QUEENSLAND TREASURY

2022–23

Report on State Finances

of the Queensland Government – 30 June 2023

Incorporating the Outcomes Report and

the AASB 1049 Financial Statements

EXHIBIT (c)(xiv)

Government of Queensland’s Consolidated Financial Statements for the Year Ended June 30, 2023

FORWARD-LOOKING STATEMENTS

This exhibit contains forward-looking statements. Statements that are not historical facts, including statements about the State of Queensland’s (the “State” or “Queensland”) beliefs and expectations, are forward-looking statements. These statements are based on current plans, budgets, estimates and projections and therefore you should not place undue reliance on them. The words “believe”, “may”, “will”, “should”, “estimate”, “continue”, “anticipate”, “intend”, “expect”, “forecast” and similar words are intended to identify forward-looking statements. Forward-looking statements speak only as of the date they are made, and neither the Queensland Treasury Corporation nor the State undertake any obligation to update publicly any of them in light of new information or future events.

Forward-looking statements are based on current plans, estimates and projections and, therefore, undue reliance should not be placed on them. Although the Queensland Treasury Corporation and the State believe that the beliefs and expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such beliefs and expectations will prove to have been correct. Forward-looking statements involve inherent risks and uncertainties. We caution you that actual results may differ materially from those contained in any forward-looking statements.

A number of important factors could cause actual results to differ materially from those expressed in any forward-looking statement. Factors that could cause the actual outcomes to differ materially from those expressed or implied in forward-looking statements include:

| • | the international and Australian economies, and in particular the rates of growth (or contraction) of the State’s major trading partners; |

| • | the effects, both internationally and in Australia, of any subsequent economic downturn, as well as the effect of ongoing economic, banking and sovereign debt risk; |

| • | the effect of natural disasters, epidemics and geopolitical events, such as the novel coronavirus (COVID-19) pandemic, the Russia-Ukraine conflict and the Israel-Hamas conflict; |

| • | increases or decreases in international and Australian domestic interest rates; |

| • | changes in and increased volatility in currency exchange rates; |

| • | changes in the State’s domestic consumption; |

| • | changes in the State’s labor force participation and productivity; |

| • | downgrades in the credit ratings of the State and Australia; |

| • | changes in the rate of inflation in the State; |

| • | changes in environmental and other regulation; and |

| • | changes in the distribution of revenue from the Commonwealth of Australia Government to the State. |

(c)(xiv)-1

QUEENSLAND TREASURY

2022–23

Report on State Finances

of the Queensland Government – 30 June 2023

Incorporating the Outcomes Report and

the AASB 1049 Financial Statements

Contents

| Page | ||||

| Message from the Treasurer |

2 | |||

| Outcomes Report - Uniform Presentation Framework |

||||

| Overview and Analysis |

3 - 1 | |||

| Operating Statement by Sector |

3 - 8 | |||

| Balance Sheet by Sector |

3 - 9 | |||

| Cash Flow Statement by Sector |

3 - 10 | |||

| General Government Sector Taxes |

3 - 11 | |||

| General Government Sector Dividend and Income Tax Equivalent Income |

3 - 11 | |||

| General Government Sector Grants Revenue |

3 - 12 | |||

| General Government Sector Grants Expenses |

3 - 12 | |||

| General Government Sector Expenses by Function |

3 - 13 | |||

| General Government Sector Purchases of Non-financial Assets by Function |

3 - 14 | |||

| Certification of Outcomes Report |

3 - 15 | |||

| AASB 1049 Financial Statements |

||||

| Overview and Analysis |

4 - 1 | |||

| Audited Financial Statements |

||||

| Operating Statement |

5 - 1 | |||

| Balance Sheet |

5 - 2 | |||

| Statement of Changes in Equity (Net Worth) |

5 - 3 | |||

| Cash Flow Statement |

5 - 5 | |||

| Notes to the Financial Statements |

5 - 7 | |||

| Certification of Queensland State Government Financial Statements |

5 - 92 | |||

| Independent Auditor’s Report to the Treasurer of Queensland |

5 - 93 | |||

| Report on State Finances 2022–23 – Queensland Government | 1 |

Message from the Treasurer

I present Queensland’s 2022-23 Report on State Finances which includes the Outcomes Report and AASB 1049 Financial Statements.

The Queensland economy has continued to grow in 2022-23 despite rising interest rates, inflationary pressures, and temporary domestic and international supply chain constraints.

The strength of the Queensland economy, including the state’s labour market performance, combined with exceptionally high prices received by the state’s coal producers have resulted in Queensland delivering an operating surplus of $13.93 billion in 2022-23. This record surplus is $1.625 billion higher than the $12.305 billion surplus estimated in the 2023-24 Budget mainly due to the Australian Government bringing forward funding from later years.

The record surplus provides Queensland with the capacity to deliver substantial cost-of-living measures support for Queensland families and businesses, while also supporting the state’s record capital program over the next four years.

The Outcomes Report

The Outcomes Report contains financial statements that are presented in accordance with the Uniform Presentation Framework (UPF) which provides comparable reporting of Commonwealth, State and Territory Governments’ financial information.

Queensland’s annual Budget was prepared in accordance with the UPF. The Outcomes Report compares the 2022-23 actual results with the revised forecasts contained in the 2023-24 Budget papers.

The UPF presentation is structured on a sectoral basis with a focus on the General Government and Public Non-financial Corporations Sectors.

AASB 1049 Financial Statements

The AASB 1049 Financial Statements outline the operations of the Queensland Government in accordance with Australian Accounting Standard AASB 1049 Whole of Government and General Government Sector Financial Reporting and other applicable standards and are audited.

These statements focus on the General Government Sector (GGS) and Total State Sector (TSS) and include detailed notes.

The statements include comparatives for the 2021-22 year, as well as analysis of variances between the published 2022-23 Budget and the 2022-23 outcome.

AASB 1049 aims to harmonise the Government Finance Statistics (GFS) and Accounting Standard frameworks. The GFS reporting framework, developed by the Australian Bureau of Statistics (ABS), is based on international statistical standards and allows comprehensive assessments to be made of the economic impact of government.

I note the assurances of Treasury officials that both the Outcomes Report and the audited financial statements are presented on a true and fair basis and that the independent auditor’s report is unqualified.

In endorsing this report, I place on record my appreciation of the professionalism and co-operation extended to Queensland Treasury by agency personnel and of the Treasury staff involved in its preparation.

The Honourable Cameron Dick MP

Treasurer

Minister for Trade and Investment

Related Publications

This report complements other key publications relating to the financial performance of the Queensland Public Sector including:

| – | the annual Budget papers; |

| – | the Treasurer’s Consolidated Fund Financial Report; |

| – | the annual reports of the various departments, statutory bodies, Government-owned corporations and other entities that comprise the Queensland Government; and |

| – | the Queensland Sustainability Report. |

| 2 | Report on State Finances 2022–23 – Queensland Government |

Outcomes Report

QUEENSLAND TREASURY

2022–2023

Outcomes Report

Uniform Presentation Framework of the

Queensland Government – 30 June 2023

Outcomes Report - Overview and Analysis

Overview

Queensland’s strong economic performance and continued exceptionally high commodity prices have resulted in a substantial improvement in the State’s fiscal position in 2022-23 compared to the original 2022-23 Budget forecasts.

The General Government Sector (GGS) realised a Uniform Presentation Framework (UPF) net operating surplus of $13.93 billion for 2022-23. This is the largest surplus in Queensland’s history and follows the previous record surplus of $4.284 billion (restated) in 2021-22.

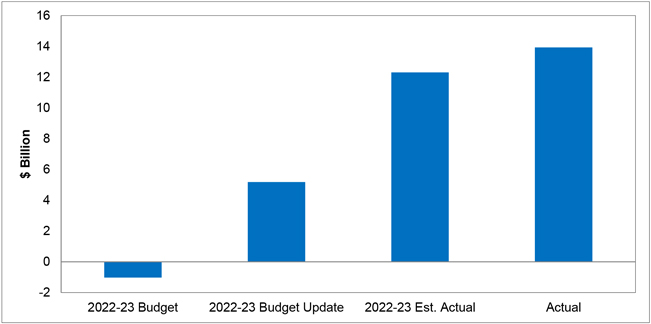

The 2022-23 operating surplus was an improvement of $1.625 billion compared to the estimated operating surplus of $12.305 billion reported in the 2023-24 Budget, and a substantial turnaround relative to the original 2022-23 Budget operating deficit estimate of $1.029 billion. Refer Chart 3.1.

The record surplus in 2022-23 reflects higher royalty revenue, driven by higher coal prices and new progressive coal royalty tiers, and strong labour market performance. The stronger revenue performance in 2022-23 has resulted in lower borrowings, enabling restoration of fiscal buffers to respond to future external shocks and build capacity for the State’s transformative capital program.

The $1.625 billion increase in net operating balance since the 2023-24 Budget is primarily due to the Australian Government providing advance payments under the Disaster Recovery Financial Arrangements (DRFA) and Social Housing Accelerator program in 2022-23.

Chart 3.1: 2022-23 General Government Sector UPF net operating balance compared to budget forecasts

Source: 2022-23 and 2023-24 Queensland State Budgets, 2022-23 Budget Update and 2022-23 Queensland Report on State Finances

In 2022-23, GGS revenue totalled $89.81 billion, up $2.187 billion on the 2023-24 Budget estimated actual revenue of $87.623 billion. The increase in revenue primarily reflects the Australian Government’s decision in late June 2023 to make advance payments of Financial Assistance Grants (FAGs), DRFA payments and Social Housing Accelerator program grants.

