As filed with the Securities and Exchange Commission on April 27, 2023

Registration Nos. 333-22375

and 811-3199

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-4

REGISTRATION STATEMENT

UNDER

| THE SECURITIES ACT OF 1933 | ☒ | |||

| Pre-Effective Amendment No. | ☐ | |||

| Post-Effective Amendment No. 37 | ☒ |

and/or

REGISTRATION STATEMENT

UNDER

| THE INVESTMENT COMPANY ACT OF 1940 | ☒ | |||

| Amendment No. 145 | ☒ |

ZALICO VARIABLE ANNUITY SEPARATE ACCOUNT

(formerly KILICO VARIABLE ANNUITY SEPARATE ACCOUNT)

(Exact Name of Registrant)

ZURICH AMERICAN LIFE INSURANCE COMPANY

(formerly KEMPER INVESTORS LIFE INSURANCE COMPANY)

(Name of Depositor)

1299 Zurich Way, Schaumburg, Illinois 60196

(Address of Depositor’s Principal Executive Offices)

Depositor’s Telephone Number, including Area Code:

(877) 301-5376

| Name and Address of Agent for Service: | Copy to: | |

| Stanislav Sukhorukov, Esq. 1299 Zurich way, Schaumburg, IL, 60196 |

Richard T. Choi, Esq. Carlton Fields, P.A. 1025 Thomas Jefferson Street, N.W., Suite 400 West Washington, DC 20007-5208 |

It is proposed that this filing will become effective (check appropriate box):

| ☐ | Immediately upon filing pursuant to paragraph (b) |

| ☒ | On May 1, 2023, pursuant to paragraph (b) |

| ☐ | 60 days after filing pursuant to paragraph (a)(1) |

| ☐ | On (date) pursuant to paragraph (a)(1) |

If appropriate, check the following box:

| ☐ | This post-effective amendment designates a new effective date for a previously-filed post-effective amendment |

|

Individual Variable, Fixed, and Market Value Adjusted Deferred Annuity Contracts Issued by Zurich American Life Insurance Company Through ZALICO Variable Annuity Separate Account |

Prospectus May 1, 2023 | |||

| Home Office 1299 Zurich Way Schaumburg, Illinois 60196

www.zurichamericanlifeinsurance.com |

Service Center Scudder DestinationsSM Service Team PO Box 19097 Greenville, SC 29602-9097 Phone: 1-800-449-0523 (toll free) 8:30 a.m. to 6:00 p.m. Eastern Time M-F |

Scudder DestinationsSM Annuity/Farmers Variable Annuity I | ||

This Prospectus describes the Scudder DestinationsSM Annuity and the Farmers Variable Annuity I, each a variable, fixed and market value adjusted deferred annuity contract (the Scudder DestinationsSM Annuity and the Farmers Variable Annuity I are each referred to herein as a “Contract”) issued by Zurich American Life Insurance Company (“we” or “ZALICO”). The Scudder DestinationsSM Annuity contracts are identical to the Farmers Variable Annuity I contracts except that they have different marketing names and were sold through different arrangements. The Contract is designed to provide annuity benefits for retirement that may or may not qualify for certain federal tax advantages. Depending on particular state requirements, the Contract may have been issued on a group or individual basis. The Contracts are currently not being issued. The Contracts were previously issued on a group basis in certain states, but no group Contracts remain in force. Additional information about certain investment products, including variable annuities, has been prepared by the Securities and Exchange Commission’s staff and is available at Investor.gov.

The date of this Prospectus is May 1, 2023.

| The Securities and Exchange Commission has not approved or disapproved the Contract or determined that this Prospectus is accurate or complete. Anyone who tells you otherwise is committing a U.S. Federal crime. |

| Not FDIC Insured | May Lose Value | No Bank Guarantee |

PAGE 1

| Page | ||||

| 4 | ||||

| IMPORTANT INFORMATION YOU SHOULD CONSIDER ABOUT THE CONTRACT |

6 | |||

| 10 | ||||

| 10 | ||||

| 10 | ||||

| 10 | ||||

| 12 | ||||

| 14 | ||||

| 17 | ||||

| 17 | ||||

| 17 | ||||

| 18 | ||||

| 18 | ||||

| 18 | ||||

| 20 | ||||

| 20 | ||||

| 21 | ||||

| 21 | ||||

| 21 | ||||

| 21 | ||||

| 22 | ||||

| 23 | ||||

| 24 | ||||

| 24 | ||||

| 24 | ||||

| 7. Policy and Procedures Regarding Disruptive Trading and Market Timing |

26 | |||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| 34 | ||||

| 34 | ||||

| 35 | ||||

| 35 | ||||

| 35 | ||||

| 35 | ||||

| 36 | ||||

| 36 | ||||

| 5. Optional Guaranteed Retirement Income Benefit (“GRIB”) Rider Charge |

37 | |||

| 38 | ||||

| 38 | ||||

| 38 | ||||

| 38 | ||||

| 39 | ||||

| 39 | ||||

| 39 | ||||

| 39 | ||||

| 41 | ||||

| 41 | ||||

PAGE 2

TABLE OF CONTENTS (CONTINUED)

| Page | ||||

| 42 | ||||

| 42 | ||||

| 42 | ||||

| 42 | ||||

| 42 | ||||

| 43 | ||||

| 44 | ||||

| 45 | ||||

| 45 | ||||

| 45 | ||||

| 47 | ||||

| 47 | ||||

| 48 | ||||

| 48 | ||||

| 49 | ||||

| 49 | ||||

| 51 | ||||

| 51 | ||||

| 53 | ||||

| 53 | ||||

| 54 | ||||

| 56 | ||||

| 57 | ||||

| 57 | ||||

| 57 | ||||

| 57 | ||||

| 57 | ||||

| 57 | ||||

| 58 | ||||

| G. Annuity Purchases by Nonresident Aliens and Foreign Corporations |

58 | |||

| 58 | ||||

| 58 | ||||

| 58 | ||||

| 58 | ||||

| 59 | ||||

| 60 | ||||

| 60 | ||||

| 60 | ||||

| 61 | ||||

| 61 | ||||

| 62 | ||||

| 62 | ||||

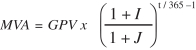

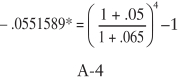

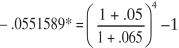

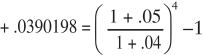

| APPENDIX A ILLUSTRATION OF THE “FLOOR” ON THE DOWNWARD MARKET VALUE ADJUSTMENT (MVA) |

A-1 | |||

| B-1 | ||||

| C-1 | ||||

PAGE 3

The following terms as used in this Prospectus have the indicated meanings:

Accumulated Guarantee Period Value—The sum of your Guarantee Period Values.

Accumulation Period—The period between the Date of Issue of a Contract and the Annuity Date.

Accumulation Unit—A unit of measurement used to determine the value of each Subaccount during the Accumulation Period.

Annuitant—The person designated to receive or who is actually receiving annuity payments and upon the continuation of whose life annuity payments involving life contingencies depend.

Annuity Date—The date on which annuity payments are to commence.

Annuity Option—One of several methods by which annuity payments can be made.

Annuity Period—The period starting on the Annuity Date.

Annuity Unit—A unit of measurement used to determine the amount of Variable Annuity payments.

Beneficiary—The person designated to receive any benefits under a Contract upon the death of the Annuitant or the Owner prior to the Annuity Period.

Company (“we”, “us”, “our”, “ZALICO”)—Zurich American Life Insurance Company. Our Home Office is located at 1299 Zurich Way, Schaumburg, Illinois 60196. For Contract services, you may contact the Service Center at Scudder DestinationsSM Service Team, PO Box 19097, Greenville, South Carolina, 29602-9097 or 1-800-449-0523.

Contract—A Variable, Fixed and Market Value Adjusted Annuity Contract that previously was offered on an individual or group basis. Contracts are represented by an individual annuity contract. No group Contracts are outstanding.

Contract Value—The sum of the values of your Separate Account Contract Value, Accumulated Guarantee Period Value and Fixed Account Contract Value.

Contract Year—Period between anniversaries of the Contract’s Date of Issue.

Contract Quarter—Periods between quarterly anniversaries of the Contract’s Date of Issue.

