|

September 2008

Preliminary Terms No.

759

Registration Statement No.

333-131266

Dated August 21,

2008

Filed pursuant to Rule

433

|

STRUCTURED

INVESTMENTS

Opportunities in

Equities

PLUS

Based

on the PowerShares® Water

Resources Portfolio due

October

20, 2009

Performance

Leveraged Upside SecuritiesSM

PLUS offer leveraged exposure to a wide

variety of assets and asset classes, including equities, commodities and

currencies. These investments allow investors to capture

enhanced returns relative to the asset’s actual positive

performance. The leverage typically applies only for a certain range

of price performance. In exchange for enhanced performance in that

range, investors generally forgo performance above a specified

maximum return. At maturity, an investor will receive an amount in

cash that may be more or less than the principal amount based upon the closing

value of the asset at maturity.

|

Issuer:

|

Morgan

Stanley

|

|

Maturity

date:

|

October

20, 2009

|

|

Underlying shares:

|

Shares of the PowerShares Water Resources

Portfolio

|

|

Aggregate principal

amount:

|

$

|

|

Payment at

maturity:

|

§ If

final share price is greater than initial

share price,

|

|

$10

+ leveraged upside payment

|

|

In

no event will the payment at maturity exceed the maximum payment at

maturity.

|

|

§ If

final share price is less than or equal to

initial share price,

|

|

$10

x share performance factor

|

|

This

amount will be less than or equal to the stated principal amount of

$10.

|

|

Share percent increase:

|

(final

share price – initial share price) / initial share

price

|

|

Leveraged upside

payment:

|

$10

x leverage factor x share percent increase

|

|

Initial share price:

|

The

closing price of one share of the underlying shares on the pricing

date

|

|

Final share price:

|

The

closing price of one share of the underlying shares on the valuation date,

times the

adjustment factor, subject to adjustment for certain market disruption

events.

|

|

Valuation

date:

|

October

16, 2009

|

|

Leverage

factor:

|

300%

|

|

Maximum payment at

maturity:

|

$11.60

to $11.80 (116%

to 118% of the stated principal amount). The actual maximum payment at

maturity will be determined on the pricing date.

|

|

Share performance

factor:

|

final

share price / initial share price

|

|

Stated principal

amount:

|

$10

|

|

Issue

price:

|

$10

(see “Commissions and Issue Price” below)

|

|

Pricing

date:

|

September ,

2008

|

|

Original issue

date:

|

September ,

2008

|

|

Adjustment

factor:

|

1.0,

subject to adjustment in the event of certain events affecting the

underlying shares.

|

|

CUSIP:

|

617480793

|

|

Listing:

|

The

PLUS will not be listed on any securities exchange.

|

|

Agent:

|

Morgan

Stanley & Co. Incorporated

|

|

Commissions and Issue

Price:

|

Price to Public(1)

|

Agent’s Commissions(1)(2)

|

Proceeds to

Company

|

|

Per PLUS

|

$10.00

|

$0.15

|

$9.85

|

|

Total

|

$

|

$

|

$

|

|

(1)

|

The

actual price to public and agent’s commissions for a particular investor

may be reduced for volume purchase discounts depending on the aggregate

amount of PLUS purchased by that investor. The lowest price

payable by an investor is $9.95 per PLUS. Please see “Syndicate

Information” on page 6 for further

details.

|

|

(2)

|

For

additional information, see “Plan of Distribution” in the accompanying

prospectus supplement for PLUS.

|

You

should read this document together with the related prospectus supplement and

prospectus, each of which can be accessed via the hyperlinks below, before you

decide to invest.

The issuer

has filed a registration statement (including a prospectus) with the SEC for the

offering to which this communication relates. Before you invest, you should read

the prospectus in that registration statement and other documents the issuer has

filed with the SEC for more complete information about the issuer and this

offering. You may get these documents for free by visiting EDGAR on the SEC Web

site at www.sec.gov. Alternatively, the issuer, any underwriter or any dealer

participating in this offering will arrange to send you the prospectus if you

request it by calling toll-free 1-800-584-6837.

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

Investment Overview

Performance Leveraged Upside

Securities

The

PowerShares Water Resources Portfolio PLUS (the “PLUS”) can be

used:

|

§

|

As an

alternative to direct exposure to the underlying shares that enhances

returns for a certain range of price performance of shares of the

underlying shares.

|

|

§

|

To enhance

returns and potentially outperform the underlying shares in a moderately

bullish scenario

|

|

§

|

To achieve

similar levels of exposure to the underlying shares as a direct investment

while using fewer dollars by taking advantage of the leverage

factor

|

The

PLUS are exposed on a 1:1 basis to the negative performance of shares of the

PowerShares Water Resources Portfolio.

|

Maturity:

|

13

Months

|

|

Leverage

factor:

|

300%

|

|

Maximum payment at

maturity:

|

$11.60 to

$11.80 per PLUS (116% to 118% of the stated principal

amount)

|

|

Principal

protection:

|

None

|

PowerShares Water Resources Portfolio

Overview

The

PowerShares Water Resources Portfolio (the “Portfolio”) is an exchange-traded

fund managed by The PowerShares Exchange-Traded Fund Trust, a registered

investment company, which seeks investment results that correspond generally to

the price and yield performance, before fees and expenses, of the Palisades

Water IndexTM. The

Palisades Water IndexTM is a

stock index calculated daily by Palisades Water Index Associates, LLC and

published daily by the American Stock Exchange, LLC, which is designed to select

companies that focus on the provision of potable water, water treatment, and

technology and services that are directly related to water

consumption. Trading in the underlying shares commenced on December

6, 2005. As of August 19, 2008, the Portfolio held the shares of 33

companies.

