States (e.g., U.S. Treasury bonds).

Economic and Market Events Risk.

Events in certain sectors historically have resulted, and may in the future result, in an unusually high degree of volatility in the financial markets, both domestic and foreign. These events have included, but are not limited to: bankruptcies, corporate restructurings, and other similar events; governmental efforts to limit short selling and high frequency trading; measures to address U.S. federal and state budget deficits; social, political, and economic instability in Europe; economic stimulus by the Japanese central bank; dramatic changes in energy prices and currency exchange rates; and China’s economic slowdown. Interconnected global economies and financial markets increase the possibility that conditions in one country or region might adversely impact issuers in a different country or region. Both domestic and foreign equity markets have experienced increased volatility and turmoil, with issuers that have exposure to the real estate, mortgage, and credit markets particularly affected. Financial institutions could suffer losses as interest rates rise or economic conditions deteriorate.

In addition, relatively high market volatility and reduced liquidity in credit and fixed-income markets may adversely affect many issuers worldwide. Actions taken by the U.S. Federal Reserve (Fed) or foreign central banks to stimulate or stabilize economic growth, such as interventions in currency markets, could cause high volatility in the equity and fixed-income markets. Reduced liquidity may result in less money being available to purchase raw materials, goods, and services from emerging markets, which may, in turn, bring down the prices of these economic staples. It may also result in emerging-market issuers having more difficulty obtaining financing, which may, in turn, cause a decline in their securities prices.

Beginning in March 2022, the Fed began increasing interest rates and has signaled the potential for further increases. As a result, risks associated with rising interest rates are currently heightened. It is difficult to accurately predict the pace at which the Fed will increase interest rates any further, or the timing, frequency or magnitude of any such increases, and the evaluation of macro-economic and other conditions could cause a change in approach in the future. Any such increases generally will cause market interest rates to rise and could cause the value of a fund’s investments, and the fund’s net asset value (NAV), to decline, potentially suddenly and significantly. As a result, the fund may experience high redemptions and, as a result, increased portfolio turnover, which could increase the costs that the fund incurs and may negatively impact the fund’s performance.

In addition, as the Fed increases the target Fed funds rate, any such rate increases, among other factors, could cause markets to experience continuing high volatility. A significant increase in interest rates may cause a decline in the market for equity securities. These events and the possible resulting market volatility may have an adverse effect on the fund.

| 5 |

Political turmoil within the United States and abroad may also impact the fund. Although the U.S. government has honored its credit obligations, it remains possible that the United States could default on its obligations. While it is impossible to predict the consequences of such an unprecedented event, it is likely that a default by the United States would be highly disruptive to the U.S. and global securities markets and could significantly impair the value of the fund’s investments. Similarly, political events within the United States at times have resulted, and may in the future result, in a shutdown of government services, which could negatively affect the U.S. economy, decrease the value of many fund investments, and increase uncertainty in or impair the operation of the U.S. or other securities markets. In recent years, the U.S. renegotiated many of its global trade relationships and imposed or threatened to impose significant import tariffs. These actions could lead to price volatility and overall declines in U.S. and global investment markets.

Uncertainties surrounding the sovereign debt of a number of European Union (EU) countries and the viability of the EU have disrupted and may in the future disrupt markets in the United States and around the world. If one or more countries leave the EU or the EU dissolves, the global securities markets likely will be significantly disrupted. On January 31, 2020, the United Kingdom (UK) left the EU, commonly referred to as “Brexit,” and the UK ceased to be a member of the EU. Following a transition period during which the EU and the UK Government engaged in a series of negotiations regarding the terms of the UK’s future relationship with the EU, the EU and the UK Government signed an agreement regarding the economic relationship between the UK and the EU. While the full impact of Brexit is unknown, Brexit has already resulted in volatility in European and global markets. There remains significant market uncertainty regarding Brexit’s ramifications, and the range and potential implications of possible political, regulatory, economic, and market outcomes are difficult to predict. This uncertainty may affect other countries in the EU and elsewhere, and may cause volatility within the EU, triggering prolonged economic downturns in certain countries within the EU. Despite the influence of the lockdowns, and the economic bounce back, Brexit has had a material impact on the UK’s economy. Additionally, trade between the UK and the EU did not benefit from the global rebound in trade in 2021, and remained at the very low levels experienced at the start of the coronavirus (COVID-19) pandemic in 2020, highlighting Brexit’s potential long-term effects on the UK economy.

In addition, Brexit may create additional and substantial economic stresses for the UK, including a contraction of the UK economy and price volatility in UK stocks, decreased trade, capital outflows, devaluation of the British pound, wider corporate bond spreads due to uncertainty and declines in business and consumer spending as well as foreign direct investment. Brexit may also adversely affect UK-based financial firms that have counterparties in the EU or participate in market infrastructure (trading venues, clearing houses, settlement facilities) based in the EU. Additionally, the spread of the coronavirus (COVID-19) pandemic is likely to continue to stretch the resources and deficits of many countries in the EU and throughout the world, increasing the possibility that countries may be unable to make timely payments on their sovereign debt. These events and the resulting market volatility may have an adverse effect on the performance of the fund.

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange trading suspensions and closures, which may lead to less liquidity in certain instruments, industries, sectors or the markets generally, and may ultimately affect fund performance. For example, the coronavirus (COVID-19) pandemic has resulted and may continue to result in significant disruptions to global business activity and market volatility due to disruptions in market access, resource availability, facilities operations, imposition of tariffs, export controls and supply chain disruption, among others. The impact of a health crisis and other epidemics and pandemics that may arise in the future, could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other pre-existing political, social and economic risks. Any such impact could adversely affect the fund’s performance, resulting in losses to your investment.