Contribution Year—Each one year period following the date a Purchase Payment is made.

Date of Issue—The date on which the first Contract Year commences.

Effective Date—The date that the endorsement to your Contract adding enhancements to the MVA Option (the “MVA Endorsement”) became effective, which is April 1, 2005.

Fixed Account—The General Account of ZALICO to which you may allocate all or a portion of Purchase Payments or Contract Value. We guarantee a minimum rate of interest on Purchase Payments allocated to the Fixed Account.

Fixed Account Contract Value—The value of your Contract interest in the Fixed Account.

Fixed Annuity—An annuity under which we guarantee the amount of each annuity payment; it does not vary with the investment experience of a Subaccount.

Fund or Funds—AIM Variable Insurance Funds (Invesco Variable Insurance Funds), The Alger Portfolios, BNY Mellon Investment Portfolios (formerly Dreyfus Investment Portfolios), BNY Mellon Sustainable U.S. Equity Portfolio, Inc. (formerly The Dreyfus Sustainable U.S. Equity Portfolio, Inc.), Deutsche DWS Investments VIT Funds, Deutsche DWS Variable Series I, Deutsche DWS Variable Series II, and Janus Aspen Series, including any Portfolios thereunder.

General Account—All our assets other than those allocated to any separate account.

Guaranteed Interest Rate—The rate of interest we establish for a given Guarantee Period.

Guarantee Period—The time during which we credit your allocation with a Guaranteed Interest Rate. Guarantee Periods may range from one to ten years, at our option. If you withdraw money from a Guarantee Period before its term has expired, you will be assessed a Market Value Adjustment.

PAGE 4

Guarantee Period Value—The Guarantee Period Value is the sum of your: (1) Purchase Payment allocated or amount transferred to a Guarantee Period; plus (2) interest credited; minus (3) withdrawals, previously assessed Withdrawal Charges and transfers; and (4) as adjusted for any applicable Market Value Adjustment previously made.

Home Office—The address of our Home Office is 1299 Zurich Way, Schaumburg, Illinois 60196.

Market Adjusted Value—A Guarantee Period Value adjusted by the Market Value Adjustment formula on any date prior to the end of a Guarantee Period.

Market Value Adjustment (“MVA”)—An adjustment of amounts held in a Guarantee Period that we compute in accordance with the Market Value Adjustment formula in your Contract if you take a withdrawal prior to the end of that Guarantee Period. The adjustment reflects the change in the value of the Guarantee Period Value due to changes in interest rates since the date the Guarantee Period started. Any downward Market Value Adjustment is subject to the MVA Floor described in the MVA Endorsement issued on April 1, 2005 and described herein.

Non-Qualified Plan Contract—A Contract which does not receive favorable tax treatment under Sections 401, 403, 408, 408A or 457 of the Internal Revenue Code.

Owner (“you”, “your”, “yours”)—The person designated in the Contract as having the privileges of ownership defined in the Contract.

Portfolio—A series of a Fund with its own objective and policies, which represents shares of beneficial interest in a separate portfolio of securities and other assets. Portfolio is sometimes referred to herein as a Fund.

Purchase Payments—Amounts paid to us by you or on your behalf.

Qualified Plan Contract—A Contract issued in connection with a retirement plan that receives favorable tax treatment under Sections 401, 403, 408, 408A or 457 of the Internal Revenue Code.

Separate Account—The ZALICO Variable Annuity Separate Account.

Separate Account Contract Value—The sum of your Subaccount Values.

Service Center—The address of our Service Center is Scudder DestinationsSM Service Team, PO Box 19097, Greenville, South Carolina, 29602-9097. The overnight address is: Scudder DestinationsSM Service Team, 2006 Wade Hampton Boulevard, Greenville, SC 29615-1064. Illumifin Corporation (formerly Concentrix Insurance Administration Solutions Corporation) is the administrator of the Contract. You can call the Service Center toll-free at 1-800-449-0523.

Start Date—The later of the Effective Date of the MVA Endorsement or the beginning of a new Guarantee Period.

Subaccounts—The nineteen subdivisions of the Separate Account, the assets of which consist solely of shares of the corresponding Portfolios or Funds.

Subaccount Value—The value of your interest in each Subaccount.

Valuation Date—Each day when the New York Stock Exchange is open for trading, as well as each day otherwise required.

Valuation Period—The interval of time between two consecutive Valuation Dates.

Variable Annuity—An annuity with payments varying in amount in accordance with the investment experience of the Subaccount(s) in which you have an interest.

Withdrawal Charge—The “contingent deferred sales charge” assessed against certain withdrawals of Contract Value in the first seven Contribution Years after a Purchase Payment is made or against certain annuitizations of Contract Value in the first seven Contribution Years after a Purchase Payment is made.

Withdrawal Value—Contract Value, plus or minus any applicable Market Value Adjustment, less any premium tax payable if the Contract is being annuitized, minus any Withdrawal Charge applicable to that Contract.

PAGE 5

IMPORTANT INFORMATION YOU SHOULD CONSIDER ABOUT THE CONTRACT

| FEES AND EXPENSES |

LOCATION IN | |||||||

| Charges for Early Withdrawal |

If you withdraw money from your Contract within 7 Contribution Years following your last Purchase Payment, you will be assessed a Withdrawal Charge. The maximum Withdrawal Charge is 7% of the Purchase Payment amount withdrawn during the first Contribution Year following your last Purchase Payment. For example, if you make an early withdrawal within the first Contribution Year, you could pay a Withdrawal Charge of up to $7,000 on a $100,000 investment.1 | CONTRACT CHARGES AND EXPENSES | ||||||

| Transaction Charges |

In addition to Withdrawal Charges, you also may be charged for other transactions, such as when you transfer cash value between investment options more than 12 times a year (not currently imposed), or when we pay premium taxes on Purchase Payments received under Contracts sold in states that impose such taxes. | CONTRACT CHARGES AND EXPENSES | ||||||

| Ongoing Fees and Expenses (annual charges) |

The table below describes the fees and expenses that you may pay each year, depending on the options you choose. Please refer to your Contract specifications page for information about the specific fees you will pay each year based on the options you have elected. | CONTRACT CHARGES AND EXPENSES | ||||||

| MINIMUM AND MAXIMUM ANNUAL FEE TABLE | ||||||||

| MINIMUM | MAXIMUM | |||||||

| 1. Base Contract |

1.416%2 | 1.416%2 | CONTRACT CHARGES AND EXPENSES | |||||

| 2. Investment options (Portfolio fees and expenses) |

0.32%3 | 1.33%3 | CONTRACT CHARGES AND EXPENSES | |||||

| 3. Optional benefits available for an additional charge (for a single optional benefit, if elected) |

0.25%4 | 0.25%4 | CONTRACT CHARGES AND EXPENSES | |||||

| 1 | If you withdraw money from a Guarantee Period before its term has expired, and during a period of rising interest rates, you may be assessed a negative Market Value Adjustment. |

| 2 | The minimum and maximum fee assumes Base Contract and administration charges calculated as a percentage of average Separate Account Contract Value, and a $30 annual Records Maintenance Charge. |

| 3 | As a percentage of average net assets in the Portfolios. |

| 4 | As a percentage of the Contract Value. |

PAGE 6

| Because your Contract is customizable, the choices you make affect how much you will pay. To help you understand the cost of owning your Contract, the following table shows the lowest and highest cost you could pay each year, based on current charges. This estimate assumes that you do not take withdrawals from the Contract, which could add Withdrawal Charges that substantially increase costs. | ||||||

| LOWEST ANNUAL COST: $1,579(a) |

HIGHEST ANNUAL COST: $2,571(a) |

|||||

| Assumes:

• Investment of $100,000

• 5% annual appreciation

• Least expensive combination of Contract classes and Portfolio fees and expenses

• No optional benefits

• No sales charges

• No additional Purchase Payments, transfers or withdrawals |

Assumes:

• Investment of $100,000

• 5% annual appreciation

• Most expensive combination of Contract classes, optional benefits, and Portfolio fees and expenses

• No sales charges

• No additional Purchase Payments, transfers or withdrawals |

|||||

| (a) | The Lowest and the Highest Annual Costs do not reflect the $30 annual Records Maintenance Charge as the charge applies only to Contracts with less than $50,000 Contract Value. |

| RISKS |

Location in | |||||

| Risk of Loss |

You can lose money by investing in this Contract. | PRINCIPAL RISKS OF INVESTING IN THE CONTRACT | ||||

| Not a Short-Term Investment |

This Contract is not designed for short-term investing and is not appropriate for an investor who needs ready access to cash.