Information as of

market close on August 19, 2008

|

Bloomberg Ticker Symbol:

|

PHO

|

|

Top Portfolio

Holdings

|

Weight in the

Fund

|

|

Current Share Price:

|

21.89

|

|

Tetra Tech

Inc.

|

4.86%

|

|

52 Weeks

Ago:

|

20.05

|

|

URS

Corp.

|

4.33%

|

|

52 Week High (on 6/5/2008):

|

22.94

|

|

Itron

Inc

|

4.29%

|

|

52 Week Low (on 1/22/2008):

|

18.15

|

|

Danaher

Corp.

|

4.23%

|

|

|

|

|

AECOM

Technology Corp.

|

4.22%

|

|

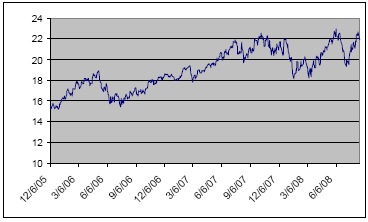

PowerShares Water Resources

Portfolio

Historical

Performance

Daily Closing

Prices

December 6, 2005 to August 19,

2008

|

|

|

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

Key Investment

Rationale

This 13 month

investment offers 300% leveraged upside, subject to a maximum payment at

maturity of $11.60 to $11.80 per PLUS.

Investors can use

the PLUS to enhance returns up to the maximum payment at maturity, while

maintaining similar risk as a direct investment in shares of the PowerShares Water Resources

Portfolio.

|

Leverage

Performance

|

The PLUS offer

investors an opportunity to capture enhanced returns relative to a direct

investment in the underlying shares within a certain range of price

performance.

|

|

Best Case

Scenario

|

The underlying

shares increase in price and, at maturity, the PLUS redeem for the maximum

payment at maturity, $11.60 to $11.80 (116% to 118% of the stated

principal amount).

|

|

Worst Case

Scenario

|

The underlying

shares decline in price and, at maturity, the PLUS redeem for less than

the stated principal amount by an amount proportional to the

decline.

|

Summary of Selected Key Risks (see page

9)

|

§

|

No guaranteed

return of principal.

|

|

§

|

Appreciation

potential is limited by the maximum payment at

maturity.

|

|

§

|

Investing in

the PLUS is not equivalent to investing in the underlying

shares.

|

|

§

|

There are

risks associated with investments in securities with concentration in a

single sector.

|

|

§

|

Adjustments to

the underlying shares or to the Palisades Water Index could adversely

affect the PLUS.

|

|

§

|

The underlying

shares may not exactly track the Palisades Water

Index.

|

|

§

|

The

antidilution adjustments do not cover every event that could affect the

underlying shares.

|

|

§

|

The PLUS will

not be listed on any securities

exchange.

|

|

§

|

Secondary

trading may be limited, and the inclusion of commissions and projected

profit from hedging in the original issue price is likely to adversely

affect secondary market prices and you could receive less, and possibly

significantly less, than the stated principal amount per PLUS if you try

to sell your PLUS prior to

maturity.

|

|

§

|

The market

price of the PLUS will be influenced by many unpredictable factors,

including the value, volatility and dividend yield of the Palisades Water

Index.

|

|

§

|

The U.S.

federal income tax consequences of an investment in the PLUS are

uncertain.

|

|

§

|

Credit risk to

Morgan Stanley.

|

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

Fact Sheet

The

PLUS offered are senior unsecured obligations of Morgan Stanley, will pay no

interest, do not guarantee any return of principal at maturity and have the

terms described in the prospectus supplement for PLUS and the prospectus, as

supplemented or modified by these preliminary terms. At maturity, an

investor will receive for each stated principal amount of PLUS that the investor

holds, an amount in cash that may be more or less than the stated principal

amount based upon the closing price of one underlying share at

maturity. The PLUS are senior notes issued as part of Morgan

Stanley’s Series F Global Medium-Term Notes program.

|

Expected Key

Dates

|

|

|

|

Pricing

Date:

|

Original Issue Date (Settlement Date):

|

Maturity Date:

|

|

September ,

2008

|

September ,

2008 (5 business days after the pricing date)

|

October

20, 2009, subject

to postponement due to a market disruption

event

|

|

Key Terms

|

|

|

Issuer:

|

Morgan

Stanley

|

|

Underlying

shares:

|

Shares of the PowerShares Water Resources Portfolio

|

|

|

$10

per PLUS. See “Syndicate Information” on page

6.

|

|

Stated principal

amount:

|

$10

per PLUS

|

|

Denominations:

|

$10

per PLUS and integral multiples thereof

|

|

Interest:

|

None

|

|

Bull market or bear market

PLUS:

|

Bull

market PLUS

|

|

Payment at

maturity:

|

§ If

the final share price is

greater than the initial share price,

|

|

|

$10

+ leveraged upside payment

|

|

|

In

no event will the payment at maturity exceed the maximum payment at

maturity.

|

|

|

§ If

the final share price is

less than or equal to the initial share price,

|

|

|

$10

x share performance factor

|

|

|

This

amount will be less than or equal to the stated principal amount of

$10.

|

|

Leveraged upside

payment:

|

$10 x leverage

factor x share percent increase

|

|

Leverage

factor:

|

300%

|

|

Share percent

increase:

|

(final

share price – initial share price) / initial share

price

|

|

Initial share

price:

|

The

closing price of one underlying share on the pricing

date.

|

|

Final share

price:

|

The

closing price of the one underlying share on the valuation date as

published under the Bloomberg ticker symbol “PHO” or any successor symbol,

times the

adjustment factor.

|

|

Valuation

date:

|

October

16, 2009, subject to adjustment for certain market disruption

events.

