UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark one)

☐ REGISTRATION STATEMENT PURSUANT TO

SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒ ANNUAL REPORT PURSUANT TO SECTION 13

OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended March 31, 2025

OR

☐ TRANSITION REPORT PURSUANT TO SECTION

13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to

_________

OR

☐ SHELL COMPANY REPORT PURSUANT TO SECTION

13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company

report __________

Commission file number 001-42594

(Exact name of the Registrant as specified in

its charter)

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

| | 140 Paya Lebar Road #07-02

AZ @ Paya Lebar, Singapore 409015 | |

(Address of principal executive offices)

Eng Chye Koh, Chief Executive Officer and Chairman

Tel: +65 3105 1699

Email: ir@io3.sg

| | 140 Paya Lebar Road #07-02

AZ @ Paya Lebar, Singapore 409015 | |

(Name, Telephone, E-mail and/or Facsimile number

and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b)

of the Act:

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Ordinary Shares, par value $0.00625 per share | | IOTR | | The Nasdaq Stock Market LLC |

Securities registered or to be registered pursuant to Section 12(g)

of the Act:

Securities for which there is a reporting obligation pursuant to Section

15(d) of the Act:

Indicate the number of outstanding shares of

each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: As of March

31, 2025, 24,000,000 Ordinary Shares, par value $0.00625 per share.

Indicate by check mark if the registrant is a well-known seasoned

issuer, as defined in Rule 405 of the Securities Act.

If this report is an annual or transition report,

indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act

of 1934.

Note – Checking the box above will not

relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations

under those Sections.

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12

months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days.

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant

is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large

accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated filer ☐ | Accelerated filer ☐ | Non-accelerated filer ☒ |

| | | Emerging Growth Company ☒ |

If an emerging growth

company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not

to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant

to Section 13(a) of the Exchange Act. ☐

| † |

The term “new or

revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting

Standards Codification after April 5, 2012. |

Indicate by check mark

whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal

control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting

firm that prepared or issued its audit report. ☐

If securities are registered

pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing

reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark

whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by

any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting

the registrant has used to prepare the financial statements included in this filing:

| US GAAP ☒ | International Financial Reporting Standards as issued | Other ☐ |

| | by the International Accounting Standards Board ☐ | |

If “Other” has been checked in response

to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

If this is an annual report, indicate by check

mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY

PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant

has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent

to the distribution of securities under a plan confirmed by a court.

Annual Report on Form 20-F

Year Ended March 31, 2025

TABLE OF CONTENTS

CERTAIN INFORMATION

As used in this Annual Report on Form 20-F (the

“Annual Report”), unless otherwise indicated or the context otherwise requires, references to:

“5G” means the

5th generation mobile network, which is a global wireless standard.

“ASC” means FASB

Accounting Standards Codification.

“AI” means artificial

intelligence.

“AR” means augmented

reality.

“British Virgin Islands”

means the United Kingdom and Northern Ireland’s territory of the Virgin Islands.

“BVI” means British

Virgin Islands.

“CAGR” means compound

annual growth rate.

“Cayman Islands”

means the Cayman Islands, a British overseas territory in the Western Caribbean islands.

“CCTV” means closed

circuit television.

“Companies Act”

means the Companies Act (as revised) of the Cayman Islands.

“COVID-19” means

the novel Coronavirus Disease of 2019.

“ERP” means enterprise

resource planning.

“EU” means the

European Union.

“Exchange Act”

means the United States Securities Exchange Act of 1934, as amended, or any similar federal statute, and the rules and regulations promulgated

by the SEC thereunder.

“FASB” means the

Financial Accounting Standards Board.

“GPS” means global

positioning system.

“IoT” means Internet

of Things.

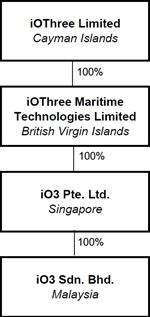

“iO3 BVI” means

iOThree Maritime Technologies Limited, a subsidiary of our Company incorporated under the laws of the British Virgin Islands on August

21, 2023.

“iO3 Cayman” means

iOThree Limited, an exempted company incorporated under the laws of the Cayman Islands on August 21, 2023 as a holding company.

“iO3 Singapore”

means iO3 Pte. Ltd. incorporated under the Singapore Companies Act as an exempt private company limited by shares on February 19, 2019.

“IRS” means the

U.S. Internal Revenue Service.

“IP phone” means

internet protocol phone.

“ISO” means International

Organization for Standardization.

“IT” means information

technology.

“JOBS Act” means

the Jumpstart Our Business Startups Act of 2012.

“LAN” means local

area network.

“Nasdaq” means

The Nasdaq Stock Market LLC.

“Nasdaq Listing Rules”

means the Listing Rules adopted by The Nasdaq Stock Market LLC, as the same may be amended from time to time.

“OT” means operational

technology.

“Sarbanes-Oxley Act”

means the Sarbanes-Oxley Act of 2002, as amended, and the rules and regulations promulgated from time to time thereunder.

“SEC” means the

U.S. Securities and Exchange Commission.

“Securities Act”

means the United States Securities Act of 1933, as amended, or any similar federal statute and the rules and regulations promulgated

by the SEC thereunder.

“Singapore Dollars”

or “S$” means Singapore dollars.

“Singapore Companies

Act” means the Companies Act 1967 of Singapore, as amended, supplemented or modified from time to time.

“Singapore Stock Exchange”

means the Singapore Exchange Securities Trading Limited.

“United States”

or “U.S.” means the United States of America, including the states, the District of Columbia and its territories and

possessions.

“U.S. Dollars”,

“US$” or “$” means U.S. dollars.

“U.S. Foreign Corrupt

Practices Act” means the United States Foreign Corrupt Practices Act 1977, as amended.

“USB” means universal

serial bus.

“VSAT” means very

small aperture terminal.

Financial Statements

The consolidated financial

statements included in this Annual Report have been prepared in accordance with accounting principles generally accepted in the United

States of America (“U.S. GAAP”) and pursuant to the regulations of the SEC.

Financial Information in U.S. Dollars

The reporting currency of

the Company is United States Dollars, or “US$”, or “$”, and the consolidated financial statements included in

this Annual Report have been expressed in United States Dollars. In addition, the Company and subsidiaries maintain their books and record

in United States Dollars or “US$”, or “$”, which is a functional currency as being the primary currency of the

economic environment in which their operations are conducted.

Transactions denominated in

currencies other than United States Dollars are translated into United States Dollars at the exchange rates prevailing at the dates of

the transaction. Monetary assets and liabilities denominated in currencies other than the functional currency are translated into the

functional currency using the applicable exchange rates at the date of the balance sheet dates. The resulting exchange differences arising

on the settlement of monetary items or on translating monetary items at the date of the balance sheet dates are recorded in the statement

of operations.