Withdrawal Charges apply for up to 7 years following your last Purchase Payment. They will reduce the value of your Contract if you withdraw money during that time. Further, a negative Market Value Adjustment may apply to amounts withdrawn before the end of a Guaranteed Period under the MVA Option. The |

PRINCIPAL RISKS OF INVESTING IN THE CONTRACT | ||||

PAGE 7

| RISKS |

Location in | |||||

| benefits of tax deferral and the Guaranteed Retirement Income Benefit (if elected) also mean the policy is more beneficial to investors with a long time horizon. Earnings on your Contract are taxed at ordinary income tax rates when You withdraw them, and You may have to pay a penalty if You take a withdrawal before age 591⁄2. | ||||||

| Risks Associated with Investment Options |

• An investment in this Contract is subject to the risk of poor investment performance and can vary depending on the performance of the investment options you choose.

• Each investment option (including the Fixed Account Option and MVA Option) has its own unique risks.

• You should review the investment options (including the Fixed Account Option and MVA Option) before making an investment decision. |

PRINCIPAL RISKS OF INVESTING IN THE CONTRACT | ||||

| Insurance Company Risks |

An investment in the Contract is subject to the risks related to ZALICO. Any obligations (including under the Fixed Account Option and MVA Option), guarantees, and benefits of the Contract are subject to the claims-paying ability of ZALICO. If ZALICO experiences financial distress, it may not be able to meet its obligations to you. More information about ZALICO, including our financial strength ratings, is available upon request from ZALICO by calling 1-800-449-0523. | PRINCIPAL RISKS OF INVESTING IN THE CONTRACT | ||||

| RESTRICTIONS |

||||||

| Investments |

• There are restrictions that may limit the investments that an investor may choose.

• We reserve the right to charge $25 for each transfer when you transfer money between Portfolios in excess of 12 times in a Contract Year.

• ZALICO reserves the right to remove or substitute Portfolios as investment options that are available under the Contract.

• ZALICO has policies and procedures that attempt to detect and deter market timing and other forms of disruptive trading in the Contract, and in those instances, there are additional limits that apply to transfers. |

PRINCIPAL RISKS OF INVESTING IN THE CONTRACT | ||||

PAGE 8

| RISKS |

Location in | |||||

| RESTRICTIONS |

||||||

| Optional Benefits |

• The Guaranteed Retirement Income Benefit does not limit or restrict the investment options you may select under the Contract. We may impose limitations and/or restrictions in the future.

• We may modify or discontinue an optional benefit at any time. |

BENEFITS AVAILABLE UNDER THE CONTRACT | ||||

| TAXES |

||||||

| Tax Implications |

• You should consult with a tax professional to determine the tax implications of an investment in and distributions received under this Contract.

• If you purchase the Contract through a tax-qualified plan or individual retirement account (IRA), you do not get any additional tax benefit.

• Earnings on your Contract are taxed at ordinary income tax rates when you withdraw them, and you may have to pay a penalty if you take a withdrawal before age 59 1/2. |

FEDERAL TAX CONSIDERATIONS | ||||

| CONFLICTS OF INTEREST |

||||||

| Investment Professional Compensation |

Some investment professionals may receive compensation for selling the Contract, in the form of commissions, special compensation, reimbursements for expenses, and other compensation programs. These investment professionals may have a financial incentive to recommend making additional Purchase Payments under this Contract over another investment. | DISTRIBUTION OF CONTRACTS | ||||

| Exchanges |

Some investment professionals may have a financial incentive to offer you a new contract in place of the one you own. You should only consider exchanging your contract if you determine, after comparing the features, fees, and risks of both contracts, that it is preferable for you to purchase the new contract rather than continue to own your existing contract. | DISTRIBUTION OF CONTRACTS | ||||

PAGE 9

The Contract is designed to assist individuals with their long-term retirement planning or other long-term needs through investments in a variety of investment options during the Accumulation Period. The Contract also offers death benefits to protect your designated beneficiaries. Through the annuitization feature, the Contract can supplement your retirement income by providing a stream of income payments. This Contract may be appropriate if you have a long investment time horizon. It is not intended for people who may need to make early or frequent withdrawals.

Accumulation Period

During the Accumulation Period, you can allocate your Purchase Payments to:

| • | a variety of Subaccounts. Each Subaccount invests in a corresponding (mutual fund) Portfolio, each of which has its own investment strategies, investment adviser(s), expense ratios, and returns. |

| • | a Fixed Account, which offers a guaranteed fixed interest rate for stated periods; and |

| • | One or more Guarantee Period of the MVA Option, which offers a guaranteed interest rate, but will be subject to a market value adjustment and possibly a surrender charge if you take a withdrawal before the end of the Guarantee Period. |

Additional information about the Portfolios in which the Subaccounts currently invest is provided in Appendix C: Portfolio Companies Available Under the Contract.

Annuity Period

You can elect to annuitize your Contract and turn your Contract Value into a stream of fixed and/or variable annuity payments from us. Currently, we offer Annuity Options that provide payments for (i) a specified period, (ii) the life of the Annuitant, (iii) the life of the Annuitant and the remainder of the specified period if the Beneficiary is an individual and payments have been made for less than the specified period, or (iv) in the case of joint Annuitants, the life of the surviving Annuitant, with payment adjusted upon the death of the other Annuitant. We may offer other options, at our discretion, where permitted by state law. At the Annuity Date, you can choose to receive fixed payments or variable payments.

Please note that if you annuitize, your Contract Value will be converted to annuity payments and you may no longer withdraw money from your Contract (although certain annuity payments under the GRIB optional benefit may be commutable) and the death benefit will terminate.

MVA Option. You may allocate your Purchase Payments and transfer Contract Value to one or more Guarantee Periods under the MVA Option. Amounts you allocate to one or more Guarantee Periods will earn a guaranteed interest rate, but will be subject to a market value adjustment (MVA) and a possible surrender charge if you take a withdrawal before the end of the Guarantee Period.

Accessing Your Money. You can choose to withdraw your Contract Value at any time (although if you withdraw early, you may have to pay a Withdrawal Charge and/or taxes, including tax penalties).

Tax Treatment. Your Purchase Payments accumulate on a tax-deferred basis. This means your earnings are not taxed until you take money out of your Contract, such as when (1) you make a withdrawal; (2) you receive an annuity payment from the Contract; or (3) upon payment of a death benefit.

Guaranteed Death Benefit. Your Contract includes a Guaranteed Death Benefit that will pay your designated beneficiaries an amount as described in the section titled Benefits Available Under the Contract.

PAGE 10

Guaranteed Retirement Income Benefit. For an additional fee, this benefit provides a minimum fixed annuity guaranteed lifetime income to the Annuitant. This benefit was made available under certain Contracts issued before May 1, 2002 and is no longer offered.

Dollar Cost Averaging. Under our Dollar Cost Averaging program, a predesignated portion of Subaccount Value is automatically transferred monthly, quarterly, semiannually or annually for a specified duration to other Subaccounts, Guarantee Periods and the Fixed Account. There is currently no charge for this service. The Dollar Cost Averaging program is available only during the Accumulation Period.

Systematic Withdrawal Plan. We offer a Systematic Withdrawal Plan (“SWP”) allowing you to pre-authorize periodic withdrawals during the Accumulation Period. You instruct us to withdraw selected amounts, or amounts based on your life expectancy, from the Fixed Account, or from any of the Subaccounts or Guarantee Periods on a monthly, quarterly, semi-annual or annual basis.

PAGE 11

The following tables describe the fees and expenses that you will pay when buying, owning, and surrendering or making withdrawals from the Contract. Please refer to your Contract specifications page for information about the specific fees you will pay each year based on the options you have elected.

The first table describes the fees and expenses that you will pay at the time that you buy the Contract, surrender or make withdrawals from the Contract, or transfer cash value between and among the Subaccounts, the Fixed Account, and the Guarantee Periods. State premium taxes may also be deducted.