|

|

Share performance

factor:

|

final

share price / initial share price

|

|

Maximum payment at

maturity:

|

$11.60

to $11.80 (116%

to 118% of the stated principal amount)

|

|

Adjustment

factor:

|

1.0,

subject to adjustment in the event of certain events affecting the

underlying shares.

|

|

Postponement

of

maturity

date:

|

If

the scheduled valuation date is not a trading day or if a market

disruption event occurs on that day so that the valuation date as

postponed falls less than two scheduled trading days prior to the

scheduled maturity date, the maturity date of the PLUS will be postponed

until the second scheduled trading day following that valuation date as

postponed.

|

|

Risk

factors:

|

Please

see “Risk Factors” on page 9.

|

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

|

General

Information

|

|

|

Listing:

|

The

PLUS will not be listed on any securities exchange.

|

|

CUSIP:

|

617480793

|

|

Minimum ticketing

size:

|

100

PLUS

|

|

Tax

considerations:

|

Although

the issuer believes that, under current law, each PLUS should be treated

as a single financial contract that is an “open transaction” for U.S.

federal income tax purposes, there is uncertainty regarding the U.S.

federal income tax consequences of an investment in the

PLUS.

|

|

|

Assuming

this characterization of the PLUS is respected and subject to the

discussion under “United States Federal Taxation” in the accompanying

prospectus supplement for PLUS, the following U.S. federal income tax

consequences should result:

|

|

|

§ A U.S. Holder should not be

required to recognize taxable income over the term of the PLUS prior to

maturity, other than pursuant to a sale or exchange;

and

|

|

|

§ upon sale, exchange or settlement

of the PLUS at maturity, a U.S. Holder should

generally recognize gain or loss equal to the difference between the

amount realized and the U.S. Holder’s tax basis in the

PLUS. Subject to the discussion below concerning the

potential application of the “constructive ownership” rule under Section

1260 of the Internal Revenue Code of 1986, as amended, any gain or loss

recognized upon sale, exchange or settlement of a PLUS should be long-term

capital gain or loss if the U.S. Holder has held the PLUS for more than one year

at such time.

|

|

|

Because

the PLUS is linked to shares of an exchange-traded fund, although the

matter is not clear, there is a substantial risk that an investment in the

PLUS will be treated as a “constructive ownership

transaction.” If this treatment applies, it is not clear to

what extent any long-term capital gain of the U.S. Holder in respect of

the PLUS will be recharacterized as ordinary income (which ordinary income

would also be subject to an interest charge). U.S. investors

should read the section of the accompanying prospectus supplement for PLUS

called “United States Federal Taxation – Tax Consequences to U.S. Holders

– Tax Treatment of the PLUS – Possible Application of Section 1260 of the

Code” for additional information and consult their tax advisers regarding

the potential application of the “constructive ownership”

rule.

|

|

|

On

December 7, 2007, the Treasury Department and the Internal Revenue Service

(the “IRS”) released a notice requesting comments on the U.S. federal

income tax treatment of “prepaid forward contracts” and similar

instruments, such as the PLUS. The notice focuses in particular

on whether to require holders of these instruments to accrue income over

the term of their investment. It also asks for comments on a

number of related topics, including the character of income or loss with

respect to these instruments; whether short-term instruments should be

subject to any such accrual regime; the relevance of factors such as the

exchange-traded status of the instruments and the nature of the underlying

property to which the instruments are linked; the degree, if any, to which

income (including any mandated accruals) realized by non-U.S. investors

should be subject to withholding tax; and whether these instruments are or

should be subject to the “constructive ownership” regime. While

the notice requests comments on appropriate transition rules and effective

dates, any Treasury regulations or other guidance promulgated after

consideration of these issues could materially and adversely affect the

tax consequences of an investment in the PLUS, possibly with retroactive

effect.

|

|

|

Both U.S.

and non-U.S. investors considering an investment in the PLUS should read

the discussion under “Risk Factors ― Structure Specific Risk Factors” in

this document and the discussion under “United States Federal

Taxation” in the accompanying prospectus supplement for PLUS and consult

their tax advisers regarding all aspects of the U.S. federal income tax

consequences of an investment in the PLUS, including possible alternative

characterizations or treatments, the potential application of the

constructive ownership regime, the issues presented by the aforementioned

notice and any tax consequences arising under the laws of any state, local

or foreign taxing jurisdiction.

|

|

Trustee:

|

The

Bank of New York Mellon (as successor trustee to JPMorgan Chase Bank,

N.A.)

|

|

Calculation

agent:

|

Morgan

Stanley & Co. Incorporated (“MS &

Co.”)

|

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

|

Use of proceeds and

hedging:

|

The

net proceeds we receive from the sale of the PLUS will be used for general

corporate purposes and, in part, in connection with hedging our

obligations under the PLUS through one or more of our

subsidiaries.

|

|

|

On

or prior to the pricing date, we, through our subsidiaries or others, will

hedge our anticipated exposure in connection with the PLUS by taking

positions in the underlying shares or in the component stocks of the

Palisades Water Index, in futures and options contracts on the underlying

shares or the component stocks of the Palisades Water Index and in any

other securities or instruments we may wish to use in connection with such

hedging. Such purchase activity could increase the price of the

underlying shares, and therefore the price at which the underlying shares

must close on the valuation date before investors would receive at

maturity a payment that exceeds the principal amount of the

PLUS. For further information on our use of proceeds and

hedging, see “Use of Proceeds and Hedging” in the prospectus supplement

for PLUS.

|

|

ERISA:

|

See

“ERISA” in the prospectus supplement for PLUS.

|

|

Contact:

|

Morgan

Stanley clients may contact their local Morgan Stanley branch office or

our principal executive offices at 1585 Broadway, New York, New York 10036

(telephone number (866) 477-4776). All other clients may

contact their local brokerage representative. Third-party

distributors may contact Morgan Stanley Structured Investment Sales at

(800) 233-1087.

|

|

Syndicate

Information

|

|

|

|

Issue price of the PLUS

|

Selling concession

|

Principal amount

of PLUS for any

single investor

|

|

$10.00

|

$0.15

|

<$999K

|

|

$9.975

|

$0.125

|

$1MM-$2.99MM

|

|

$9.9625

|

$0.1125

|

$3MM-$4.99MM

|

|

$9.95

|

$0.10

|

>$5MM

|

Selling

concessions allowed to dealers in connection with the offering may be reclaimed

by the agent, if, within 30 days of the offering, the agent repurchases the PLUS

distributed by such dealers.

