__________________________________________________________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

(Mark One) For the fiscal Or For the transaction period from ___________ to _________ Commission File No (Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.) (Address of principal executive offices, Zip Code) Securities registered pursuant to Section 12(b) of the Exchange Act: (Title of each class) Securities registered pursuant to Section 12(g) of the Exchange Act: Title of each class Trading Symbol(s) Name of each exchange on which registered Common Stock, $0.002 par value Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o Yes x Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes x Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). 1

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer Smaller reporting company Emerging growth company If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. o Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). The aggregate market value of the voting 2

TABLE OF CONTENTS Cautionary Note Regarding Forward-Looking Statements Page PART I ITEM 1: 6 ITEM 1A: 12 ITEM 1B: 24 ITEM 2: 24 ITEM 3: 38 ITEM 4: 39 PART II ITEM 5: MARKET FOR COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND PURCHASES OF EQUITY SECURITIES 39 ITEM 6: 41 ITEM 7: MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION 41 ITEM 7A: 45 ITEM 8: 46 ITEM 9: CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE 71 ITEM 9A: 71 ITEM 9B: 73 PART III ITEM 10: 73 ITEM 11: 74 ITEM 12: SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS 75 ITEM 13: CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE 76 ITEM 14: 76 PART IV ITEM 15: 77 ITEM 16: 77 78 3

Unless the context requires otherwise, references to “Santa Fe Gold,” “Santa Fe,” “we,” “us,” “our” and the “Company” refer to Santa Fe Gold Corporation and its consolidated subsidiaries. ADDITIONAL INFORMATION Descriptions of agreements or other documents contained in this Annual Report filed on Form 10-K are intended as summaries and are not necessarily complete. Please refer to the agreements or other documents filed or incorporated herein and furnished herewith as exhibits for more complete descriptions of the terms and conditions set forth therein. Please see the exhibit index at the end of this report for a complete list of those exhibits. CAUTIONARY STATEMENT ON FORWARD-LOOKING STATEMENTS This Annual Report may contain certain “forward-looking” statements as such term is defined by the Commission in its rules, regulations and releases, which represent the Company’s expectations or beliefs, including but not limited to, statements concerning the registrant’s operations, economic performance, financial condition, growth and acquisition strategies, investments, and future operational plans. For this purpose, any statements contained herein that are not statements of historical fact may be deemed to be forward-looking statements. Without limiting the generality of the foregoing, words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intent,” “could,” “estimate,” “might,” “plan,” “predict,” “strategy” or “continue” or the negative or other variations thereof or comparable terminology are intended to identify forward-looking statements. This information may involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance, or achievements to be materially different from the future results, performance or achievements expressed or implied by any forward-looking statements. Forward-looking statements, many assuming that the Company secures adequate financing and is able to continue as a going concern,

important factors that could prevent us from achieving objectives include but are not limited to those set forth in other “Risk Factors” section in this report and the following:

·our ability to continue as a going concern;

·our ability to acquire financing to allow us to remain in business

·our anticipated cash requirements and the availability for current projects and financing thereof;

·projections regarding capital costs, expenditures, potential revenues, operating costs, production and economic returns may differ significantly from those that we have anticipated;

·our ability to secure permits or other regulatory approvals to operate or explore our mineral properties;

·exposure to all of the risks associated with mining operations, if any development of one or more of our projects is found to be economically feasible;

·title to some of our mineral properties may be uncertain or defective;

·land reclamation and mine closure may be burdensome and costly;

·significant risk and hazards associated with mining operations;

·the requirements that we obtain, maintain and renew environmental, construction and mining permits, which is often a costly and time-consuming process and may be opposed by local environmental group;

·

·claims

4

·our lack of necessary financial resources to complete development of our projects and the uncertainty of our future best

·our exposure to material costs, liabilities and obligations as a result of environmental laws and regulations (including changes thereto) and permits;

·changes in the price of silver and gold;

·extensive regulation by the U.S. government as well as state and local governments;

·

·our growth strategies,

·anticipated trends in our industry;

·unfavorable weather conditions;

·the commercial and economic viability of any mines;

·availability of labor, materials and equipment;

·the volatility in the market price of our stock;

·our ability to acquire and retain key mining personnel to effectively operate and move forward the Company; ·failure of equipment to process or operate in accordance with specifications, including expected throughput, which could prevent the production of commercially viable output; and ·our ability to seek out and acquire high quality gold Actual events or results may differ materially from those discussed in forward-looking statements 5

PART I

Overview We are As an exploration mining company, we are engaged in the business of acquiring and developing mines and mining properties as well as securing production from existing and developed mining and mineral properties. Currently we own certain mining leases and other mineral rights, however none of them contain any proven or probable reserves, as defined in Regulation S-K 1300; and they are all currently considered “exploratory” in nature. Currently we have three projects, each of which management has determined is “material” based on the costs to secure the rights associated with them, as required by Regulation S-K 1304, these are: our Alhambra Property, the Jim Crow Imperial Mine and the Billali Mine, each of which are exploratory in nature and is described more fully in the properties section of this report. Although management is optimistic about its plans for developing certain such properties, to date, minimal mining activities have commenced at the Jim Crow Imperial Mine and the Billali Mine sites and there can be no assurance After the dismissal from bankruptcy in June 2016, we had no assets and approximately $20 million of indebtedness was reinstated. The properties we currently own were acquired subsequent to our dismissal from bankruptcy proceedings. We We are considered an exploration stage company, as defined in S-K 1300. The Company has not demonstrated the existence of mineral reserves at any of our properties. Under Regulation S-K 1300, the SEC defines a “mineral reserve” as “an estimate of tonnage and grade or quality of indicated and measured mineral resources that, in the opinion of the qualified person, can be the basis of an economically viable project.” To have mineral resources, there must be reasonable prospects for economic extraction. Per the SEC, “probable mineral reserves” are the economically mineable part of an indicated and, in some cases, a measured mineral resource and “proven mineral reserves” can only result from measured mineral resources. Mineral reserves cannot be considered proven or probable unless and until they are supported by a preliminary feasibility study or feasibility study, indicating that the mineral reserves have had the requisite geologic, technical and economic work performed and are economically and legally extractable. We have not completed a preliminary feasibility study or feasibility study with regard to any of our properties to date. We do not anticipate leaving exploration stage company for the foreseeable future. Under S-K we will not exit the exploration stage until such time, if ever, that we demonstrate the existence of proven or probable mineral reserves that meet the guidelines under S-K 1300. When we begin extracting material from our properties, we will remain an exploration company under S-K 1300 guidelines. 6

