Exhibit 99.1

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 OF

THE SECURITIES EXCHANGE ACT OF 1934

For the month of May 2014

Commission File No. 001-36085

CNH INDUSTRIAL N.V.

(Translation of Registrant’s Name Into English)

Cranes Farm Road

Basildon

Essex SS14 3AD

United Kingdom

Tel. No.: +44 1268 533000

(Address of Principal Executive Offices)

(Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.)

Form 20-F x Form 40-F ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ¨

Indicate by check mark whether the registrant by furnishing the information contained in this form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes ¨ No x

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): N/A.

CNH INDUSTRIAL N.V.

Form 6-K for the month of May 2014

The following exhibits are furnished herewith:

| Exhibit 99.1 | CNH Industrial N.V. Investor Day Presentations, May 8, 2014 | |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| CNH Industrial N.V. | ||

| By: | /s/ Roberto Russo | |

| Name: | Roberto Russo | |

| Title: | Corporate Secretary | |

May 9, 2014

Index of Exhibits

| Exhibit Number |

Description of Exhibit | |

| Exhibit 99.1 | CNH Industrial N.V. Investor Day Presentations, May 8, 2014 | |

| Exhibit 99.1

|

Exhibit 99.1

Opening remarks

Richard Tobin

|

|

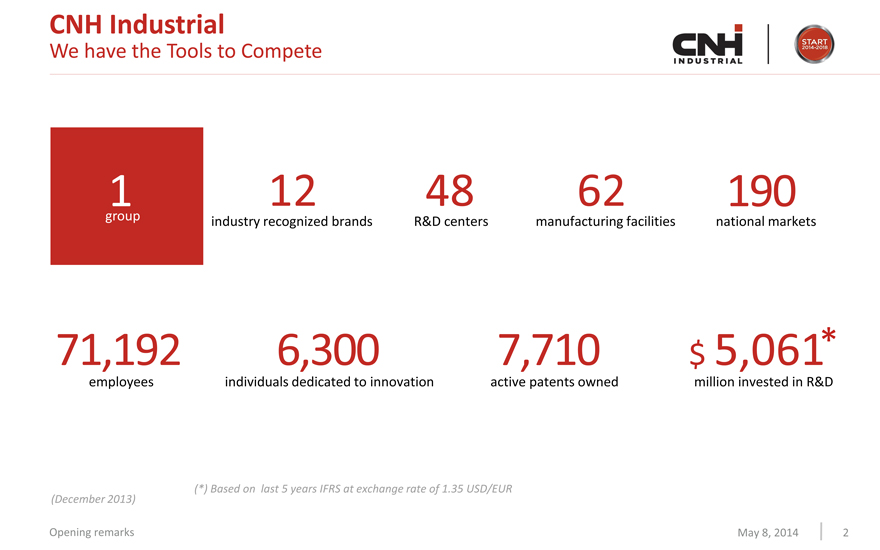

CNH Industrial

We have the Tools to Compete

1 12 48 62 190

group industry recognized brands R&D centers manufacturing facilities national markets

71,192 6,300 7,710 $ 5,061*

employees individuals dedicated to innovation active patents owned million invested in R&D

(*) Based on last 5 years IFRS at exchange rate of 1.35 USD/EUR (December 2013)

Opening remarks May 8, 2014 2

|

|

CNH Industrial

Our Products are tied together by Common Purpose

Professional industrial equipment and commercial vehicle customers

Full line distribution model with wide geographic coverage

Best in class powertrain technologies

Full lifecycle product services

Opening remarks

May 8, 2014 3

|

|

CNH Industrial

The Macro Trends driving our Business Plan

The Industrialization of the farming business Infrastructure modernization

Mission flexibility and efficiency The competitive edge

Opening remarks

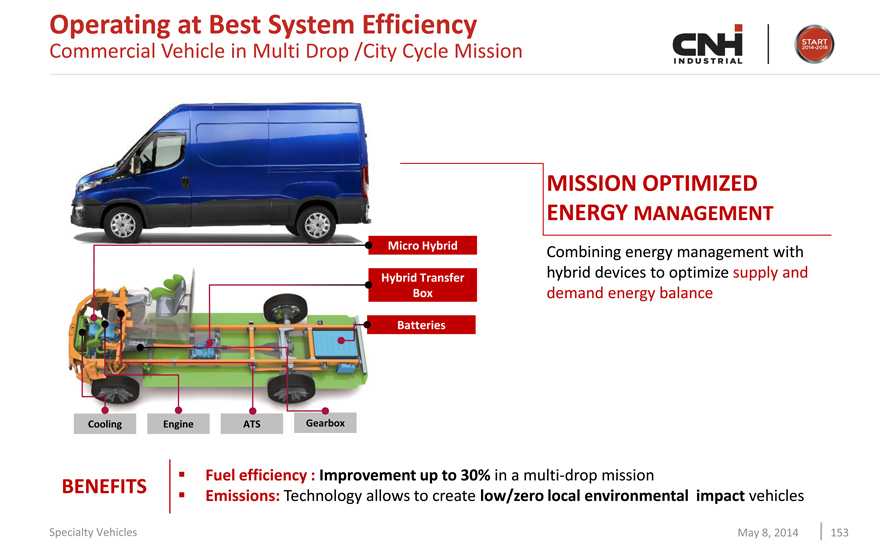

Micro Hybrid

Hybrid Transfer Box

Batteries

Cooling Engine ATS Gearbox

May 8, 2014 4

|

|

CNH Industrial

Plan Objectives

Expand world class agricultural business product portfolio and geographic reach

Re-position Construction Equipment brands and return to profitable growth

Fully realize the potential of the Commercial Vehicles new product pipeline

Leverage industry leading powertrain technologies investments commercial potential

Best in class product support and integration of support functions

Opening remarks May 8, 2014 5

|

|

CHAIRMAN Group Executive Council (GEC)

Sergio Marchionne

CEO GROUP

Rich Tobin

CHIEF OPERATING

OFFICERS NAFTA EMEA LATAM APAC IVECO POWERTRAIN

Brad Crews Andreas Klauser Vilmar Fistarol Stefano Pampalone Franco Fusignani Giovanni Bartoli

GLOBAL

BRAND Case IH New Holland Case New Holland

PRESIDENTS Ag Equipment Ag Equipment Iveco Construction Construction Parts & Service

Andreas Klauser Carlo Lambro Lorenzo Sistino Rich Tobin Rich Tobin Dino Maggioni

COMMERCIAL/

Chief Chief Precision Specialty

INDUSTRIAL Chief Manufacturing Chief Purchasing Solutions Vehicles

LEADERS Technical Officer Officer Quality Officer Officer & Telematics & GEC Coordinator

Dario Ivaldi Derek Neilson Adrian Pipe Annalisa Stupenengo Dino Maggioni Alessandro Nasi

SUPPORT/ Chief

President Chief Human

CORPORATE Financial Financial Resources

LEADERS Services Officer Officer

Oddone Incisa Max Chiara Linda Knoll

Opening remarks May 8, 2014 6

|

|

7 CNI

INDUSTRIAL

INVESTOR DAY

AUBURN HILLS

MAY 8TH, 2014

AGENDA

8:30 a.m. Opening Remarks

Case IH Brand

New Holland Agriculture

Precision Farming

Construction Equipment

Iveco

Iveco BUS

Specialty Vehicles

FPT Industrial

10:45 a.m. Break

Parts and Service

EMEA

APAC

LATAM

NAFTA

Manufacturing

12:35 p.m. Lunch

Financial Services

Q1 Results

Financial Forecast

2:50 p.m. Break

Q&A

Closing Comments

|

|

Investor day auburn hills may 8th, 2014

Case IH Brand

Andreas Klauser

|

|

Case IH Brand

Our Vision

To be the preferred partner in bringing innovative products and market leading agricultural solutions and services to our customers around the world

Our Focus

Large grain / Row crops Small grain / Cash crops Special crops

Case IH Brand May 8, 2014 9

|

|

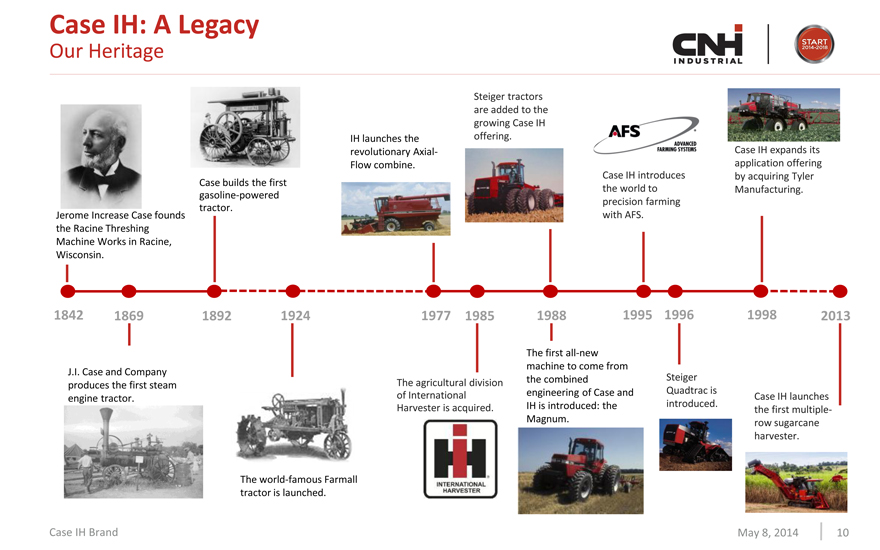

Case IH: A Legacy

Our Heritage

Steiger tractors

are added to the

growing Case IH

IH launches the offering.

revolutionary Axial- Case IH expands its

Flow combine. application offering

Case IH introduces by acquiring Tyler

Case builds the first

gasoline-powered the world to Manufacturing.

tractor. precision farming

Jerome Increase Case founds with AFS.

the Racine Threshing

Machine Works in Racine,

Wisconsin.

1842 1869 1892 1924 1977 1985 1988 1995 1996 1998 2013

The first all-new

machine to come from

J.I. Case and Company the combined Steiger

produces the first steam The agricultural division

engine tractor. of International engineering of Case and Quadtrac is Case IH launches

Harvester is acquired. IH is introduced: the introduced. the first multiple-

Magnum. row sugarcane

harvester.

The world-famous Farmall

tractor is launched.

Case IH Brand May 8, 2014 10

|

|

Case IH Brand Positioning

Who We Are

Global provider of premium equipment Key segments

Powerful Reliable Highly productive

Large grain & cash crop producers Contractors Specialty crop producers

Case IH Brand May 8, 2014 11

|

|

Case IH DNA

Recognized Global Leadership Serving Professional Farmers

Leading Products

Quadtrac Axial Flow Magnum Patriot

Feature Innovation

High Service Level Dealer Network Focused on Professional Farmers

Case IH Brand May 8, 2014 12

|

|

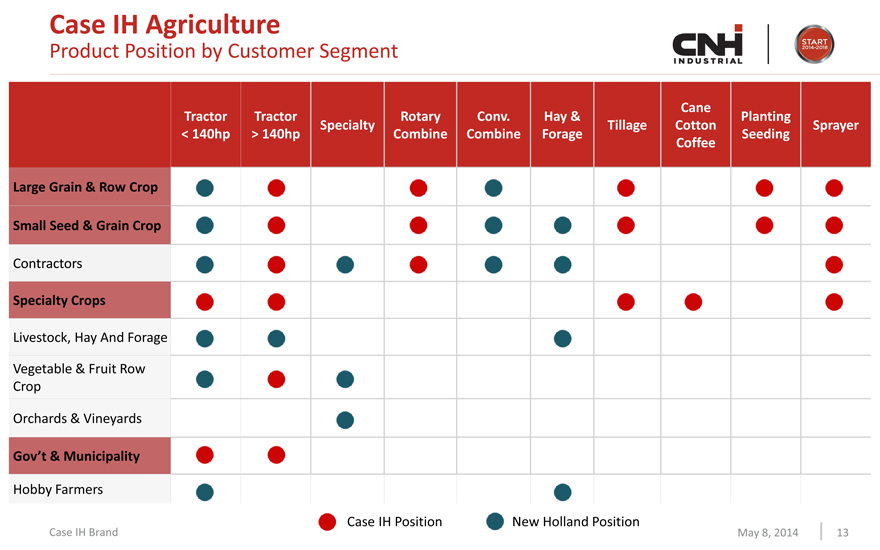

Case IH Agriculture

Product Position by Customer Segment

Cane

Tractor Tractor Rotary Conv. Hay & Planting

Specialty Tillage Cotton Sprayer

< 140hp > 140hp Combine Combine Forage Seeding

Coffee

Large Grain & Row Crop

Small Seed & Grain Crop

Contractors

Specialty Crops

Livestock, Hay And Forage

Vegetable & Fruit Row

Crop

Orchards & Vineyards

Gov’t & Municipality

Hobby Farmers

Case IH Position New Holland Position

Case IH Brand May 8, 2014 13

|

|

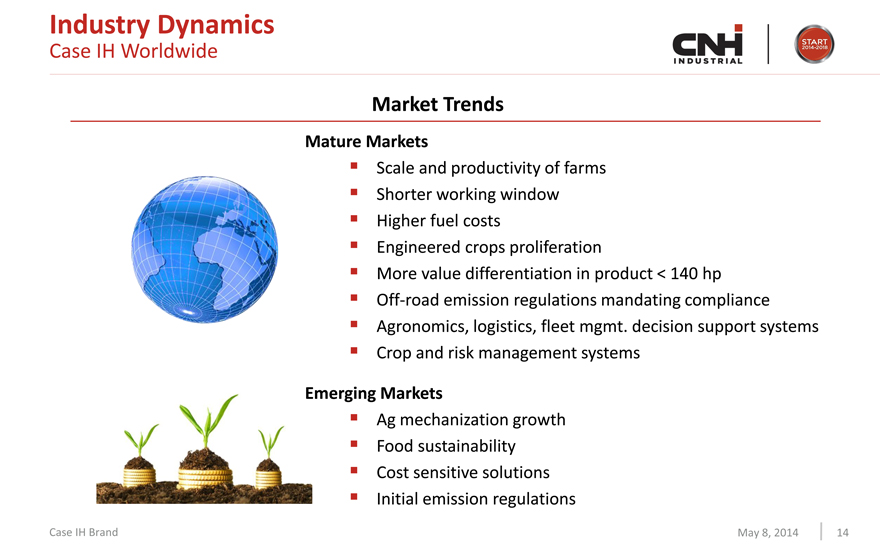

Industry Dynamics

Case IH Worldwide

Market Trends

Mature Markets

Scale and productivity of farms Shorter working window Higher fuel costs Engineered crops proliferation

More value differentiation in product < 140 hp Off-road emission regulations mandating compliance Agronomics, logistics, fleet mgmt. decision support systems Crop and risk management systems

Emerging Markets

Ag mechanization growth Food sustainability Cost sensitive solutions Initial emission regulations

Case IH Brand May 8, 2014 14

|

|

Key Product Strengths

Case IH Crop Cycle Solutions

Field Preparation: number 1 in Tillage in NAFTA Planters: Superior Seed Placement Accuracy Sprayers: Innovative Application Control Technology Combines: Best in Class Grain Quality Tractors: number 1 world wide in Track Technology

Case IH Brand May 8, 2014 15

|

|

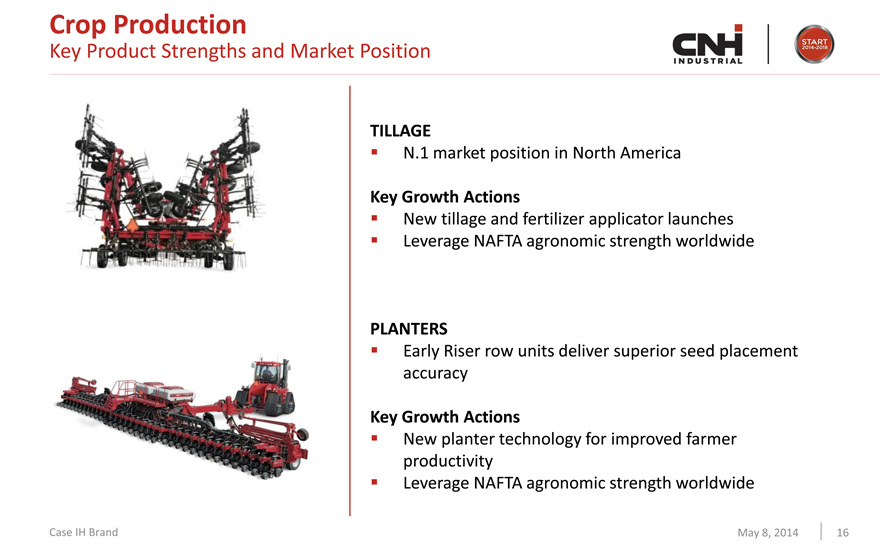

Crop Production

Key Product Strengths and Market Position

TILLAGE

N.1 market position in North America

New tillage and fertilizer applicator launches Leverage NAFTA agronomic strength worldwide

Early Riser row units deliver superior seed placement accuracy

New planter technology for improved farmer productivity Leverage NAFTA agronomic strength worldwide

Key Growth Actions

PLANTERS

Key Growth Actions Case IH Brand May 8, 2014 16

|

|

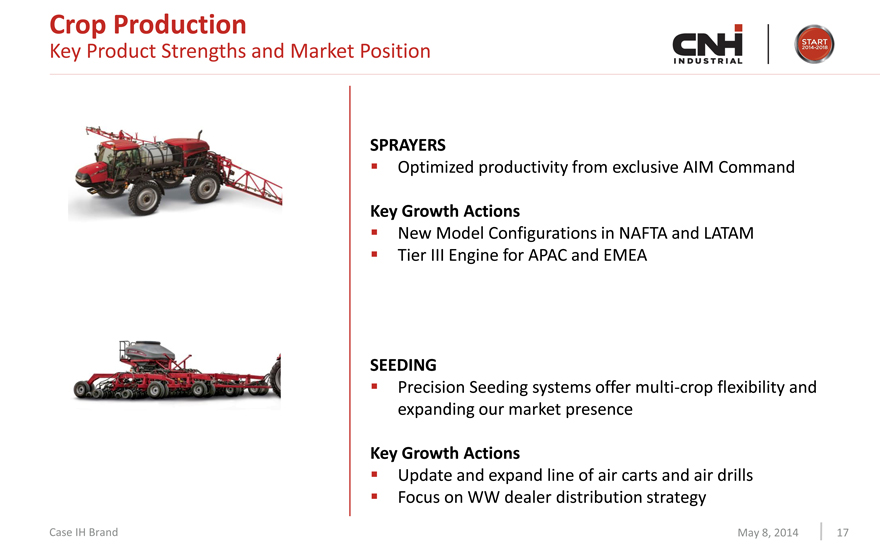

Crop Production

Key Product Strengths and Market Position

SPRAYERS

Key Growth Actions

SEEDING

Key Growth Actions

Optimized productivity from exclusive AIM Command

New Model Configurations in NAFTA and LATAM Tier III Engine for APAC and EMEA

Precision Seeding systems offer multi-crop flexibility and expanding our market presence

Update and expand line of air carts and air drills Focus on WW dealer distribution strategy

Case IH Brand May 8, 2014 17

|

|

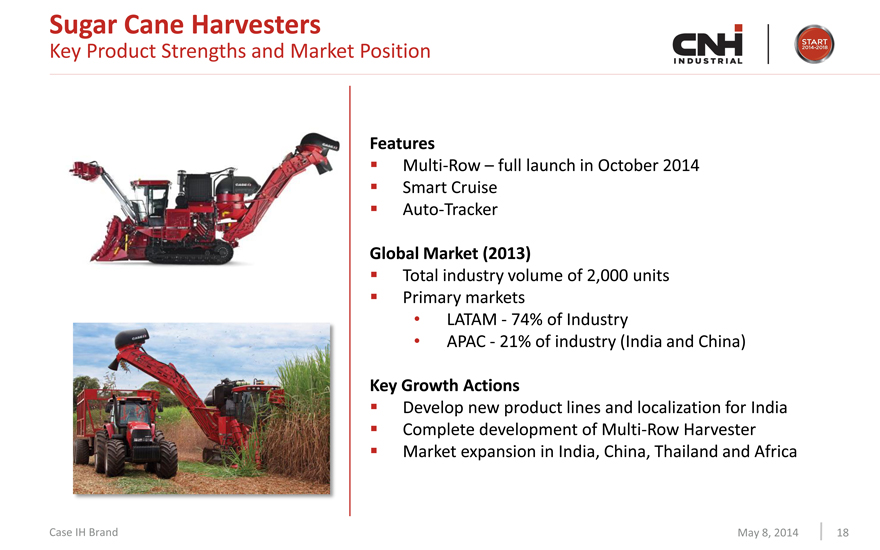

Sugar Cane Harvesters

Key Product Strengths and Market Position

Features

Multi-Row – full launch in October 2014

Smart Cruise

Auto-Tracker

Global Market (2013)

Total industry volume of 2,000 units Primary markets

LATAM—74% of Industry

APAC—21% of industry (India and China)

Key Growth Actions

Develop new product lines and localization for India Complete development of Multi-Row Harvester Market expansion in India, China, Thailand and Africa

Case IH Brand May 8, 2014 18

|

|

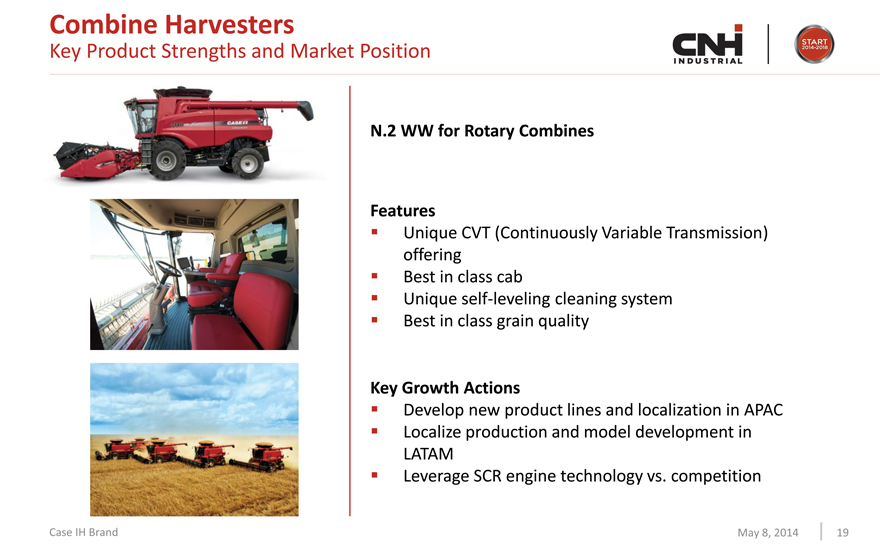

Combine Harvesters

Key Product Strengths and Market Position

N.2 WW for Rotary Combines

Features

Unique CVT (Continuously Variable Transmission) offering Best in class cab Unique self-leveling cleaning system Best in class grain quality

Key Growth Actions

Develop new product lines and localization in APAC Localize production and model development in LATAM

Leverage SCR engine technology vs. competition

Case IH Brand May 8, 2014 19

|

|

Key Product and Technology: High HP tractors

Key Product Strengths and Market Position

N.1 WW for High Horsepower Track Solutions

N.2 WW for High Horsepower Tractors

Features

Industry leading Quadtrac technology Best in class fuel efficiency Best in class operator environment CVT transmission offering

Key Growth Actions

Increase HP ranges

Extension of track offering across the line-up Extension of CVT offering across the line-up Localize production and models in APAC

Case IH Brand May 8, 2014 20

|

|

Case IH Rowtrac

The Best Solution for Row Crops

REFERENCE

INDEX ROWTRAC

COMPETITOR

HORSEPOWER Rated horsepower 370 500

TRACTION Number of tracks 2 4

COMPACTION Ground PSI 12.48 11.38

TURNING POWER Power in turns Skid steer Full power

in turns

OPERATOR COMFORT Cab suspension No Yes

3 pt. hitch lift

CAPACITY 15,300 lbs. 20,000 lbs.

capacity

HYDRAULIC FLOW Max. Up to 60 Up to 113

FUEL TANK CAPACITY Gallons 184 250

Case IH Brand May 8, 2014 21

|

|

Network Strategy

Mature and Emerging Markets

Mature Markets: Consolidation

Leverage financial strengths, stability Improve customer services, experience Improve technical service capabilities

Emerging Markets: Expansion

Expand key geographic areas Improve coverage, density

Improve service quality and customer experience

Case IH Brand May 8, 2014 22

|

|

Growth Strategies

Target Professional Farmers Deliver Best in Class Solutions Expand in Emerging Markets Strengthen Dealers & Widen Service Offering

Case IH Brand May 8, 2014 23

|

|

New Holland Agriculture

Investor day auburn hills may 8th, 2014

Carlo Lambro

|

|

New Holland Agriculture

Brand Statement

The farming generalist with a complete agricultural equipment product offering, specialized in livestock, hay & forage, small seed crop, orchards & vineyards.

A global presence with customer proximity through a strong dealer network and industry-leading solutions for profitable, sustainable agriculture

May 8, 2014 25

|

|

New Holland Agriculture

Our History – Over 100 Years of Innovation

Fiat Trattori In 1991 Fiat Geotech

became FiatAgri purchased Ford New

and

Merger

First FIAT Case IH

tractor built FiatAgri acquired Meger FiatAgri New Holland

Braud and Fiat Allis

1895 1906 1917 1918 1947 1964 1974 1984 1986 1988 1991 1998 1999 2006 2011 2013

Ford first New Holland Ford bought Sperry New Holland

tractor built changed its name and formed

into Sperry New Ford New Holland Inc

Holland

New Holland

was founded In New Holland acquired Bizon,

Pennsylvania by Sperry New Holland combine manufacturer based

Abe acquired Claeys in Płock, Poland

Zimmermann

Claeys was founded In

Zedelgem by Leon Claeys

HISTORY ACQUISITIONS/MERGERS INTEGRATION

New Holland Agriculture May 8, 2014 26

|

|

New Holland Agriculture

The Broadest Product Offering

AGRICULTURAL TRACTORS

T4F/V/N TK4000 T4 T5 T6 T7 T8 T9

Specialty tractors Medium horse power tractors High horse power tractors

HARVESTING & COMPACT TRACTORS

Rotary Conventional Conventional Forage Grape Harvester Boomer Rustler Telehandler

Flagship Value Harvester

Combines Self Propelled Forage Harvester Compact tractors

HAY AND FORAGE & APPLICATION EQUIPMENT

Round Large Disc Mower Tedders Wheel rake Air Carts / Air Sprayers

Balers Square Conditioner disk drills

Balers

Hay & Forage Application Equipment

New Holland Agriculture May 8, 2014 27

|

|

New Holland Agriculture

The Clean Energy Leader®—Sustainable, Efficient Technology

The New Holland Clean Energy Leader strategy is based on four key pillars:

1. GROWING ENERGY 2. EFFICIENT PRODUCTIVITY

Biodiesel Bioethanol Biomass

The Energy Independent Farm

Tier 4A and Tier 4B Technology Precision Land Management (PLM) Innovation

3. SUSTAINABLE FARMING 4. COMMITTED BRAND

Carbon Footprint EcoBraud Conservation Agriculture

Plant Certification Recycling

Dow Jones Sustainability Index sector leader

New Holland Agriculture May 8, 2014 28

|

|

New Holland Agriculture

Engine Technology

THE NEW HOLLAND COMPETITIVE ADVANTAGE

New Holland ECOBlue HI-eSCR Technology

Business as usual. Performance unmatched.