FORWARD-LOOKING STATEMENTS

This Annual Report contains

many statements that are “forward-looking” and uses forward-looking terminology such as “anticipate,” “believe,”

“could,” “estimate,” “expect,” “future,” “intend,” “may,” “ought

to,” “plan,” “possible,” “potentially,” “predicts,” “project,” “should,”

“will,” “would,” negatives of such terms or other similar statements. You should not place undue reliance on

any forward-looking statement due to its inherent risk and uncertainties, both general and specific. Although we believe the assumptions

on which the forward-looking statements are based are reasonable and within the bounds of our knowledge of our business and operations

as of the date of this Annual Report, any or all of those assumptions could prove to be inaccurate. Many important factors, including

those discussed under “Item 3.D. Risk Factors,” could cause our actual results to differ substantially from those

anticipated in our forward-looking statements, including:

| ● | unfavorable global and regional economic, political and health

conditions, especially in Singapore and Asia; |

| ● | environmental, social and governance matters, including global

climate change; |

| ● | current competition and the emergence of new market participants

in our industry; |

| ● | government regulation and changes in foreign currency exchange

rates; |

| ● | our expectations regarding the continued growth of our industry

in Asia and globally; |

| ● | failure to maintain and enhance our brand recognition; |

| ● | our ability to maintain and expand our supplier relationships; |

| ● | our reliance on technology; |

| ● | being subject to warranty claims, product recalls and product

liability claims; |

| ● | our ability to attract, train and retain executives and other

qualified employees; and |

| ● | our ability to successfully implement our growth strategies. |

Such risks and uncertainties are not exhaustive.

Other sections of this Annual Report include additional factors which could adversely impact our business and financial performance.

These statements reflect our current views with respect to future events and are not a guarantee of future performance. Actual results

of our operations may differ materially from information contained in the forward-looking statements. The forward-looking statements

contained in this Annual Report speak only as of the date of this Annual Report or, if obtained from third-party studies or reports,

the date of the corresponding study or report, and are expressly qualified in their entirety by the cautionary statements in this Annual

Report. Since we operate in an emerging and evolving environment and new risk factors and uncertainties emerge from time to time, you

should not rely upon forward-looking statements as predictions of future events. Except as otherwise required by the securities laws

of the United States, we undertake no obligation to update or revise any forward-looking statements to reflect events or circumstances

after the date of this Annual Report or to reflect the occurrence of unanticipated events.

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

3.A. [Reserved]

3.B. Capitalization and Indebtedness

Not applicable.

3.C. Reasons for the Offer and Use of Proceeds

Not applicable.

3.D. Risk Factors

You should carefully consider the following

risk factors and all of the information contained in this Annual Report, including but not limited to, the matters addressed in the section

titled “Forward-Looking Statements,” and our financial information before you decide whether to invest in our securities.

One or more of a combination of these risks could materially impact our business, financial condition or results of operations. In any

such case, the market price of the Ordinary Shares could decline, and you may lose all or part of your investment. Additional risks and

uncertainties not currently known to us or that we currently do not consider to be material may also materially and adversely affect

our business, financial condition or results of operations.

Summary Risk Factors

Risks Related to Our Business and Industry

| ● | We are an early-stage company with a limited operating history.

Our relatively short track record makes it difficult to evaluate our historical performance or predict our future prospects. |

| ● | Loss of key employees and the inability to continuously recruit

and retain qualified employees could hurt our competitive position. |

| ● | The emergence of a competing maritime digital shipboard platform

or other similar product and service could reduce the competitive advantage we believe we currently enjoy with JARVISS, which offers

an open, participative infrastructure for a diversified portfolio of applications to be transmitted efficiently, with built-in cybersecurity

protection. |

| ● | Satellite failures or degradations in satellite performance

could affect our business, financial condition and results of operations. |

| ● | We generate a significant percentage of our revenue from certain

key customers, and anticipate this concentration will continue for the foreseeable future, and the loss of one or more of our key customers

could negatively affect our business and operating results. |

| ● | As we rely on a small number of suppliers, supplier concentration

may expose us to significant financial credit or performance risk. |

| ● | Defects, errors or other performance problems in our software

or hardware, or the third-party software or hardware on which we rely, could harm our reputation, result in significant costs to us,

impair our ability to sell our systems and subject us to substantial liability. |

| ● | We are devoting significant resources to research and development

efforts that may be unsuccessful. If we are unable to improve our existing products and services and develop new, innovative products

and services, our sales and market share may decline. |

| ● | Our reliance on distributors could affect our ability to efficiently

and profitably distribute and market our products, maintain our existing markets and expand our business into other geographic markets. |

Risks Related to Legal, Regulatory and

Governmental Matters

| ● | Most of the registrant’s operations are carried out in

Singapore. As a result, our operations are subject to various political, economic, and other risks and uncertainties. |

| ● | It will be difficult to obtain jurisdiction and enforce liabilities

against our officers, directors and assets outside the United States. |

| ● | We may become subject to warranty claims, product recalls and

product liability claims and may be adversely affected by unfavorable court decisions or legal settlements. |

Risks Related to Intellectual Property,

Information Technology, Data Privacy and Cybersecurity

| ● | A material failure, inadequacy, interruption or security failure

of our technology networks and related systems could harm our business. |

| ● | We depend on cloud-based data services operated by third parties,

and any disruption in the operation of these services could harm our business. |

| ● | Cybersecurity breaches, attacks and other similar incidents,

as well as other disruptions, could compromise our confidential and proprietary information, including personal information, and expose

us to liability and regulatory fines, increase our expenses, or result in legal or regulatory proceedings, which would cause our business

and reputation to suffer. |

| ● | We are subject to complex and evolving laws, regulations, rules,

standards and contractual obligations regarding data privacy and cybersecurity, which can increase the cost of doing business, compliance

risks and potential liability. |

| ● | We use open-source software in our systems, which could negatively

affect our ability to offer our systems and subject us to litigation and other actions. |

Risks Related to Ownership of Our Securities

| ● | We are a foreign private issuer and, as a result, are not subject

to U.S. proxy rules but are subject to Exchange Act reporting obligations that, to some extent, are more lenient and less frequent

than those of a U.S. issuer. |

| ● | We may lose our foreign private issuer status in the future,

which could result in significant additional costs and expenses. |

| ● | In addition to being a foreign private issuer, we are a “controlled

company” within the meaning of the Nasdaq Listing Rules and, as a result, are eligible for exemptions from certain corporate governance

requirements. |

| ● | As a company incorporated in the Cayman Islands, we are permitted

to adopt certain home country practices in relation to corporate governance matters that differ significantly from Nasdaq corporate governance

listing standards. These practices may afford less protection to shareholders than they would enjoy if we complied fully with Nasdaq

corporate governance listing standards. |

| ● | You may face difficulties in protecting your interests, and

your ability to protect your rights through U.S. courts may be limited, because we are incorporated under Cayman Islands law. |

| ● | Our Amended and Restated Memorandum and Articles of Association

designate the Cayman Islands as the exclusive forum for certain litigation that may be initiated by our shareholders and the United States