Higher GGS expenses partly offset the improved revenue in 2022-23. GGS expenses totalled $75.88 billion in 2022-23, $563 million higher than the 2023-24 Budget estimated actual. The higher expenses largely reflect the on-passing to local councils of the advance payment of FAGs from the Australian Government.

| Report on State Finances 2022–23 – Queensland Government | 3-1 |

Outcomes Report - Overview and Analysis

Overview continued

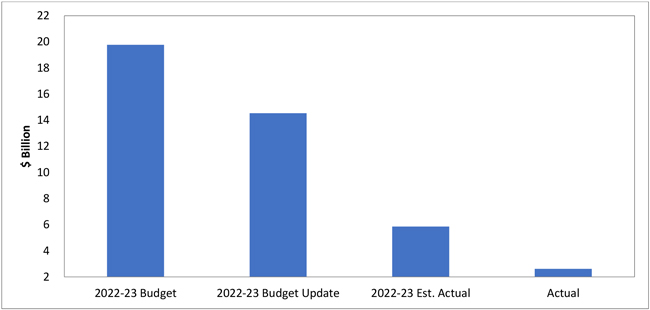

GGS net debt in 2022-23 is $2.615 billion, a $3.237 billion improvement since the 2023-24 Budget. Refer Chart 3.2.

Chart 3.2: 2022-23 General Government Sector net debt compared to budget forecasts

Source: 2022-23 and 2023-24 Queensland State Budgets, 2022-23 Budget Update and 2022-23 Queensland Report on State Finances

Higher than estimated net operating cash flows, partly as a result of advance grant payments from the Australian Government, contribute toward the lower net debt outcome in 2022-23. Better than expected market valuation of investments, loans and placements also contributed to lower net debt. These movements were partly offset by higher purchases of non-financial assets.

Net debt has improved significantly since the original 2022-23 Budget forecast of $19.772 billion as the government has used stronger royalty revenue to reduce borrowing requirements and set aside investments for future regional infrastructure. GGS net debt has declined for a third consecutive year, demonstrating the broad strength of the Queensland economy following the Government’s health response and recovery measures to the COVID-19 pandemic in 2019-20.

As at 30 June 2023, GGS borrowing totalled $53.726 billion, $967 million lower than the 2023-24 Budget estimated actual. Lower borrowing were largely due to the improved net cash inflows from operating activities, partly offset by modestly higher than expected purchases of non-financial assets.

Non-financial Public Sector (NFPS) borrowing as at 30 June 2023 was $102.821 billion, marginally higher than estimated actual in the 2023-24 Budget. Higher NFPS borrowing reflects a market value adjustment to derivatives held by energy Government-owned corporations (GOCs) to hedge movements in electricity prices, offset in part by lower GGS borrowing.

NFPS net debt is $42.848 billion as at 30 June 2023, a $2.801 billion improvement on the 2023-24 estimated actual projection. This improvement is predominantly due to the better than expected GGS net debt outcome.

Fiscal principles

In the 2021-22 Queensland Budget, the Government set out its medium-term strategy for fiscal recovery, including a new Charter of Fiscal Responsibility. The aim of the Charter is to guide Budget strategy in the medium term in response to the fiscal challenges brought on by the COVID-19 pandemic. The Charter includes Fiscal Principles to support the delivery of net operating surpluses and the stabilisation of net debt.

Principle 1 – Stabilise the General Government Sector net debt to revenue ratio at sustainable levels in the medium term, and target reductions in the net debt to revenue ratio in the long term.

Net debt is a key fiscal measure of the overall strength of the State’s fiscal position and the net debt to revenue ratio indicates the Government’s ability to service this debt.

| 3-2 | Report on State Finances 2022–23 – Queensland Government |

Outcomes Report - Overview and Analysis

Fiscal principles continued

Like other Australian jurisdictions, Queensland’s strong public health response to the COVID-19 virus and its decision to prioritise economic recovery resulted in an increase in gross borrowings and net debt, particularly in 2019-20. The Government is focused on stabilising net debt in the medium term by restoring operating surpluses, as per Fiscal Principle 2.

Queensland’s net debt to revenue ratio was 3 per cent in 2022-23, a reduction from the 15 per cent ratio reported in the 2021-22 Outcome. The continued revenue strength in 2022-23 has resulted in a consecutive year reduction in the GGS net debt to revenue ratio and reflects the Government’s prudent management of short term revenue uplifts to restore fiscal buffers and provide capacity to invest in transformative infrastructure.

Principle 2 – Ensure that average annual growth in General Government Sector expenditure in the medium term is below the average annual growth in General Government Sector revenue to deliver fiscally sustainable net operating surpluses.

Fiscal Principle 2 is designed to provide a broad measure of expenditure growth management. Delivering operating surpluses will assist debt stabilisation.

Queensland’s net operating balance has improved substantially since the 2022-23 Budget, from an operating deficit of $1.029 billion to an operating surplus of $13.93 billion. This historical surplus follows the previous record surplus of $4.284 billion (restated) in 2021-22.

In 2022-23, revenues grew by 21.1 per cent and expenses by 8.6 per cent compared to 2021-22. Adjusting revenue for the extraordinary uplift from royalty revenue driven by high commodity prices over the last 2 years, revenue growth was 9.7 per cent, over 1 per cent higher than expenses growth in 2022-23.

Principle 3 – Target continual improvements in net operating surpluses to ensure that, in the medium term, net cash flows from investments in non-financial assets (capital) will be funded primarily from net cash inflows from operating activities. The capital program will focus on supporting a productive economy, jobs and ensuring a pipeline of infrastructure that responds to population growth.

In 2022-23, GGS net cash flows from operating activities of $19.885 billion were more than double the GGS net cash flows from investments in non-financial assets of $9.718 billion, enabling lower borrowings in the short term to provide capacity for the state’s future capital program.

The capital program includes purchases of non-financial assets, capital grants and new finance leases and similar arrangements. The capital program delivered by the State Non-financial Sector in 2022-23 was $17.561 billion, $559 million, or 3.5 per cent higher than the estimated actual forecast in the 2023-24 Budget.

The Government announced in the 2023-24 Budget, the biggest infrastructure build ever undertaken by the State with a capital program of $88.729 billion planned over the next 4 years to 2026-27. The expanded infrastructure program will focus on delivering increased health system capacity, decarbonisation of the state’s energy system, improving water security and preparing for the Brisbane 2032 Olympic and Paralympic Games.

Principle 4 – Maintain competitive taxation by ensuring that, on a per capita basis, Queensland has lower taxation than the average of other states.

The fiscal principles will ensure that Queenslanders continue to pay less tax than Australians in other states and territories, providing a meaningful indication of the comparative impact of Queensland’s tax regime and policies.

At the time of the 2023-24 Budget, Queensland’s taxation per capita was $720 less than the average of other jurisdictions in 2021-22 (latest available data).

Principle 5 – Target full funding of long term liabilities such as superannuation and WorkCover in accordance with actuarial advice

Consistent with the long-standing practice of successive governments, the Queensland Government is committed to ensuring that the State sets aside assets, on an actuarially determined basis, to meet long term liabilities such as superannuation and WorkCover. The latest full actuarial review of the QSuper scheme was as at 30 June 2021 and was published in a report dated 3 December 2021. The report found the scheme to be fully funded. The next triennial review will report on the funding status of the scheme as at 30 June 2024.

As at 30 June 2023, WorkCover Queensland was fully funded.

| Report on State Finances 2022–23 – Queensland Government | 3-3 |

Outcomes Report - Overview and Analysis

Key UPF Financial Aggregates

Outlined in the table below are the key aggregates, by sector for 2022-23. The actual outcome for 2022-23 is compared to the estimated actual per the 2023-24 Budget.

| General Government Sector |

Public Non-financial Corporations Sector |

Non-financial

Public Sector | ||||||||||||||||||||

| Est. Actual | Outcome | Est. Actual | Outcome | Est. Actual | Outcome | |||||||||||||||||

| $ million | $ million | $ million | $ million | $ million | $ million | |||||||||||||||||

| Revenue |

87,623 | 89,810 | 15,835 | 16,270 | 98,403 | 100,821 | ||||||||||||||||

| Expenses |

75,317 | 75,880 | 14,887 | 15,222 | 85,660 | 86,341 | ||||||||||||||||

| Net operating balance |

12,305 | 13,930 | 948 | 1,048 | 12,743 | 14,480 | ||||||||||||||||

| Capital purchases |

9,194 | 9,899 | 4,489 | 4,497 | 13,601 | 14,300 | ||||||||||||||||

| Fiscal balance |

6,786 | 8,092 | (824 | ) | (904 | ) | 5,533 | 6,786 | ||||||||||||||

| Borrowing with QTC |

47,014 | 46,166 | 43,074 | 43,276 | 90,088 | 89,442 | ||||||||||||||||

| Leases and similar arrangements |

7,586 | 7,519 | 354 | 367 | 7,941 | 7,887 | ||||||||||||||||

| Securities and derivatives |

93 | 41 | 4,447 | 5,458 | 4,533 | 5,491 | ||||||||||||||||

| Borrowings |

54,693 | 53,726 | 47,875 | 49,101 | 102,561 | 102,821 | ||||||||||||||||

| Net Debt |

5,852 | 2,615 | 39,804 | 40,240 | 45,649 | 42,848 | ||||||||||||||||

| Notes: |

||||||||||||||||||||||

|

1. Numbers may not add due to rounding. 2. Non-financial Public Sector consolidates the General Government and Public Non-financial Corporations Sectors and excludes inter-sector transactions and balances. | ||||||||||||||||||||||

General Government Sector

Revenue

| 2022-23 | 2022-23 | |||||||||

| General Government Revenue | Est. Actual | Outcome | ||||||||

| $ million | $ million | |||||||||

| Taxation revenue |

20,563 | 20,601 | ||||||||

| Grants revenue |

36,571 | 38,335 | ||||||||

| Sales of goods and services |

6,344 | 6,483 | ||||||||

| Interest income |

3,166 | 3,226 | ||||||||

| Dividend and income tax equivalent income |

1,043 | 1,007 | ||||||||

| Other revenue |

19,937 | 20,160 | ||||||||

| Total Revenue |

87,623 | 89,810 | ||||||||

| Note: |

||||||||||

|

1. Numbers may not add due to rounding. | ||||||||||

General Government revenue totalled $89.81 billion in 2022-23, up $2.187 billion or 2.5 per cent compared to the 2023-24 Budget estimated actual projection of $87.623 billion.