Transaction Expenses

| Sales Load Imposed on Purchases (as a percentage of Purchase Payments): |

None | |||

| Maximum Withdrawal Charge4 (as a percentage of Purchase Payments): |

7% |

Withdrawal Charge (as a percentage of Purchase Payments)

| Contribution Year of Withdrawal after Purchase Payments Made |

Withdrawal Charge |

|||

| First year |

7.00% | |||

| Second year |

6.00% | |||

| Third year |

5.00% | |||

| Fourth year |

5.00% | |||

| Fifth year |

4.00% | |||

| Sixth year |

3.00% | |||

| Seventh year |

2.00% | |||

| Eighth year and following |

0.00% | |||

| Maximum Transfer Fee |

$ | 25 | 5 | |

The next table describes the fees and expenses that you will pay each year during the time that you own the Contract, not including Fund fees and expenses.

If you purchased an optional benefit, you will pay additional charges, as shown below.

| 4 | A Contract Owner may withdraw up to the greater of (i) the excess of Contract Value over total Purchase Payments subject to a Withdrawal Charge less prior withdrawals that were previously assessed a Withdrawal Charge and (ii) 10% of the Contract Value in any Contract Year without assessment of any Withdrawal Charge. In certain circumstances we may reduce or waive the Withdrawal Charge. See “Withdrawal Charge.” |

| 5 | We reserve the right to charge a fee of $25 for each transfer of Contract Value in excess of 12 transfers per calendar year. See “Transfers During the Accumulation Period.” |

Annual Contract

| Current | ||||

| Annual Records Maintenance Charge6 |

$ | 30 | ||

Annual Contract Expenses

| Base Contract Expenses7 |

1.416% | |||

| Optional Guaranteed Retirement Income Benefit8 |

0.25% |

The next item shows the minimum and maximum total operating expenses charged by the Funds that you may pay periodically during the time that you own the Contract. A complete list of Funds available under the Contract, including their annual expenses, may be found at the back of this document.

PAGE 12

Annual Fund Expenses9

| Lowest | Highest | |||||||

| Total Annual Fund Operating Expenses (total of all expenses that are deducted from Fund assets, including management fees, 12b-1 fees, and other expenses, before any contractual waivers or reimbursements of fees and expenses) | 0.32 | % | 1.33 | % | ||||

| Net Total Annual Fund Operating Expenses After Reimbursements and Waivers (total of all expenses that are deducted from Fund assets, including management fees, 12b-1 fees, and other expenses, after any contractual waivers or reimbursements of fees and expenses)10 | 0.26 | % | 1.09 | % | ||||

| 6 | The Records Maintenance Charge applies to Contracts with Contract Value less than $50,000 on the date of assessment. In the section entitled “Important Information You Should Consider About Your Contract” earlier in this prospectus, we are required to present this fee as part of the Base Contract expenses. In certain circumstances we may reduce or waive the annual records Maintenance Charge. See “Records Maintenance Charge.” |

| 7 | Base Contract Expenses include administration charges and are calculated as a percentage of average Separate Account Contract Value, If you annuitize the Contract on a variable basis, we will assess a daily Base Contract charge and administration charge at an annual rate of 1.40% on the assets held in the Separate Account. |

| 8 | We no longer offer the Guaranteed Retirement Income Benefit rider. If you have elected the Guaranteed Retirement Income Benefit rider and your rider remains in force, the 0.25% rider charge (annual rate) will continue to be deducted on the last business day of each contract quarter. The rider charge will be deducted pro rata as a percentage of Contract Value from each Subaccount, Guarantee Period, and the Fixed Account in which you have Contract Value until you annuitize or surrender the Contract or the Annuitant reaches age 91, whichever comes first. |

| 9 | The Fund expenses used to prepare this table were provided to us by the Fund(s). We have not independently verified such information. The expenses shown are those incurred for the year ended December 31, 2021. Current or future expenses may be greater or less than those shown. |

| 10 | The range of Net Total Annual Fund Operating Expenses after Reimbursements and Waivers takes into account contractual arrangements for those Funds that require a Fund’s investment adviser to reimburse or waive Fund expenses for no less than one year from the date of the Fund’s current prospectus. These arrangements may only be terminated with the consent of a fund’s board. For more information about these arrangements, consult the prospectuses for the Funds. |

EXAMPLE

This Example is intended to help you compare the cost of investing in the Contract with the cost of investing in other variable annuity contracts. These costs include transaction expenses, annual Contract expenses, and Annual Fund Expenses.

The Example assumes that you invest $100,000 in the Contract for the time periods indicated. The Example also assumes that your investment has a 5% return each year and assumes the most expensive combination of Annual Fund Expenses and optional benefits available for an additional charge. In addition, this Example assumes no transfers were made and no premium taxes were deducted. If these arrangements were considered, the expenses shown would be higher. This Example also does not take into consideration any fee waiver or expense reimbursement arrangements of the Funds. If these arrangements were taken into consideration, the expenses shown would be lower.

PAGE 13

Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

| (1) | If you surrender your Contract at the end of the applicable time period: |

| 1 year |

3 years |

5 years |

10 years |

|||||||||||

| $ | 9920 | $ | 13,821 | $ | 18,921 | $ | 30,608 | |||||||

| (2) | a. If you annuitize your Contract at the end of the available time period under Annuity Option 2, 3, 4, or under Annuity Option 1 for a period of five years or more*: |

| 1 year |

3 years |

5 years |

10 years |

|||||||||||

| $ | 2,761 | $ | 8,472 | $ | 14,446 | $ | 30,608 | |||||||

| b. | If you annuitize your Contract at the end of the available time period under Annuity Option 1 for a period of less than five years*: |

| 1 year |

3 years |

5 years |

10 years |

|||||||||||

| $ | 9,920 | $ | 13,821 | $ | 18,921 | $ | 30,608 | |||||||

| (3) | If you do not surrender or annuitize your Contract at the end of the applicable time period: |

| 1 year |

3 years |

5 years |

10 years |

|||||||||||

| $ | 2,761 | $ | 8,472 | $ | 14,446 | $ | 30,608 | |||||||

| * | Withdrawal Charges do not apply if the Contract is annuitized under Annuity Option 2, 3 or 4, or under Annuity Option 1 for a period of five years or more. Withdrawal Charges do apply if the Contract is annuitized under Annuity Option 1 for a period of less than five years. |

The Example is an illustration and does not represent past or future expenses and charges of the Subaccounts. Your actual expenses may be greater or less than those shown. Similarly, your rate of return may be more or less than the 5% assumed rate in the Example.

The Records Maintenance Charge of $30 is reflected as an annual charge of 0.013% that is determined by dividing total Records Maintenance Charges collected during 2021 ($99,812) by total average net assets attributable to the Contract during 2021 ($777,443,766).

PRINCIPAL RISKS OF INVESTING IN THE CONTRACT

Investing in the Contract involves risks, This section is intended to summarize the principal risks of investing in the Contract. Additional risks and details regarding various risks and benefits of investing in the Contract are described in the relevant sections of the Prospectus and SAI.

The Contract is not suitable as a short-term savings vehicle.

The Contract described in this Prospectus is no longer available for sale. However, we do continue to administer the Contracts and, subject to limitations, you may continue making Purchase Payments to your existing Contract.

Poor Investment Performance. You can lose money by investing in this Contract, including loss of principal. An investment in this Contract is subject to the risk of poor investment performance and can vary depending on the performance of the Subaccounts you choose. Each Subaccount invests in a corresponding Portfolio and you can make or lose money depending upon market conditions. The investment performance of the Subaccount(s) you select affects the value of your Contract and, therefore, affects the amount of the annuity payments available at the time of annuitization.

Insurance Company Risks. An investment in the Contract is subject to the risks related to ZALICO. Any obligations (including those of the Fixed Account and Guarantee Periods), guarantees, and benefits of

PAGE 14

the Contract are subject to the claims-paying ability of ZALICO. If ZALICO experiences financial distress, it may not be able to meet its obligations to you. More information about ZALICO is available upon request from ZALICO by calling the Service Center at .