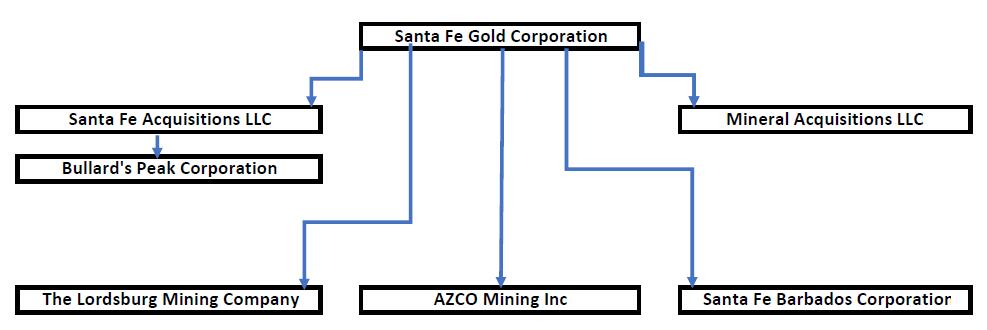

Company Organizational Chart Overview of Current Events Our Business As a mining company in the exploration stage, we are engaged in the business of acquiring mineral properties that may contain recoverable mineral deposits, (we are currently targeting gold and/or silver deposits) with a view to develop them and, if there are mineral resources identified or mineral reserves, to actively mine them. Although management is optimistic about its prospects for favorable exploration results on the properties in which it has acquired interests, to date no mineral reserves have been determined. There are however minimal mining activities that have commenced and we have conducted limited extraction activity. Nevertheless, there can be no assurance it will continue or, that if it does, that any of the mining activities will be profitable, with or without mineral reserves. Management’s continuing efforts were successfully rewarded as the Company secured, what management believes will ultimately be, promising mining leases and other mineral rights. The properties we now own are exploratory in nature and consist of certain mining leases and other mineral rights. As stated, they were acquired subsequent to our dismissal from bankruptcy proceedings and, although management is optimistic, none of them contain any proven and probable reserves. In October 2021, we exercised the purchase option for $164,335 on the mill property in Duncan, Arizona, and the transaction closed on November 9, 2021. The Company is currently in the process of acquiring a mill operation for its head ore to be located on its property in Duncan, Arizona. The seller of the mill has disassembled the mill in Kellogg, Idaho and relocated the mill to the Duncan, Arizona site. Currently all associated costs of the mill and its relocation are being accumulated and finalized by the seller. At this time there are no agreements between the seller and the Company as to terms and sales price of the delivered disassembled mill and such price is anticipated to be negotiated and determined in late fall 2022, when the necessary funding will be raised by the Company for the acquisition of the mill equipment and its construction. At the time of filing this Form 10-K, negotiations for the purchase of the disassembled mill with the seller have not taken place and will be finalized upon the Company raising the adequate funding for the acquisition and determination if the seller or the Company will be responsible for its The Company 7

Ultimately, while the underlying circumstances that gave rise to the Company’s delinquent filings were, in part, caused by an individual who was dismissed upon discovery of On May 14, 2022, the Company filed a Form 10-12G Registration statement with the SEC and was withdrawn by the Company on July 12, 2021 due to comments not completely cleared by the SEC. On July 20, 2021, we refiled a new Form 10-12G and on September 17, 2021 we withdrew the filing due to SEC comments requiring financial restatements. The Company made the required financial restatements and our auditors recertified the audited financial statements and we submitted a new Form 10-12G on June 14, 2022 and on August 4, 2022 the SEC declared our Form 10-12G Registration effective. Although the Company is not trading currently and we are a reporting Company under Section 12(g) of the Securities and Exchange Act of 1934, as amended and are required to timely file periodic and current reports with the SEC. The Company is working on securing a broker dealer to Competition The mining industry is highly competitive. We will be competing with numerous companies, substantially all of which have far greater resources available to them that we are likely to have when Compliance with Government Regulations Continuing to acquire and explore mineral properties in the State of New Mexico will require the Company to comply with all regulations, rules and directives of governmental authorities and agencies applicable to the exploration of minerals in the State of New Mexico and the United States. 8

The mining industry, (specifically the activities of exploration, drilling) operate in a legal environment that requires permits to conduct virtually all operations Local authorities, usually counties, also have control over mining activity. The various permits address such issues as prospecting, development, production, labor standards, taxes, occupational health and safety, toxic substances, air quality, water use, water discharge, water quality, noise, dust, wildlife impacts, as well as other environmental and socioeconomic issues. Like all other mining companies doing business in the United States, we are subject to a variety of federal, state and local statutes, rules and regulations designed to protect the quality of the air and water, and to protect threatened or endangered species, in the vicinity of our mining operations. These include “permitting” or “pre-operating approval” requirements that are designed: (i) to ensure the environmental integrity of a proposed mining facility, (ii) to ensure operating plans are designed to mitigate the effects of discharges into the environment during exploration, mining operations, and reclamation and (iii) that post-operation plans are designed to remediate the lands affected by a mining facility once commercial mining operations have ceased. United States Mining in the State of New Mexico is subject to federal, state and local law. Three types of laws are of particular importance to the Company’s U.S. mineral properties: those affecting land ownership and mining rights; those regulating mining operations; and those dealing with the environment.

Land Ownership On Federal Lands, mining rights are governed by the General Mining Law of 1872 (“General Mining Law”) as amended, 30 U.S.C. §§

Mining Operations The exploration of mining properties and development and operation of mines is governed by both federal and state laws. The State of New Mexico likewise requires various permits and approvals before mining operations can begin, although the state and federal regulatory agencies usually cooperate to minimize duplication of permitting efforts. The State of New Mexico Mining and Minerals Division requires mine permits for each mining location. The permit has an Annual Permit Fee that is due by April 30 of each year. The Annual Permit Fee for minimal impact mines is currently $250. Prior to receiving the necessary permits to explore or mine, the operator must comply with all regulatory requirements imposed by all governmental authorities having jurisdiction over the project. Effect of Existing or Potential Government Regulations

Mineral exploration, including mining operations 9

Environmental Laws Federal legislation in the United States and implementing regulations adopted and administered by the Environmental Protection Agency, the Forest Service, the Bureau of Land Management, the Fish and Wildlife Service, the Army Corps of Engineers and other agencies—in particular, legislation such as the federal Clean Water Act, the Clean Air Act, the National Environmental Policy Act, the Endangered Species Act, the National Forest Management Act, the Wilderness Act, and the Comprehensive Environmental Response, Compensation and Liability Act ‘have a direct bearing on domestic mining operations. These federal initiatives are often administered and enforced through state agencies operating under parallel state statutes and regulations. The Clean Water Act The Federal Clean Water Act is the principal Federal environmental protection law regulating mining operations in the United States as it pertains to water quality. At the state level, water quality is regulated by the New Mexico Environment Department. If our exploration or any future development activities could affect a ground water aquifer, we are required to apply for a ground water discharge permit in compliance with the groundwater regulations. If exploration affects surface water, then compliance with surface water regulations is required. The Clean Air Act The Federal Clean Air Act establishes ambient air quality standards, limits the discharges of new sources and hazardous air pollutants and establishes a federal air quality permitting program for such discharges. Hazardous materials are defined in the Federal Clean Air Act and enabling regulations adopted under the Federal Clean Air Act to include various metals. The Federal Clean Air Act also imposes limitations on the level of particulate matter generated from mining operations. National Environmental Policy Act (“NEPA”) NEPA requires all governmental agencies to consider the impact on the human environment of major federal actions as therein defined. Endangered Species Act (“ESA”) The ESA requires federal agencies to ensure that any action authorized, funded or carried out by such agency is not likely to jeopardize the continued existence of any endangered or threatened species or result in the destruction or adverse modification of their critical habitat. In order to facilitate the conservation of imperiled species, the ESA establishes an interagency consultation process. When a federal agency proposes an action that “may affect” a listed species, it must consult with the USFWS and must prepare a “biological assessment” of the effects of a major construction activity if the USFWS advises that a threatened species may be present in the area of the activity. National Forest Management Act The National Forest Management Act, as implemented through Title 36 of the Code of Federal Regulations, provides a planning framework for lands and resource management of the National Forests. The planning framework seeks to manage the National Forest System resources in a combination that best serves the public interest without impairment of the productivity of the land, consistent with the Multiple Use Sustained Yield Act of 1960. Wilderness Act The Wilderness Act of 1964 created a National Wilderness Preservation System composed of Federally owned areas designated by Congress as “wilderness areas” to be preserved for future use and enjoyment. The Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA”) CERCLA generally imposes joint and several liability, without regard to fault or legality of conduct, on classes of persons who are considered to be responsible for the release of a “hazardous substance” into the environment. These persons include the current owner or operator of a contaminated facility, a former owner or operator of the facility at the time of contamination and those persons that disposed or arranged for the disposal of the hazardous substance. Under CERCLA and comparable state statutes, such persons may be subject to strict joint and several liability for the costs of cleaning up the hazardous substances that have been released into the environment, for damages to natural resources and for the costs of certain health studies. In addition, it is not uncommon for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by the hazardous substances released into the environment. Governmental agencies or third parties may seek to hold the Company responsible under CERCLA and comparable state statutes for all or part of the costs to clean up sites at which such “hazardous substances” have been released. 10