The increase in revenue since the 2023-24 Budget was in large part due to the Australian Government making grant payments in advance in 2022-23. Grants revenue was $1.764 billion higher than the 2023-24 Budget estimated actual forecast. Grants revenue received in advance included $758 million DRFA grants, representing around 40 per cent of DRFA payments budgeted to be received in 2023-24, $620 million in Financial Assistance Grants (FAGs) brought forward in full from the 2023-24 financial year and $398 million in up-front funding for the Social Housing Accelerator program. National Health Reform grant funding was also higher than forecast, however, this was largely offset by lower GST revenue and the timing of infrastructure grants.

Better than expected sales revenue, interest income and other revenue, including modestly higher royalty revenue, also contributed towards higher than forecast revenue compared to the estimated actual forecast.

| 3-4 | Report on State Finances 2022–23 – Queensland Government |

Outcomes Report - Overview and Analysis

Key UPF Financial Aggregates continued

General Government Sector continued

Expenses

| 2022-23 | 2022-23 | |||||||||||

| General Government Expenses | Est. Actual | Outcome | ||||||||||

| $ million | $ million | |||||||||||

| Employee expenses |

30,279 | 30,557 | ||||||||||

| Superannuation expenses |

||||||||||||

| Superannuation interest cost |

775 | 776 | ||||||||||

| Other superannuation expenses |

3,733 | 3,756 | ||||||||||

| Other operating expenses |

20,287 | 20,014 | ||||||||||

| Depreciation and amortisation |

4,910 | 5,018 | ||||||||||

| Other interest expenses |

1,715 | 1,688 | ||||||||||

| Grants expenses |

13,618 | 14,072 | ||||||||||

| Total Expenses |

75,317 | 75,880 | ||||||||||

| Note: |

||||||||||||

|

1. Numbers may not add due to rounding. |

| |||||||||||

Total GGS expenses for 2022-23 were $563 million or 0.7 per cent higher than expected in the 2023-24 Budget.

The higher expenses largely reflect the on-passing to local councils of the advance payment of FAGs from the Australian Government.

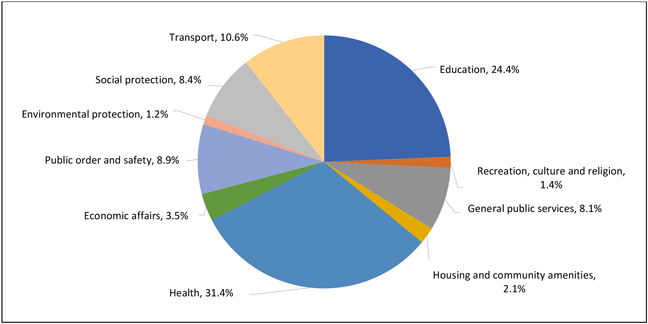

GGS expenditure is focused on the delivery of core services to the community. As shown in Chart 3.3 below, education and health account for over half of the total expenses, consistent with their share in other jurisdictions.

Chart 3.3: 2022-23 General Government Sector expenses by function 1

| 1 | Refer to page 3-13 for further detail of expenses in each function. |

| Report on State Finances 2022–23 – Queensland Government | 3-5 |

Outcomes Report - Overview and Analysis

Key UPF Financial Aggregates continued

General Government Sector continued

Net Operating Balance

The net operating balance is the net of revenue and expenses from transactions and was an operating surplus of $13.93 billion for 2022-23. The 2022-23 outcome was a $1.625 billion increase on the $12.305 billion operating surplus forecast at the time of the 2023-24 Budget. Revenue was $2.187 billion higher and expenses were $563 million higher, for the reasons discussed above.

Capital Purchases

GGS purchases of non-financial assets are the actual cash outlays per the Cash Flow Statement and totalled $9.899 billion, which was $705 million higher than the 2022-23 estimated actual. Reclassification of $245 million capital expenditure from acquisitions of non-financial assets under new finance leases to purchases of non-financial assets partly were partly a factor for the increase compared to the estimated actual projection. The net increase in capital expenditure of $459 million was due to higher than expected activity in the final quarter.

Fiscal Balance

The fiscal balance measure broadly shows how much of the acquisition of non-financial assets is financed by the net operating balance (excluding depreciation) and how much by borrowing.

The fiscal surplus of $8.092 billion for 2022-23 was $1.306 billion higher than the estimated actual projection of an $6.786 billion surplus. The larger than forecast fiscal surplus is mainly due to the improved net operating surplus, offset in part by higher than expected net acquisition of non-financial assets.

Borrowing

Borrowing was $53.726 billion, compared to the 2023-24 Budget projection of $54.693 billion, a decrease of $967 million. The lower balance partly reflects the increase in cash flows from operating activities offset in part by higher capital purchases. Not all of the improved net operating cash flows, net of higher capital purchases, flows through as a corresponding decrease in borrowings, as some of the additional net cash inflows were retained as cash balance at year end.

Net Worth

The GGS net worth was $303.973 billion as at 30 June 2023, $34.763 billion higher than the estimated actual included in the 2023-24 Budget. The increase is predominantly due to upward valuations of roads infrastructure, land under roads, school buildings and public housing.

Net Debt

Net debt is defined as the sum of particular financial liabilities: deposits held, advances received and borrowings less particular assets: cash and deposits, advances paid and investments, loans and placements. Financial liabilities exceeded financial assets in the GGS by $2.615 billion at 30 June 2023, a $3.237 billion reduction in net debt from the 2023-24 Budget estimate of $5.852 billion.

Net debt has decreased since the 2023-24 Budget due to lower borrowings and higher cash balances from the improved net cash flows from operating activities partly offset by modestly higher capital purchases. Better than expected market valuations of investments, loans and placements also contributed to the improved net debt metric.

Operating Result

The operating result measures the outcome for the State under the Accounting Standards framework, rather than the GFS framework. The GGS operating result of $14.128 billion differs from the net operating balance as it includes valuation adjustments, such as gains and losses on financial and non-financial assets. The operating result has improved $2.408 billion since the 2023-24 Budget reflecting the increased net operating surplus, better than expected market value adjustments to investments, loans and placements, and downward actuarial adjustments of the government’s self insurance liabilities, offset in part by the increase in the actuarial valuations of the Long Service Leave Central Scheme.

Comprehensive Result - Total Change in Net Worth

The comprehensive result includes the revaluation of assets taken to reserves and actuarial adjustments to defined benefit superannuation liabilities.

The comprehensive result for 2022-23 was $54.349 billion, an increase of $34.762 billion from the 2022-23 estimated actual forecast. The increase in the actual comprehensive result is mainly due to significant upward valuations of non-financial assets.

| 3-6 | Report on State Finances 2022–23 – Queensland Government |

Outcomes Report - Overview and Analysis

Key UPF Financial Aggregates continued

Public Non-financial Corporations (PNFC) Sector

The Public Non-financial Corporations Sector comprises bodies such as Government-owned corporations (GOCs) that mainly engage in the production of goods and services (of a non-financial nature) for sale in the market place at prices that aim to recover most of the costs involved.

| – | The PNFC Sector recorded a net operating surplus of $1.048 billion, $100 million higher than the 2023-24 Budget forecast. |

| – | The fiscal balance was a deficit of $904 million, compared to an estimated 2022-23 deficit of $824 million. The modest increase in fiscal deficit is due to higher net acquisitions of non-financial assets of $180 million exceeding the relative improvement in net operating balance. |

| – | PNFC borrowing with Queensland Treasury Corporation (QTC) was $202 million higher than budgeted due to the slight deterioration in net cash flows from operating activities. Securities and derivative liabilities were $5.458 billion at year end, $1.011 billion higher compared to the 2022-23 estimated actual projection. Higher securities and derivatives were primarily driven by market value movements in the value of electricity hedging contracts held by the generator GOCs. |

| – | Net debt for the PNFC sector was $40.24 billion, $436 million higher than the 2023-24 Budget estimated actual forecast. Net debt has increased since the 2023-24 Budget partly due to higher borrowing with QTC resulting from lower than projected net cash flows from operating activities. The impact of higher derivative liabilities were to a large extent negated by the associated increase in electricity derivative assets, minimising the impact to the PNFC net debt metric. |

State Financial Sector (SFS)

The State Financial Sector is the GFS terminology used for the consolidation of all State Government departments and other General Government entities, Public Non-financial Corporations, Public Financial Corporations and their controlled entities. The equivalent term for SFS used in the AASB 1049 section of this report is Total State Sector. All material inter-entity and intra-entity transactions and balances have been eliminated to the extent practicable.