Liquidity Risk. This Contract is not designed for short-term investing and is not appropriate for an investor who needs ready access to cash. Withdrawal Charges apply for up to seven Contribution Years after your last Purchase Payment. They will reduce the value of your Contract if you withdraw money during that time. If you need to make early or excess withdrawals, they could substantially reduce or even terminate the benefits available under the Contract. There may be adverse tax consequences if you make early withdrawals under the Contract. The benefits of tax deferral and the Contract’s living benefit protection also mean the Contract is better for investors with a long time horizon.

MVA Option Risk. Market Value Adjustments are sensitive to changes in interest rates. If you withdraw money from a Guarantee Period before its term has expired, and during a period of rising interest rates, you likely will be assessed a negative Market Value Adjustment. In times of rising interest rates, the negative Market Value Adjustment could result in a substantial downward adjustment to your Contract Value. Before you take a withdrawal from a Guarantee Period, you should know its expiration date, and ask the Service Center to calculate whether a Market Value Adjustment will apply and how much it will be.

Taxation Risk. Although the provisions of the Code relevant to the Contract are generally described under “Federal Tax Considerations,” an investor should consult its own tax advisor concerning the effects of federal, state, local and foreign tax law on the Contract. No assurance can be given that, even if the tax provisions currently applicable to the Contract are favorable, the law or regulations or interpretations thereunder will not change and the Contract may be disadvantaged.

Cybersecurity and Certain Business Continuity Risks. Our business is largely conducted through complex information technology and digital communications and data storage networks and systems operated by us and our service providers or other business partners (e.g., the firms involved in the distribution and sale of our products), and these operations rely on the secure processing, storage and transmission of confidential and other information. For example, many routine operations, such as processing your requests and elections and day-to-day record keeping, are all executed through computer networks and systems.

We have established administrative and technical controls and business continuity and resilience plans to protect our operations against attempts by unauthorized third parties to improperly access, modify, disrupt the operation of, or prevent access to critical networks or systems or data within them (a “cyber-attack”). Notwithstanding these protocols, there are inherent limitations in our plans and systems, including the possibility that certain risks have not been identified or that unknown threats may emerge in the future. Accordingly, successful cyber-attacks may be mounted against us, our service providers and other business partners, and such cyber-attacks could have a material, negative impact on us well as individual owners and their Contracts. In addition, unanticipated problems with, or failures of, our disaster recovery systems and business continuity plans could have a material impact on our ability to conduct business and on our financial condition and operations Other disruptive events, including (but not limited to) natural disasters, military actions, and public health crises, may adversely affect our ability to conduct business.

COVID-19 and Market Conditions Risks

The COVID-19 pandemic has at times resulted in or contributed to significant financial market volatility, travel restrictions and disruptions, quarantines, an uncertain interest rate environment, elevated inflation, global business, supply chain, and employment disruptions affecting companies across various industries, government and central bank interventions, wide-ranging changes in consumer behavior, as well as general concern and uncertainty that has negatively affected the economic environment. COVID-19 vaccine distribution in the United States has resulted in more flexible quarantine guidelines, increased consumer demand, and resurgence of travel. However, vaccination rates and vaccine availability abroad, specifically in

PAGE 15

developing and emerging market countries, continue to lad, and new COVID-19 variants have led to waves of increased hospitalizations and death. At this time, it continues to not be possible to estimate the severity or duration of the pandemic, including the severity, duration and frequency of any additional “waves” or emerging variants of COVID-19.

It likewise remains not possible to predict or estimate the longer-term effects of the pandemic, or any actions taken to contain or address the pandemic, on our business and financial condition, the financial markets, and the economy at large. ZALICO has implemented risk management and contingency plans and continues to closely monitor this evolving situation, including the impact on services provided by third-party vendors. However, there can be no assurance that any future impact from the COVID-19 pandemic will not be material to ZALICO and/or with respect to the services ZALICO or its customers receive from third-party vendors. Significant market volatility and negative investment returns in the financial markets resulting from the COVID-19 pandemic and market conditions could have a negative impact on the performance of the Funds or Portfolios.

Terrorism and Security Risk. The continued threat of terrorism, ongoing or potential military and other actions such as the Russia-Ukraine conflict, and heightened security measures may cause significant volatility in global financial markets and result in loss of life, property damage, additional disruptions to commerce and reduced economic activity. The value of our investment portfolio may be adversely affected by declines in the credit and equity markets and reduced economic activity caused by such threats. Additionally, the performance of the Funds or Portfolios may be adversely affected. This risk could be higher for Funds or Portfolios with exposure to European or Russian markets. Companies in which we maintain investments may suffer losses as a result of financial, commercial or economic disruptions, and such disruptions might affect the ability of those companies to pay interest or principal on their securities or mortgage loans. Terrorist or military actions also could disrupt our operations centers and result in higher than anticipated claims under our insurance policies.

PAGE 16

ZALICO, THE MVA OPTION, THE SEPARATE ACCOUNT AND THE FUNDS

A. Zurich American Life Insurance Company

Zurich American Life Insurance Company is the depositor of the Separate Account and is located at 1299 Zurich Way, Schaumburg, Illinois 60196.

B. The Guarantee Periods of the MVA Option

During the Accumulation Period, you may allocate Purchase Payments and Contract Value to one or more Guarantee Periods of the MVA Option with durations generally of one to ten years. You may choose a different Guarantee Period by pre-authorized telephone instructions or by giving us written notice (See “Guarantee Periods of the MVA Option”). The MVA Option may not be available in all states. At our discretion, we may offer additional Guarantee Periods or limit the number of Guarantee Periods available to three. The circumstances under which we may limit the number of Guarantee Periods include changes in the market conditions or an unexpected increase in the costs of hedging our exposure under certain Guarantee Periods.

The amounts you allocate to the MVA Option are invested under the laws regulating our General Account. Assets supporting the amounts allocated to Guarantee Periods are held in a “nonunitized” separate account. A non-unitized separate account is a separate account in which you do not participate in the performance of the assets held in the separate account. The assets of the non-unitized separate account are held to fund our guaranteed obligations. The “nonunitized” separate account is insulated, so that the assets of the separate account are not chargeable with liabilities arising out of the business conducted by any other separate account or out of any other business we may conduct. In addition, our General Account assets are available to fund benefits under the Contracts.

State insurance laws concerning the nature and quality of investments regulate our General Account investments and any non-unitized separate account investments. These laws generally permit investment in federal, state and municipal obligations, preferred and common stocks, corporate bonds, real estate mortgages, real estate and certain other investments.

We consider the return available on the instruments in which Contract proceeds are invested when establishing Guaranteed Interest Rates. This return is only one of many factors considered in establishing Guaranteed Interest Rates. (See “The Accumulation Period-4. Establishment of Guaranteed Interest Rates.”)

Our investment strategy for the non-unitized separate account is generally to match Guarantee Period liabilities with assets, such as debt instruments. We expect to invest in debt instruments such as:

| • | securities issued by the United States Government or its agencies or instrumentalities, which issues may or may not be guaranteed by the United States Government; |

| • | debt securities which have an investment grade, at the time of purchase, within the four highest grades assigned by Moody’s Investors Services, Inc. (“Moody’s”) (Aaa, Aa, A or Baa), Standard & Poor’s Corporation (“Standard & Poor’s”) (AAA, AA, A or BBB), or any other nationally recognized rating service; |

| • | other debt instruments including issues of or guaranteed by banks or bank holding companies and corporations, which obligations, although not rated by Moody’s or Standard & Poor’s, are deemed by our management to have an investment quality comparable to securities which may be otherwise purchased; and |

| • | options and futures transactions on fixed income securities. |

We are not obligated to invest the amounts allocated to the MVA Option according to any particular strategy, except as state insurance laws may require.

PAGE 17

We established the ZALICO Variable Annuity Separate Account on May 29, 1981 pursuant to Illinois law. The Separate Account is registered as a unit investment trust under the Investment Company Act of 1940, as amended (“1940 Act”). The SEC does not supervise the management, investment practices or policies of the Separate Account or ZALICO.

Benefits provided under the Contracts are our obligations. Although the assets in the Separate Account are our property, they are held separately from our other assets and are not chargeable with liabilities arising out of any other business we may conduct. Income, capital gains and capital losses, whether or not realized, from the assets allocated to the Separate Account are credited to or charged against the Separate Account without regard to the income, capital gains and capital losses arising out of any other business we may conduct.