This

offering summary represents a summary of the terms and conditions of the

PLUS. We encourage you to read the accompanying prospectus supplement

for PLUS and prospectus related to this offering, which can be accessed via the

hyperlinks on the front page of this document.

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

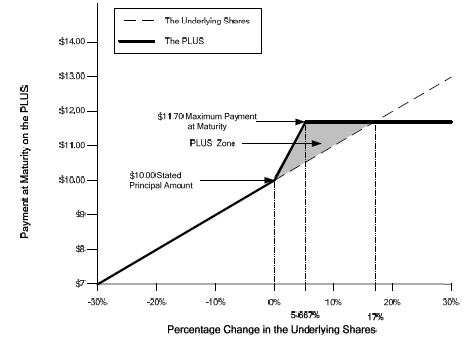

How PLUS Work

Payoff Diagram

The

payoff diagram below illustrates the payment at maturity on the PLUS based on

the following terms:

|

Stated principal

amount:

|

$10

|

|

Leverage

factor:

|

300%

|

|

Hypothetical maximum payment at

maturity:

|

$11.70 (117%

of the stated principal amount)

|

How it works

|

§

|

If the final

share price is greater than the initial share price, then investors

receive the $10 stated principal amount plus 300% of the appreciation of

the underlying shares over the term of the PLUS, subject to the

hypothetical maximum payment at maturity. In the payoff

diagram, an investor will realize the hypothetical maximum payment at

maturity at a final share price of approximately 105.667% of the initial

share price.

|

|

§

|

If the

underlying shares appreciate 5%, the investor would receive a 15% return,

or $11.50.

|

|

§

|

If the

underlying shares appreciate 25%, the investor would receive the

hypothetical maximum payment at maturity of 117% of the stated principal

amount, or $11.70.

|

|

§

|

If the final

share price is less than or equal to the initial share price, the investor

would receive an amount less than or equal to the $10 stated principal

amount, based on a 1% loss of principal for each 1% decline in the price

of the underlying shares.

|

|

§

|

If the

underlying shares depreciate 10%, the investor would lose 10% of their

principal and receive only $9 at maturity, or 90% of the stated principal

amount.

|

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

Payment at Maturity

At

maturity, investors will receive for each $10 stated principal amount of PLUS

that they hold an amount in cash based upon the price of the underlying shares,

determined as follows:

If

the final

share price

of the underlying shares

is greater than the initial

share price

of the underlying shares:

$10 + Leveraged Upside

Payment:

subject to the maximum payment at maturity

for each PLUS,

If

the final

share price

of the underlying shares

is less than or equal to the initial

share price

of the underlying shares:

$10 X Share

Performance Factor

Because the share

performance factor will be less than or equal to 1.0, this payment will be less

than or equal to $10.

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

The

following is a non-exhaustive list of certain key risk factors for investors in

the PLUS. For further discussion of these and other risks, you should

read the section entitled “Risk Factors” beginning on page S-18 of the

prospectus supplement for PLUS. We also urge you to consult your

investment, legal, tax, accounting and other advisers before you invest in the

PLUS.

Structure Specific Risk

Factors

|

§

|

PLUS do not pay interest nor

guarantee return of principal. The terms of the PLUS

differ from those of ordinary debt securities in that the PLUS do not pay

interest nor guarantee payment of the principal amount at

maturity. If the final share price is less than the initial

share price, the payout at maturity will be an amount in cash that is less

than the $10 stated principal amount of each PLUS by an amount

proportionate to the decrease in the price of the underlying

shares.

|

|

§

|

Appreciation potential is

limited. The appreciation potential of PLUS is limited

by the maximum payment at maturity of $11.60 to $11.80, or 116% to

118% of the stated principal amount. Although the leverage

factor provides 300% exposure to any increase in the price of the

underlying shares at maturity, because the payment at maturity will be

limited to 116% to 118% of the stated principal amount for the PLUS, the

percentage exposure provided by the leverage factor is progressively

reduced as the final share price exceeds approximately 105.333% to 106% of

the initial share price.

|

|

§

|

Market price influenced by many

unpredictable factors. Several factors will influence

the value of the PLUS in the secondary market and the price at which MS

& Co. may be willing to purchase or sell the PLUS in the secondary

market, including: the value, volatility and dividend yield of the

Palisades Water Index, interest and yield rates, time remaining to

maturity, geopolitical conditions and economic, financial, political and

regulatory or judicial events and creditworthiness of the

issuer.

|

|

§

|

There are risks associated with

investments in securities with concentration in a single

sector. The stocks included in the Palisades Water Index

and that are generally tracked by the underlying shares are stocks of

companies involved in the provision of potable water, water treatment, and

technology and services that are directly related to water

consumption. Companies involved in the water industry are

subject to environmental considerations, taxes, government regulation,

price and supply fluctuations, competition and water

conservation.