| – | The net operating balance for 2022-23 was a surplus of $11.098 billion. |

| – | Purchases of non-financial assets for the SFS were $14.309 billion. |

| – | The SFS net worth was $311.514 billion, an increase of $55.842 billion compared to that published in the 2021-22 Outcomes Report. This was mainly due to non-financial asset revaluations and operating result achieved in 2022–23. |

| Report on State Finances 2022–23 – Queensland Government | 3-7 |

2022 - 23 Operating Statement by Sector ($ million)

| General

Government

|

Public

Non-financial

|

Non-financial Public Sector (b)

|

Public

|

State

|

||||||||||||||||||||||||||||||

| Est. Actual | Outcome | Est. Actual | Outcome | Est. Actual | Outcome | Outcome (c) | Outcome (c) | |||||||||||||||||||||||||||

| Revenue from Transactions |

||||||||||||||||||||||||||||||||||

| Taxation revenue |

20,563 | 20,601 | - | - | 20,190 | 20,189 | - | 20,051 | ||||||||||||||||||||||||||

| Grants revenue |

36,571 | 38,335 | 867 | 912 | 36,592 | 38,352 | - | 38,233 | ||||||||||||||||||||||||||

| Sales of goods and services |

6,344 | 6,483 | 14,314 | 14,735 | 17,719 | 18,161 | 3,140 | 20,838 | ||||||||||||||||||||||||||

| Interest income |

3,166 | 3,226 | 92 | 117 | 3,238 | 3,312 | 4,355 | 2,184 | ||||||||||||||||||||||||||

| Dividend and income tax equivalent income |

1,043 | 1,007 | - | - | 167 | 164 | - | - | ||||||||||||||||||||||||||

| Other revenue |

19,937 | 20,160 | 562 | 506 | 20,497 | 20,644 | 144 | 20,778 | ||||||||||||||||||||||||||

| Total Revenue from Transactions |

87,623 | 89,810 | 15,835 | 16,270 | 98,403 | 100,821 | 7,639 | 102,084 | ||||||||||||||||||||||||||

| Expenses from Transactions |

||||||||||||||||||||||||||||||||||

| Employee expenses |

30,279 | 30,557 | 2,491 | 2,532 | 32,623 | 32,925 | 453 | 32,988 | ||||||||||||||||||||||||||

| Superannuation expenses |

||||||||||||||||||||||||||||||||||

| Superannuation interest cost |

775 | 776 | - | (17 | ) | 775 | 759 | - | 759 | |||||||||||||||||||||||||

| Other superannuation expenses |

3,733 | 3,756 | 290 | 308 | 4,024 | 4,063 | 29 | 4,092 | ||||||||||||||||||||||||||

| Other operating expenses |

20,287 | 20,014 | 7,087 | 7,608 | 24,427 | 24,544 | 2,934 | 27,468 | ||||||||||||||||||||||||||

| Depreciation and amortisation |

4,910 | 5,018 | 2,945 | 2,720 | 7,855 | 7,737 | 23 | 7,760 | ||||||||||||||||||||||||||

| Other interest expenses |

1,715 | 1,688 | 1,679 | 1,675 | 3,159 | 3,107 | 7,300 | 4,712 | ||||||||||||||||||||||||||

| Grants expenses |

13,618 | 14,072 | 25 | 29 | 12,798 | 13,206 | 119 | 13,206 | ||||||||||||||||||||||||||

| Other property expenses |

- | - | 369 | 369 | - | - | 56 | - | ||||||||||||||||||||||||||

| Total Expenses from Transactions

|

|

75,317

|

|

|

75,880

|

|

|

14,887

|

|

|

15,222

|

|

|

85,660

|

|

|

86,341

|

|

|

10,913

|

|

|

90,986

|

| ||||||||||

| Net Operating Balance |

12,305 | 13,930 | 948 | 1,048 | 12,743 | 14,480 | (3,274 | ) | 11,098 | |||||||||||||||||||||||||

| Other economic flows - included in operating result |

(585 | ) | 198 | (594 | ) | (574 | ) | (1,339 | ) | (466 | ) | 4,024 | 5,052 | |||||||||||||||||||||

| Operating Result |

11,720 | 14,128 | 355 | 474 | 11,404 | 14,014 | 750 | 16,150 | ||||||||||||||||||||||||||

| Other economic flows - other movements in equity |

7,866 | 40,221 | 3,711 | 3,316 | 8,181 | 40,333 | (108 | ) | 39,692 | |||||||||||||||||||||||||

| Comprehensive Result - Total Change in Net Worth (d) |

19,587 | 54,349 | 4,065 | 3,790 | 19,585 | 54,347 | 643 | 55,842 | ||||||||||||||||||||||||||

| KEY FISCAL AGGREGATES |

||||||||||||||||||||||||||||||||||

| Net Operating Balance |

12,305 | 13,930 | 948 | 1,048 | 12,743 | 14,480 | (3,274 | ) | 11,098 | |||||||||||||||||||||||||

| Net Acquisition/(Disposal) of Non-financial Assets |

||||||||||||||||||||||||||||||||||

| Purchases of non-financial assets |

9,194 | 9,899 | 4,489 | 4,497 | 13,601 | 14,300 | 9 | 14,309 | ||||||||||||||||||||||||||

| Less |

Sales of non-financial assets | 104 | 181 | 38 | 63 | 142 | 243 | - | 243 | |||||||||||||||||||||||||

| Less |

Depreciation | 4,910 | 5,018 | 2,945 | 2,720 | 7,855 | 7,737 | 23 | 7,760 | |||||||||||||||||||||||||

| Plus |

Change in inventories | 65 | 79 | 169 | 129 | 234 | 208 | - | 208 | |||||||||||||||||||||||||

| Plus |

Other movements in non-financial assets | 1,275 | 1,058 | 97 | 108 | 1,371 | 1,167 | 2 | 1,169 | |||||||||||||||||||||||||

| Equals |

Total Net Acquisition of Non-financial Assets | 5,520 | 5,838 | 1,772 | 1,952 | 7,210 | 7,694 | (12 | ) | 7,682 | ||||||||||||||||||||||||

| Fiscal Balance |

6,786 | 8,092 | (824 | ) | (904 | ) | 5,533 | 6,786 | (3,262 | ) | 3,416 | |||||||||||||||||||||||

| Notes: | ||||||||||||||||||||||||||||||||||

|

(a) Numbers may not add due to rounding and have been restated where necessary to ensure comparability.

(b) The Non-financial Public Sector (NFP) consolidates the GGS and PNFC Sectors, eliminating inter-sector balances and transactions such as dividend and income tax equivalent income. The State Financial Sector consolidates the NFP and the PFC Sectors.

(c) In accordance with UPF, estimates for Public Financial Corporations (PFC) and State Financial Sectors are not required in Budget documentation.

(d) For GFS, the change in Net Worth is the change from the previous published outcome. This differs from the AASB 1049 statements where prior year adjustments are permitted under IFRS. |

| |||||||||||||||||||||||||||||||||

| 3-8 | Report on State Finances 2022–23 – Queensland Government |

2022 - 23 Balance Sheet by Sector ($ million)

| General

Government

|

Public

Non-financial

|

Non-financial Public Sector (b)

|

Public

|

State

|

||||||||||||||||||||||||||||

| Est. Actual | Outcome | Est. Actual | Outcome | Est. Actual | Outcome | Outcome (c) | Outcome (c) | |||||||||||||||||||||||||

| Assets |

||||||||||||||||||||||||||||||||

| Financial assets |

||||||||||||||||||||||||||||||||

| Cash and deposits |

1,072 | 2,357 | 851 | 1,031 | 1,923 | 3,388 | 7,801 | 9,007 | ||||||||||||||||||||||||

| Advances paid |

1,222 | 1,239 | 1,597 | 1,675 | 1,223 | 1,215 | - | 1,215 | ||||||||||||||||||||||||

| Investments, loans and placements |

48,330 | 49,426 | 5,638 | 6,194 | 53,967 | 55,619 | 175,822 | 103,039 | ||||||||||||||||||||||||

| Receivables |

4,075 | 4,320 | 2,238 | 2,742 | 5,413 | 6,256 | 485 | 6,603 | ||||||||||||||||||||||||

| Equity |

||||||||||||||||||||||||||||||||

| Investments in other public sector entities |

24,717 | 24,414 | - | - | 3,033 | 3,006 | - | - | ||||||||||||||||||||||||

| Investments - other |

165 | 175 | 56 | - | 221 | 174 | - | 174 | ||||||||||||||||||||||||

| Total financial assets |

79,580 | 81,930 | 10,380 | 11,642 | 65,780 | 69,657 | 184,108 | 120,039 | ||||||||||||||||||||||||

|

Non-Financial Assets |

||||||||||||||||||||||||||||||||

| Land and other fixed assets |

290,149 | 322,812 | 68,471 | 68,176 | 358,619 | 390,987 | 132 | 391,119 | ||||||||||||||||||||||||

| Other non-financial assets |

6,915 | 9,743 | 1,608 | 4,707 | 1,125 | 1,229 | 267 | 1,216 | ||||||||||||||||||||||||

| Total Non-financial Assets |

297,064 | 332,554 | 70,079 | 72,883 | 359,743 | 392,216 | 399 | 392,335 | ||||||||||||||||||||||||

| Total assets |

376,644 | 414,484 | 80,459 | 84,526 | 425,523 | 461,873 | 184,507 | 512,373 | ||||||||||||||||||||||||

| Liabilities |

||||||||||||||||||||||||||||||||

| Payables |

5,295 | 5,921 | 2,035 | 2,105 | 6,484 | 7,275 | 171 | 7,340 | ||||||||||||||||||||||||

| Superannuation liability |

21,205 | 20,913 | (400 | ) | (354 | ) | 20,805 | 20,559 | - | 20,559 | ||||||||||||||||||||||

| Other employee benefits |

9,559 | 10,419 | 956 | 1,040 | 10,516 | 11,460 | 181 | 11,641 | ||||||||||||||||||||||||

| Deposits held |

- | - | 11 | 14 | 11 | 14 | 10,298 | 5,104 | ||||||||||||||||||||||||

| Advances received |

1,782 | 1,909 | 4 | 25 | 190 | 235 | - | 235 | ||||||||||||||||||||||||

| Borrowing (d) |

54,693 | 53,726 | 47,875 | 49,101 | 102,561 | 102,821 | 162,312 | 132,216 | ||||||||||||||||||||||||

| Other liabilities |

14,898 | 17,622 | 8,294 | 11,185 | 15,746 | 15,537 | 8,541 | 23,765 | ||||||||||||||||||||||||

| Total liabilities |

107,434 | 110,511 | 58,774 | 63,117 | 156,313 | 157,900 | 181,502 | 200,859 | ||||||||||||||||||||||||

| Net Worth |

269,210 | 303,973 | 21,685 | 21,409 | 269,210 | 303,973 | 3,006 | 311,514 | ||||||||||||||||||||||||

| KEY FISCAL AGGREGATES |

||||||||||||||||||||||||||||||||

| Net Financial Worth |

(27,853 | ) | (28,581 | ) | (48,395 | ) | (51,474 | ) | (90,533 | ) | (88,243 | ) | 2,606 | (80,820 | ) | |||||||||||||||||

| Net Financial Liabilities |

52,570 | 52,995 | NA | NA | 93,566 | 91,249 | NA | 80,820 | ||||||||||||||||||||||||

| Net Debt |

5,852 | 2,615 | 39,804 | 40,240 | 45,649 | 42,848 | (11,014 | ) | 24,293 | |||||||||||||||||||||||

| Notes: |

||||||||||||||||||||||||||||||||

| (a) Numbers may not add due to rounding and have been restated where necessary to ensure comparability.