Tier4 Final implementation for the North American and European markets with FPT Hi-eSCR engine technology providing best in class solution for:

Performance Efficiency Simplicity Consistency

Consistency

0 1 2 3 4 5 6 7 8 9 10

0 0.1 0.2 0.3 0.4 0.5 0.6

PM NOx

Tier-4B (2014)

Tier-4A (2011)

Tier-3 (2006)

Tier-2 (2002)

Tier-1 (1996)

New Holland Agriculture May 8, 2014 29

|

|

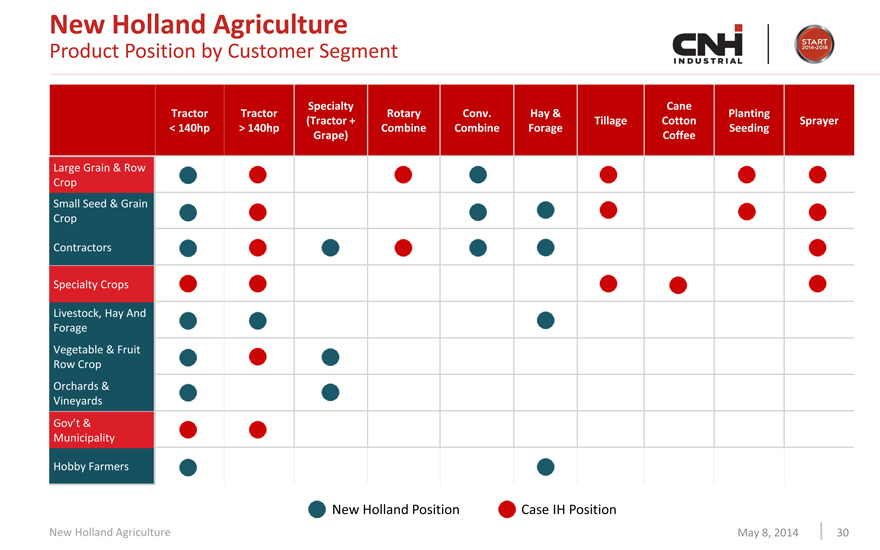

New Holland Agriculture

Product Position by Customer Segment

Specialty Cane

Tractor Tractor Rotary Conv. Hay & Planting

(Tractor + Tillage Cotton Sprayer

< 140hp > 140hp Combine Combine Forage Seeding

Grape) Coffee

Large Grain & Row

Crop

Small Seed & Grain

Crop

Contractors

Specialty Crops

Livestock, Hay And

Forage

Vegetable & Fruit

Row Crop

Orchards &

Vineyards

Gov’t &

Municipality

Hobby Farmers

New Holland Position Case IH Position

New Holland Agriculture May 8, 2014 30

|

|

Key Product Strengths

Industry Leading Conventional Combine Technology Number 1 Worldwide in Specialty Segment Worldwide Leader in Hay & Forage Equipment Advanced Solutions for Mid-Range Tractor Applications Complete Tier4b Compliance Product Offering

New Holland Agriculture May 8, 2014 31

|

|

Tractors

Key Product Strengths and Market Position

Number 2 Worldwide in Mid-Range Horse Power Segment

T5 – T6 – T7 segment:

Features

Eco BlueTM HI-eSCR

3 levels of transmission technology Best in Class Operator environment

Single touch screen monitor can allow control of both tractor and precision farming functions Higher traction levels while reducing soil compaction

Key Growth Actions

New tractor (CCM heavy duty) launch in EMEA, 2015 Fully renewed range (localized production) in LATAM, 2014 to 2016 Utilize CNH Industrial low cost country manufacturing locations to serve NAFTA value segment

New Holland Agriculture May 8, 2014 32

|

|

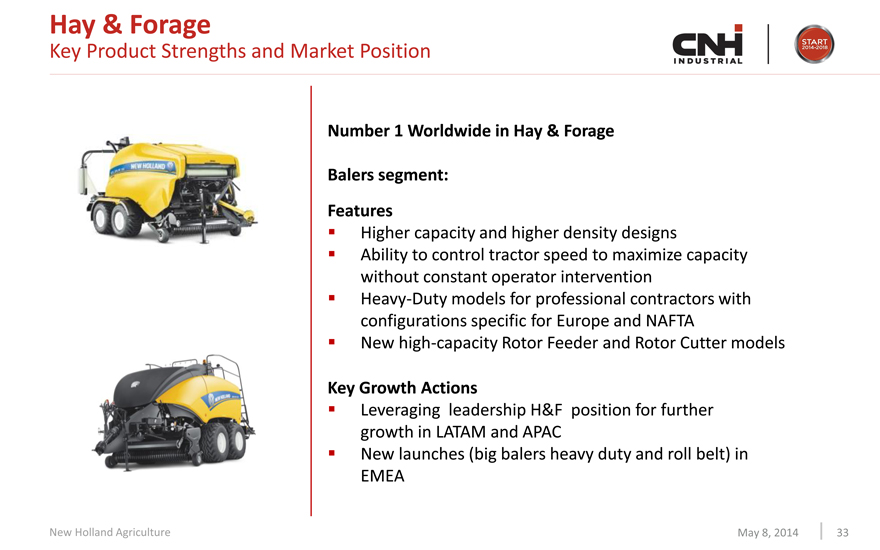

Hay & Forage

Key Product Strengths and Market Position

Number 1 Worldwide in Hay & Forage

Balers segment:

Features

Higher capacity and higher density designs Ability to control tractor speed to maximize capacity without constant operator intervention Heavy-Duty models for professional contractors with configurations specific for Europe and NAFTA New high-capacity Rotor Feeder and Rotor Cutter models

Key Growth Actions

Leveraging leadership H&F position for further growth in LATAM and APAC

New launches (big balers heavy duty and roll belt) in EMEA

New Holland Agriculture May 8, 2014 33

|

|

Specialty

Key Product Strengths and Market Position

Number 1 Worldwide in the Specialty Segment

Self Propelled Grape Harvester and Specialty Tractors:

Features

Suspended SuperSteer Front Axle for best in class 4WD maneuverability and driving comfort Tractors link with Braud harvesters: same driver interface and vehicle to vehicle connectivity Braud—Opti-GrapeTM system

Key Growth Actions

Leverage leader position in the segment to further grow in NAFTA

Launch new premium product in EMEA

Launch both new harvesters and specialty tractors in LATAM Product offering for coffee, orange and small fruit harvesting

New Holland Agriculture May 8, 2014 34

|

|

Combine Harvesters

Key Product Strengths and Market Position

Number 1 Worldwide in Conventional Combines

Flagship and Value Conventional segment:

Features

Best in class productivity

New Harvest SuiteTM Ultra BIC cabs

SmartSieveTM self leveling cleaning with Opti-FanTM system Triple-CleanTM system: 15% increased cleaning in major crops

Key Growth Actions

Additional localized model in Latin America Develop new product lines and localization for APAC New product features to consolidate strong European position

New Holland Agriculture May 8, 2014 35

|

|

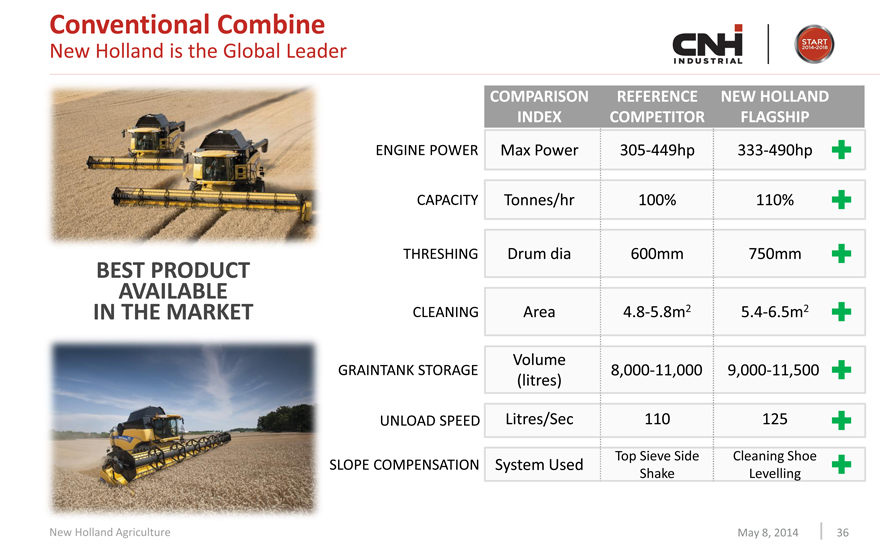

Conventional Combine

New Holland is the Global Leader

COMPARISON REFERENCE NEW HOLLAND

INDEX COMPETITOR FLAGSHIP

ENGINE POWER Max Power 305-449hp 333-490hp

CAPACITY Tonnes/hr 100% 110%

THRESHING Drum dia 600mm 750mm

CLEANING Area 4.8-5.8m2 5.4-6.5m2

Volume

GRAINTANK STORAGE 8,000-11,000 9,000-11,500

(litres)

UNLOAD SPEED Litres/Sec 110 125

SLOPE COMPENSATION System Used Top Sieve Side Cleaning Shoe

Shake Levelling

BEST PRODUCT AVAILABLE IN THE MARKET

New Holland Agriculture May 8, 2014 36

|

|

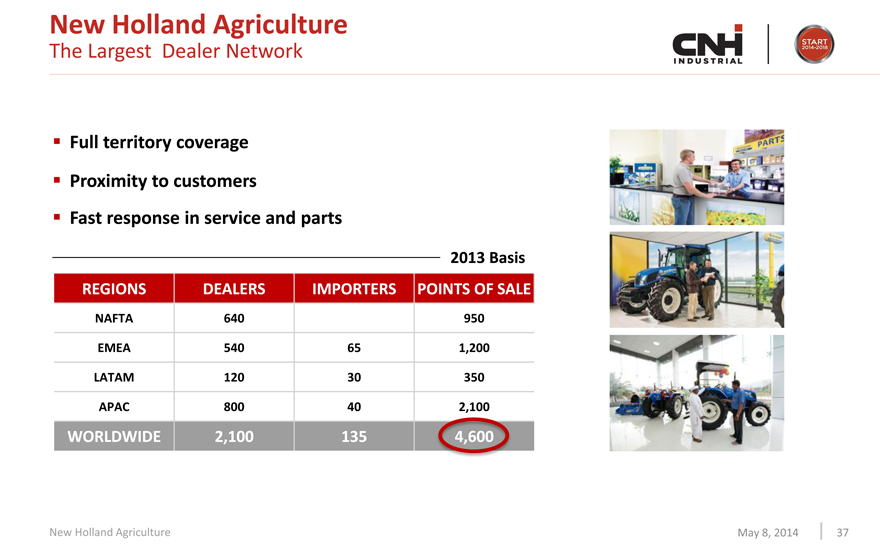

New Holland Agriculture

The Largest Dealer Network

Full territory coverage

Proximity to customers

Fast response in service and parts

2013 Basis

REGIONS DEALERS IMPORTERS POINTS OF SALE

NAFTA 640 950

EMEA 540 65 1,200

LATAM 120 30 350

APAC 800 40 2,100

WORLDWIDE 2,100 135 4,600

New Holland Agriculture May 8, 2014 37

|

|

New Holland Agriculture

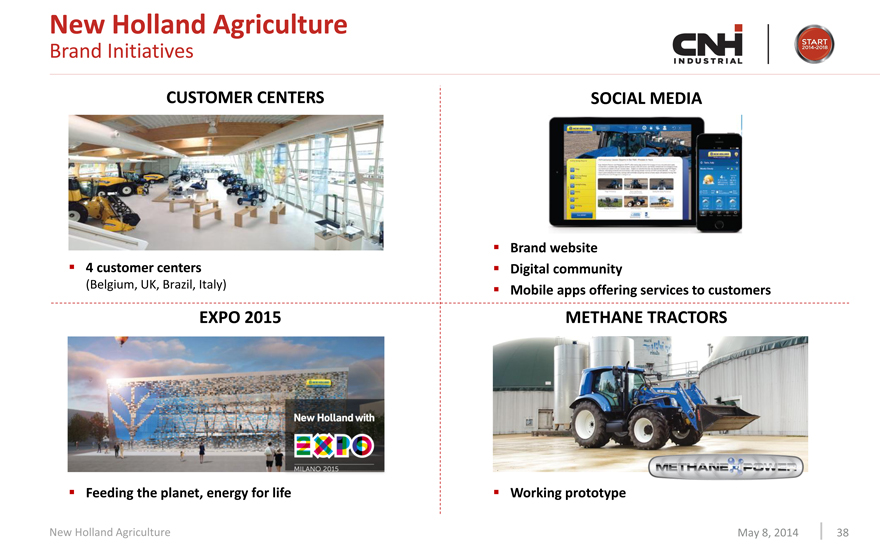

Brand Initiatives

CUSTOMER CENTERS SOCIAL MEDIA

Brand website Digital community

Mobile apps offering services to customers

EXPO 2015 METHANE TRACTORS

Feeding the planet, energy for life

Working prototype

4 customer centers

(Belgium, UK, Brazil, Italy)

New Holland Agriculture

May 8, 2014 38

|

|

New Holland Growth Strategy

Leverage new product introduction Provide Industry-leading Offer the widest agricultural in mature markets and expand solutions for efficient and equipment product range geographical presence in emerging sustainable farming markets

Through a Strong Dealer Network ensuring Proximity to Customers and Complete Business Solutions

New Holland Agriculture

May 8, 2014 39

|

|

Investor day auburn hills may 8th, 2014

Precision Farming

David Larson

|

|

Executive Summary

CNH Industrial Precision Farming Direction

1. CNH Industrial Precision Farming base technology

Increasing integration into core products

Some technologies also utilized in Construction and Commercial Vehicles

2. Roles of participants in the Precision Farming market are changing

Telematics will create new data centric opportunities Open Data architecture will become a paradigm for OEM CNH Industrial is well positioned for the evolving market structure

3. CNH Industrial will create alliances with best in class technology providers

Integrating components from these providers into core products To develop open and secure data systems To deliver best in class, flexible, and innovative products

CNH Industrial’s goal is to enable our customers to realize

full value from their machines and machine data

Precision Farming May 8, 2014 41

|

|

Precision Farming Product Offering

Major Product Families and Customer Drivers

Factory and dealer installed solutions

Creating value for our customers through the farming cycle: Planting, Growing, Harvesting & Planning

Application Attribute & Yield Telematics &

Guidance

Control Monitoring Integrated Solutions

Displays

Improve efficiency Lower input costs Increase yield Support decisions

Guide the correct Plant/ fertilize / Understand Select paths and turns spray only where needed in-field variability the right seed and fertilizers

CNH Industrial Complete Precision Farming Product Offering

An Integral Part of All New Products – Built in not Added On

Precision Farming May 8, 2014 42

|

|

CNH Industrial Market Facing Approach

Common System with Branded Offerings for Case IH and NH

Precision Farming Brands

Single Precision Farming System across Product Lines, Regions and Brands

Case IH and New Holland offer uniquely branded offerings comprised of common CNH Industrial Precision Farming System components

Precision Farming May 8, 2014 43

|

|

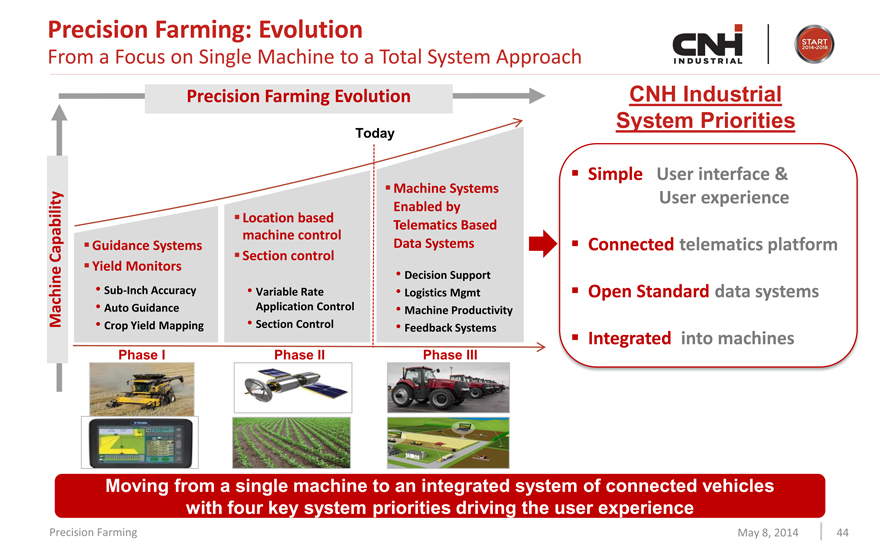

Precision Farming: Evolution

From a Focus on Single Machine to a Total System Approach

Precision Farming Evolution

Today

Machine Systems

Enabled by

Location based Telematics Based

machine control

Guidance Systems Data Systems

Capability Section control

Yield Monitors Decision Support

Sub-Inch Accuracy Variable Rate Logistics Mgmt

Machine Auto Guidance Application Control Machine Productivity

Crop Yield Mapping Section Control Feedback Systems

Phase I Phase II Phase III

Simple User interface & User experience

Connected telematics platform Open Standard data systems Integrated into machines

CNH Industrial

System Priorities

Moving from a single machine to an integrated system of connected vehicles

with four key system priorities driving the user experience

Precision Farming May 8, 2014 44

|

|

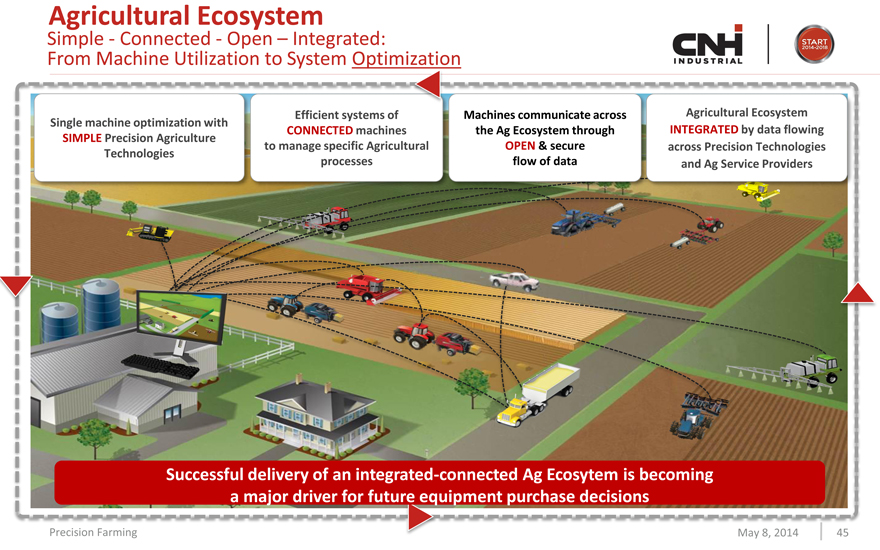

Agricultural Ecosystem

Simple - Connected - Open – Integrated: From Machine Utilization to System Optimization

Machines communicate across Agricultural Ecosystem the Ag Ecosystem through INTEGRATED by data flowing OPEN & secure across Precision Technologies flow of data and Ag Service Providers

Successful delivery of an integrated-connected Ag Ecosytem is becoming a major driver for future equipment purchase decisions

Precision Farming May 8, 2014 45

Single machine optimization with SIMPLE Precision Agriculture Technologies

Efficient systems of CONNECTED machines to manage specific Agricultural processes

|

|

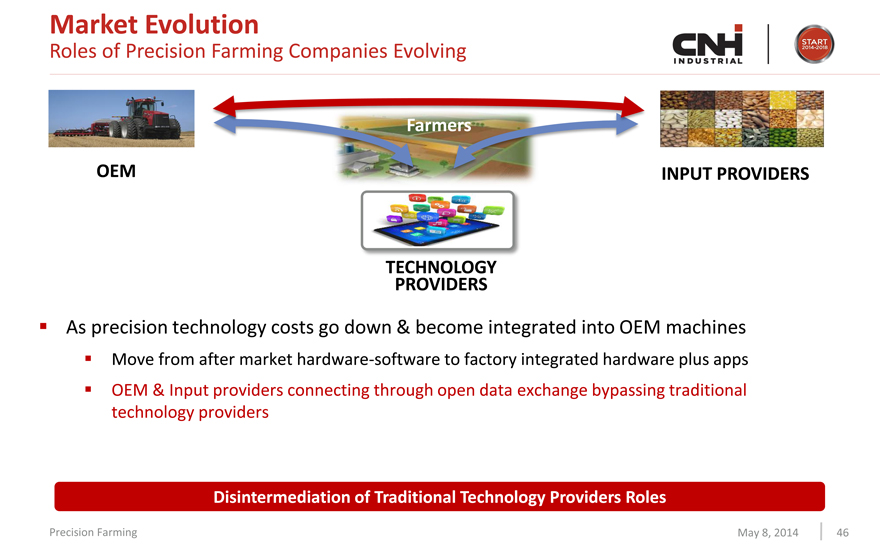

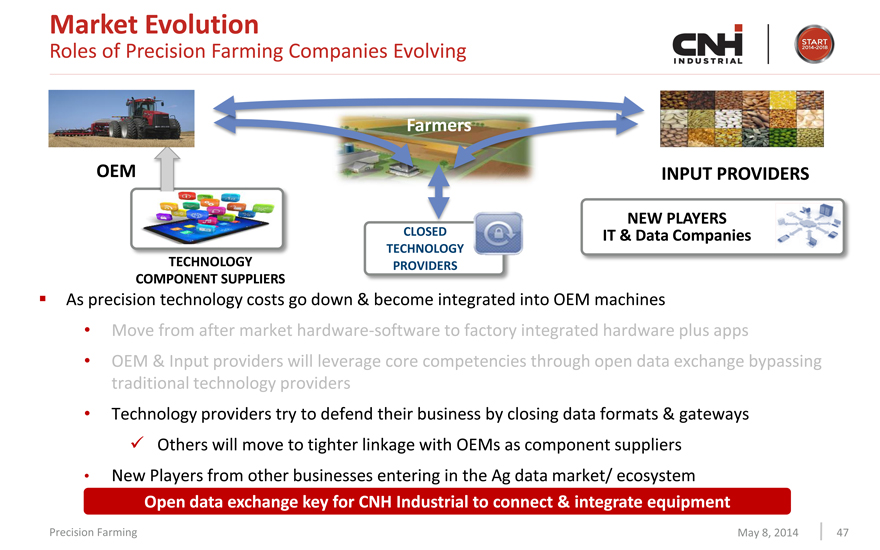

Market Evolution

Roles of Precision Farming Companies Evolving

Farmers

OEM INPUT PROVIDERS

TECHNOLOGY PROVIDERS

As precision technology costs go down & become integrated into OEM machines

Move from after market hardware-software to factory integrated hardware plus apps OEM & Input providers connecting through open data exchange bypassing traditional technology providers

Disintermediation of Traditional Technology Providers Roles

May 8, 2014 46

Precision Farming

|

|

Market Evolution

Roles of Precision Farming Companies Evolving

Farmers

OEM INPUT PROVIDERS

NEW PLAYERS IT & Data Companies

TECHNOLOGY

CLOSED TECHNOLOGY PROVIDERS

COMPONENT SUPPLIERS

As precision technology costs go down & become integrated into OEM machines

Move from after market hardware-software to factory integrated hardware plus apps

OEM & Input providers will leverage core competencies through open data exchange bypassing traditional technology providers Technology providers try to defend their business by closing data formats & gateways

Others will move to tighter linkage with OEMs as component suppliers

Open data exchange key for CNH Industrial to connect & integrate equipment

New Players from other businesses entering in the Ag data market/ ecosystem Precision Farming May 8, 2014 47

|

|

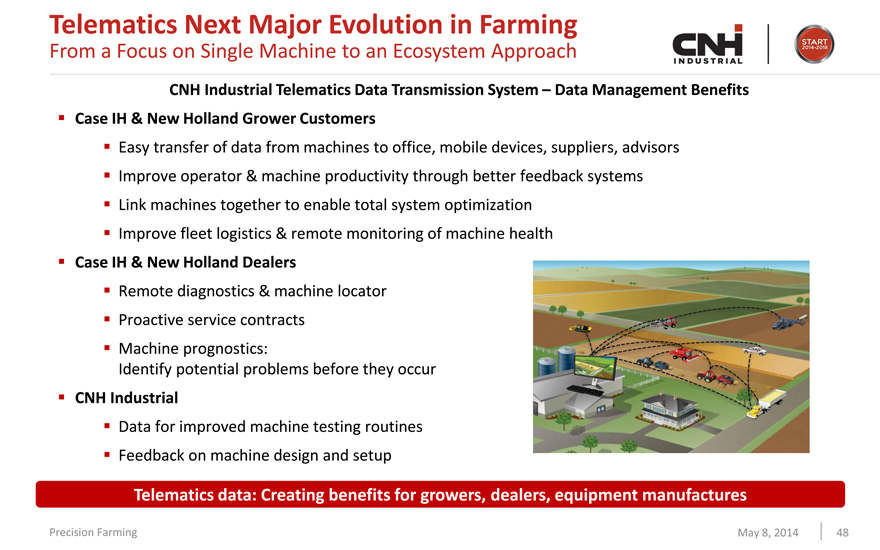

Telematics Next Major Evolution in Farming

From a Focus on Single Machine to an Ecosystem Approach

CNH Industrial Telematics Data Transmission System – Data Management Benefits

Case IH & New Holland Grower Customers

Easy transfer of data from machines to office, mobile devices, suppliers, advisors Improve operator & machine productivity through better feedback systems Link machines together to enable total system optimization Improve fleet logistics & remote monitoring of machine health

Case IH & New Holland Dealers

Remote diagnostics & machine locator Proactive service contracts Machine prognostics: Identify potential problems before they occur

CNH Industrial

Data for improved machine testing routines Feedback on machine design and setup

Telematics data: Creating benefits for growers, dealers, equipment manufactures

Precision Farming May 8, 2014 48

|

|

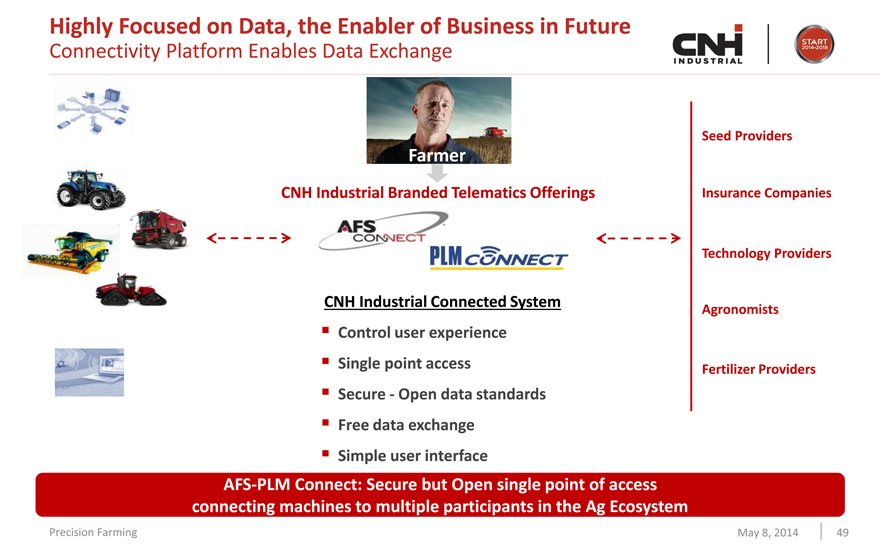

Highly Focused on Data, the Enabler of Business in Future

Connectivity Platform Enables Data Exchange

Farmer

CNH Industrial Branded Telematics Offerings

Seed Providers Insurance Companies Technology Providers Agronomists Fertilizer Providers

CNH Industrial Connected System

Control user experience Single point access Secure—Open data standards Free data exchange Simple user interface