The Resource Conservation and Recovery Act (“RCRA”) RCRA was designed and implemented to regulate the disposal of solid and hazardous wastes. It restricts solid waste disposal practices and the management, reuse or recovery of solid wastes and imposes substantial additional requirements on the subcategory of solid wastes that are determined to be hazardous. Like the Clean Water Act, RCRA provides for citizens’ suits to enforce the provisions of the law. National Historic Preservation Act The National Historic Preservation Act was designed and implemented to protect historic and cultural properties. Compliance with the Act is necessary where federal properties or federal actions are undertaken, such as mineral exploration on federal land, which may impact historic or traditional cultural properties, including native or Indian cultural sites. Reclamation We generally will be required to mitigate long-term environmental impacts by stabilizing, contouring, re-sloping and revegetating various portions of a site after mining and mineral processing operations are completed. These reclamation efforts would be conducted in accordance with detailed plans, which must be reviewed and approved by the appropriate regulatory agencies. As soon as we have a mining operation, we will be required to arrange and pledge certificates of deposits for reclamation with the state regulatory agencies. At this time no reclamation cost is required to be calculated or carried forward. Employees We currently have Employment Agreements Effective July 7, 2020, the Company retained a new Chief Financial Officer and the Insurance We normally maintain property, liability and workmen’s compensation insurance Exploration The Company has spent only nominal amounts during each of the last Seasonality We have no properties at this time that are subject to material restrictions on our operations due to seasonality. Office Facilities Our principal

11

Dismissal of Bankruptcy Proceeding and Emergence from Voluntary Reorganization

In August 2015, the Company filed for Bankruptcy protection under Chapter 11

After the dismissal

·The approximately $20 million of indebtedness outstanding on account of the Company’s

·The

The Company received Bankruptcy Court confirmation of the dismissal in June 2016, and subsequently emerged from bankruptcy. The only funds available for the future administrative costs were prepaid insurance funds of approximately $49,000. The Company subsequently began selling, on a best-efforts basis, equity for the cash needed for working capital purposes. Currently we have no continuing commitment from any party to provide working capital, and there is no certainty that the Company will be able to continue its current business plan.

Available Information

We make available, free of charge, on or through our Internet website, at www.santafegoldcorp.com, our annual report on Form 10-K, our quarterly reports on Form 10-Q and our current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the U.S. Securities Exchange Act of 1934. Our Internet website and the information contained therein or connected thereto are not intended to be, and are not, incorporated into this report on Form 10-K.

You can read our SEC filings, including this annual report as well as our other periodic and current reports, on the SEC’s website at www.sec.gov. You may also read and copy any document we file with the SEC at its public reference facilities at 100 F Street, N.E., Room 1580, Washington, D.C. 20549. You may also obtain copies of the documents at prescribed rates by writing to the Public Reference Section of the SEC at 100 F Street, N.E., Room 1580, Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the operation of the public reference facilities.

The Company operates in a rapidly changing environment that involves numerous risks and uncertainties involving precious metal prices, explorations costs and government oversight. Investors should carefully consider the risks described below before purchasing the Company’s common shares. The occurrence of any of the following events could negatively affect our business operations and our results of operations. If these events occur, the trading price of the Company’s common shares could decline, and shareholders may lose part or even all of their investment.

Risk Associated with Our Business

You should invest in our common stock only if you can afford to lose your entire investment. Your decision to invest in our common stock should only be made after you have knowingly accepted the possibilities of such a loss and the associated risks. 12

Risks Related to Our Business All of our properties are in the exploration stage. There can be no assurance that we will establish the existence of any mineral resource or We have not established that any of our mining properties contain The commercial viability of an established mineral deposit will depend on a large number of factors; including, by way of example, the size, grade and other attributes of the mineral Even if commercial viability of a mineral or metal deposit is established, we may be required to expend significant resources until production is possible, during which time the economic feasibility of production may change. Substantial expenditures are required to both establish proven and probable reserves as well as those required to implement permitting and drilling operations. Because of these uncertainties, investors have no assurances that our drilling programs will result in commercially viable operations nor that we will be successful in the establishment or expansion of any resources or reserves. Any failure in our ability to successfully execute on the forgoing will adversely impact our business results of operations, in turn leading to losses for investors. As the Company has adopted the required disclosure prescribed in Regulation S-K 1300 et. seq., the concept of a feasibility study is “mineral resources,” as the term under Reg. S-K 1300 means not only that there are mineral deposits present but that they have been determined to be economically viable for extraction. The mineral deposits on our properties have a great amount of uncertainty as to their existence, and great uncertainty as to their economic If we establish the existence of commercially viable mineral If we do discover mineral Our exploration and extraction activities may not be commercially successful. 13

While we believe there are positive indicators that our properties contain commercially exploitable minerals and metals, such belief has been based solely on preliminary tests that we have conducted and data provided by third parties. There can be no assurance that the tests and data upon which we have relied are correct or accurate. Moreover, mineral exploration is highly speculative in nature, involves many risks and is frequently non-productive. ·the identification of potential mineralization based on analysis; ·the availability of permits; ·compliance with environmental requirements; ·increases in operating mining related costs; ·the quality of our management and our geological and technical expertise; and ·the capital available for mining operations. Substantial expenditures and time are required to establish existing proven and probable reserves through drilling and analysis, and to develop the mines and facilities and infrastructure at any site chosen for mining. There may be challenges to the title of our mineral properties. The Company has acquired certain rights to its properties by unpatented claims, ownership of land or by lease from those owning the property and its patented claims are limited. The validity of title to many types of natural resource property depends upon numerous circumstances and factual matters (many of which are not discoverable of record or by other readily available means) and is subject to many uncertainties of existing law and its application. There can be no assurance that the validity of our titles to our properties will be upheld or that third parties will not otherwise seek to invalidate those rights. In the event the validity of our title to any of these properties are not upheld, such events would have a material adverse effect on us. Mineral operations are subject to applicable law and government regulations. Even if we discover a mineral resource in a commercially exploitable quantity, these laws and regulations could restrict or prohibit the exploitation of them. If we cannot exploit any mineral resources that we discover on our properties, our business may fail. Both mineral exploration and extraction require permits from various foreign, federal, state, provincial and local governmental authorities and are governed by laws and regulations, including those with respect to prospecting, mine development, mineral production, transport, export, taxation, labor standards, occupational health, waste disposal, toxic substances, land use, environmental protection, mine safety and other matters.

Companies, such as ours that plan to engage in exploration and extraction activities, often experience increased costs and delays in production and other schedules as a result of the need to comply with applicable laws, regulations and permits. Issuance of permits for our activities is subject to the discretion of government authorities, and we may be unable to obtain or maintain such permits. Permits required for future exploration or development may not be obtainable on reasonable terms, on a timely basis or at all. There can be no assurance that we will be able to obtain or maintain any of the permits required for the continued exploration or development of our mineral properties or for the construction and operation of a mine on our properties at economically viable costs. If we cannot accomplish these objectives, our business could face difficulty and/or fail.