|

|

§

|

Several of the components of the Palisades Water Index are small or

medium-sized companies. Investing in securities of small and

medium-sized companies involves greater risk than is generally associated

with investing in more established companies. These companies’

stocks may be more volatile and less liquid than those of more established

companies. These stocks may have returns that vary, sometimes

significantly, from the overall stock market. Often smaller and medium

capitalization companies and the industries in which they are focused are

still evolving and this may make them more sensitive to changing market

conditions.

|

|

§

|

Adjustments to the underlying

shares or to the Palisades Water Index could adversely affect the value of

the PLUS. PowerShares Capital Management LLC is the

investment adviser to the PowerShares Water Resources Portfolio, which

seeks investment results that correspond generally to the price and yield

performance, before fees and expenses, of the Palisades Water

Index. Palisades Water Index Associates, LLC is responsible for

calculating and maintaining the Palisades Water

Index. Palisades Water Index Associates, LLC can add, delete or

substitute the stocks underlying the Palisades Water Index or make other

methodological changes that could change the value of the Palisades Water

Index. Pursuant to its investment strategy or otherwise,

PowerShares Capital Management LLC may add, delete or substitute the

stocks composing the PowerShares Water Resources Portfolio. Any

of these actions could adversely affect the price of the underlying shares

and, consequently, the value of the

PLUS.

|

|

§

|

Not equivalent to investing in

the underlying shares. Investing in the PLUS is not

equivalent to investing in the underlying shares or the Palisades Water

Index. Investors in the PLUS will not have voting rights or

rights to receive dividends or other distributions or any other rights

with respect to the underlying shares or the stocks that constitute the

Palisades Water Index.

|

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

|

§

|

The underlying shares and the

Palisades Water Index are different. The performance of

the underlying shares may not exactly replicate the performance of the

Palisades Water Index because the PowerShares Water Resources Portfolio

will reflect transaction costs and fees that are not included in the

calculation of the Palisades Water Index. It is also possible

that the PowerShares Water Resources Portfolio may not fully replicate or

may in certain circumstances diverge significantly from the performance of

the Palisades Water Index due to the temporary unavailability of certain

securities in the secondary market, the performance of any derivative

instruments contained in this fund or due to other circumstances.

PowerShares Capital Management LLC may invest up to 10% of the PowerShares

Water Resources Portfolio’s assets in securities not in the Palisades

Water Index which PowerShares Capital Management LLC believes are

appropriate to substitute for certain securities in the Palisades Water

Index or utilize various combinations of other available investment

techniques, in seeking to track the Palisades Water

Index.

|

|

§

|

The antidilution adjustments

the calculation agent is required to make do not cover every event that

could affect the underlying shares. MS & Co., as

calculation agent, will adjust the amount payable at maturity for certain

events affecting the underlying shares. However, the

calculation agent will not make an adjustment for every event that could

affect the underlying shares. If an event occurs that does not

require the calculation agent to adjust the amount payable at maturity,

the market price of the PLUS may be materially and adversely

affected.

|

|

§

|

The inclusion of commissions

and projected profit from hedging in the original issue price is likely to

adversely affect secondary market prices. Assuming no

change in market conditions or any other relevant factors, the price, if

any, at which MS & Co. is willing to purchase PLUS in secondary market

transactions will likely be lower than the original issue price, since the

original issue price included, and secondary market prices are likely to

exclude, commissions paid with respect to the PLUS, as well as the

projected profit included in the cost of hedging the issuer’s obligations

under the PLUS. In addition, any such prices may differ from

values determined by pricing models used by MS & Co., as a result of

dealer discounts, mark-ups or other transaction

costs.

|

|

§

|

The U.S. federal income tax

consequences of an investment in the PLUS are

uncertain. Please read the discussion under “Fact Sheet

― General

Information ― Tax

Considerations” in this document and the discussion under “United States

Federal Taxation” in the accompanying prospectus supplement for PLUS

(together the “Tax Disclosure Sections”) concerning the U.S. federal

income tax consequences of an investment in the PLUS. If the

Internal Revenue Service (the “IRS”) were successful in asserting an

alternative characterization or treatment, the timing and character of

income on the PLUS

might differ significantly from the tax treatment described in the Tax

Disclosure Sections. For example, as discussed in the Tax

Disclosure Sections, there is a substantial risk that the “constructive

ownership” rule could apply, in which case all or a portion of any

long-term capital gain recognized by a U.S. Holder might be

recharacterized as ordinary income (which ordinary income would also be

subject to an interest charge). Under another characterization,

U.S. Holders could be required to accrue original issue discount on the

PLUS every year at a

“comparable yield” determined at the time of issuance and recognize all

income and gain in respect of the PLUS as ordinary

income. The issuer does not plan to request a ruling from the

IRS regarding the tax characterization or treatment of the PLUS, and the IRS or a

court may not agree with the tax characterization and treatment described

in the Tax Disclosure Sections. On December 7, 2007, the

Treasury Department and the IRS released a notice requesting comments on

the U.S. federal income tax treatment of “prepaid forward contracts” and

similar instruments, such as the PLUS. The notice

focuses in particular on whether to require holders of these instruments

to accrue income over the term of their investment. It also

asks for comments on a number of related topics, including the character

of income or loss with respect to these instruments; whether short-term

instruments should be subject to any such accrual regime; the relevance of

factors such as the exchange-traded status of the instruments and the

nature of the underlying property to which the instruments are linked; the

degree, if any, to which income (including any mandated accruals) realized

by non-U.S. investors should be subject to withholding tax; and whether

these instruments are or should be subject to the “constructive ownership”

regime. While the notice requests comments on appropriate

transition rules and effective dates, any Treasury regulations or other

guidance promulgated after consideration of these issues could materially

and adversely affect the tax consequences of an investment in the PLUS, possibly with

retroactive effect. Both U.S. and Non-U.S. Holders should

consult their tax advisers regarding the U.S. federal income tax

consequences of an investment in the PLUS, including possible

alternative characterizations or treatments, the potential application of

the constructive ownership regime, the issues presented by this notice and

any tax consequences arising under the laws of any state, local or foreign

taxing jurisdiction.