AFS-PLM Connect: Secure but Open single point of access

connecting machines to multiple participants in the Ag Ecosystem

Precision Farming May 8, 2014 49

|

|

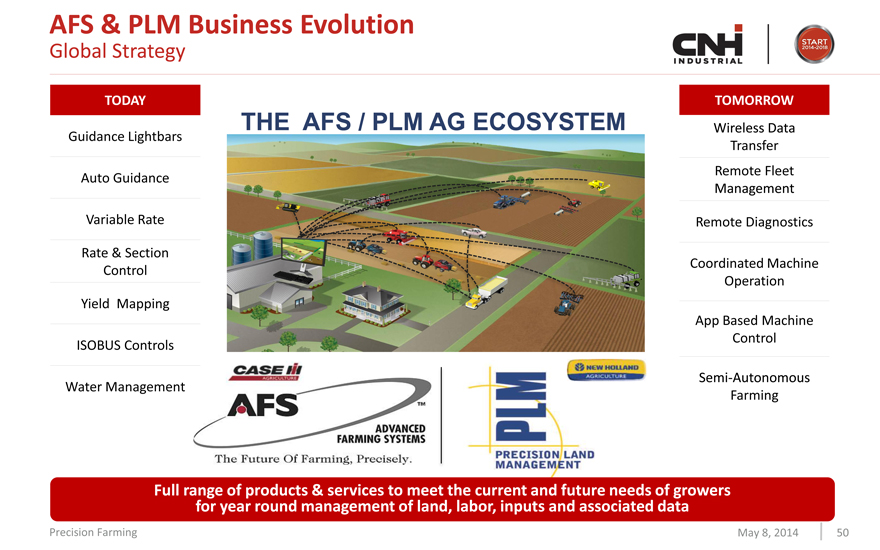

AFS & PLM Business Evolution

Global Strategy

THE AFS / PLM AG ECOSYSTEM

TODAY

Guidance Lightbars Auto Guidance Variable Rate

Rate & Section Control

Yield Mapping ISOBUS Controls Water Management TOMORROW

Wireless Data

Transfer

Remote Fleet

Management

Remote Diagnostics

Coordinated Machine Operation

App Based Machine Control

Semi-Autonomous

Farming

Full range of products & services to meet the current and future needs of growers

for year round management of land, labor, inputs and associated data

Precision Farming May 8, 2014 50

|

|

FARM WITH PRECISION

Precision Farming May 8, 2014 51

|

|

Investor day auburn hills may 8th, 2014

Construction Equipment

Richard Tobin

|

|

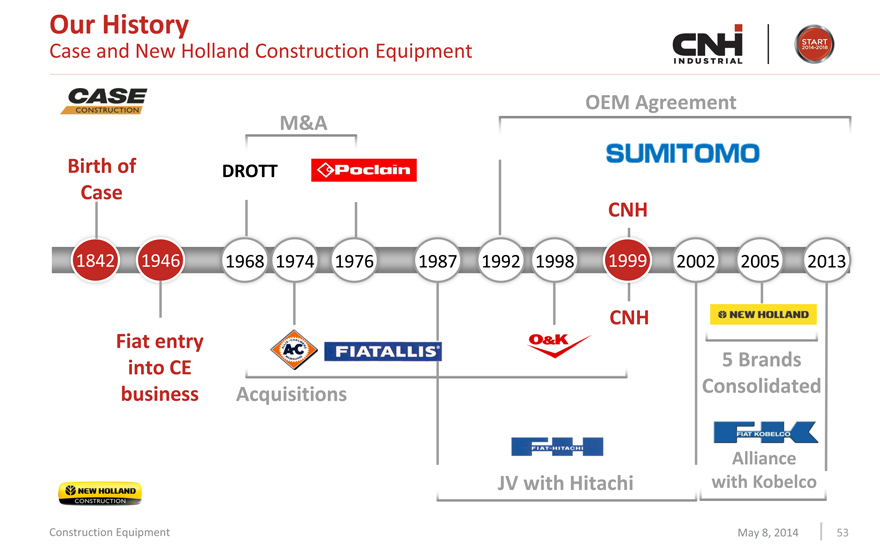

Our History

Case and New Holland Construction Equipment

OEM Agreement

M&A

Birth of DROTT

Case

CNH

1842 1946 1968 1974 1976 1987 1992 1998 1999 2002 2005 2013

CNH

Fiat entry

into CE 5 Brands

business Acquisitions Consolidated

Alliance

JV with Hitachi with Kobelco

Construction Equipment May 8, 2014 53

|

|

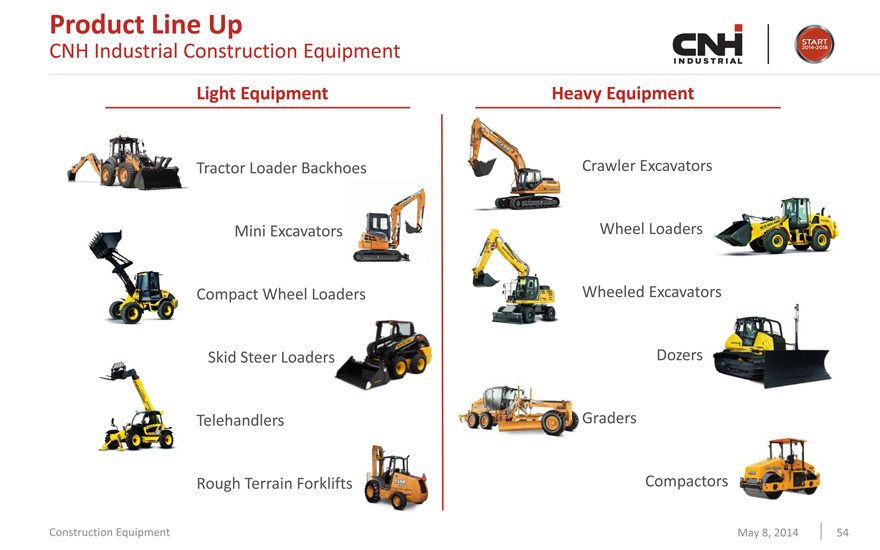

Product Line Up

CNH Industrial Construction Equipment

Light Equipment Heavy Equipment

Tractor Loader Backhoes Crawler Excavators Mini Excavators Wheel Loaders Compact Wheel Loaders Wheeled Excavators Skid Steer Loaders Dozers Telehandlers Graders Rough Terrain Forklifts Compactors

Construction Equipment May 8, 2014 54

|

|

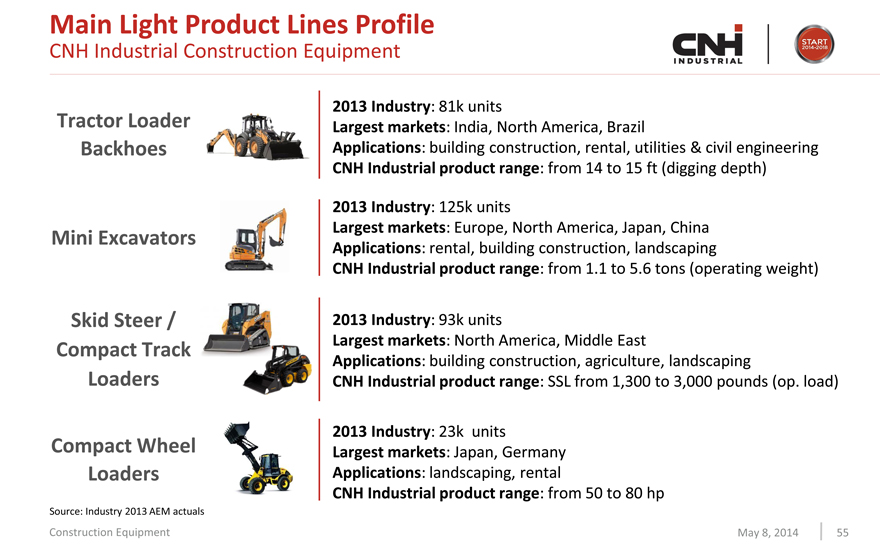

Main Light Product Lines Profile

CNH Industrial Construction Equipment

2013 Industry: 81k units

Tractor Loader Largest markets: India, North America, Brazil

Backhoes Applications: building construction, rental, utilities & civil engineering

CNH Industrial product range: from 14 to 15 ft (digging depth)

2013 Industry: 125k units

Mini Excavators Largest markets: Europe, North America, Japan, China

Applications: rental, building construction, landscaping

CNH Industrial product range: from 1.1 to 5.6 tons (operating weight)

Skid Steer / 2013 Industry: 93k units

Compact Track Largest markets: North America, Middle East

Applications: building construction, agriculture, landscaping

Loaders CNH Industrial product range: SSL from 1,300 to 3,000 pounds (op. load)

2013 Industry: 23k units

Compact Wheel Largest markets: Japan, Germany

Loaders Applications: landscaping, rental

CNH Industrial product range: from 50 to 80 hp

Source: Industry 2013 AEM actuals

Construction Equipment May 8, 2014 55

|

|

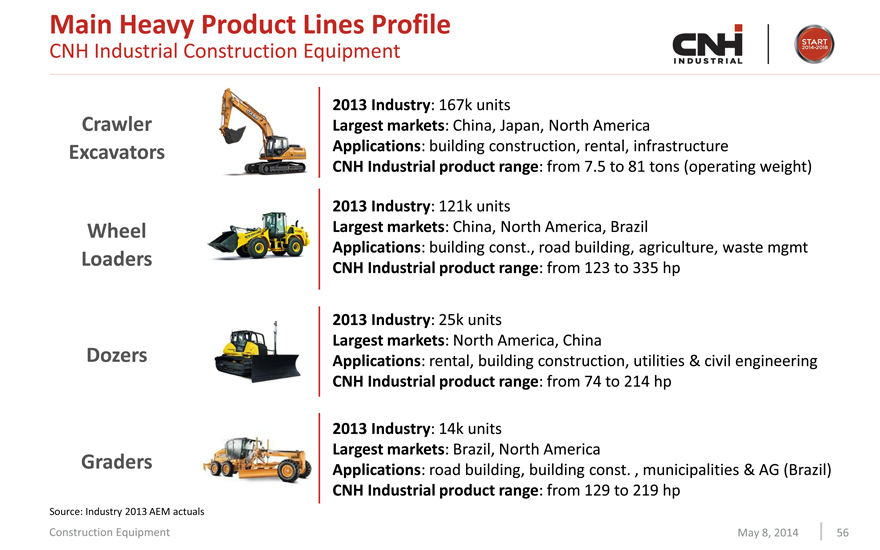

Main Heavy Product Lines Profile

CNH Industrial Construction Equipment

Crawler Excavators

Wheel

Loaders

Dozers

Graders

2013 Industry: 167k units

Largest markets: China, Japan, North America

Applications: building construction, rental, infrastructure

CNH Industrial product range: from 7.5 to 81 tons (operating weight)

2013 Industry: 121k units

Largest markets: China, North America, Brazil

Applications: building const., road building, agriculture, waste mgmt

CNH Industrial product range: from 123 to 335 hp

2013 Industry: 25k units

Largest markets: North America, China

Applications: rental, building construction, utilities & civil engineering

CNH Industrial product range: from 74 to 214 hp

2013 Industry: 14k units

Largest markets: Brazil, North America

Applications: road building, building const. , municipalities & AG (Brazil)

CNH Industrial product range: from 129 to 219 hp

Source: Industry 2013 AEM actuals

Construction Equipment May 8, 2014 56

|

|

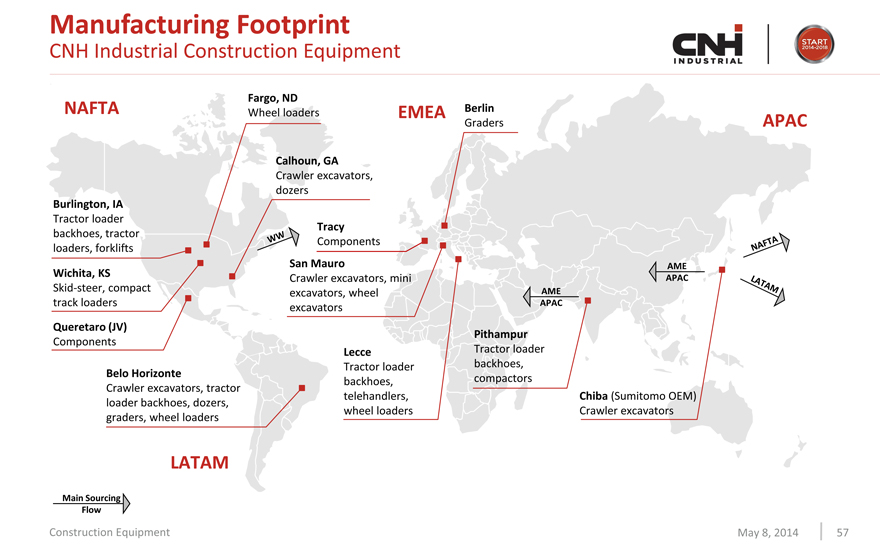

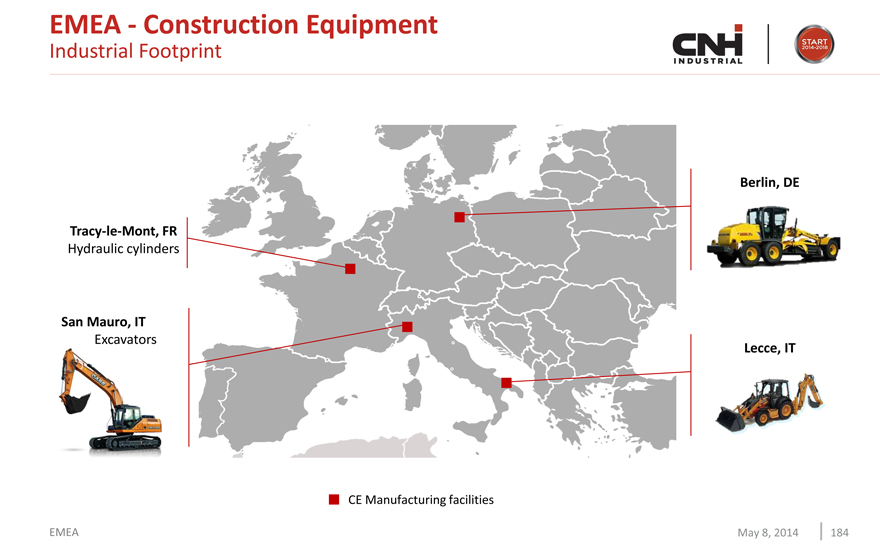

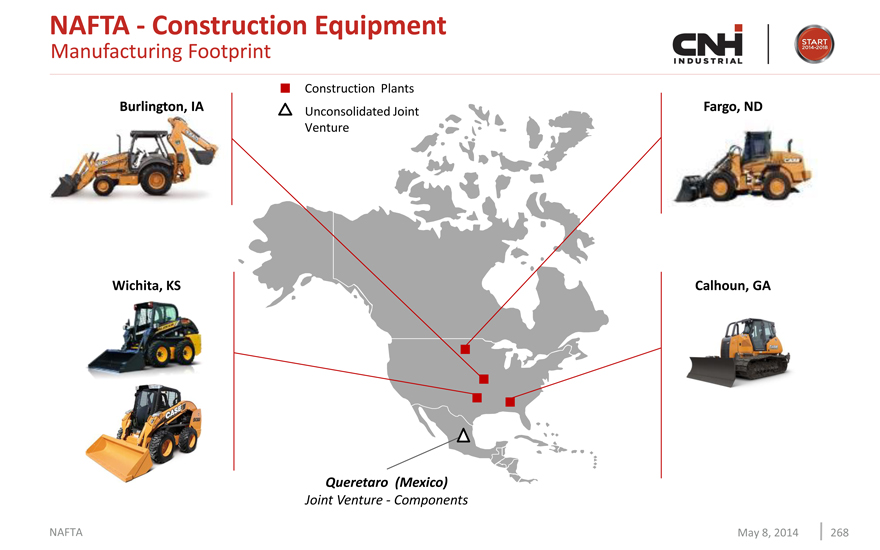

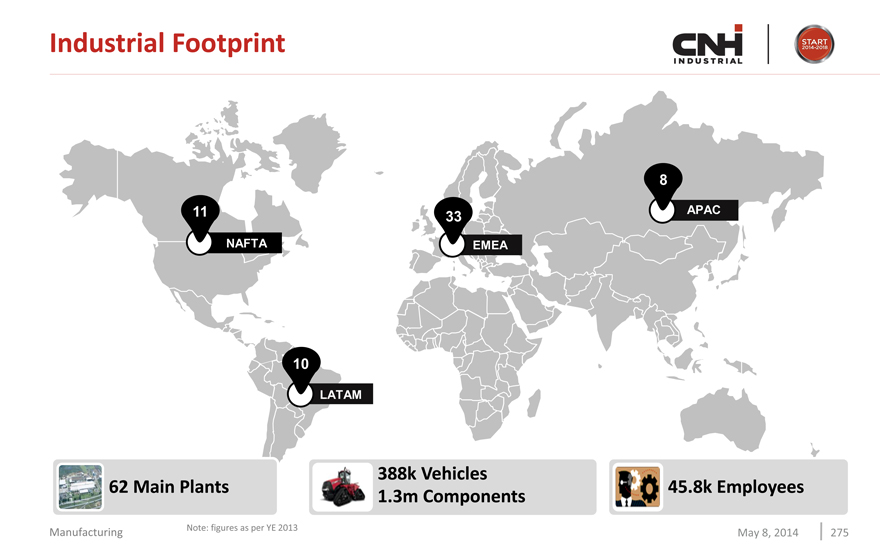

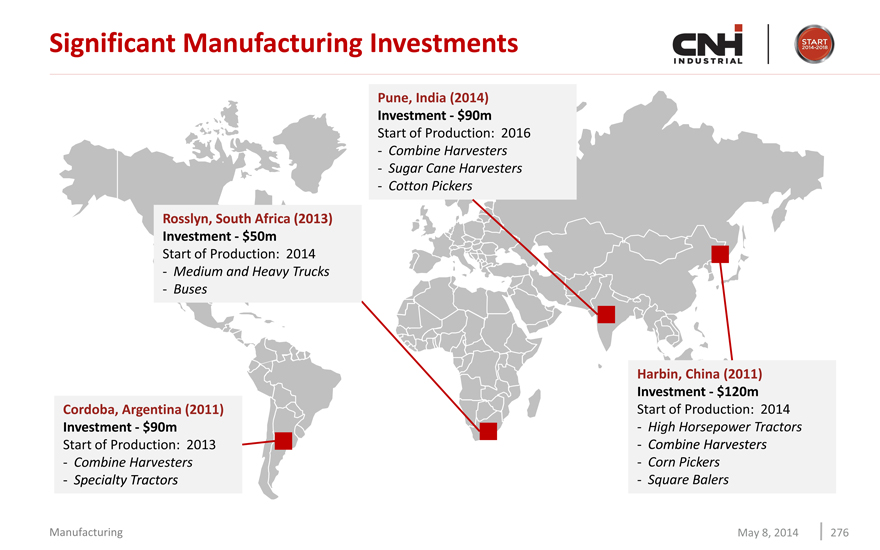

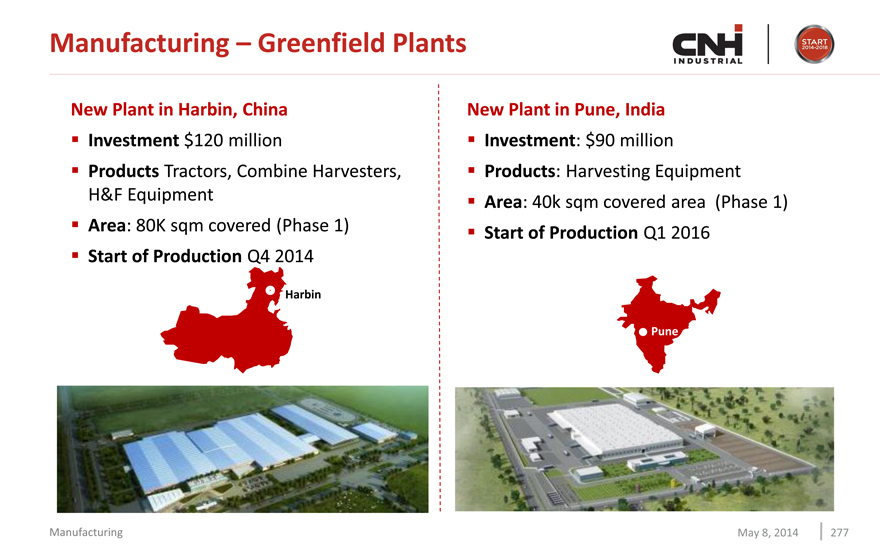

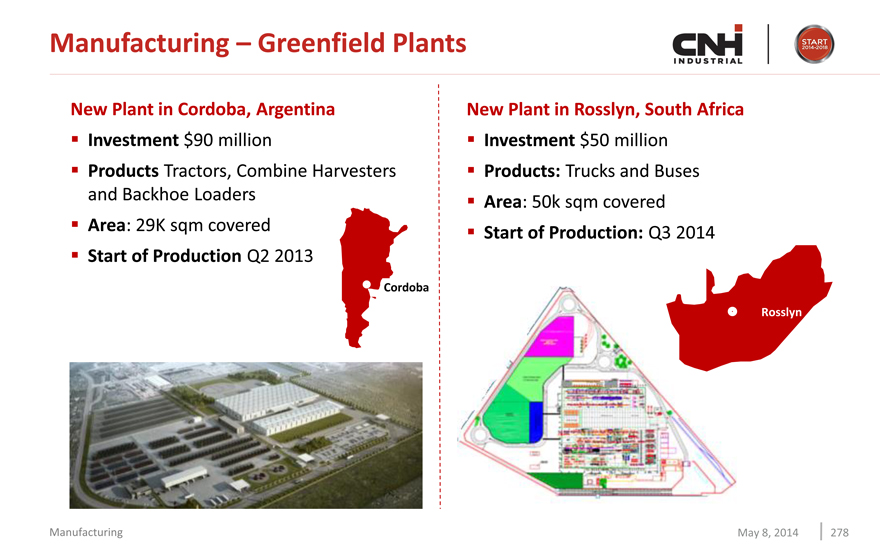

Manufacturing Footprint

CNH Industrial Construction Equipment

Fargo, ND

NAFTA Wheel loaders EMEA Berlin

Graders APAC

Calhoun, GA

Crawler excavators,

dozers

Burlington, IA

Tractor loader

Tracy

backhoes, tractor

Components

loaders, forklifts

Wichita, KS San Mauro AME

Crawler excavators, mini APAC NAFTA

Skid-steer, compact AME

excavators, wheel

track loaders excavators APAC

Queretaro (JV)

Pithampur

Components

Lecce Tractor loader

Tractor loader backhoes,

Belo Horizonte

backhoes, compactors

Crawler excavators, tractor

telehandlers, Chiba (Sumitomo OEM)

loader backhoes, dozers,

wheel loaders Crawler excavators

graders, wheel loaders

LATAM

Main Sourcing

Flow

Construction Equipment May 8, 2014 57

|

|

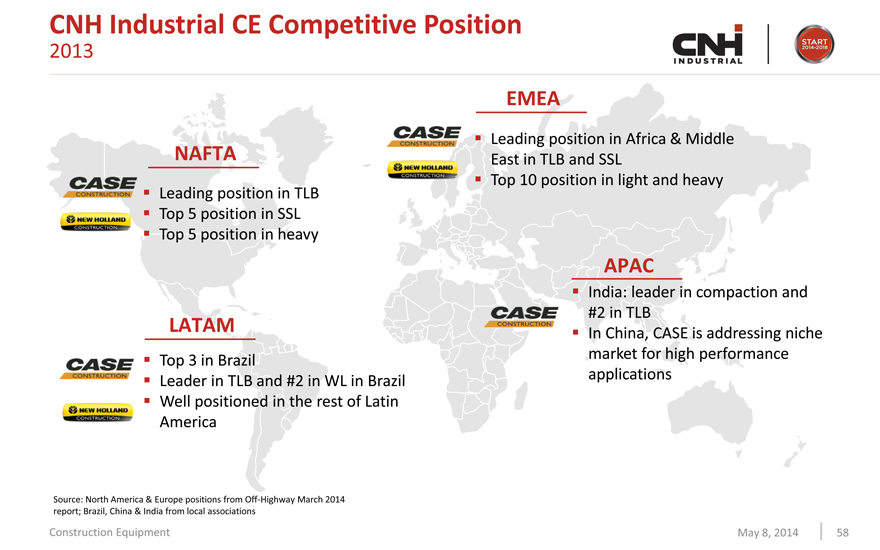

CNH Industrial CE Competitive Position

2013

EMEA

Leading position in Africa & Middle

NAFTA East in TLB and SSL

Top 10 position in light and heavy

Leading position in TLB

Top 5 position in SSL

Top 5 position in heavy

APAC

India: leader in compaction and

#2 in TLB

LATAM In China, CASE is addressing niche

Top 3 in Brazil market for high performance

Leader in TLB and #2 in WL in Brazil applications

Well positioned in the rest of Latin

America

Source: North America & Europe positions from Off-Highway March 2014 report; Brazil, China & India from local associations