Nineteen Subaccounts of the Separate Account are currently available. Each Subaccount invests exclusively in shares of one of the corresponding Funds or Portfolios. We may add or delete Subaccounts in the future. Not all Subaccounts may be available in all jurisdictions or under all Contracts.

The Separate Account purchases and redeems shares from the Funds at net asset value. We redeem shares of the Funds as necessary to pay withdrawals, provide benefits, to deduct Contract charges and to transfer assets from one Subaccount to another as you request. All dividends and capital gains distributions received by the Separate Account from a Fund or Portfolio are reinvested in that Fund or Portfolio at net asset value and retained as assets of the corresponding Subaccount.

The Separate Account’s financial statements appear in the Statement of Additional Information.

The Portfolios, which sell their shares to the Subaccounts, may discontinue offering their shares to the Subaccounts. We will not discontinue a Subaccount available for investment without receiving the necessary approvals, if any, from the SEC and applicable state insurance departments. We will notify you of any changes. We reserve the right to make other structural and operational changes affecting the Separate Account.

A description of each Fund available under the Contract, including each Fund’s name, type, investment adviser and any sub-adviser, current expenses and performance is available under Appendix C.

You can also find more detailed information about each Fund in the Fund prospectus. You can obtain free copies of the Fund prospectuses by contacting us at 1-800-449-0523 or online at http://dfinview.com/zalico/TAHD/ZALI00001.

The Funds provide investment vehicles for variable life insurance and variable annuity contracts and, in the case of Janus Aspen Series, for certain qualified retirement plans. Shares of the Funds are sold only to insurance company separate accounts and qualified retirement plans. Shares of the Funds may be sold to separate accounts of other insurance companies, whether or not affiliated with us.

The Funds or Portfolios offered through the Contracts are selected by ZALICO, and ZALICO may consider various factors, including, but not limited to asset class coverage, the strength of the investment adviser’s (and/or subadviser’s) reputation and tenure, brand recognition, performance, and the capability and qualification of each investment firm. We also consider whether the Fund or Portfolio or one of its service providers (e.g., the investment adviser, administrator and/or distributor) will make payments to us in connection with certain administrative, marketing, and support services, or whether the Funds or Portfolios adviser was an affiliate. We review the Portfolios periodically and may remove a Portfolio, or limit its availability to new premiums and/or transfers of Contract Value if we determine that a Portfolio no longer satisfies one or more of the selection criteria and/or if the Portfolio has not attracted significant allocations from Contract Owners.

PAGE 18

You are responsible for choosing to invest in the Subaccounts that, in turn, invest in the Funds or Portfolios. You are also responsible for choosing the amounts allocated to each Subaccount that are appropriate for your own individual circumstances and your investment goals, financial situation, and risk tolerance. Since you bear the investment risk of investing in the Subaccounts, you should carefully consider any decisions regarding allocations of Purchase Payments and Contract Value to each Subaccount.

In making your investment selections, we encourage you to thoroughly investigate all of the information regarding the Funds or Portfolios that is available to you, including each Fund or Portfolio’s prospectus, statement of additional information, and annual and semi-annual reports. Other sources such as the Fund or Portfolio’s website or newspapers and financial and other magazines provide more current information, including information about any regulatory actions or investigations relating to a Fund or Portfolio. After you select Subaccounts in which to allocate Purchase Payments or Contract Value, you should monitor and periodically re-evaluate your investment allocations to determine if they are still appropriate.

You bear the risk that the Contract Value of your Contract may decline as a result of negative investment performance of the Subaccounts you have chosen.

We do not provide investment advice and we do not recommend or endorse any of the particular Funds or Portfolios available as variable options in the Contract.

Administrative, Marketing, and Support Services Fees.

The following applies to the Scudder DestinationsSM Annuity:

The Funds and Portfolios currently available for investment under the Contract do not charge 12b-1 fees.

We may receive payments from some of the Funds’ service providers in connection with certain administrative and other services we perform and expenses we incur. The amount of the payment is based on a percentage of the assets of the particular Funds attributable to the Contract and/or to certain other variable insurance products that we issue. These percentages currently range from .10% to .25%. Some service providers pay us more than others. These payments may be derived, in whole or in part, from the advisory fee deducted from Portfolio assets. Contract owners, through their indirect investment in the Portfolios, bear the costs of these advisory fees (see the Portfolios’ prospectuses for more information).

The chart below provides the current maximum percentages of fees that we anticipate will be paid to us on an annual basis:

Incoming Payments to ZALICO

| From the following Funds or their Service Providers: |

Maximum % of assets* | |||

| AIM |

.25 | % | ||

| Alger |

.25 | % | ||

| BNY Mellon Sustainable U.S. Equity Portfolio, Inc. (formerly The Dreyfus Sustainable U.S. Equity Portfolio, Inc.) |

.25 | % | ||

| From the following Funds or their Service Providers: |

Maximum % of assets* | |||

| Deutsche |

.25 | % | ||

| Janus Aspen |

.25 | % | ||

| * | Payments are based on a percentage of the average assets of each Fund owned by the Subaccounts available under this Contract and/or under certain other variable insurance products offered by our affiliates and us. |

PAGE 19

Additional amounts we may receive, as applicable to both the Scudder DestinationsSM Annuity and the Farmers Variable Annuity I:

We and/or our affiliates also may directly or indirectly receive additional amounts or different percentages of assets under management from some of the Funds’ service providers with regard to other variable insurance products we issue. These payments may be derived, in whole or in part, from the profits the investment adviser or sub-adviser realizes from the advisory fee deducted from Portfolio assets. Contract Owners, through their indirect investment in the Funds, bear the costs of these advisory fees. Certain investment advisers or their affiliates may provide us and/or selling firms with wholesaling services to assist us in servicing the Contract, may pay us and/or certain affiliates and/or selling firms amounts to participate in sales meetings or may reimburse our sales costs, and may provide us and/or certain affiliates and/or selling firms with occasional gifts, meals, tickets or other compensation. The amounts in the aggregate may be significant and may provide the investment adviser (or other affiliates) with increased access to us and to our affiliates.

Proceeds from these payments by the Funds or their service providers may be used for any corporate purpose, including payment of expenses that we and/or our affiliates incur in distributing and administering the Contracts, and that we incur, in our role as intermediary, in marketing and administering the underlying Portfolios. We and our affiliates may profit from these payments.

For further details about the compensation payments we make in connection with the sale of the Contracts, see “Distribution of Contracts” in this Prospectus.

We reserve the right to make additions to, deletions from, or substitutions for the shares held by the Separate Account or that the Separate Account may purchase. We may eliminate the shares of any of the Funds or Portfolios and substitute shares of another portfolio or of another investment company, if the shares of a Fund or Portfolio are no longer available for investment, or if in our judgment further investment in any Fund or Portfolio becomes inappropriate in view of the purposes of the Separate Account. We will not substitute any shares attributable to your interest in a Subaccount without prior notice and the SEC’s prior approval, if required. The Separate Account may purchase other securities for other series or classes of contracts, or may permit a conversion between series or classes of contracts on the basis of requests made by Owners.

We may establish additional subaccounts of the Separate Account, each of which would invest in a new portfolio of the Funds, or in shares of another investment company. New subaccounts may be established when, in our discretion, marketing needs or investment conditions warrant. New subaccounts may be made available to existing Owners as we determine. We may also eliminate or combine one or more subaccounts, transfer assets, or substitute one subaccount for another subaccount, if, in our discretion, marketing, tax, or investment conditions warrant. We will notify all Owners of any such changes.

If we deem it to be in the best interests of persons having voting rights under the Contract, the Separate Account may be: (a) operated as a management company under the 1940 Act; (b) deregistered under the 1940 Act in the event such registration is no longer required; or (c) combined with our other separate accounts. To the extent permitted by law, we may transfer the assets of the Separate Account to another separate account or to the General Account.

Amounts allocated or transferred to the Fixed Account are part of our General Account, supporting insurance and annuity obligations. Interests in the Fixed Account are not registered under the Securities Act of 1933 (“1933 Act”), and the Fixed Account is not registered as an investment company under the 1940 Act. Accordingly, neither the Fixed Account nor any interests therein generally are subject to the provisions of the 1933 or 1940 Acts. Disclosures regarding the Fixed Account, however, may be subject to the general

PAGE 20

provisions of the federal securities laws relating to the accuracy and completeness of statements made in prospectuses.