We believe that we are in compliance with all material laws and regulations that currently apply to our activities but there can be no assurance that we can continue to do so. Current laws and regulations could be amended and we might not be able to comply with them, as amended. Further, there can be no assurance that we will be able to obtain or maintain all permits necessary for our future operations, or that we will be able to obtain them on reasonable terms. To the extent such approvals are required and are not obtained, we may be delayed or prohibited from proceeding with planned exploration or development of our mineral properties.

Environmental hazards unknown to us, which have been caused by previous or existing owners or operators of the properties, may exist on the properties in which we hold an interest.

14

Competition in the mining industry is intense, and we have limited financial and personnel resources with which to compete.

Competition in the mining industry for desirable properties, investment capital, equipment and personnel are intense. Numerous companies headquartered in the United States, Canada and elsewhere throughout the world compete for properties on a global basis, including areas where we intend to operate. We are currently an insignificant participant in the mining industry due, in part, to our limited financial and personnel resources. We may be unable to: i) attract the necessary investment capital or a joint venture partner to fully develop our mineral properties, ii) acquire other desirable properties, iii) attract and hire necessary personnel, or iv) purchase necessary equipment.

The nature of mineral exploration and production activities involves a high degree of risk and the possibility of uninsured losses.

The business of exploring for and extracting minerals and metals involves a high degree of risk. Few properties are ultimately developed into producing mines. Whether a mineral deposit can be commercially viable depends upon a number of factors, including the particular attributes of the deposit, including size, grade and proximity to infrastructure, metal prices, which can be highly variable, and government regulation, including environmental and reclamation obligations. These factors are not within our control. Uncertainties as to the metallurgical amenability of any minerals discovered may not warrant the mining of these metals or minerals on the basis of available technology. Our operations are subject to all of the operating hazards and risks normally incident to exploring for and developing mineral or metal properties, such as, but not limited to:

·encountering unusual or unexpected formations;

·environmental pollution;

·personal injury, flooding and landslides;

·variations in grades of minerals or metals;

·political and economic related conditions;

·labor disputes; and

·a decline in the price of gold

We currently have no insurance or hedges to guard against any of these risks. If we determine that capitalized costs associated with any of our mineral interests are not likely to be recovered, we would incur a write-down on our investment in such property interests.

Our exploration and development activities are subject to environmental risks, which could expose us to significant liability and delay, suspension or termination of our operations.

The exploration, possible future development and production phases of our business will be subject to federal, state and local environmental regulation. These regulations mandate, among other things, the maintenance of air and water quality standards and land reclamation. They also set out limitations on the generation, transportation, storage and disposal of solid and hazardous waste. Environmental legislation is evolving in a manner which will require stricter standards and enforcement, increased fines and penalties for non-compliance, more stringent environmental assessments, and a heightened degree of responsibility for companies and their officers, directors and employees. Future changes in environmental regulations, if any, may adversely affect our operations. If we fail to comply with any of the applicable environmental laws, regulations or permit requirements, we could face regulatory or judicial sanctions. Penalties imposed by either the courts or administrative bodies could delay or stop our operations or require a considerable capital expenditure. Although we intend to comply with all environmental laws and permitting obligations in conducting our business, there is always a possibility that those opposed to exploration and mining may attempt to interfere with our operations, whether by legal process, regulatory process or otherwise.

We could be subject to environmental lawsuits.

Neighboring landowners, other third parties and governmental entities could file claims based on environmental statutes and common law for personal injury and property damage allegedly caused by the release of hazardous substances or other waste material into the environment on or around our properties.

The Company’s industry is highly competitive and we have less capital and resources than many of our competitors which may give them an advantage in developing and securing mining claims and marketing products similar to ours or make our products obsolete.

We are involved in a highly competitive industry where we may compete with numerous other companies who offer alternative methods or approaches. These competitors may have far greater resources, more experience, and personnel perhaps more qualified than we do.

15

Such resources may give our competitors an advantage in developing and marketing products similar to ours or products that make our products obsolete. There can be no assurance that we will be able to successfully compete against these other entities.

The Company’s failure to continue to attract, train, or retain highly qualified personnel could harm the Company’s business:

The Company’s success also depends on the Company’s ability to attract, train, and retain qualified personnel, specifically those with management and product development skills. In particular, the Company must hire additional skilled personnel to further the Company’s research and development efforts. Competition for such personnel is intense. If the Company does not succeed in attracting new personnel or retaining and motivating the Company’s current personnel, the Company’s business could be harmed.

Risks Related to

Litigation with respect to Mr. Laws may not result in additional funds being obtained to reduce his indebtedness owed to the Company.

The Company has determined by its records that Mr. Laws initially

There were also expenses associated with engaging the special committee to conduct a forensic review of the Company’s books and records in connection with the transactions giving rise to the Missing Funds.

There can be no assurance the Company will successfully implement its plans.

We have historically incurred net losses from operations and we expect losses in the future periods. Our likelihood of success must be considered in light of the problems, expenses, difficulties, complications and delays frequently encountered in connection with the formation of a new business which seeks to obtain funds to finance its operations in a highly competitive environment. There can be no assurance that we will successfully implement any of our plans (including without limitation production of any mine, shipping ore to a smelter or otherwise commercially exploit our properties) in a timely or effective manner or that we will ever be profitable. In addition, there can be no assurances that we will choose to continue to develop any of our current properties because we intend to consider and, as appropriate, to divest ourselves of properties that may no longer be a strategic fit to our business strategy or that we lack the necessary capital to develop. If we lack the capital to implement our plans, we will be forced to curtail or cease operations.

Mineral exploration and development inherently

The exploration for and development of mineral deposits involves significant financial risks, which even a combination of careful evaluation, experience and knowledge may not eliminate. Unprofitable efforts may result from the failure to discover mineral deposits. Even if mineral deposits are found, such deposits may be insufficient in quantity and quality to return a profit from production, or it may take a number of years until production is possible, during which time the economic viability of the project may change. Few properties which are explored are ultimately developed into producing mines. Mining companies rely on consultants and others for exploration, development, construction and operating expertise.

Substantial expenditures are required to establish ore reserves, extract metals from ores and, in the case of new properties, to construct mining and processing facilities. The economic feasibility of any development project is based upon, among other things, estimates of the size and grade of ore reserves, proximity to infrastructures and other resources (such as water and power), metallurgical recoveries, production rates and capital and operating costs of such development projects, and metals prices. Development projects are also subject to the completion of favorable feasibility studies, issuance and maintenance of necessary permits and receipt of adequate financing.

Once a mineral deposit is developed, whether it will be commercially viable depends on a number of factors, including: the particular attributes of the deposit, such as size, grade and proximity to infrastructure; government regulations including taxes, royalties and land tenure; land use, importing and exporting of minerals and environmental protection; and mineral prices. Factors that affect adequacy of infrastructure include: reliability of roads, bridges, power sources and water supply; unusual or infrequent weather phenomena; sabotage; and government or other interference in the maintenance or provision of such infrastructure. All of these factors are highly cyclical. The exact effect of these factors cannot be accurately predicted, but the combination may result in not receiving an adequate return on invested capital.

16

Significant investment risks and operational costs are associated with our exploration activities. These risks and costs may result in lower economic returns and may adversely affect our business.

Mineral exploration, particularly for gold, involves many risks and is frequently unproductive. If mineralization is discovered, it may take a number of years until production is possible, during which time the economic viability of the project may change. Development projects may have no operating history upon which to base estimates of future operating costs and capital requirements. Development project items such as estimates of reserves, metal recoveries and cash operating costs are to a large extent based upon the interpretation of geologic data, obtained from a limited number of drill holes and other sampling techniques, and feasibility studies. Estimates of cash operating costs are then derived based upon anticipated tonnage and grades of ore to be mined and processed, the configuration of the ore body, expected recovery rates of metals from the ore, comparable facility and equipment costs, anticipated climate conditions and other factors. As a result, actual cash operating costs and economic returns of any and all development projects may materially differ from the costs and returns estimated, and accordingly, our financial condition and results of operations may be negatively affected.