Construction Equipment May 8, 2014 58

|

|

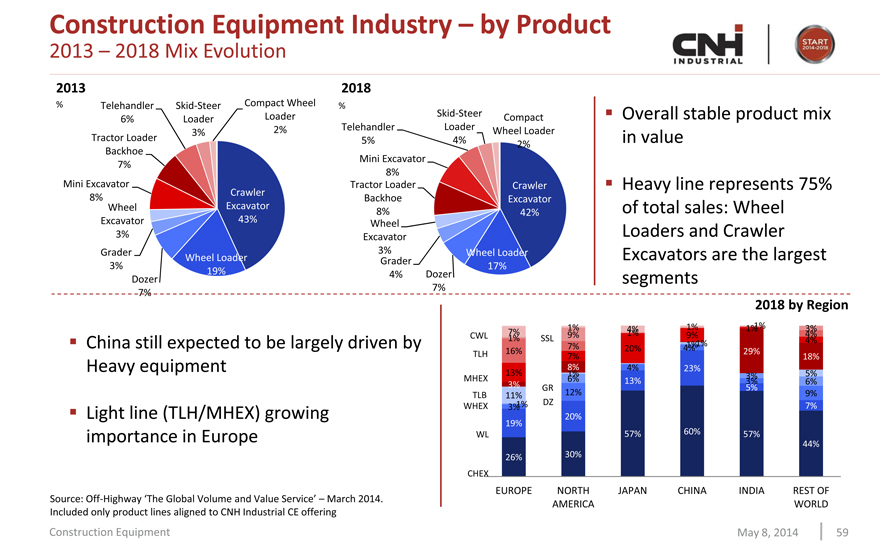

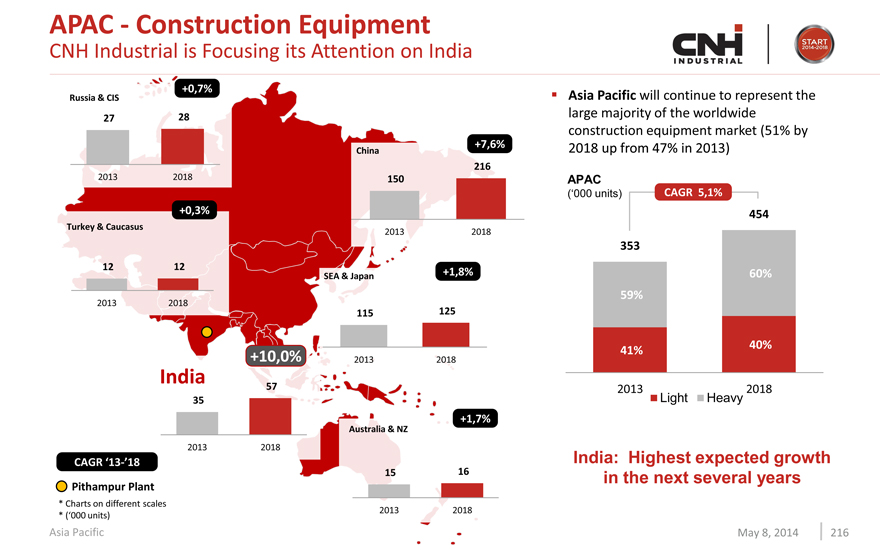

Construction Equipment Industry – by Product

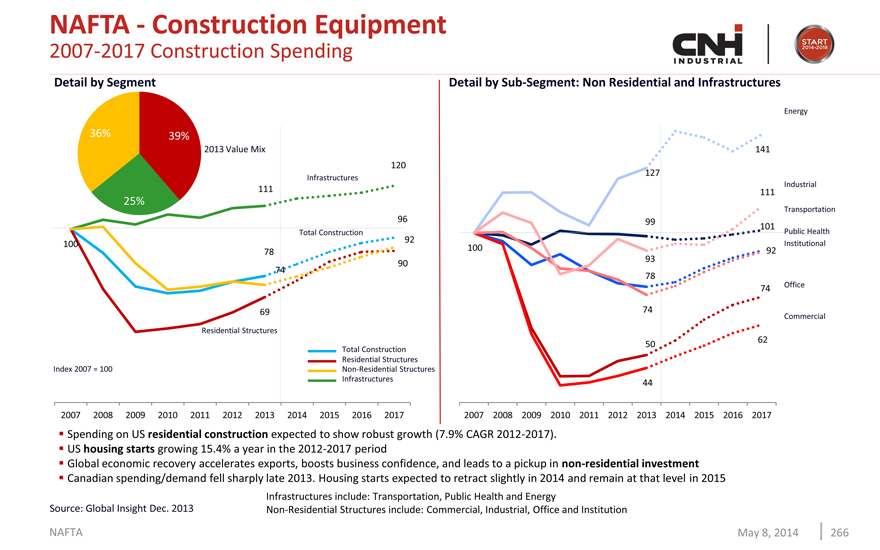

2013 – 2018 Mix Evolution

2013 2018

% Skid-Steer Compact Wheel % Telehandler

Loader Skid-Steer Compact Overall stable product mix

6% Loader

2% Telehandler Loader Wheel Loader 3%

Tractor Loader 5% 4% in value Backhoe 2%

7% Mini Excavator 8%

Mini Excavator Crawler Tractor Loader Crawler Heavy line represents 75%

8% Excavator Backhoe Excavator

8% 42% of total sales: Wheel

Wheel 43%

Wheel

Excavator Loaders and Crawler

Grader Excavator 3%

3% 3% Wheel Loader Excavators are the largest

Wheel Loader Grader 17%

Dozer 19% 4% Dozer segments 7% 7%

China still expected to be largely driven by Heavy equipment

Light line (TLH/MHEX) growing importance in Europe

1% 4% 1% 1% 1% 3% CWL 7% 9% 1% 9% 4%

1% SSL 4%

7% 1% 1%

16% 20% 4% 29%

TLH 7% 18%

8% 4% 23%

13% 1% 3% 5% MHEX 6% 13% 3% 6%

3% GR 12% 5%

TLB 11% 9%

1% DZ 7% WHEX 3% 19% 20% WL 57% 60% 57% 44% 26% 30% CHEX

EUROPE NORTH JAPAN CHINA INDIA REST OF AMERICA WORLD

2018 by Region

Construction Equipment May 8, 2014 59

|

|

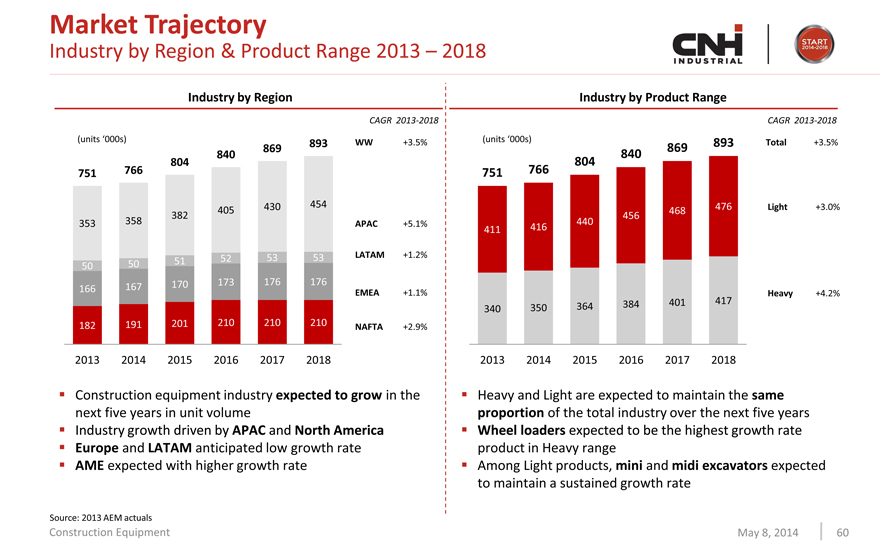

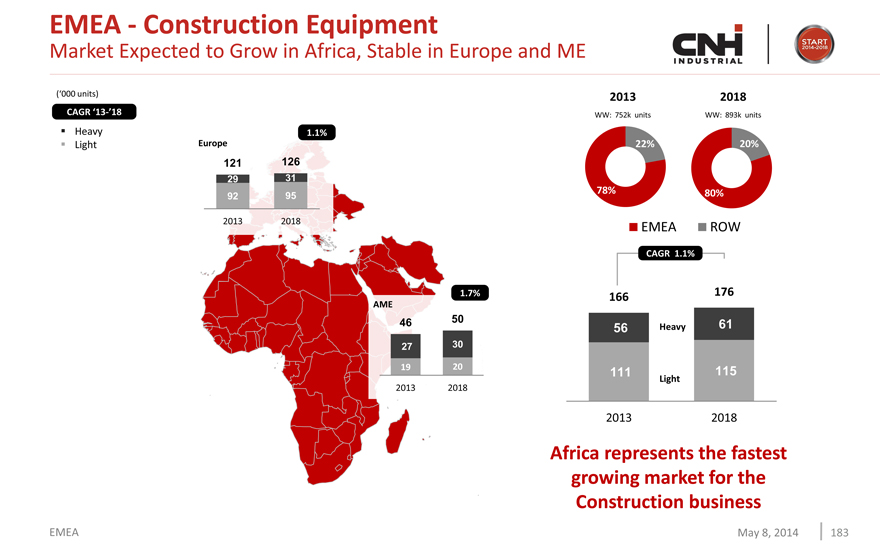

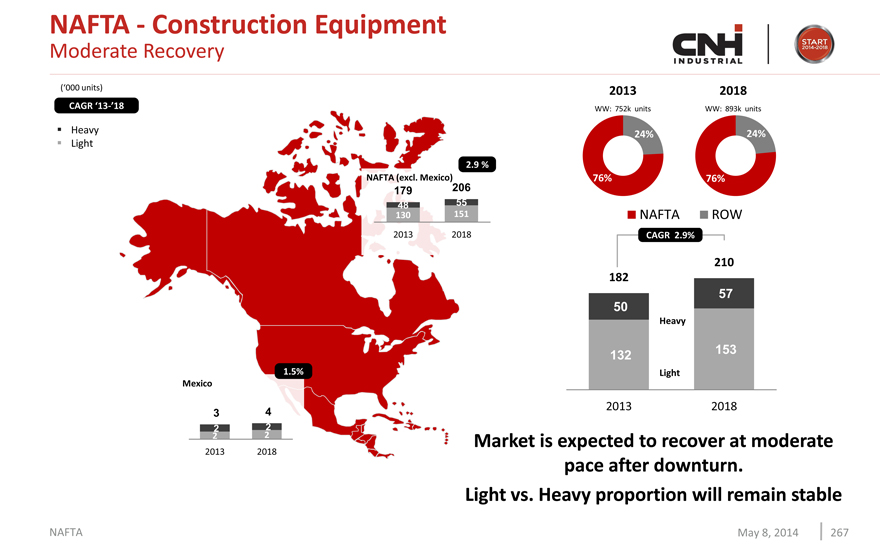

Market Trajectory

Industry by Region & Product Range 2013 – 2018

Industry by Region Industry by Product Range

CAGR 2013-2018 CAGR 2013-2018

(units ‘000s) 893 WW +3.5% (units ‘000s) 869 893 Total +3.5%

869

840 840 804 804 751 766 751 766

430 454 476 Light +3.0% 405 468 382 456 353 358 APAC +5.1% 440 411 416

52 53 53 LATAM +1.2%

50 51 50

170 173 176 176 166 167

EMEA +1.1% 417 Heavy +4.2%

364 384 401 340 350 182 191 201 210 210 210

NAFTA +2.9%

2013 2014 2015 2016 2017 2018 2013 2014 2015 2016 2017 2018

Construction equipment industry expected to grow in the next five years in unit volume

Industry growth driven by APAC and North America

Europe and LATAM anticipated low growth rate AME expected with higher growth rate

Heavy and Light are expected to maintain the same proportion of the total industry over the next five years

Wheel loaders expected to be the highest growth rate product in Heavy range Among Light products, mini and midi excavators expected to maintain a sustained growth rate

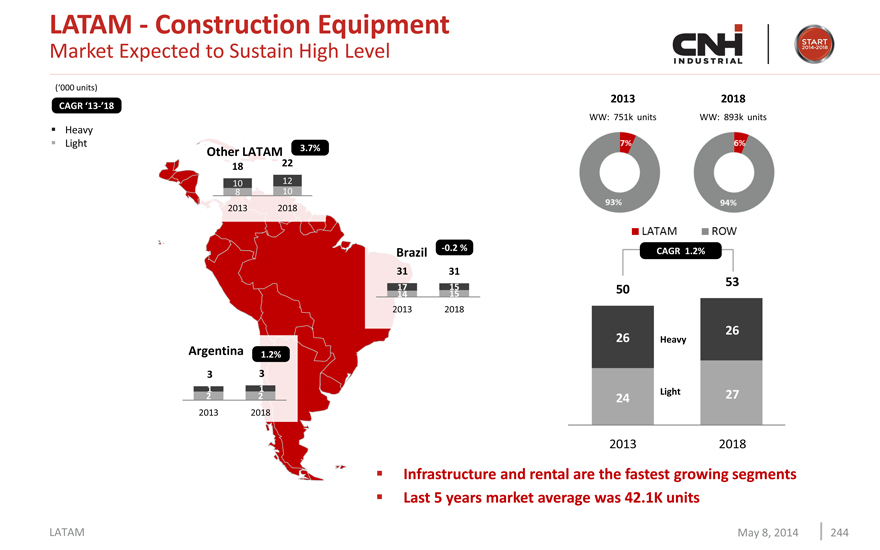

Source: 2013 AEM actuals

Construction Equipment

May 8, 2014 60

|

|

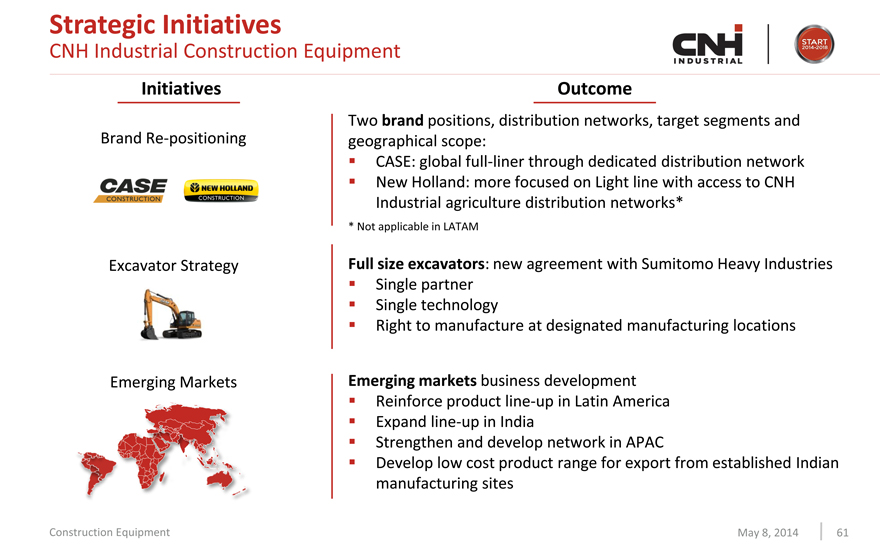

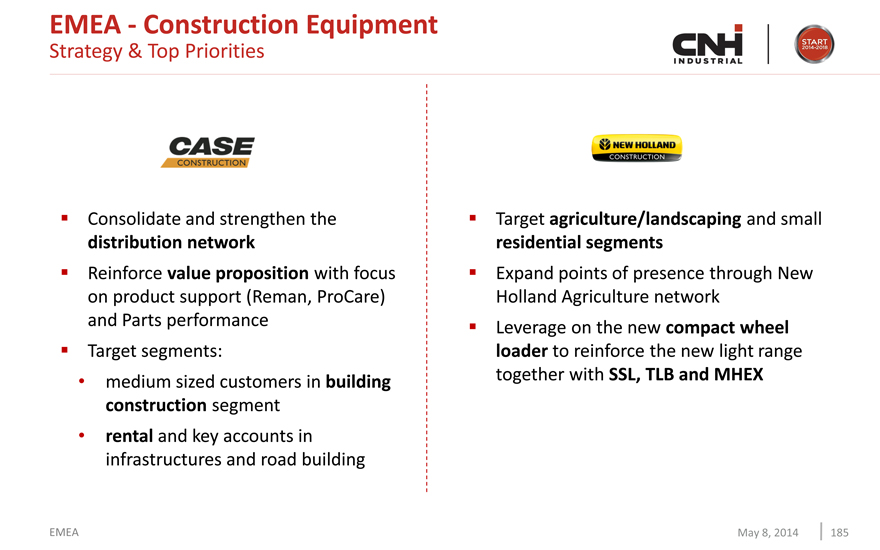

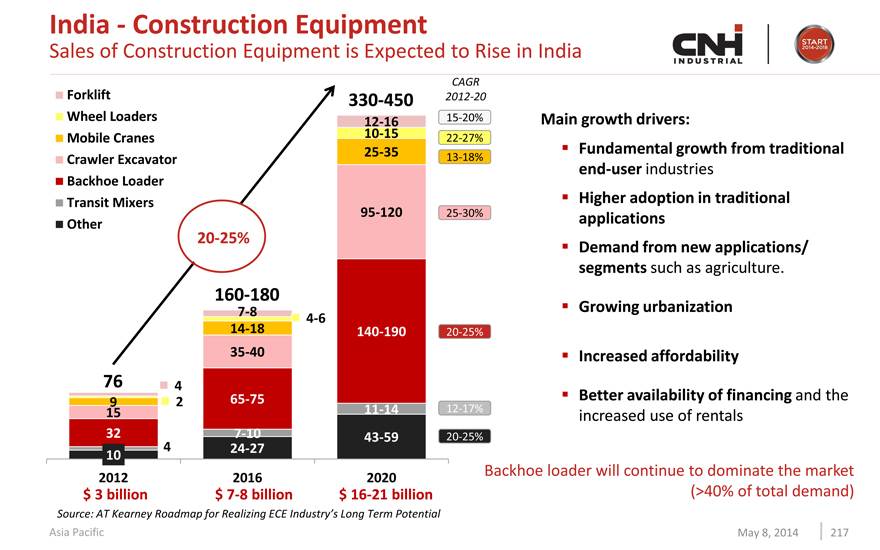

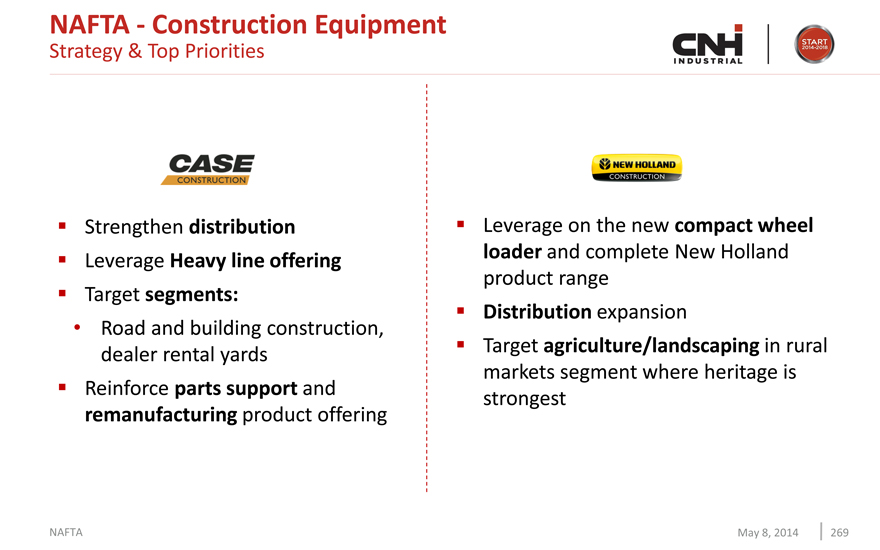

Strategic Initiatives

CNH Industrial Construction Equipment

Initiatives

Brand Re-positioning Excavator Strategy Emerging Markets

Outcome

Two brand positions, distribution networks, target segments and geographical scope:

* Not applicable in LATAM

Full size excavators: new agreement with Sumitomo Heavy Industries

Single partner Single technology

Right to manufacture at designated manufacturing locations

Emerging markets business development

Reinforce product line-up in Latin America Expand line-up in India Strengthen and develop network in APAC

Develop low cost product range for export from established Indian manufacturing sites

Construction Equipment

May 8, 2014 61

|

|

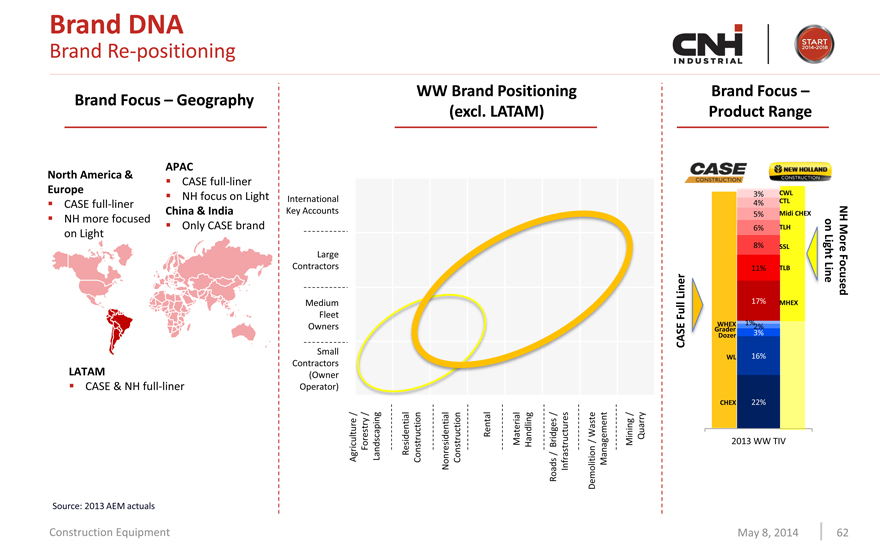

Brand DNA

Brand Re-positioning

WW Brand Positioning Brand Focus – Brand Focus – Geography (excl. LATAM) Product Range

APAC North America &

CASE full-liner

Europe

NH focus on Light CASE full-liner

China & India

NH more focused

Only CASE brand on Light

LATAM

CASE & NH full-liner

ContractorsKey Operator) (Owner Small OwnersFleetMediumContractorsLargeAccountsInternational Agriculture / Forestry / Landscaping

Residential Construction

Nonresidential Construction

Rental

Material Handling

Roads / Bridges / Infrastructures

Demolition / Waste Management

Mining / Quarry

3% CWL

4% CTL

5% Midi CHEX NH

6% TLH on

8% SSL More Light 11% TLB Line Focused Liner

17% MHEX

Full

WHEX 1%

Grader 3% 2%

CASE Dozer

WL 16%

CHEX 22%

2013 WW TIV

Source: 2013 AEM actuals

Construction Equipment

May 8, 2014 62

|

|

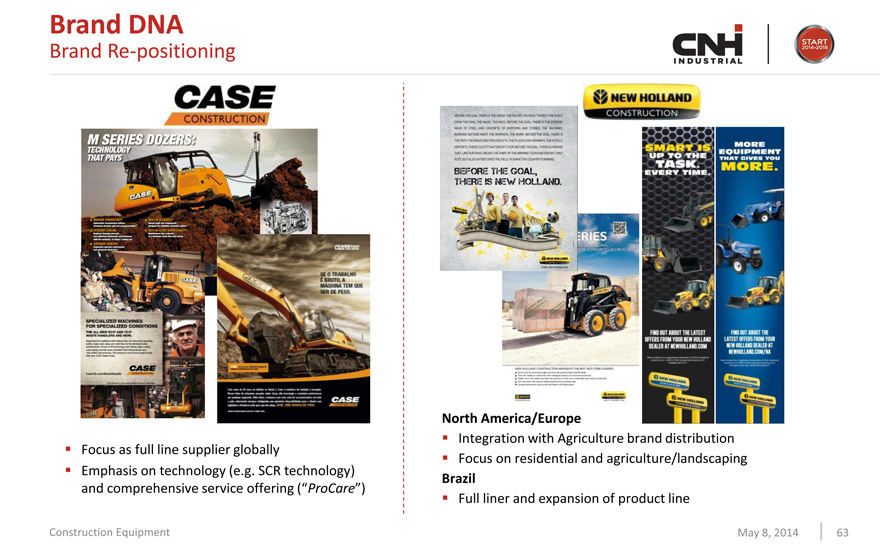

Brand DNA

Brand Re-positioning

Focus as full line supplier globally

Emphasis on technology (e.g. SCR technology) and comprehensive service offering (“ProCare”)

Construction Equipment

North America/Europe

Integration with Agriculture brand distribution Focus on residential and agriculture/landscaping

Brazil

Full liner and expansion of product line

May 8, 2014 63

|

|

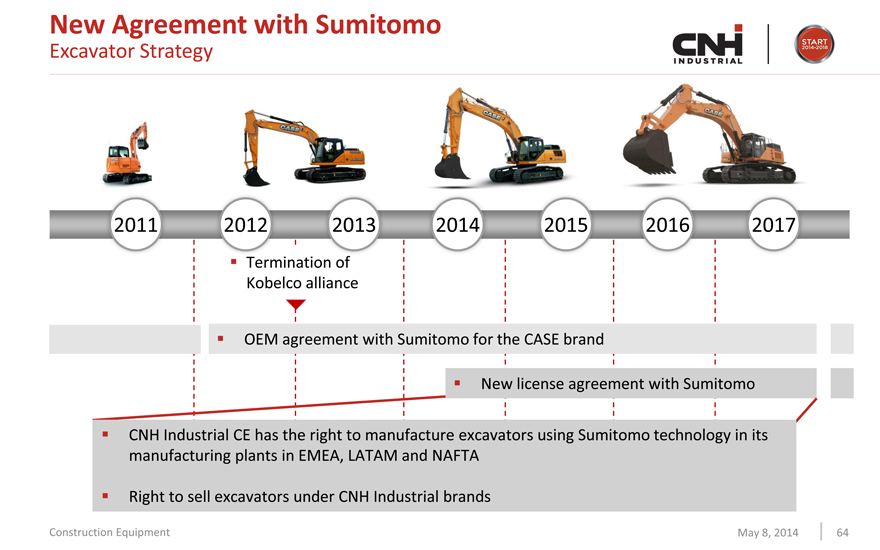

New Agreement with Sumitomo

Excavator Strategy

2011 2012 2013 2014 2015 2016 2017

Termination of Kobelco alliance

OEM agreement with Sumitomo for the CASE brand

New license agreement with Sumitomo

CNH Industrial CE has the right to manufacture excavators using Sumitomo technology in its manufacturing plants in EMEA, LATAM and NAFTA

Right to sell excavators under CNH Industrial brands

Construction Equipment

May 8, 2014 64

|

|

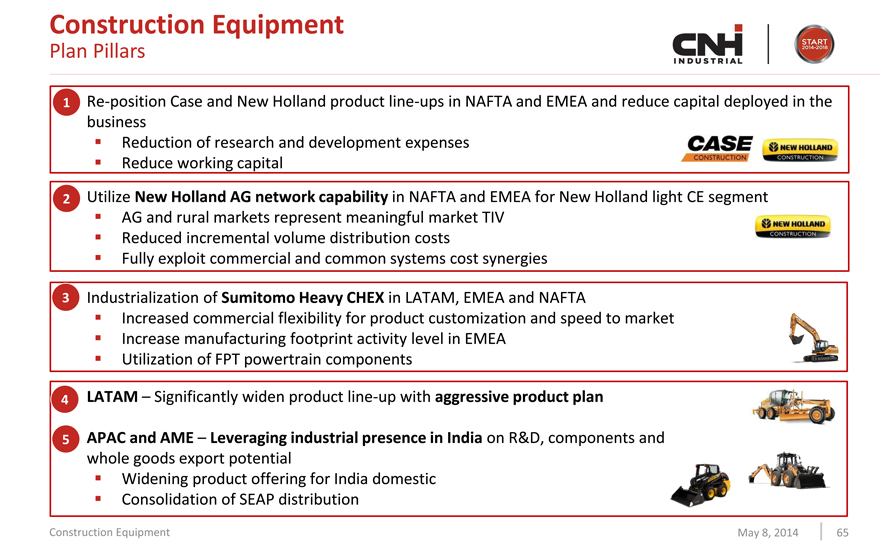

Construction Equipment

Plan Pillars

1 Re-position Case and New Holland product line-ups in NAFTA and EMEA and reduce capital deployed in the

business

Reduction of research and development expenses

Reduce working capital

2 Utilize New Holland AG network capability in NAFTA and EMEA for New Holland light CE segment

AG and rural markets represent meaningful market TIV

Reduced incremental volume distribution costs

Fully exploit commercial and common systems cost synergies

3 Industrialization of Sumitomo Heavy CHEX in LATAM, EMEA and NAFTA

Increased commercial flexibility for product customization and speed to market

Increase manufacturing footprint activity level in EMEA

Utilization of FPT powertrain components

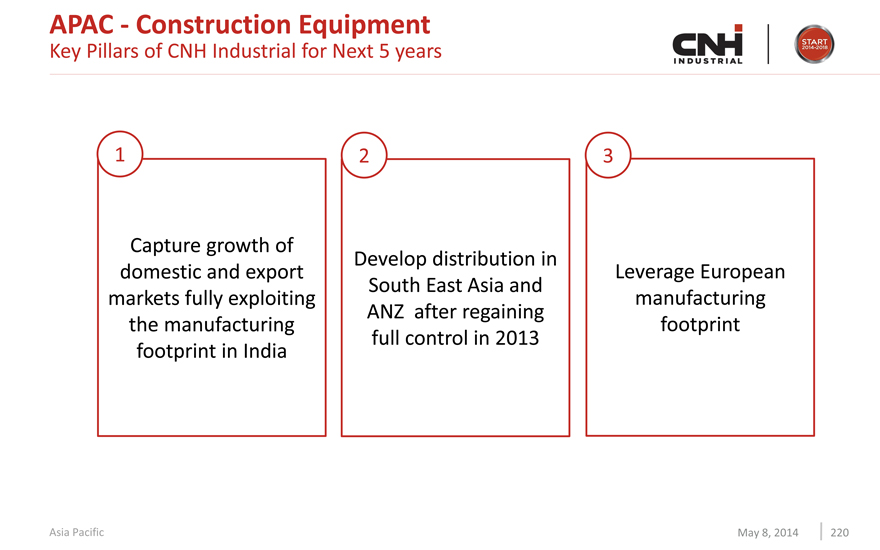

4 LATAM – Significantly widen product line-up with aggressive product plan

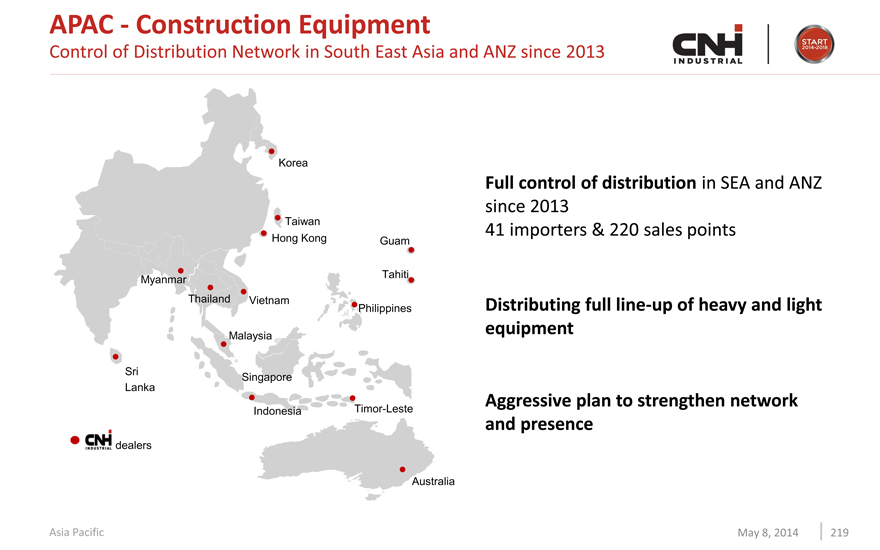

5 APAC and AME – Leveraging industrial presence in India on R&D, components and

whole goods export potential

Widening product offering for India domestic

Consolidation of SEAP distribution

Construction Equipment

May 8, 2014 65

|

|

Investor day auburn hills may 8th, 2014

IVECO

Lorenzo Sistino

|

|

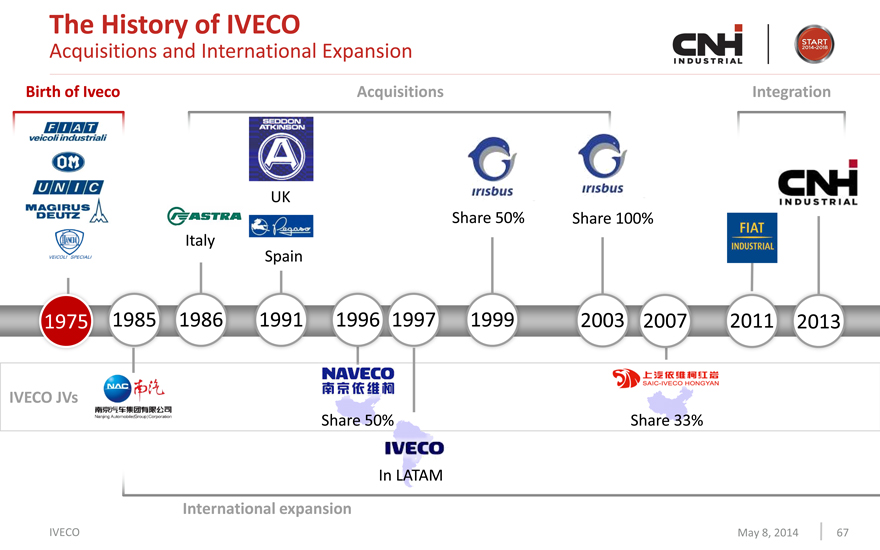

The History of IVECO

Acquisitions and International Expansion

Birth of Iveco Acquisitions Integration

UK

Share 50% Share 100% Italy Spain

1975 1985 1986 1991 1996 1997 1999 2003 2007 2011 2013

Share 50% Share 33%

In LATAM

International expansion

Iveco May 8, 2014 67

|

|

IVECO

Brand Statement

IVECO

Equipped with best in class powertrain technologies, Iveco

offers the widest commercial vehicle line up across a large

distribution network.