Under the Fixed Account Option, we pay a fixed interest rate for stated periods. This Prospectus describes only the aspects of the Contract involving the Separate Account and the MVA Option, unless we refer to fixed accumulation and annuity elements.

We guarantee that payments allocated to the Fixed Account earn a minimum fixed interest rate not less than the minimum rate allowed by state law. At our discretion, we may credit interest in excess of the minimum guaranteed rate. We reserve the right to change the rate of excess interest credited. We also reserve the right to declare different rates of excess interest depending on when amounts are allocated or transferred to the Fixed Account. As a result, amounts at any designated time may be credited with a different rate of excess interest than the rate previously credited to such amounts and to amounts allocated or transferred at any other designated time.

This Contract is no longer offered for sale, although we continue to accept additional Purchase Payments under the Contract. The minimum additional Purchase Payment is $500 ($50 or more for IRAs). The minimum additional Purchase Payment is $100 if you authorize us to draw on an account via check or electronic debit. Effective on and after August 1, 2014, the maximum total Purchase Payments under the Contract is $10,000. Cumulative Purchase Payments in excess of $10,000 require our prior approval. We reserve the right to waive or modify the minimum and maximum initial and subsequent Purchase Payments limits. The Internal Revenue Code may also limit the maximum annual amount of Purchase Payments. An allocation to a Subaccount, the Fixed Account or a Guarantee Period must be at least $500.

We may, at any time, amend the Contract in accordance with changes in the law, including applicable tax laws, regulations or rulings, and for other purposes. We will notify you in writing of such amendments.

During the Accumulation Period, you may assign the Contract or change a Beneficiary at any time by signing our form and sending our form back to the Service Center completed and in good order. No assignment or Beneficiary change is binding on us until we receive our form in good order. We reserve the right, except to the extent prohibited by applicable laws, regulations, or actions of the State insurance commissioner, to require that the assignment will be effective only upon acceptance by us, and to refuse assignments or transfers at any time on a non-discriminatory basis. We assume no responsibility for the validity of the assignment or Beneficiary change. An assignment may subject you to immediate tax liability and a 10% tax penalty.

Amounts payable during the Annuity Period may not be assigned or encumbered. In addition, to the extent permitted by law, annuity payments are not subject to levy, attachment or other judicial process for the payment of the Annuitant’s debts or obligations.

You designate the Beneficiary. If you or the Annuitant die, and no designated Beneficiary or contingent beneficiary is alive at that time, we will pay your or the Annuitant’s estate.

Under a Qualified Plan Contract, the provisions of the applicable plan may prohibit a change of Beneficiary. Generally, an interest in a Qualified Plan Contract may not be assigned.

1. Application of Purchase Payments.

You select how to allocate your Purchase Payments among the Subaccount(s), Guarantee Periods, and/or Fixed Account. The amount of each Purchase Payment allocated to a Subaccount is based on the value of an Accumulation Unit, as next computed after we receive the Purchase Payment in good order at the Service Center or the bank we have designated to receive Purchase Payments (“the bank”). Generally, we

PAGE 21

determine the value of an Accumulation Unit as of 4:00 p.m. Eastern Time on each day that the New York Stock Exchange (“NYSE”) is open for trading. Purchase Payments that we receive at the Service Center in good order after 4:00 p.m. Eastern Time will be priced using the Accumulation Unit values next determined at the end of the next regular trading session of the NYSE. Electronic payments received by wire or through electronic credit or debit transactions at the bank in good order after 4:00 p.m. Eastern Time will be priced using the Accumulation Unit values next determined at the end of the next regular trading session of the NYSE. Please contact the Service Center for wiring instructions or instructions on automatic electronic debiting.

Purchase Payments allocated to a Guarantee Period or to the Fixed Account begin earning interest one day after we receive them in good order at the Service Center or the bank. Upon receipt of a Purchase Payment to be allocated to a Subaccount in good order, we determine the number of Accumulation Units credited by dividing the Purchase Payment allocated to a Subaccount by the Subaccount’s Accumulation Unit value, as next computed after we receive the Purchase Payment.

Some of the Funds reserve the right to delay or refuse purchase requests from the Separate Account, as further described in their prospectuses and/or statements of additional information. Therefore, if you request a transaction under your Contract that is part of a purchase request delayed or refused by a Fund, we will be unable to process your request. In that event, we will notify you promptly in writing or by telephone.

The number of Accumulation Units will not change due to investment experience. Accumulation Unit value, on the other hand, varies to reflect the investment experience of the Subaccount and the assessment of charges against the Subaccount, other than the Withdrawal Charge, the Records Maintenance Charge and Guaranteed Retirement Income Benefit Charge (See “BENEFITS AVAILABLE UNDER THE CONTRACT”). The number of Accumulation Units is reduced when the Records Maintenance Charge and Guaranteed Retirement Income Benefit Charge are assessed.

Each Subaccount has an Accumulation Unit value. When Purchase Payments or other amounts are allocated to a Subaccount, the number of units purchased is based on the Subaccount’s Accumulation Unit value at the end of the current Valuation Period. When amounts are transferred out of or deducted from a Subaccount, units are redeemed in a similar manner.

The Accumulation Unit value for each subsequent Valuation Period is the investment experience factor for that Valuation Period times the Accumulation Unit value for the preceding Valuation Period. Each Valuation Period has a single Accumulation Unit value which applies to each day in the Valuation Period.

Each Subaccount has its own investment experience factor. The investment experience of the Separate Account is calculated by applying the investment experience factor to the Accumulation Unit value in each Subaccount during a Valuation Period.

The investment experience factor of a Subaccount for any Valuation Period is determined by the following formula:

(a divided by b) minus c, where:

“a” is:

| • | the net asset value per share of the Portfolio held in the Subaccount as of the end of the current Valuation Period; plus |

| • | the per share amount of any dividend or capital gain distributions made by the Portfolio held in the Subaccount, if the “ex-dividend” date occurs during the current Valuation Period; plus or minus |

| • | a credit or charge for any taxes reserved for the current Valuation Period which we determine have resulted from the investment operations of the Subaccount; |

PAGE 22

“b” is the net asset value per share of the Portfolio held in the Subaccount as of the end of the preceding Valuation Period; and

“c” is the factor representing asset-based charges (the mortality and expense risk and administration charges).

3. Guarantee Periods of the MVA Option.

You may allocate Purchase Payments and transfer Contract Value to one or more Guarantee Periods with durations of one to ten years under the MVA Option. Amounts you allocate to one or more Guarantee Period will earn a guaranteed interest rate, but will be subject to a market value adjustment (MVA) and a possible surrender charge if you take a withdrawal before the end of the Guarantee Period. Interest is credited daily at the effective annual rate.

The MVA Option may not be available in all states. The MVA Option is only available during the Accumulation Period. We may limit the number of Guarantee Periods we offer at our discretion. We credit interest daily to amounts allocated to the MVA Option. We declare the rate at our sole discretion. We guarantee amounts allocated to the MVA Option at Guaranteed Interest Rates for the Guarantee Periods you select. These guaranteed amounts are subject to any applicable Withdrawal Charge, Market Value Adjustment or Records Maintenance Charge. We will not change a Guaranteed Interest Rate for the duration of the Guarantee Period. However, Guaranteed Interest Rates for subsequent Guarantee Periods are set at our discretion. At the end of a Guarantee Period, a new Guarantee Period for the same duration starts, unless you timely elect another Guarantee Period. The interests under the Contract relating to the MVA Option are not registered under the 1933 Act and the insulated, nonunitized separate account supporting the MVA Option is not registered as an investment company under the 1940 Act.

The following example illustrates how we credit Guarantee Period interest.