|

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

Other

Risk Factors

|

§

|

Secondary trading may be

limited. The PLUS will not be listed on any securities

exchange. Therefore, there may be little or no secondary market

for the PLUS. Even if there is a secondary market, it may not

provide significant liquidity. Accordingly, you should be

willing to hold your PLUS to

maturity.

|

|

§

|

Potential adverse economic

interest of the calculation agent. The hedging or

trading activities of the issuer’s affiliates on or prior to the pricing

date and prior to maturity could adversely affect the price of the

underlying shares and, as a result, could decrease the amount an investor

may receive on the PLUS at maturity. Any of these hedging or

trading activities on or prior to the pricing date could potentially

affect the initial share price and, therefore, could increase the price at

which the underlying shares must close before an investor receives a

payment at maturity that exceeds the issue price of the

PLUS. Additionally, such hedging or trading activities during

the term of the PLUS, including on the valuation date, could potentially

affect the price of the underlying shares on the valuation date and,

accordingly, the amount of cash an investor will receive at

maturity.

|

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

Information about the Underlying

Shares

The

PowerShares Water

Resources Portfolio

The

PowerShares Water Resources Portfolio is an exchange-traded fund managed by The

PowerShares Exchange-Traded Fund Trust (the “Trust”), a registered investment

company, which seeks investment results that correspond generally to the price

and yield performance, before fees and expenses, of the Palisades Water

Index. It is possible that this fund may not fully replicate the

performance of the Palisades Water Index due to the temporary unavailability of

certain securities in the secondary market or due to other extraordinary

circumstances. Information provided to or filed with the Securities and Exchange

Commission (the “Commission”) by the Trust pursuant to the Securities Act of

1933 and the Investment Company Act of 1940 can be located by reference to

Commission file numbers 333-102228 and 811-21265, respectively, through the

Commission’s website at http://www.sec.gov. In addition, information

may be obtained from other sources including, but not limited to, press

releases, newspaper articles and other publicly disseminated

documents. We make no representation or warranty as to the accuracy

or completeness of such information.

These preliminary

terms relate only to the PLUS offered hereby and do not relate to the underlying

shares. We have derived all disclosures contained in this preliminary

terms regarding the Trust from the publicly available documents described in the

preceding paragraph. In connection with the offering of the PLUS,

neither we nor the Agent has participated in the preparation of such documents

or made any due diligence inquiry with respect to the Trust. Neither we nor the

Agent makes any representation that such publicly available documents or any

other publicly available information regarding the Trust is accurate or

complete. Furthermore, we cannot give any assurance that all events occurring

prior to the date hereof (including events that would affect the accuracy or

completeness of the publicly available documents described in the preceding

paragraph) that would affect the trading price of the underlying shares (and

therefore the price of the underlying shares at the time we price the PLUS) have

been publicly disclosed. Subsequent disclosure of any such events or

the disclosure of or failure to disclose material future events concerning the

Trust could affect the value received at maturity with respect to the PLUS and

therefore the trading prices of the PLUS.

Neither we nor any

of our affiliates makes any representation to you as to the performance of the

underlying shares.

We and/or our

affiliates may presently or from time to time engage in business with the

Trust. In the course of such business, we and/or our affiliates may

acquire non-public information with respect to the Trust, and neither we nor any

of our affiliates undertakes to disclose any such information to

you. In addition, one or more of our affiliates may publish research

reports with respect to the underlying shares. The statements in the

preceding two sentences are not intended to affect the rights of investors in

the PLUS under the securities laws. As a prospective purchaser of the

PLUS, you should undertake an independent investigation of the Trust as in your

judgment is appropriate to make an informed decision with respect to an

investment in the underlying shares.

PowerShares® is a

registered mark of PowerShares Capital Management, LLC (“PCM”). The

PLUS are not sponsored, endorsed, sold, or promoted by PCM. PCM makes

no representations or warranties to the owners of the securities or any member

of the public regarding the advisability of investing in the

PLUS. PCM has no obligation or liability in connection with the

operation, marketing, trading or sale of the PLUS.

The

Palisades Water

Index

The Palisades Water

Index (the “Index”) is a modified equal-dollar weighted index comprised of

publicly traded companies whose businesses focus on the provision of potable

water, the treatment of water and technology and services that are directly

related to water consumption. The Index is rebalanced each March,

June, September and December. The Index divisor was initially determined to

yield a benchmark value of 1,000.00 at the close of trading December 31, 2003.

The Index was created by and is a trademark of Palisades Water Index Associates,

LLC. We have derived all information contained in these preliminary

terms regarding the Palisades Water Index including, without limitation, its

make-up, method of calculation and changes in its components, from publicly

available information, and we have not participated in the preparation of, or

verified, such publicly available information. Such information

reflects the policies of, and is subject to change by, Palisades Water Index

Associates, LLC. See “The Palisades Water Index” in Annex A to these

preliminary terms for more information.