IVECO

May 8, 2014 68

|

|

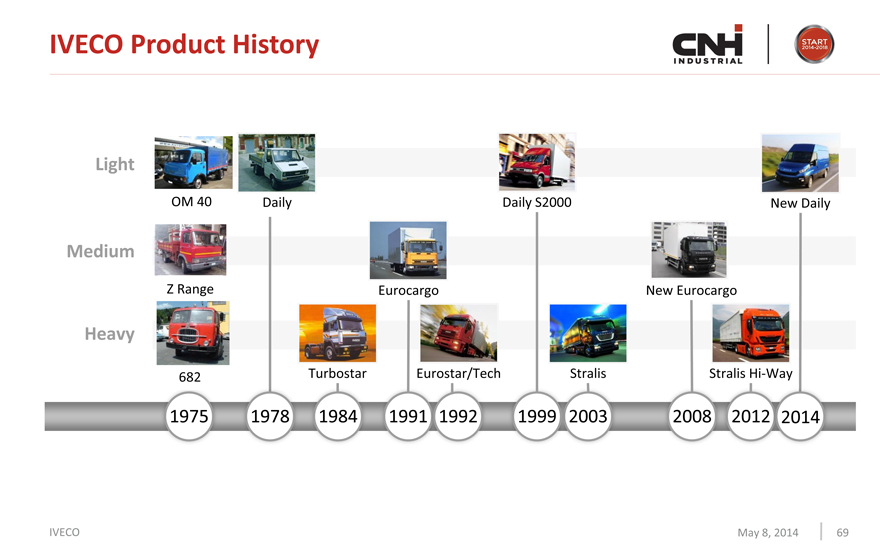

IVECO Product History

Light

OM 40 Daily Daily S2000 New Daily

Medium

Z Range Eurocargo New Eurocargo

Heavy

682 Turbostar Eurostar/Tech Stralis Stralis Hi-Way

1975 1978 1984 1991 1992 1999 2003 2008 2012 2014

IVECO

May 8, 2014 69

|

|

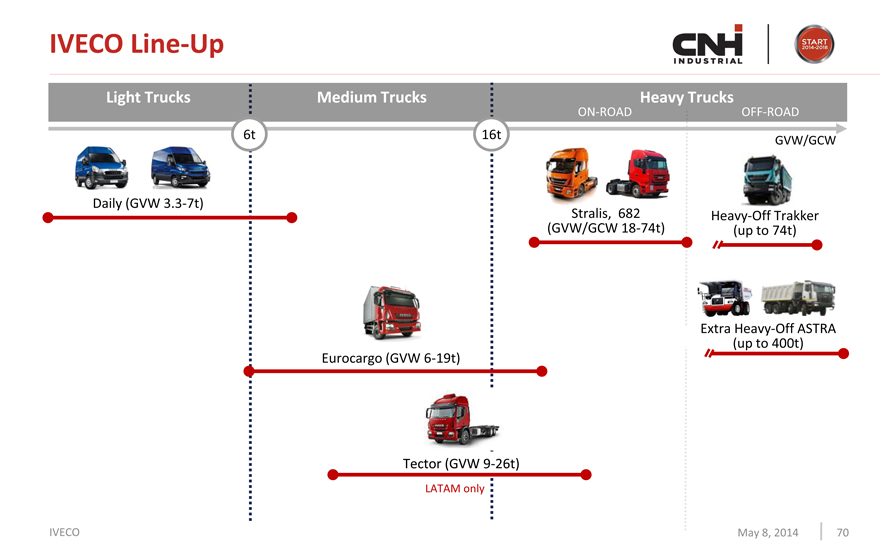

IVECO Line-Up

Light Trucks Medium Trucks Heavy Trucks

ON-ROAD OFF-ROAD

6t 16t

GVW/GCW

Daily (GVW 3.3-7t)

Stralis, 682 Heavy-Off Trakker (GVW/GCW 18-74t) (up to 74t)

Eurocargo (GVW 6-19t)

Extra Heavy-Off ASTRA (up to 400t)

Tector (GVW 9-26t)

LATAM only

IVECO

May 8, 2014 70

|

|

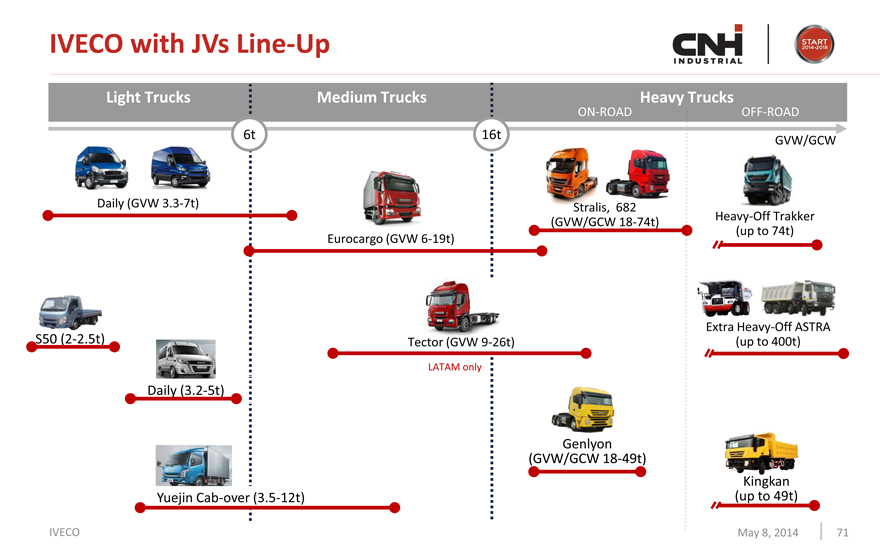

IVECO with JVs Line-Up

Light Trucks Medium Trucks Heavy Trucks

ON-ROAD OFF-ROAD

6t 16t

GVW/GCW

Daily (GVW 3.3-7t) Stralis, 682

Eurocargo (GVW 6-19t)

Stralis, 682 (GVW/GCW 18-74t)

Heavy-Off Trakker (up to 74t)

S50 (2-2.5t)

Tector (GVW 9-26t)

Extra Heavy-Off ASTRA (up to 400t)

LATAM only

Daily (3.2-5t)

Yuejin Cab-over (3.5-12t)

Kingkan (up to 49t)

Genlyon

(GVW/GCW 18-49t) IVECO

May 8, 2014 71

|

|

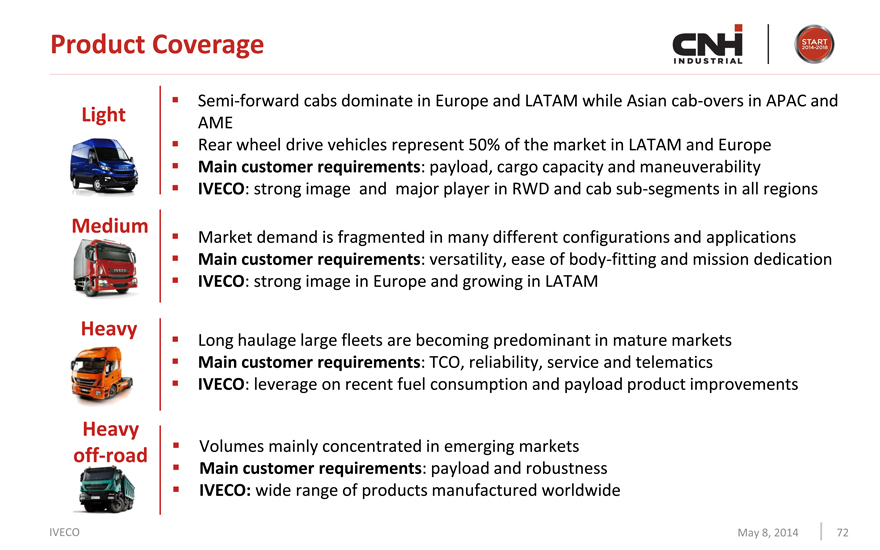

Product Coverage

Semi-forward cabs dominate in Europe and LATAM while Asian cab-overs in APAC and AME

Rear wheel drive vehicles represent 50% of the market in LATAM and Europe Main customer requirements: payload, cargo capacity and maneuverability IVECO: strong image and major player in RWD and cab sub-segments in all regions

Market demand is fragmented in many different configurations and applications Main customer requirements: versatility, ease of body-fitting and mission dedication IVECO: strong image in Europe and growing in LATAM

Long haulage large fleets are becoming predominant in mature markets Main customer requirements: TCO, reliability, service and telematics IVECO: leverage on recent fuel consumption and payload product improvements

Volumes mainly concentrated in emerging markets

Main customer requirements: payload and robustness

IVECO: wide range of products manufactured worldwide

Light

Medium

Heavy

Heavy

off-road

IVECO

May 8, 2014 72

|

|

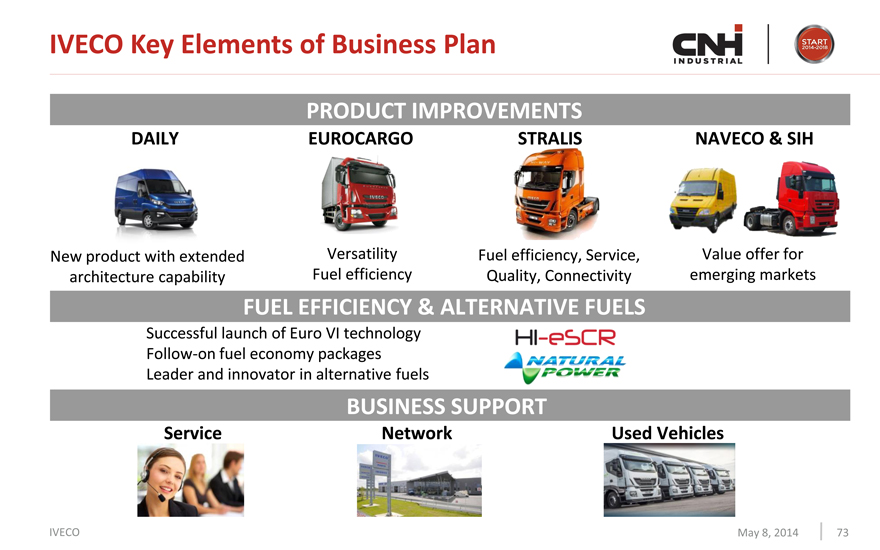

IVECO Key Elements of Business Plan

PRODUCT IMPROVEMENTS

DAILY EUROCARGO STRALIS NAVECO & SIH

New product with extended Versatility Fuel efficiency, Service, Value offer for

architecture capability Fuel efficiency Quality, Connectivity emerging markets

FUEL EFFICIENCY & ALTERNATIVE FUELS

Successful launch of Euro VI technology Follow-on fuel economy packages Leader and innovator in alternative fuels

BUSINESS SUPPORT

Service Network Used Vehicles

IVECO

May 8, 2014 73

|

|

IVECO Light Trucks

IVECO

May 8, 2014 74

|

|

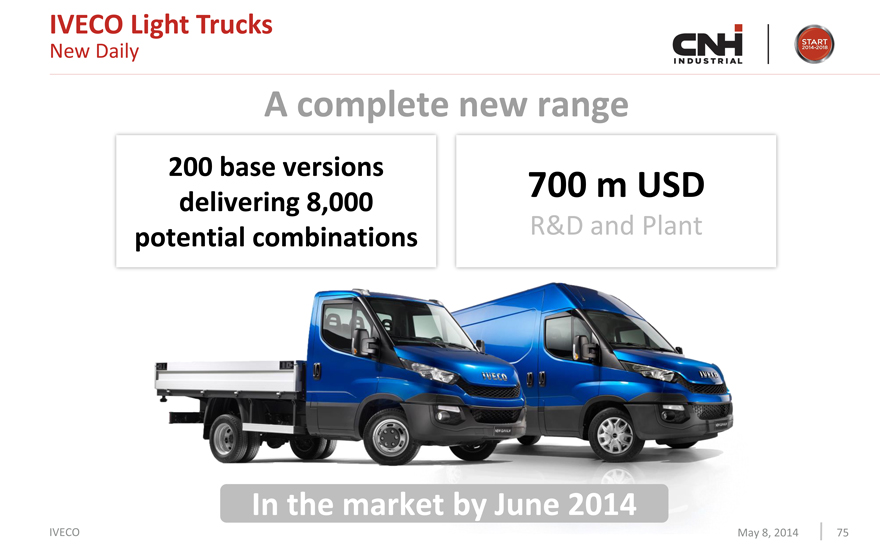

IVECO Light Trucks

New Daily

A complete new range

200 base versions

700 m USD

delivering 8,000

R&D and Plant potential combinations

In the market by June 2014

IVECO

May 8, 2014 75

|

|

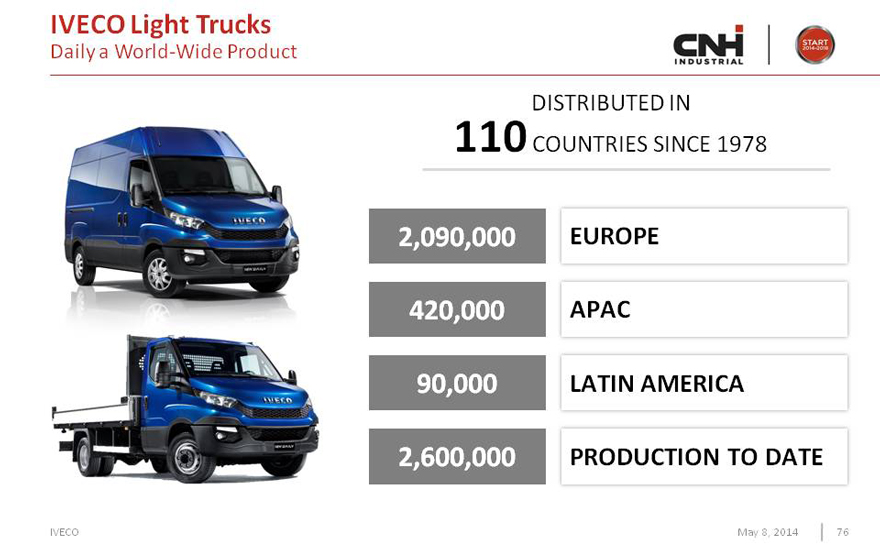

IVECO Light Trucks

Daily a World-Wide Product

DISTRIBUTED IN 110 COUNTRIES SINCE 1978

2,090,000 EUROPE

420,000 APAC

90,000 LATIN AMERICA

2,600,000 PRODUCTION TO DATE

IVECO

May 8, 2014 76

|

|

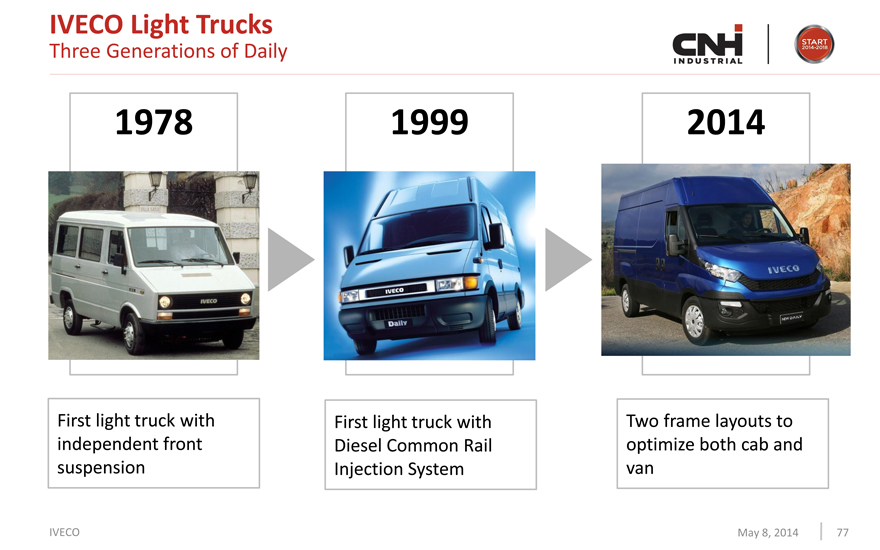

IVECO Light Trucks

Three Generations of Daily

1978 1999 2014

First light truck with First light truck with Two frame layouts to independent front Diesel Common Rail optimize both cab and suspension Injection System van

IVECO

May 8, 2014 77

|

|

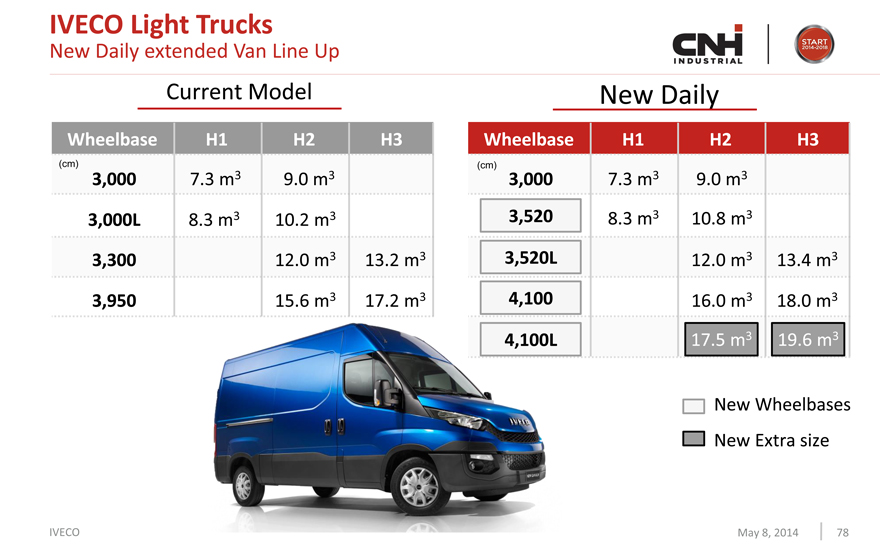

IVECO Light Trucks

New Daily extended Van Line Up

Current Model New Daily

Wheelbase H1 H2 H3 Wheelbase H1 H2 H3

(cm) (cm)

3,000 7.3 m3 9.0 m3 3,000 7.3 m3 9.0 m3

3,000L 8.3 m3 10.2 m3 3,520 8.3 m3 10.8 m3

3,300 12.0 m3 13.2 m3 3,520L 12.0 m3 13.4 m3

3,950 15.6 m3 17.2 m3 4,100 16.0 m3 18.0 m3

4,100L 17.5 m3 19.6 m3

New Wheelbases

New Extra size

IVECO

May 8, 2014 78

|

|

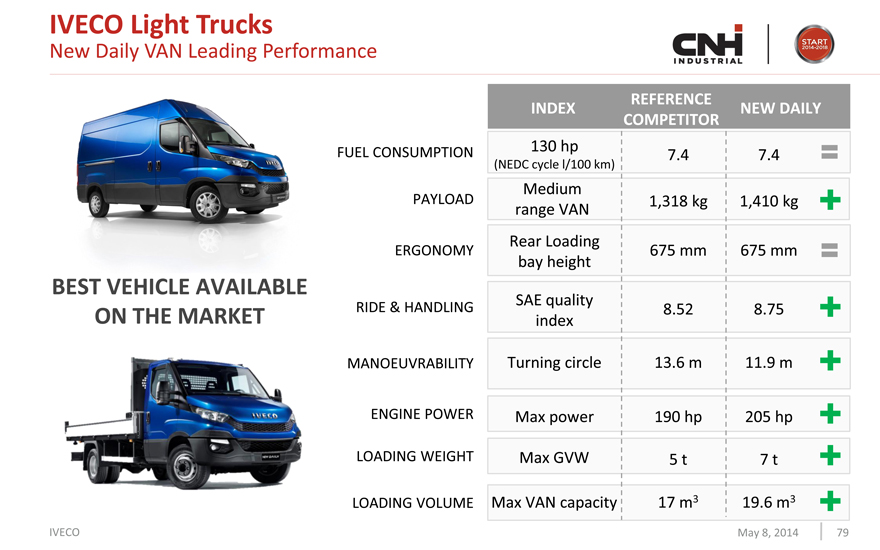

IVECO Light Trucks

New Daily VAN Leading Performance

REFERENCE

INDEX NEW DAILY

COMPETITOR

130 hp

FUEL CONSUMPTION 7.4 7.4

(NEDC cycle l/100 km)

Medium

PAYLOAD 1,318 kg 1,410 kg

range VAN

Rear Loading

ERGONOMY 675 mm 675 mm

bay height

SAE quality

RIDE & HANDLING 8.52 8.75

index

MANOEUVRABILITY Turning circle 13.6 m 11.9 m

ENGINE POWER Max power 190 hp 205 hp

LOADING WEIGHT Max GVW 5 t 7 t

LOADING VOLUME Max VAN capacity 17 m3 19.6 m3

BEST VEHICLE AVAILABLE ON THE MARKET

IVECO

May 8, 2014 79

|

|

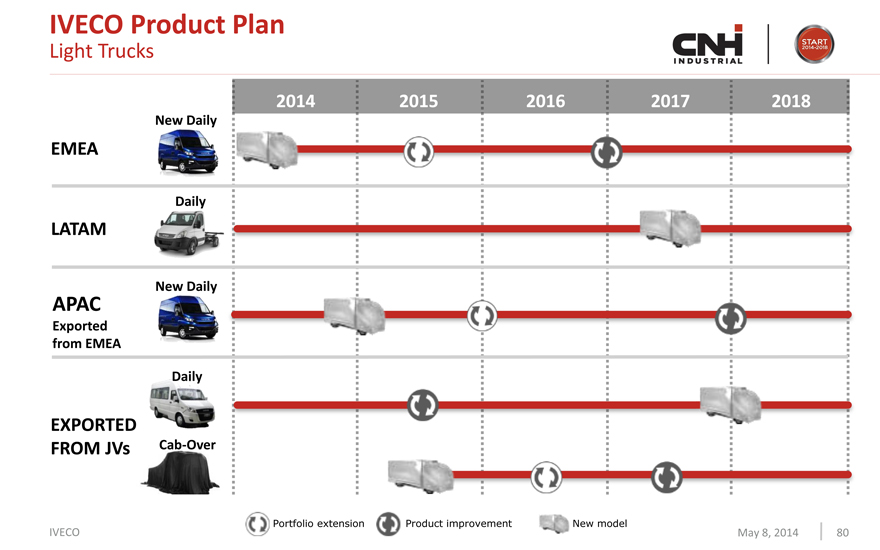

IVECO Product Plan

Light Trucks

2014 2015 2016 2017 2018

New Daily

EMEA

Daily

LATAM

New Daily

APAC

Exported

from EMEA

Daily

EXPORTED

FROM JVs Cab-Over

Portfolio extension Product improvement New model

IVECO May 8, 2014 80

|

|

IVECO Light Trucks

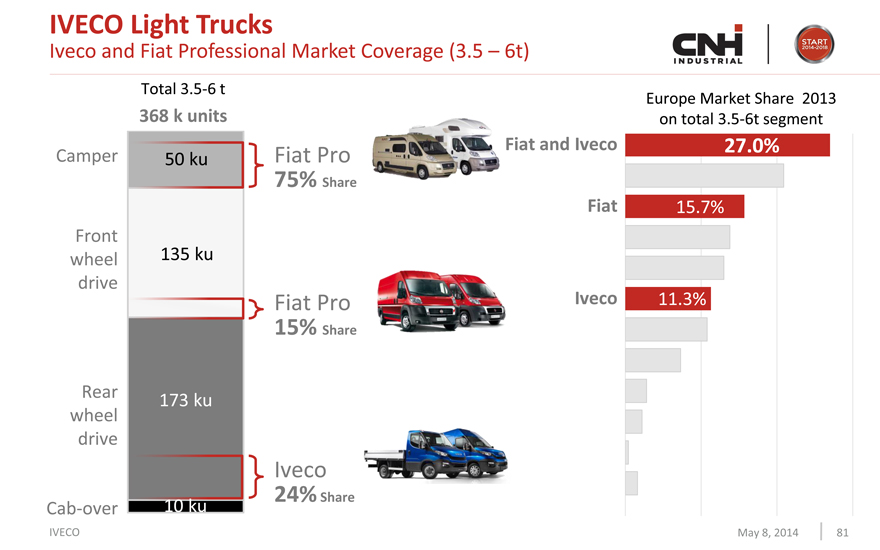

Iveco and Fiat Professional Market Coverage (3.5 – 6t)

Total 3.5-6 t Europe Market Share 2013

368 k units on total 3.5-6t segment

Camper 50 ku Fiat Pro Fiat and Iveco 27.0%

75% Share

Fiat 15.7%

Front

wheel 135 ku

drive

Fiat Pro Iveco 11.3%

15% Share

Rear 173 ku

wheel

drive

Iveco

Cab-over 10 ku 24% Share

IVECO May 8, 2014 81

|

|

IVECO Medium Trucks

IVECO

May 8, 2014 82

|

|

IVECO Medium Trucks

Key Attributes

Extended portfolio up to 26 ton GVW

11,000 Product configurations

Best payload Easy body-fitting

Co-leader in Europe

Produced in Europe & LATAM, distributed worldwide

IVECO

May 8, 2014 83

|

|

IVECO Medium Trucks

Product Technical Highlights

2 ENGINE TYPE Tector 5 (4 cyl.) and Tector 7 (6 cyl.) from 160 to 320 hp

2 HEIGHTS standard or high roof

8 DRIVER CABINS day, sleeper, crew cab

13 TRANSMISSIONS 6 manual, 4 automated, 3 fully automatic

14 GVW VARIANTS from 6 to 26 t

15 WHEELBASE from 2,790 to 6,570 mm

DRIVE 4x2, 4x4 (6x2, 6x4 LATAM only)