The United States responded to the coronavirus (COVID-19) pandemic and resulting economic distress with fiscal and monetary stimulus packages. In late March 2020, the government passed the Coronavirus Aid, Relief, and Economic Security Act, a stimulus package providing for over $2.2 trillion in resources to

| 6 |

small businesses, state and local governments, and individuals adversely impacted by the coronavirus (COVID-19) pandemic. In late December 2020, the government also passed a spending bill that included $900 billion in stimulus relief for the coronavirus (COVID-19) pandemic. Further, in March 2021, the government passed the American Rescue Plan Act of 2021, a $1.9 trillion stimulus bill to accelerate the United States’ recovery from the economic and health effects of the coronavirus (COVID-19) pandemic. In addition, in mid-March 2020 the Fed cut interest rates to historically low levels and promised unlimited and open-ended quantitative easing, including purchases of corporate and municipal government bonds. The Fed also enacted various programs to support liquidity operations and funding in the financial markets, including expanding its reverse repurchase agreement operations, adding $1.5 trillion of liquidity to the banking system, establishing swap lines with other major central banks to provide dollar funding, establishing a program to support money market funds, easing various bank capital buffers, providing funding backstops for businesses to provide bridging loans for up to four years, and providing funding to help credit flow in asset-backed securities markets. The Fed also extended credit to small- and medium-sized businesses.

Political and military events, including in Ukraine, North Korea, Russia, Venezuela, Iran, Syria, and other areas of the Middle East, and nationalist unrest in Europe and South America, also may cause market disruptions.

As a result of continued political tensions and armed conflicts, including the Russian invasion of Ukraine commencing in February of 2022, the extent and ultimate result of which are unknown at this time, the United States and the EU, along with the regulatory bodies of a number of countries, have imposed economic sanctions on certain Russian corporate entities and individuals, and certain sectors of Russia’s economy, which may result in, among other things, the continued devaluation of Russian currency, a downgrade in the country’s credit rating, and/or a decline in the value and liquidity of Russian securities, property or interests. These sanctions could also result in the immediate freeze of Russian securities and/or funds invested in prohibited assets, impairing the ability of a fund to buy, sell, receive or deliver those securities and/or assets. These sanctions or the threat of additional sanctions could also result in Russia taking counter measures or retaliatory actions, which may further impair the value and liquidity of Russian securities. The United States and other nations or international organizations may also impose additional economic sanctions or take other actions that may adversely affect Russia-exposed issuers and companies in various sectors of the Russian economy. Any or all of these potential results could lead Russia’s economy into a recession. Economic sanctions and other actions against Russian institutions, companies, and individuals resulting from the ongoing conflict may also have a substantial negative impact on other economies and securities markets both regionally and globally, as well as on companies with operations in the conflict region, the extent to which is unknown at this time. The United States and the EU have also imposed similar sanctions on Belarus for its support of Russia’s invasion of Ukraine. Additional sanctions may be imposed on Belarus and other countries that support Russia. Any such sanctions could present substantially similar risks as those resulting from the sanctions imposed on Russia, including substantial negative impacts on the regional and global economies and securities markets.

In addition, there is a risk that the prices of goods and services in the United States and many foreign economies may decline over time, known as deflation. Deflation may have an adverse effect on stock prices and creditworthiness and may make defaults on debt more likely. If a country’s economy slips into a deflationary pattern, it could last for a prolonged period and may be difficult to reverse. Further, there is a risk that the present value of assets or income from investments will be less in the future, known as inflation. Inflation rates may change frequently and drastically as a result of various factors, including unexpected shifts in the domestic or global economy, and a fund’s investments may be affected, which may reduce a fund’s performance. Further, inflation may lead to the rise in interest rates, which may negatively affect the value of debt instruments held by the fund, resulting in a negative impact on a fund’s performance. Generally, securities issued in emerging markets are subject to a greater risk of inflationary or deflationary forces, and more developed markets are better able to use monetary policy to normalize markets.

| 7 |

Fees and gates risk. The Fund has adopted policies and procedures such that the Fund will be able to impose liquidity fees on redemptions and/or temporarily suspend redemptions for up to 10 business days in any 90-day period in the event that the Fund’s weekly liquid assets were to fall below a designated threshold, subject to a determination by the Fund’s Board that such a liquidity fee or redemption gate is in the Fund’s best interest. If the Fund’s weekly liquid assets fall below 30% of its total assets, the Fund may impose liquidity fees of up to 2% of the value of the shares redeemed and/or temporarily suspend redemptions, if the Board, including a majority of the independent Trustees, determines that imposing a liquidity fee or temporarily suspending redemptions is in the Fund’s best interest. In addition, if the Fund’s weekly liquid assets fall below 10% of its total assets at the end of any business day, the Fund must impose a 1% liquidity fee on shareholder redemptions unless the Board, including a majority of the independent Trustees, determines that imposing such fee is not in the best interests of the Fund.

Fixed-income securities risk. Fixed-income securities are affected by changes in interest rates and credit quality. A rise in interest rates typically causes bond prices to fall. The longer the average maturity or average duration of the bonds held by the Fund, the more sensitive the Fund is likely to be to interest-rate changes. There is the possibility that the issuer of the security will not repay all or a portion of the principal borrowed and will not make all interest payments.

Floating net asset value money market risk. The Fund will not maintain a constant NAV per share. The value of the Fund’s shares will be calculated to four decimal places and will fluctuate reflecting the value of the portfolio of investments held by the Fund. It is possible to lose money by investing in the Fund.

Foreign securities risk.

Funds that invest in securities traded principally in securities markets outside the United States are subject to additional and more varied risks, as the value of foreign securities may change more rapidly and extremely than the value of U.S. securities. Less information may be publicly available regarding foreign issuers, including foreign government issuers. Foreign securities may be subject to foreign taxes and may be more volatile than U.S. securities. Currency fluctuations and political and economic developments may adversely impact the value of foreign securities. The securities markets of many foreign countries are relatively small, with a limited number of companies representing a small number of industries. Additionally, issuers of foreign securities may not be subject to the same degree of regulation as U.S. issuers. Reporting, accounting, and auditing standards of foreign countries differ, in some cases significantly, from U.S. standards. There are generally higher commission rates on foreign portfolio transactions, transfer taxes, higher custodial costs, and the possibility that foreign taxes will be charged on dividends and interest payable on foreign securities, some or all of which may not be reclaimable. Also, adverse changes in investment or exchange control regulations (which may include suspension of the ability to transfer currency or assets from a country); political changes; or diplomatic developments could adversely affect a fund’s investments. In the event of nationalization, expropriation, confiscatory taxation, or other confiscation, the fund could lose a substantial portion of, or its entire investment in, a foreign security. Some of the foreign securities risks are also applicable to funds that invest a material portion of their assets in securities of foreign issuers traded in the United States.