(b) The Non-financial Public Sector (NFP) consolidates the GGS and PNFC Sectors, eliminating inter-sector balances and transactions such as dividend and income tax equivalent income. The State Financial Sector consolidates the NFP and the PFC Sectors.

(c) In accordance with UPF, estimates for Public Financial Corporations (PFC) and State Financial Sectors are not required in Budget documentation.

(d) Borrowing line is comprised of |

| |||||||||||||||||||||||||||||||

| Borrowing with QTC |

47,014 | 46,166 | 43,074 | 43,276 | 90,088 | 89,442 | - | - | ||||||||||||||||||||||||

| Leases and other similar arrangements |

7,586 | 7,519 | 354 | 367 | 7,941 | 7,887 | 485 | 8,372 | ||||||||||||||||||||||||

| Securities and derivatives |

93 | 41 | 4,447 | 5,458 | 4,533 | 5,491 | 161,827 | 123,844 | ||||||||||||||||||||||||

| 54,693 | 53,726 | 47,875 | 49,101 | 102,561 | 102,821 | 162,312 | 132,216 | |||||||||||||||||||||||||

| Report on State Finances 2022–23 – Queensland Government | 3-9 |

2022 - 23 Cash Flow Statement by Sector ($ million)

| General

Government

|

Public

Non-financial

|

Non-financial Public Sector (b)

|

Public

|

State

|

||||||||||||||||||||||||||||

| Est. Actual | Outcome | Est. Actual | Outcome | Est. Actual | Outcome | Outcome (c) | Outcome (c) | |||||||||||||||||||||||||

| Cash Receipts from Operating Activities |

||||||||||||||||||||||||||||||||

| Taxes received |

20,561 | 20,410 | - | - | 20,189 | 20,002 | - | 19,864 | ||||||||||||||||||||||||

| Grants and subsidies received |

36,948 | 38,684 | 844 | 841 | 36,956 | 38,701 | - | 38,583 | ||||||||||||||||||||||||

| Sales of goods and services |

5,712 | 6,886 | 17,086 | 17,092 | 19,495 | 20,825 | 3,404 | 23,777 | ||||||||||||||||||||||||

| Interest receipts |

3,169 | 3,201 | 92 | 106 | 3,242 | 3,279 | 4,353 | 2,150 | ||||||||||||||||||||||||

| Dividends and income tax equivalents |

837 | 922 | - | - | 91 | 101 | - | - | ||||||||||||||||||||||||

| Other receipts |

20,498 | 22,502 | 425 | 402 | 20,838 | 22,843 | 176 | 23,010 | ||||||||||||||||||||||||

| 87,725 | 92,604 | 18,447 | 18,442 | 100,811 | 105,752 | 7,934 | 107,384 | |||||||||||||||||||||||||

| Cash Payments for Operating Activities |

||||||||||||||||||||||||||||||||

| Payments for employees |

(34,791 | ) | (34,232 | ) | (2,758 | ) | (2,750 | ) | (37,403 | ) | (36,818 | ) | (475 | ) | (36,903 | ) | ||||||||||||||||

| Payments for goods and services |

(20,955 | ) | (23,090 | ) | (9,449 | ) | (9,727 | ) | (27,094 | ) | (29,729 | ) | (2,103 | ) | (31,835 | ) | ||||||||||||||||

| Grants and subsidies |

(13,532 | ) | (13,777 | ) | (25 | ) | (29 | ) | (12,720 | ) | (12,984 | ) | (119 | ) | (12,984 | ) | ||||||||||||||||

| Interest paid |

(1,639 | ) | (1,616 | ) | (1,674 | ) | (1,671 | ) | (3,078 | ) | (3,036 | ) | (7,298 | ) | (4,641 | ) | ||||||||||||||||

| Other payments |

(1 | ) | (4 | ) | (1,117 | ) | (1,149 | ) | (612 | ) | (554 | ) | (344 | ) | (837 | ) | ||||||||||||||||

| (70,918 | ) | (72,719 | ) | (15,023 | ) | (15,325 | ) | (80,907 | ) | (83,120 | ) | (10,340 | ) | (87,200 | ) | |||||||||||||||||

| Net Cash Flows from Operating Activities |

16,807 | 19,885 | 3,424 | 3,117 | 19,904 | 22,631 | (2,406 | ) | 20,184 | |||||||||||||||||||||||

| Cash Flows from Investing Activities |

||||||||||||||||||||||||||||||||

|

Non-financial Assets |

||||||||||||||||||||||||||||||||

| Purchases of non-financial assets |

(9,194 | ) | (9,899 | ) | (4,489 | ) | (4,497 | ) | (13,601 | ) | (14,300 | ) | (9 | ) | (14,309 | ) | ||||||||||||||||

| Sales of non-financial assets |

104 | 181 | 38 | 63 | 142 | 243 | - | 243 | ||||||||||||||||||||||||

| (9,090 | ) | (9,718 | ) | (4,451 | ) | (4,434 | ) | (13,459 | ) | (14,056 | ) | (9 | ) | (14,065 | ) | |||||||||||||||||

| Financial Assets (Policy Purposes) |

(774 | ) | (766 | ) | (703 | ) | (711 | ) | 35 | 56 | - | 56 | ||||||||||||||||||||

| Financial Assets (Liquidity Purposes) |

(7,122 | ) | (8,035 | ) | 370 | 463 | (6,752 | ) | (7,573 | ) | 875 | (550 | ) | |||||||||||||||||||

| Net Cash Flows from Investing Activities |

(16,986 | ) | (18,519 | ) | (4,784 | ) | (4,682 | ) | (20,177 | ) | (21,573 | ) | 866 | (14,559 | ) | |||||||||||||||||

| Net Cash Flows from Financing Activities |

||||||||||||||||||||||||||||||||

| Advances received (net) |

482 | 598 | (1 | ) | (1 | ) | (62 | ) | (28 | ) | - | (28 | ) | |||||||||||||||||||

| Borrowing (net) |

(942 | ) | (1,318 | ) | 1,592 | 2,202 | 650 | 885 | (1,337 | ) | (452 | ) | ||||||||||||||||||||

| Dividends paid |

- | - | (246 | ) | (246 | ) | - | - | (40 | ) | - | |||||||||||||||||||||

| Deposits received (net) |

- | - | - | 3 | - | 3 | 1,878 | (1,536 | ) | |||||||||||||||||||||||

| Other financing (net) |

- | - | (296 | ) | (523 | ) | (1,264 | ) | (1,401 | ) | 3,439 | (1,084 | ) | |||||||||||||||||||

| Net Cash Flows from Financing Activities |

(460 | ) | (719 | ) | 1,049 | 1,435 | (676 | ) | (542 | ) | 3,940 | (3,099 | ) | |||||||||||||||||||

| Net Increase/(Decrease) in Cash Held |

(638 | ) | 647 | (311 | ) | (130 | ) | (949 | ) | 516 | 2,400 | 2,526 | ||||||||||||||||||||

| KEY FISCAL AGGREGATES |

||||||||||||||||||||||||||||||||

| Net cash from operating activities |

16,807 | 19,885 | 3,424 | 3,117 | 19,904 | 22,631 | (2,406 | ) | 20,184 | |||||||||||||||||||||||

| Net cash from investments in non-financial assets |

(9,090 | ) | (9,718 | ) | (4,451 | ) | (4,434 | ) | (13,459 | ) | (14,056 | ) | (9 | ) | (14,065 | ) | ||||||||||||||||

| Dividends paid |

- | - | (246 | ) | (246 | ) | - | - | (40 | ) | - | |||||||||||||||||||||

|

Cash Surplus/(Deficit) |

7,717 | 10,167 | (1,273 | ) | (1,563 | ) | 6,444 | 8,575 | (2,455 | ) | 6,119 | |||||||||||||||||||||

| Derivation of ABS GFS Cash Surplus/Deficit |

||||||||||||||||||||||||||||||||

| Cash surplus/(deficit) |

7,717 | 10,167 | (1,273 | ) | (1,563 | ) | 6,444 | 8,575 | (2,455 | ) | 6,119 | |||||||||||||||||||||

| Acquisitions under finance leases and similar arrangements |

(1,082 | ) | (849 | ) | (34 | ) | (49 | ) | (1,116 | ) | (899 | ) | (2 | ) | (900 | ) | ||||||||||||||||

| ABS GFS Cash Surplus/(Deficit) Including Finance Leases and Similar Arrangements |

6,635 | 9,318 | (1,307 | ) | (1,613 | ) | 5,328 | 7,676 | (2,457 | ) | 5,219 | |||||||||||||||||||||

| Notes: |

| |||||||||||||||||||||||||||||||

|

(a) Numbers may not add due to rounding and have been restated where necessary to ensure comparability.