District Court for the Southern District of New York as the exclusive forum for litigation arising under the federal securities laws

of the United States, which could limit our shareholders’ ability to obtain a favorable judicial forum for disputes with us. |

| ● | Because we do not expect to pay dividends in the foreseeable

future, you must rely on price appreciation of our Ordinary Shares for a return on your investment. |

| ● | Our Ordinary Shares will be subject to potential delisting if

we do not meet or continue to maintain the listing requirements of Nasdaq. |

| ● | Our share price has fallen significantly and we could be delisted

in which case broker-dealers may be discouraged from effecting transactions in our Ordinary Shares because they may be considered penny

stocks and thus be subject to the penny stock rules. |

| ● | Our officers, directors and principal shareholders currently

own a substantial number of our Ordinary Shares and have the power to significantly influence the vote on all matters submitted to a

vote of our shareholders. |

| ● | For as long as we are an emerging growth company, we will not

be required to comply with certain requirements that apply to other public companies. |

Risks Related to Our Business and Industry

We are an early-stage

company with a limited operating history. Our relatively short track record makes it difficult to evaluate our historical performance

or predict our future prospects.

Since inception in 2019, we

have devoted substantially all of our resources to designing, developing and manufacturing our systems and technology, enhancing our

engineering capabilities, building our business and establishing relations with our customers, raising capital and providing general

and administrative support for these operations. We are still in the early stages of our development and have a limited operating history.

Consequently, any assessment you make about our current business or future success or viability may not be as accurate as it could be

if we had a longer operating history or an established track record in generating predictable revenues or operating cash flows sufficient

to fund our working capital requirements.

Although we have several customer

contracts, we have limited insight into trends that may emerge and affect our business, including our ability to attract and retain customers,

the amount of revenue we will generate from our customers and the competition we will face. If our revenue grows slower than we anticipate

or we otherwise fall materially short of our forecasts and expectations, we may not be able to maintain sustained profitability and our

financial condition will be materially and adversely affected which could cause our share price to decline and investors to lose confidence

in us.

Additionally, our relatively

short track record makes it difficult to evaluate our historical performance or predict our future prospects. Investors should consider

our business and prospects in light of the risks, expenses, and challenges frequently encountered by companies in the early stages of

development. Any failure to address these challenges effectively could have a material adverse effect on our business, financial condition,

and results of operations.

Loss of key employees

and the inability to continuously recruit and retain qualified employees could hurt our competitive position.

We depend on a limited number

of key technical, marketing and management personnel to manage and operate our business. In particular, we believe our success depends

to a significant degree on our ability to attract and retain highly skilled engineers to facilitate the enhancement of our existing technologies

and the development of new systems. In order to compete effectively, we must:

| ● | hire and retain qualified professionals; |

| ● | continue to develop leaders for key business units and functions;

and |

| ● | train and motivate our employee base. |

The competition for qualified

personnel is intense, and the number of candidates with relevant experience, particularly in radio-frequency device and satellite communications

systems development and engineering, integrated circuit and technical pre- and post-sale support, is limited. Changes in employment-related

laws and regulations may also result in increased operating costs and less flexibility in how we meet our changing workforce needs. Additionally,

we may in the future decide to dismiss, certain personnel in order to save on costs and focus on our core competencies, which may have

an adverse effect on our reputation and our ability to retain additional qualified personnel in the future. We cannot assure that we

will be able to attract and retain skilled personnel in the future, which could harm our business and our results of operations.

The markets in which

we compete are relatively competitive and our competitors may have greater resources than us.

Although we have not encountered

any direct competitors as there is no one company that operates and provides both business segments, the markets in which we compete

are still relatively competitive and competition is increasing. In addition, because the markets in which we operate are constantly evolving

and characterized by rapid technological change, it is difficult for us to predict whether, when and by whom new competing technologies,

products or services may be introduced into our markets. Currently, we face competition in each of our segments. See “Item 4.B.

Business Overview — Competition” of this report for a discussion of the competitive environment in each of

our segments. Many of our competitors have significant competitive advantages, including strong customer relationships, more experience

with regulatory compliance, greater financial and management resources and access to technologies not available to us. Many of our competitors

are also substantially larger or more specialized than we are and may have more extensive engineering, manufacturing and marketing capabilities

than we do. As a result, these competitors may be able to adapt more quickly to changing technology or market conditions or may be able

to devote greater resources to the development, promotion and sale of their products. Our ability to compete in each of our segments

may also be adversely affected by limits on our capital resources and our ability to invest in maintaining and expanding our market share.

Our competitors may

develop products that are less expensive, are safer or more effective, and thus may diminish or eliminate the commercial success of any

potential products that we may commercialize.

Our competitors may develop

products that are less expensive, are safer or more effective, and thus may diminish or eliminate the commercial success of any potential

products that we may commercialize. If there are competitors’ market products that are less expensive, safer or more effective

than our future products developed from our product candidates, or that reach the market before our product candidates, we may not achieve

commercial success. The market may choose to continue utilizing the existing products for any number of reasons, including familiarity

with or pricing of these existing products. The failure of any of our product candidates to compete with products marketed by our competitors

would impair our ability to generate revenue, which would have a material adverse effect on our future business, financial condition

and results of operations. We expect to compete with several companies and our competitors may:

| ● | Develop and market products that are less expensive or more

effective than our future products; |

| ● | Commercialize competing products before we can launch any products

developed from our product candidates; |

| ● | Operate larger or more specialized research and development

programs or have substantially greater financial resources than we do; |

| ● | Initiate or withstand substantial price competition more successfully

than we can; |

| ● | Have greater success in recruiting skilled technical and scientific

workers from the limited pool of available talent; |

| ● | More effectively negotiate third-party licenses and strategic

relationships; and |

| ● | Take advantage of acquisition or other opportunities more readily

than we can. |

The emergence of a competing

maritime digital shipboard platform or other similar products and services could reduce the competitive advantage we believe we currently

enjoy with JARVISS, which offers an open, participative infrastructure for a diversified portfolio of applications to be transmitted

efficiently, with built-in cybersecurity protection.