If applicable, depositary receipts are subject to most of the risks associated with investing in foreign securities directly because the value of a depositary receipt is dependent upon the market price of the underlying foreign equity security. Depositary receipts are also subject to liquidity risk. Additionally, the Holding Foreign Companies Accountable Act (HFCAA) could cause securities of foreign companies, including American depositary receipts, to be delisted from U.S. stock exchanges if the companies do not allow the U.S. government to oversee the auditing of their financial information. Although the requirements of the HFCAA apply to securities of all foreign issuers, the SEC has thus far limited its enforcement efforts to securities of Chinese companies. If securities are delisted, a fund’s ability to transact in such securities will be impaired, and the liquidity and market price of the securities may decline. The fund may also need to seek other markets in which to transact in such securities, which could increase the fund’s costs.

| 8 |

Interest-rate risk. Fixed-income securities are affected by changes in interest rates. When interest rates decline, the market value of fixed-income securities generally can be expected to rise. Conversely, when interest rates rise, the market value of fixed-income securities generally can be expected to decline. The longer the duration or maturity of a fixed-income security, the more susceptible it is to interest-rate risk. Duration is a measure of the price sensitivity of a debt security, or a fund that invests in a portfolio of debt securities, to changes in interest rates, whereas the maturity of a security measures the time until final payment is due. Duration measures sensitivity more accurately than maturity because it takes into account the time value of cash flows generated over the life of a debt security. Recent and potential future changes in government monetary policy may affect interest rates.

Beginning in March 2022, the Federal Reserve Board (Fed) began increasing interest rates and has signaled the potential for further increases. It is difficult to accurately predict the pace at which the Fed will increase interest rates any further, or the timing, frequency or magnitude of any such increases, and the evaluation of macro-economic and other conditions could cause a change in approach in the future. Any such increases generally will cause market interest rates to rise and could cause the value of a fund’s investments, and the fund’s net asset value, to decline, potentially suddenly and significantly. As a result, the fund may experience high redemptions and, as a result, increased portfolio turnover, which could increase the costs that the fund incurs and may negatively impact the fund’s performance.

The fixed-income securities market has been and may continue to be negatively affected by the coronavirus (COVID-19) pandemic. As with other serious economic disruptions, governmental authorities and regulators responded with significant fiscal and monetary policy changes, including considerably lowering interest rates, which, in some cases could result in negative interest rates. These actions, including their reversal or potential ineffectiveness, could further increase volatility in securities and other financial markets and reduce market liquidity. To the extent the fund has a bank deposit or holds a debt instrument with a negative interest rate to maturity, the fund would generate a negative return on that investment. Similarly, negative rates on investments by money market funds and similar cash management products could lead to losses on investments, including on investments of the fund’s uninvested cash.

Issuer risk. The value of fixed income securities may decline for a number of reasons which directly relate to the issuer, such as management performance, financial leverage, reduced demand for the issuer’s goods and services, historical and prospective earnings of the issuer and the value of the assets of the issuer. An issuer of securities held by the Fund could default or have its credit rating downgraded. These risks could adversely impact the value of the Fund’s portfolio and the Fund’s ability to achieve its investment objective.

Liquidity risk. The extent (if at all) to which a security may be sold without negatively impacting its market value may be impaired by reduced market activity or participation, legal restrictions, or other economic and market impediments. Funds with principal investment strategies that involve investments in securities of companies with smaller market capitalizations, foreign securities, or securities with substantial market and/or credit risk tend to have the greatest exposure to liquidity risk. Exposure to liquidity risk may be heightened for funds that invest in securities of emerging markets that are not widely traded, and that may be subject to purchase and sale restrictions.

The capacity of traditional dealers to engage in fixed-income trading has not kept pace with the bond market’s growth. As a result, dealer inventories of corporate bonds, which indicate the ability to “make markets,” i.e., buy or sell a security at the quoted bid and ask price, respectively, are at or near historic lows relative to market size. Because market makers provide stability to fixed-income markets, the significant reduction in dealer inventories could lead to decreased liquidity and increased volatility, which may become exacerbated during periods of economic or political stress.

Operational and cybersecurity risk. With the increased use of technologies, such as mobile devices and “cloud”-based service offerings and the dependence on the internet and computer systems to perform necessary business functions, the fund’s service providers are susceptible to operational and

| 9 |

information or cybersecurity risks that could result in losses to the fund and its shareholders. Intentional cybersecurity breaches include unauthorized access to systems, networks, or devices (such as through “hacking” activity or “phishing”); infection from computer viruses or other malicious software code; and attacks that shut down, disable, slow, or otherwise disrupt operations, business processes, or website access or functionality. Cyber-attacks can also be carried out in a manner that does not require gaining unauthorized access, such as causing denial-of-service attacks on the service providers’ systems or websites rendering them unavailable to intended users or via “ransomware” that renders the systems inoperable until appropriate actions are taken. In addition, unintentional incidents can occur, such as the inadvertent release of confidential information (possibly resulting in the violation of applicable privacy laws).

A cybersecurity breach could result in the loss or theft of customer data or funds, loss or theft of proprietary information or corporate data, physical damage to a computer or network system, or costs associated with system repairs. Such incidents could cause a fund, the advisor, a manager, or other service providers to incur regulatory penalties, reputational damage, additional compliance costs, litigation costs or financial loss. In addition, such incidents could affect issuers in which a fund invests, and thereby cause the fund’s investments to lose value.

Cyber-events have the potential to materially affect the fund and the advisor’s relationships with accounts, shareholders, clients, customers, employees, products, and service providers. The fund has established risk management systems reasonably designed to seek to reduce the risks associated with cyber-events. There is no guarantee that the fund will be able to prevent or mitigate the impact of any or all cyber-events.

The fund is exposed to operational risk arising from a number of factors, including, but not limited to, human error, processing and communication errors, errors of the fund’s service providers, counterparties, or other third parties, failed or inadequate processes and technology or system failures.

In addition, other disruptive events, including (but not limited to) natural disasters and public health crises (such as the coronavirus (COVID-19) pandemic), may adversely affect the fund’s ability to conduct business, in particular if the fund’s employees or the employees of its service providers are unable or unwilling to perform their responsibilities as a result of any such event. Even if the fund’s employees and the employees of its service providers are able to work remotely, those remote work arrangements could result in the fund’s business operations being less efficient than under normal circumstances, could lead to delays in its processing of transactions, and could increase the risk of cyber-events.