IVECO

May 8, 2014 84

|

|

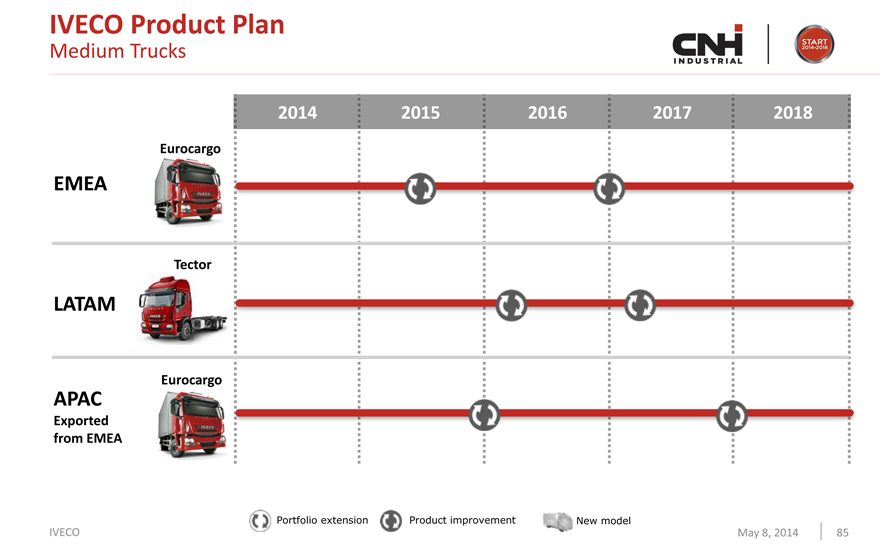

IVECO Product Plan

Medium Trucks

2014 2015 2016 2017 2018

Eurocargo

EMEA

Tector

LATAM

Eurocargo

APAC

Exported from EMEA Portfolio extension Product improvement New model

May 8, 2014 85

IVECO

|

|

IVECO Heavy Trucks

May 8, 2014 86

IVECO

|

|

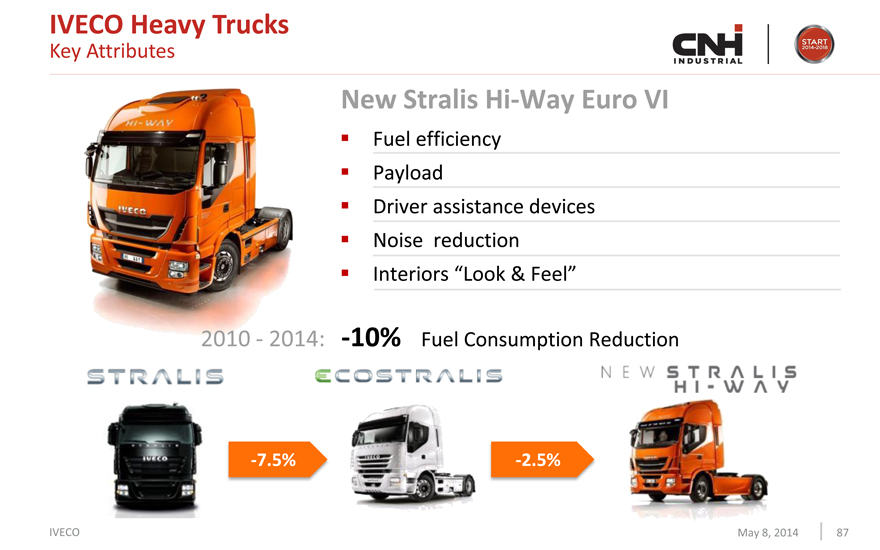

IVECO Heavy Trucks

Key Attributes

New Stralis Hi-Way Euro VI

Fuel efficiency Payload

Driver assistance devices

Noise reduction

Interiors “Look & Feel”

2010—2014: -10% Fuel Consumption Reduction

-7.5%

-2.5%

IVECO

May 8, 2014 87

|

|

IVECO Heavy Trucks

Hi-eSCR after Treatment Solution

COMPETITORS CHOICE CHOICE

NOX & PM REDUCTION EFFICIENCY

SELECTIVE

EXHAUST GAS

CATALYST

REDUCTION RECIRCULATION

NOX & PM REDUCTION EFFICIENCY

Lower fuel consumption Better payload Lower maintenance

IVECO

May 8, 2014 88

|

|

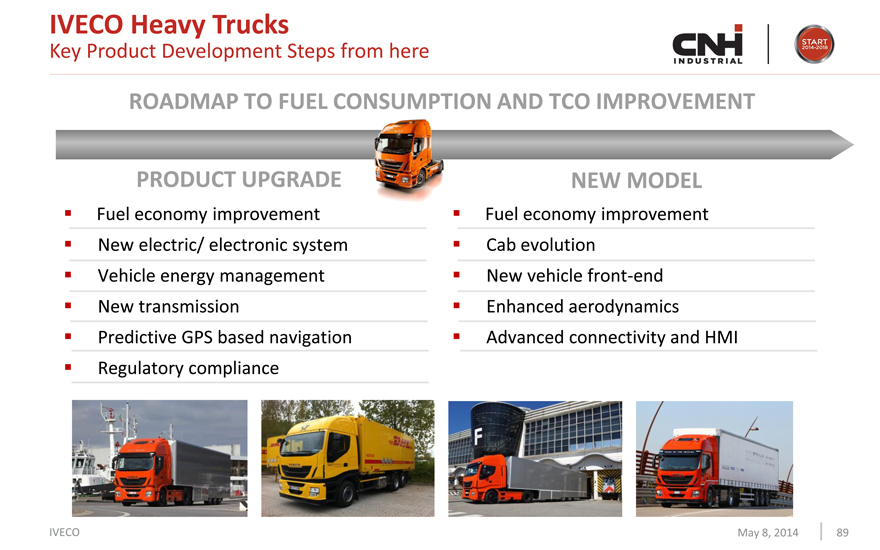

IVECO Heavy Trucks

Key Product Development Steps from here

ROADMAP TO FUEL CONSUMPTION AND TCO IMPROVEMENT

PRODUCT UPGRADE NEW MODEL

Fuel economy improvement New electric/ electronic system Vehicle energy management New transmission Predictive GPS based navigation Regulatory compliance

Fuel economy improvement Cab evolution New vehicle front-end Enhanced aerodynamics Advanced connectivity and HMI

IVECO

May 8, 2014 89

|

|

IVECO Heavy OFF

Key Attributes

Wide product offering Robustness Performance Body-fitting adaptability

Produced and distributed worldwide

IVECO

May 8, 2014 90

|

|

IVECO ASTRA: Extra Heavy OFF

Key Attributes

Built for extreme off-road missions Basic, durable & robust Overloading capabilities All-wheel drive up to 8x8 Multiple axles and transmissions availability Extra wide-load up to 400t GCW

IVECO

May 8, 2014 91

|

|

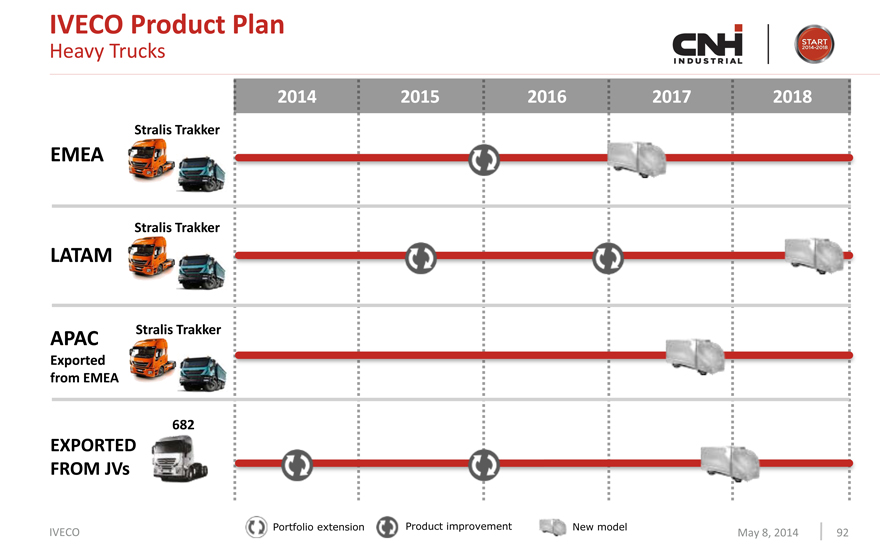

IVECO Product Plan

Heavy Trucks

2014 2015 2016 2017 2018

Stralis Trakker

EMEA

Stralis Trakker

LATAM

APAC Stralis Trakker

Exported

from EMEA

682

EXPORTED

FROM JVs

Portfolio extension Product improvement New model

IVECO May 8, 2014 92

|

|

IVECO Service

Striving for Excellence

Leverage on current IVECO strengths…

Service

Assistance Parts Network Non Stop 24/7 availability capillarity

Calls answered in 20 seconds

The largest assistance network in Europe

Leverage on Group synergies

…to improve in After Sales & Service

IVECO May 8, 2014 93

|

|

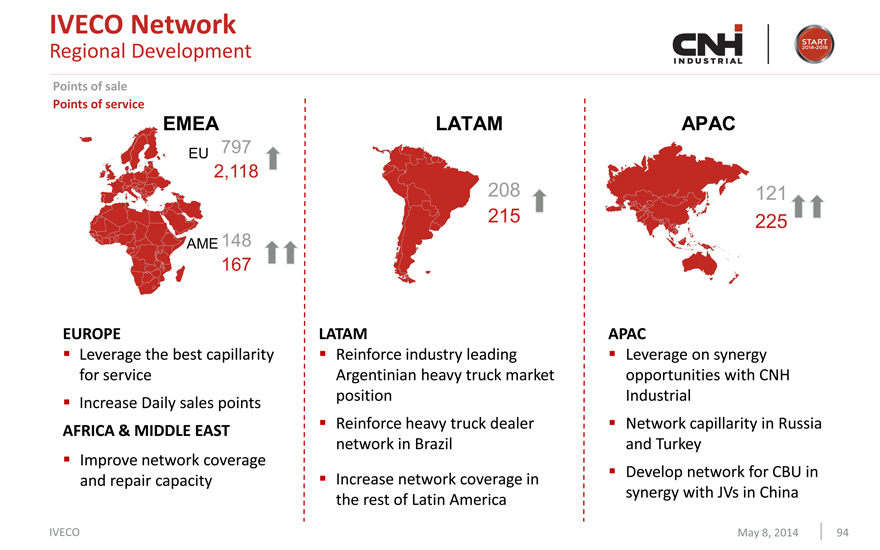

IVECO Network

Regional Development

Points of sale

Points of service

EMEA LATAM APAC

EU 797

2,118

208 121

215 225

AME 148

167

EUROPE LATAM APAC

Leverage the best capillarity Reinforce industry leading Leverage on synergy

for service Argentinian heavy truck market opportunities with CNH

Increase Daily sales points position Industrial

AFRICA & MIDDLE EAST Reinforce heavy truck dealer Network capillarity in Russia

network in Brazil and Turkey

Improve network coverage

and repair capacity Increase network coverage in Develop network for CBU in

the rest of Latin America synergy with JVs in China

IVECO May 8, 2014 94

|

|

IVECO Action Plan

Regional Roadmap

EMEA LATAM APAC

EUROPE BRAZIL APAC

Target Northern and Central EU Improve presence in large fleets Increase penetration in off-road

Markets leveraging Group synergies premium segments mainly in South

Focus on service, TCO, and residual ARGENTINA East Asia

value to increase presence in fleets Leverage on local manufacturing Develop new business

Improve residual value and used presence opportunities through local

vehicle business partnerships

REST OF LATIN AMERICA

AFRICA & MIDDLE EAST Leverage JVs line-up to target value

Improve presence in Chile, Colombia

New JV in South Africa for and Peru segments across the region

distribution in RHD markets

JVs product offer to increase share

in value segment

IVECO May 8, 2014 95

|

|

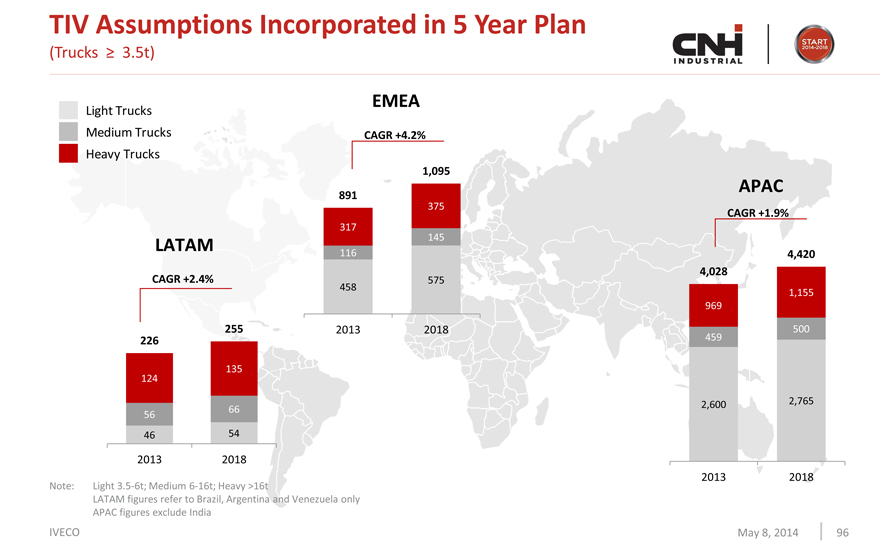

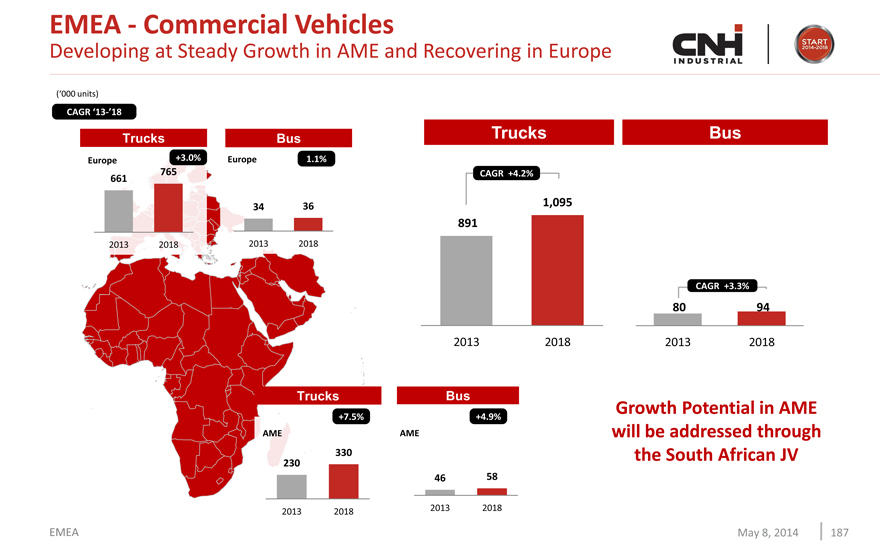

TIV Assumptions Incorporated in 5 Year Plan

(Trucks 3.5t)

EMEA

Light Trucks

Medium Trucks CAGR +4.2% Heavy Trucks

1,095

APAC

891

375

CAGR +1.9%

317

LATAM 145

116 4,420 4,028 CAGR +2.4% 458 575

1,155 969

255 2013 2018 459 500

226

135 124

66 2,600 2,765 56

46 54

2013 2018

Note: Light 3.5-6t; Medium 6-16t; Heavy >16t 2013 2018 LATAM figures refer to Brazil, Argentina and Venezuela only APAC figures exclude India

IVECO May 8, 2014 96

|

|

IVECO

May 8, 2014 97

|

|

Investor day auburn hills may 8th, 2014

Iveco Bus

Pierre Lahutte

|

|

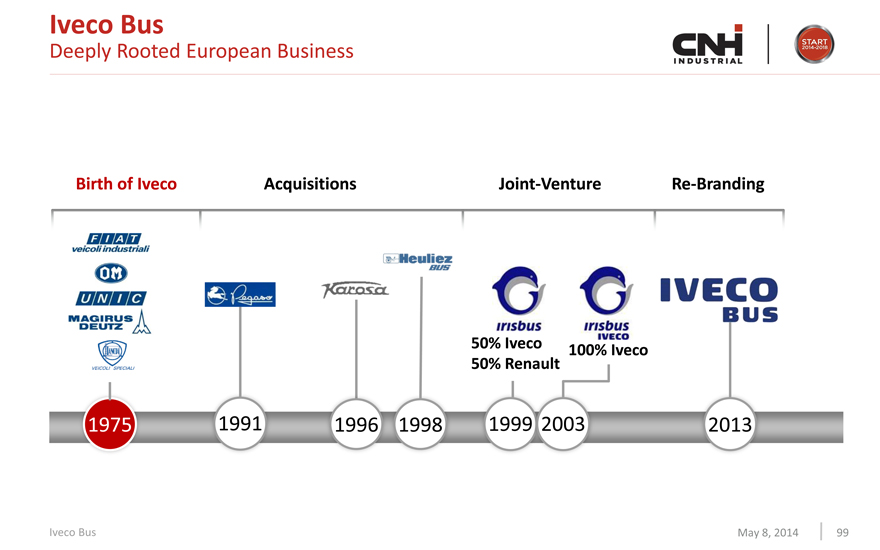

Iveco Bus

Deeply Rooted European Business

Birth of Iveco Acquisitions Joint-Venture Re-Branding

50% Iveco

100% Iveco 50% Renault 1975

1991 1996 1998 1999 2003 2013

IVECO BUS May 8, 2014 99

|

|

Public Transport Scenario

Bus Business Drivers

Urbanization Mobility Congestion Health Funding Liberalization

Bus is the Cheapest and Quickest Solution to address a growing Public Transport Need

Total Cost of Ownership: Fuel Economy and Passenger Capacity Sustainability: Diesel replacement by Gas / Hybrid / Electric / Plug-in Attractiveness: Style, Comfort, Accessibility and Infotainment

Iveco Bus

May 8, 2014 100

|

|

CNH INDUSTRIAL

START 2014-2018

Iveco Bus

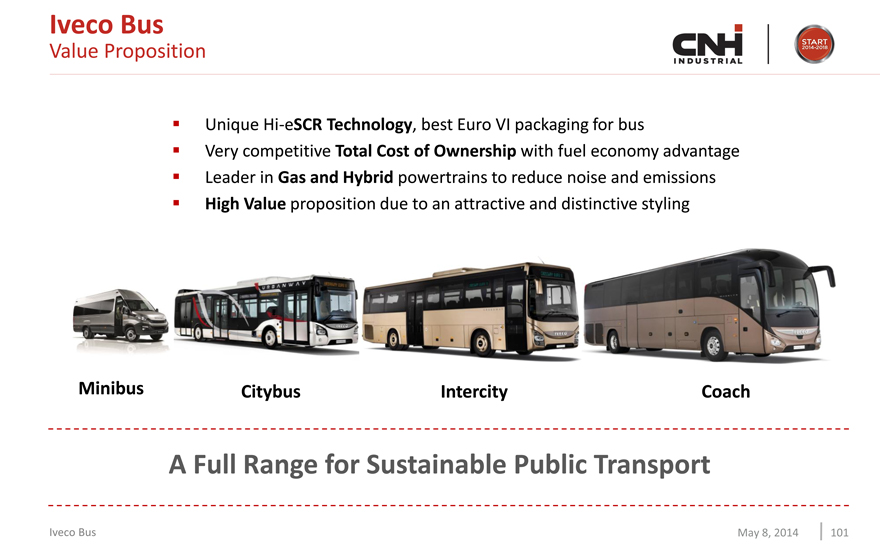

Value Proposition

Unique Hi-eSCR Technology, best Euro VI packaging for bus

Very competitive Total Cost of Ownership with fuel economy advantage Leader in Gas and Hybrid powertrains to reduce noise and emissions High Value proposition due to an attractive and distinctive styling

Minibus

Citybus

Intercity

Coach

A Full Range for Sustainable Public Transport

Iveco Bus

May 8, 2014

101

|

|

CNH INDUSTRIAL

START 2014-2018

Iveco Bus

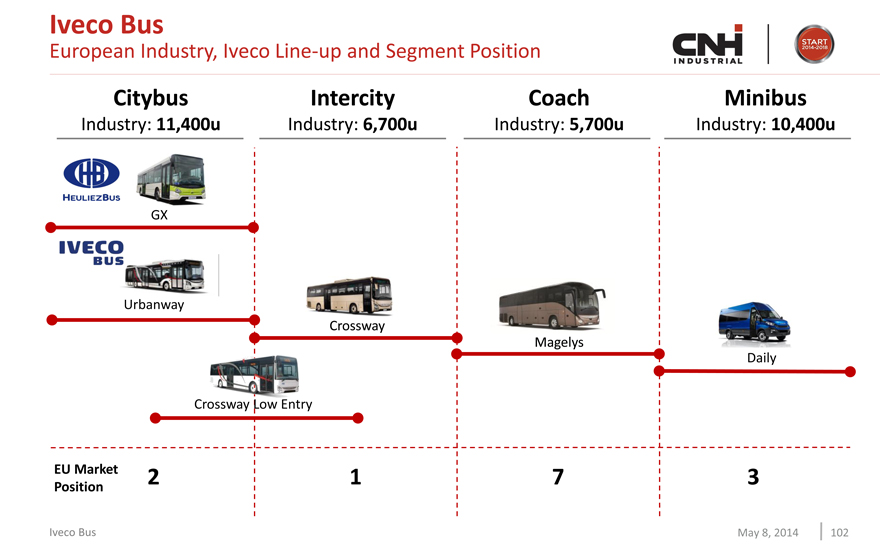

European Industry, Iveco Line-up and Segment Position

Citybus

Industry: 11,400u

Intercity

Industry: 6,700u

Coach

Industry: 5,700u

Minibus

Industry: 10,400u

HEULIEZ BUS

GX

IVECO BUS

Urbanway

Crossway

Magelys

Daily

Crossway Low Entry

EU Market Position

2 1 7 3

Iveco Bus

May 8, 2014

102

|

|

CNH INDUSTRIAL

START 2014-2018

Iveco Bus

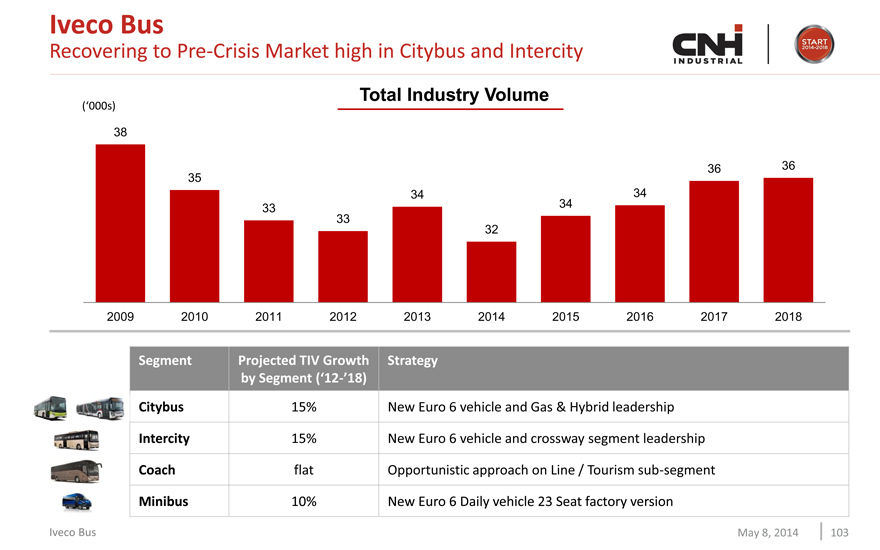

Recovering to Pre-Crisis Market high in Citybus and Intercity

Total Industry Volume

(‘000s)

38 35 33 33 34 32 34 34 36 36

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Segment

Projected TIV Growth by Segment (‘12-’18)

Strategy

Citybus

Intercity

Coach

Minibus

15%

15%

flat

10%

New Euro 6 vehicle and Gas & Hybrid leadership

New Euro 6 vehicle and crossway segment leadership

Opportunistic approach on Line / Tourism sub-segment

New Euro 6 Daily vehicle 23 Seat factory version

Iveco Bus

May 8, 2014

103

|

|

CNH INDUSTRIAL

START 2014-2018

Citybus

Urbanway

Iveco Bus

May 8, 2014

104

|

|

CNH INDUSTRIAL

START 2014-2018

Citybus

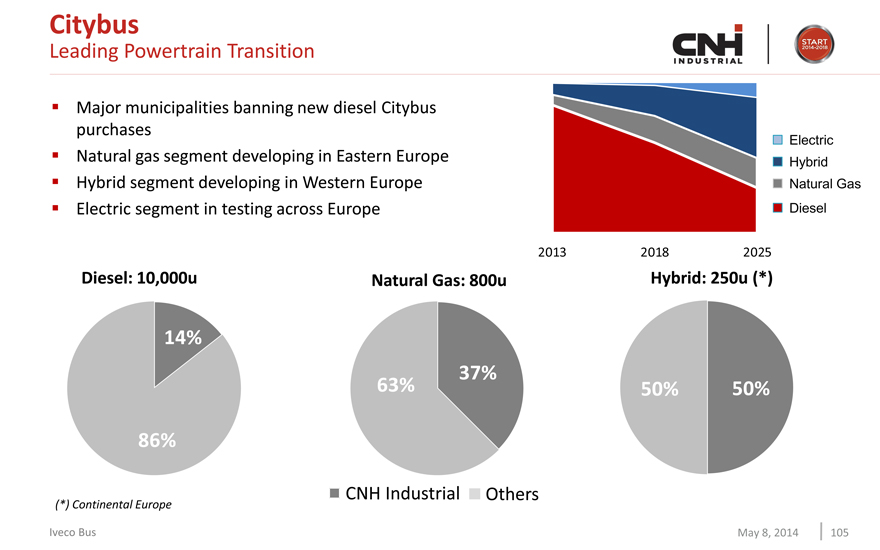

Leading Powertrain Transition

Major municipalities banning new diesel Citybus purchases Natural gas segment developing in Eastern Europe Hybrid segment developing in Western Europe Electric segment in testing across Europe

Electric

Hybrid

Natural Gas

Diesel

2013 2018 2025

Diesel: 10,000u

14% 86%

Natural Gas: 800u

63% 37%

Hybrid: 250u (*)

50% 50%

CNH Industrial

Others

(*) Continental Europe

May 8, 2014

Iveco Bus

105

|

|

CNH INDUSTRIAL

START 2014-2018

Citybus

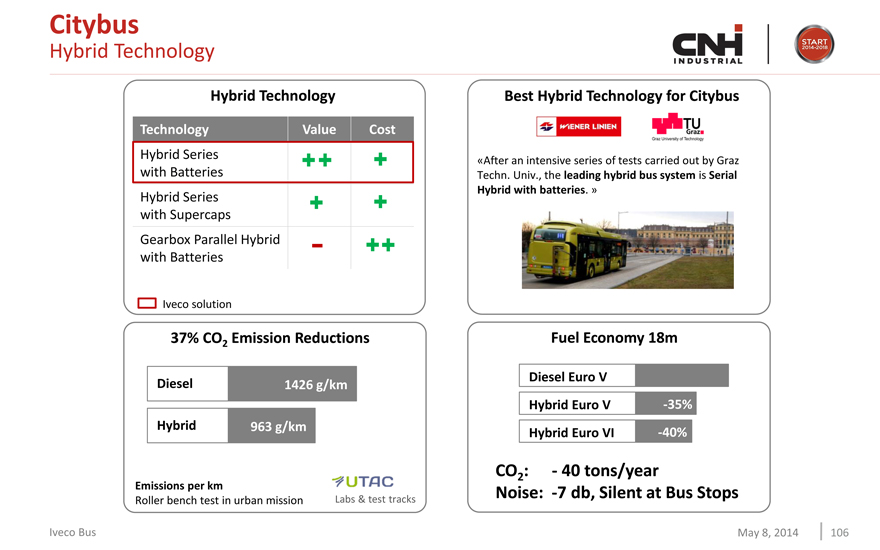

Hybrid Technology

Hybrid Technology

Technology Value Cost

Hybrid Series with Batteries ++ +

Hybrid Series with Supercaps + +

Gearbox Parallel Hybrid with Batteries - ++

Iveco solution

37% CO2 Emission Reductions

Diesel 1426 g/km

Hybrid 963 g/km

Emissions per km

Roller bench test in urban mission

UTAC

Labs & test tracks

Best Hybrid Technology for Citybus

«After an intensive series of tests carried out by Graz Techn. Univ., the leading hybrid bus system is Serial Hybrid with batteries. »