(b) The Non-financial Public Sector (NFP) consolidates the GGS and PNFC Sectors, eliminating inter-sector balances and transactions such as dividend and income tax equivalent income. The State Financial Sector consolidates the NFP and the PFC Sectors.

(c) In accordance with UPF, estimates for Public Financial Corporations (PFC) and State Financial Sectors are not required in Budget documentation. |

| |||||||||||||||||||||||||||||||

| 3-10 | Report on State Finances 2022–23 – Queensland Government |

Outcomes Report - Other General Government UPF Data

Data in the following tables is presented in accordance with the Uniform Presentation Framework.

General Government Sector

| Taxes |

2022-23

|

|||

| Taxes on employers’ payroll and labour force |

5,850 | |||

| Taxes on property |

||||

| Land taxes |

1,732 | |||

| Other |

625 | |||

| Taxes on the provision of goods and services |

||||

| Stamp duties on financial and capital transactions |

5,309 | |||

| Financial institutions’ transactions taxes |

350 | |||

| Taxes on gambling |

1,911 | |||

| Taxes on insurance |

1,409 | |||

| Taxes on use of goods and performance of activities |

||||

| Motor vehicle taxes |

3,017 | |||

| Other |

396 | |||

| Total Taxation Revenue

|

|

20,601

|

| |

| Note: |

||||

|

1. Numbers may not add due to rounding. |

||||

| Dividend and Income Tax Equivalent Income | 2022-23 Outcome $ million |

|||

| Dividend and Income Tax Equivalent income from PNFC sector |

843 | |||

| Dividend and Income Tax Equivalent income from PFC sector |

164 | |||

| Total Dividend and Income Tax Equivalent income

|

|

1,007

|

| |

| Note: |

||||

|

1. Numbers may not add due to rounding.

|

||||

| Report on State Finances 2022–23 – Queensland Government | 3-11 |

Outcomes Report - Other General Government UPF Data

General Government Sector continued

| Grants Revenue | 2022-23 Outcome $ million |

|||

| Current grants revenue |

||||

| Current grants from the Commonwealth |

||||

| General purpose grants |

18,310 | |||

| Specific purpose grants |

10,699 | |||

| Specific purpose grants for on-passing |

4,740 | |||

| Total current grants from the Commonwealth |

33,749 | |||

| Other contributions and grants |

453 | |||

| Total current grants revenue |

34,202 | |||

| Capital grants revenue |

||||

| Capital grants from the Commonwealth |

||||

| Specific purpose grants |

4,088 | |||

| Other contributions and grants |

44 | |||

| Total capital grants revenue |

4,133 | |||

|

Total grants revenue |

38,335 | |||

| Note: |

||||

|

1. Numbers may not add due to rounding. |

||||

| Grants Expense | 2022-23 Outcome $ million |

|||

| Current grants expenses |

||||

| Private and not-for-profit sector |

3,219 | |||

| Private and not-for-profit sector on-passing |

4,015 | |||

| Local Government |

267 | |||

| Local Government on-passing |

776 | |||

| Grants to other sectors of Government |

2,921 | |||

| Other |

446 | |||

| Total current grants expense |

11,643 | |||

| Capital grants expenses |

||||

| Private and not-for-profit sector |

619 | |||

| Local Government |

1,615 | |||

| Grants to other sectors of Government |

70 | |||

| Other |

125 | |||

| Total capital grants expenses |

2,430 | |||

| Total grants expenses

|

|

14,072

|

| |

| Note: |

||||

|

1. Numbers may not add due to rounding.

|

||||

| 3-12 | Report on State Finances 2022–23 – Queensland Government |

Outcomes Report - Other General Government UPF Data

General Government Sector continued

|

Expenses by Function |

2022-23 | 2022-23 | ||||||||

| Outcome | Outcome | |||||||||

| $ million | $ million | |||||||||

| General Public Services |

6,135 | Health | 23,864 | |||||||

| Executive and legislative organs, financial and |

Outpatient services |

3,571 | ||||||||

| fiscal affairs, external affairs |

991 | Hospital services |

13,057 | |||||||

| General services |

338 | Mental health institutions |

707 | |||||||

| Public debt transactions |

1,650 | Community health services |

4,972 | |||||||

| Transfers of a general character between level |

Public health services |

536 | ||||||||

| of government |

1,017 | R&D - Health |

224 | |||||||

| General public services n.e.c. |

2,139 | Health n.e.c. |

797 | |||||||

| Public Order and Safety |

6,703 | Recreation, Culture and Religion | 1,081 | |||||||

| Police services |

3,145 | Recreation and sporting services |

469 | |||||||

| Civil and fire protection services |

784 | Cultural services |

426 | |||||||

| Law courts |

1,105 | Recreation, culture and religion n.e.c. |

186 | |||||||

| Prisons |

1,615 | |||||||||

| Public order and safety n.e.c. |

53 | Education | 18,497 | |||||||

| Pre-primary and primary education |

8,803 | |||||||||

| Economic Affairs |

2,672 | Secondary education |

6,309 | |||||||

| General economic, commercial and labour |

Tertiary education |

1,528 | ||||||||

| affairs |

352 | Subsidiary services to education |

205 | |||||||

| Agriculture, forestry, fishing and hunting |

461 | Education n.e.c. |

1,652 | |||||||

| Fuel and energy |

964 | |||||||||

| Mining, manufacturing and construction |

487 | Social Protection | 6,390 | |||||||

| R&D - Economic affairs |

182 | Sickness and disability |

2,292 | |||||||

| Other industries |

205 | Old age |

20 | |||||||

| Economic affairs |

20 | Family and children |

2,227 | |||||||

|

|

Housing |

390 | ||||||||

| Environmental Protection |

894 | Social exclusion n.e.c. |

259 | |||||||

| Protection of biodiversity and landscape |

508 | Social protection n.e.c. |

1,202 | |||||||

| Environmental protection n.e.c. |

386 | |||||||||

| Transport | 8,047 | |||||||||

| Housing and Community Amenities |

1,597 | Road transport |

3,547 | |||||||

| Housing development |

903 | Bus transport |

127 | |||||||

| Community development |

137 | Water transport |

184 | |||||||

| Water supply |

253 | Railway transport |

2,389 | |||||||

| Housing and community amenities n.e.c. |

303 | Multi-mode urban transport |

933 | |||||||

| Transport n.e.c. |

867 | |||||||||

| Total | 75,880 | |||||||||

| Note: |

||||||||||

| 1. Numbers may not add due to rounding. |

||||||||||

|

|

||||||||||

| Report on State Finances 2022–23 – Queensland Government | 3-13 |

Outcomes Report - Other General Government UPF Data

General Government Sector continued

|

Purchases of Non-financial Assets by Function |

|

2022-23 Outcome $ million |

| |

| General public services |

255 | |||

| Public order and safety |

568 | |||

| Economic affairs |

24 | |||

| Environmental protection |

80 | |||

| Housing and community amenities |

458 | |||

| Health |

1,561 | |||

| Recreation, culture and religion |

83 | |||

| Education |

1,350 | |||

| Social protection |

83 | |||

| Transport |

5,437 | |||

| Total |

9,899 | |||

|

|

||||

| Note: |

||||

| 1. Numbers may not add due to rounding. |

||||

|

|

||||

| 3-14 | Report on State Finances 2022–23 – Queensland Government |

Certification of Outcomes Report

Management Certification

The foregoing Outcomes Report contains financial statements for the Queensland State Government, prepared and presented in accordance with the Uniform Presentation Framework (UPF) agreed to at the 1991 Premiers’ Conference and revised in 2008 to align with AASB 1049 Whole of Government and General Government Sector Financial Reporting.

This report separately discloses outcomes for the General Government, Public Non-financial Corporations, Public Financial Corporations and State Financial Sectors within Queensland. Entities excluded from this report include local governments and universities. Queensland public sector entities consolidated for this report are listed in the AASB 1049 Financial Statements, taking into account intra and inter-agency eliminations.

Only those agencies considered material by virtue of their financial transactions and balances are consolidated in this report.

We certify that, in our opinion, the Outcomes Report has been properly drawn up, in accordance with UPF requirements, to present a true and fair view of:

(i) the Operating Statement and Cash Flows of the Queensland State Government for the financial year; and

(ii) the Balance Sheet of the Government at 30 June 2023.

At the date of certification of this report, we are not aware of any material circumstances that would render any particulars included in the Outcomes Report misleading or inaccurate.

| Dennis Molloy |

Michael Carey | |

| Deputy Under Treasurer |

Under Treasurer | |

| Queensland Treasury |

Queensland Treasury | |

16 October 2023

| Report on State Finances 2022–23 – Queensland Government | 3-15 |

AASB 1049 Overview

QUEENSLAND TREASURY

2022–23

AASB 1049

Financial Statements

Overview and Analysis – 30 June 2023

AASB 1049 - Overview and Analysis

The following analysis compares current year General Government Sector (GGS) and Total State Sector (TSS) performance with last year’s balances, restated for changes in accounting policies, presentational and timing differences and errors.

AASB 1049 Whole of Government and General Government Sector Financial Reporting aims to harmonise the disclosure presentation to be consistent with the Uniform Presentation Framework disclosed in the Outcomes Report.