Prepayment risk. During periods of declining interest rates, borrowers may exercise their option to prepay principal earlier than scheduled. For fixed rate securities, such payments often occur during periods of declining interest rates, forcing the Fund to reinvest in lower yielding securities, resulting in a possible decline in the Fund’s income and distributions to shareholders. This is known as prepayment or “call” risk. Floating rate loans are also subject to prepayment risk. Securities subject to prepayment risk can offer less potential for gains when the credit quality of the issuer improves.

Redemption risk. Substantial redemptions of shares by the Fund’s investors within a short period of time could require the Fund to liquidate positions more rapidly than would otherwise be desirable, which could result in losses that would adversely affect the NAV of both the shares being redeemed and the remaining outstanding shares. Shares held by the Advisor, its affiliates or investment companies under their management are expected to represent a substantial portion of the Fund’s assets. The Advisor and its affiliates are not under any obligation to the Fund with respect to the amount or timing of these investments or redemption of their investments.

Reinvestment risk. Reinvestment risk is the risk that income from the Fund’s portfolio will decline if the Fund invests the proceeds from matured, traded or called fixed income securities at market interest rates that are below the Fund’s portfolio’s current earnings rate.

| 10 |

Repurchase agreements risk. The risk of a repurchase agreement transaction is limited to the ability of the seller to pay the agreed-upon sum on the delivery date. In the event of bankruptcy or other default by the seller, the instrument purchased may decline in value, interest payable on the instrument may be lost and there may be possible difficulties and delays in obtaining collateral and delays and expense in liquidating the instrument. If an issuer of a repurchase agreement fails to repurchase the underlying obligation, the loss, if any, would be the difference between the repurchase price and the underlying obligation’s market value. The fund might also incur certain costs in liquidating the underlying obligation. Moreover, if bankruptcy or other insolvency proceedings are commenced with respect to the seller, realization upon the underlying obligation might be delayed or limited.

U.S. Government Obligations. U.S. government obligations are debt securities issued or guaranteed as to principal or interest by the U.S. Treasury. These securities include treasury bills, notes and bonds.

GNMA Obligations. GNMA obligations are mortgage-backed securities guaranteed by the GNMA, which guarantee is supported by the full faith and credit of the U.S. government.

U.S. Agency Obligations. U.S. government agency obligations are debt securities issued or guaranteed as to principal or interest by an agency or instrumentality of the U.S. government pursuant to authority granted by Congress. U.S. government agency obligations include, but are not limited to:

| • | SLMA; |

| • | FHLBs; |

| • | FICBs; and |

| • | Fannie Mae. |

U.S. Instrumentality Obligations. U.S. instrumentality obligations include, but are not limited to, those issued by the Export-Import Bank and Farmers Home Administration.

Some obligations issued or guaranteed by U.S. government agencies or instrumentalities are supported by the right of the issuer to borrow from the U.S. Treasury or the Federal Reserve Banks, such as those issued by FICBs. Others, such as those issued by Fannie Mae, FHLBs and Freddie Mac, are supported by discretionary authority of the U.S. government to purchase certain obligations of the agency or instrumentality. In addition, other obligations, such as those issued by the SLMA, are supported only by the credit of the agency or instrumentality. There also are separately traded interest components of securities issued or guaranteed by the U.S. Treasury.

No assurance can be given that the U.S. government will provide financial support for the obligations of such U.S. government-sponsored agencies or instrumentalities in the future, since it is not obligated to do so by law. In this Part A, “U.S. government securities” refers not only to securities issued or guaranteed as to principal or interest by the U.S. Treasury but also to securities that are backed only by their own credit and not the full faith and credit of the U.S. government.

It is possible that the availability and the marketability (liquidity) of the securities discussed in this section could be adversely affected by actions of the U.S. government to tighten the availability of its credit. In 2008, FHFA, an agency of the U.S. government, placed Fannie Mae and Freddie Mac into conservatorship, a statutory process with the objective of returning the entities to normal business operations. The FHFA will act as the conservator to operate Fannie Mae and Freddie Mac until they are stabilized. It is unclear what effect this conservatorship will have on the securities issued or guaranteed by Fannie Mae or Freddie Mac.

(d) Portfolio Holdings

| 11 |

A description of the Fund’s policies and procedures with respect to the disclosure of the Fund’s portfolio securities is available in the Fund’s Part B.

ITEM 10. MANAGEMENT, ORGANIZATION AND CAPITAL STRUCTURE

(a)(1) Management

John Hancock Investment Management LLC serves as the Fund’s investment advisor. The Advisor’s address is 200 Berkeley Street, Boston, MA 02116.

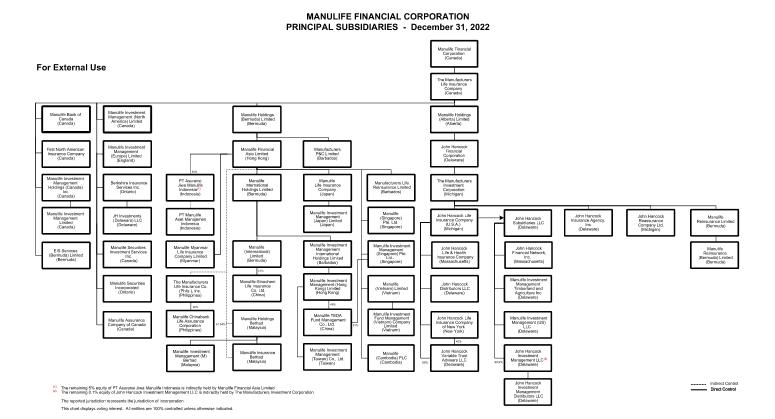

Founded in 1968, the Advisor is an indirect principally owned subsidiary of John Hancock Life Insurance Company (U.S.A.), which in turn is a subsidiary of Manulife Financial Corporation.

The Advisor’s parent company has been helping individuals and institutions work toward their financial goals since 1862. The Advisor offers investment solutions managed by leading institutional money managers, taking a disciplined team approach to portfolio management and research, leveraging the expertise of seasoned investment professionals. As of December 31, 2022, the Advisor had total assets under management of approximately $144.3 billion.