Any of our future acquisitions may result in significant risks, which may adversely affect our business.

An important element of our business strategy is the opportunistic acquisition of operating mines, properties and businesses or interests therein within our geographical area of interest. While it is our practice to engage independent mining consultants to assist in evaluating and making acquisitions, any mining properties or interests therein we may acquire may not be developed profitably or, if profitable when acquired, that profitability might not be sustained. In connection with any future acquisitions, we may incur indebtedness or issue equity securities, resulting in increased interest expense, or dilution of the percentage ownership of existing shareholders. We cannot predict the impact of future acquisitions on the price of our business or our common stock. Unprofitable acquisitions, or additional indebtedness or issuances of securities in connection with such acquisitions, may impact the price of our common stock and negatively affect our results of operations.

Our ability to find and acquire new mineral properties is uncertain. Accordingly, our prospects are uncertain for the future growth of our business.

Because mines have limited lives based on proven and probable ore reserves, we may seek to replace and expand our future ore reserves, if any. Identifying promising mining properties is difficult and speculative. Furthermore, we encounter strong competition from other mining companies in connection with the acquisition of properties producing or capable of producing gold. Many of these companies have greater financial resources than we do. Consequently, we may be unable to replace and expand future ore reserves through the acquisition of new mining properties or interests therein on terms we consider acceptable. As a result, our future revenues from the sale of gold or other precious metals, if any, may decline, resulting in lower income and reduced growth.

Delaware law and our by-laws protect our directors from certain types of lawsuits.

Delaware law provides that our directors will not be liable to us or our stockholders for monetary damages except for certain types of conduct as directors. Our by-laws require us to indemnify our directors and officers against all damages incurred in connection with our business to the fullest extent provided or allowed by law. The exculpation provisions may have the effect of preventing stockholders from recovering damages against our directors caused by their negligence, poor judgment, or other circumstances. The indemnification provisions may require us to use our assets to defend our directors and officers against claims, including claims arising out of their negligence, poor judgment, or other circumstances.

The Company is in the preliminary stages of mining operations in the Jim Crow

17

Dismissal of Bankruptcy

After the dismissal of the bankruptcy petition in June 2016 and the sale of the Company’s significant assets, the Company emerged with

·The approximately $20 million of indebtedness outstanding on account of the Company’s senior notes and unsecured claims were reinstated; and

·The courts established a trust in April 2016 for the benefit of certain creditors. A profit interest was attached to the Summit mine with the benefit for certain creditors holding unsecured claims filed by each creditor.

Accordingly, there can be no assurance that the Company’s remaining liabilities

We have a history of operating losses and expect to incur substantial operating losses and negative operating cash flows for the foreseeable future, and we may never achieve or maintain profitability.

We have had no revenues

We may never be able to write-down certain liabilities and this may have a negative impact on our ability to raise capital and on the market price of our common stock, when we resume trading.

At the end of the Company’s fiscal year ending June 30, 2019, the Company wrote off debt and related accrued interest aggregating $12,507,540. The write off of debt was related to two finance facilities governed by and enforceable under British Columbia statutes. The Company retained legal services in British Columbia to research the British Columbia statutes of limitations on the collectability of the finance facilities. Legal counsel reviewed all related documents, records of proceedings and all records and documents deemed relevant to the two finance facilities. The finance facilities were subject to the laws of the Providence of British Columbia and the National laws of Canada and as a result, the Company secured a written legal opinion from Canadian counsel that any liability under the two finance facilities, because of the Limitations Act (British Columbia) and the relevant case law in British Columbia, were no longer enforceable. That is, because the statute of limitations had run for the two liabilities, pursuant to the Limitations Act (British Columbia), no future claims could be commenced in the Province of British Columbia and therefore, the Company had no outstanding legal obligations on the two finance facilities. With this, the Company wrote down $12,507,540 in liabilities and this has been the Company’s position; however, upon review of earlier Registration Statements that were subsequently withdrawn, the SEC Staff expressed its concern with the Company taking this write-down because FASB ASC 405-20-40-1(b) states that “a liability has been extinguished if the debtor is legally released from being the primary obligor under the liability, either judicially or by the creditor.” Since management knew that one of the creditors had been dissolved and was no longer in existence and the other creditor had written-off the amounts that had been owed to it by the Company in one of its annual reports, it knew that it would be difficult if not impossible to get both creditors to release it from liability and that obtaining a court order would be time consuming and expensive at best. The Commission Staff was willing to allow an opinion of counsel, however the opinions we provided did not meet the standard that the Commission requires. The standard that the Commission Staff requires is what is sometimes referred to as a “would” or “will” opinion. In requiring a “will” or “would” opinion, the Commission is looking for greater assurance that the Company “would” or “will” be successful in the event that one of the creditors sought to collect on the liabilities. Although this standard may seem subjective, “will opinions” are regularly used in the context of tax law where a tax opinion is needed. In that context the term “will” means that the drafter of the opinion believes and is effectively stating that there is a 90%-95% probability that a given result “will” come to pass based on the facts present. Absent the availability of one of these three routes to write-off the liabilities, he Commission Staff’s position is that

18

the correct treatment of the aforementioned liabilities is to continue carrying them on the Company’s balance sheets. The Company was not able to procure a judicial order in a timely manner, specific written agreement of the creditors nor an opinion of counsel meeting the “would” or “will” standard, therefore it determined the most expeditious course of action was to restate the consolidated financial statements so that the liabilities that were written-off are now included in the liabilities of the Company once again; in effect, restating the consolidated financial statements as of June 30, 2019 and 2020. Although, in a future period, while the Company plans to either seek a judicial determination or an opinion of counsel that meets the “would” or “will” standard with respect to the liabilities, there can be no assurance that the Company will be successful in meeting the requirements necessary to write-off the aforementioned liabilities or that the Commission will agree that the judicial determination or opinion of counsel satisfies the requirements and spirit of FASB ASC 405-20-40-1(b). To meet the requirements of the Commission, the Company reinstated the debt and restated our financial statements in question in our Registration Statement on Form 10-12G filed on June 14, 2022 and became effective on August 4, 2022. As a result of these restated financial statements and the forward impact on future financial statements, our stock prices as well as our ability to secure necessary financial funding could be harmed as a result.

We have a limited operating history on which to base an evaluation of our business and properties.

Any investment in the Company’s securities should be considered a high-risk investment because investors will be placing funds at risk in an early

Successful expansion of our business will depend on our ability to effectively attract and manage staff, strategic business relationships, and shareholders. Specifically, we will need to hire skilled management and technical personnel as well as manage partnerships and joint ventures to navigate shifts in the general economic environment. Expansion has the potential to place significant strains on financial, management, and operational resources, yet failure to expand will inhibit our profitability goals.

If we cannot secure additional funding, we will be unable to implement our business plan.

Since we do not generate any revenues, we may not have sufficient financial resources ourselves, to undertake all planned development activities relating to our business plan.

Our resources may not be sufficient to manage our expected growth; failure to properly manage our potential growth would be detrimental to our business.

Even if we obtain funding for operations, we may fail to adequately manage our anticipated future growth. Any growth in our operations will place a significant strain on our administrative, financial and operational resources, and increase demands on our management, as well as our operational and administrative systems, controls and other resources. There can be no assurances that our existing personnel, systems, procedures or controls will be adequate to support our operations in the future; or that we will be able to successfully implement appropriate measures consistent with our growth strategy. As part of this growth, we may have to implement new operational and financial systems, procedures and controls to expand, train and manage our employee base, and maintain close coordination among our staff. There can be no guarantee that we will be able to do so, or that if we are able to do so, we will be able to effectively integrate them into our existing staff and systems.