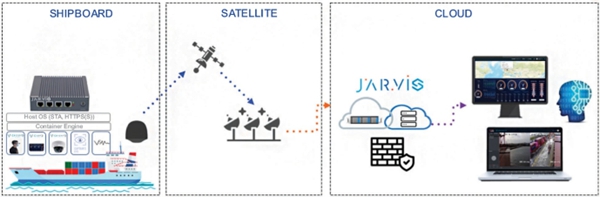

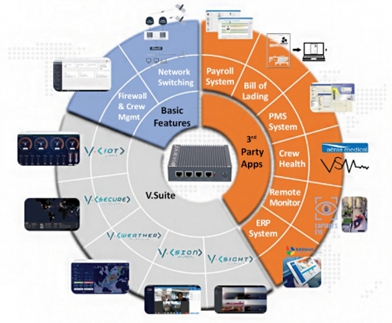

JARVISS is a unified digital

shipboard platform that encompasses the full spectrum end-to-end from shipboard edge device to cloud services for operational efficiencies

and safer voyages. JARVISS provides a diversified portfolio of digital solutions and is fully customizable and designed to meet our customers’

individual requirements. We believe that our array of competitive advantages positions us to not only maintain but also strengthen our

position in the industry. Due to our unique business offering, we have not encountered and are unaware of any direct competitors as there

is no one company that operates and provides both business segments (i.e., connectivity and digitalization and other solutions), but

any introduction of such a product or company could adversely impact our success. In addition, other companies could replicate some of

the distinguishing features of our products, which could potentially reduce the appeal of our solution, increase price competition, and

adversely affect sales. We do, however, face different competitors in each of the business segments. Our main competitors are Navarino,

Marlink and Inmarsat for satellite connectivity solution; and Alpha Ori, Zero North and Storm Geo for the ‘digitalization’

segment under ‘digitalization and other solutions’, and Navarino, Radio Holland, and DNV for the ‘other solutions’

segment under ‘digitalization and other solutions’. Moreover, our current and future competitors vary in size and in the

breadth and scope of the products and services they offer. They may have longer operating histories or have greater available financial,

technical, sales, marketing and other resources than we do. Future competitors such as venture backed startups that are purely software

focused may be able to benefit from more capital being injected into the research and development of their products as well as business

development efforts.

Any failure to maintain our brand recognition and

value may adversely affect our business.

We believe our strong market

positions have contributed to the Company’s strong brand recognition and value. Maintaining and developing our brand recognition

and value will depend largely on the success of our marketing efforts and our ability to provide consistent, high-quality customer service.

In addition, brand recognition and value are based in large part on perceptions of subjective qualities, and even isolated incidents

can erode trust and confidence, particularly if they result in adverse publicity, governmental investigations or litigation. Our Company,

including our brand recognition and value, could be adversely affected if our public image or reputation is tarnished by negative publicity.

Any loss of confidence on the part of customers in our brand or brand image would be difficult and costly to overcome and could have

a material adverse effect on our business, financial condition and results of operations.

Satellite failures or

degradations in satellite performance could affect our business, financial condition and results of operations.

Our solutions utilize satellites

to provide our customers with stable communications and other technological capabilities. Satellites utilize highly complex technology,

operate in the harsh environment of space and are subject to significant operational risks while in orbit. These risks include malfunctions

(commonly referred to as anomalies), such as malfunctions in the deployment of subsystems and/or components, interference from electrostatic

storms, and collisions with meteoroids, decommissioned spacecraft or other space debris. Anomalies can occur as a result of various factors,

including satellite manufacturer error, problems with the power or control sub-system of a satellite or general failures caused by the

harsh space environment. Our satellite providers may experience anomalies in the future. Any single anomaly or other operational failure

or degradation on the satellites we use could have a material adverse effect on our business, financial condition and results of operations.

Although the satellite operators we use have redundant or backup systems and components that operate in the event of an anomaly, operational

failure or degradation of primary critical components, these redundant or backup systems and components are subject to risk of failure

similar to those experienced by the primary systems and components. The occurrence of a failure of any of these redundant or backup systems

and components could materially affect our business, financial condition and results of operations.

We generate a significant

percentage of our revenue from certain key customers, and anticipate this concentration will continue for the foreseeable future, and

the loss of one or more of our key customers could negatively affect our business and operating results.

We derive a significant portion

of our revenue from a limited number of customers. For the years ended March 31, 2025, 2024 and 2023, our top five customers contributed

approximately 44.0%, 34.1% and 39.7% of the total revenue of our company, respectively. If we fail to deliver upon contracts with these

five customers, or upon the contracts of other large customers, or if demand by these customers for our products decreases substantially,

our revenues and operating results could be materially adversely affected. Any slowdown or a disruption in the growth of these customers’

markets could adversely affect our financial condition and results of operations.

As we rely on a small

number of suppliers, supplier concentration may expose us to significant financial credit or performance risk.

Our solutions rely on the

supply of services, equipment, or software which we may purchase from a small number of third-party suppliers. Purchases from our five

largest suppliers contributed approximately 50.1%, 49.8% and 60.7% of our total cost of sales for the years ended March 31, 2025, 2024

and 2023, respectively. As we continue to grow our business, we may need to establish a more diverse supplier network, while attempting

to continue to leverage our purchasing power to obtain favorable pricing and delivery terms. The failure to diversify our supplier network

could have an adverse effect on our results of operations, financial condition and cash flows.

Furthermore, despite our efforts

to maintain good relationships with our existing suppliers, we could lose one or more of our existing suppliers at any time. The loss

of one or more key suppliers could increase our reliance on higher cost or lower quality supplies, which could negatively affect our

profitability. Any interruptions to, or decline in, the amount or quality of our supplies could materially disrupt our operations and

adversely affect our business, financial condition and financial prospects.

Deterioration of the

financial condition of our customers could adversely affect our operating results.

Deterioration of the financial

condition of our customers could adversely impact our collection of accounts receivable and may result in delays in product orders or

contract negotiations. For the years ended March 31, 2025, 2024 and 2023, our top five customers contributed approximately 44.0%,

34.1% and 39.7% of the total revenue of our company, respectively. As of March 31, 2025, 2024 and 2023, accounts receivable with

these customers were approximately $269,844, $118,000 and $422,000, respectively. We regularly review the collectability and creditworthiness

of our customers to determine an appropriate allowance for credit losses. Based on our review of our customers, we currently have no

reserves for uncollectible accounts. If our accounts receivable become uncollectible, our operating results would be negatively impacted.

Further, recent global inflationary trends and financial markets volatility have resulted in funding constraints that may affect the

timing and scale of investments in new communications technologies by some of our existing and prospective customers. The effects of

recent macroeconomic uncertainties on our customers have also resulted in delays to contract negotiations or customer orders, and may

result in further delays. Any new or further delays in new contracts or customer orders could materially adversely affect our financial

condition and operating results.

Some of our customers

may require our products and systems to undergo a demonstration process that does not assure future sales or customer contracts.