Subject to general oversight by the Board of Trustees, the Advisor manages and supervises the investment operations and business affairs of the Fund. The Advisor selects, contracts with, and compensates one or more subadvisors to manage all or a portion of the Fund’s portfolio assets, subject to oversight by the advisor. In this role, the advisor has supervisory responsibility for managing the investment and reinvestment of the Fund’s portfolio assets through proactive oversight and monitoring of the Subadvisor and the Fund, as described in further detail below. The Advisor is responsible for developing overall investment strategies for the Fund and overseeing and implementing the Fund’s continuous investment program and provides a variety of advisory oversight and investment research services. The Advisor also provides management and transition services associated with certain fund events (e.g., strategy, portfolio manager or subadvisor changes) and coordinates and oversees services provided under other agreements.

The Advisor has ultimate responsibility to oversee the Subadvisor and recommend to the Board of Trustees its hiring, termination, and replacement. In this capacity, the Advisor, among other things: (i) monitors on a daily basis the compliance of the Subadvisor with the investment objectives and related policies of the Fund; (ii) monitors significant changes that may impact the Subadvisor’s overall business and regularly performs due diligence reviews of the Subadvisor; (iii) reviews the performance of the Subadvisor; and (iv) reports periodically on such performance to the Board of Trustees. The Advisor employs a team of investment professionals who provide these ongoing research and monitoring services.

The Fund relies on an order from the Securities and Exchange Commission (“SEC”) permitting the Advisor, subject to approval by the Board of Trustees, to appoint a subadvisor or change the terms of a subadvisory agreement without obtaining shareholder approval. The Fund, therefore, is able to change subadvisors or the fees paid to a subadvisor from time to time without the expense and delays associated with obtaining shareholder approval of the change. This order does not, however, permit the Advisor to appoint a subadvisor that is an affiliate of the Advisor or the Fund (other than by reason of serving as a subadvisor to the Fund), or to increase the subadvisory fee of an affiliated subadvisor, without the approval of the shareholders.

Manulife IM (US) serves as the Fund’s subadvisor. The Subadvisor’s address is 197 Clarendon Street, Boston, MA 02116.

The Subadvisor provides investment advisory services to individual and institutional investors. Manulife IM (US) is a wholly owned subsidiary of John Hancock Life Insurance Company (U.S.A.) (a subsidiary of

| 12 |

Manulife Financial Corporation) and, as of December 31, 2022, had total assets under management of approximately $181.4 billion.

The Fund pays the Advisor a management fee for its services to the Fund. The Advisor in turn pays the fees of the Subadvisor. The management fee is stated as an annual percentage of the aggregate net assets of the Fund determined in accordance with the following schedule, and that rate is applied to the average daily net assets of the Fund.

| Average Daily Net Assets of the Fund | Fee (Annual Rate) |

| First $1.5 billion | 0.50% |

| Over $1.5 billion | 0.48% |

| A contractual management fee waiver of 0.45% is in effect until April 30, 2024. | |

During its most recent fiscal period, the Fund paid the Advisor a management fee equal to 0.04% of average daily net assets (including any waivers and/or reimbursements).

The basis for the Board of Trustees’ approval of the advisory fees, and of the investment advisory agreement, including the subadvisory agreement, is discussed in the Fund’s most recent semi-annual shareholder report for the period ended June 30.

(a)(2) Portfolio Management

Following are brief biographical profiles of the leaders of the Fund’s investment management team, in alphabetical order. These managers are jointly and primarily responsible for the day-to-day management of the Fund’s portfolio. These managers are employed by Manulife IM (US). For more details about these individuals, including information about their compensation, other accounts they manage, and any investments they may have in the Fund, see Part B.

Pearl Natalie Andrada

| • | Fixed income trader of Manulife IM (US) |

| • | Associated with the Subadvisor since 2022 |

| • | Associated with the Fund since 2022 |

| • | Began business career in 2010 |

Bridget Bruce

| ▪ | Fixed income trader of Manulife IM (US) |

| ▪ | Associated with the Subadvisor since 2009 |

| ▪ | Associated with the Fund since 2015 |

| ▪ | Began business career in 2007 |

Christopher Coccoluto

| ▪ | Senior fixed income trader of Manulife IM (US) |

| ▪ | Associated with the Subadvisor since 2010 |

| ▪ | Associated with the Fund since 2015 |

| ▪ | Began business career in 2008 |

Michael Lorizio

| ▪ | Senior fixed income trader of Manulife IM (US) |

| ▪ | Associated with the Subadvisor since 2000 |

| ▪ | Associated with the Fund since 2015 |

| ▪ | Began business career in 1999 |

James Madison

| ▪ | Fixed income trader at Manulife IM (US) |

| 13 |

| ▪ | Associated with the Subadvisor since 2015 |

| ▪ | Associated with the Fund since 2015 |

| ▪ | Began business career in 2005 |

Connor Minnaar, CFA

| ▪ | Associate Portfolio Manager of Manulife IM (US) |

| ▪ | Associated with the Subadvisor since 2006 |

| ▪ | Associated with the Fund since 2022 |

| ▪ | Began business career in 2002 |

(a)(3) Legal Proceedings

There are no legal proceedings to which the Trust or the Advisor is a party that are likely to have a material adverse effect on the Fund or the ability of the Advisor to perform its contract with the Fund.

(b) Capital Stock

Fund shares may not be transferred, but an investor may redeem all or any portion of its shares in the Fund at NAV on any day on which the New York Stock Exchange (“NYSE”) is open, subject to certain exceptions. For more information about the ability of an investor to redeem all or any portion of its investment in the Fund, please see Item 11 herein. The Fund reserves the right to issue additional shares. Investors in the Fund have no preemptive or conversion rights, and shares when issued will be fully paid and non-assessable, except as set forth below.

The Fund has no current intention to hold annual meetings of investors, except to the extent required by the 1940 Act, but will hold special meetings of investors when, in the judgment of the Trustees, it is necessary or desirable to submit matters for an investor vote. Each investor in the Fund will participate equally in accordance with its pro rata interests in the assets of the Fund. Upon liquidation of the Fund, investors would be entitled to share, in proportion to their investment in the Fund, in the assets of the Fund available for distribution to investors.