Summary of Key Financial Aggregates of the Consolidated Financial Statements

The table below provides aggregate information under AASB1049:

| General Government | Total State | |||||||||||||||

| Sector | Sector | |||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||

| $ million | $ million | $ million | $ million | |||||||||||||

| Taxation revenue |

20,601 | 20,011 | 20,051 | 19,508 | ||||||||||||

| Grants revenue |

38,335 | 34,135 | 38,233 | 34,034 | ||||||||||||

| Sales of goods and services |

6,483 | 5,896 | 20,838 | 20,282 | ||||||||||||

| Interest income |

3,226 | 2,643 | 2,184 | 1,188 | ||||||||||||

| Dividend and income tax equivalent income |

1,007 | 790 | - | - | ||||||||||||

| Other revenue |

20,160 | 10,710 | 20,778 | 11,164 | ||||||||||||

| Continuing Revenue from Transactions |

89,810 | 74,185 | 102,084 | 86,176 | ||||||||||||

| Employee expenses |

30,557 | 28,068 | 32,988 | 30,251 | ||||||||||||

| Superannuation expenses |

4,532 | 3,763 | 4,851 | 4,045 | ||||||||||||

| Other operating expenses |

20,014 | 18,229 | 27,468 | 26,075 | ||||||||||||

| Depreciation and amortisation |

5,018 | 4,506 | 7,760 | 7,250 | ||||||||||||

| Other interest expenses |

1,688 | 1,508 | 4,712 | 4,064 | ||||||||||||

| Grants expenses |

14,072 | 13,827 | 13,206 | 13,167 | ||||||||||||

| Continuing Expenses from Transactions

|

|

75,880

|

|

|

69,902

|

|

|

90,986

|

|

|

84,853

|

| ||||

| Net Operating Balance |

13,930 | 4,284 | 11,098 | 1,323 | ||||||||||||

| Other Economic Flows - Included in Operating Result |

198 | (913 | ) | 5,052 | 16,227 | |||||||||||

| Operating Result |

14,128 | 3,371 | 16,150 | 17,550 | ||||||||||||

| Other Economic Flows - Other Movements in Equity |

40,255 | 36,755 | 39,727 | 36,538 | ||||||||||||

| Comprehensive Result 1 |

54,383 | 40,126 | 55,877 | 54,088 | ||||||||||||

| Purchases of non-financial assets |

9,899 | 7,878 | 14,309 | 11,136 | ||||||||||||

| Fiscal Balance |

8,092 | (72 | ) | 3,416 | (3,596 | ) | ||||||||||

| Borrowing with QTC |

46,166 | 49,000 | - | - | ||||||||||||

| Leases and other similar arrangements |

7,519 | 7,671 | 8,372 | 8,532 | ||||||||||||

| Securities and derivatives |

41 | 93 | 123,844 | 136,591 | ||||||||||||

| Assets |

414,484 | 363,430 | 512,373 | 469,802 | ||||||||||||

| Liabilities |

110,511 | 113,840 | 200,859 | 214,165 | ||||||||||||

| Net Worth |

303,973 | 249,590 | 311,514 | 255,637 | ||||||||||||

| Net Debt |

2,615 | 10,997 | 24,293 | 36,753 | ||||||||||||

|

Note: | ||||||||||

| 1. | Comprehensive result is different to the Outcomes Report as it reflects the movement from the 2022 recast position, rather than the 2022 published position. | |||||||||

| 2. |

Numbers may not add due to rounding. | |||||||||

| Report on State Finances 2022–23 – Queensland Government | 4-1 |

AASB 1049 - Overview and Analysis

Net Operating Balance

After a strong economic rebound in 2021-22, Queensland’s economy has continued to strengthen in 2022-23 despite inflationary pressures both globally and domestically. The GGS net operating balance was an historically high surplus of $13.93 billion compared to a restated surplus of $4.284 billion in 2021-22. The 2022-23 record surplus was driven by the exceptionally high coal prices that have continued to be received by Queensland’s coal producers, as well as the state’s strong labour market performance.

GGS revenue rose by around 21 per cent ($15.625 billion) while expenses grew by 8.6 per cent ($5.978 billion).

The Total State Sector (TSS) net operating balance showed an operating surplus of $11.098 billion compared to a restated surplus of $1.323 billion in 2021-22.

The variances are explained below.

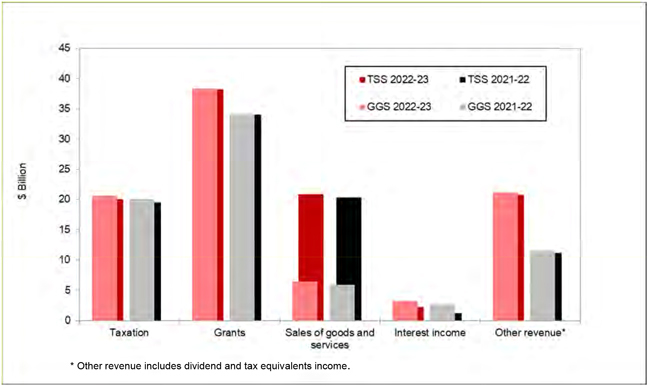

Revenue

Revenue from transactions increased by 21 per cent from $74.185 billion in 2021-22 to be $89.81 billion in the GGS and totalled $102.084 billion in the TSS, a rise of $15.908 billion over 2021-22.

Revenues by type for the GGS and TSS are shown in the following chart:

Chart 4.1: General Government and Total State Sector Revenue by type compared to 2021-22

Taxation revenues for the GGS were $20.601 billion in 2022-23, $590 million or 2.9 per cent higher than 2021-22 and increased $543 million to total $20.051 billion for the TSS.

The increase in GGS taxation revenue reflects the strength of the domestic economic activity and the state’s strong jobs growth and labour market performance. Aside from transfer duties, all taxation revenues experienced strong growth in 2022-23.

Payroll tax increased $668 million, or 13.4 per cent in 2022-23 driven by strong employment and wages growth. In addition, from 1 January 2023, Queensland introduced a mental health levy for large businesses with national payrolls of more than $10 million to provide a sustainable on-going funding source for mental health services and investment. Mental health levies collected in the first half of 2023 from businesses (outside of Queensland government) totalled $182 million.

Gaming machine taxes and levies and motor vehicle registration were respectively $266 million and $123 million higher than 2021-22. Land taxes increased $99 million in 2022-23 as a result of material increases in land values in recent years.

| 4-2 | Report on State Finances 2022–23 – Queensland Government |

AASB 1049 - Overview and Analysis

Revenue continued

Duties declined $826 million compared to 2021-22 in large part due to lower transfer duty as a result of significant moderation in both residential and non-residential activity following the exceptional rebound in property markets over the preceding two years.

Commonwealth and other grants comprised 43 per cent of GGS revenue and 38 per cent of TSS revenue. Grant revenue increased $4.2 billion from 2021-22 for both the GGS and the TSS. The increase was due to

| – | higher GST revenue of $2.227 billion primarily driven by a larger national GST pool; |

| – | advance payment of $758 million of disaster recovery funding, representing around 40% of DRFA payments expected to be received in 2023-24; |

| – | an uplift in funding for Quality Schools, including for non-government schools; |

| – | $398 million in up-front funding for the Social Housing Accelerator program. |

GGS sales of goods and services were $587 million higher than 2021-22 largely due to revenue from public transport sales, hospital fees and transport and traffic fees. TSS sales of goods and services increased $556 million compared to 2021-22.

Interest income of $3.226 billion for the GGS was $583 million higher than the 2021-22 due in part to interest earnings on investment of royalty windfalls in 2022 ($2.5 billion) and 2023 ($3 billion), and investment of an additional $1 billion to support the Housing Investment Fund. TSS interest income increased $996 million compared to 2021-22 driven by earnings on financial assets held by Queensland Treasury Corporation.

Dividend and income tax equivalent revenue for the GGS increased by $217 million in comparison to 2021-22, reflecting a return to the normal GOC dividend policy in 2022-23 following the government’s decision to allow GOCs to retain 2021-22 dividends for reinvestment in critical infrastructure. Higher dividend income is partly offset by lower tax equivalent revenue from electricity network GOCs.

GGS other revenue was $20.16 billion in 2022-23, $9.45 billion higher than 2021-22 predominantly due to an increase in royalties and land rents. The increase in royalties was primarily driven by the combination of extraordinary strength in global coal and oil prices received by Queensland’s key commodity producers and the introduction of new progressive coal royalty tiers. This increase flows through to the TSS.

Expenses

Total expenses for 2022-23 were $75.88 billion for the GGS and $90.986 billion for the TSS, $5.978 billion and $6.133 billion more than the previous year, respectively.

Expenses by type are shown in the following chart:

Chart 4.2: General Government and Total State Sector Expenses by Type compared to 2021-22

| Report on State Finances 2022–23 – Queensland Government | 4-3 |

AASB 1049 - Overview and Analysis

Expenses continued

GGS employee and superannuation expenses together were $3.258 billion or 10.2 per cent higher in 2022-23, broadly consistent with the estimate in the 2023-24 Budget. TSS employee and superannuation expenses were $3.543 billion higher in 2022-23.

GGS employee expenses were $2.489 billion (or 8.9 per cent) higher in 2022-23 in part due to numerous public sector agreements being certified within the financial year, combined with a 2.7 per cent increase in full time equivalent employees. Newly certified public sector agreements included wage increases of 4 percent in year one and two and 3 per cent in year 3, an uplift from expiring agreements annual wage increase of 2.5 per cent. In addition, certified agreements included a Cost of Living Adjustment (COLA) payment for employees where inflation exceeds headline wage increases established in agreements, capped at 3 per cent. COLA payments were triggered for newly certified agreements at the maximum cap of 3 percent, applied to base wages.

An increase in GGS superannuation expenses of $769 million in 2022-23 arose from higher defined benefit costs due to changes in actuarial assumptions and new Queensland public sector superannuation arrangements coming into effect from 1 July 2023. The Queensland Government has simplified its employer contribution arrangements to 18 per cent of salary for police officers, 14.25 per cent for fire service officers and 12.75 per cent of salary for other employees. Superannuation contributions are payable on base salary, ordinary time allowances and paid leave.

Other operating expenses were $1.785 billion higher in 2022-23 for the GGS mainly due to the $175 Cost of Living Rebate on Queensland household’s power bills, increased demand for health, education and child and family services, and an increase in operating costs associated with the delivery of the State’s road and rail infrastructure program. TSS other operating expenses were $1.393 billion higher in comparison to 2021-22 due to the higher costs in the GGS, offset in part by lower claims expenses for the Queensland National Injury Insurance Scheme.