Fuel Economy 18m

Diesel Euro V

Hybrid Euro V

-35%

Hybrid Euro VI

-40%

CO2: - 40 tons/year

Noise: -7 db, Silent at Bus Stops

Iveco Bus

May 8, 2014

106

|

|

CNH INDUSTRIAL

START 2014-2018

Citybus

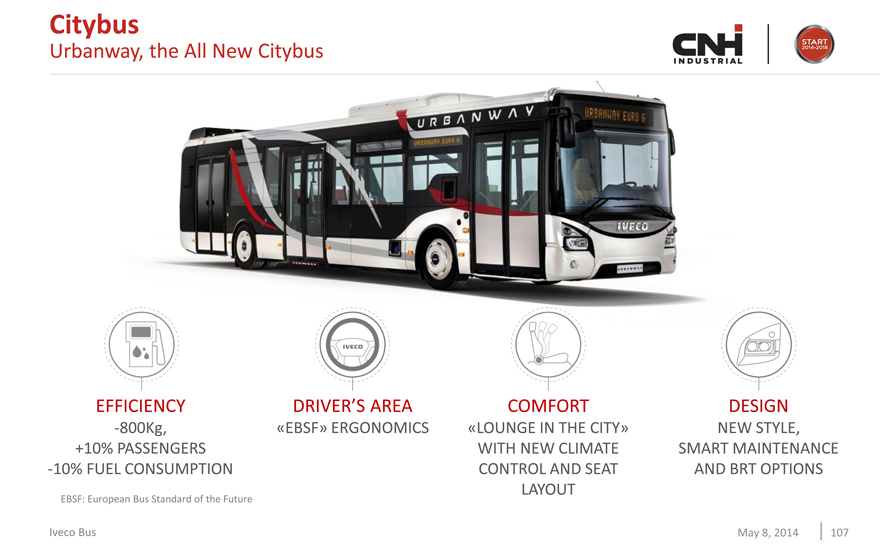

Urbanway, the All New Citybus

EFFICIENCY

-800Kg, +10% PASSENGERS

-10% FUEL CONSUMPTION

DRIVER’S AREA

«EBSF» ERGONOMICS

COMFORT

«LOUNGE IN THE CITY» WITH NEW CLIMATE CONTROL AND SEAT LAYOUT

DESIGN

NEW STYLE, SMART MAINTENANCE AND BRT OPTIONS

EBSF: European Bus Standard of the Future

Iveco Bus

May 8, 2014

107

|

|

CNH INDUSTRIAL

START 2014-2018

Citybus

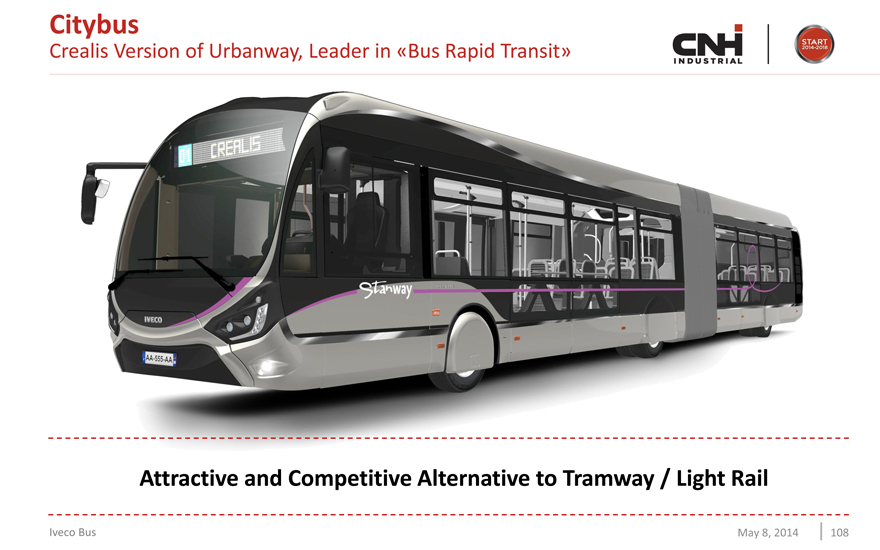

Crealis Version of Urbanway, Leader in «Bus Rapid Transit»

Attractive and Competitive Alternative to Tramway / Light Rail

Iveco Bus

May 8, 2014

108

|

|

CNH INDUSTRIAL

START 2014-2018

Citybus

Heuliez Bus

Premium brand in the Citybus market

Innovative brand: 1st articulated, 1st Gas, 1st Hybrid

Relevant Electrical Trolleybus knowhow

HB HEULIEZBUS

Iveco Bus

May 8, 2014

109

|

|

CNH INDUSTRIAL

START 2014-2018

Intercity

Crossway

Iveco Bus

May 8, 2014

110

|

|

CNH INDUSTRIAL

START 2014-2018

Intercity

Crossway, the Customer’s Money Maker

PRODUCTIVITY

BEST IN CLASS TOTAL COST OF OWNERSHIP

VERSATILITY

THREE LENGTHS (10.8M - 12M - 13M) ONLY 63 SEAT INTERCITY WITHIN 13M

DESIGN

MODERN STYLE EASY MAINTENANCE

FUEL ECONOMY

LOW CO2 EMISSIONS

Iveco Bus

May 8, 2014

111

|

|

CNH INDUSTRIAL

START 2014-2018

Iveco Bus

Low Entry

Crossway Low Entry

May 8, 2014

112

|

|

CNH INDUSTRIAL

START 2014-2018

Low Entry

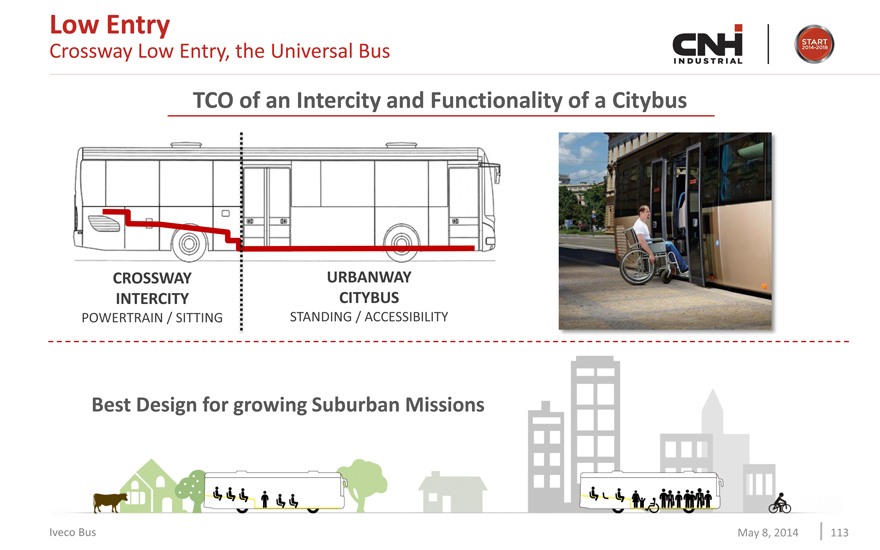

Crossway Low Entry, the Universal Bus

TCO of an Intercity and Functionality of a Citybus

CROSSWAY INTERCITY

POWERTRAIN / SITTING

URBANWAY CITYBUS

STANDING / ACCESSIBILITY

Best Design for growing Suburban Missions

Iveco Bus

May 8, 2014

113

|

|

CNH INDUSTRIAL

START 2014-2018

Coach

Magelys

Iveco Bus

May 8, 2014

114

|

|

CNH INDUSTRIAL

START 2014-2018

Coach

The High Value Coach

EFFICIENCY

HI-eSCR SMART DRIVELINE

SAFETY

ADVANCED ACTIVE AND PASSIVE SAFETY DEVICES: LANE DEPARTURE WARNING SYSTEM” & “ADAPTIVE CRUISE CONTROL”

HIGH COMFORT

NEW HVAC SYSTEM TAILORED SOLUTIONS

DESIGN

NEW LIGHTING WITH LED INTEGRATION

Iveco Bus

May 8, 2014

115

|

|

CNH INDUSTRIAL

START 2014-2018

Minibus

New Daily

Iveco Bus

May 8, 2014

116

|

|

CNH INDUSTRIAL

START 2014-2018

Minibus

Game Changer Derived from 19.6m3 New Daily

PRODUCTIVITY

BEST IN CLASS PASSENGER CAPACITY AND FUEL ECONOMY

DESIGN

NEW STYLE AND DASHBOARD

DRIVER’S AREA

IMPROVED ERGONOMICS AND DRIVING COMFORT

ACCESSIBILITY

NEW PASSENGER DOOR AND INTERIORS

Iveco Bus

May 8, 2014

117

|

|

CNH INDUSTRIAL

START 2014-2018

Iveco Bus

Ready to go, Ready to grow!

Iveco Bus

May 8, 2014

118

|

|

CNH INDUSTRIAL

START 2014-2018

INVESTOR DAY

AUBURN HILLS MAY 8TH 2014

Specialty Vehicles

Alessandro Nasi

|

|

CNH INDUSTRIAL

START 2014-2018

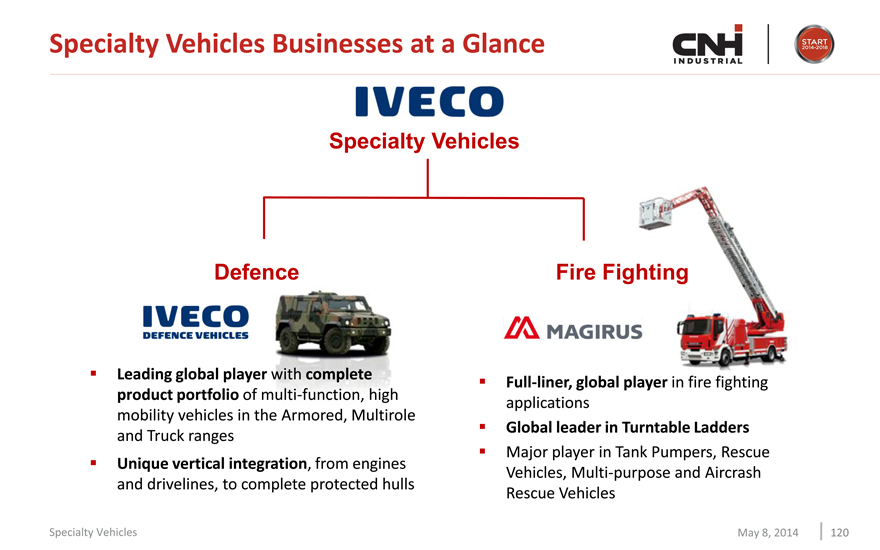

Specialty Vehicles Businesses at a Glance

IVECO

Specialty Vehicles

Defence

IVECO DEFENCE VEHICLES

Leading global player with complete product portfolio of multi-function, high mobility vehicles in the Armored, Multirole and Truck ranges

Unique vertical integration, from engines and drivelines, to complete protected hulls

Fire Fighting

MAGIRUS

Full-liner, global player in fire fighting applications

Global leader in Turntable Ladders

Major player in Tank Pumpers, Rescue Vehicles, Multi-purpose and Aircrash Rescue Vehicles

Specialty Vehicles

May 8, 2014

120

|

|

CNH INDUSTRIAL

START 2014-2018

Defence Vehicles

IVECO DEFENCE VEHICLES

Specialty Vehicles

May 8, 2014

121

|

|

CNH INDUSTRIAL

START 2014-2018

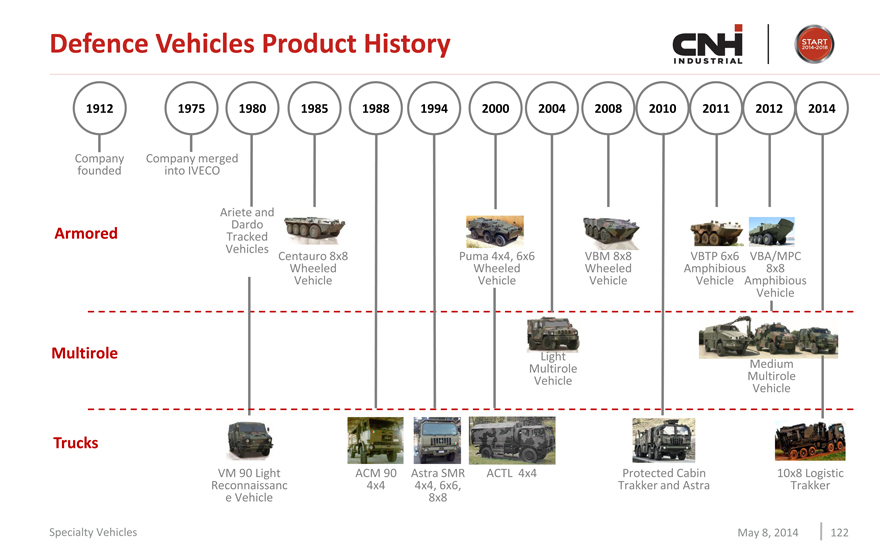

Defence Vehicles Product History

1912 1975 1980 1985 1988 1994 2000 2004 2008 2010 2011 2012 2014

Company founded

Company merged into IVECO

Ariete and Dardo Tracked Vehicles

Centauro 8x8 Wheeled Vehicle

Puma 4x4, 6x6 Wheeled Vehicle

VM 90 Light Reconnaissance Vehicle

ACM 90 4x4

Astra SMR 4x4, 6x6, 8x8

ACTL 4x4

Protected Cabin Trakker and Astra

Light Multirole Vehicle

VBM 8x8 Wheeled Vehicle

VBTP 6x6 Amphibious Vehicle

10x8 Logistic Trakker

VBA/MPC 8x8 Amphibious Vehicle

Medium Multirole Vehicle

Armored

Multirole

Trucks

Specialty Vehicles

May 8, 2014

122

|

|

CNH INDUSTRIAL

START 2014-2018

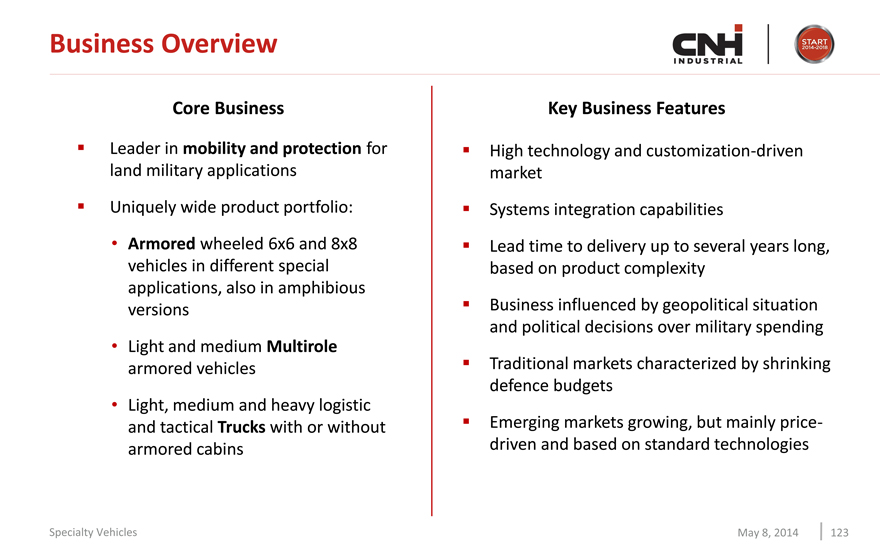

Business Overview

Core Business

Leader in mobility and protection for land military applications

Uniquely wide product portfolio:

Armored wheeled 6x6 and 8x8 vehicles in different special applications, also in amphibious versions

Light and medium Multirole armored vehicles

Light, medium and heavy logistic and tactical Trucks with or without armored cabins

Key Business Features

High technology and customization-driven market

Systems integration capabilities

Lead time to delivery up to several years long, based on product complexity

Business influenced by geopolitical situation and political decisions over military spending

Traditional markets characterized by shrinking defence budgets

Emerging markets growing, but mainly price-driven and based on standard technologies

Specialty Vehicles

May 8, 2014

123

|

|

CNH INDUSTRIAL

START 2014-2018

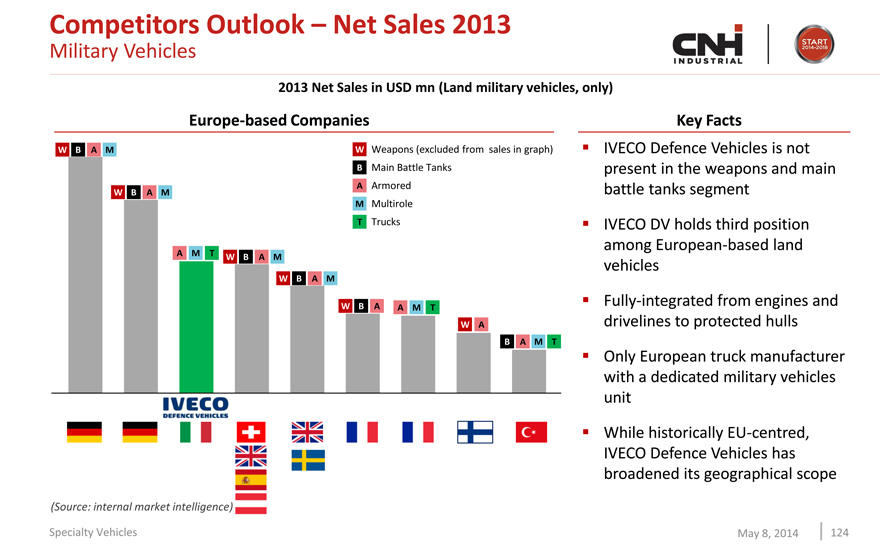

Competitors Outlook – Net Sales 2013

Military Vehicles

2013 Net Sales in USD mn (Land military vehicles, only)

Europe-based Companies

WBAM

WBAM

AMT

WBAM

WBAM

WBA

AMT

WA

BAMT

W Weapons (excluded from sales in graph) B Main Battle Tanks A Armored M Multirole T Trucks

(Source: internal market intelligence)

IVECO DEFENCE VEHICLES

Key Facts

IVECO Defence Vehicles is not present in the weapons and main battle tanks segment

IVECO DV holds third position among European-based land vehicles

Fully-integrated from engines and drivelines to protected hulls

Only European truck manufacturer with a dedicated military vehicles unit

While historically EU-centred, IVECO Defence Vehicles has broadened its geographical scope

Specialty Vehicles

May 8, 2014

124

|

|

CNH INDUSTRIAL

START 2014-2018

Production Footprint & Commercial Organization

IVECO Defence Vehicles employs >1,000 employees worldwide, located in:

Production facilities in Italy (Bolzano, Vittorio Veneto, Piacenza) and Brazil (Sete Lagoas) Commercial offices throughout Europe and Latin America

Brazil, Sete Lagoas

Defence Vehicles

Commercial Offices Italy, Bolzano Spain, Madrid Norway, Oslo Belgium, Brussels Germany, Ulm France, Paris - Trappes UK, London - Watford Brazil, Belo Horizonte (IVECO)

Plants

Commercial offices

Italy, Piacenza

Astra Defence

Italy, Bolzano

Defence Vehicles

Italy, Vitt.Veneto

Defence Vehicles

Specialty Vehicles

May 8, 2014

125

|

|

START 2014-2018

Product Portfolio

Armored

Multi-function vehicles with ballistic steel hull and add-on protection

Multirole

High mobility protected tactical carriers for reconnaissance missions and combat support

Tactical & Logistics Trucks

Wide range of on-and off-road standard to high performance, protected and unprotected vehicles

Specialty Vehicles

May 8, 2014

126

|

|

CNH INDUSTRIAL

START 2014-2018

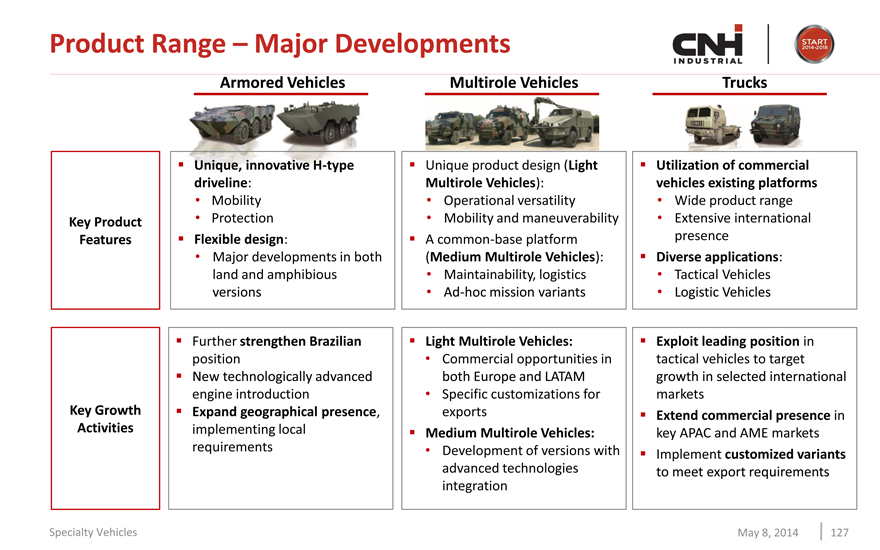

Product Range – Major Developments

Armored Vehicles

Multirole Vehicles

Trucks

Key Product Features

Unique, innovative H-type driveline:

Mobility Protection

Flexible design:

Major developments in both land and amphibious versions

Unique product design (Light Multirole Vehicles):

Operational versatility

Mobility and maneuverability A common-base platform (Medium Multirole Vehicles):

Maintainability, logistics

Ad-hoc mission variants

Utilization of commercial vehicles existing platforms

Wide product range

Extensive international presence

Diverse applications:

Tactical Vehicles

Logistic Vehicles

Further strengthen Brazilian position New technologically advanced engine introduction

Expand geographical presence, implementing local requirements

Light Multirole Vehicles:

Commercial opportunities in both Europe and LATAM

Specific customizations for exports

Medium Multirole Vehicles:

Development of versions with advanced technologies integration

Exploit leading position in tactical vehicles to target growth in selected international markets

Extend commercial presence in key APAC and AME markets

Implement customized variants to meet export requirements

Specialty Vehicles

May 8, 2014

127

|

|

CNH INDUSTRIAL

START 2014-2018

Focus on VBTP Brazil

Long term contract signed with the Brazilian Army in 2009 Contract for 10 different versions Localized industrial organization established in 2012 with R&D, manufacturing and customer service competencies

VBTE AMB-MR

VBE PC-MR

Specialty Vehicles

May 8, 2014

128

|

|

CNH INDUSTRIAL

START 2014-2018

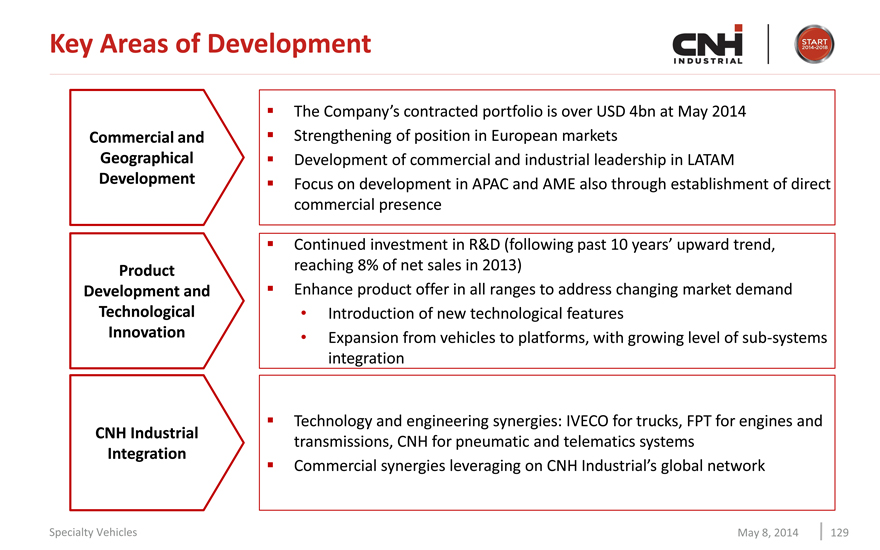

Key Areas of Development

Commercial and Geographical Development

The Company’s contracted portfolio is over USD 4bn at May 2014

Strengthening of position in European markets

Development of commercial and industrial leadership in LATAM

Focus on development in APAC and AME also through establishment of direct commercial presence

Product Development and Technological Innovation

Continued investment in R&D (following past 10 years’ upward trend, reaching 8% of net sales in 2013) Enhance product offer in all ranges to address changing market demand

Introduction of new technological features

Expansion from vehicles to platforms, with growing level of sub-systems integration

CNH Industrial Integration

Technology and engineering synergies: IVECO for trucks, FPT for engines and transmissions, CNH for pneumatic and telematics systems

Commercial synergies leveraging on CNH Industrial’s global network

Specialty Vehicles

May 8, 2014

129

|

|

CNH INDUSTRIAL

START 2014-2018

Concluding Remarks

IVECO Defence Vehicles Benefits from:

Top player position in Europe and developing market leadership in Brazil Wide international customer base Recognized leadership in technology for protection and mobility

High flexibility to adapt to customer needs and respond to local content requirements

Integration with CNH Industrial’s technological, industrial, and commercial capabilities

Growth in the coming years will be supported by:

Expansion of business beyond traditional markets

Extension of product portfolio to meet evolving customer requirements New technological applications to develop system-integrator capabilities

Specialty Vehicles

May 8, 2014

130

|

|

CNH INDUSTRIAL

START 2014-2018

Fire Fighting Vehicles

MAGIRUS

Specialty Vehicles

May 8, 2014

131

|

|

CNH INDUSTRIAL

START 2014-2018

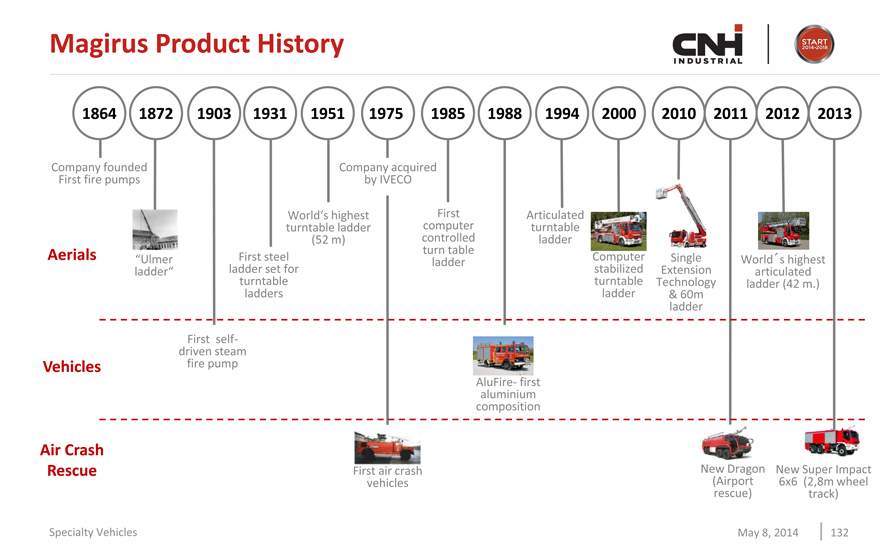

Magirus Product History

1864 1872 1903 1931 1951 1975 1985 1988 1994 2000 2010 2011 2012 2013

Company founded First fire pumps

Aerials

“Ulmer ladder”

Vehicles

First self-driven steam fire pump

First steel ladder set for turntable ladders

World‘s highest turntable ladder (52 m)

for

Company acquired by IVECO

First computer controlled turn table ladder

Articulated turntable ladder

Computer stabilized turntable ladder

Single Extension Technology

& 60m ladder

World´s highest articulated ladder (42 m.)