The Fund is organized as a Massachusetts business trust. Under Massachusetts law, shareholders of a Massachusetts business trust could, under certain circumstances, be held personally liable for acts or obligations of the trust. However, the Trust’s Declaration of Trust contains an express disclaimer of shareholder liability for acts, obligations and affairs of the Fund. The Trust’s Declaration of Trust also provides for indemnification out of the Fund’s assets for all losses and expenses of any shareholder held personally liable by reason of being or having been a shareholder. Furthermore, the Fund shall not be liable for the liabilities of any other John Hancock fund. Liability is therefore limited to circumstances in which the Fund itself would be unable to meet its obligations.

The Fund has entered into contractual arrangements with various parties that provide services to the Fund, which may include, among others, the Advisor and Subadvisor, as described above and in Part B. Fund shareholders are not parties to, or intended or “third-party” beneficiaries of, any of these contractual arrangements. These contractual arrangements are not intended to, nor do they, create in any individual shareholder or group of shareholders any right, either directly or on behalf of the Fund, to either: (a) enforce such contracts against the service providers; or (b) seek any remedy under such contracts against the service providers.

This Part A provides information concerning the Fund that an investor should consider in determining whether to purchase shares of the Fund. Each of this Part A, Part B, or any contract that is an exhibit to the Fund’s registration statement, is not intended to, nor does it, give rise to an agreement or contract between the Fund and any investor. Each such document also does not give rise to any contract or create rights in any individual shareholder, group of shareholders, or other person. The foregoing

| 14 |

disclosure should not be read to suggest any waiver of any rights conferred expressly by federal or state securities laws.

ITEM 11. SHAREHOLDER INFORMATION

(a) Pricing of Fund Shares

The offering price that applies to a purchase order is the next NAV calculated after the purchase order is received and accepted by the Fund or its agent. The Fund normally calculates the NAV of its shares at 4:00 p.m. Eastern Time on each day that the NYSE is open. In case of emergency or other disruption resulting in the NYSE not opening for trading or the NYSE closing at a time other than the regularly scheduled close, the NAV may be determined as of the regularly scheduled close of the NYSE pursuant to the Fund’s Valuation Policies and Procedures. The time at which shares and transactions are priced and until which orders are accepted may vary to the extent permitted by the SEC and applicable regulations. On holidays or other days when the NYSE is closed, the NAV is not calculated and the Fund does not transact purchase or redemption requests. Trading of securities that are primarily listed on foreign exchanges may take place on weekends and U.S. business holidays on which the Fund’s NAV is not calculated. Consequently, the Fund’s portfolio securities may trade and the NAV of the Fund’s shares may be significantly affected on days when a shareholder will not be able to purchase or redeem shares of the Fund.

Generally, trading in non-U.S. securities, U.S. government securities and money market instruments is substantially completed each day at various times prior to the close of trading on the NYSE. The values of such securities used in computing the NAV of the Fund’s shares are determined as of such times and are generally transmitted to the Fund prior to 4:00 p.m. Eastern Time. These prices are intended to represent the market value of the relevant security and are based on the last market price quotation in the market in which they are traded. Debt obligations are typically valued based on evaluated prices provided by an independent pricing vendor. The value of securities denominated in foreign currencies is converted into U.S. dollars at the exchange rate supplied by an independent pricing vendor.

Pricing vendors may use matrix pricing or valuation models that utilize certain inputs and assumptions to derive values, including transaction data, broker-dealer quotations, credit quality information, general market conditions, news, and other factors and assumptions. The Fund may receive different prices when it sells odd-lot positions than it would receive for sales of institutional round lot positions. Pricing vendors generally value securities assuming orderly transactions of institutional round lot sizes, but the Fund may hold or transact in such securities in smaller, odd lot sizes.

The Pricing Committee engages in oversight activities with respect to the Fund’s pricing vendors, which includes, among other things, monitoring significant or unusual price fluctuations above predetermined tolerance levels from the prior day, back-testing of pricing vendor prices against actual trades, conducting periodic due diligence meetings and reviews, and periodically reviewing the inputs, assumptions and methodologies used by these vendors. Nevertheless, market quotations, official closing prices, or information furnished by a pricing vendor could be inaccurate, which could lead to a security being valued incorrectly.

The Board has designated the Fund’s Advisor as the valuation designee to perform fair value functions for the fund in accordance with the Advisor’s valuation policies and procedures. As valuation designee, the Advisor will determine the fair value, in good faith, of securities and other assets held by the Fund for which market quotations are not readily available and, among other things, will assess and manage material risks associated with fair value determinations, select, apply and test fair value methodologies, and oversee and evaluate pricing services and other valuation agents used in valuing the Fund’s investments. The Advisor is subject to Board oversight and reports to the Board information regarding the fair valuation process and related material matters. The Advisor carries out its responsibilities as valuation designee through its Pricing Committee.

| 15 |

If market quotations or official closing prices are not readily available or are otherwise deemed unreliable because of market- or issuer-specific events, a security will be valued at its fair value as determined in good faith by the Board’s valuation designee, the Advisor. In certain instances, therefore, the Pricing Committee may determine that a reported valuation does not reflect fair value, based on additional information available or other factors, and may accordingly determine in good faith the fair value of the assets, which may differ from the reported valuation.

Fair value pricing of securities is intended to help ensure that the Fund’s NAV reflects the fair market value of the Fund’s portfolio securities as of the close of regular trading on the NYSE. However, a security’s valuation may differ depending on the method used for determining value, and no assurance can be given that fair value pricing of securities will successfully eliminate all potential opportunities for such trading gains.

The use of fair value pricing has the effect of valuing a security based upon the price the Fund might reasonably expect to receive if it sold that security in an orderly transaction between market participants, but does not guarantee that the security can be sold at the fair value price. Further, because of the inherent uncertainty and subjective nature of fair valuation, a fair valuation price may differ significantly from the value that would have been used had a readily available market price for the investment existed and these differences could be material. With respect to any portion of the Fund’s assets that is invested in another open-end investment company, that portion of the Fund’s NAV is calculated based on the NAV of that investment company. The prospectus for the other investment company explains the circumstances and effects of fair value pricing for that other investment company.

(b) Purchase of Fund Shares

Shares of the Fund are issued after the acceptance of purchase orders by the Fund or its agent solely in private placement transactions that do not involve any “public offering” within the meaning of Regulation D under the 1933 Act. Investments in the Fund may only be made by certain “accredited investors” within the meaning of Section 4(a)(2) of the 1933 Act, including other investment companies. This Part A does not constitute an offer to sell, or the solicitation of an offer to buy, any “security” within the meaning of the 1933 Act.