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

Historical

Information

The

following table presents the published high, low and end-of-quarter closing

share prices for each quarter in the period from December 6, 2005, the date of

inception for the PowerShares Water Resources Portfolio, through August 19,

2008. The closing share price on August 19, 2008 was

$21.89. The issuer obtained the closing share prices and other

information below from Bloomberg Financial Markets, without independent

verification. You should not take the historical closing share prices

as an indication of future performance.

|

PowerShares Water Resources

Portfolio

|

High

|

Low

|

Period

End

|

|

2005

|

|

|

|

|

Fourth Quarter

(from December 6, 2005)

|

15.78

|

15.20

|

15.20

|

|

2006

|

|

|

|

|

First

Quarter

|

18.19

|

15.41

|

18.08

|

|

Second

Quarter

|

18.92

|

15.69

|

16.67

|

|

Third

Quarter

|

17.27

|

15.42

|

16.91

|

|

Fourth

Quarter

|

18.66

|

16.67

|

18.41

|

|

2007

|

|

|

|

|

First

Quarter

|

19.37

|

17.84

|

18.69

|

|

Second

Quarter

|

20.95

|

18.74

|

20.92

|

|

Third

Quarter

|

21.97

|

19.68

|

21.35

|

|

Fourth

Quarter

|

22.53

|

20.41

|

21.40

|

|

2008

|

|

|

|

|

First

Quarter

|

21.48

|

18.15

|

19.24

|

|

Second

Quarter

|

22.94

|

19.47

|

20.71

|

|

Third Quarter

(through August 19, 2008)

|

22.63

|

19.36

|

21.89

|

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

Annex A

The

Palisades Water

Index

The

Palisades Water Index (the “Index”) is a modified equal-dollar weighted index

comprised of U.S. exchange traded companies whose business stands to benefit

significantly from the quantity and/or quality issues associated with the global

provision of clean drinking water. The Index is rebalanced each March, June,

September and December. The Index divisor was initially determined to yield a

benchmark value of 1000.00 at the close of trading December 31, 2003. The Index

was created by and is a trademark of Palisades Water Index Associates, LLC (the

“Index Provider”).

Sector

Definitions

Water Utilities: Water

utilities are the regulated purveyors of water responsible for getting water

supplies to residential, commercial and industrial users. As public utilities,

they are under the jurisdiction of regulatory bodies and must comply with

federal and state regulatory requirements to ensure the safety of drinking water

and the protection of the environment. Foreign water utilities may operate under

different regulatory frameworks than U.S. water utilities. The investor-owned

water utilities included in the index generally oversee the water and wastewater

facilities for a specific geographical region or are structured as holding

companies comprised of geographically diverse operating divisions.

Treatment: Treatment refers to

the application of technologies and/or processes that alter the composition of

water to achieve a beneficial objective in its use. Water treatment specifically

refers to the process of converting source water to drinking water of sufficient

quality to comply with applicable regulations or to treat water in the

optimization of an industrial process. Wastewater treatment, though extricably

linked to the provision of potable water and sanitation, can be differentiated

within the treatment category by the objective of environmental protection. The

treatment category, therefore, comprises those companies that play a key role in

the physical, chemical or biological integrity of water and wastewater supplies.

While conventional centralized water and wastewater treatment equipment is the

core of the treatment group, advanced treatment methods, enabling convergent

technologies and innovative treatment systems are key drivers. Subsectors

include chemicals/media, filtration/separation, disinfection, desalination, and

decentralized technologies such as point-of-use (POU) or point-of-use-reuse

(POUR) applications.

Analytical/Monitoring: The

Analytical Group includes companies that provide services, manufacture

instrumentation or develop techniques for the analysis, testing or monitoring of

water and/or wastewater quality parameters. These analytics are applied to,

directly or indirectly, achieve either a mandated compliance requirement or a

management objective in optimizing the function of water relative to a specific

use, whether municipal or industrial. The group is driven by the convergence of

materials technologies, information technologies (protocol algorithms), sensor

technologies and advanced electronics.

Infrastructure/Distribution:

This category includes the companies that stand to benefit from the

construction, replacement, repair and rehabilitation of water distribution

systems, wastewater systems, and stormwater collection systems throughout the

world. Companies within the group service and supply the components

of the vast interconnected network of pipelines, mains, pumps, storage tanks,

lift stations, and smaller appurtenances of a distribution system such as valves

and flow meters. The group also includes the rehabilitation market comprised of

‘in-situ’ technologies utilized to upgrade, maintain and restore pipe networks

as a cost-effective alternative to new construction.

Water Resource Management:

Water resource management is a service-oriented approach to the integration of

the economic principles of resource sustainability with global water usage. This

group includes companies that provide engineering, construction, operations, and

related technical services to public and private customers in virtually all

aspects of managing water resources, agricultural irrigation, and privatization

activities.

Conglomerates: The

Conglomerates sector comprises those companies that contribute significantly to

the water industry yet are extensively diversified into other industries or

markets such that the contribution of water-related

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

activities is

relatively small. Conglomerates are reviewed on a case-by-case basis. These

companies may not be conglomerates in the traditional sense but may have instead

sought to apply a particular platform technology, product-line or service

capability across several global markets, including water. While companies

classified in other index sectors may be said to be engaged in the water

industry when viewed externally, the conglomerates sector contains leading

companies that have business brands or activities that are widely recognized

from within the water industry.

Eligibility

Criteria for Index Components

The Index includes

companies that focus on the provision of potable water, the treatment of water

and wastewater for municipal, agricultural and industrial processes and the

technologies and services that are directly related to water consumption across

applications that are listed on the New York Stock Exchange, American Stock

Exchange, or quoted on the Nasdaq National Market System. To be included in the

Index, new index components must meet the following criteria each Determination

Date:

• Market

capitalization is at least $150 million.

• Traded

volume greater than 100,000 shares for each of the prior three

months.

• A

minimum Average Daily Traded Volume (ADTV) of at least $500,000 for the prior

three months.

