Prospectus

Blackstone Private Credit Fund

Class S, Class D and Class I Shares

Maximum Offering of $36,500,000,000

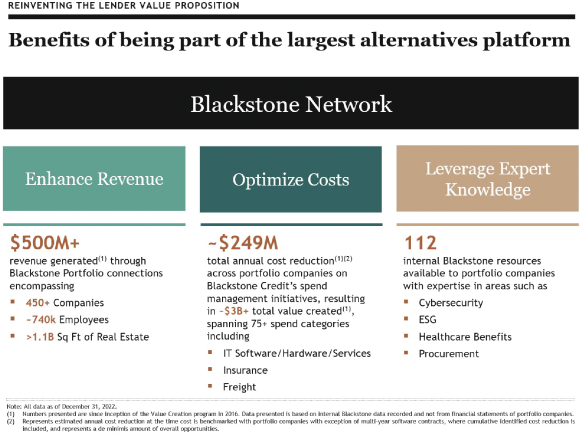

Blackstone Private Credit Fund is a Delaware statutory trust that seeks to invest primarily in originated loans and other securities, including broadly syndicated loans, of U.S. private companies and to a lesser extent European and other non-U.S. companies. We are externally managed by an affiliate of Blackstone Inc. (formerly, The Blackstone Group Inc.) (“Blackstone”), which is the largest alternative asset manager in the world with deep investment expertise and preeminent investment businesses across asset classes. Our investment objectives are to generate current income and, to a lesser extent, long-term capital appreciation. Throughout the prospectus, we refer to Blackstone Private Credit Fund as the “Fund,” the “Company,” “BCRED,” “we,” “us” or “our.”

We are a non-diversified, closed-end management investment company that has elected to be regulated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). Our adviser, Blackstone Credit BDC Advisors LLC (the “Adviser”) is an affiliate of Blackstone Alternative Credit Advisors LP, the credit-focused business of Blackstone (“Blackstone Credit”). We have elected to be treated for federal income tax purposes, and intend to qualify annually, as a regulated investment company (a “RIC”) under the Internal Revenue Code of 1986, as amended (the “Code”).

We are offering on a continuous basis up to $36,500,000,000 of our common shares of beneficial interest (“Common Shares”). We are offering to sell any combination of three classes of Common Shares—Class S shares, Class D shares and Class I shares—with a dollar value up to the maximum offering amount. The share classes have different ongoing shareholder servicing and/or distribution fees. The purchase price per share for each class of Common Shares equals our net asset value (“NAV”) per share, as of the effective date of the monthly share purchase date. This is a “best efforts” offering, which means that Blackstone Securities Partners L.P., the intermediary manager for this offering, will use its best efforts to sell shares, but is not obligated to purchase or sell any specific amount of shares in this offering.

Investing in our Common Shares involves a high degree of risk. See “Risk Factors” beginning on page 35 of this prospectus. Also consider the following:

| • | We have limited prior operating history and there is no assurance that we will achieve our investment objectives. |

| • | This is a “blind pool” offering and thus you will not have the opportunity to evaluate our investments before we make them. |

| • | You should not expect to be able to sell your shares regardless of how we perform. |

| • | You should consider that you may not have access to the money you invest for an extended period of time. |

| • | We do not intend to list our shares on any securities exchange, and we do not expect a secondary market in our shares to develop prior to any listing. |

| • | Because you may be unable to sell your shares, you will be unable to reduce your exposure in any market downturn. |

| • | We have implemented a share repurchase program, but only a limited number of shares will be eligible for repurchase and repurchases will be subject to available liquidity and other significant restrictions. |