All investments are made at the NAV next determined after a purchase order and payment for the investment is received by the Fund or its agent by the designated cutoff time for each accredited investor. There is no minimum initial or subsequent investment in the Fund. The Fund reserves the right to stop accepting investments in the Fund at any time or to reject any investment order.

(c) Redemption of Fund Shares

An investor in the Fund may sell (redeem) some or all of its investment by submitting a redemption request to the Fund or its agent on any business day the NYSE is open for trading. Shares will be redeemed at the current NAV calculated after the order is received by the Fund or its agent. Shares redeemed will not receive distributions declared on the effective date of the redemption. The proceeds of a redemption will be paid either by Fedwire, other immediately available funds or Fund property, normally on the business day on which the shares are redeemed. Payment may be delayed for not more than seven (7) days after the receipt and acceptance of the redemption order if reasonably necessary to prevent such redemption from having a material adverse impact on the Fund or the remaining shareholders, except as otherwise permitted by the 1940 Act or as provided by the SEC. The Fund reserves the right to pay redemptions in kind. Shares of the Fund may not be transferred.

The right of any investor to receive payment with respect to any redemption may be suspended or the payment of the redemption proceeds postponed during any period in which the NYSE is closed (other than weekends or holidays) or trading on such exchange is restricted, or, to the extent otherwise

| 16 |

permitted by the 1940 Act or the SEC, if an emergency exists. In no event will the Fund or any Trustee be liable to a beneficial owner for interest on the proceeds of any redemption.

The Fund typically expects to mail or wire redemption proceeds between 1 and 3 business days following the receipt of the shareholder’s redemption request. Processing time is not dependent on the chosen delivery method. In unusual circumstances, the Fund may temporarily suspend the processing of sell requests or may postpone payment of proceeds for up to three business days or longer, as allowed by federal securities laws.

Under normal market conditions, the Fund typically expects to meet redemption requests through holdings of cash or cash equivalents or through sales of portfolio securities, and may access other available liquidity facilities. In unusual or stressed market conditions, such as, for example, during a period of time in which a foreign securities exchange is closed, in addition to the methods used in normal market conditions, the Fund may meet redemption requests through the use of its line of credit, interfund lending facility, redemptions in kind, or such other liquidity means or facilities as the Fund may have in place from time to time.

Certain Special Limitations Affecting Redemptions. The SEC has implemented a number of requirements, including liquidity fees and temporary redemption gates, for money market funds based on the amount of Fund assets that are “weekly liquid assets,” which generally includes cash, direct obligations of the U.S. government, certain other U.S. government or agency securities and securities that will mature or are subject to a demand feature that is exercisable and payable within five business days.

The Fund has adopted policies and procedures such that the Fund will be able to impose liquidity fees on redemptions and/or temporarily suspend redemptions for up to 10 business days in any 90-day period in the event that the Fund’s weekly liquid assets were to fall below a designated threshold, subject to a determination by the Fund’s Board that such a liquidity fee or redemption gate is in the Fund’s best interest. If the Fund’s weekly liquid assets fall below 30% of its total assets, the Fund may impose liquidity fees of up to 2% of the value of the shares redeemed and/or temporarily suspend redemptions, if the Board, including a majority of the independent Trustees, determines that imposing a liquidity fee or temporarily suspending redemptions is in the Fund’s best interest. If the Fund’s weekly liquid assets fall below 10% of its total assets at the end of any business day, the Fund will impose a liquidity fee of 1% on all redemptions beginning on the next business day, unless the Board, including a majority of the independent Trustees, determines that imposing such a fee would not be in the best interests of the Fund or determines that a lower or higher fee (not to exceed 2%) would be in the best interests of the Fund, which would remain in effect until weekly liquid assets return to 30% or the Board determines that the fee is no longer in the best interests of the Fund. In the event that a liquidity fee is imposed and/or redemptions are temporarily suspended, the Board may take certain other actions based on the particular facts and circumstances, including but not limited to modifying the timing and frequency of its NAV determinations. All liquidity fees payable by shareholders of the Fund would be payable to the Fund and could offset any losses realized by the Fund when seeking to honor redemption requests during times of market stress.

If liquidity fees are imposed or redemptions are temporarily suspended, the Fund will notify shareholders on the Fund’s website or by press release. In addition to identifying the Fund, such notifications will include the Fund’s percentage of total assets invested in weekly liquid assets, the time of implementation of the liquidity fee and/or redemption gate and details regarding the amount of the liquidity fee. The imposition and termination of a liquidity fee or redemption gate will also be reported by the Fund to the SEC on Form N-CR.

If redemptions are temporarily suspended, the Fund will not accept redemption orders until the Fund has notified shareholders that the redemption gate has been lifted. Shareholders wishing to redeem shares once the redemption gate has been lifted will need to submit a new redemption request to the Fund.

| 17 |

All liquidity fees payable by shareholders to the Fund can be used to offset any losses realized by the Fund when seeking to honor redemption requests during times of market stress. The Fund expects to treat such liquidity fees as not constituting income to the Fund.

A liquidity fee imposed by the Fund will reduce the amount a shareholder will receive upon the redemption of its shares and will decrease the amount of any capital gain or increase the amount of any capital loss a shareholder will recognize from such redemption. Although there is some degree of uncertainty with respect to the tax treatment of liquidity fees received by money market funds, it is anticipated at this time that a liquidity fee will have no tax effect for the Fund. As the tax treatment will likely be the subject of future guidance issued by the Internal Revenue Service (IRS), the Fund will re-visit the applicable tax treatment of liquidity fees when they are received.

In addition, the right of any investor to receive payment with respect to any redemption may be suspended or the payment of the redemption proceeds postponed during any period in which the NYSE is closed (other than weekends or holidays) or trading on the NYSE is restricted or, to the extent otherwise permitted by the 1940 Act, if an emergency exists as a result of which disposal by the Fund of securities owned by it is not reasonably practicable or it is not reasonably practicable for the Fund fairly to determine the value of its net assets. In addition, the SEC may by order permit suspension of redemptions for the protection of shareholders of the Fund.