EXAMPLE OF GUARANTEED INTEREST RATE ACCUMULATION

| Purchase Payment | $40,000.00 | |

| Guarantee Period | 5 Years | |

| Guaranteed Interest Rate | 3.00% Effective Annual Rate | |

| Year |

Interest Credited During Year |

Cumulative Interest Credited |

||||||||

| 1 | $ | 1,200.00 | $ | 1,200.00 | ||||||

| 2 | 1,236.00 | 2,436.00 | ||||||||

| 3 | 1,273.08 | 3,709.08 | ||||||||

| 4 | 1,311.27 | 5,020.35 | ||||||||

| 5 | 1,350.61 | 6,370.96 | ||||||||

Accumulated value at the end of 5 years is:

$40,000.00 + $6,370.96 = $46,370.96

Note: This example assumes that no withdrawals or transfers are made during the five-year period. If you make withdrawals or transfers during this period, Market Value Adjustments and Withdrawal Charges apply.

The hypothetical interest rate is not intended to predict future Guaranteed Interest Rates. Actual Guaranteed Interest Rates for any Guarantee Period may be more than that shown.

At the end of any Guarantee Period, we send written notice of the beginning of a new Guarantee Period. A new Guarantee Period for the same duration starts unless you elect another Guarantee Period within 30 days after the end of the terminating Guarantee Period. You may choose a different Guarantee Period by calling the Service Center or by mailing us written notice in good order. You should not select a

PAGE 23

new Guarantee Period extending beyond the Annuity Date. Otherwise, the Guarantee Period amount available for annuitization will be subject to Market Value Adjustments and may be subject to Withdrawal Charges. In a rising interest rate environment, the Market Value Adjustment could result in a substantial downward adjustment to your Contract Value. (See “Market Value Adjustment” and “Withdrawal Charge” below.)

The amount reinvested at the beginning of a new Guarantee Period is the Guarantee Period Value for the Guarantee Period just ended. The Guaranteed Interest Rate in effect when the new Guarantee Period begins applies for the duration of the new Guarantee Period.

You may call or write us at the Service Center for the new Guaranteed Interest Rates.

4. Establishment of Guaranteed Interest Rates.

We declare the Guaranteed Interest Rates for each of the durations of Guarantee Periods from time to time at our discretion. Once established, rates are guaranteed for the respective Guarantee Periods. We advise you of the Guaranteed Interest Rate for a chosen Guarantee Period when we receive a Purchase Payment, when a transfer is effectuated or when a Guarantee Period renews. Withdrawals of Accumulated Guarantee Period Value are subject to Withdrawal Charges and Records Maintenance Charges and may be subject to a Market Value Adjustment. (See “Market Value Adjustment” below.)

We have no specific formula for establishing the Guaranteed Interest Rates. The determination may be influenced by, but not necessarily correspond to, the current interest rate environment. (See “Guarantee Periods of the MVA Option”.) We may also consider, among other factors, the duration of a Guarantee Period, regulatory and tax requirements, sales commissions and administrative expenses we bear, and general economic trends.

We make the final determination of the Guaranteed Interest Rates to be declared. We cannot predict or guarantee the level of future Guaranteed Interest Rates.

On any Valuation Date, Contract Value equals the total of:

| • | the number of Accumulation Units credited to each Subaccount, times |

| • | the value of a corresponding Accumulation Unit for each Subaccount, plus |

| • | your Accumulated Guarantee Period Value in the MVA Option, plus |

| • | your interest in the Fixed Account. |

6. Transfers During the Accumulation Period.

During the Accumulation Period, you may transfer the Contract Value among the Subaccounts, the Guarantee Periods and the Fixed Account subject to the following provisions:

| • | the amount transferred must be at least $100 unless the total Contract Value attributable to a Subaccount, Guarantee Period or Fixed Account is transferred; |

| • | the Contract Value remaining in a Subaccount, Guarantee Period or Fixed Account must be at least $500 unless the total value is transferred; |

| • | transfers may not be made from any Subaccount to the Fixed Account over the six months following any transfer from the Fixed Account into one or more Subaccounts; |

| • | transfers from the Fixed Account may be made one time during the Contract Year during the 30 days following an anniversary of a Contract Year; and |

| • | transfer requests we receive must be in good order. |

PAGE 24

We may charge a $25 fee for each transfer in excess of 12 transfers per calendar year. However, transfers made pursuant to the Asset Allocation and Dollar Cost Averaging programs do not count toward these 12 transfers. In addition, transfers of Guarantee Period Value are subject to Market Value Adjustment unless the transfer is made within 30 days of the end of the Guarantee Period. Because a transfer before the end of a Guarantee Period is subject to a Market Value Adjustment, the amount transferred from the Guarantee Period may be more or less than the requested dollar amount.

We will make transfers pursuant to your mailed, faxed or telephone instructions that specify in detail the requested changes and are in good order. Transfers involving a Subaccount are based upon the Accumulation Unit values, as next calculated after we receive transfer instructions in good order at the Service Center. We may suspend, modify or terminate the transfer provision. We disclaim all liability if we follow in good faith instructions you give to us in accordance with our procedures, including requests for personal identifying information, that are designed to limit unauthorized use of the privilege. Therefore, you bear the risk of loss in the event of a fraudulent telephone transfer.

Mail, Fax, and Telephone Access. You may request transfers in writing by mailing your request (in good order) to our Service Center, or by faxing your request (in good order) to our Service Center at 1-866-605-3962. You may also request transfers by telephone by calling our Service Center at 1-800-449-0523 and providing us with all required information.

Website Access. You may request transfers through our website. Our website address at www.zurichamericanlifeinsurance.com is available 24 hours a day. Our website will allow you to request transfers among the Subaccounts, Fixed Account, and the Guarantee Periods and inquire about your Contract. To use the website for access to your Contract information or to request transfers, you must enter your Contract number and Personal Identification Number (PIN), which you can obtain from our Service Center.

Pricing of Transfers. We will price any transfer request that we receive in good order at the Service Center (by mail, fax, or telephone) or through our website address before the NYSE closes for regular trading (usually, 4:00 p.m. Eastern Time) using the Accumulation Unit values next determined at the end of that regular trading session of the NYSE.

And we will price any transfer request that we receive in good order at the Service Center (by mail, fax, or telephone) or through our website after the close of the regular business session of the NYSE, on any day the NYSE is open for regular trading, using the Accumulation Unit values next determined at the end of the next regular trading session of the NYSE.

E-mail Access. Currently, we do not allow transfer requests or withdrawals by e-mail. You may e-mail us through our website to request an address change or to inquire about your Contract. Please identify your Contract number in any transaction request or correspondence sent to us by e-mail.

Limitations on Transfers. The following transfers must be requested through standard first-class United States mail and must have an original signature:

| • | transfers in excess of $250,000, per Contract, per day, and |

| • | transfers into and out of the DWS International Growth VIP, the DWS Global Small Cap VIP, or the DWS CROCI® International VIP Subaccounts in excess of $50,000, per Contract, per day. |

These administrative procedures have been adopted under the Contract to protect the interests of the remaining Contract Owners from the adverse effects of frequent and large transfers into and out of variable annuity Subaccounts that can adversely affect the investment management of the underlying Funds or Portfolios.

We reserve the right to further amend the transfer procedures in the interest of protecting remaining Contract Owners.

PAGE 25

Some of the Funds reserve the right to delay or refuse purchase requests from the Separate Account, as further described in their prospectuses and/or statements of additional information. Therefore, if you request a transaction under your Contract that is part of a purchase request delayed or refused by a Fund, we will be unable to process your request. In that event, we will notify you promptly in writing or by telephone.

Additional Telephone, Fax, and Online Access Rules and Conditions. We will employ reasonable procedures to confirm that telephone, fax, e-mail and website instructions are genuine. Such procedures may include confirming that instructions are in good order, requiring forms of personal identification prior to acting upon any telephone, fax, e-mail and website instructions, providing written confirmation of transactions to you, and/or tape recording telephone instructions and saving fax, e-mail and website instructions received from you. We disclaim all liability if we follow in good faith instructions given in accordance with our procedures that are designed to limit unauthorized use of the telephone, fax, e-mail and website privileges. Therefore, you bear the risk of loss in the event of a fraudulent telephone, fax, e-mail and website request.

In order to access our website or our automated customer response system, you will need to obtain a PIN by calling into the Service Center. You should protect your PIN, because the automated customer response system will be available to your representative of record and to anyone who provides your PIN. We will not be able to verify that the person providing electronic instructions is you or authorized by you.