Prior to purchasing our satellite

communications systems, some of our customers may require that products undergo extensive demonstration processes, which may involve

the testing of our products in the customers’ systems or via a prototype demonstration. We may also undertake to commit resources

to prepare a demonstration for a prospective customer, in which case we would bear the expenses of the demonstration. The demonstration

process varies by the customer and the product, and may take several months. The demonstration of our products to a customer does

not assure any sales of such product to that customer. Despite these uncertainties, we may devote substantial resources, including design,

engineering, sales, marketing and management efforts, to demonstrate our products to customers in anticipation of sales and without an

expectation of reimbursement of these costs or generating future revenues and gross profits from the projected sale of our systems.

Our estimates, including

market opportunity estimates and market growth forecasts, are subject to inherent challenges in measurement and significant uncertainty,

and real or perceived inaccuracies in those metrics and estimates may harm our reputation and negatively affect our business.

We track certain key metrics

and market data, including, among others, our estimated demand for maritime digital technology, which may differ from estimates or similar

metrics published by third parties due to differences in sources, methodologies or the assumptions on which we rely. Our methodologies

for tracking these data may change over time, which could result in changes to our metrics, including the metrics we publicly disclose.

While our key metrics and market data are based on what we believe to be reasonable estimates for the applicable period of measurement,

there are inherent challenges in measuring our performance. For example, the accuracy of our projected potential contract revenue pipeline

could be impacted by developments outside of our control, such as changes in customers’ plans, supply chain difficulties and the

availability of alternative products. In addition, limitations with respect to how we measure data or with respect to the data that we

measure may affect our understanding of certain details of our business, which could affect our long-term strategies. If our estimates

of operating metrics and market data are not accurate representations of our business, if investors do not perceive our operating metrics

to be accurate, or if we discover material inaccuracies with respect to these figures, our business, financial condition, results of

operations and prospects could be materially and adversely affected. Additionally, industry data, forecasts, estimates and projections

included elsewhere in this report are subject to inherent uncertainty as they necessarily require certain assumptions and judgments.

Certain facts, forecasts and other statistics relating to the industries in which we compete have been derived from various public data

sources, including third-party industry reports and analyses. Accordingly, our use of the terms referring to our markets and industries

may be subject to interpretation, and the resulting industry data, projections and estimates are inherently uncertain. If any one or

more of the assumptions underlying the market data are later found to be incorrect, actual results may differ from the projections based

on these assumptions. Furthermore, our industry data and market share data should be interpreted in light of the defined markets in which

we operate. Any discrepancy in the interpretation thereof could lead to varying industry data, measurements, forecasts and estimates.

Further, the sources on which such industry and market data and estimates are based were prepared as of a certain point in time, and

any changes in global macroeconomic conditions, including recent global inflationary trends and financial markets volatility, could also

lead to changes in these data, measurements, forecasts and estimates. Furthermore, we do not, as a matter of general practice, publicly

disclose long-term forecasts or internal projections of our future performance, revenue, financial condition or other results.

Fluctuations in our

net sales and results of operations could depress the market price of our Ordinary Shares.

Our future net sales and results

of operations could vary significantly due to a number of factors, many of which are outside our control. Accordingly, you should not

rely on year-to-year comparisons of our results of operations as an indication of future performance. It is possible that our net sales

or results of operations in a quarter will fall below the expectations of securities analysts or investors. If this occurs, the market

price of our Ordinary Shares could fall significantly. Our results of operations in any financial year can fluctuate for many reasons,

including changes in demand for our products and services; delays in order fulfillment; the mix of products and services we sell; our

ability to test and deliver products in a timely and cost-effective manner, including the availability of components from our suppliers;

our success in winning competitions for orders; the timing of new product introductions by us or our competitors; the scope and success

of our investments in research and development; expenses incurred in pursuing acquisitions and investments; expenses incurred in expanding,

maintaining, or improving our global network; market and competitive pricing pressures; unanticipated charges or expenses, such as increases

in warranty claims; expenses incurred in responding to shareholder activism; general economic climate; and the impact of supply chain

disruptions. A large portion of our expenses, including expenses for network infrastructure, facilities, equipment, and personnel, are

relatively fixed. Accordingly, if our net sales decline or do not grow as much or as quickly as we anticipate, we might be unable to

maintain or improve our operating margins. Any failure to achieve anticipated net sales could therefore significantly harm our operating

results for a particular fiscal period.

Defects, errors or other

performance problems in our software or hardware, or the third-party software or hardware on which we rely, could harm our reputation,

result in significant costs to us, impair our ability to sell our systems and subject us to substantial liability.

Our software and hardware,

and those of third parties on which we rely, is complex and may contain defects or errors when implemented or when new functionality

is released, as we may modify, enhance, upgrade and implement new systems, procedures and controls to reflect changes in our business,

technological advancements and changing industry trends. Despite our testing, from time to time we have discovered and may in the future

discover defects or errors in our software and hardware. Any performance problems or defects in our software or hardware, or those of

third parties on which we rely, could materially and adversely affect our business, financial condition and results of operations. Defects,

errors or other similar performance problems or disruptions, whether in connection with day-to-day operations or otherwise, could

be costly for us, damage our customers’ businesses, harm our reputation and result in reduced sales or a loss of, or delay in,

the market acceptance of our systems. In addition, if we have any such errors, defects or other performance problems, our clients could

seek to terminate their contracts, delay or withhold payment or make claims against us. Any of these actions could result in liability,

lost business, increased insurance costs, difficulty in collecting accounts receivable, costly litigation or adverse publicity, which

could materially and adversely affect our business, financial condition and results of operations.

Acquisitions and strategic

relationships may disrupt our operations or adversely affect our results.

We evaluate opportunities

to acquire other businesses and pursue other strategic relationships as they arise. The expenses we incur evaluating and pursuing acquisitions

and strategic relationships could have a material adverse effect on our results of operations. If we acquire a business, we may be unable

to manage it profitably or successfully integrate its operations with our own. Moreover, we may be unable to realize the strategic, financial,

operational and other benefits we anticipate, and any acquisition or strategic relationship may increase our operating expenses. Further,

our approach to acquisitions and strategic relationships may involve a number of special financial and business risks, such as entry

into new and unfamiliar lines of business or markets, which may present challenges or risks that we did not anticipate; entry into new

or unfamiliar geographic regions, including exposure to additional tax and regulatory regimes; increased expenses associated with the

amortization of acquired intangible assets; increased exposure to fluctuations in foreign currency exchange rates; charges related to

any abandoned acquisition; diversion of our management’s time, attention, and resources; loss of key personnel; increased costs

to improve or coordinate managerial, operational, financial, and administrative systems, including internal control over financial reporting;

dilutive issuances of equity securities; the assumption of legal liabilities; and losses arising from impairment charges associated with

goodwill or intangible assets.