If the Fund’s weekly liquid assets fall below 10% of its assets on a business day, the Fund may cease honoring redemptions and liquidate at the discretion of the Board, including a majority of the independent Trustees. Prior to suspending redemptions, the Fund would be required to notify the SEC of its decision to liquidate and suspend redemptions. If the Fund ceases honoring redemptions and determines to liquidate, the Fund expects that it would notify shareholders on the Fund’s website or by press release. Distributions to shareholders of liquidation proceeds may occur in one or more disbursements.

Under certain circumstances, the Fund may honor redemption orders (or pay redemptions without adding a liquidity fee to the redemption amount) if the Fund can verify that the redemption order was received in good order by the Fund before the Fund imposed liquidity fees or temporarily suspended redemptions.

(d) Dividends and Distributions

The Fund generally declares dividends daily and pays them monthly. Capital gains, if any, are typically distributed at least annually. Most of the Fund’s dividends are income dividends. Dividends begin accruing the day the Fund receives payment and continue up until the day your shares are actually redeemed. Dividends generally will be paid in cash, unless a shareholder elects to have dividends automatically reinvested in additional shares of the Fund.

(e) Frequent Purchases and Redemption of Fund Shares

The Fund does not knowingly accept shareholders who engage in “market timing” or other types of excessive short-term trading. Short-term trading into and out of the Fund can disrupt portfolio investment strategies and may increase Fund expenses for all shareholders, including long-term shareholders who do not generate these costs. However, because this Fund is intended to serve as a vehicle for cash management purposes, investors in the Fund value the ability to add and withdraw their funds quickly and without restrictions. In addition, the Fund does not offer shares of the Fund for sale to the general public. For these reasons, the Board has not adopted policies and procedures with respect to frequent purchases and redemptions of the Fund’s shares, and the Fund does not impose redemption fees or minimum holding periods on its investors.

(f) Tax Consequences

| 18 |

For investors who are not exempt from federal income taxes, dividends received from the Fund are generally considered taxable, whether received in cash or reinvested in additional shares of the Fund. Dividends from the Fund’s short-term capital gains are taxable as ordinary income. Dividends from the Fund’s long-term capital gains (if any) are taxable to individuals at a lower rate. The Fund generally does not expect to make any distributions from long-term capital gains. Whether gains are short-term or long-term depends on the Fund’s holding period. Some dividends paid in January may be taxable as if they had been paid the previous December.

Any time an investor sells shares, it may be considered a taxable event for the investor if the investor is not exempt from federal income taxes. Depending on the purchase price and the sale price of the shares sold, an investor may have a gain or a loss on the transaction. Each investor is responsible for any tax liabilities generated by its transactions.

(g) Website Posting Portfolio Holdings and Other Fund Information

Information concerning the Fund’s portfolio holdings is available via the link to the Fund at https://www.jhinvestments.com/collateral-trust. Such information is posted on the website no later than five business days after month end then remains posted on the website for six months thereafter. The Fund’s Weighted Average Maturity and Weighted Average Life, Daily and Weekly Liquid Assets and Daily Flows are posted every business day and remain posted on the website for six months thereafter.

The Fund files with the SEC a complete schedule of its portfolio holdings as of the close of each month on “Form N-MFP.” Form N-MFP is available on the SEC’s website at sec.gov. Shareholders may access Form N-MFP via the link to the Fund at https://www.jhinvestments.com/collateral-trust.

ITEM 12. DISTRIBUTION ARRANGEMENTS

(a) Sales Loads.

Not applicable.

(b) Rule 12b-1 Fees

Not applicable.

(c) Multiple Class and Master-Feeder Funds

Not applicable.

| 19 |

JOHN HANCOCK COLLATERAL TRUST

PART B

Dated: April 26, 2023

This Part B provides information about John Hancock Collateral Trust (the “Fund”), a series of John Hancock Collateral Trust (the “Trust”), in addition to the information that is contained in the Fund’s Part A. This Part B is not a prospectus. It should be read in conjunction with the prospectus in Part A, dated April 26, 2023. Unless otherwise stated, capitalized terms in this Part B have the same meaning as in Part A. Eligible Investors may obtain a copy of Part A free of charge by contacting John Hancock Signature Services, Inc. at P.O. Box 219909, Kansas City, MO 64121-9909.

NEITHER PART A NOR THIS PART B CONSTITUTES AN OFFER TO SELL, OR THE SOLICITATION OF AN OFFER TO BUY, ANY INTERESTS IN THE FUND.

The Fund was organized as a Massachusetts business trust on December 4, 2014, under the laws of the Commonwealth of Massachusetts

| 20 |

ITEM 16. DESCRIPTION OF THE FUND AND ITS INVESTMENTS AND RISKS

(a) Classification

The Fund is a diversified, open-end, management investment company.

(b) Investment Strategies and Risks

The following information supplements the discussion of the Fund’s investment objective and policies discussed in the Part A.

The Fund’s investment objective is to seek current income, while maintaining adequate liquidity, safeguarding the return of principal and minimizing risk of default. The Fund invests in high quality money market instruments. The Fund’s investments will be subject to the market fluctuation and risks inherent in all securities. There is no assurance that the Fund will achieve its investment objective.

The Fund seeks to achieve its objective by investing in money market instruments including, but not limited to, U.S. government, municipal and foreign governmental securities; obligations of international organizations (e.g., the World Bank and the International Monetary Fund); obligations of U.S. and foreign banks and other lending institutions; corporate obligations; repurchase agreements and reverse repurchase agreements. All of the Fund’s investments will be denominated in U.S. dollars.

Under Rule 2a-7, the Fund may generally invest in “eligible securities” which include securities issued by another money market fund, government securities or securities that have a remaining maturity of no more than 397 calendar days and are determined by the Fund’s board or its delegate to present minimal credit risk based on an assessment of the issuer’s credit quality, including the capacity of the issuer or guarantor to meet its financial obligations. The Fund’s Board has adopted procedures by which the Adviser will conduct this initial and ongoing assessment, as required.

At the time the Fund acquires its investments, such “eligible securities” will be rated (or issued by an issuer that is rated with respect to a comparable class of short-term debt obligations) in one of the two highest rating categories for short-term debt obligations assigned by at least two of the following nationally recognized statistical rating organizations (“NRSROs”) (or one NRSRO if the obligation was rated by only that NRSRO): S&P Global Ratings (“S&P”), Moody’s Investors Service, Inc. (“Moody’s”), and Fitch Ratings (“Fitch”).