19

If we are unable to manage growth effectively, our business, operating results and financial condition could be materially adversely affected. As with all expanding businesses, the potential exists that growth will occur rapidly. If we are unable to effectively manage this growth, our business and operating results could suffer. Anticipated growth in future operations may place a significant strain on management systems and resources. In addition, the integration of new personnel will continue to result in some disruption to ongoing operations. The ability to effectively manage growth in a rapidly evolving market requires effective planning and management processes. We will need to continue to improve operational, financial and managerial controls, reporting systems and procedures, and will need to continue to expand, train and manage our work force.

The loss of key personnel could adversely impact the Company.

The nature of our business, including our ability to continue our current activities depends, in large part, on the efforts of our key personnel, the loss of any of which could have a material adverse effect on our business.

We may be unable to continue as a going concern.

As a result of our financial condition, our auditors have expressed doubt as to our ability to continue as a going concern which may have an adverse impact on our relationship with third parties with whom we do business, and could make it challenging and difficult for us to raise additional debt or equity financing, all of which could have a material adverse impact on our business, results of operations, financial condition and future prospects. The consolidated financial statements have been prepared on a going concern basis, which contemplates the realization of assets and satisfaction of liabilities and commitments in the normal course of business. Should the Company be unable to continue as a going concern, it may be unable to realize the carrying value of its assets and to meet its liabilities as they become due.

A substantial or extended decline in gold and silver prices would have a material adverse effect on the value of our assets, on our ability to raise capital and could result in lower than estimated economic returns.

The value of our assets, our ability to raise capital and any future economic returns are substantially dependent on the prices of gold and silver. Gold and silver prices fluctuate

·gold sales or leasing by governments and central banks or changes in their monetary policy, including gold inventory management and reallocation of reserves;

·speculative short positions taken by significant investors or traders in gold;

·the relative strength of the U.S. dollar;

·expectations of the future rate of inflation;

·interest rates;

·changes to economic activity in the United States, China, India and other industrialized or developing countries;

·geopolitical conflicts;

·changes in industrial, jewelry or investment demand;

·changes in supply from production, disinvestment and scrap; and

·

Risks Related to our Common Stock

The Company’s Common Stock was Deregistered and Trading was Halted.

In July of 2020, the Company received notice from the SEC that it was seeking to deregister the Company’s common stock pursuant to Section 12(j), based on the Company’s failure to file periodic reports with the Commission and otherwise provide current information to the market. This failure was based in large part from the need to restate its financial statements and the need to find and engage a PCAOB auditor who was willing to conduct and provide the required audits amid the SEC and DOJ’s investigations. Although we were able to secure a qualified auditor, we were not able to make our filings quickly enough and by the time they were completed, the Commission had already sent a notice under Section 12(k). The Commission takes a hardline position in these situations such that once they have instituted deregistration proceedings, the only options available to the Company were to litigate or settle and consent to the deregistration of the Company’s common stock. Historically, registrants have not been successful in litigating with the Commission over Section 12(j) matters and therefore the Company determined that the best course of action was to consent to deregistration of its common stock and then file a new registration statement on Form 10-12G. The Company has signed a settlement agreement with the SEC with respect to the registration of its common stock in response to the Commission’s institution of deregistration proceedings under Section 12(j), and has re-registered the same under Section 12(g) by way of filing our Form 10-12G and the filing has been ordered effective by the SEC on August 4, 2022. Currently the Company is preparing the application to the Over-the-Counter Markets Group (“the OTC”) to trade on their QB tier. Upon the OTC completing their due diligence on the application their and approval of the

20

application, it will submit a Form 211 to the Financial Industry Regulatory Authority (“FINRA”) for their final review and acceptance of the OTC due diligence process. The Company filed a complete and current Form 10-12G and it meets the informational requirements of the SEC Rule 15c2-11. Upon the FINRA approval, they will issue our trading symbol and the Company will begin trading. Any delay or failure in securing FINRA’s final approval and issuance of our trading symbol would result in our shareholders not having a public market to sell their shares. Further, it would make it more difficult for the Company to obtain the financing it requires.

Our common stock is not currently traded, and there is no guarantee that our stock will be tradable or that if it is as to the prices at which the shares may trade.

Trading of our common stock

Currently the Company is preparing the application to the OTC to trade on their QB tier. Upon the OTC completing their due diligence on the application and their approval of the application, it will submit a Form 211 to the Financial Industry Regulatory Authority (“FINRA”) for their final review and acceptance of the OTC due diligence process. The Company filed a complete and current Form 10-12G and it meets the informational requirements of the SEC Rule 15c-211. Upon the FINRA approval, they will issue our trading symbol and the Company will begin trading. Any delay or failure in securing FINRA’s final approval and issuance of our trading symbol would result in our shareholders not having a public market to sell their shares. This in turn would negatively affect the Company’s ability to secure the funding required for it to execute on its business plan, which would negatively affect its operations and could result in a complete loss to investors.

Although our Form 10-12G became effective, with all comments cleared, we still face challenges in receiving FINRA approval and even if we are successful and resume trading, trading may still be limited or suffer because we are not listed on an established securities exchange.

Although management is optimistic that we will receive approval to resume trading and views any delays as a short-term issue as of the date of

Because our common stock is currently a “penny stock,” it may be difficult to sell shares at times and prices that are acceptable.

Assuming we are successful in having our stock resume trading on OTC Markets, our common stock will likely be considered a “penny stock.” Broker-dealers who sell penny stocks must provide purchasers of these stocks with a standardized risk disclosure document prepared by the SEC. This document provides information about penny stocks and the nature and level of risks involved in investing in the penny stock market. A broker must also give a purchaser, orally or in writing, bid and offer quotations and information regarding broker and salesperson compensation, make a written determination that the penny stock is a suitable investment for the purchaser, and obtain the purchaser’s written agreement to the purchase. Assuming a market maker are allowed to provide bid and offer quotations because we have been successful in securing through our OTC application process and we are able to satisfy FINRA’s requirements, we will continue to be considered a “penny stock.” The penny stock rules may make it difficult for you to sell your shares of our common stock. Because of these rules, many brokers choose not to participate in penny stock transactions and there is less trading in penny stocks overall as a result. Accordingly, you may not always be able to resell shares of our common stock in ordinary transactions at times and prices that you feel are appropriate.

21

Any sales of a significant amount of common stock by existing shareholders may depress the price otherwise causing the price of our common stock may decline.

A small number of existing shareholders own a significant portion of our common stock, which could limit your ability to influence the outcome of any shareholder vote.

A relatively small number of shareholders hold large concentrations of shares and under our certificate of incorporation and Delaware law, the vote of a majority of the shares outstanding is generally required to approve most shareholder actions. As a result, these individuals and entities will be able to influence the outcome of shareholder votes for the foreseeable future, including votes concerning the election of directors, amendments to our certificate of incorporation or proposed mergers or other significant corporate transactions.

The market price of our common stock

The Company will not pay dividends on its common stock.

We have never paid any cash dividends on any shares of our capital stock, and we do not anticipate that we will pay any dividends in the foreseeable future. Our current business plan is to retain any future earnings to finance the expansion of our business. Any future determination to pay cash dividends will be at the discretion of our Board of Directors, and will be dependent upon our financial condition, results of operations, capital requirements and other factors as our board of directors may deem relevant at that time. If we do not pay cash dividends, our stock may be less valuable because a return on your investment will only occur if our stock price appreciates. This may never happen and investors may lose all of their investment in our company.