We depend on our main

facility in Singapore and are susceptible to any event that could adversely affect its condition or the condition of our other facilities.

We depend on our main facility

in Singapore and are susceptible to any event that could adversely affect its condition or the condition of our other facilities. A material

portion of our operational capacity, our principal offices and principal research and development facilities for the principal part of

our business are concentrated in a single location in Singapore. We also have business arrangements with a few local agents in Taiwan

and Vietnam. Fire, natural disaster, lockdowns, or any other cause of material disruption in our operations in any of these locations

could have a material adverse effect on our business, financial condition and operating results.

We may not be able to

raise equity and debt financing sufficient to meet our capital and operating needs and to comply with the covenants that we expect will

be contained in our debt agreements, which could have a material adverse effect on our business, financial condition, results of operations

and cash flows.

We may not be able to raise

equity and debt financing sufficient to meet our capital and operating needs and to comply with the covenants that we expect will be

contained in our debt agreements, which could have a material adverse effect on our business, financial condition, results of operations

and cash flows. We cannot assure you that the net proceeds from any future equity offering or debt financing would be sufficient to satisfy

our capital and operating needs and enable us to comply with various debt covenants that we expect will be contained in future debt agreements.

In such case, we may not be able to raise additional equity capital or obtain additional debt financing or refinance our existing indebtedness,

if necessary. If we are not able to comply with the covenants that we expect will be contained in future debt agreements and our lenders

choose to accelerate our indebtedness and foreclose their liens, we could be required to sell any vessels we may own and our ability

to continue to conduct our business would be impaired.

We are devoting significant

resources to research and development efforts that may be unsuccessful. If we are unable to improve our existing products and services

and develop new, innovative products and services, our sales and market share may decline.

The market for maritime connectivity

and digital solutions is characterized by rapid technological change, frequent new product innovations, changes in customer requirements

and expectations, and evolving industry standards. For example, we are starting to face competition from other maritime communication

companies. For instance, our main competitors are Navarino, Marlink and Inmarsat for satellite connectivity solution; and Alpha Ori,

Zero North and Storm Geo for the ‘digitalization’ segment under ‘digitalization and other solutions’, and Navarino,

Radio Holland, and DNV for the ‘other solutions’ segment under ‘digitalization and other solutions’. If we fail

to make innovations in our existing products and services and reduce the costs of our products and services in a timely way, our market

share may decline. Products or services using new technologies, or emerging industry standards, could render our products and services

obsolete. If our competitors successfully introduce new or enhanced products or services that outperform our products or services, or

are perceived as doing so, we may be unable to compete successfully in the markets affected by these changes. Research and development

in our industry is inherently complex and uncertain, and our current and anticipated research and development projects may not achieve

the results we seek. The financial resources that we can devote to our research and development efforts may be insufficient to achieve

our goals. Our efforts may not result in any viable products or may result in products whose performance, features, price or availability

may not be attractive to customers or that we cannot manufacture and sell profitably.

Our reliance on distributors

could affect our ability to efficiently and profitably distribute and market our products, maintain our existing markets

and expand our business into other geographic markets.

Our ability to maintain and

expand our existing markets for our products, and to establish markets in new geographic distribution areas, is dependent on our ability

to establish and maintain successful relationships with reliable distributors strategically positioned to serve those areas. Such distributors

may sell and distribute competing products, and our products may represent a small portion of their businesses. There is a risk that

such distributors may not adequately perform their functions by, without limitation, failing to distribute to sufficient retailers or

positioning our products in localities that may not be receptive to our product. Our ability to incentivize and motivate distributors

to manage and sell our products is affected by competition from other companies who have greater resources than we do. To the extent

that our distributors are distracted from selling our products or do not employ sufficient efforts in managing and selling our products,

our sales and results of operations could be adversely affected. Furthermore, such third-parties’ financial position or market

share may deteriorate, which could adversely affect our distribution, marketing, and sales activities.

Our ability to maintain and

expand our distribution network and attract additional distributors will depend on a number of factors, some of which are outside our

control. Some of these factors include:

| ● | the level of demand for our brands and products in a particular

distribution area; |

| ● | our ability to price our products at levels competitive with

those of competing products; and |

| ● | our ability to deliver products in the quantity and at the time

ordered by distributors. |

We may not be able to successfully

manage all or any of these factors in any of our current or prospective geographic areas of distribution. Our inability to achieve success

with regards to any of these factors in a geographic distribution area will have a material adverse effect on our relationships in that

particular geographic area, thus limiting our ability to maintain or expand our market, which will likely adversely affect our revenues

and financial results.

Since we cannot exert

the same level of influence or control over our independent distributors as we could were they our own employees, our distributors could

fail to comply with our distributor policies and procedures, which could result in claims against us that could harm our financial condition

and operating results.

Our distributors are independent

and, accordingly, we are not in a position to directly provide the same direction, motivation and oversight as we would if distributors

were our own employees. As a result, there can be no assurance that our distributors will participate in our marketing strategies or

plans, accept our introduction of new products, or comply with our distributor policies and procedures.

Extensive national and local

laws regulate our business and products. Although we have implemented distributor policies and procedures designed to govern distributor

conduct and to protect the goodwill associated with our trademarks and tradenames, it can be difficult to enforce these policies and

procedures because of the large number of distributors and their independent status. Violations by our independent licensed distributors

of applicable law or of our policies and procedures in dealing with customers could reflect negatively on our products and operations

and harm our business reputation.

Risks Related to Legal, Regulatory and

Governmental Matters

Unfavorable global and

regional economic, political and health conditions could adversely affect our business, financial condition or results of operations.

Our results of operations

could be adversely affected by global or regional economic, political and health conditions. A global financial crisis or global or regional

political and economic instability (including changes in inflation, interest rates and overall economic conditions and uncertainties),

wars, terrorism, civil unrest, outbreaks of disease (for example, COVID-19), and other unexpected events, such as supply chain constraints

or disruptions, could cause extreme volatility, increase our costs and disrupt our business. Business disruptions could include, among

others, disruptions to our commercial activities, including due to supply chain or distribution constraints or challenges, as well as

temporary closures of our facilities and the facilities of suppliers or contract manufacturers in our supply chain. For example,

these macroeconomic factors could affect the ability of our current or potential future manufacturers, sole source or single source suppliers,

licensors or licensees to remain in business, or otherwise manufacture or supply components, materials or services relevant to our products.

Any failure by any of them to remain in business could affect our ability to manufacture products or meet demand for our products. In

addition, if inflation or other factors were to significantly increase our business costs, we may be unable to pass through price increases

to our customers. Interest rates and the ability to access credit markets could also adversely affect the ability of our customers to

purchase our products.