Depreciation and amortisation increased by $512 million for the GGS mainly due to increases in the stock and value of infrastructure.

GGS interest costs were $1.688 billion, an increase of $180 million on the previous year due to a rise in interest rates with GGS borrowing actually lower. The interest expense for TSS was $648 million higher which reflects the increase in interest on client deposits, the nominal increase in external borrowing and higher interest rates.

Grant expenses were $14.072 billion in the GGS, $245 million higher than 2021-22. Contributing to the increase in grants expenses were higher Australian Government grants on-passed to non-government schools, payments as part of the Energy Price Relief Plan agreed by National Cabinet in December 2022 and higher community service obligations to Energy Queensland Limited. Higher grants expenses in 2022-23 were partly offset by the impact of waste levy payments made to councils in 2021-22 and the winding down of the Australian Government’s HomeBuilder Grants program.

Operating Result

The operating result is the surplus or deficit for the year under the Australian Accounting Standards framework. Valuation and other adjustments such as deferred tax, capital returns and market value interest are shown as other economic flows and are included in the operating result.

The GGS operating result for the 2022-23 year was a surplus of $14.128 billion, compared to a surplus of $3.371 billion in 2021-22. The significant upturn in the operating result is mainly due to the improved net operating balance, discussed above, improved market value adjustments to the fixed rate notes with QTC and actuarial adjustments to self-insurance liabilities.

The TSS operating result was a surplus of $16.15 billion in 2022-23. This result is due in large part to the comparable improvement in the 2022-23 net operating balance and the net effect of realised and unrealised market value adjustments to investments and borrowings.

Fiscal Balance

The GGS fiscal surplus was $8.092 billion for 2022-23 compared to a deficit of $72 million for 2021-22. The TSS fiscal surplus was $3.416 billion for 2022-23 compared to a deficit of $3.596 billion for 2021-22. The changes are driven by the improved net operating balances offset to an extent by higher total net acquisitions of non-financial assets.

Assets

Assets controlled by the GGS at 30 June 2023 totalled $414.484 billion, an increase of $51.054 billion on 2021-22, while assets controlled by the TSS at 30 June 2023 totalled $512.373 billion. This is an increase of $42.571 billion from the 2021-2022 balance of $469.802 billion.

| 4-4 | Report on State Finances 2022–23 – Queensland Government |

AASB 1049 - Overview and Analysis

Assets continued

Financial assets in the GGS increased $10.554 billion in the year to total $81.93 billion as at 30 June 2023. This was mainly due to an increase in securities held following additional long-term asset investments made from the improved net operating cash flows and an increase in the investment in public enterprises. Higher investments reflect the $3 billion investment of royalty windfalls to fund regional priority infrastructure projects and an additional $1 billion investment to support the Housing Investment Fund, combined with the reinvestment of interest earnings for the Debt Retirement Fund. The increase in investments in public sector entities is largely due to improved net worth of government-owned electricity businesses and the National Injury Insurance Scheme, Queensland.

Financial assets of the TSS declined by $1.738 billion, reflecting market value adjustments to derivatives held by government-owned electricity generation businesses, offset to a large extent by higher cash balances and securities held mainly by QTC.

Non-financial assets increased by $40.499 billion in the GGS due to revaluations of land under roads, road infrastructure and schools, as well as capital purchases exceeding depreciation. The increase at the TSS level was $44.31 billion.

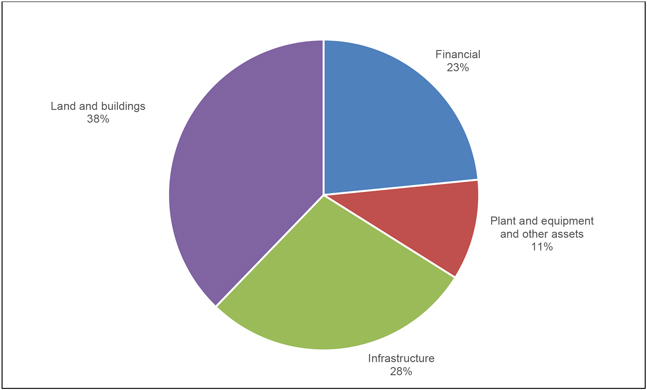

Of the TSS assets, GGS assets comprised 81 per cent. Total assets are made up of:

| General Government |

Total State | |||||||

| $M | $M | |||||||

| Financial |

81,930 | 120,039 | ||||||

| Infrastructure |

90,560 | 144,911 | ||||||

| Land and buildings |

188,326 | 193,617 | ||||||

| Plant and equipment and other |

44,642 | 53,807 | ||||||

| Deferred tax asset |

9,026 | — | ||||||

|

|

|

|

|

|||||

| 414,484 | 512,373 | |||||||

|

|

|

|

|

|||||

The main types of assets owned by the State are detailed in the following chart:

Chart 4.3: Total State Assets by Type

| Report on State Finances 2022–23 – Queensland Government | 4-5 |

AASB 1049 - Overview and Analysis

Liabilities

Liabilities at 30 June 2023 totalled $110.511 billion for the GGS and $200.859 billion for the TSS, a decrease of $3.329 billion over 2021-22 for the GGS and a decrease of $13.306 billion for the State.

The overall decline in liabilities for the GGS is due to some extent to the record operating surplus in 2022-23 partly flowing through to reduced borrowing with QTC ($2.834 billion). Lower deferred tax liabilities ($1.285 billion), mainly from Stanwell Corporation, also contribute to the decline in liabilities within the year.

For the TSS, derivatives held by GOC electricity generation businesses declined $11.945 billion, largely reflecting downward valuations of hedging contracts. Lower deposits primarily held by QTC ($1.535 billion) also factored into the decline in TSS liabilities.

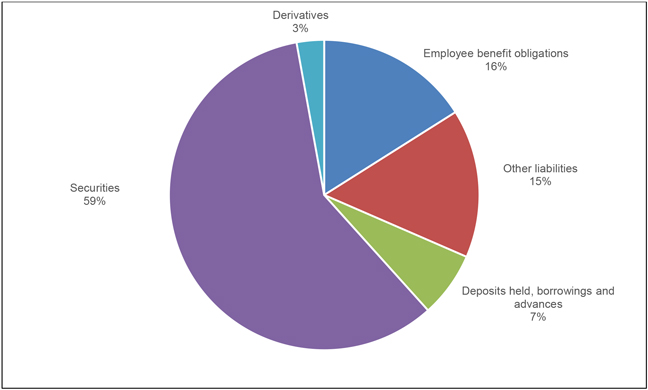

Of the TSS liabilities, GGS liabilities comprised 55 per cent. Total liabilities are made up of:

| General Government |

Total State | |||||||

| $M | $M | |||||||

| Securities |

— | 118,114 | ||||||

| Derivatives |

41 | 5,729 | ||||||

| Deposits held, borrowings and advances |

55,594 | 13,711 | ||||||

| Employee benefit obligations |

31,332 | 32,200 | ||||||

| Other liabilities |

23,544 | 31,105 | ||||||

|

|

|

|

|

|||||

| 110,511 | 200,859 | |||||||

|

|

|

|

|

|||||

The components of State liabilities are shown in the following chart:

Chart 4.4: Total State Liabilities by Type

| 4-6 | Report on State Finances 2022–23 – Queensland Government |

AASB 1049 - Overview and Analysis

Net Debt

The GGS net debt was $2.615 billion at 30 June 2023, compared to $10.997 billion in 2021-22, an improvement of $8.382 billion. The improvement in net debt is largely driven by the record net operating surplus in 2022-23 flowing through to higher cash balances, investments and reduced borrowings with QTC.

TSS net debt at 30 June 2023 was $24.293 billion, an improvement of $12.46 billion on 2022, largely due to an increase in securities held by QTC for whole-of-government long term liabilities and capital market operations, and a net decrease in derivative liabilities held by energy GOCs to hedge market movements in electricity prices.

Cash Flow Statement

The GGS recorded positive net cash flows from operating activities of $19.885 billion which were used to fund net investments in non-financial assets of $9.718 billion, resulting in a cash surplus of $10.167 billion (cash surplus of $2.816 billion in 2021-22).

The TSS recorded net cash flows from operating activities for the 2022-23 financial year of $20.184 billion. After net investments in non-financial assets of $14.065 billion, the resulting cash surplus is $6.119 billion, compared to a $182 million cash deficit for 2021-22.

| Report on State Finances 2022–23 – Queensland Government | 4-7 |

Audited Information

QUEENSLAND TREASURY

2022–23

Audited Information

Queensland General Government and

Whole of Government Consolidated

Financial Statements

30 June 2023

Operating Statement for Queensland

for the Year Ended 30 June 2023

| General Government | Total State | |||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||||||

| Notes | $M | $M | $M | $M | ||||||||||||||||

| Continuing Operations |

||||||||||||||||||||

| Revenue from Transactions |

||||||||||||||||||||

| Taxation revenue |

3 | 20,601 | 20,011 | 20,051 | 19,508 | |||||||||||||||

| Grants revenue |

4 | 38,335 | 34,135 | 38,233 | 34,034 | |||||||||||||||

| Sales of goods and services |

5 | 6,483 | 5,896 | 20,838 | 20,282 | |||||||||||||||

| Interest income |

6 | 3,226 | 2,643 | 2,184 | 1,188 | |||||||||||||||

| Dividend and income tax equivalent income |

7 | 1,007 | 790 | - | - | |||||||||||||||

| Other revenue |

8 | 20,160 | 10,710 | 20,778 | 11,164 | |||||||||||||||

| Total Revenue from Transactions |

89,810 | 74,185 | 102,084 | 86,176 | ||||||||||||||||

| Expenses from Transactions |

||||||||||||||||||||