We have offered and sold and will continue to offer and sell shares without registration under the Securities Act, through exemptions available under the Securities Act. All such shares are "restricted securities" as defined by Rule 144 ("Rule 144") when issued under available exemptions from registration under the Securities Act, and cannot be resold without registration except in reliance on Rule 144 or another applicable exemption from registration. In general, under Rule 144, our non-affiliates (who have not been affiliates within the past 90 days) can sell restricted shares held for at least six months, subject only to the requirement that we make current information available publicly as required by Rule 144.

No prediction can be made as to the effect, if any, that future sales of restricted shares of common stock, or the availability of such common stock for sale,

Risk Factors Related to the COVID-

An

22

Because we may issue additional shares of our common stock, investment in our company could be subject to substantial dilution.

Investors’ interests in our Company will be diluted and investors may suffer dilution in their net book value per share when we issue additional shares. We are authorized to issue 550,000,000 shares of common stock, $0.002 par value per share. As of June 30, 2022 and 2021 there were 441,308,551 and 433,018,551, shares of our common stock issued and outstanding, respectively. We anticipate that all or at least some of our future funding, if any, will be in the form of equity financing from the sale of our common stock. If we do sell more common stock, investors’ investment in our company will likely be diluted. Dilution is the difference between what investors pay for their stock and the net tangible book value per share immediately after the additional shares are sold by us. If dilution occurs, any investment in our Company’s common stock could seriously decline in value.

Our prior trading in our common stock on the OTC Pink Exchange has been subject to wide fluctuations.

Our common stock was quoted for public trading on OTC Markets prior to Commission order suspending trading that went into effect on December 17, 2020. Historically, the trading price of our common stock has been subject to wide fluctuations. Assuming trading resumes, of which there can be no assurance, the trading prices of our common stock may fluctuate in response to a number of factors, many of which will be beyond our control. The stock market has generally experienced extreme price and volume fluctuations that have often been unrelated or disproportionate to the operating performance of companies with limited business operations. There can be no assurance that trading prices and price earnings ratios previously experienced by our common stock will be matched or maintained. These broad market and industry factors may adversely affect the market price of our common stock, regardless of our operating performance. In the past, following periods of volatility in the market price of a company’s securities, securities class-action litigation has often been instituted. Such litigation, if instituted, could result in substantial costs for us and a diversion of management’s attention and resources.

Delaware law our Certificate of Incorporation and our by-laws provide for the indemnification of our officers and directors at our expense, and correspondingly limits their liability, which may result in a major cost to us and hurt the interests of our shareholders because corporate resources may be expended for the benefit of officers and/or directors.

Our Certificate of Incorporation and By-Laws include provisions that eliminate the personal liability of our directors for monetary damages to the fullest extent possible under the laws of the State of Delaware or other applicable law. These provisions eliminate the liability of our directors and our shareholders for monetary damages arising out of any violation of a director of his fiduciary duty of due care. Under Delaware law, however, such provisions do not eliminate the personal liability of a director for (i) breach of the director's duty of loyalty, (ii) acts or omissions not in good faith or involving intentional misconduct or knowing violation of law, (iii) payment of dividends or repurchases of stock other than from lawfully available funds, or (iv) any transaction from which the director derived an improper benefit. These provisions do not affect a director's liabilities under the federal securities laws or the recovery of damages by third parties.

FINRA sales practice requirements may also limit a stockholder’s ability to buy and sell our stock.

In addition to the “penny stock” rules described above, the Financial Industry Regulatory Authority (known as “FINRA”) has adopted rules that require that in recommending an investment to a customer, a broker-dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative low-priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer’s financial status, tax status, investment objectives and other information. Under interpretations of these rules, FINRA believes that there is a high probability that speculative low-priced securities will not be suitable for at least some customers. FINRA requirements make it more difficult for broker-dealers to recommend that their customers buy our common shares, which may limit your ability to buy and sell our stock and have an adverse effect on the market for our shares.

Trading was suspended on our common stock following the deregistration of our common stock in accordance with our settlement with the SEC.

Trading in our common stock was suspended after the SEC commenced Administrative Proceedings under 12k of the Exchange Act. The Commission then commenced proceedings under 12j of the Exchange Act to deregister our common stock because we had not posted current information by filing the required Periodic Reports on Forms 10-K and 10-Q. We had not made these filings because of the need to restate our financial statements following the misappropriation of funds by our former CEO, Thomas Laws. However, notwithstanding these mitigating circumstances, the failure to file the required reports is a matter of strict liability and has resulted in the deregistration of our common stock, which became effective on December 17, 2020 following execution of our settlement agreement with the Commission. We may not be able unable to satisfy FINRA’s requirements in a timely manner or at all, market makers will not post bids or offers for our common stock.

On September 28, 2021, the SEC compliance date of their amended Rule 15c2-11and the amended FINRA rule 6432 went into effect. The amended Rule 15c2-11 allows a qualified IDOS (i.e., the OTC Markets) to comply with the information review requirements, to

23

publish an affirmative determination that it has conducted such review, and for the broker-dealer to rely on the OTC markets determination without conducting an independent review. As long as the OTC Markets makes it known to the public that it has completed a review, a broker-dealer can quote or resume quoting the securities and be in compliance with Rule 15c2-11. The amended Rule 6432 requires that (i) a qualified inter-dealer quotation system (Qualified IDOS) (i.e. OTC Markets) submit a modified Form 211 filing to FINRA in connection with each initial information review that it conducts; (ii) a Qualified IDOS ( OTC Markets) that makes a certain publicly available determination under Rule 15c2-11 submit a daily security file to FINRA containing applicable summary information for all securities quoted on its system, and (iii) other changes to the FINRA Rule 6432 and the form 211 to further clarify the operation of the rule and conform it to the amended Rule 15c2-11.

The Company has registered its common stock with the SEC on Form 10-12G and the filing has been declared effective by the SEC on August 4, 2022, resulting in the Company becoming an Exchange Act reporting company at that time. The information contained in its Form 10-12G filing was complete and current information, and as a result, the effective filing contains the current information that meets the requirements of Rule 15c2-11.

We hold

Unpatented Mining Claims:

maintained in accordance with the U.S. General Mining Law of 1872, or the “General Mining Law.” Unpatented mining claims are unique U.S. property interests and are generally considered to be subject to greater title risk than other real property interests because the validity of unpatented mining claims is often uncertain. The validity of an unpatented mining claim, in terms of both its location and its maintenance, is dependent on strict compliance with a complex body of federal and state statutory and decisional law that supplement the General Mining Law. Also, unpatented mining claims and related rights, including rights to use the surface, are subject to possible challenges by third parties or contests by the federal government. In addition, there are few public records that definitively control the issues of validity and ownership of unpatented mining claims. We have not filed a patent application for any of our unpatented mining claims that are located on federal public lands in the United States and, under possible future legislation to change the General Mining Law, patents may be difficult to obtain.

Our exploration, development and mining rights relate to patented and unpatented mining claims covering federal and State lands in the State of New Mexico. Location of mining claims under the General Mining Law, is a self-initiation system under which a person physically stakes an unpatented mining claim on public land that is open to location, posts a location notice and monuments the

24

boundaries of the claim in compliance with federal laws and regulations and with state location laws, and files notice of that location in the county records and with the Bureau of Land Management (“BLM”). Mining claims can be located on land as to which the surface was patented into private ownership under the Stock

The holder of a valid unpatented mining claim has possessory title to the land covered thereby, which gives the claimant exclusive possession of the surface for mining purposes and the right to mine and remove minerals from the claim. Legal title to land encompassed by an unpatented mining claim remains in the United States, and the government can contest the validity of a mining claim. The General Mining Law requires the performance of annual assessment work for each claim, and subsequent to enactment of the Federal Land Policy and Management Act of 1976, 43 U.S.C. §1201 et seq., mining claims are invalidated if evidence of assessment work is not timely filed with the BLM. However, in 1993 Congress enacted a provision requiring payment of a small claim maintenance fee in lieu of performing assessment work, subject to an exception for small miners having less than 10 claims. No royalty is paid to the United States with respect to minerals mined and sold from a mining claim. The General Mining Law provides a procedure for a qualified claimant to obtain a mineral patent (i.e., fee simple title to the mining claim) under certain conditions. It has become much more difficult in recent years to obtain a patent. Beginning in 1994, Congress imposed a funding moratorium on the processing of mineral patent applications which had not reached a designated stage in the patent process at the time the moratorium went into effect. Additionally, Congress has considered several bills in recent years to repeal the General Mining Law or to amend it to provide for the payment of royalties to the United States and to eliminate or substantially limit the patent provisions of the law. Any such changes to the law and increases to our costs would have a negative impact on our results of operations.