Also, ongoing geopolitical

instability, including the continuing conflict between Russia and Ukraine, the U.S. government’s escalation of trade tariffs in

a broader trade war, and renewed violence in the Middle East, poses significant risks to global economic conditions. The governments

of the United States, EU, Japan and other jurisdictions have imposed or expanded sanctions targeting certain sectors, entities and

individuals, as well as enhanced export controls affecting certain technologies and products. These actions, along with any retaliatory

measures by Russia, China, or other affected jurisdictions, could disrupt the global supply chains, reduce the availability of critical

raw materials and components, increase costs, and contribute to broader volatility in global financial markets, which may have a material

adverse effect on our business, financial condition, and results of operations.

Most of our operations

are carried out in Singapore. As a result, our operations are subject to various political, economic, and other risks and uncertainties

inherent to operating in that jurisdiction.

Most of our operations are

carried out in Singapore. As a result, our business is subject to various political, economic, legal, and regulatory risks inherent to

operating in that jurisdiction. While Singapore is generally considered to have a stable political environment and pro-business regulatory

framework, any changes in government policies, laws, or regulations—including those related to taxation, labor, trade, data privacy,

or foreign investment—could adversely impact our operations. Additionally, external factors such as regional geopolitical tensions,

shifts in global trade policies, inflationary pressures, or supply chain disruptions may also have indirect effects on the Singaporean

economy and, consequently, on our business, financial condition, and results of operations.

It will be difficult

to obtain jurisdiction and enforce liabilities against our officers, directors and assets outside the United States.

All of our assets are currently

located outside of the United States. Additionally, our directors and officers reside outside of the United States. Additionally,

our key management and operations are primarily based in Singapore. As a result, it may not be possible for United States investors

to enforce their legal rights, to effect service of process upon our directors or officers or to enforce judgments

of United States courts predicated upon civil liabilities and criminal penalties of our directors and officers under Federal securities

laws in Singapore or the Cayman Islands. Moreover, we have been advised that Singapore and Cayman Islands do not have a treaty

providing for the reciprocal recognition and enforcement of judgments of courts with the United States.

Risks associated with

environmental, social and governance matters, including global climate change, and legal, regulatory or market responses to these matters

could harm our reputation and business.

Increasing shareholder environmental,

social and governance (ESG) expectations, physical and transition risks associated with climate change, emerging ESG regulation, contractual

requirements and policy requirements present short, medium and long-term risks to our business and financial condition. Changes in environmental

and climate change laws or regulations could lead to additional operational restrictions and compliance requirements upon us. Compliance

with current and future environmental laws and regulations may require significant operating and capital costs. Our suppliers may face

similar business interruptions and incur additional costs that may be passed on to us. In addition, customers, shareholders and institutional

investors continue to increase their focus on ESG, including our environmental sustainability practices and commitments with respect

to our business and operations. If our responses to new or evolving legal and regulatory requirements or other sustainability concerns

are unsuccessful or perceived as inadequate for the U.S. or our international markets, we also may suffer damage to our reputation,

which could have a material adverse impact on our business, financial condition and results of operations.

We could incur additional

legal compliance costs associated with our international operations and could become subject to legal penalties if we do not comply with

certain regulations.

As a result of our international

operations, we are subject to a number of legal requirements, including the U.S. Foreign Corrupt Practices Act and the customs,

export, trade sanctions and anti-boycott laws of the United States, including those administered by the U.S. Customs and Border

Protection, the Bureau of Industry and Security, the Department of Commerce, the Department of State, and the Office of Foreign Assets

Control of the Treasury Department, as well as those of other nations in which we do business. In addition, many of the countries where

our customers use our products and services have licensing and regulatory requirements for the importation and use of satellite communications

and reception equipment, including the use of such equipment in territorial waters, the transmission of satellite signals on certain

radio frequencies, the transmission of voice over the internet services using such equipment, and, in some cases, the reception of certain

video programming services. These laws and regulations are continually changing, making compliance complex. We incur costs identifying

and maintaining compliance with applicable licensing and regulatory requirements. In addition, our training and compliance programs and

our other internal control policies may be insufficient to protect us from acts committed by our employees, agents or third-party contractors.

Any violation of these requirements by us or our employees, agents or third-party contractors may subject us to significant criminal

and civil liability.

Changes in foreign currency

exchange rates may negatively affect our financial condition and results of operations.

The reporting currency of

the Company is U.S. Dollars, to date the majority of the Company’s revenues and costs are denominated in US$ and S$, a majority

of the Company’s assets are denominated in US$ and S$ and a significant portion of the Company’s liabilities are denominated

in S$. As a result, the Company is exposed to foreign exchange risk as its revenues and results of operations may be affected by

fluctuations in the exchange rate between US$ and S$. For example, during 2022 and 2023, the U.S. dollar strengthened against

certain foreign currencies and this may cause a decrease in some of our monetary assets which are denominated in foreign currencies and

lead to the recognition of foreign exchange losses. Moreover, certain of our products and services are sold internationally in U.S. dollars;

if the U.S. dollar continues to strengthen, the relative cost of these products and services to customers located in foreign countries

would increase, which could adversely affect export sales. In addition, most of our financial obligations must be satisfied in U.S. dollars.

Our exposures to changes in foreign currency exchange rates may change over time as our business practices evolve and could result in

increased costs or reduced revenue and could adversely affect our cash flow. Changes in the relative values of currencies occur regularly

and may have a significant impact on our operating results. We cannot predict with any certainty changes in foreign currency exchange

rates or the degree to which we can cost-effectively mitigate this exposure.

Potential liability

claims relating to our products or services could have a material adverse effect on our business.

We may be subject to liability

claims relating to the products we sell or services we provide. Potential liability claims could include, among others, claims for debts

and for breaching service level availability obligations. We endeavor to include in our agreements with our business customers provisions

designed to limit our exposure to potential claims. However, we may fail to include limitations of our liability in our contracts, or

our contractual limitations of liability maybe rejected or limited in certain jurisdictions. Additionally, our insurance does not cover

all relevant claims, such as claims for force majeure, and does not provide sufficient coverage. To date, we have not been subject to

any material product liability claim. Our business, financial condition and operating results could be materially adversely affected

if costs resulting from future claims are not covered by our insurance or exceed our coverage.

We may become subject

to warranty claims, product recalls and product liability claims and may be adversely affected by unfavorable court decisions or legal

settlements.