Air Crash Rescue

First air crash vehicles

AluFire- first aluminium composition

New Dragon (Airport rescue)

New Super Impact 6x6 (2,8m wheel track)

Specialty Vehicles

May 8, 2014

132

|

|

CNH INDUSTRIAL

START 2014-2018

Business Overview

Core Business

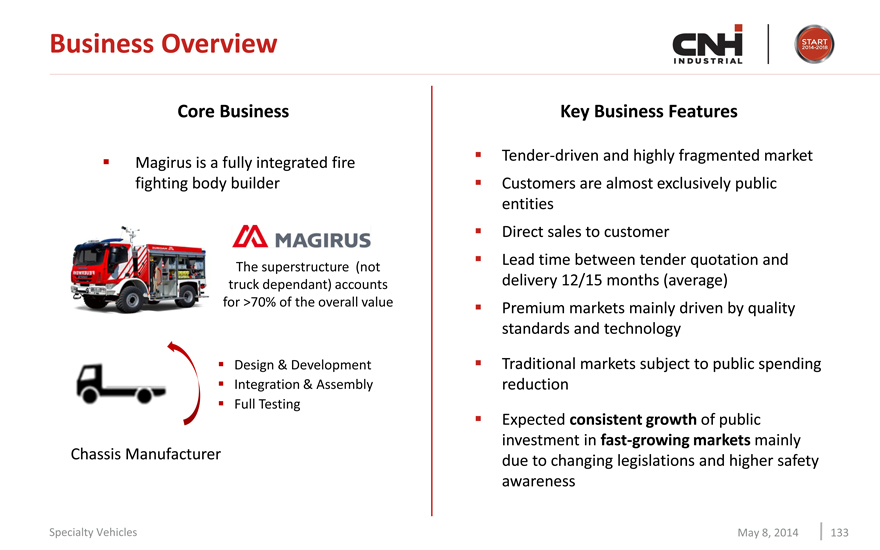

Magirus is a fully integrated fire fighting body builder

The superstructure (not truck dependant) accounts for >70% of the overall value

Design & Development Integration & Assembly Full Testing

Chassis Manufacturer

Key Business Features

Tender-driven and highly fragmented market Customers are almost exclusively public entities Direct sales to customer Lead time between tender quotation and delivery 12/15 months (average) Premium markets mainly driven by quality standards and technology

Traditional markets subject to public spending reduction

Expected consistent growth of public investment in fast-growing markets mainly due to changing legislations and higher safety awareness

Specialty Vehicles

May 8, 2014

133

|

|

CNH INDUSTRIAL

START 2014-2018

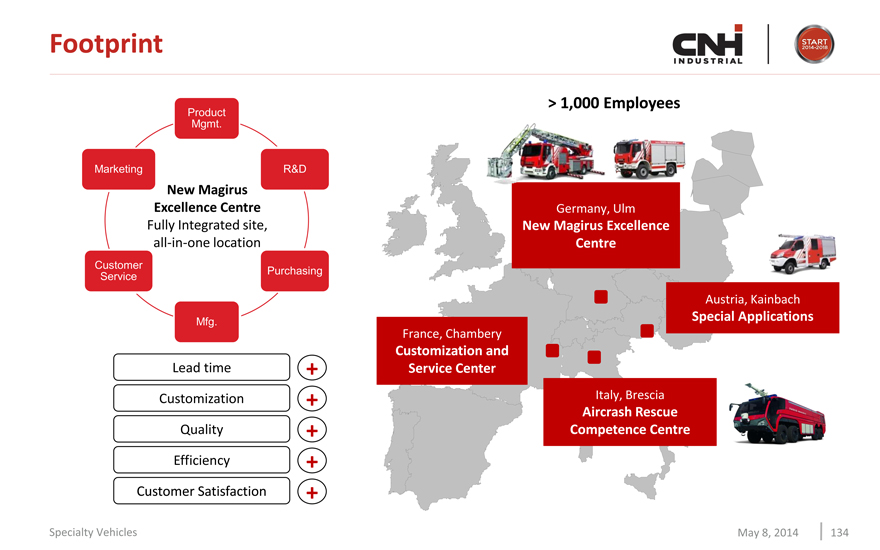

Footprint

Product Mgmt.

Marketing

Customer Service

Mfg.

Purchasing

R&D

New Magirus Excellence Centre

Fully Integrated site, all-in-one location

Lead time

Customization

Quality

Efficiency

Customer Satisfaction

> 1,000 Employees

Germany, Ulm

New Magirus Excellence

Centre

France, Chambery

Customization and Service Center

Italy, Brescia

Aircrash Rescue Competence Centre

Austria, Kainbach

Special Applications

Specialty Vehicles

May 8, 2014

134

|

|

CNH INDUSTRIAL

START 2014-2018

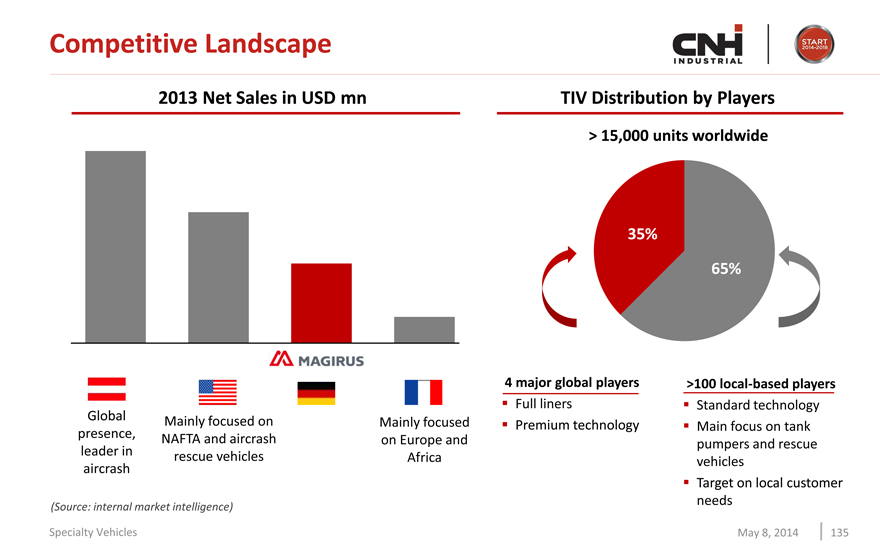

Competitive Landscape

2013 Net Sales in USD mn

TIV Distribution by Players

> 15,000 units worldwide

Global presence, leader in aircrash

Mainly focused on NAFTA and aircrash rescue vehicles

(Source: internal market intelligence)

35%

65%

Mainly focused on Europe and Africa

4 major global players

Full liners

Premium technology

>100 local-based players

Standard technology

Main focus on tank pumpers and rescue vehicles

Target on local customer needs

Specialty Vehicles

May 8, 2014

135

|

|

CNH INDUSTRIAL

START 2014-2018

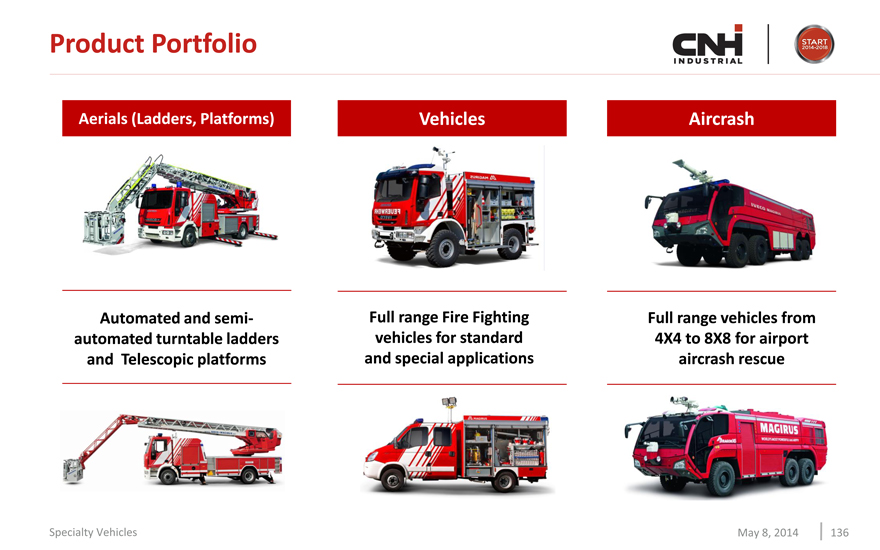

Product Portfolio

Aerials (Ladders, Platforms)

Automated and semi-automated turntable ladders and Telescopic platforms

Vehicles

Full range Fire Fighting vehicles for standard and special applications

Aircrash

Full range vehicles from 4X4 to 8X8 for airport aircrash rescue

Specialty Vehicles

May 8, 2014

136

|

|

CNH INDUSTRIAL

START 2014-2018

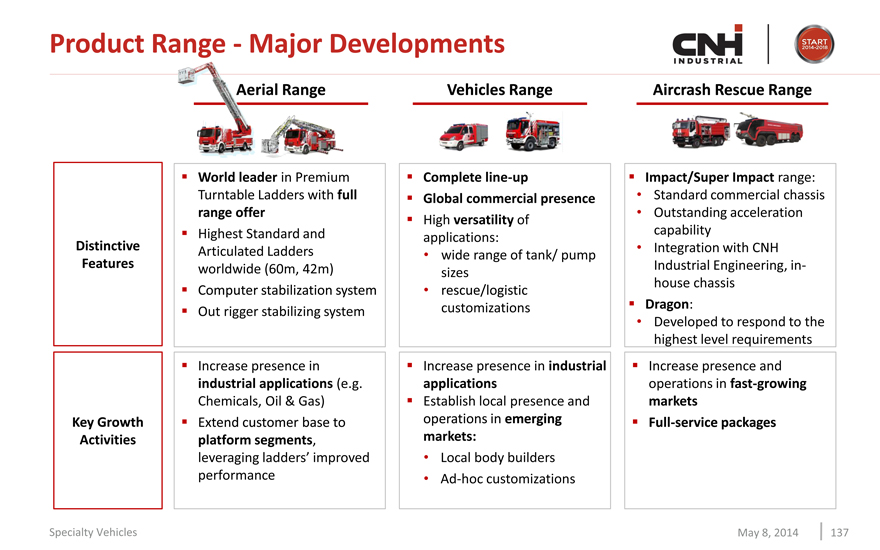

Product Range - Major Developments

Aerial Range

Vehicles Range

Aircrash Rescue Range

Distinctive

Features

World leader in Premium Turntable Ladders with full range offer

Highest Standard and Articulated Ladders worldwide (60m, 42m) Computer stabilization system Out rigger stabilizing system

Complete line-up

Global commercial presence High versatility of applications:

wide range of tank/ pump sizes

rescue/logistic customizations

Impact/Super Impact range:

Standard commercial chassis Outstanding acceleration capability Integration with CNH Industrial Engineering, in-house chassis

Dragon:

Developed to respond to the highest level requirements

Key Growth Activities

Increase presence in industrial applications (e.g. Chemicals, Oil & Gas) Extend customer base to platform segments, leveraging ladders’ improved performance

Increase presence in industrial applications

Establish local presence and operations in emerging markets:

Local body builders

Ad-hoc customizations

Increase presence and operations in fast-growing markets Full-service packages

Specialty Vehicles

May 8, 2014

137

|

|

CNH INDUSTRIAL

START 2014-2018

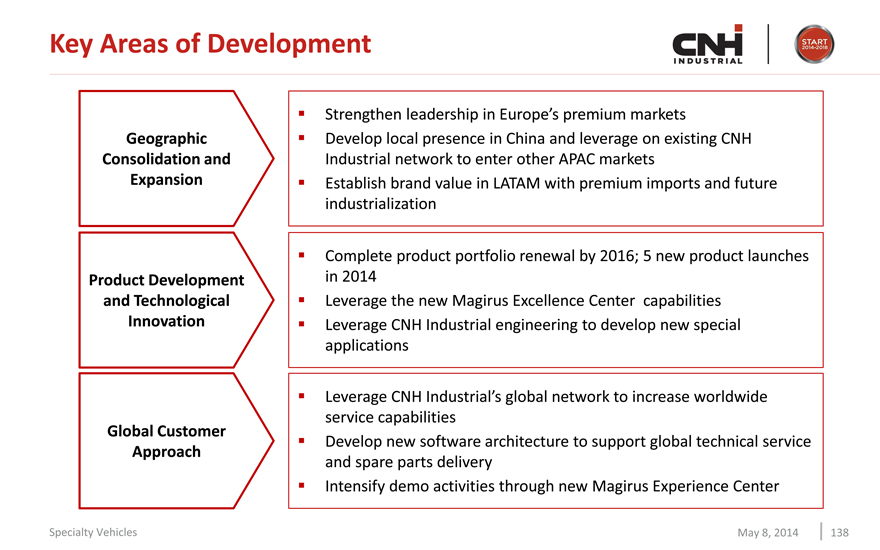

Key Areas of Development

Geographic Consolidation and Expansion

Strengthen leadership in Europe’s premium markets

Develop local presence in China and leverage on existing CNH Industrial network to enter other APAC markets Establish brand value in LATAM with premium imports and future industrialization

Product Development and Technological Innovation

Complete product portfolio renewal by 2016; 5 new product launches in 2014 Leverage the new Magirus Excellence Center capabilities Leverage CNH Industrial engineering to develop new special applications

Global Customer Approach

Leverage CNH Industrial’s global network to increase worldwide service capabilities Develop new software architecture to support global technical service and spare parts delivery Intensify demo activities through new Magirus Experience Center

Specialty Vehicles

May 8, 2014

138

|

|

CNH INDUSTRIAL

START 2014-2018

Conclusive Remarks

Magirus benefits from:

150 years of tradition, strong brand recognition with continuous technological innovation All-in-one integrated manufacturer (superstructure, chassis, driveline) Leading market position in Fire Ladders Fully integrated development and manufacturing at New Magirus Excellence Centre CNH Industrial integration opportunities (engineering, suppliers, distribution)

Growth in the coming years will be supported by:

Continued expansion of business beyond traditional markets

Extension of product portfolio to meet evolving customer requirements

Specialty Vehicles

May 8, 2014

139

|

|

CNH INDUSTRIAL

START 2014-2018

INVESTOR DAY

AUBURN HILLS

MAY 8TH, 2014

FPT Industrial

Giovanni Bartoli

|

|

CNH INDUSTRIAL

START 2014-2018

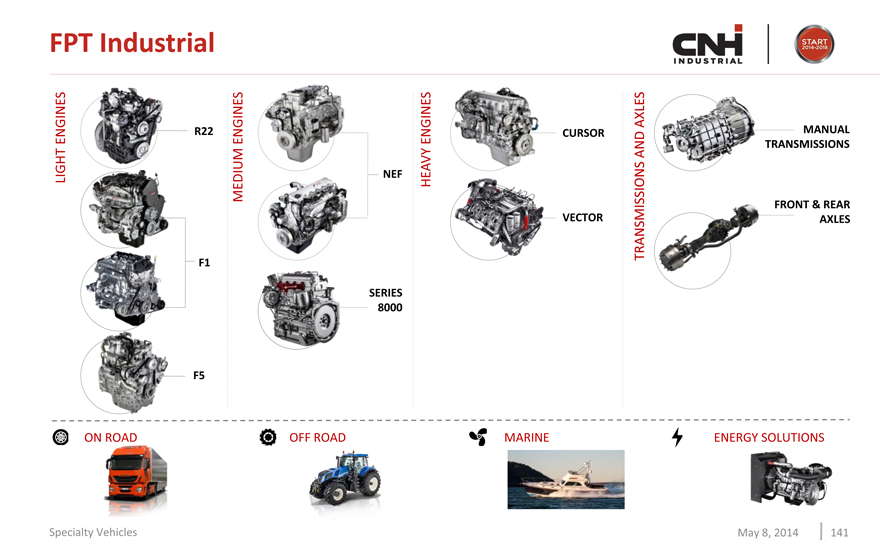

FPT Industrial

LIGHT ENGINES

R22

F1

F5

MEDIUM ENGINES

NEF

SERIES

8000

HEAVY ENGINES

CURSOR

VECTOR

TRANSMISSIONS AND AXLES

MANUAL

TRANSMISSIONS

FRONT & REAR

AXLES

ON ROAD

OFF ROAD

MARINE

ENERGY SOLUTIONS

Specialty Vehicles

May 8, 2014

141

|

|

CNH INDUSTRIAL

START 2014-2018

FPT Industrial DNA

Recognized leader in engine and after treatment solutions

Contribution to the development and first to introduce Common Rail

First to introduce turbocharging technology on diesel engines

First to introduce maintenance free emission reduction system without

Exhaust Gas Recirculation (EGR) and Diesel Particulate Filter (DPF) for Tier 4B

Strategy based on the development of technologies that:

Improve the final customer’s productivity by increasing performance

Reduce the total cost of ownership by improving efficiency

Maintaining a leadership position:

In fuel consumption

In emission reduction solutions

Specialty Vehicles

May 8, 2014

142

|

|

CNH INDUSTRIAL

START 2014-2018

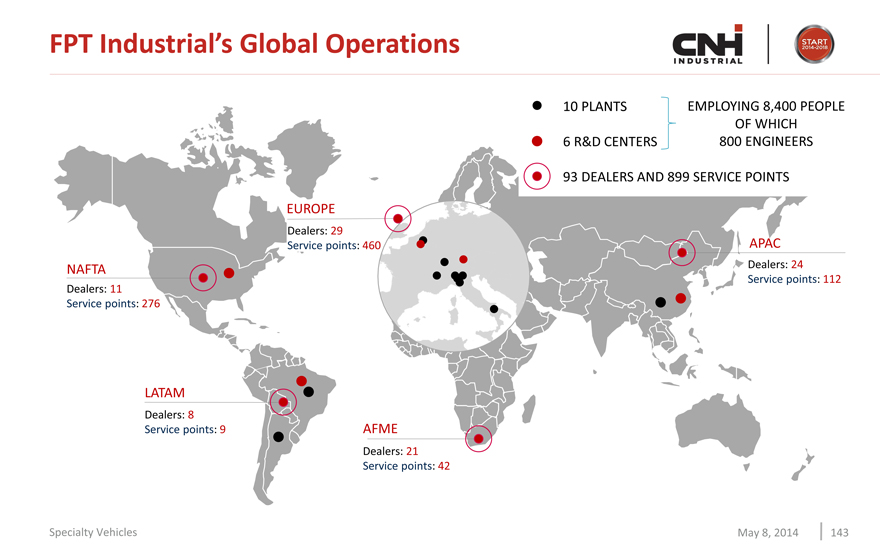

FPT Industrial’s Global Operations

10 PLANTS

6 R&D CENTERS

93 DEALERS AND 899 SERVICE POINTS

EMPLOYING 8,400 PEOPLE OF WHICH

800 ENGINEERS

EUROPE

Dealers: 29 Service points: 460

NAFTA

Dealers: 11

Service points: 276

LATAM

Dealers: 8 Service points: 9

AFME

Dealers: 21 Service points: 42

APAC

Dealers: 24

Service points: 112

Specialty Vehicles

May 8, 2014

143

|

|

CNH INDUSTRIAL

START 2014-2018

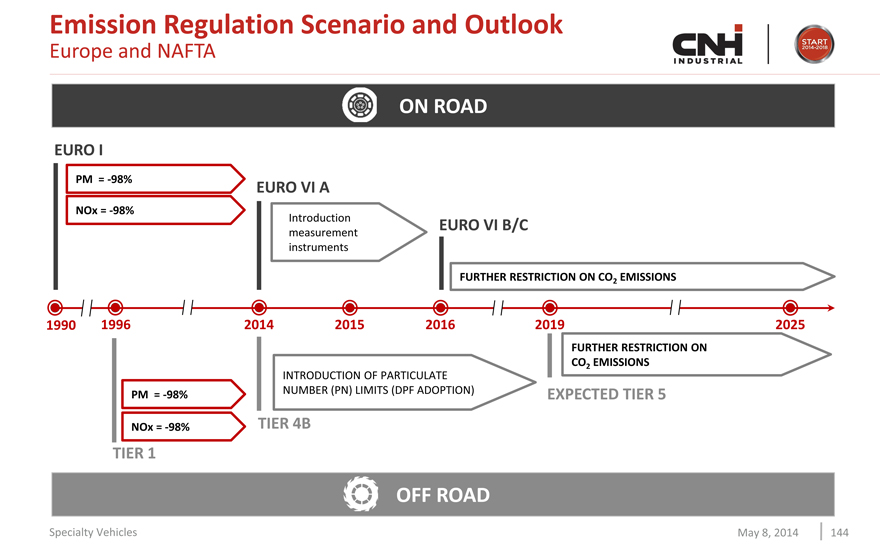

Emission Regulation Scenario and Outlook

Europe and NAFTA

ON ROAD

EURO I

PM = -98%

NOx = -98%

EURO VI A

Introduction measurement instruments

EURO VI B/C

1990

1996

2014

2015

2016

2019

2025

FURTHER RESTRICTION ON CO2 EMISSIONS

PM = -98%

NOx = -98%

INTRODUCTION OF PARTICULATE NUMBER (PN) LIMITS (DPF ADOPTION)

FURTHER RESTRICTION ON CO2 EMISSIONS

EXPECTED TIER 5

OFF ROAD

TIER 4B

TIER 1

Specialty Vehicles

May 8, 2014

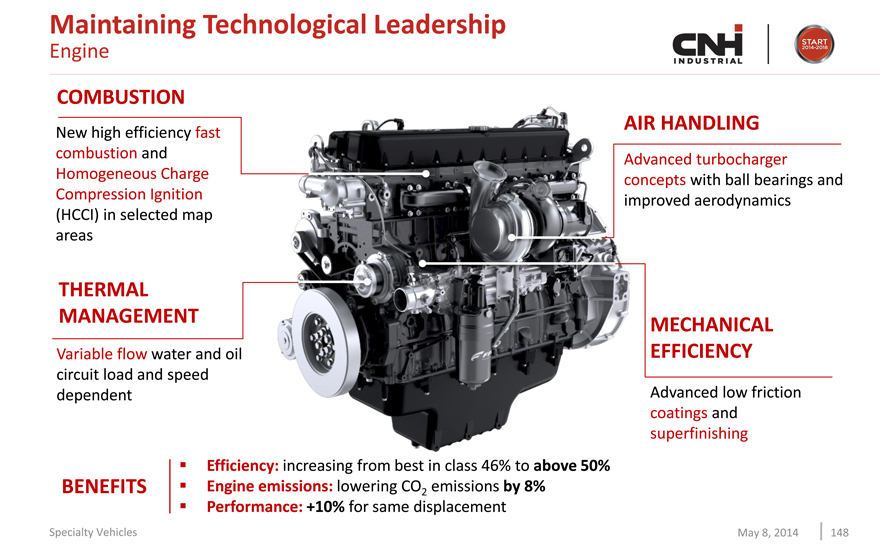

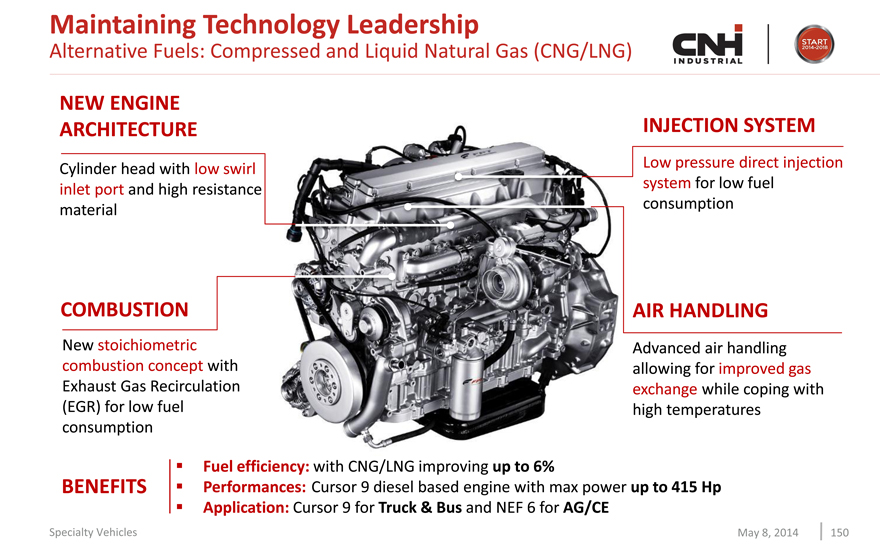

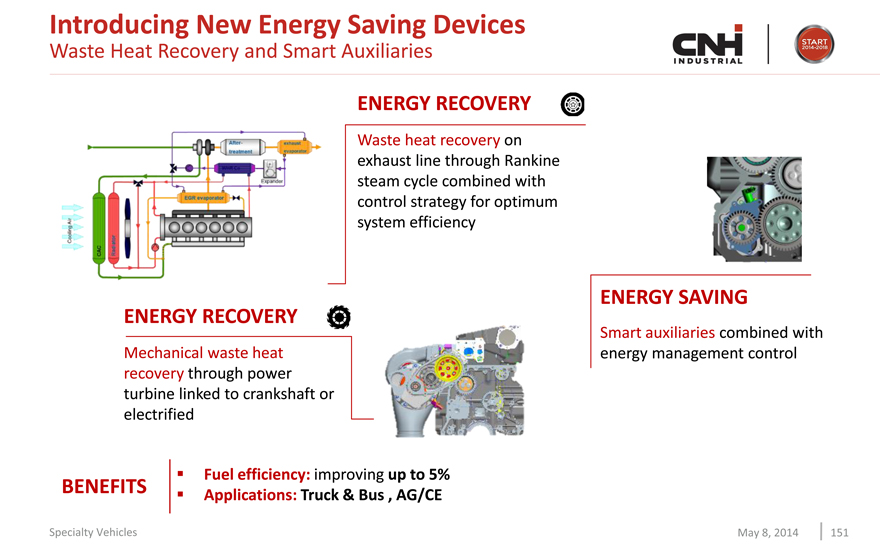

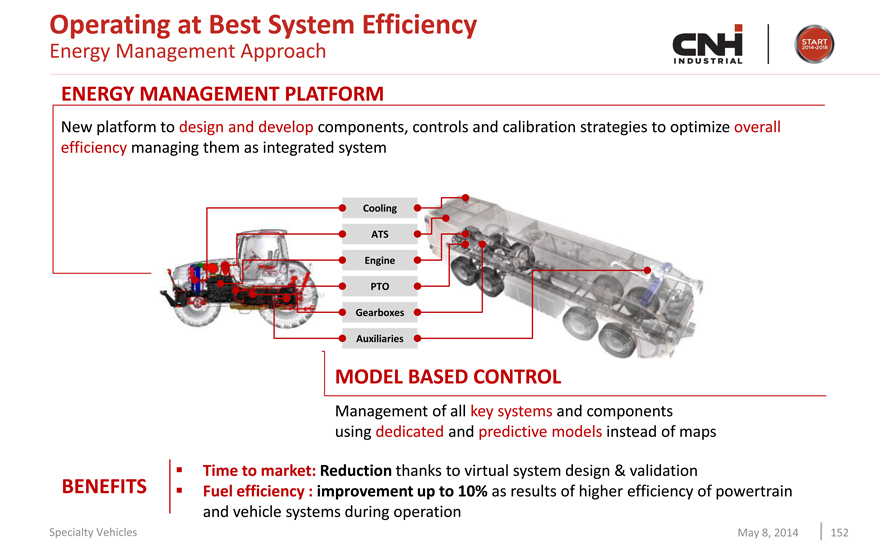

144

|

|

CNH INDUSTRIAL

START 2014-2018

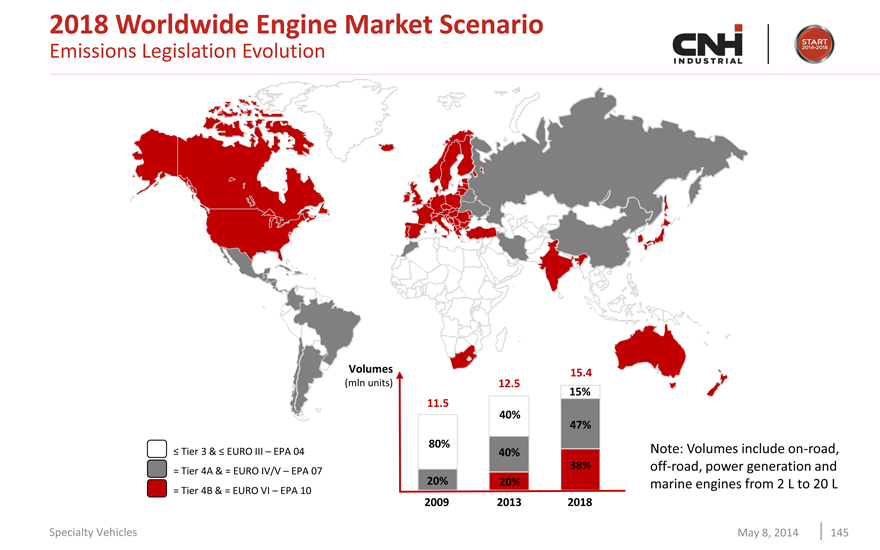

2018 Worldwide Engine Market Scenario

Emissions Legislation Evolution

Volumes

(mln units)

£ Tier 3 & £ EURO III – EPA 04

= Tier 4A & = EURO IV/V – EPA 07

= Tier 4B & = EURO VI – EPA 10

11.5

80%

20%

2009

12.5 40% 40%

20% 2013

15.4 15%

47% 38% 2018