Mining claims are conveyed by deed or leased by the claimant to the party seeking to develop the property. Such a deed or lease (or memorandum of it needs to be recorded in the real property records of the county where the property is located, and evidence of such transfer needs to be filed with

[The Remainder of this Page is Intentionally Left Blank]

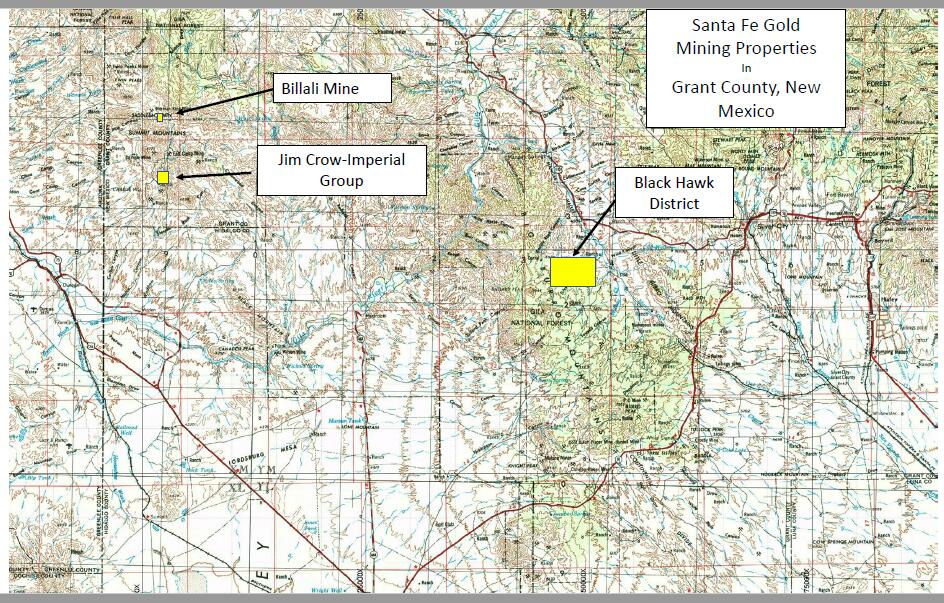

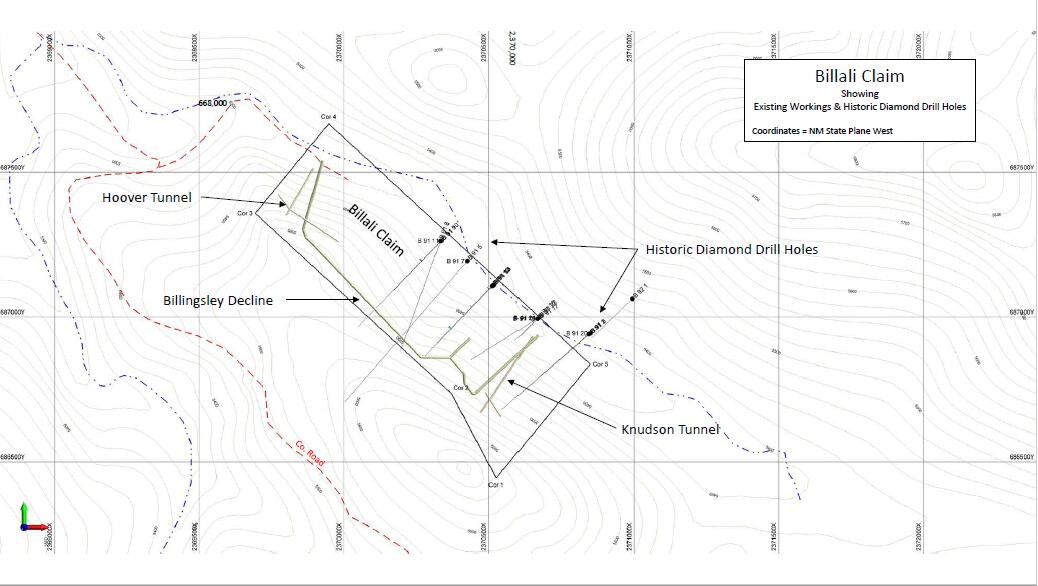

Steeple Rock District, Grant County New Mexico –

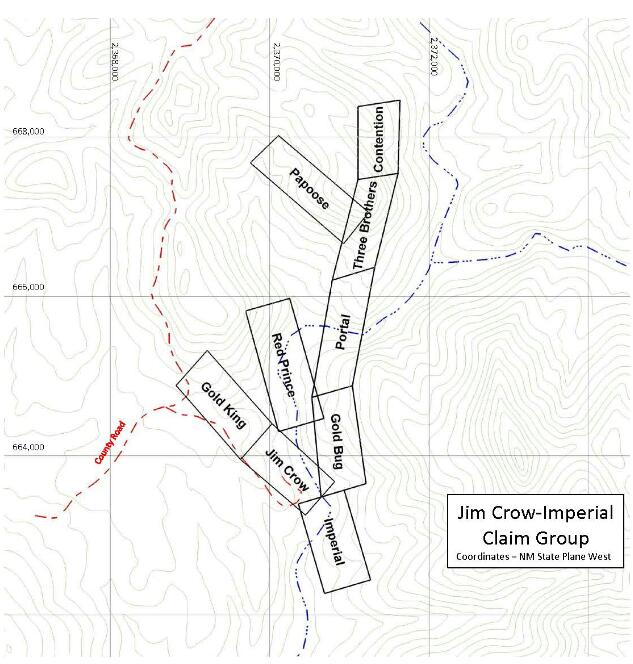

Properties - The Jim Crow, Imperial and Billali Mines

Santa Fe’s properties consist of the Jim Crow group of patented and unpatented claims in the southern part of the district and the Billali patented claim in the northern part of the district. The Jim Crow group is made up of

Patented Lode Claims

| Name | MS No. |

1 | Imperial Lode | MS 1012 A |

2 | Jim Crow Lode | MS 1012 B |

3 | Gold King Lode | MS 1012 C |

4 | Portal Lode | MS 1012 D |

5 | Gold Bug Lode | MS 1012 E |

6 | Red Prince Lode | MS 1012 F |

7 | Three Brothers Lode | MS 1012 G |

8 | Contention Lode | MS 1012 H |

The Jim Crow group also consists of two unpatented mining claims and Mineral Acquisitions, LLC controls nine unpatented mining claims.

Unpatented Lode Claims

26

| All the combined mining claims for this project encompass approximately 343 acres.

| |||||||||||||||||||||||||||||||||||||

Location and Access

The Steeple Rock mining district is in the western part of Grant County, New Mexico. The district lies approximately 45 miles east of the town of Safford, Arizona and approximately 10 miles northeast of Duncan, Arizona. The district is reached by well-maintained county roads from Duncan.

District, Historical and Prior Operations