The Index Provider

may at any time and from time to time change the number of issues comprising the

Index by adding or deleting one or more components or sectors, or replacing one

or more issues contained in the Index with one or more substitute stocks of its

choice, if, in the Index Provider’s discretion, such addition, deletion or

substitution is necessary or appropriate to maintain the quality and/or

character of the industry groups to which the Index relates.

Calculation

Methodology

The Index is

calculated using a modified equal weighting methodology. Component securities

are equally weighted within their respective Sector. Each Sector is assigned an

aggregate weight within the index. Sector weightings were initially determined

by the Index Provider and are reviewed each quarter in conjunction with the

scheduled quarterly review of the Index. Within each sector the component

weightings cannot exceed five percent (5%) of the Index. As of December 31,

2007, the Sectors are weighted as follows:

|

Sector Name

|

Sector

Weight

|

|

Water

Utilities

|

9%

|

|

Treatment

|

17%

|

|

Analytical/Montoring

|

15%

|

|

Infrastructure/Distribution

|

22%

|

|

Conglomerates

|

12%

|

|

Resource

Management

|

25%

|

|

Total

|

100%

|

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

Quarterly

Updates to the Index

The component

weights will be determined and announced at the close of trading two days prior

to the Rebalance Date. The Index components are determination five days prior to

the Rebalance Date. For a component to remain in the Index, the component must

meet the following continued inclusion rules:

•

Maintain a total market capitalization above $100 million on the

determination date.

•

Maintain traded volume greater than 100,000 shares for each of the prior

three months.

•

Maintain a minimum Average Daily Traded Volume (ADTV) of at least $500,000

for the prior three months.

In conjunction with

the quarterly review, the share weights used in the calculation of the Index are

updated based upon newly assigned Sector weights and index component prices as

of the close of trading two business days prior to the Rebalance Date. The share

weight of each component in the Index portfolio remains fixed between quarterly

reviews except in the event of certain types of corporate actions such as

splits, reverse splits, stock dividends, or similar events.

Maintenance

of the Index

In the event of a

merger between two components, the share weight of the surviving entity may be

adjusted to account for any shares issued in the acquisition. The Index Provider

may substitute components or change the number of issues included in the index,

based on changing conditions in the industry or in the event of certain types of

corporate actions, including mergers, acquisitions, spin-offs, and

reorganizations. In the event of component or share weight changes to the Index

portfolio, the payment of dividends other than ordinary cash dividends,

spin-offs, rights offerings, re-capitalization, or other corporate actions

affecting a component of the Index; the Index divisor may be adjusted to ensure

that there are no changes to the Index level as a result of non-market

forces.

PLUS based on the PowerShares Water Resources

Portfolio due October 20, 2009

Performance Leveraged Upside

SecuritiesSM

The table below sets

out the sectors composing the Index and the component stocks currently included

within each sector as of the August 19, 2008. The table below sets

forth the components and weightings in the Index, which may differ from the

components’ weightings in the PowerShares Water Resources

Portfolio:

|

Components

|

Component Ticker

Symbols

|

Component

Country

|

Weighting

|

|

Tetra Tech,

Inc.

|

TTEK

|

USA

|

4.55%

|

|

Badger

Meter

|

BMI

|

USA

|

4.11%

|

|

Urs

Corp.

|

URS

|

USA

|

4.05%

|

|

Itron

Inc.

|

ITRI

|

USA

|

4.01%

|

|

Danaher

Corp.

|

DHR

|

USA

|

3.96%

|

|

Aecom

Technology Corp.

|

ACM

|

USA

|

3.95%

|

|

Veolia

Environnement

|

VE

|

France

|

3.89%

|

|

Calgon

Carbon

|

CCC

|

USA

|

3.88%

|

|

Lindsay

Manufacturing Co.

|

LNN

|

USA

|

3.80%

|

|

Valmont

Industries, Inc.

|

VMI

|

USA

|

3.74%

|

|

Agilent

Technologies

|

A

|

USA

|

3.69%

|

|

Pentair,

Inc.

|

PNR

|

USA

|

3.48%

|

|

Mueller Water

Products Inc.

|

MWA

|

USA

|

3.48%

|

|

ITT

Industries

|

ITT

|

USA

|

3.39%

|

|

Watts Water

Technologies Inc.

|

WTS

|

USA

|

3.39%

|

|

Ameron

International Corp

|

AMN

|

USA

|

3.26%

|

|

Pall

Corp

|

PLL

|

USA

|

3.22%

|

|

Nalco Holding

Co.

|

NLC

|

USA

|

3.15%

|

|

Insituform

Technologies

|

INSU

|

USA

|

3.12%

|

|

General

Electric Co.

|

GE

|

USA

|

2.97%

|

|

Flowserve

Corp.

|

FLS

|

USA

|

2.91%

|

|

Franklin

Electric Co. Inc.

|

FELE

|

USA

|

2.87%

|

|

Idex

Corp.

|

IEX

|

USA

|

2.86%

|

|

Siemens

Aktiengesellschaft

|

SI

|

Germany

|

2.81%

|

|

Layne

Christensen Co.

|

LAYN

|

USA

|

2.75%

|

|

Gorman-Rupp

Co.

|

GRC

|

USA

|

2.66%

|

|

Roper

Industries Inc.

|

ROP

|

USA

|

2.57%

|

|

Consolidated

Water Co. Inc.

|

CWCO

|

Cayman

Islands

|

1.51%

|

|

America States

Water

|

AWR

|

USA

|

1.32%

|

|

Southwest

Water Co.

|

SWWC

|

USA

|

1.30%

|

|

Aqua

America

|

WTR

|

Brazil

|

1.23%

|

|

American Water

Works

|

AWK

|

USA

|

1.06%

|

|

Companhia de

Saneamento Basico do Estado de Sao Paulo

|

SBS

|

Brazil

|

1.03%

|