From time to time, we may

be subject to warranty or product liability claims as a result of defects in our products and systems that could lead to significant

expense. If we or one of our suppliers recalls any of our products, we may incur significant costs and expenses, including replacement

costs, direct and indirect product recall-related costs, diversion of technical and other resources and reputational harm. Our customer

contracts typically contain warranty and indemnification provisions, and in certain cases may also contain liquidated damages provisions

related to product delivery obligations. The potential liabilities associated with such provisions are significant, and in some cases,

including in agreements with some of our largest customers, are potentially unlimited. Any such liabilities may greatly exceed any revenue

we receive from the sale of the relevant products. Costs, payments or damages incurred or paid by us in connection with warranty and

product liability claims and product recalls could materially and adversely affect our financial condition and results of operations.

Risks Related to Intellectual Property,

Information Technology, Data Privacy and Cybersecurity

A material failure,

inadequacy, interruption or security failure of our technology networks and related systems could harm our business.

A material failure, inadequacy,

interruption or security failure of our technology networks and related systems could harm our business. Our information technology networks

and related systems are essential to our ability to conduct our day-to-day operations. As a result, we face risks associated with

security breaches, whether through cyber-attacks or cyber intrusions over the internet, malware, computer viruses, attachments to emails,

persons who access our systems from inside or outside our organization and other significant disruptions of our information technology

networks and related systems. A security breach or other significant disruption involving our information technology networks and related

systems or those of our vendors could: disrupt our operations; result in the unauthorized access to, and the destruction, loss, theft,

misappropriation or release of, proprietary, personally identifiable, confidential, sensitive or otherwise valuable information including

tenant information and lease data, which others could use to compete against us or which could expose us to damage claims by third parties

for disruptive, destructive or otherwise harmful outcomes; require significant management attention and resources to remedy any damages

that result; subject us to claims for breach of contract, damages, credits, penalties or termination of leases or other agreements; or

damage our business relationships or reputation generally. Any or all of the foregoing could materially and adversely affect our business

and the value of our shares.

We depend on cloud-based

data services operated by third parties, and any disruption in the operation of these services could harm our business.

Some of our content services

and business records are hosted by various cloud-based data services operated by third parties. Any failure or downtime in one of these

services could affect a significant percentage of our customers. Although we control and have access to the components of our network

that are located in our internal facilities and certain of our external data facilities, we do not control the operation of external

facilities. The providers of our data management services have no obligation to renew their agreements with us on commercially reasonable

terms, or at all. If we are unable to renew these agreements on commercially reasonable terms, or if one or more of our data management

suppliers is acquired, closes, suffers financial difficulty or is unable to meet our growing capacity needs, we may be required to transfer

our data to other services, and we may incur significant costs and service interruptions in connection with doing so, which could harm

our reputation with our customers and adversely affect our revenues and results of operations.

Cybersecurity breaches,

attacks and other similar incidents, as well as other disruptions, could compromise our confidential and proprietary information, including

personal information, and expose us to liability and regulatory fines, increase our expenses, or result in legal or regulatory proceedings,

which would cause our business and reputation to suffer.

We rely on trade secrets,

technical know-how and other unpatented confidential and proprietary information relating to our product development and production activities

to provide us with competitive advantages. We also collect, maintain and otherwise process certain sensitive and other personal information

regarding our employees, as well as contact information of our customers and suppliers, in the ordinary course of business. One of the

ways we protect this information is by entering into confidentiality agreements with our employees, consultants, customers, suppliers,

strategic partners and other third parties with which we do business. We also design our computer networks and implement various procedures

to restrict unauthorized access to dissemination of our confidential and proprietary information. We, and our suppliers which may have

access to any such information, face various internal and external cybersecurity threats and risks. For example, current, departing or

former employees or other individuals or third parties with which we do business could attempt to improperly use or access our computer

systems and networks, or those of our suppliers, to copy, obtain or misappropriate our confidential or proprietary information, including

personal information, or otherwise interrupt our business. Additionally, like others, we and our suppliers are subject to significant

system or network or computer system disruptions from numerous causes, including cybersecurity breaches, attacks or other similar incidents,

facility access issues, new system implementations, human error, fraud, energy blackouts, theft, fire, power loss, telecommunications

failure or a similar catastrophic event. Moreover, computer viruses, worms, malware, ransomware, phishing, spoofing, malicious or destructive

code, social engineering, denial-of-service attacks, and other cyber-attacks have become more prevalent and sophisticated in recent years.

Attacks of this nature may be conducted by sophisticated and organized groups and individuals with a wide range of motives and expertise,

including organized criminal groups, “hacktivists,” terrorists, nation states, nation state-supported actors, and others.

We have been subject to attempted cyberattacks in the past, including attempted phishing attacks, and may continue to be subject to such

attacks in the future. While we defend against these threats and risks on a daily basis, we do not believe that any such incidents to

date have caused us any material damage. Because the techniques used by computer hackers and others to access or sabotage networks and

computer systems constantly evolve and generally are not recognized until launched against a target, we and our suppliers may be unable

to anticipate, detect, react to, counter or ameliorate all of these techniques or remediate any incident as a result therefrom. Further,

the COVID-19 pandemic has increased cybersecurity risk due to increased online and remote activity. As a result, our and our customers’

and employees’ confidential and proprietary information, including personal information, may be subject to unauthorized release,

accessing, gathering, monitoring, loss, destruction, modification, acquisition, transfer, use or other processing, and the impact of

any future incident cannot be predicted. While we generally perform cybersecurity diligence on our key suppliers, because we do not control

our suppliers and our ability to monitor their cybersecurity is limited, we cannot ensure the cybersecurity measures they take will be

sufficient to protect any information we share with them. Due to applicable laws and regulations or contractual obligations, we may be

held responsible for cybersecurity breaches, attacks or other similar incidents attributed to our suppliers as they relate to the information

we share with them. We routinely implement improvements to our network security safeguards and we are devoting increasing resources designed

to protect the security of our information technology systems. We cannot, however, assure that such safeguards or system improvements

will be sufficient to prevent or limit a cybersecurity breach, attack or other similar incident or network or computer system disruption,

or the damage resulting therefrom. We may be required to expend significant additional resources to continue to modify or enhance our

protective measures or to investigate or remediate any cybersecurity vulnerabilities, breaches, attacks or other similar incidents. Any

cybersecurity incident, attack or other similar incident, or our failure to make adequate or timely disclosures to the public, regulators,

or law enforcement agencies following any such event, could harm our competitive position, result in violations of applicable data privacy

or cybersecurity laws or regulations, result in a loss of customer confidence in the adequacy of our threat mitigation and detection

processes and procedures, cause us to incur significant costs to remedy the damages caused by the incident or defend legal claims, subject

us to additional regulatory scrutiny, expose us to civil litigation, fines, damages or injunctions, cause disruption to our business

activities, divert management attention and other resources or otherwise adversely affect our internal operations and reputation or degrade

our financial results. The costs related to cybersecurity breaches, attacks or other similar incidents or network or computer system